Below is our original “Wait-To-Buy” recommendation on Biocept (BIOC) from last August, and our March 30 “Buy” recommendation.

Our investment newsletter has been published for over 35 years, providing key buy-sell advice on technology, biotechnology, and some precious metals stocks. It was rated #1 or #2 for performance for various one-, five-, and ten-year periods by the independent industry watchdog, the Hulbert Financial Digest.

For the extremely difficult five years, 2008-2012, New World Investor was Hulbert’s #1 performing letter. In 2016, our average recommendation was up 30.5%.

We don’t hire professional copywriters to churn out solicitations like “This Stock Could Be Bigger Than Buffett’s Berkshire Hathaway” or “Buy This the $7 iPhone Killer.” They over-promise and under-deliver. We don’t want dumb subscribers. We also don’t suck you in with a $99 letter and then spam your inbox to upsell a $1,500 or letter or a $3,000 service to tell you what our model portfolio is. We aren’t a chart trading service, either.

We simply provide the premier, money-making technology stock letter in layman’s language to cut-to-the-bottom-line investors. Our intelligent, experienced Mastermind community comments on every issue, and Michael is right in there with you.

Editor Michael Murphy is a Harvard graduate with honors in economics and a Chartered Financial Analyst. He worked for American Express Investment Management and Capital Research/American Funds. He’s written three books, including the Random House business best-seller Every Investor;s Guide to High-Tech Stocks and Mutual Funds.

Michael has managed venture capital, mutual funds, pension funds, separate accounts and all-short funds. Starting in 1968, he grew up with Silicon Valley – he was the CEO of two software companies.

Original August 11, 2016 “Wait-To-Buy” Recommendation

Get Ready To Buy Biocept

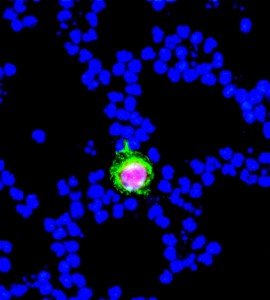

The scary thing about cancer is that it metastasizes – it spreads. A tumor in the breast suddenly is joined by a tumor in the brain. How did that happen? There have been different theories over the years, and we now know that cancer cells – especially the most aggressive ones – get into the bloodstream. When they get into a tight place, a capillary, they stop. And then your immune system kills them – well, most of them. But the ones that don’t get killed form new tumors that consume energy resources until your bodily processes are spending all their effort supporting and growing the tumors. And if surgery, radiation, chemotherapy or your immune system can’t kill them, you die.

The larger a tumor is, the more cells it contains, and the more likely there will be enough cells circulating in the blood to find some. Blood may only have 100 to 1,000 cancer cells per liter, which makes it difficult to find them. But technology has advanced enough that we can find them. Here is a single prostate cancer cell circulating in blood:

I am very interested in the liquid biopsy technology. The acquisition of Sequenom by Labcorp took away our exposure to this revolutionary technology. I’ve looked at other stocks in this area, like Trovagene (TROV), and I think I’ve found the winner.

Biocept (BIOC) is a small cancer diagnostics company in San Diego developing circulating tumor cell and circulating tumor DNA assays utilizing a standard blood sample. These assays provide data for oncologists to design personalized treatment for their patients based on details of the characteristics of tumors. It offers assays for solid tumor indications, including breast cancer, lung cancer, gastric cancer, colorectal cancer, prostate cancer, and melanoma.

The chart is terrible:

Click for larger graphic

Click for larger graphic

At today’s closing price of 63 cents a share, the company has a total market value of only $15.6 million. It is tiny. Like Arch Therapeutics (ARTH), this is a stock you do not need to buy a lot of, because I think it can return 20-to-1 or better over the next few years. Biocept is the best in the industry. They were the first to proved the superiority of liquid biopsy over directed needle tumor biopsy, because the most aggressive cells appear more in circulation than in the tumor, where needles can miss them. Insiders are buying the stock, revenues are growing, and millions of insured lives are covered by their methods.

But now is not the time to buy. They are out of money, and big dilution lies just ahead. At the end of June, they had $3.8 million in cash. They burn about that much each quarter, so as of today they probably have about six weeks of cash left.

On April 29 they sold five million shares at $1 a share, and gave five-year warrants to buy 3.5 million additional shares at $1.30. The company netted $4.4 million.

If they only raise the same amount of money in the next few weeks, they will have to sell about nine million shares (plus warrants), which is pretty substantial dilution of the current 25 million shares outstanding. And that will only carry them one more quarter. We have to wait to see what the offering looks like. Hopefully, Labcorp won’t buy them.

The March 30, 2017 “Buy” Recommendation

This is my second attempt to buy Biocept (BIOC). The first attempt was in the August 11, 2016 Radar Report when the stock was at 63¢, before a 1-for-3 reverse split ($1.89 split-adjusted). Biocept is a small cancer diagnostics company in San Diego developing circulating tumor cell and circulating tumor DNA assays utilizing a standard blood sample. Diagnosing cancer with a blood test is called a “liquid biopsy.” Because the most malignant cells are the most likely to break away from a tumor and get into the blood stream, it can be more valuable than a regular biopsy. It’s a difficult technology, and I think Biocept is the best in the world at it.

These assays provide data for oncologists to design personalized treatment for their patients based on details of the characteristics of tumors. Biocept offers assays for solid tumor indications, including breast cancer, lung cancer, gastric cancer, colorectal cancer, prostate cancer, and melanoma. It can keep adding assays and eventually move into leukemias, or cancers of the blood.

In addition to the impending reverse split, Biocept was out of money last August and I thought had to do an offering. So I said to wait. They did the reverse split on September 29 and the stock dropped from a split-adjusted $1.89 to 78¢ at the end of the year. I was waiting for the offering. They managed to squeak through the December quarter on cash coming in from warrant exercises. Then, on January 10, they announced they had signed a provider agreement with Blue Cross Blue Shield of Texas. The stock shot up to $2.71 on very heavy volume. It then backed off to the $1.50 area until February 9, when the CEO posted a very positive letter to shareholders announcing another agreement with with a large, national health plan association. He also said the company will transition to accrual accounting in 2017, which will let them report much smaller losses or earlier breakeven.

The stock jumped again, to $2.37. I was still waiting for the inevitable capital raise. They reported 2016 results on March 9. On Monday, March 14, the stock closed at $2.16. On Tuesday they announced the capital raise on these remarkable terms:

* * 4,320,000 shares of stock at $2.15 a share – essentially no discount!

* * warrants for another 2,160,000 shares at an exercise price of $2.50 – a fat premium!

The company will net $8.4 million, which should give them a cash runway into the first quarter of 2018. Roth Capital led the deal. with WestPark Capital and Chardan Capital as co-placement agents. But I’ve never seen Roth do another deal this good. I think someone at Biocept, probably the very experienced Chief Financial Officer, really knows what they are doing. They kept the company alive on fumes, did the reverse split, made the positive contract announcements, posted the CEO’s letter, got the stock up – and then did a great financing. We want these people on our side!

They gave an excellent presentation at the Oppenheimer Healthcare Conference (AUDIO AND SLIDES HERE).

As you can see from the lower left, today they process all samples in their lab in San Diego. This year they will develop a kit that can be sold in 2018 to allow hospitals and other labs to run the diagnosis. The liquid biopsy costs about $1,200, compared to $5,000 to $15,000 for a tissue biopsy. Some parts of the body are difficult to biopsy, like the lungs, or near-impossible, like the brain. A biopsy can cause complications that cost thousands of dollars to fix. And often the doctor can’t repeat the tissue biopsy, as in a monitoring situation, where it’s easy to take another blood sample.

Click for larger graphic

Click for larger graphic

JPMorgan thinks the worldwide market for liquid biopsy will be $22 billion by 2020. Biocept could be the largest provider by then, and I think will at least be in the top three. That makes today’s total market capitalization of under $55 million, after accounting for warrants and options, ridiculously cheap. The stock could dip a bit more over the next couple of weeks if there is a general market decline, but I want you to Buy BIOC under $2.25.

I have been trying to use very low target prices in response to subscriber complaints about my “wild-eyed” targets in the past. But these are “buy right and sit tight” stocks that can go up hundreds of percent if they work, or drop to zero if they don’t. I’m not sure what to do about the target prices on stocks like this, or Arch Therapeutics (ARTH) or ScyNexis (SCYX). I don’t know why someone would not want to know my real targets.

So here’s the deal. I think BIOC will go over $5 in the next 12 months. That’s one target. But I also think it is a $40 stock someday – a mere $1.2 billion total market value for one of the top companies in a $22 billion market. That’s the “buy right and sit tight” target.

Click for larger graphic

Click for larger graphic

—————————————————————-

We are updating the New World Investor website, and when we are done the subscription rates will be $495 a year or $57 a month. As an Inside reader, you can subscribe today at the current, deeply discounted rate of only $245 a year or $25 a month. This rate will expire shortly.

Thank you for becoming a New World Investor subscriber!

Gold ($245 annually)

Monthly ($25 monthly)

Troubles with PayPal?

You can subscribe for one year only for $245 by sending a check made out to the publisher, GwynRose LLC, to:

GwynRose LLC

10643 Empire Grade

Santa Cruz, CA 95060