Dear New World Investor:

Click for larger graphic – h/t Keith Fitz-Gerald

Click for larger graphic – h/t Keith Fitz-Gerald

TL:DR

* * Excess debt suppresses economic growth

* * So demand can’t rise enough to generate inflation

* * Or push up interest rates

* * The very thing you would expect to cause increased inflation – more debt – actually causes lower inflation because the marginal revenue produced by debt falls and pulls the velocity of money down.

* * As long as excess debt is pushing velocity lower, aggregate demand will keep falling and sustained, broad inflation is impossible.

* * The Fed believes this is not real inflation we are seeing, we are seeing distortions and disturbances in the data that are being skewed by the lingering effects of the pandemic. I think they are right.

* * Think how much cost the digitization of the economy, electric vehicles, and even cryptocurrency will take out of day-to-day life. Lower costs are deflation.

* * The Fed said they will wait until they know that all pandemic-related job losses have been recovered before raising interest rates again. They will not act based just on employment forecasts or inflation metrics.

* * You can like what the Fed is doing or not, the budget deficit or not, paying people not to work, or not, but those are the realities we need to align with to invest successfully. For us investors, it doesn’t matter if Powell turns out to be right or wrong – it’s all probabilities anyway – but what matters is that is what the Fed is thinking.

A few months ago the bears were saying the stock markets would fall, excessive debt would cause a huge crash, and the recovery would stall. But here we are setting new highs. I continue to think:

* * 4200 was and is a reasonable S&P 500 target for 2021. We could see something closer to 4400 by the end of the year as investors discount 2022.

* * The market is likely to churn at a high level through the summer.

* * A 10%+ correction could happen any time. It would be a buying opportunity.

* * Sectors that lagged in the first half – biotech! – will outperform in the second half.

** The drops in tech and biotech stocks in February-March and April-May will be unnoticeable on the charts a few years from now after the world has completely recovered from the pandemic.

The core Personal Consumption Expenditures inflation (top chart), the Fed’s preferred measure, increased by the most in nearly 20 years in April. But the price index (bottom chart) is only slightly above the pre-COVID trend.

Click for larger graphic

Click for larger graphic

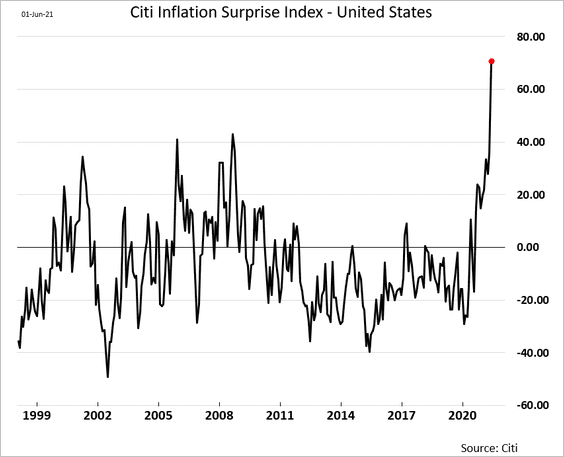

Economists have been surprised by the intensity of the recent price gains. The Citi Inflation Surprise Index hit a record high.

Click for larger graphic

Click for larger graphic

The Fed already said they would start unwinding their $13.8 billion corporate bond portfolio. At the end of April, they held $8.6 billion in corporate bond exchange-traded funds and $5.2 billion in individual corporate bonds. They expect to sell them all by the end of this year, and said: “Portfolio sales will be gradual and orderly, and will aim to minimize the potential for any adverse impact on market functioning by taking into account daily liquidity and trading conditions for exchange-traded funds and corporate bonds.”

But the Fed also has said they want to see a few monthly payroll gains near one million jobs before they taper. That means no tapering until the end of this year or in 2022.

The bears are hoping high inflation will force the Fed to admit it isn’t transitory and raise interest rates, causing a stock market crash. Indeed, I wrote a book about this in 2010, Survive The Great Inflation. But don’t buy it or read it because I was wrong. Here’s why.

Dr. Lacy Hunt of Hoisington Management has been consistently right about inflation (little), interest rates (flat to down), and Treasury bonds (bullish) for years. He contends that:

* * excess debt suppresses economic growth

* * so demand can’t rise enough to generate inflation

* * or push up interest rates.

He points out that we have had five major debt bubbles in the last two centuries, each of which led to deflation (before 1930) or disinflation (since then).

Click for larger graphic Source: Hoisington Management

Click for larger graphic Source: Hoisington Management

He also points out that core Personal Consumption Expenditures inflation is a lagging indicator that doesn’t show up until we are a few years into the recovery from a recession. Even when the lags are shorter, like 2001 and 2009, the inflation rate was still near its low two to four years later.

Click for larger graphic Source: Hoisington Management

Click for larger graphic Source: Hoisington Management

The reason for this is simple: If we start to recover and inflation takes off, it curtails the recovery. But what about the money printer going brrr…brrr…brrr for so long? Dr. Hunt points out that the speed at which money turns over – the velocity of money – is hitting an all-time low because we’re taking on too much debt. The very thing you would expect to cause increased inflation – more debt – actually causes lower inflation because the marginal revenue produced by debt falls and pulls the velocity of money down. This is the key point I missed when I wrote Survive The Great Inflation.

Dr. Hunt believes another major problem is that debt reduces savings. The red line in the chart below shows the government surplus or deficit. The gray area is private savings. The green line is the total or net of the two.

Click for larger graphic Source: Hoisington Management

Click for larger graphic Source: Hoisington Management

One of the first things we learn in Econ 101 is that net national savings equals net national investment. Without savings you can’t invest, and without investment the standard of living can’t rise. It’s true that thanks to technology it takes much less investment to produce the same increase in the standard of living, but there still has to be savings.

As you can see, the government ran a 14% deficit in 2020, bigger than in World War II. President Biden’s plan is to run similar deficits this year and next. Although private savings should be higher than in 2020, it just won’t be enough to get the green line much above zero. Dr. Hunt believes that if we don’t have the resources to fund investment to obtain a higher standard of living, the economy will falter and inflation will move lower. As long as excess debt is pushing velocity lower, aggregate demand will keep falling and sustained, broad inflation is impossible.

The Fed believes this is not real inflation we are seeing, we are seeing distortions and disturbances in the data that are being skewed by the lingering effects of the pandemic. I think they are right.

At their June meeting, the Federal Reserve announced no change to the Fed funds target rate, which remains at 0.0% – 0.25%. In March they said they didn’t expect to increase rates until 2024, but at the June meeting some of them indicated that rate hikes might come as early as 2023. Also, they raised their inflation expectation a full percentage point to 3.4%. Yet they didn’t even hint at cutting back on their $120 billion worth of bond purchases every month and Chairman Powell said that they would provide “advance notice” before announcing any decision to taper the bond-buying program.

In the June press conference, Powell said that the dot-plot projections should be taken with a “big grain of salt” and that Fed fund increases are “well into the future.”

I know it’s hard to believe inflation is transient when producer prices just surged at a 6.6% annual rate – the most on record – and very smart people like billionaire hedge fund manager Paul Tudor Jones says he is “all in” on the inflation trade. Think how much cost the digitization of the economy, electric vehicles, and even cryptocurrency will take out of day-to-day life. Lower costs are deflation.

At his recent Congressional testimony, Powell said factors that have weighed on the labor market and other factors that have contributed to increased levels of inflation should both be transitory, and he expects strong jobs creation this fall. During the question and answer session, he said maximum employment is a key focus of the policy committee. They are looking at a “broader set of data” (whatever that means) to understand the “true” employment picture. They will wait until they know that allpandemic-related job losses have been recovered before raising interest rates again. They will not act based on employment forecasts or inflation metrics.

The Fed believes most of the inflation overshoot is directly related to categories driven by the economic reopening. Powell said items like car and semiconductor inventories should replenish, and as that happens, price rises will fade.

After the 2009 recession and Quantitative Easing, the Fed tapered its bond-buying in December 2013. The first rate increase came in 2015. I expect a similar time frame going forward. The Fed should see payrolls expanding at their target one million a month in the fall. They could start tapering the bond-buying at the end of this year or in 2022 and raise interest rates in 2023.

Until then, monetary policy is going to remain easy and fiscal stimulus from President Biden’s deficits is off the charts. That will drive economic activity and a steady stock market rally in the S&P 500 and Nasdaq Composite indexes.

You can like what the Fed is doing or not, the budget deficit or not, paying people not to work, or not, but those are the realities we need to align with to invest successfully. For us investors, it doesn’t matter if Powell turns out to be right or wrong – it’s all probabilities anyway – but what matters is that is what the Fed is thinking.

They want to see a few consecutive months with payroll gains around one million before they start tightening. Even then, “tightening” only means tapering bond purchases for over a year. As long as the government runs a huge deficit, it has to will be financed by selling Treasury bonds, and the Fed is the buyer of last resort. Oddly, markets initially reacted as if the Fed had hiked rates already, instead of leaving over $2 trillion in Quantitative Easing still on deck after the Fed meeting.

In the June 10 Radar Report I pointed to the Biden Administration’s policies to sharply raise the price of oil, the ESG fad that led an anti-oil activist hedge fund to win three seats on Exxon Mobile’s Board of Directors, and a European court decision to essentially force Royal Dutch Shell out of the oil exploration business, as reasons to expect oil to go to $200-$300 a barrel over the coming years. I forgot to mention another important factor: Banks, especially those that are public, are under pressure to cut or eliminate lending for fossil fuel development.

I concluded: “As always, third-world countries, poor people, and people of color will be hurt the worst. I’m going to start looking for investments in this area – $300 oil is a MegaShift, for sure. But maybe only private companies will benefit.” Indeed, owners of private oil companies that are self-funding are going to get very, very rich, not to mention Middle East sheiks. Russia will go from “a gas station masquerading as a country” to a major global power. You probably don’t like it – I don’t like it – but we can make a bundle, too, by investing in…

Read the June 10 Radar Report for the background on this investment, and the June 17 issue for a cheap, easy way to buy it. We’re expecting a 180% to 325% return on this one with little risk. JUST CLICK HERE to subscribe.

Each issue now includes my 5 best short-term buys and 5 best long-term buys. The June 24 issue has a thorough review of a fast-growing company crucial to the digital economy, what to do with gold and bitcoin right now, and much more. Don’t miss the absolute leader in high-precision 3D printing, the easiest cannabis double (or much more!) around, backing a famous billionaire on the prowl for his next acquisition – SUBSCRIBE TODAY!