Dear New World Investor:

The S&P 500 fell 4.6% in the March quarter, its weakest first quarter performance since 2022. In addition to the negative of high oil and gasoline prices today outweighing the positive – at least in the market’s mind – of not having Iran blow us all to smithereens tomorrow, investors foolishly gave up on the AI trade that I think will be the biggest investment opportunity ever. Nvidia, which has the first trillion dollar backlog in history, dropped 6.5%, Apple fell 6.6%, Alphabet (Google) was down 8.1%, Amazon booked -9.7%, Meta Platforms -13.3%, Tesla -17.3%, and Microsoft was clobbered for 23.4%. Many of the smaller tech stocks suffered 30% to 40% declines.

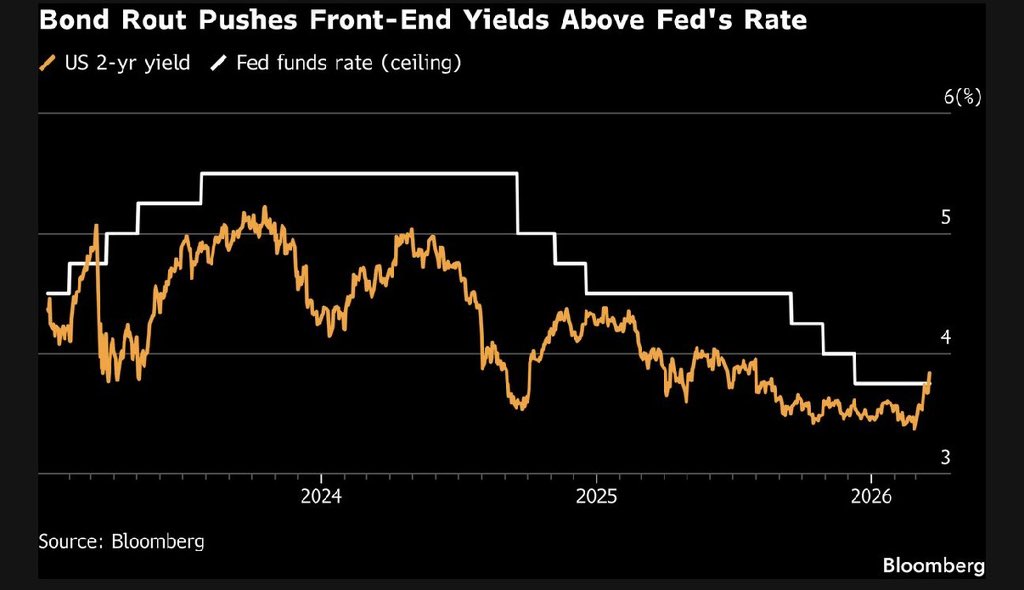

And there may be more to come. The Fed tends to follow the 2-year Treasury note rate (tell me again why we need them?), and the most recent bond rout has pushed the 2-year yield above the Fed’s range:

Click for larger graphic h/t Mohamed El-Erian via @Not_Mr_Risk

Click for larger graphic h/t Mohamed El-Erian via @Not_Mr_Risk

Not since 2023, when the Fed was still lifting rates, has the 2-year yield risen so much above the Fed’s rate ceiling. Last Friday, 5-year yields surpassed 4% for the first time since July, while the 10-year climbed to 4.39%, the highest since August. The bond vigilantes are upset.

So what should you do? History says:

1. This, too, shall pass

2. Markets will go to new highs in the future

3. The newest technologies will create the most opportunities

Or, to be more direct: Don’t sell. Put together your buy list. Start nibbling or dollar-cost averaging.

Market Outlook

After all the sturm und drang, the S&P 500 lost only 0.3% over the last two weeks. The Index is down 3.8% year-to-date. The Nasdaq Composite lost 1.0% and is down 5.9% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) won the two weeks, climbing 5.4% to be up 5.7% year-to-date. The small-cap Russell 2000 sneaked up 1.4% and is up 3.2% in 2026.

Top 5

Changes this week: Added INO to Near-Term, see below

Near-Term – chronological order

INO Inovio – bounce back from equity offering + FDA allows 6-month review of INO-3107

AKBA Akebia Therapeutics – Vafseo launch

BTC-USD Bitcoin – rebound from sell-off

ETH-USD Ethereum – rebound from sell-off

EQT EQT – natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model forecast for March quarter real GDP growth has fallen sharply to +1.6%, well below Wall Street’s expectations. That could push the Fed to cut the Fed funds rate,

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, April 3

Markets Closed

March Payrolls – 8:30am – +60,000 expected; February was -92,000

Thursday, April 9

December quarter GDP – 8:30am – Third estimate, should be a small increase

Personal Consumption Expenditures Index (PCE) – 8:30am – The Fed’s favorite inflation indicator

Friday, April 10

Consumer Price Index – 8:30am

Short Interest After the close

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $255.92) introduced Apple Business, their latest effort to compete with Microsoft. It’s a new all-in-one platform for businesses of all sizes that combines mobile device management, business email and calendar services with custom domain support, and a new option that enables businesses in North America to place local ads in Maps during potential customers’ search and discovery.

That might be useful for restaurants and such. Any added penetration of business computing would be a nice add-on, but I don’t expect this to be any more successful than their many past efforts to compete with Windows. Apple’s computers are just too expensive to deploy widely, and I speak as someone who used to be an all-Macintosh shop.

At this year’s World Wide Developers Conference (WWDC – week of June 8), the rumor is that Apple will feature an updated version of Siri that would allow the digital assistant to handle multiple tasks from a single prompt. This would allow a user to ask Siri to play music, send a text message, and make a phone call in a single request. Currently, users have to make a separate request for each action.

Melius Research reiterated its Buy rating, saying: “Given Apple’s free cash flow and we are about to embark on one of its most lucrative product rollouts since the big screen iPhones in 2014 – there is a case for Apple’s stock regaining some ground.” I believe they are mainly talking about the iPhone 17e and MacBook Neo, although Apple has also recently introduced (checks notes) a refreshed iPad Air, a new MacBook Air, a MacBook Pro, new Studio Displays, and an updated version of the AirPods Max 2 over-the-ear headphones. AAPL is a Buy under $205.

Gilead Sciences (GILD – $139.71) acquired privately-held Ouro Medicines for $1.675 billion in cash, half to be funded by Galapagos (GLPG) in return for ongoing royalties. Ouro develops T cell engager therapies for autoimmune diseases. Their OM336 (gamgertamig) is in a Phase 1/2 trial for severe antibody-mediated orphan diseases, including autoimmune hemolytic anemia (AIHA) and immune thrombocytopenia (ITP). It has been granted both Fast Track and Orphan Drug Designation by the FDA and is expected to enter registrational studies in 2027. This adds to Gilead’s growing inflammation portfolio. GILD is a Long-Term Buy under $115 for a first target of $150.

Meta Platforms (META – $574.46) introduced prescription versions of their Ray-Ban Augmented Reality glasses that can be worn comfortably all day. The company also is testing a premium Instagram subscription tier with exclusive features and AI tools.

The AR glasses roll out in Europe has been delayed by a European Union battery regulation requiring that from February 18, 2027 portable batteries in devices sold on the EU market must be readily removed. Meta’s smart glasses do not have removable batteries.

They also partnered with ARM plc to develop a new class of CPUs to support data centers and large-scale AI deployments. They plan to develop multiple generations of CPUs with Arm, building a silicon portfolio to deliver AI experiences at scale. I am surprised ARM did this, as it puts them in competition with many of their customers, but I don’t see much downside (or upside) for Meta.

Taking a page from Elon Musk’s playbook, Zuck put in place an extremely lucrative options plan for executives if the company hits a market capitalization of more than $9 trillion by 2031, an increase of 500% from its current $1.5 trillion. It isn’t likely they’ll hit it, but we’ll be well served if they do half of that. META is a Buy under $705 for a long-term hold.

Nvidia (NVDA – $177.39) has moved on from the H100 and H200 Hopper chips to the Blackwell GPU. Everyone expected Hopper rental prices would drop considerably as Blackwell deployments ramped up, given the latter’s much lower cost of compute. However, according to SemiAnalysis, the opposite happened in late 2025. The demand for H100s is holding firm, and in many cases, strengthening. H100 1-year GPU rental contract pricing has surged almost 40% from a low of $1.70/hour/GPU in October to $2.35/hour/GPU in March. This is a real-time measure of the true demand for AI compute, primarily inferencing and image/video generation.

SemiAnalysis surveyed over 100 market participants and found that rental capacity is sold out across all GPU types. H100s are getting renewed at the exact same rate they were signed at two to three years ago and some H100 contracts are being renewed for four years. The report noted that the stock market is still anchored to a narrative of eventual oversupply and commoditization, but the reality on the ground points to sustained scarcity and pricing power given an aggressive shortage.

Wells Fargo maintained their Overweight rating and $265 target price. They said Nvidia’s forecast of $1 trillion in data center revenue from its Blackwell and Rubin line of GPUs could wind up being conservative. By a lot. They wrote: “We see 15%-20%+ upside to NVDA’s 2026-2027 data center estimates.”

NVDA is a Hold for a $180 first target.

Palantir (PLTR – $148.46) got the Pentagon’s blessing for their Maven AI system as Deputy Secretary of Defense Steve Feinbergit officially made it a Program of Record. That means it is a core component of US defense.

Palantir and Anduril Industries are working together to develop the core software for the US Golden Dome missile-defense initiative. They expect to have the Golden Dome software ready for testing as early as this summer. The $185 billion Golden Dome is a space-based missile shield designed to counter ballistic, cruise, and hypersonic threats. PLTR is a Buy under $160 for a $200 first target.

Snap (SNAP – $4.63) surged following a public letter from activist investor Irenic Capital Management, which manages $2.5 billion. Irenic, which holds a 2.5% stake in Snap, called for an immediate 21% workforce reduction, a pivot toward AI, and the spinoff or shutdown of the AR Specs division to significantly increase shareholder value. Irenic said that the company’s current strategy is not working and the suggested changes could lift the stock price to over $26.

One way or the other, spinoff or not, I think Snap is extremely cheap. SNAP is a Buy under $11 for a $17+ target.

SoftBank (SFTBY – $11.95) said the PayPay IPO underwriters exercised the entire “green shoe” for more stock, so the SVF II Piranha investment fund controlled by SoftBank netted $369 million. SFTBY is a Buy under $35 for a first target of $50 and then higher as the discount to hard book value disappears.

Small Tech

Fastly (FSLY – $33.50) was named a Leader in The Forrester Wave: Edge Development Platforms, Q1 2026 report (CLICK HERE). This report evaluates top platforms in the market that enable developers to build and deploy applications on distributed infrastructure closer to users and data sources. The company was also the only evaluated vendor to receive above-average customer feedback.

According to the Forrester Wave report: “Customers highlight Fastly’s strong performance, reliability, and developer experience” and “praise the vendor’s highly engaged technical support and proactive partnership. Fastly’s strategy emphasizes a global compute fabric rooted in Wasm security, interoperability, and deterministic performance. Fastly aims to strengthen its already impressive innovative position in AI-assisted development and edge-first event streaming while expanding containers and components to increase workload flexibility. Fastly is a top choice for performance-critical, event-driven, security-sensitive, and globally consistent edge workloads.”

High praise from a respected market research firm and all true. FSLY is a Buy under $10 for a 3- to 5-year hold to $50+.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $6.50) also was highly rated as a Leader and an Outperformer in the 2026 GigaOm Radar for IT Incident Response Platforms report (CLICK HERE).

In addition, PagerDuty had the highest average score across key feature evaluations in this year’s report, underscoring the strength and completeness of its platform. The report places PagerDuty in the Innovation / Platform Play quadrant and recognizes the PagerDuty Operations Cloud for its continued evolution as a centralized system of action for managing time-critical operational work. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

ARK Venture Fund (ARKVX – $48.70) has 17.96% of its assets in SpaceX stock. SpaceX filed for an IPO targeting a $1.75 trillion valuation on only $15.5 billion in revenue – 116x sales. That’s silly. If they can get half of that, ARKVX will shoot up – and we’ll sell it. I’ve been thinking the OpenAI IPO might mark a major AI top, but maybe it will be SpaceX. ARKVX is a Buy for the SpaceX IPO.

Primary Risk: Cathie sells the stock before the IPO.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $1.38) held a virtual R&D day (VIDEO HERE and SLIDES HERE and TRANSCRIPT HERE) to present their kidney disease pipeline.

The pipeline is impressive. Praticiguat is in a Phase 2 trial for a $4.8 billion US market. AKB-097 is in a Phase 1 trial with three potential target markets totaling $45.1 billion. AKB9090 is entering the clinic this quarter.

Click for larger graphic

Click for larger graphic

This was an excellent, detailed presentation, but reality is that Vafseo revenues will drive the stock for at least the next two years. All they said here was that they still expect to become the standard of care for anemia in dialysis patients, and they expect the VOCAL trial top-line data in the December quarter and the VOICE trial top-line data in the first quarter of 2027.

Click for larger graphic

Click for larger graphic

Buy AKBA up to $4 for the Vafseo launches in the EU, UK, and US. I think GSK and/or Amgen will make a bid for the company.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: 2026

Probable time of next financing: Never

Compass Pathways (CMPS – $5.79) announced December quarter results and, as usual, couldn’t say much about the two ongoing Phase 3 trials of COMP360. They are going to meet with the FDA and expect to complete their New Drug Application in the December quarter, targeting approval in 2027. The 26-week data from COMP006 early in the September quarter is expected to be the final dataset for NDA submission.

Management said COMP360 is expected to fit seamlessly across diverse healthcare settings within the current infrastructure of over 7,300 centers offering multi-hour treatments. Treatment centers are growing rapidly, and existing centers are already scaling in anticipation of a COMP360 launch. They believe COMP360 will offer a highly differentiated, patient friendly dosing schedule with a compelling clinical profile and is expected to be a blockbuster (over $1 billion in revenues) opportunity. CMPS is a Buy under $10 for a very long-term hold to $200.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2027

Probable time of next financing: Never

Editas Medicine (EDIT – $2.67) said that the US Patent and Trademark Office reaffirmed the Patent Trial and Appeal Board’s (PTAB) previous decision favoring Editas and the Broad Institute in the patent interference involving specific patents for CRISPR/Cas9 editing in human cells. This action by the PTAB is its third favorable decision determining that Broad was the first to invent the use of CRISPR/Cas9 for gene editing in eukaryotic cells, including human cells. It can, of course, be appealed…again. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved. Owned: Going into the clinic mid-2025.

Probable time of next FDA approval: 2028

Probable time of next financing: Late 2026 or never

Inovio (INO – $1.13) dropped today after they raised about $16 million in an underwritten public offering of 12.5 million shares of stock plus Series A and Series B warrants to purchase up to 12.5 million shares each, all priced at a combined $1.40 per share. The warrants have an exercise price of $1.40 per share.

As I always say, the second-worst news a biotech investor can get is their company is raising money. The first-worst news? Their company can’t raise money.

I expect the next news from Inovio will be that the SEC has granted them 6-month accelerated approval after all, so take advantage of this dip – it won’t last. I added INO to the Near-Term Top 5 list. INO is a Buy under $5 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2026

Probable time of next financing:After FDA approval in 2026

ScyNexis (SCYX – $0.89) acquired PXL-770 (now SCY-770) from Poxel SA for an upfront payment of $8 million, with future potential payments of up to $8 million in development milestones, and up to $180 million in commercial milestones, of which $125 million is triggered by annual net sales at or above $1 billion.

SCY-770 is a novel, highly selective, direct AMP-activated protein kinase (AMPK) activator for the treatment of ADPKD, the leading genetic cause of end-stage renal failure. SCY-770 is designed to address many of the underlying drivers of ADPKD by reducing cyst growth and disease progression. It has already been granted Orphan Drug Designation by the FDA.

Click for larger graphic

Click for larger graphic

It’s an oral therapy that has been evaluated in eight clinical trials, with a favorable safety profile. ScyNexis will begin a Phase 2 proof-of-concept study in ADPKD patients in the December quarter, with an early efficacy readout in the second half of 2027.

On the conference call, (CALL HERE and SLIDES HERE and TRANSCRIPT HERE), CEO David Angulo said: “We are excited about this transformative asset acquisition, strengthening our pipeline, and dedicating our development expertise and resources to tackle severe and rare diseases. SCY-770 is supported by a strong pre-clinical data package and a novel differentiated MOA that targets multiple key drivers of ADPKD progression, positioning it as a promising candidate in a significant rare disease market with a high unmet need.”

ScyNexis had $56 million in cash at the end of 2025 and just did a $40 million offering. They have a cash runway into 2029, no debt, and the potential to receive up to $146 million in Brexafemme sales milestones plus low-to-mid single-digit royalties from GSK. Buy SCYX under $2.50 for a target price of $20.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2028

Probable time of next financing: Never

Inflation MegaShift

Gold ($4,702.70) pulled back hard, from over $5,000 to around $4,100 last Monday, before gaining half of the loss back. Every shakeout over the past two years has been a buying opportunity, and so is this one. The underlying drivers (dollar debasement, central bank accumulation, safe haven demand) haven’t gotten any weaker. They’re stronger.

The worse private credit gets, the more the Fed will print. The more they print, the higher gold goes. It’s not complicated – it’s just math that most people don’t want to accept. $5,000+ may be as good as it gets in 2026, but I think we’ll see $6,000+ next year and, unless something dramatic changes, you can add $1,000 to the upper end of the range every year.

Miners & Related

Coeur Mining (CDE – $19.09) gave a corporate update following the March 20 completion of the acquisition of New Gold, including consolidated 2026 guidance, 2025 mineral reserves and resources for the newly-acquired New Afton and Rainy River mines, and an updated financial policy highlighted by a robust new return of capital program.

On a conference call, (CALL HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Mitch Krebs said they expect 2026 consolidated gold production of 680,000-815,000 ounces, up from 419,046 ounces in 2025. Silver production will increase from 17.9 million ounces in 2025 to 18.7-21.9 million ounces this year. Copper production will hit 50-65 million pounds. All of these include only nine months of contribution from the two new Canadian mines, so further growth in 2027 is baked in.

The Board authorized an expanded $750 million stock buyback program. Also, Coeur entered into a new $1.0 billion revolving credit facility to further bolster its liquidity profile. CDE is a Buy under $10 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $21.84) has launched a $75 million restart plan for its Jerritt Canyon gold mine in Nevada. You may remember that they mothballed it in March 2023 when gold prices were in the $1,600-$1,900 range, citing high contractor costs and multiple extreme weather events affecting northern Nevada during the winter of 2022-23.

In addition to the higher price of gold, successful drilling results over the past two years have expanded the mineral resource. At the end of 2025, Jerritt Canyon had 4.1 million ounces of gold in the Measured & Indicated category, with an additional 3.7 million ounces Inferred.

BMO Capital upgraded the stock from Market Perform to Outperform with a C$35 target price, saying it is discounted compared to historical trading multiples. AG trades at 2.2x net asset value and 10x next-12-month cash flow from operations, compared to historical multiples often exceeding 3x NAV and 15x cash flow. They also pointed to the expanding processing capacity at the Santa Elena and Gatos mines, the restart potential at Jerritt Canyon, and the development of newly discovered deposits at Santa Elena. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Royal Gold (RGLD – $262.63) moved up after a good Investor Day conference call (CALL HERE and SLIDES HERE and TRANSCRIPT HERE). CEO Bill Heissenbuttel said they expect 2026 sales of 290,000 to 320,000 ounces of gold (+32% from 2025), 3.0 to 3.5 million ounces of silver (+8% from last year), 21.0 to 25.0 million pounds of copper (+40%), and $34 million to $38 million of other metals, including nickel, zinc, and lead.

For the first time ever, they issued a 5-year outlook for 430,000 to 480.000 total gold equivalent ounces in 2030. They’ll update this every year to include assets that will begin production during the following five years. The 2026 outlook did not include Cactus (mining on RGLD’s royalty area), Fourmile, Gualcamayo, Horne 5, MARA, Oyu Tolgoi, and increased production from the Platreef Phase 3 expansion, because all those will begin production after 2030.

They also didn’t assume any contribution from the 30% joint venture interest in the Hod Maden project that was part of the Sandstorm acquisition because they plan to convert their direct joint venture ownership into a stream or royalty interest. You can download their 2025/2026 Asset Handbook HERE.

In a final bit of good news, in March they paid down another $125 million on their revolving credit facility, reducing the outstanding amount to $600 million and increasing the available amount to $800 million. RGLD is a Buy under $180.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly.

Bitcoin (BTC-USD on Yahoo – $66,941.51) is bouncing along its year-to-date lows, acting more like a volatile stock afraid of the Iran war than a safe haven alternative to gold – which is what it is. I still think the next top is around $150,000.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $37.97) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Ethereum Trust (ETHA- $15.63) remains the cheapest and easiest way to buy ethereum. ETHA is a Buy for the coming explosion in token-funded start-ups.

Primary Risk: Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $112.06

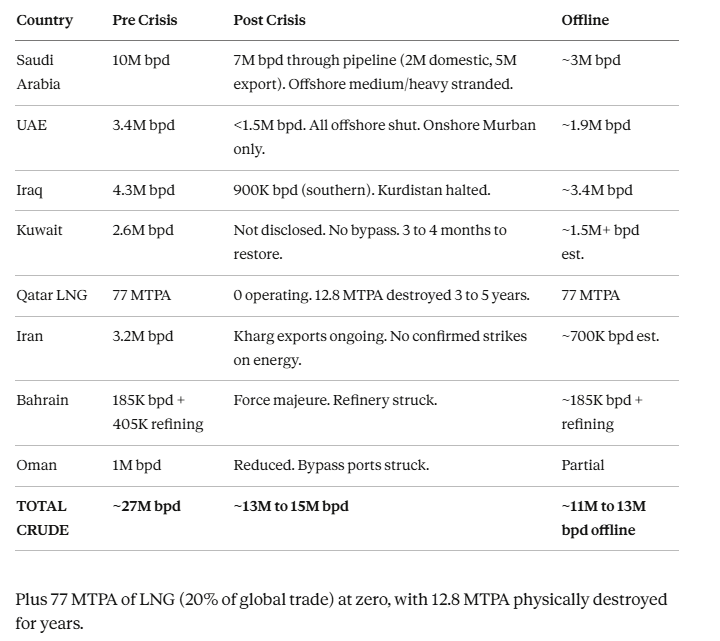

If the war ended tomorrow (it won’t), it would take many months to rebuild the Mideast energy infrastructure. Pipelines, storage facilities, refineries, oil and gas fields – the damage is extensive. The paper “oil glut” is gone for years.

How big is the reduction in Mideast oil supplies?

Click for larger graphic h/t @chigrl

Click for larger graphic h/t @chigrl

Most people outside of energy don’t realize how much 11 to 13 million barrels a day of shut-in for crude is. In a “typical tight” oil market, the deficit is usually anything above ~1 million barrels a day over the span of a year. The marginal barrel sets the price.

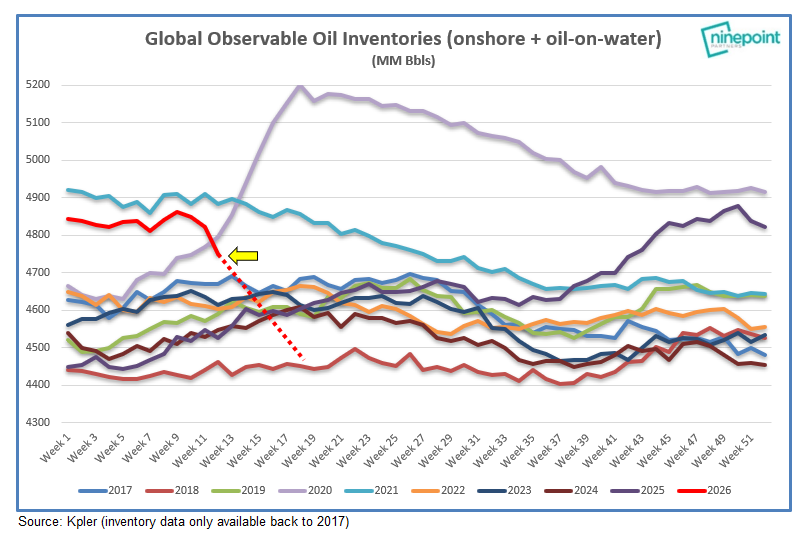

While the worst energy crisis of our lifetimes remains, the Strait of Hormuz was always going to reopen someday. I’m more interested in what happens after it reopens. The oil-on-water inventories will be falling by over five million barrels a day with less than 35 million barrels of Russian and Iranian floating storage to unsanction.

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

Production is down 11 to 13 million barrels a day and will take time to be restored even when the Strait fully opens. The “oil glut” narrative is officially dead as those barrels are gone forever. The biggest bear thesis is no more.

Given SPR refilling, product hoarding, the twilight of US shale, the peaking of non-OPEC production, the lack of meaningful OPEC spare capacity, and the decades ahead of oil demand growth, I have to think oil is going higher.

The September 2027 Crude Oil Futures (CLU7.NYM – $68.37) are a Buy under $75 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $48.30) is a Buy under $40 for a $100+ target.

Energy Fuels (UUUU – $17.75) produced its first kilogram (kg) of terbium (Tb) oxide at its White Mesa Mill in Utah. Using monazite ore sourced from the US, they achieved a purity of 99.9% Tb at pilot scale, which meets the specifications of global manufacturers of rare earth permanent magnets. This achievement follows their recent announcement that they have produced nearly 30 kg of 99.9% pure dysprosium (Dy) oxide production, another critical “heavy” rare earth oxide (REO) used in permanent magnets. Like their Dy oxide, the Tb oxide has been requested by multiple magnet manufacturers and OEMs around the world to begin product validation. Both Dy and Tb are subject to Chinese export controls, highlighting the need for secure, western supply chains.

Adding Dy and Tb to permanent magnets makes a superior product for electric vehicles and hybrids, drones, robotics, and defense technologies by improving operational capabilities in high heat conditions and enabling smaller, lighter, and more powerful motors and actuators. The Mill expects to continue producing terbium oxide at an approximate rate of one kilogram per week in its existing pilot circuit. An expanded commercial circuit is expected to be operational as early as 2027, with planned production recovery of up to approximately 35 tonnes of Dy and 12 tonnes of Tb per year. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

EQT (EQT – $59.70) had $1 billion in free cash flow in a single month in January because they came into 2026 unhedged, which is unlike them, and were able to sell their monthly production at a much higher price because of the extreme cold snap across most of the eastern US.

EQT will grow revenues by about 15% this year with earnings per share forecast to jump from $3.05 last year to $4.70 in 2026. That means, at about $59, we’re paying only about 12.6x earnings and, because depletion and depreciation charges have a big impact, around 6.5x cash flow per share. EQT is a buy under $70 for a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

Click for larger graphic h/t @a16z

Click for larger graphic h/t @a16z

* * * * *

Click for larger graphic h/t Emerging AI

Click for larger graphic h/t Emerging AI

* * * * *

RIP Dash Crofts

the singer-songwriter half of Seals and Crofts

* * * * *

Your considering Iran’s centers of gravity and how they are being attacked Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 4/2/26. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $255.92) – Buy under $205

Gilead Sciences (GILD – $139.71) – Buy under $115, first target price $150

Meta (META – $574.46) – Buy under $705 for a long-term hold

Nvidia (NVDA – $177.39) – Buy under $200 for a long-term hold

Onsemi (ON – $62.19) – Buy under $60, first target price $130

Palantir (PLTR – $148.46) – Buy under $160 for $200 first target price

PayPal (PYPL – $45.34) – Buy under $50, target price $150

Snap (SNAP – $4.63) – Buy under $11, target price $17+

Small Tech

Enovix (ENVX – $5.06) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $64.19) – Buy under $75; 3- to 5-year hold

Fastly (FSLY – $33.50) – Buy under $10 for a 3- to 5-year hold to $50+

PagerDuty (PD – $6.40) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $9.92) – Buy under $10, target price $40

ARK Venture Fund (ARKVX – $48.70) – Buy for SpaceX IPO

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.52) – Buy under $6, target $30+

Akebia Therapeutics (AKBA – $1.38) – Buy under $4, target $20

Compass Pathways (CMPS – $5.79) – Buy under $10, hold a long time for a 20x return

Editas Medicines (EDIT – $2.67) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $1.13) – Buy under $5, hold a long time

Medicenna (MDNAF – $0.46) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $0.89) – Buy under $2.50, target price $20, then $50

TG Therapeutics (TGTX – $33.53) – Buy under $30 for buyout at $40+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($73.17) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $78.58) – Buy under $50, target price $75

Sprott Junior Gold Miners ETF (SGDJ – $88.25) – Buy under $60, target price $100

Sprott Physical Gold and Silver Trust (CEF – $47.05) – Buy under $35, target price $60

Global X Silver Miners ETF (SIL – $92.65) – Buy under $60, target price $100

Coeur Mining (CDE – $19.09) – Buy under $10, target price $20

Paramount Gold Nevada (PZG – $1.72) – Buy under $1, first target price $10

Royal Gold (RGLD – $262.63) – Buy under $180

Cryptocurrencies

Bitcoin (BTC-USD – $66,941.51) – Buy

iShares Bitcoin Trust (IBIT – $37.97) – Buy

Ethereum (ETH-USD – $2,052.77)– Buy

iShares Ethereum Trust (ETHA- $15.63) – Buy

Commodities

Crude Oil Futures – September 2027 (CLU7.NYM – $68.37) – Buy under $75; $200+ target

United States 12 Month Oil Fund, LP (USL – $48.30) – Buy under $40; $100+ target

Vermilion Energy (VET – $13.38) – Buy under $11; $24+ target

Energy Fuels (UUUU – $17.75) – Buy under $18; $30 target

EQT (EQT – $59.70) – Buy under $70; hold for much higher prices ($100+)

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

SoftBank (SFTBY – $11.95) – Hold

Dakota Gold (DC – $5.23) – Hold for higher gold prices

First Majestic Mining (AG – $21.84) – Hold for higher silver prices

Freeport McMoRan (FCX – $61.38) – Hold for higher copper prices

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2026

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

“Summer Breeze makes me feel fine, blowin’ through the jasmine in my mind”… brings back very clear images of sitting on the side of my bed with a guitar in my hand, trying to make the little two chord shift of that intro sound exactly like the one coming out of my clock radio…but making my voice mimic the tight harmonies of those two unique voices, well, that was never gonna happen… thanks for the memory MM, music always seems to trigger so many vivid ones… RIP Dash Crofts (& Jim Seals)

MM, on AKBA, R&D for the rare kidney diseases will cost a fortune. If Vafseo sales don’t dramatically increase to fund all this, the stock will plunge. Generic Auryxia is an imminent risk also. Vafseo sales will have to offset Auryxia sales declines, although Auryxia is in the TDAPA bundle for as long as TDAPA lasts. If TDAPA is not extended past 2026, that is another risk. Please comment.

They aren’t so dumb that they will spend a fortune on R&D. They can get through Phase 1 trials pretty cheaply. After that, you’re right that it gets very expensive.

Auryxia sales have held up much better than anyone expected, but I don’t think those sales are in anybody’s valuation model. It’s all Vafseo.

Butler’s huge mistake was not dealing with the initial hematocrit drop when a patient is switched from an ESA to Vafseo. He must have known about it. That’s what caused the sharp inventory decline in the December quarter.

I want to see March end-user sales over $15 million, plus some inventory restocking. That would set the stage for rapid revenur growth in the next 3 quarters.

Also, why hasn’t Fresenius signed on, or at least started a 100-center pilot program?

And, why is Butler now asking for an increase in authorized shares from 350MM to 500MM plus 25MM in preferreds? He still has roughly 100million shares of common that he could issue why asking for these enormous potential dilutions, and why NOW!!???

One of YOUR main bullish points recently has been AKBA large net cash position and the growing cash flow from Vafseo which would protect shareholders against excessive and value destructive dilutions. So much for that…now we have to understand if Butler has Terry Norchi’s disease, the shareholder’s account as an ATM machine.

The Terry Norchi disease is more common among small companies than HBP in the general population. I fear that Q1 sales of Auryxia + Vafseo weren’t so great, and dilution is needed to raise money for pipeline adventures.

I used to mix Seals and Croft at the Troubador in LA….nice people, super talented….RIP

You worked at the Troubador? When is your book coming out?

Hoping to read some views on INO. They diluted 50% if you include warrents and droped 35% on Friday.

A quick recap of recent history to start.

INO was smart and raised $664 million in the 2020-2021 timeframe when biotech was booming and INO was also trading at lofty prices. I’m sure they thought that would be more than enough to get one or more drugs launched but as is often the case in the biotech space, INO suffered a number of setbacks.

Current Cash & investments:

INO should end Q2 with between $35 million & $40 million in cash.

It appears INO has reduced their discomfort level for their cash & investments balance from roughly $50 million in 2025 to $35 million in 2026.

Shares: INO has gone from ~8 million shares when MM recommended the stock in 2018,

It’s likely that INO does one more financing at the end of Q2, and if the FDA doesn’t revise their approval date a second raise in Q3 is likely. Given the stock price & likely associated warrants, these offerings will be highly dilutive. Just one additional similar sized offering could take INO to ~100 million shares + 70 million warrants.

For me, it’s too early and there is far too much uncertainty regarding the remainder of 2026 to view now as a good entry point.

For anyone considering doing so a few things to ask yourself would be:

Thanks Brent

im not sure it works. plasmids have been tried before by VICL with a different delivery method. electropireces (sp.) INO delivery method might work to get the plasmids through the cell wall but im not convinced once in the cell, it will have a significant result.

twice burned 4-shy

Any thoughts on who will benefit from ORCL sacking scads of employees

Larry Elliswine, the second richest person in human history??

Michael any thoughts on the probability of quantum computers and their code breaking abilities as they relate to crypto, specifically BTC and if so the timing of any concern? Thanks

Also any timeline predictions on PZG selling or partnering Grassy and or Sleeper? Thanks again

Quantum breaking BTC addresses is a long way off. You can always move your wallet to offline storage and have 0 risk.

PZG should sell or partner both projects in the next 12 months. They’ve done as much as they can as a prospect developer, which is what they are.

If quantum breaking BTC addresses do come out will it cause a lack of confidence in the public such that they sell and collapse the price or sell simply due to the potential? Thanks

This was the theme song for 1000’s of high school graduations in the late 1970’s:

https://youtu.be/1qlNoF0C_h4?list=RD1qlNoF0C_h4&t=3

Medicenna Therapeutics Appoints Dr. Nageatte Ibrahim as Chief Medical Officer – Medicenna Therapeutics

The most notable part of her resume is her time at Merck, where she played a pivotal role in the development of pembrolizumab (Keytruda).

Always good to see a heavyweight decide to move to one of our companies.

New World Investor for 4.16.26 is posted.

MM,the word on the street is staying butler from akba wants to issue another couple of hundred million more shares to have at his disposal to put out into the market,the shorts must have gotten wind of it,and there it went …

Is saying butler wants to dilute more