Dear New World Investor:

New Recommendation: Vermilion Energy (VET) – See below under Oil

Last Friday, stocks rallied sharply after December payroll additions were revised up from +216,000 to +333,000. We learned that the US added another 353,000 jobs in January, the most since January 2023, nearly twice the consensus estimate (180,000) and the largest increase in a year. Or did we? Wait – January?

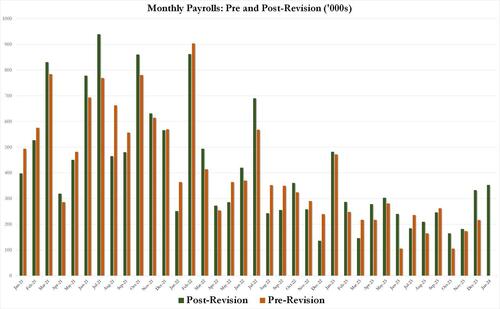

Every year in January, the Bureau of Labor Statistics conducts its “annual re-benchmarking and update of seasonal adjustment factors.” Long story short, what was until December some mediocre jobs numbers have now been miraculously transformed into substantial gains, as shown in the chart below. While the seasonally adjusted January payrolls were up 353,000, the unadjusted was down 2.635 million.

Click for larger graphic h/t @zerohedge

Click for larger graphic h/t @zerohedge

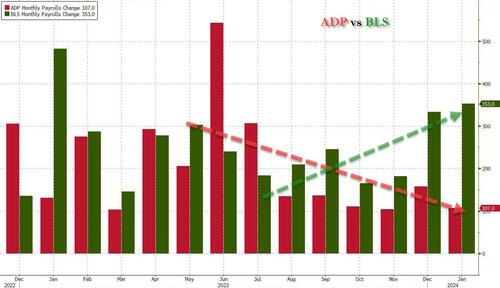

A comparison between the revised BLS Payrolls number and the ADP payrolls show the BLS numbers are now clearly rising even as the impartial ADP (which directly logs employment numbers at the company level and is actually far more accurate), shows an accelerating slowdown.

Click for larger graphic h/t @zerohedge

Click for larger graphic h/t @zerohedge

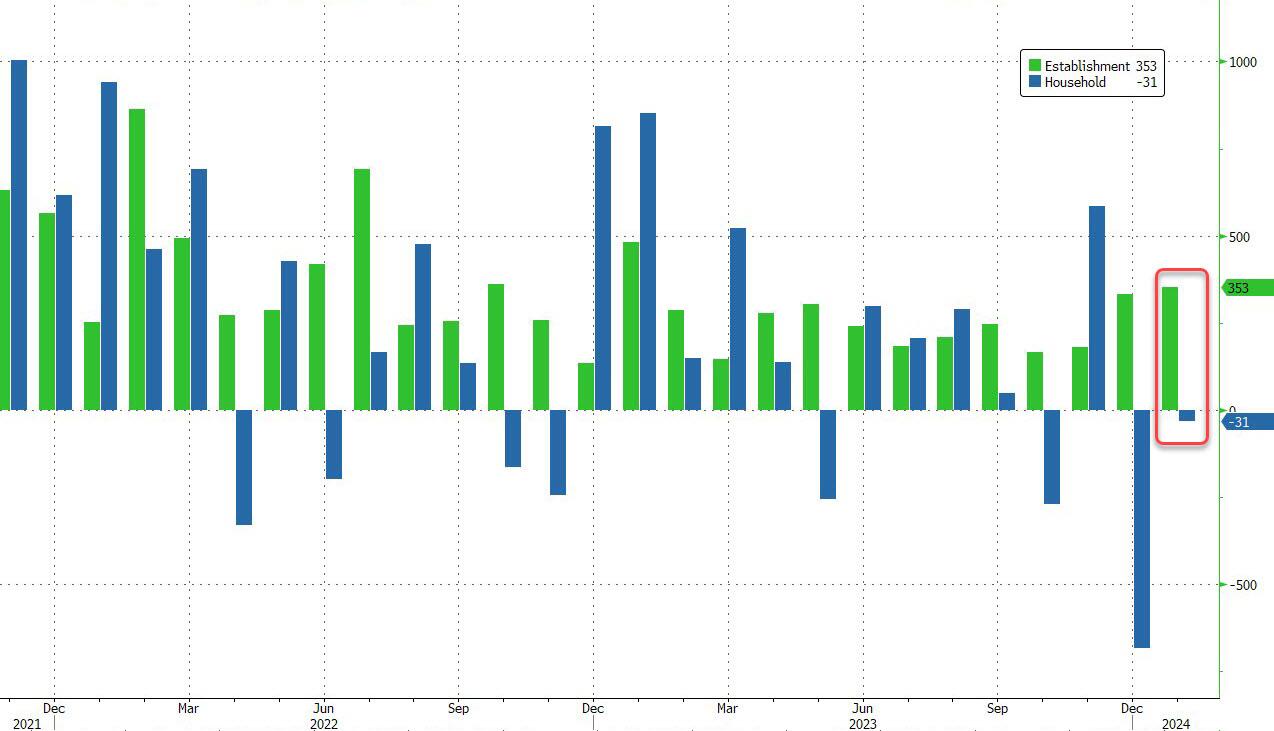

And the the latest divergence between the Establishment (payrolls) survey and the much more accurate Household (actual employment) survey showed that in contrast to the BLS claim that January added 353,000 jobs, the Household survey found that the number of actually employed workers dropped again, this time by 31,000 from 161,183.000 to 161,152,000.

Click for larger graphic h/t @zerohedge

Click for larger graphic h/t @zerohedge

The problem here is the Establishment survey contacts larger firms to answer hiring questions and then estimates small business job creation based on the large companies answers. If there is stress that’s specific to smaller business, as there is now, the estimates will be far too rosy.

Most of those new jobs are part-time as people take on second and third jobs to cope with past inflation. Full-time jobs aren’t growing:

Click for larger graphic h/t @DiMartinoBooth

And according to outplacement firm Challenger, Gray & Christmas , job cut announcements in January increased to its highest level in 10 months, a 136% surge from December. But Wall Street bought the BLS numbers and stocks rallied.

Those high spirits took a knock after Powell, in a 60 Minutes interview that aired last Sunday, doubled down on his midweek message that the central bank will tread cautiously in deciding when to cut rates. He said the “danger of moving too soon is the job’s not quite done” in quelling inflation.

High – but not higher – for longer. Where have I heard that before?

Money Supply

M1 is a measure of cash and coins in circulation, as well as demand deposits in checking accounts. It’s money that can be easily accessed and spent by consumers.

The M2 money supply is everything in M1 plus savings accounts, money market funds, and certificates of deposit (CDs) below $100,000. This money can also be spent by consumers, but it requires a little extra work to access it.

Growing economies require more capital in circulation to facilitate transactions, which results in M2 increasing virtually every year. But it’s those rare instances where M2 does decline, and consumers are forced to forgo some of their purchases, that have resulted in trouble for the US economy and Wall Street. M2 peaked at roughly $21.7 trillion in July 2022. As of December 2023, M2 sat at approximately $20.87 trillion.

Click for larger graphic h/t @stlouisfed

Click for larger graphic h/t @stlouisfed

That chart doesn’t look like much of a downturn, but look at the percentage drop from its high:

Click for larger graphic h/t @themotleyfool

Click for larger graphic h/t @themotleyfool

M2 has fallen by 1.68% on a year-over-year basis and 3.86% since its summer 2022 peak. This represents the first meaningful decline in M2 since the Great Depression.

On a nominal basis, a 3.86% drop probably doesn’t sound like much. In fact, with M2 expanding by a record 26% on a year-over-year basis during the pandemic, a reasonable argument could be made that a 3.86% retracement since mid-2022 is nothing more than a reversion to the mean for money supply. Could be.

But in the past, M2 drops of 2% or more have been signs of an economic downturn. There have been only five instances since 1870 where M2 has fallen by at least 2%: 1878, 1893, 1921, 1931-1933, and July 2022-currently. All four previous instances led to deflationary depressions and a sizable increase in the U.S. unemployment rate.

Click for larger graphic

Click for larger graphic

The depressions in 1878 and 1893 occurred before to the creation of the Fed. With the tools available now, it’s highly unlikely a depression would happen. But history suggests that significant declines in the M2 money supply shouldn’t be ignored. A recession is coming, even if Wall Street doesn’t believe it.

Market Outlook

The S&P 500 added 1.9% since last Thursday, touched 5000 today, and has traded higher on the calendar week for 13 of the last 14 weeks, which has not happened in almost 30 years. The Index is up 4.8% year-to-date.

So are investors all in? As if! Since the start of 2024, investors have pulled $29.2 billion from the SPDR S&P 500 ETF Trust (SPY), the largest outflows of any ETF by far, and larger than any annual outflow for SPY, other than 2015’s $32.3 billion.

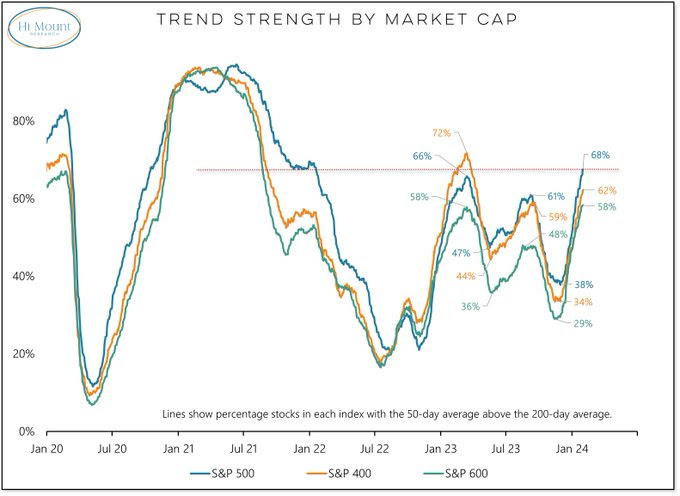

How narrow can the rally be when more than two-thirds of the stocks in the S&P 500 have 50-day averages above their 200-day averages? That’s the best level in more than two years and is still rising.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

The Nasdaq Composite gained 2.8% as Big Tech came back in favor. It is up 5.2% for the year. The consolidation / break-up tango is continuing:

Click for larger graphic h/t @themarketear

Click for larger graphic h/t @themarketear

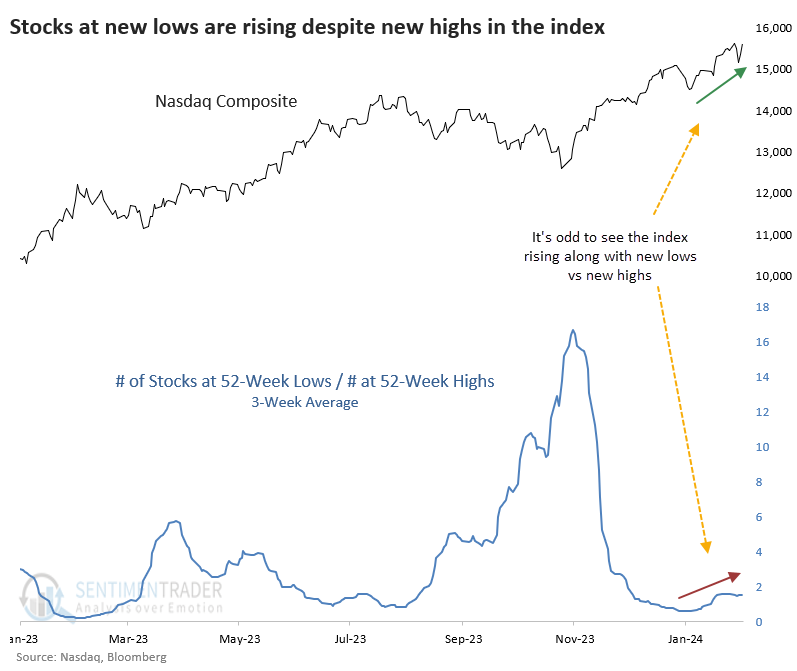

But it’s concerning that despite the Composite hitting multiple new highs in recent weeks, more stocks have been falling to new lows than new highs. This is a highly unusual split that has typically preceded weak returns.

Click for larger graphic h/t @sentimentrader

Click for larger graphic h/t @sentimentrader

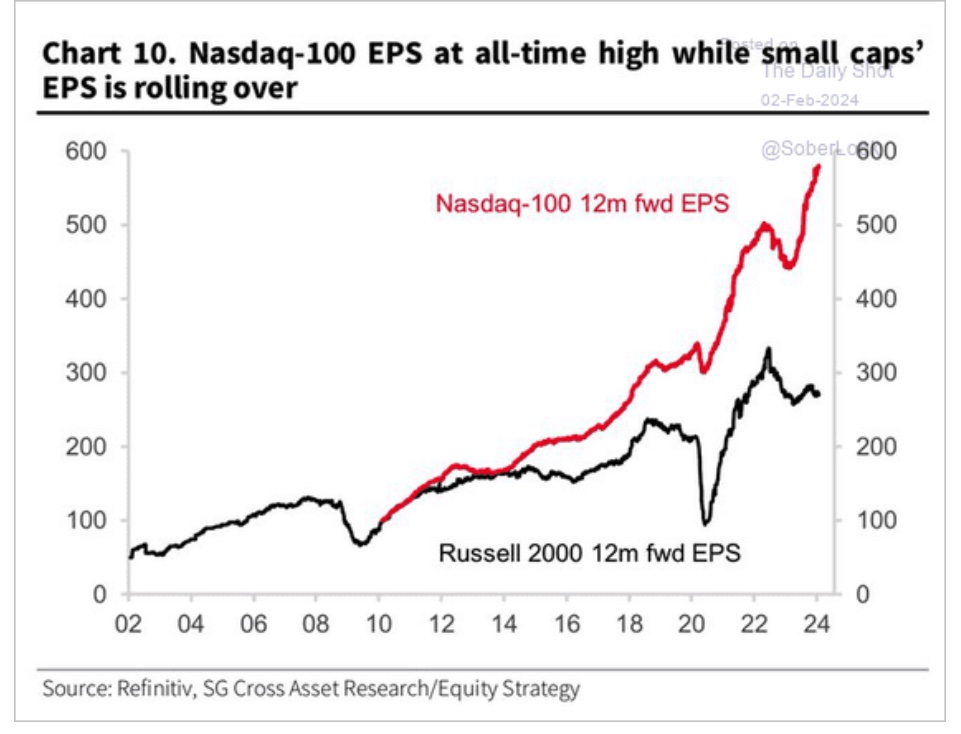

The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 2.8% but is just flat year-to-date. The small-cap Russell 2000 eked out a 0.3% gain and is down 2.3% in 2024. As @BobEUnlimited pointed out, we have to consider whether the relative cheapness of an index is appropriate given the fundamentals. The underperformance of the Russel 2000 compared to Nasdaq probably is in large part driven by the significant divergence in the level and trend of earnings.

Click for larger graphic h/t

Click for larger graphic h/t

And most days it feels like:

Click for larger graphic h/t @BeenThereCap

Click for larger graphic h/t @BeenThereCap

In this new bull market, the S&P 500 is now up 36.7% from its October 12, 2022 closing low of 3,577.03. The prior bear market saw the index fall 25.4% over 282 days.

Click for larger graphic h/t @bespokeinvest

Click for larger graphic h/t @bespokeinvest

The fractal dimension is extended below 30, meaning this rally is done. Yes, it could go further – Wall Street loves round numbers, so an S&P 500 close over 5,000 is in the cards. Maybe it will even go up through Nvidia’s earnings report on February 21, but we are on very thin ice.

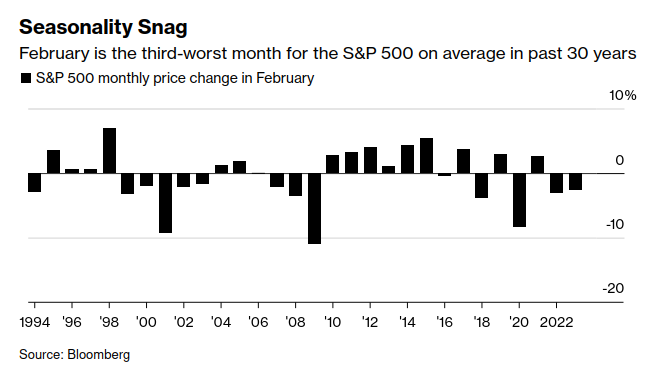

February is the third-worst month for the S&P 500 on average over the last 30 years, particularly the last two weeks, and especially true in election years.

Click for larger graphic h/y @Mayhem4Markets

Click for larger graphic h/y @Mayhem4Markets

But the uptrend that started in late November 1971, which this one resembles, rallied for 15 weeks initially (this one 13 weeks), had a 3 week pullback, then made a multi week high on week 20. IF – big “if” – the 2023-2024 rally keeps resembling it, the next multi-week high will happen in March around 5110.

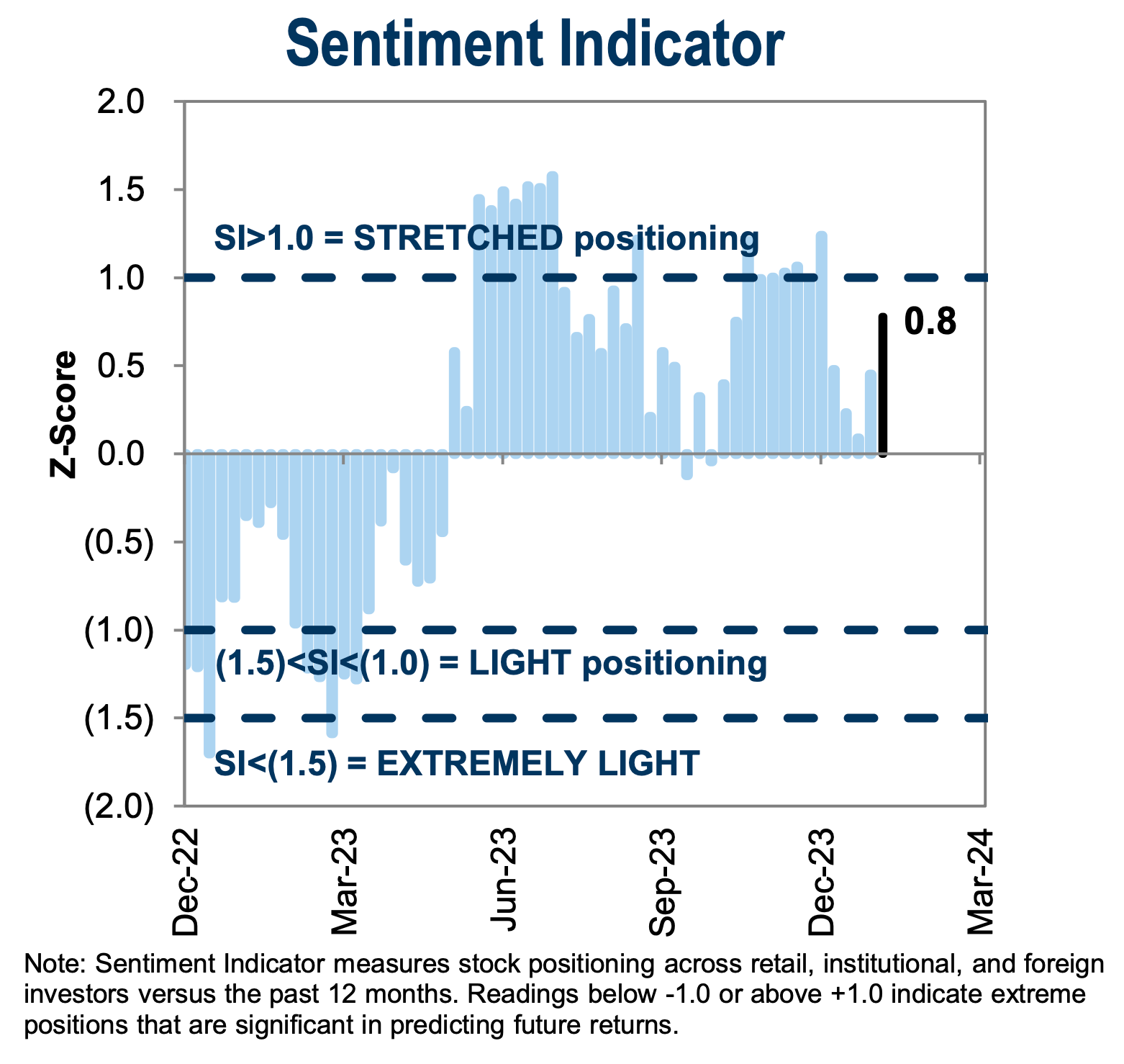

Goldman’s sentiment indicator is rising but is not yet stretched.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

Stocks will outperform bonds as long as the economy keeps going. The economy will keep going as long as stocks and home prices don’t fall too much. Prices of stocks and homes won’t fall too much as long as bond yields don’t rise too high for too long.

Top 5

Changes this week: Removed NVTA from Long-Term as they deal with their finances

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Citi Economic Surprise Index is at its highest since November.

Click for larger graphic h/t @dailychartbook

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, February 9

Short interest – After the close

Tuesday, February 13

Consumer Price Index – 8:30am –

CMPS – Compass Pathways – 2:00pm – Oppenheimer Life Sciences Conference fireside chat

EQT – EQT – After the close – Earnings release; call tomorrow

Wednesday, February 14

EQT – EQT – 10:00am – Earnings conference call

RKLB – Rocket Lab – 10:45am – TD Cowen Aerospace & Defense Conference

INO – Inovio – 12:40pm – Oppenheimer Life Sciences Conference

FSLY – Fastly – 4:30pm – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $188.32) is working on developing a foldable “clamshell” iPhone, which seems to be an attractive form factor again. Arch competitor Samsung’s Galaxy Z Fold 5 and Flip 5 are selling well. Apple’s version won’t be a me-too – that’s not their style. Expect some amazing features.

Nor is their AI me-too. CEO Tim Cook said they have been investing in AI and “We’ve got some things that we are incredibly excited about that we will be showing later this year…I think there is a huge opportunity for Apple with gen. AI and AI.”

The Vision Pro teardowns have started, with no blockbuster news yet. Apple expects a large business market for the spatial computing headset, citing Bloomberg, Nike, SAP, Vanguard, and Walmart as early customers. Cook said: “What has happened over the last several years is that employees are in a position in many companies to choose their own technology that is the best for them, That is a huge advantage for Apple.”

For all you USHER fans out there, Apple Music curated a collection of exclusive content ahead of his Apple Music Super Bowl LVIII Halftime Show this Sunday, including his complete studio album discography in Spatial Audio. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $31.72) announced a 28¢ quarterly dividend. That’s a 3.5% yield while we wait for their consumer markets to rebound – as they will. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

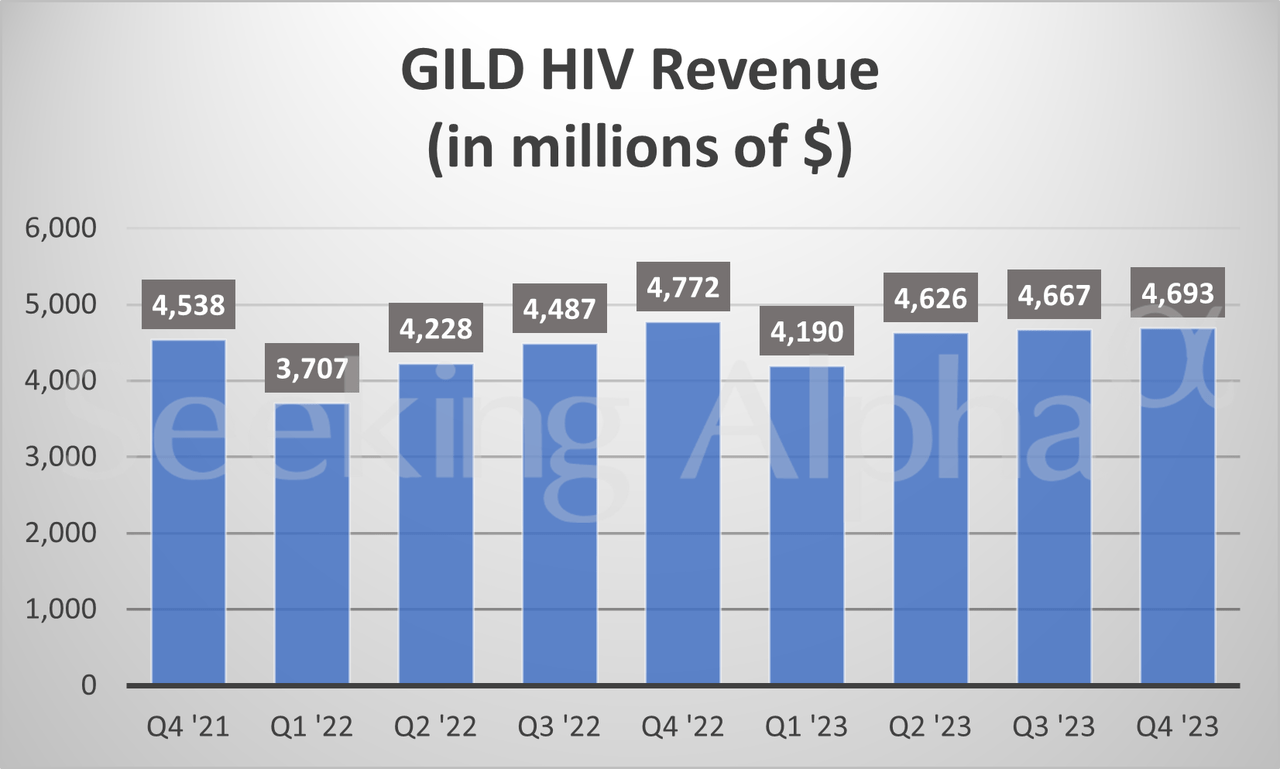

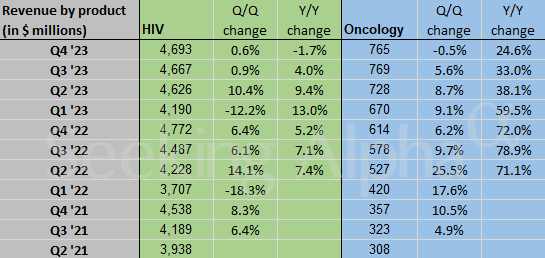

Gilead Sciences (GILD – $73.80) reported December quarter revenues down 3.7% from last year to $7.12 billion, although $20 million better than the $7.1 billion estimate. Pro forma earnings per share of $1.72 missed by four cents.

HIV revenue is pretty flat:

Click for larger graphic h/t Seeking Alpha

Click for larger graphic h/t Seeking Alpha

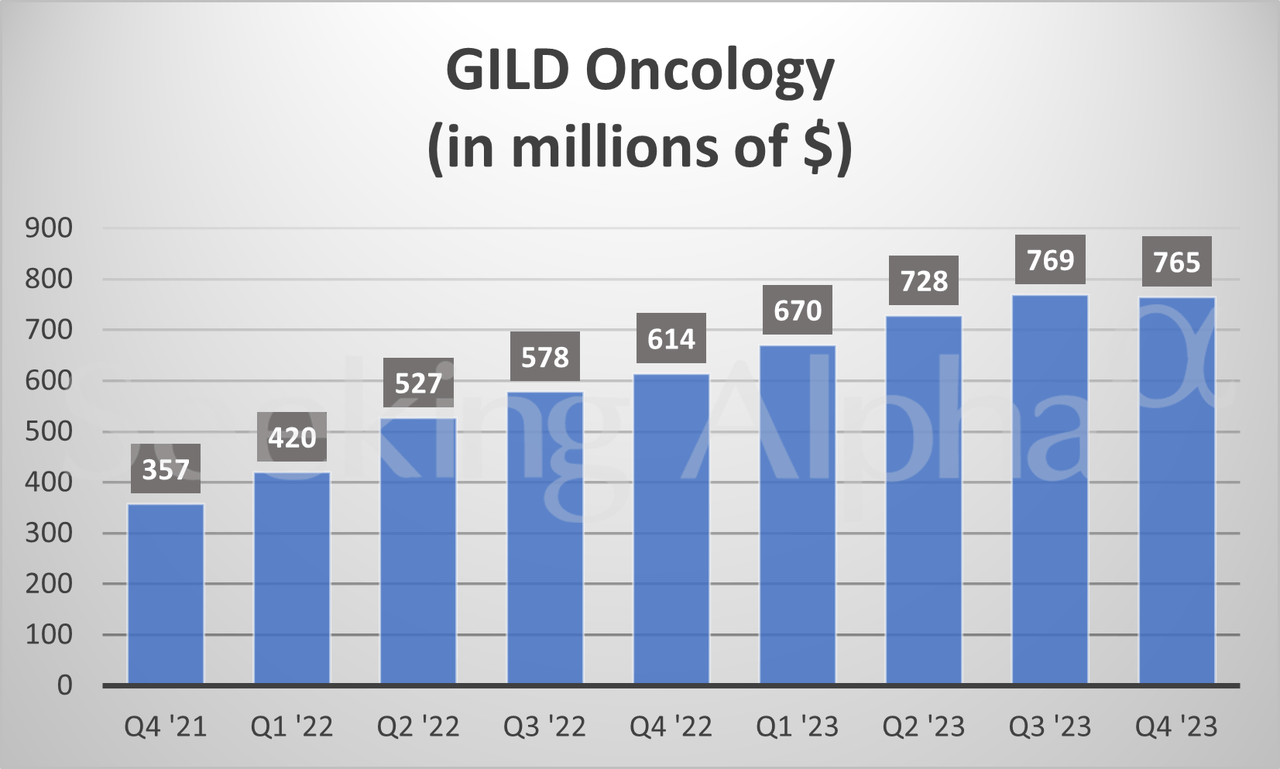

Oncology revenue has been growing rapidly, but the December quarter was down from September:

Click for larger graphic h/t Seeking Alpha

Click for larger graphic h/t Seeking Alpha

Click for larger graphic h/t Seeking Alpha

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management guided for full-year 2024 product sales of $27.1 billion to $27.5 billion, including Veklury (remdesivir). Excluding $1.3 billion in Veklury sales, they are expecting $25.8 billion to $26.2 billion. That should yield pro forma earnings of $6.85 to $7.25 a share. The Street consensus was at $7.19. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $470.00) added $197 billion to its market cap last Friday, a stock market record for a single day that eclipsed the $190 billion gains made by Apple and Amazon in 2022. Meta shares closed at $474.99 on Friday; at its lows in 2022, the stock fell to $90. I recommended it on April 5, 2018 at $159.34, and I also recommended it in Boomberg on October 28, 2022 at $99.20.

With the stock well over my 2024 target price of $400, I would not chase it. I will have to raise the buy limit later this year to get ready for a $500 target in 2025. For now, META remains a Buy under $345 for a $400 target in 2024.

SoftBank (SFTBY – $26.66) reported $11.9 billion in revenues and a $6.6 billion profit in the December quarter after four straight quarters of losses driven by Vision Fund losses. But there have been higher valuations in recent funding rounds for Vision Fund companies, and it looks like the environment for tech startups has turned positive.

On the conference call (VIDEO HERE and SLIDES HERE and TRANSCRIPT HERE), management said they have almost $30 billion in cash available for new investments.

The stock surged 18.2% today after 90.6%-owned ARM Holdings reported December quarter results well above estimates, guided the March quarter to $850 million to $900 million in revenue versus the $778 million estimated, and jumped 47.9% today. SoftBank made more on that one-day move than they lost in the entire WeWork disaster. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

PagerDuty (PD – $24.21) found a 16% increase in enterprise incidents amid the race to AI adoption. Their 2024 State of Digital Operations study surveyed 350 business and technical leaders across numerous industries.

There was a 13% year-over-year increase in customer-facing incidents, reflecting rising levels of complexity and risk as businesses drive operational transformation at scale. 77% of leaders plan to expand investment in cloud services. 45% ranked security and reducing risk among their top three business imperatives, with 29% naming this the number one priority and 73% expecting to increase security budgets.

This is what PagerDuty does. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Velo3D‘s (VLD – $0.26) new CEO, Brad Kreger, gave an excellent interview on his plan to revitalize the company. He sad the company will be EBITDA (Earnings Before Interest, Taxes, Depreciation & Amortization) positive by yearend.

Regarding the $200,000 revenue recognition issue – trivial on its face, yet disastrous to the share price, he said: “Our lender…ultimately tuned back in and invested $5 million, so that they have confidence in us.”

VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Aptose Biosciences (APTO – $2.07) is the clear beneficiary of Gilead discontinuing its Phase 3 trial of magrolimab in acute myeloid leukemia (AML), following the recommendation of an independent Data Monitoring Committee which reviewed top-line data from an interim analysis for overall survival (OS). In that analysis, magrolimab in combination with azacitidine plus venetoclax demonstrated futility and an increased risk of death was observed, primarily driven by infections and respiratory failure. The FDA placed all magrolimab studies in myelodysplastic syndromes (MDS) and AML, including related expanded access programs, on full clinical hold.

In contrast, Aptos’ tuspetinib/venetoclax combination is effective with low side effects. The doublet is planned for a registrational trial in patients who have failed venetoclax starting in the December quarter. They’ll get response rates in 2025 and get accelerated approval by the end of the year or early in 2026. They’ll get full approval after the Overall Survival data in 2026, so probably in 2027. This is a $400 million market. Aptose is planning a pilot study of TUS/VEN with azacitidine in newly diagnosed AML patients, a $1 billion market.

Click for larger graphic

Click for larger graphic

Aptose is an obvious partner for Gilead. APTO is a Buy under $2.50 for a $300 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Invitae (NVTA – $0.09) crashed after The Wall Street Journal wrote: SoftBank-Backed Medical Genetics Company Invitae Prepares for Bankruptcy.

Well, maybe. They finished September with $254.6 million in cash and they do have to restructure $1.5 billion in debt. Cathie Wood didn’t wait around to find out; ARK dumped 25.4 million shares for likely around two cents. And…

Click for larger graphic

Click for larger graphic

Venture capitalists say the losers show up early and the winners only later. I’ve been trying to buy some with a tight limit – no fill yet. But I have to change my recommendation to Hold NVTA while they sort out their financial future.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Mid-2024.

ScyNexis (SCYX – $1.92) presented more preclinical efficacy data on its second generation fungerp candidate SCY-247 for the treatment of mucormycosis. In vivo data demonstrated a response rate for oral SCY-247 similar to the current standard of care, intravenous Liposomal Amphotericin B. Non-inferiority is enough to get FDA approval.

But here’s the interesting part. The combination of SCY-247 and Liposomal Amphotericin B showed significant enhancement in survival and reduction in fungal burden in lung and brain tissue compared to monotherapies. ScyNexis plans to have SCY-247 in human clinical trials before the end of 2024.

The company did a fireside chat at the Guggenheim Biotechnology Conference (WEBCAST HERE). They said GSK is managing the manufacturing process to get Brexafemme back on the market and they have a big team working on it.

The FURI, CARES and VANQUISH trial data will be announced by June 30. They get a $10 million milestone from GSK when they present the data and another $13 million when they restart the MARIO study after the manufacturing issue is resolved. Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2024

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,049.10) is making repeated attempts to break above $2,050, including today, yet there is no tailwind at all from ETF investors. That’s the definition of a high quality rally, and when it breaks higher the ETFs will pile in, driving prices much higher.

Click for larger graphic h/t @albertedwards99

Click for larger graphic h/t @albertedwards99

Gold is the all-time tease! After going below the 55 fractal, indicating a new (up)trend had begun, it quickly reversed to back above 55, indicating “Nuh-unh I’m going to consolidate for a wile, see you at 70,” only to re-reverse and close today right on the 55 line. Will she? Won’t she? Tune in next week to see what the shiny metal wants to do.

Miners & Related

First Majestic (AG – $4.65) announced positive drilling results from its 2023 exploration programs at San Dimas, Santa Elena, and Jerritt Canyon The CEO said: “The recent drilling has accomplished multiple goals from highlighting new geologically prospective areas to expanding and further defining known silver and gold mineralization. These results provide the basis for First Majestic’s year-end update of Mineral Resource and Mineral Reserve estimates expected to be released at the end of March.

“At San Dimas, we have tested previously undrilled veins like the Peggy vein and have explored extensions of known mineralization such as the Perez, Santa Teresa and Rosario veins. At Santa Elena, infill drilling of the Ermitaño vein intersected mineralization that is in many cases better than expected while follow up drilling of the new Javelin target at Jerritt Canyon has identified what appears to be a new gold mineralized zone near underground infrastructure and continues to highlight the exploration potential of the asset.”

AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $4.41) did an interesting interview at the Future Metals Forum, including comments on copper.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $45,327.37) is all the way back to the mid-$40,000 area as the flow into the new spot exchange-traded funds exceeds the outflow from the Grayscale Bitcoin Trust ETF.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

The Grayscale Bitcoin Trust ETF (GBTC- $40.68) is undergoing self-inflicted asset outflows due to their ridiculously high 1.5% management fee. Most of the outflow is going into other ETFs, so it isn’t weighing on bitcoin’s price. Here are the alternatives, ranked from lowest management fee to highest:

Click for larger graphic

Click for larger graphic

If you won’t have a big tax bill, I recommend switching from GBTC to either the VanEck, Fidelity, or iShares ETFs, or cashing out and holding your bitcoin in either a Coinbase cold wallet or a hardware wallet in your possession. I am going to switch the GBTC recommendation to the iShares Bitcoin Trust (IBIT). Buy IBIT for the 2024 and 2028 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $76.46

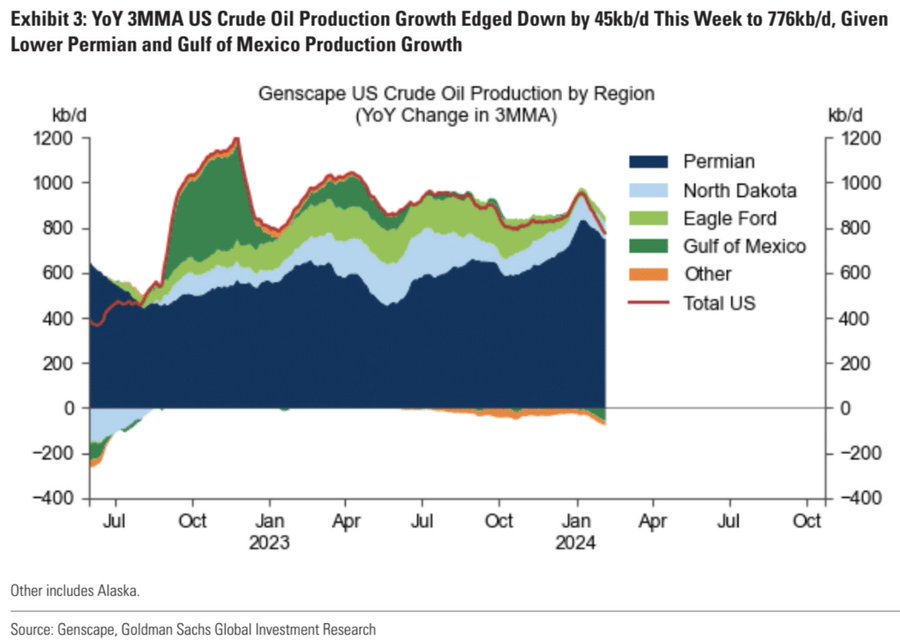

Oil is up over $4 a barrel this week. As I expected, US oil production is starting to fall.

Click for larger graphic h/t @AyeshaTariq

Click for larger graphic h/t @AyeshaTariq

Cushing stocks are at their lowest since November – and the lowest in over a decade for February.

Click for larger graphic Source: Bloomberg

Because refinery maintenance season is in full swing with refineries running at 82.4% of capacity, I expect commercial crude storage to build for the rest of February. The key to paper oil prices will be how fast refined products draw down.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

New Buy: Vermilion Energy

I expect WTI (West Texas Intermediate) oil to trade above $75 for at least the next six months or so. At that level there are several high quality midcap exploration and development oil companies trading at over 15% free cash flow (FCF) yields.

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

The most undervalued company on the left-hand side of this graphic is Vermilion Energy (VET). The stock closed today at a market cap of $1.711 billion, a Price/Earnings ratio of only 2.5x trailing 12 -month earnings, and a 41% discount to book value. It’s 34.6% below its 52-week high.

VET is a 30-year-old oil company headquartered in Calgary. They are internationally diversified. producing about two-thirds of their oil and natural gas in North America and the other one-third in Europe and Australia. Their wells and exploration activities are:

* * an 82% working interest in 796,648 net acres of developed land in Canada

* * an 85% working interest in 384,237 net acres of undeveloped land in Canada

* * 149,043 net acres of land in the Powder River basin in the US

* * a 96% working interest in 258,125 net acres of developed land and a 100% working interest in 106,993 net acres of undeveloped land in the Aquitaine and Paris Basins in France

* * a 53% working interest in 1,604,206 net acres of land in the Netherlands

* * 107,351 net developed acres and 1,549,929 net undeveloped acres in Germany

* * 975,374 net acres land in Croatia

* * 614,625 net acres land in Hungary

* * 97,907 net acres land in Slovakia

* * a 20% interests in the offshore Corrib natural gas field in Ireland

* * a 100% working interest in the Wandoo offshore oil field and related production facilities that covers 59,552 acres located on Western Australia’s northwest shelf

They’ll report December quarter results early in March. On the September quarter conference call (SLIDES HERE and TRANSCRIPT HERE) they said quarterly production was at the top end of their guidance range, generating $270 million Funds From Operations ($1.65 a share) while Free Cash Flow grew 80% from the June quarter to 88¢ a share. They returned $28 million to shareholders in the quarter through dividends and stock buybacks, and were targeting to return 30% of Free Cash Flow in 2023.

They reduced net debt to $1.2 billion at September 30 and expected to be down to $1.0 billion by the end of March, equal to their 2023 Funds From Operations. For 2024, they are forecasting $1.3 billion in Funds From Operations and $700 million in Free Cash Flow. At today’s close of $10.45, the stock is selling for only 2.44x Free Cash Flow. I want you to Buy VET under $11 for a target price of $24 or more. As always, I will not buy the stock for at least two days after this recommendation.

The July 2026 Crude Oil Futures (CLN26.NYM – $67.35) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $37.02) is a Buy under $40 for a $100+ target.

Energy Fuels (UUUU – $7.00) is beginning to reflect the uranium squeeze. Kazatomprom, the world’s largest producer, had previously announced a 2024 increase in uranium production of 11.2 million pounds, but just revised that downward to only 1.95 million pounds. They said they may not even meet the revised 2024 targets: “Concurrently, entities engaged in mining operations at newly established deposits face delays in the construction of surface facilities and infrastructure. These delays, in turn, are a consequence of the extended timelines required for the development and subsequent approval of project design documentation.”

Meanwhile, the secondary supply from dismantled nuclear bombs that was used to compensate for the annual uranium mining deficit in 2018-2023 is now depleted, while uranium demand is price inelastic! The mining deficit can only be solved by new production. Good luck with that! UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $38.12) CEO Richard Adkerson is staying as Chairman of the Board, but on June 11 he is handing over the CEO job to Kathleen Quirk. She’s been at Freeport for 35 years and the CFO since 2023.

Chinese smelters process over half the world’s copper concentrate into refined metal. China’s top industry body last week floated options to limit oversupply, from bringing forward maintenance work to postponing new plants, to even cutting production outright. Their problem is that the fees that processors charge miners have collapsed to a record low of $21.90 a ton because there’s not enough ore to go around.

Collapsing fees mean the global shortage of copper may be arriving sooner than expected. ANZ Banking Group said they see growing risks around the supply of the refined metal, and predicts prices may rise nearly 4% to $8,800 a ton by the end of this quarter.

At the Metals Investors Forum Vancouver in mid-January, Resource Maven founder Gwen Preston said 2024 isn’t the year for copper because investors aren’t positioning for global growth. Nor is supply at the point where end users are unable to source the metal. She said: “We need to run out of copper, actually like have moments where people cannot buy the copper that they need. And/or we need investors to start positioning for global growth. We need to get to a point where that’s the driving investor push and when we get to those things, ideally both or one or the other, then copper is going to I think go pretty crazy.”

I still think that moment will happen early this year.

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

International & Other Recommendations

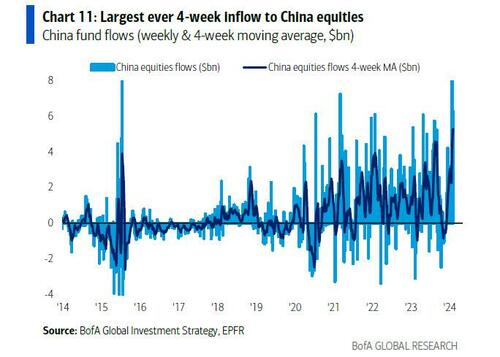

It is important to hold some non-US assets, especially in China. We’ve just seen the largest four-week inflow ever into Chinese stocks, although without much of a price impact.

Click for larger graphic h/y @Mayhem4Markets

Click for larger graphic h/y @Mayhem4Markets

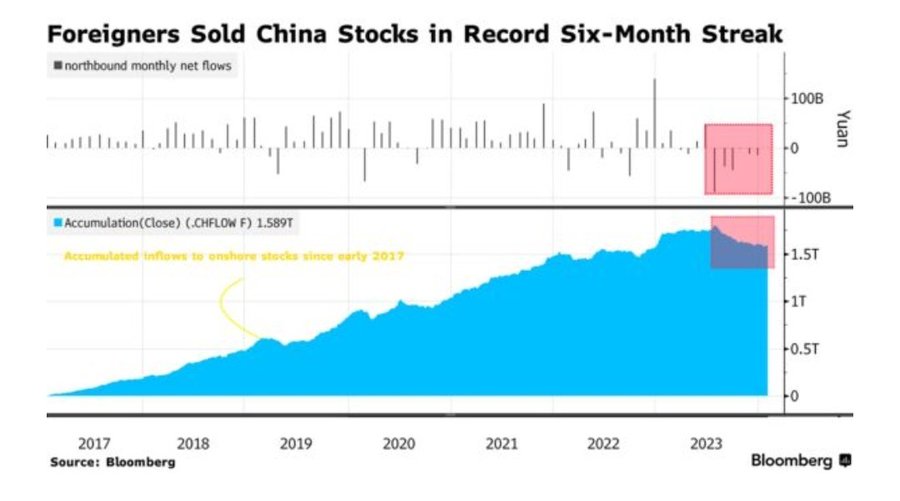

Bloomberg said foreign investors have been relentlessly selling China’s onshore equities into the new year as traders grow impatient over the lack of stronger policy support for the country’s economy and stock market. Global funds offloaded $2 billion worth of shares on a net basis in January. extending their selling to a record sixth month. That brings the total amount of stocks sold since August to $28 billion.

Click for larger graphic h/t @chigrl

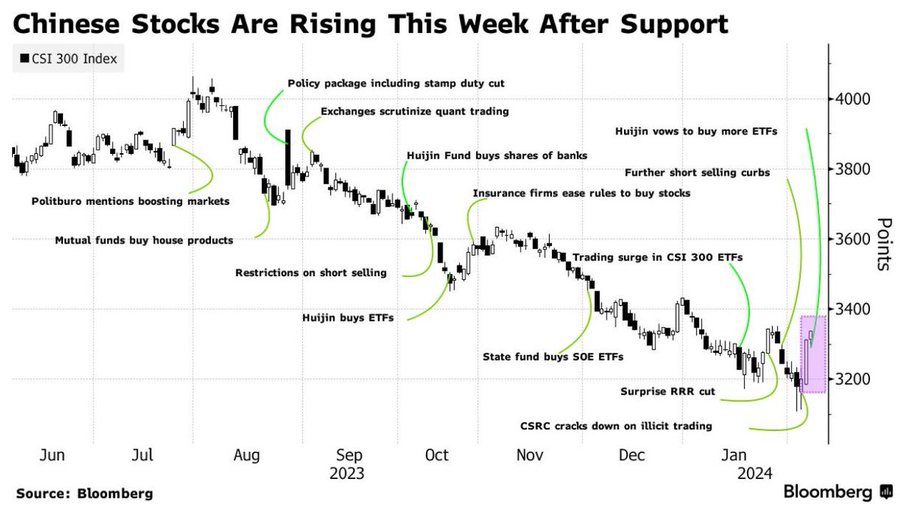

As Bloomberg pointed out, every policy action taken to stem the Chinese stock market declines over the last eight months created a pop that looked like a turn, but subsequently failed:

Click for larger graphic h/t @BobEUnlimited

Click for larger graphic h/t @BobEUnlimited

According to the South China Morning Post, they just appointed Wu Qing, who ran the Shanghai Stock Exchange from 2016 to 2017, to head the nation’s securities regulator one day after the country’s sovereign wealth fund said it would ramp up buying shares in the open market. The appointment comes after regulators planned to brief President Xi Jinping this week. All of which means Chinese stocks have bottomed just before the Chinese New Year holidays.

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.47) is a Buy under $38 for a $66 target in 12 to 18 months.

KraneShares Bosera MSCI China A Share Fund (KBA – $20.00) is a Buy under $40 for a three- to five-year hold.

Morgan Stanley China A-Share Closed-End Fund (CAF – $12.65) is a Buy under $18 for a three- to five-year hold.

KraneShares CSI China Internet Exchange-Traded Fund (KWEB – $23.96) is a Buy under $40 for a double over the next three years.

Primary Risk of all four of these: China falls into a recession.

* * * * *

La Invitación

* * * * *

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

* * * * *

Your learning about the House of Wisdom Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 2/8/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $188.32) – Buy under $150 for new iPhones

Corning (GLW – $31.73) – Buy under $33, target price $60

Gilead Sciences (GILD – $73.80) – Buy under $80, target price $120

Meta (META – $470.00) – Buy under $345, target price $400

SoftBank (SFTBY – $26.66) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $10.70) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $57.84) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $23.27 – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $24.21) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $12.52) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.30) – Buy under $13, target price $30+

Velo3D (VLD – $0.26) – Buy under $6, target price $50

$20-for-$1 Biotech

Akebia Biotherapeutics (AKBA – $1.63) – Buy under $2, target $20

Aptose Biosciences (APTO – $2.07) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $11.09) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $5.74) – Buy under $14, hold a long time

Invitae (NVTA – $0.09) – Buy under $10, first target $50, then $100+

Medicenna (MDNAF – $0.34) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.92) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $14.64) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($22.64) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $22.34) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $26.53) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.51) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $24.87) – Buy under $30, target price $50

Coeur Mining (CDE – $2.68) – Buy under $5, target price $20

First Majestic Mining (AG – $4.65) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.35) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.41) – Buy under $10, target price $25

Sprott Inc. (SII – $36.76) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $45,327.37) – Buy

iShares Bitcoin Trust (IBIT – $26.03) – Buy

Ethereum (ETH-USD – $2,425.86) – Buy

Grayscale Ethereum Trust (ETHE – $20.38) – Buy

Commodities

Vermilion Energy (VET – $10.45) – Buy under $11; $24 target

Crude Oil Futures – July 2026 (CLN26.NYM – $67.35 – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $37.02) – Buy under $40; $100+ target

EQT (EQT – $34.75) – Buy under $35; $70 first target

Energy Fuels (UUUU – $7.00) – Buy under $8; $30 target

Freeport McMoRan (FCX – $38.12) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.47) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $20.00) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.65) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $23.96) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.21) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.11) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $2.85) – Hold for buyout

Swap

Sell b>Grayscale Bitcoin Trust (GBTC – $40.68) and Buy iShares Bitcoin Trust (IBIT – $26.03)

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

NVTA….????!!!

Wow! Michael you recommended NVTA forever being the amazon of its field , so what happen. I lost a good amount of money.

Your not the only one,so much for knowledge and experience,nvta

MM–your general economic/market analysis is excellent, but WHY do you persist in calling for completely unrealistic buy/target prices such as VLD? VLD is rallying now, but today’s investor should buy way under $1, more like 50 cents at the most. The investor in 2030 might buy under $6, your buy price. It is a lottery ticket to get there, but today’s prudent speculator could do well from current prices to realistic target of $1 or more.

JGMD,

I totally agree with you on this. My next question is how long do they have in order to get over $1 before they would have to do a Reverse Split?

Even if business doesn’t pick up and the stock is still below $1, VLD has about 6 months (I believe) before either delisting or doing reverse split. It is weird that VLD is on the NYSE instead of Nasdaq–different time frames for over $1 requirement. There have been long discussions on YMB about this. Personally, I don’t regard reverse split for VLD as a negative. Delisting would be a disaster because it would handicap their ability to raise capital if needed–YMB poster Columbo had good insights about this. The R/S would allow more sources of capital, because an investor group could take VLD shares (over $1) in the deal, whereas the investors would not be allowed to take shares under $1 if VLD got delisted. The negatives of R/S amount to letting management become lazy if there is no pressure to get the stock above $1. But this new CEO Kreger seems motivated to restore business and will do what shareholders want–long term recovery.

MM – With regard to Corning (GLW), what annual sales revenue will be required to achieve your 2025 $60/share price target? How does that number compare with management’s most recent revenue growth guidance?

Management says they can add $3 billion in revenues without any increase in G&A or capital spending. They did $12.6 billion in 2023 and should do about $13.5 billion this year and $14.5 billion in 2025. Because the revenue growth will come with high incremental net profit margins, that should be enough to get the stock to $60 in 2025.

NVTA- Takeaways:

Changes this week: Removed NVTA from Long-Term as they deal with their finances.

Mike just won’t admit defeat. Ever.

Late Dec 2023, I reviewed stocks I have owned for a long time to see how they behaved in past years from tax loss time to Jan-Feb. Buying low during tax loss is a good strategy if the company is reasonably sound, so they bounce a few months later. For dying companies like NVTA, you’re right that tax loss buying doesn’t work. But for other companies that are turning around, it may take a lot longer than Jan to bounce. If the current anti-business administration is replaced by a pro-business one, and interest rates are lowered later in 2024, small caps will do well later as well. VLD had a 30% bounce yesterday and a good one today. I am looking for a retest of the bottom at 20 cents to get my final load. But if the bounce is sustained, I may have to settle for a higher buy price. It will still be only 3% of my total portfolio.

This “anti-business” administration has led to record highs for the S&P and the Nasdaq. I had my best year ever in 2023. You can’t blame the president for crappy MM picks.

As stubborn as MM is about adjusting his buy/target prices, you are equally stubborn in not admitting inferiority of socialist policies vs free market capitalism in general economic well-being, which in the long run translates into better market performance. Record highs now are mainly due to money printing, which socialists advocate especially.

Ok so maybe you can differentiate Trump’s economic policies from Biden’s. Perhaps you can explain the 8 trillion printed under the Trump administration.

Wake up. Both parties are controlled by corporations. This fantasy you have about free market vs socialism simply doesn’t exist in corporate driven America.

But you missed my point. Nothing will save companies like NVTA and VLD. It has nothing to do with policies, they are simply horrible picks.

You get all your claims from MSM, a Biden apologist. Who could possibly approve of the current border fiasco? Oh, you conveniently relocated to Canada. You would just love the terrorist/drug dealing migrants coming to invade your home.

I don’t think you have much common sense understanding. When dealing with individuals, is it better to reason and negotiate with them, or to be forced to accept inflexible rules and regulations? It is impossible to deal with the latter situation, so business is much less likely to take place. Or if you feel the rule/regulator guy puts you in a desperate situation, you won’t continue doing business with him. If you understand this, and you still think that the party of regulation and oppression from big govt is your friend, you have a mental problem.

Stock picks, whether good or bad, will do better in a free market. Unless the business model is stealing and shafting the consumer. Both NVTA and VLD are good for the consumer. VLD has a reasonable chance of making it.

Saddest part for nvta,they couldn’t even wait for the fuc..ng earnings to come out first,before announcing this,way to go Ken knight you got your money

Maybe Amazon sent Ken over to nvta for a reason

From a Potential Amazon of its field to 2 cents !

They have not announced anything.

I started the year quite bearish. Years ending in 4 are always problematic and come with a large dose of volatility. I have been very focused on the geopolitical situation which is possibly the worst and most dangerous since the days of the VietNam war.

Mr. Market, however, not only is ignoring the heightened risk of nukes flying, it is seemingly feeding off it, by making new high after new high in the SPX. Some of it may be Middle East and Euro capital fleeing the regional wars and getting reinvested in the US, still, I decided not argue with success. So, I reduced the pharma and gold positions and switched to the Gold Heir Apparent, BTC, and stuff like DIS, PLTR and U. Still have some TGTX though it is not trading well. ENVX seems ok.

Check out ARM, CYBR, ENPH, AXON as well. ARM did have a ridiculous run up yesterday so maybe not great right now.

PLTR is perhaps the best AI play out there.

PLTR- Guy at Wedbush has a $30 target; above that the technicals indicate $55.-

It could go completely crazy and land much higher still in tune with the insane mkt.

Buy more TGTX at $10-12 which represent very conservative and pessimistic outlooks for peak sales. The momentum players had overoptimistic outlooks recently at $23. For once, I agree with MM’s buy up to $12, with target of over $30. If Briumvi gets much higher market share among CD20 drugs, $100 or more is possible.

Investors in TGTX should have declared victory and sold when the stock jumped up to $35ish in mid 2023 and then put that money to work elsewhere. Instead those that didn’t sell have seen a 50% reduction with who knows how long before it returns to the 30s. One wonders just how much additional return were they expecting to get from $30+?

Totally agree. I was caught up in the FOMO momentum. I have held on since my average cost is $6. My best move was buying on Oct 31 at $7.25 when there was fear that the shorts would crash it to $5.

Bought NVTA under two cents

How many stocks have you had success with buying under 2 cents? Mike, this stock is dead. Why can’t you admit it?

Never bought a stock under two cents before. Maybe over $200 million in cash is dead, but it gives them a lot of wiggle room to restructure the debt.

A gamble worth taking in my opinion.

Nvitae files for Chapter 11 bankruptcy to address huge debt load

https://seekingalpha.com/news/4066528-invitae-files-for-chapter-11-bankruptcy

Invitae gets court approval for five-month bankruptcy sale

https://www.reuters.com/business/healthcare-pharmaceuticals/invitae-gets-court-approval-five-month-bankruptcy-sale-2024-02-15/

MM – I guess I missed your explanation, do we not have access to your bio moonshot recommendstions? Specifically this one: – a biotech company down 95% from its high, selling for less than 2x cash, with major Big Pharma partners and an update coming in less than two weeks. It’s right under the paywall.

In NWI this Thursday. AbCellera Biotherapeutics (ABCL). Reports December results Feb 20.

MM have you researched PTN, only $64 MC with multiple drugs in the pipeline and several reporting’s this year (see chart attached)

I looked at it a while ago. It seemed to have too many drug programs and they have to perpetually raise money, so I stopped. I see they just raised $10 million vs. a $6-$7 million quarterly burn rate, report this Thursday, and have some top-line results later this month.

Our old nemesis Feuerstein is pushing PTN for the eye trial.

I have bitcoin at Robinhood, should I put it in one of those wallets? How do you do that? Thanks

https://robinhood.com/us/en/support/articles/robinhood-wallet/

Ask them if this is a cold wallet, which means not connected to the Internet. Hot wallets can be hacked.

Thanks

https://www.amazon.com/Ledger-Nano-Plus-Pastel-Green/dp/B0C9M7QHNL/ref=asc_df_B0C9M7QHNL/?tag=hyprod-20&linkCode=df0&hvadid=666640267346&hvpos=&hvnetw=g&hvrand=6955107604468426872&hvpone=&hvptwo=&hvqmt=&hvdev=c&hvdvcmdl=&hvlocint=&hvlocphy=1020991&hvtargid=pla-2187047705950&mcid=56f3a3c735e23b6fb34993259f89ee85&th=1

It takes a bit of time to set up but virtually unhackable.

The problem with Coinbase and Robinhood is those companies own your keys. Not you.

“The Robinhood Wallet app is a self-custody wallet that’s your portal to web3 where you can store and manage your crypto on the Ethereum, Bitcoin, Dogecoin, Arbitrum, Polygon, Optimism, and Base networks. Robinhood Wallet gives you full control over your crypto, which means you hold the private keys to your assets.”

https://robinhood.com/us/en/support/articles/robinhood-wallet/

Could be misleading, IDK.

I believe that the wallet app is indeed a self custody wallet. Remember and store your seed words safely somewhere as that is your only access/ability to restore. You lose that and it’s gone.

Thanks

MM – Given recently announced mergers in the natural gas space (Chesapeake/Southwestern and Diamondback/Endeavor), do you still consider EQT to be the best investment option in that sector? As applicable, why or why not?

[Note: Opinions from other subscribers are also welcome.]

SCYX

MM, typically when might we expect the manufacturing problem to be rectified? Any day, by end of March, 3 more months? What would be your best estimation?

MM recently said end of June, or 9 months after the shutdown. YMB guys say GSK is in charge of the manufacturing problem. Wait before buying more. The upcoming results of VVC trials, probably positive, won’t matter much, since GSK gets most of the revenue, I believe. The real catalyst will be the MARIO trial for serious C. auris infections, to start once the manufacturing problem is resolved.

Thank you JGMD, glad for your DD. Have a full truckload now. Finally a NWI stock that will do well with the backing of GSK. One thing I have learned with following MM, when securities become pennies it’s time to exit, while MM clings to his original premise for buying and maintains ludicrous forecasts. I exited NVTA and ARTH long ago. MM will never admit defeat, “SELL” is not in his vocabulary.

I like several NWI companies, but they have to be bought at realistic prices, which must be updated to reflect current status. Buy mainly on pessimism. Sometimes the pessimism will reflect bankruptcy, but buying at those prices will greatly reduce the odds of nearly total loss. NWI stocks that rise from the ashes of pessimism will be HUGE 10-100x winners.

MM–take note for the benefit of yourself and subscribers.

What’s your average cost on the SCYX truckload? Mine was about $12, which I reduced to $4.70 after buying more a few months ago at $1.70. I’m looking to buy more at $1.50 or so.

Cost is$1.90 per share.initially on a few thousand much higher

U

Anyone have SMCI? Went over $1000 today. My small position helped offset my losses in NVTA.

New World Investor for 2.15.24 is posted. New Buy: ABCL