Dear New World Investor:

As expected, yesterday the Federal Reserve raised the Fed funds rate by half a percentage point (50 basis points or bps), bringing the benchmark interest rate to a range of 4.25% to 4.50%, the highest level since 2007, while making it clear more rate hikes are coming in 2023. I can’t imagine anyone was surprised, although the sell-off yesterday afternoon and today indicates someone was.

Chairman Powell said: “Over the course of the year, we have taken forceful actions to tighten the stance of monetary policy. We have covered a lot of ground, and the full effects of our rapid tightening so far are yet to be felt. Even so, we have more work to do. The Committee anticipates that ongoing increases in the target range will be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2% over time.”

Powell added that we are “getting close to a sufficiently restrictive rates level.”

New economic forecasts show they now see benchmark interest rates peaking at 5.1% in 2023, 50 basis points higher than the September projection of 4.6%. They then see rates coming down to 4.1% in 2024, slightly higher than previously projected. The bond market keeps laughing at the Fed’s forecasts and sees a 4.4% yearend rate in 2023, 0.7% below the Fed.

The Fed cut their 2023 real GDP growth estimate from 1.2% to 0.5%, picking up slightly to 1.6% in 2024. They don’t see core inflation coming back down close to their target until 2024, with inflation rounding this year at 4.8%, then 3.5% in 2023, and 2.5% in 2024. That is where they are most wrong – I expect core inflation, which will exclude soaring oil prices but finally include falling rents, to fall much faster than that.

Click for larger graphic

Click for larger graphic

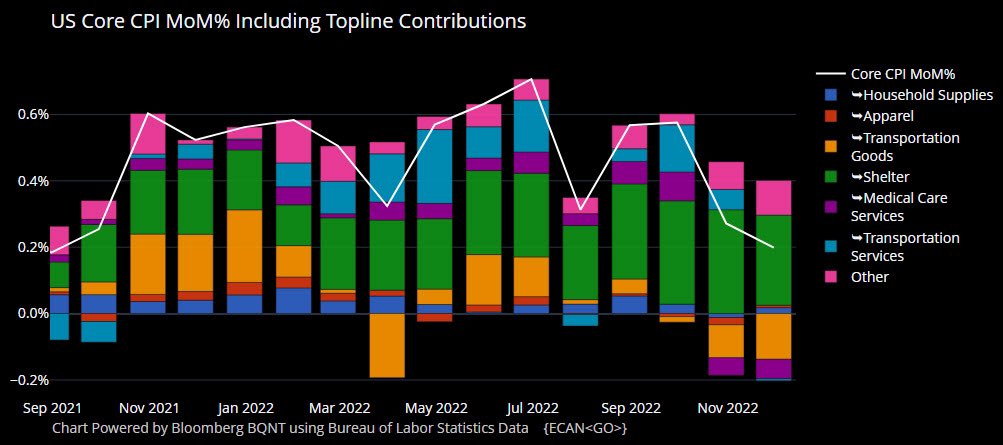

The disinflation cycle continues apace. Consumer prices rose less than expected in November, the second-straight month inflation pressures moderated more than anticipated by economists.

Click for larger graphic

Click for larger graphic

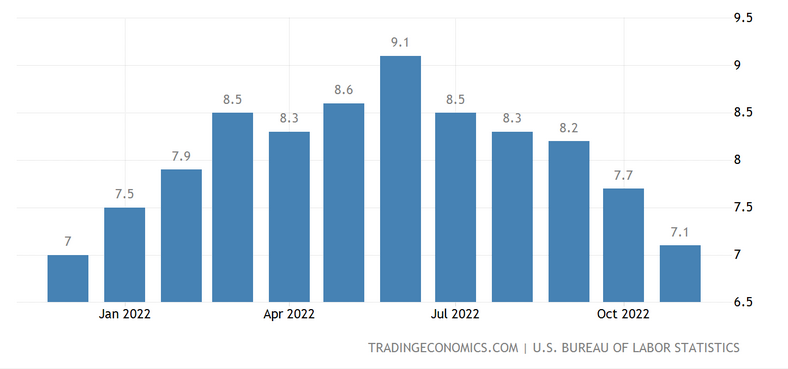

The Consumer Price Index (CPI) for November showed a 7.1% increase in prices over last year and a 0.1% increase over October. Economists had expected prices to rise at a 7.3% clip over last year and 0.3% month-over-month. It was the biggest drop in the year-over-year headline CPI (0.64%) since April 2020.

Core inflation, which strips out the volatile food and energy components of the report, climbed 6.0% year-over-year and 0.2% over the prior month. Consensus estimates called for a 6.1% annual increase and 0.3% monthly. The report showed a fairly broad-based slowdown, and core CPI ex-shelter was -0.13%. November shelter prices were up 7.1% year-over-year and accounted for about half of the total increase in core CPI. The housing CPI is calculated with about a nine-month lag and will keep upward pressure on inflation before reversing hard.

Click for larger graphic

Click for larger graphic

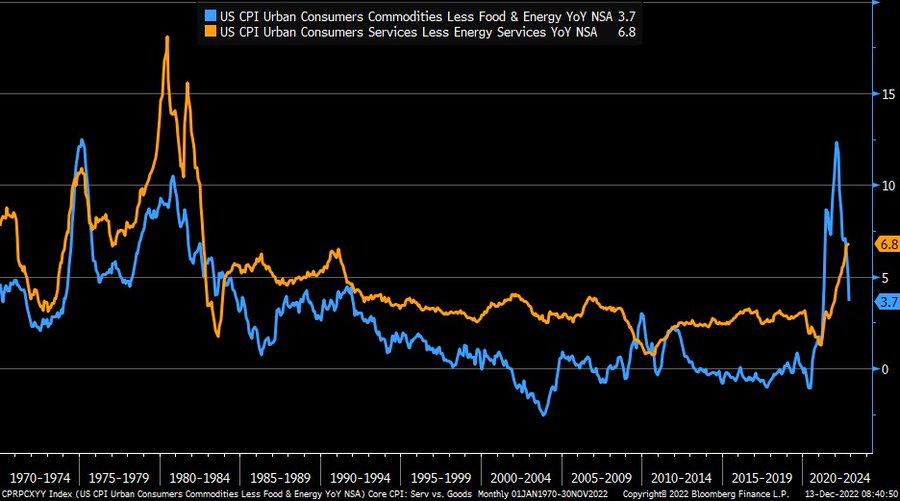

Core goods (blue line, labeled “commodities”) are in meaningful disinflation, while core services (orange line) are perhaps finally peaking:

Click for larger graphic

Click for larger graphic

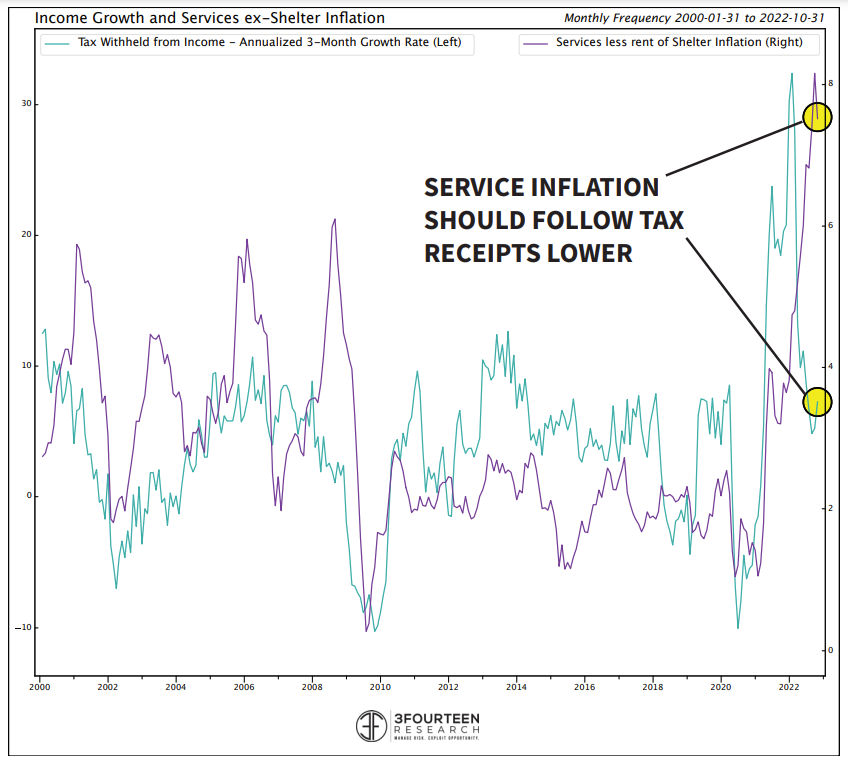

Powell said: “We see goods prices coming down. We understand what will happen with housing services” via lower inflation rates that lag. “But the big story will really be the rest of it [core inflation ex-goods+shelter], and there’s not much progress there.”

CPI Services ex-shelter is now flat for two straight months. This is the key slice of the CPI data and where a “wage-price spiral” would show up. The divergence between real-time tax receipt data and services points to continued disinflation.

Click for larger graphic

Click for larger graphic

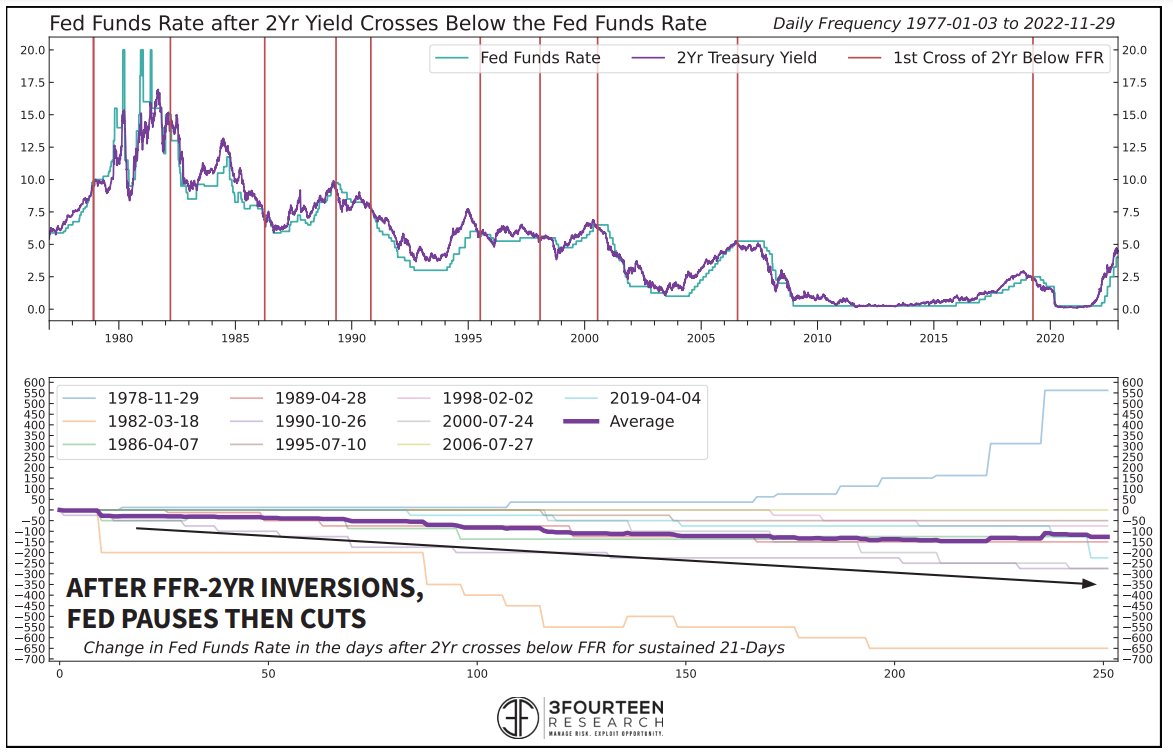

Remember that the Fed has never hiked their Fed funds rate past the level of 2-year Treasury yields. The 50 bps hike in December basically got us there. Any additional hike in 2023 will push us into uncharted territory. Historically, after the Fed funds minus 2-year inverts, the Fed is done tightening.

Click for larger graphic

Click for larger graphic

“The inflation data received so far for October and November show a welcome reduction in the monthly pace of price increases,” Powell said. “But it will take substantially more evidence to give confidence that inflation is on a sustained downward path.”

The Fed is upset that employment rates remain high, as they want to crush demand. But this is a badly flawed model. If you look in depth at employment rates in the Household Survey, more people are having to work two or more part-time jobs, yet labor force participation rates keep declining. These “models” need an overhaul

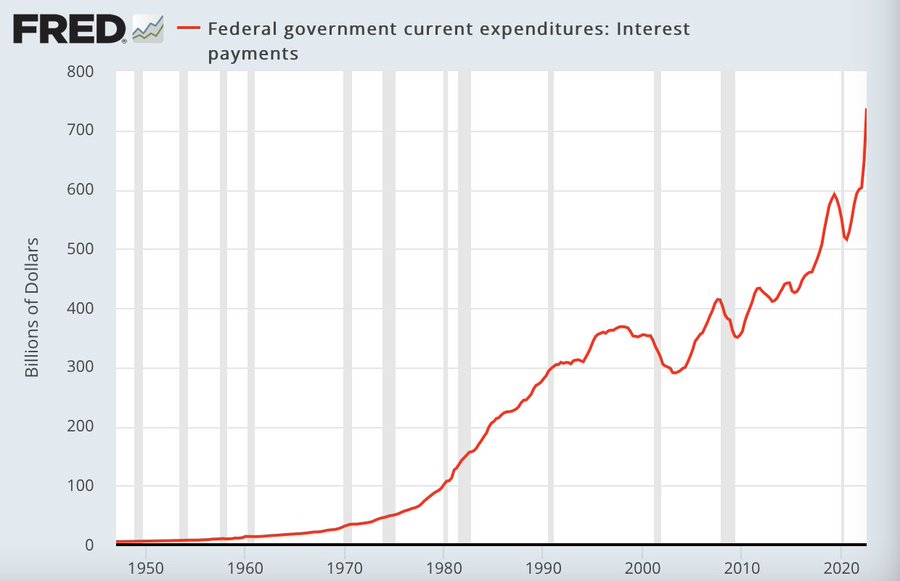

It won’t matter what the Fed thinks it’s going to do with its own rates, it’s when reality hits home hard enough they will realize what they thought they were going to do was based on lagging data. Not even the short end of the interest rate curve is buying this hawkish nonsense Powell’s trying to sell. And he’s making the budget deficit worse:

Click for larger graphic

Click for larger graphic

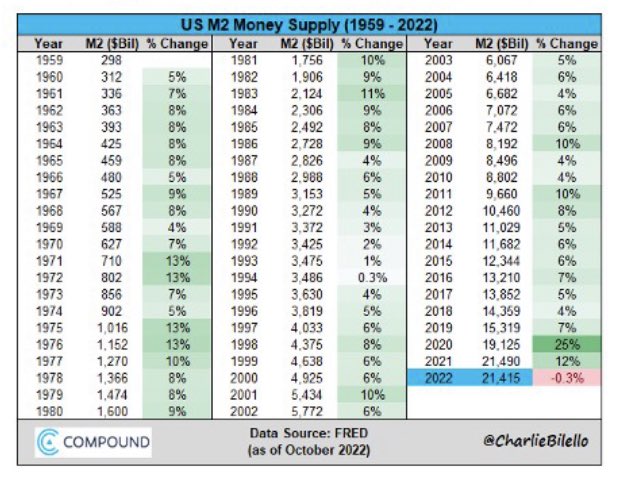

Our fiat/credit-based system encourages the process of money creation. Since the ’60s, there has never been a single year where M2 dropped. 2022 is on track to be the very first year with negative year-over-year M2 growth in over 60 years. M2 has grown every year. Now it’s shrinking. Watch out below — defaults are coming.

Click for larger graphic

Click for larger graphic

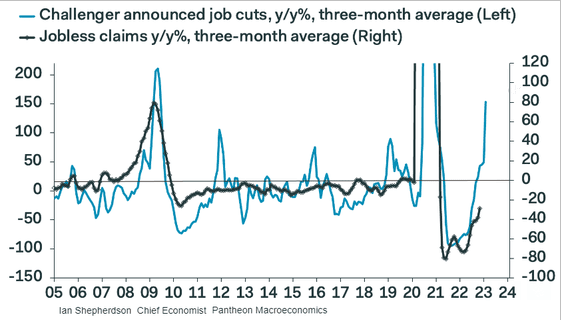

Elevated layoffs point to higher jobless claims ahead.

Click for larger graphic

Click for larger graphic

Market Outlook

Tomorrow is another quadruple witching event. For S&P 500 linked options, this will be the largest notional expiration in the past 10 years, with over $3.7 trillion set to roll over or expire.

Due entirely to today’s drop, the S&P 500 lost 1.7% since last Thursday. The Index is down 18.3% year-to-date. The Nasdaq Composite lost 2.4%, also due entirely to today’s drop. It is down 30.9% for the year. The small-cap Russell 2000 also dropped 2.4% and is down 21.0% in 2022.

The fractal dimension is even more consolidated after the volatile action this week. The next trend is going to be a sight to see.

This 60-year chart of the S&P shows that markets find support at one of three different levels when measured in 52-week increments: 0% (red circles); -20% (blue circles, the biggest 52-week drawdowns seen in secular bulls); and -45% (we’ve hit this twice in 60 years, both at secular bottoms).

Click for larger graphic

Click for larger graphic

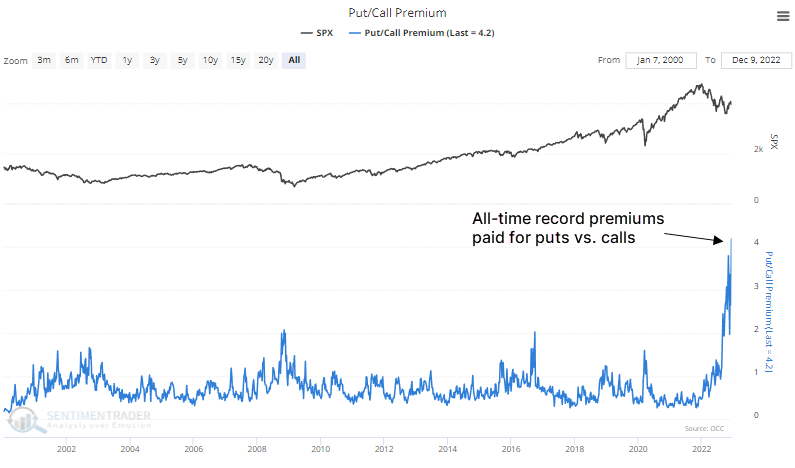

Traders have never spent so much on expectations for a crash. Last week, all traders across all US exchanges bought to open $4.20 in put options for every $1 in call options. That’s double what they spent during all the other panics over the past 22 years.

Click for larger graphic

Click for larger graphic

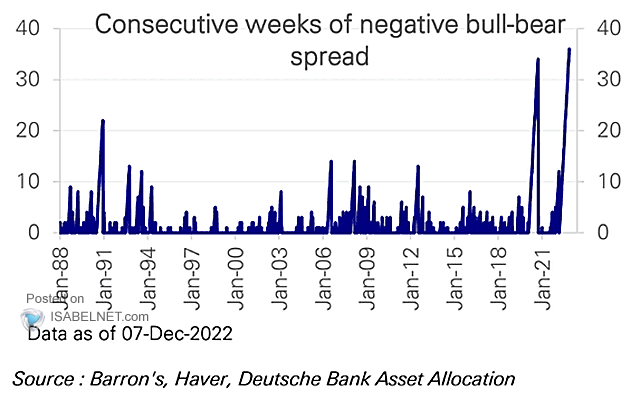

And we are at a record-long period of negative sentiment:

Click for larger graphic

Click for larger graphic

As a contrarian, you know what to do!

Top 5

Changes this week: None

Near-Term – chronological order

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

INO Inovio – VGX-3100 HPV Phase 3 results by yearend

TGTX TG Therapeutics – FDA approval on December 28

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphite Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

This morning the Atlanta Fed’s December quarter real GDP growth forecast dropped from +3.2% to +2.8% due to declines in the estimates of personal consumption expenditures growth, private domestic investment growth, and government spending growth. The Blue Chip economists are up to +1.1%.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Wednesday, December 21

Winter Solstice – 4:48pm

Thursday, December 22

September quarter real GDP – 8:30am – Third estimate

Friday, December 23

Personal Consumption Expenditures Index – 8:30am

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations are typically very low. At the same time, Initial Public Offering valuations had moved very high. We were seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors make 5x to 10x in a reasonable, three- to four-year period if they buy at those valuations. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Aptose Biosciences (APTO – $0.58) did their update call from the American Society of Hematology annual meeting (AUDIO HERE and SLIDES HERE). They said tuspetinib (formerly HM43239) safely delivered complete remissions as a monotherapy across four dose levels (40 milligrams, 80 milligrams, 120 milligrams, and 160 milligrams) in 60 very ill and heavily pre-treated relapsed or refractory acute myeloid leukemia (AML) patients that previously had been failed by chemotherapy, Bcl-2 inhibitors, hypomethylating agents, competitor FLT3 inhibitors, and hematopoietic stem cell transplants. They think that due to its safety and potency profile it can become the preferred kinase inhibitor for triplet combination, maintenance therapy, and patients failed by prior FLT3 inhibitors and become a billion-dollar drug. That’s a blockbuster.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

They are planning a global dose expansion trial to support a Phase 2 registrational trial (no Phase 3 needed!) for accelerated approval and then additional drug combination trials for broad commercialization.

Luxeptinib had another complete response in a diffuse large B-cell lymphoma patient and the new formulation shows an 18x improvement in bioavailability. They recently dosed the first patient and think that 9 to 15 patients will determine if G3 is safe and achieves desired exposures to deliver clinical responses.

Click for larger graphic

Click for larger graphic

After the ASH meeting, Aptose announced an up-to-$50 million At-The-Market facility with JonesTrading Institutional Services. It hit the stock 10%, probably because investors confused it with an imminent offering. It isn’t. APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 1a

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $136.50) announced Freeform, an all-new app that helps users organize and visually lay out content on a flexible canvas, giving them the ability to see, share, and collaborate all in one place without worrying about layouts or page sizes.

Click for larger graphic

Click for larger graphic

Users can add a wide range of files and preview them inline without ever leaving the board and collaborate with others while on a FaceTime call. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Other Tech

QuickLogic (QUIK – $5.03) presented at the Oppenheimer 5G Summit (ZOOM HERE). Most of it was the CFO giving the usual backgrounder:

Click for larger graphic

Click for larger graphic

They expect to be pro forma profitable in 2023.

Click for larger graphic

Click for larger graphic

In the fireside chat part of the presentation, the CFO said their five-year outlook is that they will have $100 million in revenues. Their multi-year pipeline already is $115 million, with many very large deals likely to close in 2023 and add to the pipeline. QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets and wearables.

Primary Risk: New sensor hub competitor emerges.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $4.03) will launch three satellites for Hawkeye tomorrow, inaugurating their Virginia launch complex.

CNBC’S Investing in Space newsletter briefly covered RKLB and its four public competitors. It’s clear that SpaceX and Rocket Lab are the leaders. As CEO Peter Beck said: “Launch is the keys to space…but once you have the keys to space, then you need to drive the car. The big space companies of the future are not just a launch company on its own or a spacecraft manufacturer on its own. It’s a combined entity where you provide an end-to-end service.”

RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Velo3D (VLD – $1.68) hired a very experienced Executive Vice President of Operations to manage production growth, quality standards, and cost reduction. I’m encouraged to see them building the company beyond their technology leadership. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,786.70) jumped Tuesday to a five-month high after the inflation report as the dollar hit a six-month low, but then gave it back to close unchanged from last Thursday. Like the S&P 500, the fractal dimension shows extreme consolidation.

Miners & Related

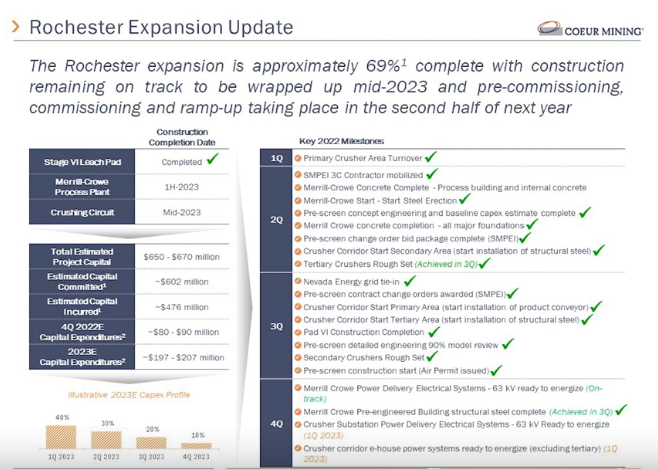

Coeur Mining (CDE – $3.17) held their Investor Day this morning (Highly recommended two-hour ZOOM HERE). They are banking on the mid-2023 start-up of the Rochester Mine to provide the next major step up in production, revenues, and earnings.

Click for larger graphic

Click for larger graphic

Rochester will give Coeur a well-balanced North American mine portfolio and put them in the top rank of silver miners.

Click for larger graphic

Click for larger graphic

The payoff: Over the next three years, they expect to increase gold production by 15% and silver production by a whopping 51%:

Click for larger graphic

Click for larger graphic

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $17,411.75) has stabilized above $17,000 in spite of – or maybe because of? – the ongoing volatility in crypto. I still think the fear over Grayscale Bitcoin Trust‘s (GBTC- $8.30) bitcoin holdings is naive, so GBTC is a gift at 47.8% under net asset value.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE all are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $76.29

Oil has digested a Russian inventory dump, insane Chinese lockdowns, the refinery shoulder season, and the tail end of the Strategic Petroleum Reserve purge, including last week’s 4.7 million barrel drain – the largest weekly release since early October. The SPR now has just 382.3 million barrels, the lowest since January 1984. All of these will reverse soon, and meanwhile OPEC+ is going to force President Biden to drain even faster in the March quarter because they want $80 to $100 oil.

China has swung from “Someone in Shanghai sneezed, so lock the whole city down” to China’s top medical adviser saying omicron’s risk is the same as the flu, a death rate of 0.1%. This follows the new government line on the coronavirus, which apparently got much less dangerous just because people were rioting in the streets. China’s reopening is going to be a gas guzzler. Standard & Poor sees it sucking up 3.3 million barrels of oil a day and wrote: “If the energy crunch was bad this year, China’s recent loosening of COVID-19 protocols could spell a disastrous global crisis in 2023.”

Meanwhile, Bloomberg said the oil giants are poised to halve their international spending growth in 2023 in response to lower crude prices, dealing another blow to a global market already facing a slowdown in production from US shale fields.

2023 budgets are getting set this month. Boards of Directors are not going to approve spending increases with the cash market in the low $70s and anti-fossil fuel sentiment in the Department of Energy. Production isn’t going to increase much in shale, with the backlog of Drilled but Uncompleted wells all but gone, materials and labor shortages widespread, and anti-fossil fuel lenders cutting bank lines. Russian production is rolling off. Meanwhile, stopping the SPR releases takes 1.5 million barrels a day out of supply while the China rebound adds 3.3 million barrels a day to demand. That’s a 4.8 million barrels a day deficit. Plus India and MENA (Middle East, North Africa) are ramping demand at double digits. Where will the supply growth in 2023 come from?

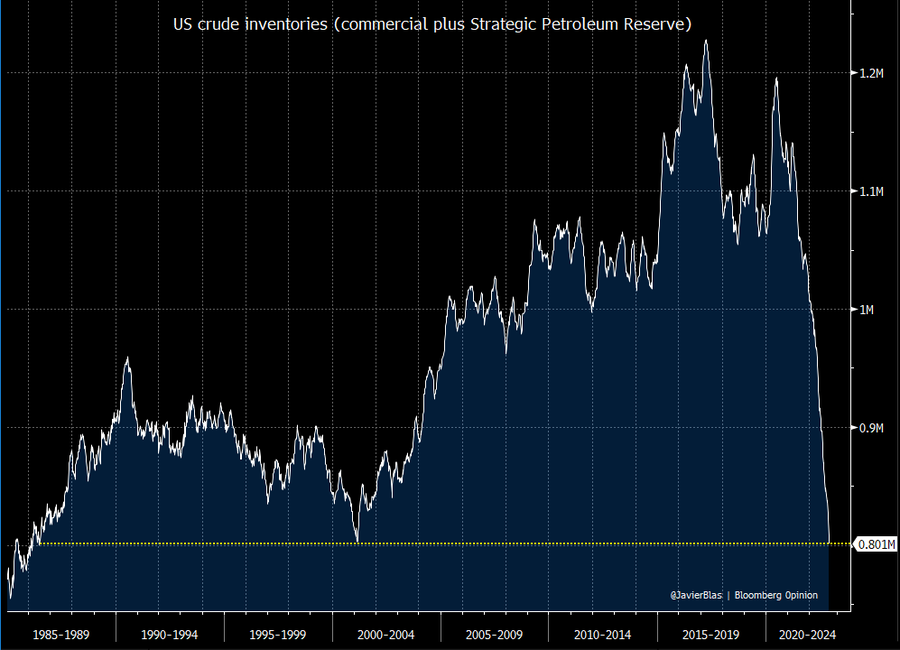

US total crude oil inventories, both commercial and the Strategic Petroleum Reserve, have fallen to a 36-year low, dropping below the previous bottom set in 2001. This is a problem.

Click for larger graphic

Click for larger graphic

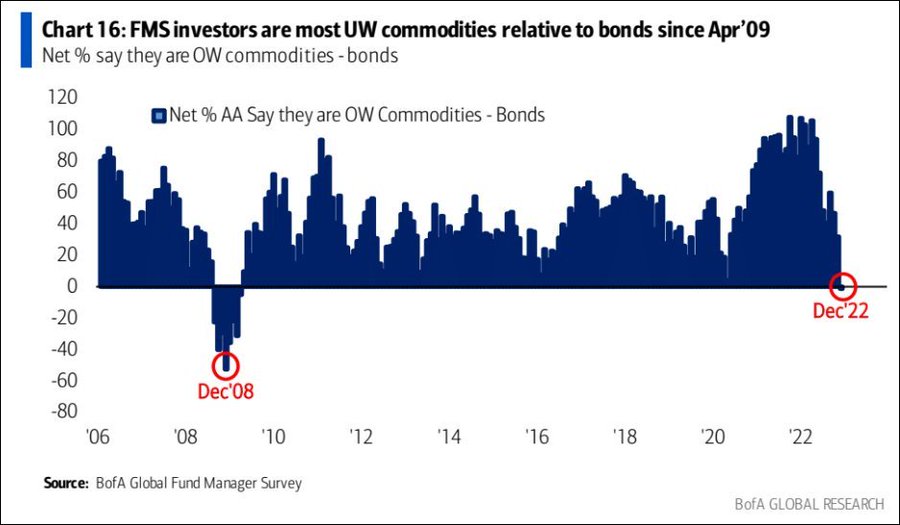

Yet the most recent BofA Fund Manager Survey showed professional investors are the most underweight commodities relative to bonds since April 2009.

Click for larger graphic

Click for larger graphic

At the same time, the ratio of money manager long to short positions in Brent oil is below where we ended the oil sell-off back in 2018 around 2.15. Levels approaching this area have always produced a rebound in the following weeks and months. I think this time will be no different.

Click for larger graphic

And traders that pursue trend-following strategies are shorting WTI crude oil futures to an extent they haven’t in more than two years.

Click for larger graphic

Click for larger graphic

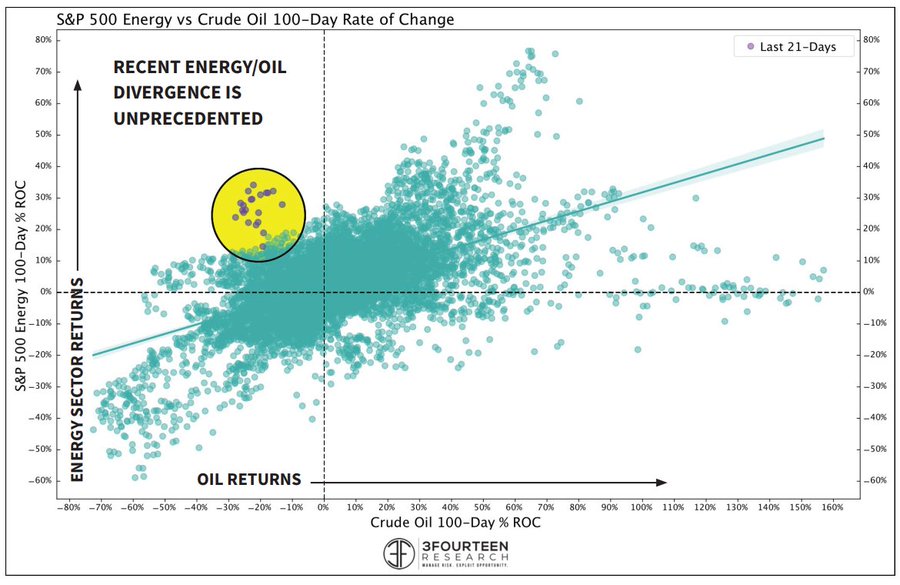

We’re also seeing an unprecedented divergence between oil and energy stocks. Over the past 100 trading sessions, the Energy Sector has surged, while oil has collapsed. Historically, the slow drip from equities will continue for a bit, but the larger divergence is resolved through an oil rally.

Click for larger graphic

Click for larger graphic

There’s going be a four to six million barrels a day deficit by the second half of 2023. I think oil prices are going to slingshot something fierce. Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.67) is a Buy under $36 for an $80+ target.

* * * * *

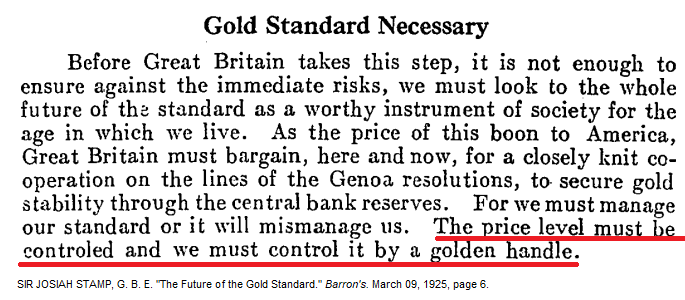

1925: A gold standard proponent argues his case. It turns out, a gold “standard” is simply a form of price control.

Click for larger graphic

Click for larger graphic

* * * * *

Happy 97th Birthday Dick Van Dyke (12/13/1925)

Click for larger graphic

* * * * *

Your trying to work on important problems Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.58) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $0.80) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $9.75) – Buy under $20, hold a long time for a 10x return

Graphite Bio (GRPH – $3.03) – Buy under $9, hold a long time

Inovio (INO – $1.76) – Buy under $7, hold a long time

Invitae (NVTA – $2.09) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.51) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.95) – Buy under $3, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $8.62) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $136.50) – Buy under $150 for new iPhones

Corning (GLW – $32.79) – Buy under $33, target price $60

Gilead Sciences (GILD – $86.58) – Buy under $70, target price $100

Meta (META – $116.15) – Buy under $250, target price $400

SoftBank (SFTBY – $22.23) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $39.53) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $8.90) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $26.44) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $5.03) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.03) – Buy under $13, target price $30+

Velo3D (VLD – $1.68) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Buy while fixed mortgage rates are low

Bag of Junk Silver – ($23.27) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $23.95) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $27.99) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.38) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $27.60) – Buy under $30, target price $50

Coeur Mining (CDE – $3.17) – Buy under $5, target price $20

First Majestic Mining (AG – $8.48) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.37) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.02) – Buy under $10, target price $25

Sprott Inc. (SII – $32.32) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $17,411.75) – Buy

Grayscale Bitcoin Trust (GBTC – $8.30) – Buy

Ethereum (ETH-USD – $1,266.52) – Buy

Grayscale Ethereum Trust (ETHE – $5.79) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.77) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $25.78) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $14.14) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $29.95) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $1.12) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.10) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.67) – Buy under $36; $80+ target

Energy Fuels (UUUU – $5.77) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $1.86) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.45) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.04) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1st in a long time !

#1

A poor third

What a surprise, the market sold off again today?? NOT. Big companies are laying off in response to Powell’s jabs at trying to fix the FED’s economic nightmare. Over sixty present of the US population were living paycheck to paycheck before those layoff’s . Meaning the idiots were spending more than they were making with the help of plastic money from Visa and MC and others. So they have NO savings in an emergency rainy day fund to fall back on now that they are getting laid off. And if they were living paycheck to paycheck before the layoff how in hell are they going to survive on a skimpy unemployment check? Hello Visa, more debt is coming. But , look at the bright side they will still be spending and the consumer spending numbers will still be looking good !! Energy in Europe has become so expensive that the government is subsidizing the people with energy assistance. Walmart is closing stores because people are stealing so much merchandise that it isn’t viable to keep them open. The FED needs to take a closer look at blue collar America instead of focusing all of his energy on the PPI and CPI numbers. Just say’in.

Amen brother!

AMEN again. Excessive world govt debt. Excessive private debt limits govt ability to tax (steal) private entities. All this leads to hyperinflation, debt defaults. Lenders won’t lend if they get stiffed by debt defaults. Higher interest rates are inevitable. $31 trillion (probably more) of govt debt will be defaulted on and hyper inflated away. The book, Bankruptcy 1995 will be proven correct in time.

Shorted the DOW via SDOW Wednesday. The DOW has held up fairly well compared to the NAZ, that should change soon. 2023 won’t be a good year.

Also a gentle reminder to get rid of GBTC as soon as possible. This thing is way to detached from the BTC spot and is nosediving.

Actually might be wise to unload any of the picks that have killed you this year. My 2 worst picks were APPH (mine) and CWBR (MM’s) .. well technically they were both my picks but I cleaned out that trash today.

too detached.

Michael – what do you recommend for 2023?

All – what are everyone’s top 2-3 picks for 2023? Please don’t be shy, all responses are appreciated, as MM says there are some intelligent people on this board, lets help each other out and see if we find a consensus. I’ll start, I believe (hope) Bitcoin, Ether and SKYE (an early stage biotech using cannabis to cure glaucoma).

I know that’s more than 2-3, 2023 should be very challenging as interest rates manifest into a recession and job losses. Eventually the FED will pivot but timing that is impossible. I’m currently about 75% cash.

Michael I agree with most of your thoughts but Elon is a turd and Tesla is Elon. I agree it can trade up at times but the good old days are over now. Tesla, like many companies, and their ceo have never operated in an increasing rate environment or in a real recession as a public company. Anything worked in 2010-2021. We live in a different world now. He’s the greatest stock price manipulator and short squeezer in history but those tactics won’t work in this environment.

Yes the brand has been tarnished but the only EV you can order and receive in a couple weeks is a Tesla. Also, take a test ride in all the other EV offering and then try out a Model 3. Absolutely no comparison.

Obviously all car manufacturers will be taking a hit during a recession but people forget that Tesla is expanding their supercharger network at about 50% a year. These things are huge money makers as they pay around .14 a kwh in the US and charge back around .35-.40 per kwh to customers.

I have a smidgen and will add on weakness but not until Musk gets his face out of Twitter. The market is screaming that Twitter is a huge overhang.

Also, the more I think about META, the more I worry. Meta is facing an advertising slowdown and HUGE competition from TikTok. The metaverse is years away and will most likely be owned by Google, MSFT and Apple .. not Meta.

I like oil tankership owner/operator NAT. At 3.50/share, it just went ex-div for $.05, but says they’ll announce a $.10 div for March in February, Meanwhile you can squeeze extra juice by selling the $4 Call. Founder, Chair, CEO said Friday, “This is the best market in decades.” I can easily see a dividend yield of >10% plus what you get from selling OTM Calls = easy money. I added more shares on Dec 2 at 3.49 and made 8.5% in two weeks (even though price has barely moved) with div and selling calls.

Also ACXP should have P2b results in H1’23 and ink a deal that will at least give a 5x return.

NGENF got a $15M investment from biotech entrepeneur Adam Mesh MD but needs $25M more to complete P2 in Spinal Cord Injury, Alzheimers and MS. Recently got $1.5M for TBI from DoD, but this could be the best investment opportunity around now if any P2s work.

NGENF–How do you factor in the very slow enrollment in trials in Australia and lack of money?

ACXP–much safer.

I like ACXP. Results were 100% on p2a. If p2b come in the same I think the stock will soar. I don’t know why MM did not recommend it when Chris suggested it.

Chris tell me what you think or dont think of KNOP here?

KNOP moves oil from off-shore oil rigs to onshore containers, pipelines or refineries. Fracking killed the big offshore drilling companies like Seadrill and Transocean (just look at that 5, 10 or 20 year chart). While a 22% dividend yield is very interesting, one has to wonder how sustainable it is.

These recent words from the company give me pause:

“We remain focused on securing additional employment for our fleet for the next and coming quarters, during which pandemic and other related delays to the start-up of offshore oil production, particularly in the North Sea and in the Norwegian sector, have created an oversupply of shuttle tanker capacity at a time when we have multiple vessels coming back into the market, and which situation has also restricted the rates that are achievable for charter opportunities.

“As we are concerned that this North Sea situation may continue in 2023, we are also considering opportunities for our North Sea-based vessels in the conventional tanker market as a potential alternate source of income and employment. However, in practice, and despite strong headline rates, the all-in returns from conventional tanker employment may be insufficient once utilization and fuel costs are considered. If we are unable to employ our North Sea vessels in the near term at acceptable rates, either on third party charters or in the conventional tanker market, we are likely to experience a material adverse effect on our distributable cash flow.

https://www.knotoffshorepartners.com/investor-relations/investor-information/news/press-release-details/2022/KNOT-Offshore-Partners-LP-Earnings-ReleaseInterim-Results-for-the-Period-Ended-September-30-2022/default.aspx

Also, the options prices are indicating a lack of optimism. At current price of 9.35, the July $5 Call is offered at 4.50 and the $7.50 is offered at 2.15

And higher interest rates are hurting the company. Interest expense for the second quarter was $8.3 million, increasing $3.9 million to $12.2 million for the third quarter. The increase is mainly due to an increase in the US dollar LIBOR rate,

But thanks for making me look, I am considering PBR which has also pays a nice dividend, but has pulled back in part due to Brazil’s recent election. The Options market shows more optimism for PBR.

Dividends are a fraud for all companies. The net asset value (NAV) is the same whether a company returns the cash as a dividend. If the company didn’t pay the divvy, the share price would rise by the value of the divvy. Worse, when selling the stock, the divvy is taxed at higher ordinary rates, but if a non divvy stock is sold, the long term capital gain is higher due to lower capital gain taxes. The divvy is used to establish more confidence in a company’s cash position, but a shady company can borrow money to pay the high divvy, a wasteful practice just to market the stock as a more stable company.

I like PBR as well. They just had an acquisition. The Biden administration just announced a 3 million barrel purchase of oil to refill the SPR. They need to buy an additional 208 million barrels to get back to the level at the end of 2021. Right now we only have 3 weeks of demand stored in there. The US produces 18.8 million barrels a day but uses 20.5 million barrels a day. Oil plants are running at the high 90’s percent in efficiency and production and oil inventories are low. Enjoy the lower gas prices. They won’t be around for long. IMO.

What do you think oil prices will be in a mild, moderate, or severe recession? Michael (not MM) originally thought $50, but lately said $20-30 is possible.

Just look at the 2008 recession and the forced 2020 lockdown for reference.

OK, but this recession will actually be stagflation. Even if the money supply were to contract from here, it will still vastly higher than in the last recession, so oil as an inflation hedge should be much higher than in 2008 and 2020. Bottom at $50-60?

Thanks for the nicely detailed reply and heads up on PBR

How sensitive is the fractal dimension metric? How soon can you make a distinction between the start of the next trend vs. noise? Hi put/call ratio seems like a move up would be likely. However, with recent trend being down and Fed being so aggressive with their intentions with a higher/longer terminal rate, a continued down trend seems equally plausible. I’d like to reposition a little once the energy begins releasing and the direction is known. Thanks!

I like SAVA for potential Alzheimer’s patients. Asked MM about it when it was under $30 currently $38 with OL results due around year end. Also been buying NGL preferred stock at large discount to face value. If they turn things around should be a 3 bagger ($25 face value) and the yield will return $2.5 a year in dividends. Currently less than $10 a share. Dividends suspended but accruing. They are a mid-Stream Energy company. Oil will affect their results.

This is the NASH play that MM should have had us invested in instead of CWBR!!

Shares of Madrigal Pharmaceuticals Inc. MDGL, +1.43% soared 209.6% in premarket trading on Monday after the company shared positive data from a pivotal Phase 3 clinical trial assessing its experimental treatment for nonalcoholic steatohepatitis (NASH) with liver fibrosis. Madrigal said it is aiming to get an accelerated approval for the drug, resmetirom. There are no approved treatments for NASH with liver fibrosis, and patients are at risk of liver failure, liver cancer, and premature death. About 5% of the U.S. population has NASH, according to the American Liver Foundation. The full data will be published in a medical journal, Madrigal said. The company’s stock is down 24.7% so far this year, while the S&P 500 SPX, -1.11% has declined 19.1%.

So NVTA has a news release today, selling off an asset it to raise capital. The street doesn’t like it and down goes the stock yet again. So companies not making money are being punished in this market. Here we go again, riding another NWI stock to oblivion. Merry Christmas to us all.

I guess Frank the 48 million will go towards there Christmas bonuses before they close up shop,what a gem of a recommendation,merry Christmas to you also

KPMG surveyed more than 900 automobile industry experts, and the media expectation for US EV sales in 2030 has dropped to just 35% of the market… from 65% last year. Nearly cut in half!

Meanwhile in China … https://www.investors.com/news/china-ev-sales-november-2022-nio-li-xpeng-byd-hopeful-positive-signs/

Mike, take off the blinders. This is the new world investor letter .. right?

Long on oil, higher prices are certain, and people won’t want 100 MPGe vehicles. Yeah, right.

The Radar Report for 12.22.22 is posted. New recommendation: EQT (EQT)