Dear New World Investor:

Inflation is slowing towards the Fed’s current 2% target. Employment is slowing rapidly, with the March payrolls number due during tomorrow’s stock and bond market holiday.

In February, the personal consumption expenditures (PCE) price index — the Federal Reserve’s preferred measure of inflation — was up 5.0% from a year earlier and 0.3% month-over-month. The core PCE index, which excludes food and energy costs, posted a year-over-year increase of 4.6% and also was up 0.3% month-over-month, just below the 0.4%% estimate.

A 0.3% monthly increase compounds to 2.0% a year – the Fed’s target.

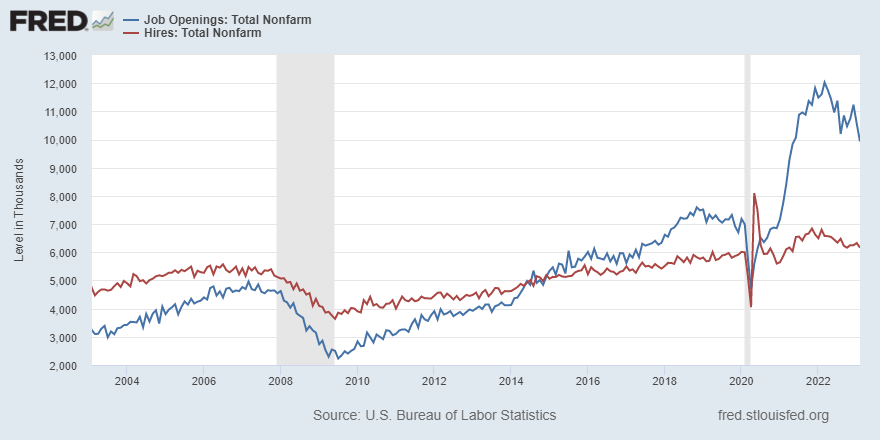

On the employment front, the JOLTS report (Job Openings and Labor Turnover Survey) for February declined by 632,000 to 9.931 million. That was well below estimates and was the first time the number dropped below 10 million since May 2021. Hires also decreased, by 164,000 to 6.2 million. There is an embedded slowdown in the March and future month numbers if the banking meltdown has the expected effect.

Click for larger graphic

Click for larger graphic

This morning we learned that applications for US unemployment benefits rose by 228,000 for the week ended April 1, higher than the consensus estimate of 200,000. The prior week was revised up to 246,000 and continuing claims were also revised up. Yesterday, the ADP report showed that employers added only 145,000 jobs in March as the labor market showed signs of slowing from its strong pace so far this year. That was far below the consensus estimate of 210,000 and much lower than the revised 261,000 jobs gained in February.

A softer nonfarm payrolls report tomorrow could put the Fed on hold. According to the futures, the chances of a rate hike at the May 3 meeting are only 47%, down from 70% earlier in the week. Economists expect Friday’s jobs report to show 240,000 jobs created last month – significantly lower than the average job gains of 343,000 over the last six months

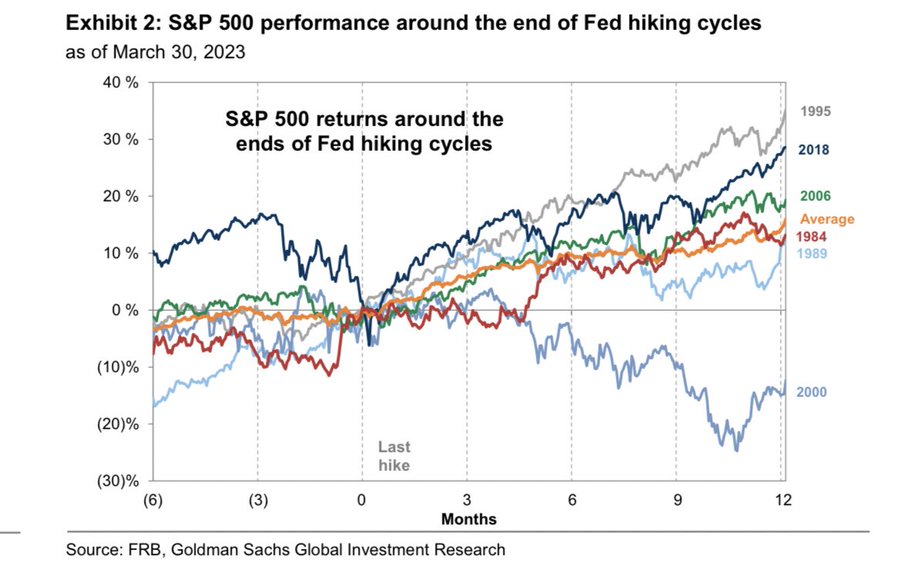

Goldman Sachs said stocks have “generally rallied .. following the end of past Fed tightening cycles. .. The exceptions were when the economy entered recession near the end of tightening .. Our baseline year-end $SPX forecast of 4000 .. would be a break with the historical pattern.”

Click for larger graphic

Click for larger graphic

Market Outlook

The S&P 500 added 1.3% since last Thursday. The Index rose 5+% over the two consecutive quarters. That’s happened 23 times since 1950, and stocks have been higher a year later 20 of the 23 times, or roughly 87% of the time. The Index is up 6.9% year-to-date. The Nasdaq Composite gained only 0.6% and is up 15.5% for the year. The small-cap Russell 2000 dropped 0.8% and is down 0.4% in 2023.

The fractal dimension still is working its way down to the 55 level that will signal a new uptrend is underway. The next trend should get close to the all-time highs.

JPMorgan traders are warning clients of a possible market-wide short squeeze amid stubbornly dismal sentiment. Bring it!

Top 5

Changes this week: None

Near-Term – chronological order

EQT EQT –natural gas price rebound

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

BLPH Phase 3 results mid-2023

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

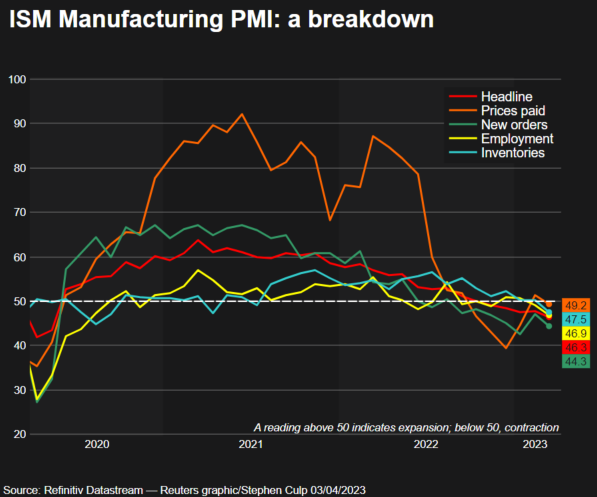

The US manufacturing sector was the weakest in nearly three years in March. The Institute of Supply Management survey showed all subcomponents of its manufacturing Purchasing Managers Index below the 50 threshold for the first time since 2009.

Click for larger graphic

Click for larger graphic

The latest ISM services data also showed further sequential weakening, indicating a recession is coming or already here. The services index was down from 55.1 to 51.2 New orders fell from 62.6 to 52.2, a whopping 10.4 percentage points decline New export orders were even worse, down from 61.7 to 43.7, an 18.0 percentage point decline.

The usual pattern of weakness in a recession is @MichaelKantro’s HOPE model. Housing breaks first, followed by Orders (where we are now), then Profits (where we might be in June quarter announcements), and finally Employment (where we might get an early sign tomorrow morning).

Click for larger graphic h/t Prometheus Research

Click for larger graphic h/t Prometheus Research

Since March 23, the baseline GDPNow forecast has fallen from +3.5% to +1.5%.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, April 7

Markets Closed – Good Friday

March payrolls – 8:30am – +240K expected; was +311K in February

Tuesday, April 11

AG – First Majestic – Through 4/13 – Gold Forum Europe

AKBA – Akebia Therapeutics – 10:00am – Shareholders meeting – reverse split, vote NO

Wednesday, April 12

Consumer Price Index – 8:30am – Expected: Headline 6.1% YoY, 0.2% MoM (previous month 0.4%). Core: 5.5% YoY, 0.5% MoM (previous month 0.5%)

Short Interest – After the close

Friday, April 14

AG – First Majestic – SilverCon 2023

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Arch Therapeutics (ARTH – $3.36) said the Centers for Medicare and Medicaid Services HCPCS code for AC5 went into effect on April 1, 2023. Dan Yrigoyen, VP:Sales said: “Since the announcement last month that CMS created an HCPCS code for AC5 Advanced Wound System, we have had new product inquiries by potential customers in offices and other outpatient facilities who previously indicated they were unwilling to order AC5 absent an available dedicated reimbursement code. We believe that A2020 will facilitate new and ongoing engagement with a growing number of interested potential customers in outpatient settings.” ARTH is a Hold for a buyout.

Primary Risk: AC5 fails to sell or the internal trial fails.

Clinical stage of lead product: External approved. Internal trial 2023

Probable time of first FDA approval: External done. Internal 2024

Probable time of next financing: March or June 2023 quarter

Bellerophon Therapeutics (BLPH – $10.20) finished 2022 with a $19.8 million loss, or $2.08 per share. They had $6.9 million in cash on December 31. In the March quarter they got $1.7 million from New Jersey’s R&D tax credit program, $6.0 million from the China license to Baylor Biosciences, and $5.0 million from the stock sale to Kevin Tang. They probably burned another $5 million, so at the end of March they should have had around $14.5 million. That will carry them through the midyear data release on the pivotal Phase 3 trial in fibrotic Interstitial Lung Disease (fILD).

Then they’ll raise more money, presumably at a much higher price, to take them through an FDA filing around yearend and approval in 2024. They will start a six-month Phase 2 double-blinded placebo-controlled study of iNO45 for Pulmonary Hypertension-Sarcoidosis (PH-Sarc) as soon as they have the cash resources. Buy BLPH under $5 for a $30 first target and $100 someday.

Primary Risk: The Phase 2b PH-ILD trial fails or the FDA turns down the INOpulse.

Clinical stage of lead product: Phase 2 transitioning to Phase 3 in the March quarter

Probable time of first FDA approval: 2024

Probable time of next financing: September 2023 quarter

Inovio (INO – $0.77) is evaluating several data readouts to determine their next steps. The VGX-3100 Phase 3 trial was successful, so they may proceed to a registrational Phase 3 trial.

The INO-3107 Phase 1/2 interim data in recurrent respiratory papillomatosis was very strong and I expect them to announce they are going to do a registrational Phase 3 trial. This is leapfrogging VCX-3100 as Inovio’s lead therapy.

They have to decide what to do with INO-5401 for glioblastoma (brain cancer). It seems to work, but this is a very tough disease to defeat.

They discontinued their MERS (Middle East Respiratory Syndrome) and Lassa fever candidates, mostly due to a lack of further funding support for these relatively small markets. They had very positive Phase 1 data for INO-4201 as a booster for Ervebo for Ebola and will continue development if the funding partners pony up.

WHO is still testing INO-4800 as a universal booster for all COVID-19 vaccines. INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: Mid-2024

ScyNexis (SCYX – $3.47) reported a December quarter loss of $14.4 million or 30¢ per share, beating the 40¢ loss estimate.

Brexafemme had $1.4 million in sales in the quarter and was prescribed by 2.546 healthcare professionals, an increase of 2% over the September quarter even though they didn’t promote it.

Case Western Reserve University researchers got a $3+ million grant from the National Institutes of Health to investigate SCY-247, a second-generation fungerp not part of the Glaxo SmithKline deal, as a potential treatment for Candida auris, the multidrug-resistant yeast that causes serious and often deadly infections.

The company ended the year with $73.5 million in cash. When they get the first $90 million from GSK, they’ll have a projected cash runway of more than two years. As the milestone payments and royalties start flowing, I don’t think they’ll ever need to raise money again. Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2023/2024

Probable time of next financing: Never

Biotech MegaShift

Akebia Therapeutics (AKBA- $0.54) tried an alternative three-times-a-week dosing regimen for vadadustat and both the 600-milligram and 900-milligram doses were non-inferior to the long-acting erythropoiesis-stimulating agent Mircera. We should be hearing the FDA’s decision on Akebia’s appeal of the Complete Response Letter shortly. AKBA is a Hold for the results of the FDA appeal on vadadustat.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Vadadustat NDA filed; CRL

Probable time of next FDA approval: Unknown

Probable time of next financing: Unknown

TG Therapeutics (TGTX – $15.48) said the European Medicines Agency’s Committee for Medicinal Products for Human Use recommended the approval of Briumvi to treat adult patients with relapsing forms of multiple sclerosis. The European Commission is expected to make a decision on the medicine in about two months. Buy TGTX under $7 for a target price in a buyout of $25 or more now that the MS drug is approved.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Second half of 2023

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $164.66) and Meta are leading the market’s rally year-to-date. Apple is up 26.9% and pushing toward its all-time high of $182.94 on January 4, 2022, but it’s not time to sell. Wedbush’s long-time and very good Apple analyst Dan Ives said investors should be feeling confident about its capacity to go further as a result of sustained demand for iPhones and future services revenue. He said Apple is benefiting from strong demand in Asia for the iPhone 14, with no major production cuts. He raised his target price from $190 to $205 while continuing to rate it Outperform. He wrote: “While Apple clearly has benefited this quarter from December unit shortages that slipped into January/February, we have seen China iPhone demand in particular see a clear tick up this quarter with a strong month of March.”

He added that in addition to Apple’s continued strength in phone sales, investors should be counting on an acceleration in services revenue in the coming quarters, based on price increases and the 100 million new iPhone users added over the past 15 months. He said: “We believe overall the services business is worth $1.2 trillion to $1.3 trillion for Apple’s sum-of-the-parts valuation and remains an underappreciated asset by the Street.”

UBS said Apple’s iPhone sell-through data in February showed signs of improvement. Market research firm Counterpoint Research said sell-through data in February was down 3% year-over-year, compared to an 11% decline in January and roughly 18% drop in December 2022.

UBS said that over the past two years, January and February typically account for roughly 70% of March quarter sell-through, implying a March 2023 quarter sell-through of 56 million phones, down about 7% from last year’s 60 million phones.

The year-over-year sell-through data has turned around in the US and was up 6.6% in March to 4.9 million phones, the first positive monthly figure since October 2022. The China sell-through data was up 4.7% year-over-year to roughly 4.5 million units. iPhone sell-through in India is up 28% year-over-year, accounting for roughly 4% of total iPhone sell-through. UBS has a Buy rating with target price of $180.

The real key to Apple as a foundational stock for your portfolio comes from the annual Piper Sandler survey of teenagers. This year’s survey of 5,700 people with an average age of 16.2 years, 87% of respondents said they own an iPhone. 25% said they plan to upgrade to an iPhone 14 in the spring or summer.

In addition, the survey showed that teenagers continue to own Apple’s other hardware products in droves. More than 35% of respondents said they already owned an Apple Watch and 73% said they owned AirPods, both of which are new records for the survey. 9% said they intend to buy AirPods in the next 12 months.

Other major findings from the survey show that 31% of teen respondents use a fitness app as part of their workout regimen and 39% said Apple Pay was their top payment app. Interestingly, just 29% of teenagers own a VR headset and only 14% and 4% use it on a weekly and daily basis. As soon as Apple launches its mixed-reality headset, incorporating virtual and augmented reality, they’ll have a ready market.

My teen has an iPhone so she can FaceTime her friends who all have iPhones. As long as Apple can capture millions of more teenagers every year, their future growth is built-in. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $83.37) is enrolling patients for two late-stage trials for obeldesivir, an oral version of Veklury (remdesivir). Once metabolized, the drug acts similarly to Veklury and targets viral replication by inhibiting the microbe’s RNA polymerase. Gilead plans to test a twice-daily obeldesivir tablet for five days. That will give it an advantage over Pfizer’s Paxlovid (three pills twice a day for five days) and Merck’s Lagevrio (four capsules twice a day for five days).GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $216.10) is up 79.6% so far this year and up 145.3% from its 52-week low of $88.09 on November 4. Credit Suisse maintained their Outperform rating abd raised their 2023 pro forma earnings estimate from $13.96 to $14.71 and their 2024 estimate from $15.36 to $16.91. They said: “With two rounds of cost cuts already announced and behind us, the investment rationale now hinges on revenue growth outperformance. We believe there is significant room for Meta to ramp revenue as it continues to highlight the value of both Messenger and WhatsApp to marketers. Our estimates currently reflect no increase in the number of messages per user or price per message—only ongoing user growth.”

They believe the company has managed to adapt to Apple’s 2021 privacy changes that necessitated user consent for advertising tracking on iPhones and iPads. They pointed to features like “Click-to-Message for Messenger and WhatsApp” which are ads that feature a box that customers can click to message the brands directly about the advertised products or services. They also think the rollout of advertisements in Instagram search results also will be meaningful. They wrote: “While details at this point are sparse, this does make us revisit the original assumptions we had been carrying in our models for search revenue when the company first mentioned Graph Search almost a decade ago. This has the potential to add a new stream of high-margin revenue—potentially reaching close to $1 billion over the next several years.”

They also are less worried about competition from TikTok, pointing to SimilarWeb data that show an uptick in recent months for Instagram minutes spent a day.

Argus Research also joined the running of the bulls with an upgrade to Buy with a $270 target. They wrote: “Cost cutting will not do much for Meta’s revenue issues, which reflect macroeconomic uncertainty, the slowdown in digital advertising, and the impact of Apple’s ad tracking policy. However, the cost cuts do demonstrate prudence by management and should improve profitability, thus giving the market what it wants.”

But Jefferies really gets it. They said that Meta can accelerate revenue growth in the second half of this year. A combination of artificial intelligence investments leading to higher engagement and easier comparisons will speed up growth, while the expense cuts combined with more buybacks will drive an upside in earnings per share. META is a Buy under $150 for a $400 target in 2024.

Other Tech

Velo3D (VLD – $1.95) sold another Sapphire XC large-format printer to Keselowski Advanced Manufacturing, a new customer. CEO Brad Keselowski said: “We feel confident that our Sapphire XC will allow us to serve new industries by increasing the physical size of the parts we can deliver. This will be our first Sapphire XC but as demand for these parts increases, we can easily add more printers to our fleet due to Velo3D’s machine-to-machine repeatability.”

VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Inflation MegaShift

Gold ($2,022.80) broke decisively over $2,000, pushing closer to its all-time record high around $2,070, as the US dollar and Treasury yields weakened after the data showed job openings dropping to a 21-month low and factory orders falling.

Gold has outperformed the S&P in 2023, up 10.4%. The fractal dimension will signal a new uptrend next week, with plenty of energy to add hundreds of dollars to gold’s price. Got gold?

Miners & Related

First Majestic (AG – $7.48) announced their yearend mineral reserve and resource estimates. Proven and Probable mineral reserves estimates at their three producing mines totaled 136.8 million silver-equivalent ounces, consisting of 61.5 million ounces of silver and 781,000 ounces of gold. Silver ounces remained relatively unchanged, decreasing only 2% after the exploration programs successfully offset depletion due to production during the year.

Gold ounces decreased 41%, primarily due to their decision to report only resource estimates for the Jerritt Canyon property after temporarily suspending production.

Measured and Indicated mineral resource estimates for all four mines totaled 351.5 million silver-equivalent ounces, consisting of 101.7 million ounces of silver and 2.82 million ounces of gold, representing an 8% and 2% decrease in silver and gold, respectively.

These are merely OK numbers. They need to replace the mined metal at a higher rate in 2023 and get Jerritt Canyon operating again. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $6.20) sold a record 28,400 attributable gold equivalent ounces in the March quarter, up 51.5% from last year’s 18,741 ounces. That generated record preliminary revenues of $44.0 million, plus they got a one-time $10.0 million royalty payment for a total of $54.0 million, up 52.5% from last year’s $35.4 million. Their cash operating profit margin was about $1,659 per attributable gold equivalent ounce.

They increased their stock buyback program to buy up to 24 million more shares, up to 9.7% of the publicly floating stock. In the last 12 months they bought 336,201 shares. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $28,094.41) is up 75% from its lows and clinging to the $28,000 level, but as we know it is very volatile and can spike down – or up – at any time. The next halving is due in less than a year, and history says we should see $100,000 before then.

Click for larger graphic

Click for larger graphic

One cause of the volatility is that liquidity remains low as the crypto “tourists” stay away due to a widening US regulatory crackdown on ishtcoins and exchanges, plus the collapse of a few crypto-adjacent banks. Also, institutions are less willing to trade and offer liquidity because they don’t want to get caught in the middle of a battle between US regulators and exchanges. This will pass as SEC Chairman Gary Gensler is forced to establish written regulations instead of his case-by-case actions. BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $16.21) has 0.00090813 bitcoin per share. That times today’s closing bitcoin price of $28,094.41 means you get $25.51 worth of bitcoin for each share of GBTC, which closed today at $16.21. $25.51 for $16.21 means you are getting a 36.5% discount from net asset value. Or, to put it another way, when GBTC converts to an exchange-traded fund you will make $25.51 / $16.21 = 57.4% on your investment even if bitcoin goes nowhere. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $80.41

Surprise! Saudi, Russia, Iraq, UAE, Kuwait, and four other OPEC nations made deep voluntary oil production cuts totaling 1,657,000 barrels per day from May 1 to Dec 31. Given the number of days from 5/1 to 12/31, the cuts are roughly the equivalent of the number of barrels we need to refill our Strategic Petroleum Reserve. OPEC+ just raised the middle finger to Fed Chairman Powell’s demand destruction and the Biden Administration’s energy policy, while blowing up a bunch of oil shorts for fun and profit.

Even before the cuts hit, gasoline prices nationwide have notched up to a five-month high, surpassing $3.50 per gallon, according to data from AAA. As HFI Research said: “The initial market reaction is correct to push oil prices higher, but in order for prices to sustainably move higher, we will need to see crude exports fall. What will be interesting about the latest announcement is that it will coincide with summer power burn demand in the Gulf coast countries. Normally, summer crude exports fall because of higher domestic demand, so the timing is interesting and could impact crude exports more than meets the eye.”

Energy Secretary Jennifer Granholm said the Administration isn’t willing to pay more than $72 a barrel for oil and “it could take years” to refill the Strategic Petroleum Reserve. As Goldman Sachs said: “OPEC+ has very significant pricing power relative to the past. Today’s surprise cut is consistent with their new doctrine to act pre-emptively because they can without significant losses in market share.” And BofA added: “OPEC is no longer afraid of a major US shale oil supply response if Brent crude oil prices trade above $80 per barrel, so cutting volumes to push oil prices higher does not carry the same risks it did five years ago .”

Just as supply gets cut, oil demand is starting to surprise to the upside, driven by gasoline and jet fuel. As you can see in the 4-week average implied demand charts below, gasoline is now firmly above 2022 and on pace to reach 2019 levels by this summer, while jet fuel is firmly above 2020 and 2022.

Click for larger graphic h/t HFI Research

Click for larger graphic h/t HFI Research

And product storage is going to hit a new low this summer if refinery throughput doesn’t pick up soon. Gasoline storage already is at its lowest level for this time of year. Got OIL?

Click for larger graphic h/t HFI Research

Click for larger graphic h/t HFI Research

The July 2026 Crude Oil Futures (CLN26.NYM – $64.78) are a Buy under $65 for a $200+ target. Only buy futures for all-cash; do not use margin.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $30.58) is a Buy under $36 for an $80+ target.

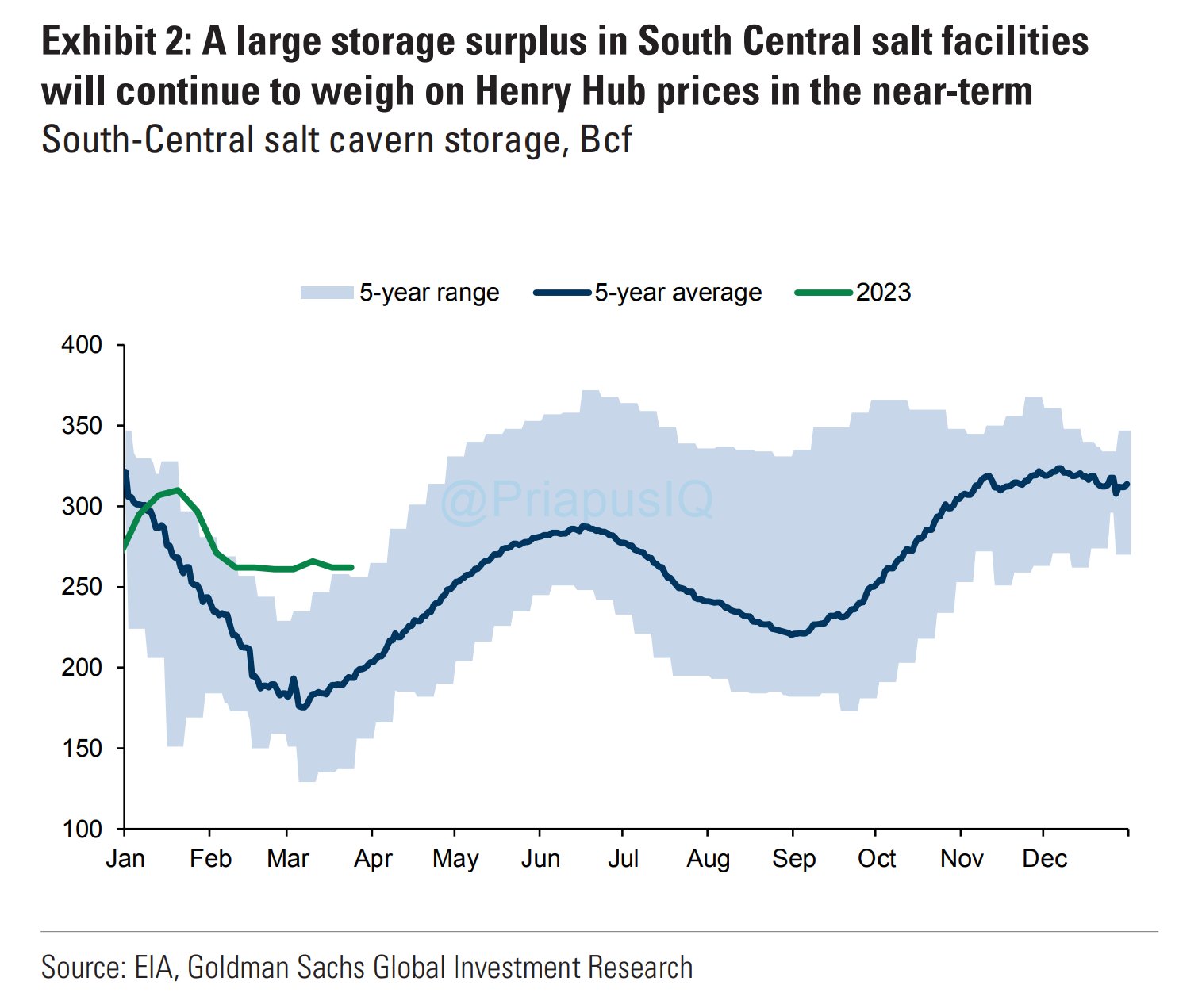

EQT (EQT – $32.12) is stuck around $30-$32 as US natural gas futures stay weak on rising output and forecasts for milder weather and less heating demand than previously expected,. That also allows utilities to start injecting gas into stockpiles for the summer air conditioning demand.

The natty price decline occurred despite a rise in the amount of gas flowing to liquefied natural gas (LNG) export plants to a record high after Freeport LNG’s export plant in Texas exited an eight-month outage in February and returned to full power. (Freeport LNG shut in June 2022 after a fire.) When operating at full power, Freeport LNG consumes about 2% of the total US gas supply. Average gas flows to all seven big US LNG export plants have risen to 14.1 billion cubic feet a day (bcfd) so far in April, up from a record 13.2 bcfd in March.

The natgas market has been extremely volatile in recent weeks with the front-month gaining or losing more than 5% in 11 of the past 21 trading days. The drop in gas prices coupled with a 20% increase in crude futures over the past couple of weeks boosted oil’s premium over gas to its highest in almost 11 years. The oil-to-gas ratio, or the level at which oil trades compared with gas, jumped to 39-to-1, its highest since May 2012. Crude’s premium has averaged 29x gas so far in 2023, up from 15x in 2022 and 20x during the past five years (2018-2022).

On an energy equivalent basis, oil should trade at 6x gas. This is why an investment in EQT makes so much sense. Last week, gas speculators cut their net short futures and options positions on the New York Mercantile and Intercontinental Exchanges for the fifth week in a row to their lowest since July 2022.

Goldman Sachs said: “While a larger than expected end-of-March storage leads us to lower our Summer 2023/Winter 2023-2024 Henry Hub price forecasts to $3.00/$3.10 from $3.50/$3.40 previously, we expect sequentially tighter balances to lift US gas prices significantly versus the current prompt contract, reaching $3.30 by July.” That would push EQT’s stock price higher.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $5.07) posted a new presentation. The key slides:

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

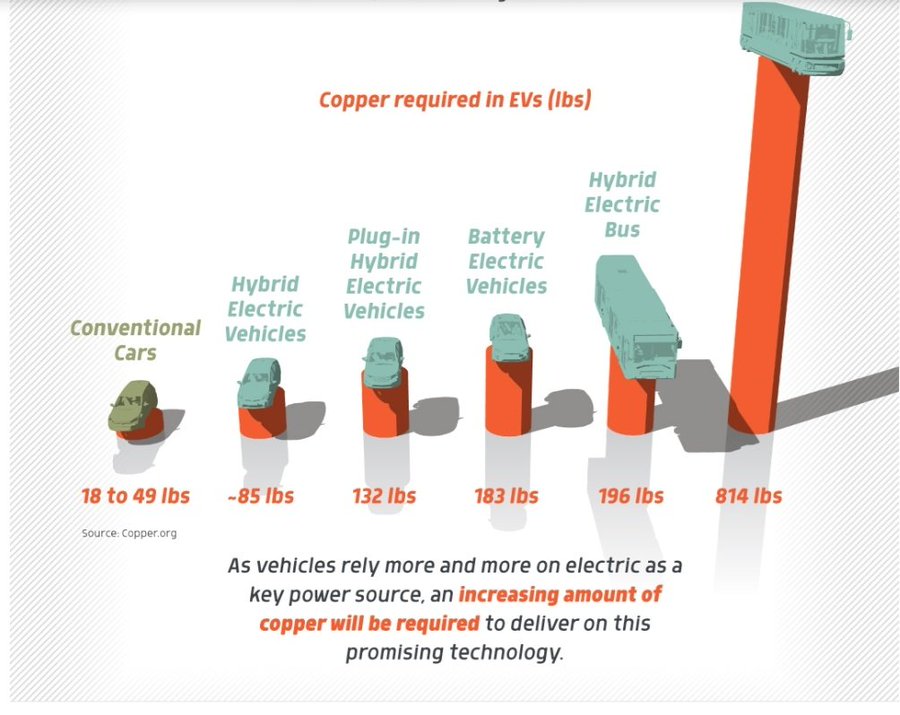

Freeport McMoRan (FCX – $40.29) is a direct beneficiary of the move to EVs, no matter which manufacturers win the race.

Click for larger graphic

Click for larger graphic

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

* * * * *

RIP Gordon Moore

On a personal note, Intel cofounder Gordon Moore died at 94. I was at American Express Investment Management when we did the last private venture round in Intel before the IPO. Gordon was born in a little California farming town just south of my ranch in Half Moon Bay, and he never lost that rural coast courtliness and thoughtfulness. He was kind enough to be a guest on a television show I hosted for three years in Silicon Valley, which skyrocketed the ratings. May his memory and Moore’s Law last forever.

* * * * *

Your seeing too many tents Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.55) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $10.20) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $10.49) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.77) – Buy under $7, hold a long time

Invitae (NVTA – $1.32) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.58) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $3.47) – Buy under $2.50, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $15.48) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $164.66 ) – Buy under $150 for new iPhones

Corning (GLW – $34.10) – Buy under $33, target price $60

Gilead Sciences (GILD – $83.37) – Buy under $80, target price $120

Meta (META – $216.10) – Buy under $250, target price $400

SoftBank (SFTBY – $19.92) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $42.00) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $15.74) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $32.20) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $5.77) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.77) – Buy under $13, target price $30+

Velo3D (VLD – $1.95) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Hold

Bag of Junk Silver – ($25.13) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $29.95) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $34.77) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $19.40) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $31.59) – Buy under $30, target price $50

Coeur Mining (CDE – $4.12) – Buy under $5, target price $20

First Majestic Mining (AG – $7.48) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.36) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $6.20) – Buy under $10, target price $25

Sprott Inc. (SII – $35.81) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $28,094.41) – Buy

Grayscale Bitcoin Trust (GBTC – $16.21) – Buy

Ethereum (ETH-USD – $1,872.57) – Buy

Grayscale Ethereum Trust (ETHE – $9.26) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $31.30) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $25.95) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $14.13) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $30.43) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.77) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.06) – Buy under $1.30; long-term hold

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $64.78) – Buy under $65; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $30.58) – Buy under $36; $80+ target

EQT (EQT – $32.12) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.12) – Buy under $8; $30 target

Freeport McMoRan (FCX – $40.29) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Akebia Biotherapeutics (AKBA – $0.54) – Hold for FDA decision

Arch Therapeutics (ARTH – $3.36) – Hold for buyout

Graphite Bio (GRPH – $2.53) – Hold until they update their strategy

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1st

s

Second

MM – hopefully youre keeping commitment to be more responsive on tgis message board. I have 2 questions: (1) when do you expect ibrexafungerp is approved for hospital use and well see a major stock price move (2) BLPH you say buy under $5 but its now $10, is it still a buy near term?

1 SCYX has said potential approval for invasive candidiasis in 2024

2 BLPH is a Hold at these levels.

I left the board for a while and I’m kicking myself seeing BLPH at $12!! Ugh. Missed it completely.

INO, APTO, Do they have similar potential as BLPH had?

We need Kevin Tang to take a position in all of our sub $100M market cap stocks. It’s amazing what his investment in BLPH has does for the stock price.

MM–quick correction. 0.3% monthly inflation compounds to 12 X 0.3, or about 3.6% annualized, not 2%. There will be more money printing to bail out the next batch of failing banks, producing more inflation down the road. Powell is NOT finished.

The Bank Term Funding Program is a lending program for purposes of raising short term liquidity, not a (bailout) purchase of toxic loans.

It doesn’t matter. Does the money for the Bank Term Funding Program grow on trees? Yes, when the FED prints more money due to public pressure during crises. The solution to eliminating bad/toxic loans is not MORE regulation, but NO regulation so that bank officers are held personally liable for making bad loans. Lack of personal liability creates moral hazard.

You are correct about 0.3% – spreadsheet error on my part. There’s no need to print money to save failing banks. They have many other tools, primarily selling the failed bank at a big discount to a larger bank.

Good point. But still present in today’s world is the moral hazard of fiduciary irresponsibility. This leads to more bank failures, with more depositors getting FDIC payments. As a fed agency, the FDIC lives on money printing, so this is inflationary.

JGMD and MM. A compounded monthly inflation rate of 0.3% translates to an annual inflation rate of 3.66% (i.e., 1.003 raised to the 12th power.)

Right. (1 + x) to the nth power is very close to 1 + nx when x is low. When x is high, there is a big difference. 1.26 to the 3rd power is about 2.00, rather than 1.78. 1.20 to the 4th power is over 2. Buffett used to have a long term track record of 22% annually, showing the great power of compounding.

MM or anyone –

can anyone recommend an ETN parallel to OIL ? Same reasoning as oil. ESG sentiment can regulate companies to non-profitability. Much harder to regulate spot copper.

Alternatively, a good copper ETF ?

Copper play seems wise. Question is how best to play it.

Copper – iPath Series B Bloomberg Copper Subindex Total Return ETN (JJC)

Futures – United States Copper Index Fund (owns copper futures) (CPER)

Miners – Global X Copper Miners ETF (COPX)

I am buying FCX after all. JJC and CPER seem lightly traded, so spreads may get out of whack. I was exploring not buying miners, but FCX seems like an equally good bet as COPX.

Thanx.

TGTX up nearly 20%. Any news?

See above. “TG Therapeutics (TGTX – $15.48) said the European Medicines Agency’s Committee for Medicinal Products for Human Use recommended the approval of Briumvi to treat adult patients with relapsing forms of multiple sclerosis. The European Commission is expected to make a decision on the medicine in about two months.”

https://www.investors.com/news/technology/tgtx-stock-rockets-on-solid-jump-in-ms-drug-sales/?src=A00220

TG Therapeutics Logs ‘Solid Jump’ In Sales; Shares Rocket

TG Therapeutics‘ (TGTX) new multiple sclerosis drug, Briumvi, experienced a “solid jump” in March sales, according to a report that sent TGTX stock flying on Monday.

In the second month following Briumvi’s launch, the MS treatment generated $3.3 million in sales, Cantor Fitzgerald analyst Prakhar Agrawal wrote in a note to clients Sunday. That compares with $500,000 in sales during February, he said, citing Symphony Health data.

Overall, first-quarter sales were about $4 million, above forecasts for $2.5 million to $3.8 million, Agrawal said. TGTX stock analysts polled by FactSet predict $3.8 million in sales.

“We estimate that Briumvi is likely to meet/exceed the current first-quarter consensus revenue estimates,” Agrawal said.

On today’s stock market, TGTX stock rocketed 22.8% to close at 19.01 That put shares near a buy point at 19.69 out of a consolidation, according to MarketSmith.com.

TGTX Stock: Briumvi Sales Likely To Beat

Investors have been nervous that Briumvi would miss first-quarter expectations following sales that came in below forecasts for February, Agrawal said.

“But after the jump in March sales, this should no longer be a concern,” he said.

It’s still early days for Briumvi, he said. The MS treatment still doesn’t have a permanent code for insurance billing purposes. It should have that code in July. Therefore, sales in the second half of the year will be more important for assessing the overall trajectory for Briumvi, he said.

“Investor focus during the initial period seems to be more on the feedback from neurologists regarding Briumvi use which, based on our recent physician checks, is very positive and bodes well for the rest of the year,” he said.

Agrawal has an overweight rating and $24 price target on TGTX stock.

Drug Class Is Growing

Briumvi belongs to a class of drugs that block CD20, a protein found on white blood cells. This has been important in treating some neurological diseases like multiple sclerosis. Similar drugs include Biogen (BIIB) and Roche‘s (RHHBY) Ocrevus, and Kesimpta from Novartis (NVS).

Cantor’s Agrawal says the anti-CD20 drug class is growing. Ocrevus is in its sixth year after launch and sales in the first quarter are on track for $1.4 billion, up about 16% year over year. Kesimpta sales appear to have surged more than 95% vs. the year-earlier period to $390 million, he said.

“Net-net: the anti-CD20 class in the U.S. continues to grow significantly and should also benefit Briumvi,” he said.

The Briumvi sales projection sent TGTX stock above its 50-day moving average.

TGTX was up 15.36 percent. Overall up 52.52 percent. My initial position is now $9188. BLPH was up 11.62 percent. Overall up 132.69 percent. My initial position is now $8908. Who said all NWI stocks are dogs? The month of April is traditionally a strong month for the markets. More to come in my opinion.

Well it all depends on when you bought those stocks. Both are well off their MM buy prices.

TGTX Original Recommendation: October 20, 2016 @ $6.06

Do you have the original recommendation on nvta mm,since you are looking,tx

They are all on the portfolio page

https://newworldinvestor.com/portfolio/

NVTA Original Recommendation: January 18, 2018 @ $7.03

Ok,tx

The new Radar Report for 4.13.23 is posted.