Dear New World Investor:

“I thought inflation would go down because of the war,” said no one, ever. The headline Consumer Price Index for March rose 3.3% from last year and 0.9% from February – triple the 0.3% increase in February and the biggest monthly increase since 2022. Even if you drive a Tesla, you will not be surprised to learn that gasoline jumped 21.2%, the single-largest monthly increase since the government began tracking the series in 1967, and that accounted for nearly 3/4 of the monthly gain. The monthly increase was right on expectations and the annual increase was actually 0.1% lower than expected.

Core inflation, ex-energy and food, rose 2.6% year-over-year and 0.2% from February. Both were below the consensus expectations for 0.3% and 2.7%, but well above the Fed’s 2.0% target. High oil prices eventually lead to high everything else prices, from fertilizer to plastics to transportation. Those will be in core inflation for quite a while. Unless the economy weakens dramatically – and as you will see below, March quarter GDP isn’t looking so great – the Fed is going to stand pat.

Market Outlook

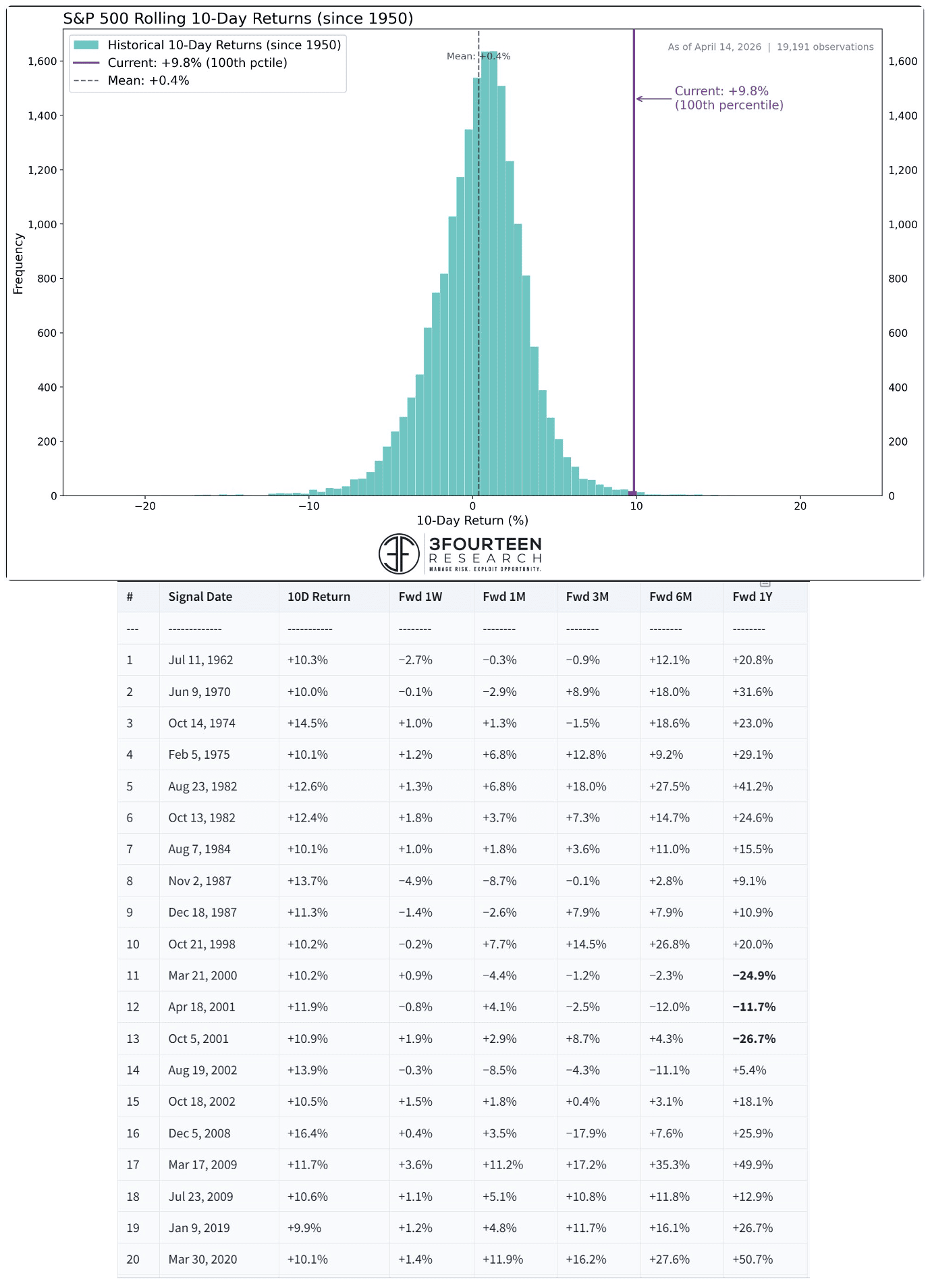

The S&P 500 added 6.7% over the last two weeks in the 5th-quickest recovery ever from a deep pullback. It got back into positive territory for the year, and reclaimed all of its losses since the start of the war in Iran. It hit new intraday (7,051.23) and closing (7,041.28) highs today. The last 10 days have been unlike any 10-day period in the market since 1950. The S&P 500 is up 9.8% in 10 days, which is in the 99.7th percentile of all 10-day returns. Since 1950, there have been 20 cases where the stock market has risen this much in 10 days. The general conclusion is that these are bullish momentum thrusts.

Click for larger graphic h/t @warrenpies

Click for larger graphic h/t @warrenpies

The S&P is now up 2.9% year-to-date. The Nasdaq Composite gained a whopping 10.2% and also booked record intraday and closing highs today. It is up 3.7% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 5.1% to new highs yesterday. It is up 11.1% year-to-date. The small-cap Russell 2000 soared 7.5% and is up 9.6% in 2026.

Top 5

Changes this week: None

Near-Term – chronological order

INO Inovio – bounce back from equity offering + FDA allows 6-month review of INO-3107

AKBA Akebia Therapeutics – Vafseo launch

BTC-USD Bitcoin – rebound from sell-off

ETH-USD Ethereum – rebound from sell-off

EQT EQT – natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model estimate of March quarter real GDP growth has fallen to +1.3%, well below the consensus expectation. The real question will be whether stocks go up because the Fed is more likely to cut, or stocks go down because the economy is stalling out. We’ll find out at 8:30am on April 30, which happens to be the date of the next issue of New World Investor.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, April 17

AG – First Majestic – Through 4/18 – INVEST Stuttgart

Tuesday, April 21

ABCL – AbCellera – 9:00am – Bloom Burton Healthcare Investor Conference

RGLD – Royal Gold – 10:00am – Another Renmark Financial Virtual Non-Deal Roadshow Series

MDNAF – Medicenna – 12:00pm – (AACR)

EQT – EQT – After the close – Earnings release; call tomorrow

MDNAF – Medicenna – 3:00pm – Bloom Burton Healthcare Investor Conference

Wednesday, April 22

EQT – EQT – 10:00am – Earnings conference call

INO – Inovio – 9:45pm – World Federation of Hemophilia Congress

Friday, April 24

Short Interest – After the close

Wednesday, April 29

Business Employment Dynamics – 10:00am – September quarter payroll revisions

Fed meeting – 2:00pm press release; 2:30pm press conference

META – Meta Platforms – 5:30pm – Earnings conference call

Thursday, April 30

March quarter GDP – 8:30am – First estimate – expect “surprisingly” weak

Personal Consumption Expenditures Index – 8:30am –The Fed’s favorite inflation indicator – expect “surprisingly” strong

GILD – Gilead – 1:00pm – Annual meeting

AAPL – Apple – 5:00pm – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $263.40) is holding iPhone prices steady as competitor Samsung increased Galaxy Flip 7 with 512GB of storage from $1,219 to $1,299, Galaxy S25 FE 256GB from $709 to $749, and the Galaxy S25 Edge 512GB from $1,219 to $1,299.The price hikes probably are due to increased memory costs, which is a bit ironic because Samsung is a major DRAM supplier while Apple buys memory.

BofA said Apple is likely to report strong March quarter results on April 30, due largely to demand for the iPhone 17 lineup and its services offerings. They wrote: “We see upside to Street estimates given continued strong sales of iPhone, double-digit growth in Services revs, and benefit from FX. Upcoming catalysts include expected new buyback authorization, WWDC in June, and launch of a foldable iPhone in the fall & [the] launch of an enhanced Siri with integration with Gemini AI which can drive higher upgrades.”

They reiterated their Buy rating on Apple and slightly raised their target price target from $320 to $325. They now expect 60 million iPhone sales, up from a prior view of 58 million, due to “strong demand” for the iPhone 17. They expect Services revenue growth of 14% year-over-year. They think, as I do, that Neo is a very important product. Last week they wrote: “We see the intro of Neo as a meaningful tailwind to Mac revs and total company EPS as the majority of revenue should be incremental to Apple. We size the [total addressable market] for 2026 at $32 billion, which we derived from notebook units priced between $300 to $800 shipped in 2025, adjusted down 10% in 2026 due to ongoing PC/memory dynamics and multiplied by Apple’s competitive education ASP of $499.”

According to Bloomberg, Apple is testing four designs for its smart AI glasses that will rival Meta’s product, with plans to launch some or all of them. The styles being tested are a large rectangular frame copying Meta’s Ray-Ban Wayfarers, a slimmer rectangular design similar to CEO Tim Cook’s glasses, larger oval or circular frames, and a smaller refined oval or circular option. The company is aiming to integrate its glasses with the iPhone and offer a higher-end build in its effort to outdo rivals.

Apple is looking to unveil the AI glasses, internally named N50, at the end of 2026 or early 2027. The actual release is targeted for 2027. The latest units are reportedly made from acetate, which is more durable than the standard plastic used by many brands. Apple is also exploring a range of finishes, including black, ocean blue, and light brown. Bloomberg wrote: “If executed properly with a functional Siri, these glasses could follow a trajectory similar to the Apple Watch: not first to market, but ultimately dominant.”

AAPL is a Buy under $205.

Gilead Sciences (GILD – $138.55) continued their acquisition binge by buying Tubulis GmbH, a German biotech developing next-generation antibody-drug conjugates (ADCs), for an upfront cash payment of $3.15 billion, payable at closing, and up to $1.85 billion in contingent milestone payments. This expands Gilead’s oncology pipeline, immediately adding TUB-040, a NaPi2b-targeting ADC for ovarian cancer and other solid tumors. It is in a Phase 1b/2 trial for platinum-resistant ovarian cancer and non-small cell lung cancer. Gilead also gets TUB-030, a 5T4 targeted ADC, which has demonstrated promising initial clinical data across various solid tumor types.

The company warned that its March quarter GAAP and non-GAAP diluted earnings per share could be impacted by a one-time charge of nearly 7¢ due to approximately $107 million in acquired in-process R&D expenses to be recognized during the quarter. They attributed the charge mainly to a roughly $80 million upfront payment they made when acquiring global rights to an experimental cancer therapy from China’s Genhouse Bio in February. The in-process R&D from the Arcellx and Tubulis transactions will be reflected in the June quarter. Wall Street almost always ignores these charges. GILD is a Long-Term Buy under $115 for a first target of $150.

Meta Platforms (META – $675.87) rose after they launched Muse Spark, their most powerful Large Language Model yet, and the first from the Meta Superintelligence Lab (MSL). Meta founded the lab in response to criticisms that its prior AI models didn’t live up to expectations. Zuckerberg subsequently hired a host of AI heavyweights, including Scale.AI founder Alexandr Wang, and established MSL.

Meta is currently using Muse Spark to power its Meta AI services and the company is already working on larger models. Zuck said: “It’s a world-class assistant and particularly strong in areas related to personal superintelligence like visual understanding, health, social content, shopping, games, and more.”

Evercore maintained their Outperform rating and $900 target price, and wrote: “Even with the recent mini-rally, Meta shares are dislocated, trading at an 18x price-to-earnings ratio (within ~10% of its trailing 3-year trough multiple) on concerns regarding the company’s aggressive 2026 capital expenditure plans as well as recent legal/regulatory developments. In our view, Meta is fully capable of addressing both issues. Meta’s recent release of Muse Spark, its first model released since the formation of Superintelligence Labs, demonstrates the company’s ability to translate elevated AI spend into a tangible frontier model that could not only improve/enhance the core advertising engine but also unlock additional monetization opportunities across Meta AI, WhatsApp Business Messaging, etc.”

Meta partnered with Broadcom to co-develop multiple generations of their next-generation MTIA (Meta Training and Inference Accelerator) custom silicon that powers AI across all of Meta’s apps and services. MTIA is a purpose-built accelerator optimized for inference and recommendation at scale. Meta expects to develop and deploy four new generations of MTIA chips in the next two years to support ranking and recommendations, along with generative AI workloads.

In a change Wall Street does not expect, market research firm Emarketer said Meta is on track to overtake Google (GOOG) in terms of total digital advertising revenues by the end of the year. Meta is forecast to reach $243.46 billion in net worldwide ad revenues in 2026, up 24.1% from $196.17 billion in 2025. Google’s net global ad revenues are expected to grow only 11.9% to $239.54 billion in 2026, compared to $214.06 billion in 2025.

Meta is also set to become the top digital advertising engine, with its share in global ad spend seen reaching 26.8% in 2026. Google’s share is forecast to hit 26.4%. Emarketer said that Meta is unlocking more value across its entire ecosystem at the same time. They wrote: “Tools like its Advantage+, AI-generated ad creatives, and its broader automation stack are improving performance across both Facebook and Instagram, with Reels being a big beneficiary. As a result, advertisers are getting better bang for their buck, and that’s pulling more ad dollars onto the platform.

“Google has plenty of levers it can pull to try to speed up growth. But the diversity of its business — it generates billions of dollars in subscriber revenues from YouTube Premium, for example — may make it harder for it to leapfrog past Meta in terms of digital ad revenues.”

META is a Buy under $705 for a long-term hold.

Nvidia (NVDA – $198.35) announced the world’s first family of open source quantum AI models, NVIDIA Ising, designed to help researchers and enterprises build quantum processors capable of running useful applications. To achieve useful quantum applications at scale, the Ising family provides high-performance, scalable AI tools for quantum error correction and calibration — two of the most critical challenges in building hybrid-quantum classical systems.

Ising models run the world’s best quantum processor calibration and enable researchers to tackle much larger, more complex problems with quantum computers by delivering up to 2.5x faster performance and 3x higher accuracy for the decoding process needed for quantum error correction. CEO Jensen Huang said: “AI is essential to making quantum computing practical. With Ising, AI becomes the control plane — the operating system of quantum machines — transforming fragile qubits to scalable and reliable quantum-GPU systems.”

According to the market research firm Resonance, the quantum computing market is expected to surpass $11 billion in 2030. NVDA is a Hold for a $180 first target.

Onsemi (ON – $79.93) was upgraded by BofA from Neutral to Buy with a target price raised from $70 to $85. They wrote: “The slow auto/EV environment makes our ON upgrade potentially a tad early, but we like the company’s 1) pipeline (rising AI power, Treo products), 2) solid FCF [free cash flow] generation (~6% FCF yield), 3) buyback commitment ($6bn/next 3 years, essentially 100% of FCF), 4) model leverage (EBIT margins could reach 1.5x to ~30% by CY28E), and 5) and low balance sheet leverage (dry power for potential M&A, as discussed by management).”

They added that there is catch-up potential, with the stock down 36% in the past three years on auto/EV/Tesla-related weakness. They noted that On has responded well by pruning its portfolio, cutting costs, and focusing on free cash flow generation and returns to shareholders. The company has also invested in boosting its AI power exposure, likely a focus at the upcoming analyst day in September, which is a potentially positive catalyst. ON is a Buy under $60 for a $130 first target.

Palantir (PLTR – $142.76), in just two years, has helped Britain’s National Health Service give 110,000 operations patients wouldn’t have had otherwise, reduce discharge delays by 15%, and increased the number of patients who get notified of a cancer diagnosis within 28 days by 6.8%. A spokesman said: “We’re delivering £5 for every £1 the government has spent. We’re delivering for patients.”

PLTR is a Buy under $160 for a $200 first target.

PayPal Holdings (PYPL – $49.81) is evolving Venmo from a peer-to-peer app into a comprehensive money movement app for the next generation of consumers. They expanded Stash, their rewards program, to give customers a new way to earn cash back on everyday purchases from some of their favorite lifestyle brands, dinner with friends, a rideshare home, to a new outfit. The more customers spend with Venmo, the more they get back.

PayPal said the Venmo debit card and Venmo’s checkout experience have become two of their fastest-growing products, with transaction volume and monthly active accounts both growing at double-digit rates year-over-year. PYPL is a Buy under $50 for a triple in three years.

Snap (SNAP – $6.02) said March quarter revenues were up 12% from last year to $1.529 billion, a skotch above the consensus estimate for $1.52 billion, with pro forma earnings before interest, taxes, depreciation & amortization (EBITDA) of approximately $233 million –

23% above the high end of their guidance, and 26% better than consensus estimates.

They also announced organizational changes, laying off 16% or 1,000 of the full time employees and closing 300 open roles. That will reduce their annualized costs by $500 million, beginning in the second half of 2026. Citi Research said this is expected to create a path to 60% gross margins and the potential to reach net income profitability by 2027. They wrote: “While Snap is cutting headcount, productivity appears to be improving with 65% of new code now generated by AI, AI agents resolving 1M+ support questions per month, and Snap restructuring towards leaner teams with AI-augmented workflows.”

The Specs smart glasses launching later this year will use Qualcomm’s Snapdragon XR processor platform. Snap established its Specs unit in January to compete with Meta, whose Ray-Ban AI smart glasses developed with EssilorLuxottica have become one of the few breakthrough successes in that category. SNAP is selling for less than 2x 2026 revenue per share. Buy under $11 for a $17+ target.

SoftBank‘s (SFTBY – $14.87) PayPay (PAYP) initial public offering was a big success. Coverage was initiated by:

Benchmark with a Buy recommendation and a $31 target price

BofA Securities with a Buy recommendation and a $26 target price

Citigroup with a Neutral recommendation and a $23 target price

Morgan Stanley with an Equal Weight recommendation and a $24 target price

Mizuho with an Outperform recommendation and a $26 target price

Jefferies with a Buy recommendation and a $28 target price

SoftBank sold $1.5 billion of senior notes. $400 million at 7.625% interest are due in 2029. $600 million at 8.25% interest are due in 2031. $500 million at 8.5% interest are due in 2036. The proceeds are meant to redeem foreign currency-denominated senior notes and for the partial repayment of the amount outstanding under the bridge loan primarily for the follow-on investments in OpenAI. I think OpenAI will go bankrupt before they can IPO, or maybe soon after, which is the main reason I moved the stock to a Hold. Hold SFTBY for a first target of $50 and then higher as the discount to hard book value disappears.

Small Tech

Fastly (FSLY – $24.88) and LALIGA, Spain’s Professional Football Association, partnered to develop technical solutions to address the illegal streaming of live sports, with special focus on LALIGA’s matches. LALIGA estimating that piracy costs its clubs between $700-$800 million each year. The collaboration was motivated by the scale of illegal streaming of live sports, with numerous unauthorized streaming sites active on each match day. A 2025 study by Grant Thornton revealed that at least 10.8 million unauthorized retransmissions of live events were detected in 2024, over 81% of these retransmissions were never suspended, and only 2.7% were addressed within the first 30 minutes of the event.

Fastly has developed a targeted, intelligent detection system that leverages AI and proprietary content signals to identify illegal streams in real time. It enables the removal of illegal content by its platform customers with enhanced precision and dramatically reduces the window of opportunity for piracy.

In a classic Wall Street move, Craig-Hallum raised their target price on Fastly from $15 to $24 and then downgraded the stock from Buy to Hold. They wrote: “For the negatives/concerns: first, capex (and increasingly, margin) is going to be challenged by surging prices for memory and other key network hardware, as demand from Al infrastructure buildouts exceeds supply. Second, Al has now clearly surpassed human capabilities with respect to detection and exploitation of security vulnerabilities in virtually all systems, making it increasingly hard to charge for value-add services layered on top of the core network (i.e. WAF, etc), with that value more likely now to accrue to leading frontier models (security currently 22% of revenue).”

I think that’s wrong. Fastly will use AI to make security better.

Third, they said that compares will get more difficult, mainly as Edgio tailwinds abate. That’s true. In December 2024, Akamai Technologies acquired select assets of Edgio, leading many customers to churn off, likely landing on Fastly’s platform at renewal time.

On the positive side, they said that pricing remains compelling, with mid-single-digit declines yielding the best gross margin in years. They noted that remaining performance obligations, or RPOs (future revenues), have surged, with at least a meaningful portion related to efforts to extract higher minimum-commitments from customers, increasing visibility. They also said that Al is comprising an increased percentage of overall traffic, as bots/agents perform tasks, and concluded: “In sum, the company has done a very nice job executing, integrating product and improving go-to-market. At the same time, we are stepping aside as much appears reflected in the current valuation and we await a more attractive risk/reward entry,”

Well, that’s what makes markets. I think Fastly is an AI winner because they can use any AI model to improve their product. FSLY is a Buy under $10 for a 3- to 5-year hold to $50+.

Primary Risk:Content and applications delivery networks are a competitive area.

QuickLogic (QUIK – $12.40) named Quantum Leap Solutions as an authorized sales representative. The CEO of Quantum Leap said: “We are excited to represent QuickLogic based on their long-standing FPGA expertise. Customers are increasingly requesting embedded FPGA to enable post-silicon flexibility as application requirements evolve. QuickLogic’s proven eFPGA Hard IP reduces costs, lowers development risk, and accelerates time to revenue.”

QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

ARK Venture Fund (ARKVX – $50.03) has a stellar portfolio of private investments. The only ones I worry about are OpenAI and, to a lesser extent, Anthropic.

Click for larger graphic

Click for larger graphic

ARKVX is a Buy for the SpaceX IPO.

Primary Risk: Cathie sells the stock before the IPO.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Despite significant biotech outperformance and relative strength versus the market averages , the one-week and one-month average daily put-to-call ratios of the iShares Biotechnology ETF (IBB) and SPDR S&P Biotech ETF (XBI) remain elevated, showing sentiment is cautious. Out of 50 index and sector exchange-traded funds (ETFs) monitored, XBI has the fifth highest put-to-call ratio as traders fade biotech’s persistent strength rather than embrace it. The wall-of-worry persists – there is no crowding here. Yet.

Click for larger graphic h/t @EdenRahim

Click for larger graphic h/t @EdenRahim

Akebia Therapeutics (AKBA- $1.35) held private one-on-one meetings at the Raymond James 2026 Biotech Innovation Symposium on Tuesday, April 14. I don’t know what they said, but the stock dropped 20¢ today.

The company said they dosed the first participants in their Phase 1 clinical trial of intravenous AKB-9090, the internally developed hypoxia-inducible factor-prolyl hydroxylase (HIF-PH) inhibitor being evaluated for the treatment of cardiac surgery-associated acute kidney injury (AKI). This Phase 1 trial is randomized, double-blind, and placebo-controlled, with single and multiple ascending doses. Buy AKBA up to $4 for the Vafseo launches in the EU, UK, and US. I think GSK and/or Amgen will make a bid for the company.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: 2026

Probable time of next financing: Never

Compass Pathways (CMPS – $6.66) began a US grant program to create training content for healthcare providers to deliver COMP360 psilocybin treatment after approval. Compass expects to award up to three organizations grants to support the development of foundational psychedelic and COMP360-specific training.

CEO Kabir Nath, CCO Lori Englebert, and Chief Patient Officer (CPO) Steve Levine made another brokerage firm presentation at the Needham Virtual Healthcare Conference (WEBCAST HERE). Their focus is on the upcoming launch of COMP360, because given the top-line data released so far, at this point I think approval is a given. They are in the midst of a rolling submission and will complete their New Drug Application by the end of this year. They probably will get a priority review with approval in mid-2027 – the first psychedelic drug approval ever. CMPS is a Buy under $10 for a very long-term hold to $200.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2027

Probable time of next financing: Never

TG Therapeutics (TGTX – $34.30) completed enrollment of the Phase 3 trial of subcutaneous Briumvi and expects to give us top-line data by the end of this year or early in 2027. Buy TGTX under $30 for a target price in a buyout of $40 or more.

Primary Risk: Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($4,811.50) gained as the dollar weakened again, plus it is being heavily bought by China’s central bank. They bought the most gold bullion in more than a year in March – 160,000 troy ounces, or about five tons. They have added to holdings for 17 months straight, and they tend to under-report. Société Générale analysts estimated China’s total gold purchases could reach 250 tonnes, roughly 10 times higher than the officially reported 25 tonnes, through much of the year.

Miners & Related

Coeur Mining (CDE – $19.51) presented at Mining Forum Europe and, as always, violated SEC Regulation FD by blocking us from the presentation. The did share the slides HERE, which was enough for me to see it was the usual blather background presentation.

Click for larger graphic

Click for larger graphic

Thanks to the timely New Gold acquisition, 2026 is going to be a barn-burner for Coeur:

Click for larger graphic

Click for larger graphic

Although I rag on them for not caring enough about the stock price to post the audio/video of their presentations, they have done a great job of running the company. When I recommended holding the stock at $3.67 after they acquired our Paramount Gold & Silver Mexican assets way back in May 2009, I thought they would rebuild their balance sheet and get costs down enough to get a double or better on the stock. They did that, then the price of gold and silver took off, and then they did the excellent New Gold acquisition at a great price. So here we are at $19.51, and I’m moving CDE to a Hold as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $21.05) said that total production in the March first quarter of was 3.5 million ounces of silver (26% of their 2026 guidance), 34,341 ounces of gold (28% of guidance), 15.4 million pounds of zinc, 8.7 million pounds of lead, and 262,913 pounds of copper. During the quarter, they completed a total of about 216,400 feet of drilling with up to 27 drill rigs active. Hold.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $1.79) has begun an Initial Assessment under SEC S-K 1300 for its 100%-owned Sleeper Gold Project. It will focus on a potentially lower-cost, staged development approach on heap-leachable material only, including approximately 54 million tons of material of economic interest. This includes surface material from previously unevaluated waste dumps, as well as oxide and mixed in-situ mineralization amenable to heap leaching. This approach has the potential to support an accelerated path to cash flow and enhance overall project economics. It is also expected to contribute to development planning and the evaluation of potential future expansion opportunities.

And, of course, it will make the project more salable. Subscriber BRAD asked on the Comments board: “Any timeline predictions on PZG selling or partnering Grassy and or Sleeper?” I replied: “PZG should sell or partner both projects in the next 12 months. They’ve done as much as they can as a prospect developer, which is what they are.”

PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: 2026

Royal Gold (RGLD – $262.13) also presented at Mining Forum Europe (VIDEO HERE and SLIDES HERE and TRANSCRIPT HERE). SVP: Corporate Development Dan Breeze said Royal Gold has the longest track record of consecutive dividend increases in the GDX index – 25 years. It is the only precious metals company in the S&P High Yield Dividend Aristocrats Index.

The portfolio is 95% precious metals, global, and weighted towards lower risk and mining friendly regions. It spans all stages of development. There are roughly 80 producing properties at the moment with 30 more in development and then more than 250 properties behind that in earlier stages of work, all bought and paid for. They have only 39 employees, so it is a very high margin business.

Click for larger graphic

Click for larger graphic

RGLD is a Buy under $180.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly.

Bitcoin (BTC-USD on Yahoo – $75,146.29) touched a three-week high as investors turned more optimistic after the ceasefire deal between the US and Iran. The Iranian regime is looking to charge fees of $1 per barrel of oil for tankers crossing the Strait of Hormuz, with payments to be made in cryptocurrency. I doubt President Trump will let them collect fees.

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $42.73) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $2,351.93) also rallied sharply after the ceasefire. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

iShares Ethereum Trust (ETHA- $17.82) remains the cheapest and easiest way to buy ethereum. ETHA is a Buy for the coming explosion in token-funded start-ups.

Primary Risk: Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $89.94

In the last two weeks, oil has been as high as $117.63 and as low as $86.96. Oil drops whenever it looks like a ceasefire is likely, then shoots back up as hopes fade. But here’s the thing – it doesn’t matter. The damage is done. Saudi Arabia said strikes on its energy infrastructure crimped flows through an East-West pipeline the kingdom has been using to export crude via the Red Sea. The attacks cut output capacity by more than 600,000 barrels a day and reduced the pipeline flows by 700,000 barrels a day. The Strait of Hormuz’s near-closure since the end of February has disrupted a fifth of global oil and liquefied natural gas flows, triggering a severe supply shock.

Countries heavily reliant on Middle Eastern supplies, including Japan, have begun tapping inventories. Prime Minister Sanae Takaichi said they will release about 20 days of oil from their stockpiles in May. In China, state refiners were given the green light to tap into commercial reserves, while India’s largest private refiner has started to cap fuel purchases at pumps to manage stocks.

There are about 13 million barrels a day (b/d) of crude oil production shut-in now. The breakdown: Iraq 4 million b/d, Kuwait 2.4 million b/d, Bahrain 0.18 million b/d, UAE 1.8 million b/d, Saudi 4.5 million b/d . The shut-in is massive. I think one crazy thing to note is that none of the oil specialists are disagreeing with each other on the math. The reason for that is because the outage is so large, 1 to 2 million barrels won’t matter all that much. During normal times, 1 to 2 million barrels is the difference between $50 WTI and $75 WTI.

The December quarter of 2018 was widely considered to be one of the tightest quarters in history because the deficit was 1.6 million b/d. Oil markets have never had a deficit larger than 3 million b/d. In 2022, markets started pricing in a structural 2 million b/d deficit, oil spiked, and equity markets sold off. Now, people are talking about a sustained 5 million b/d deficit as somehow being manageable? No. That’s not how the oil market works. Because oil is traded on the margin, that last barrel would push prices to the extreme. We are eating into onshore oil inventories now, and the market is still asleep.

Before the war, the world was producing about 100 million barrels of oil a day, and consuming about 100 million barrels of oil a day. Now the world is producing somewhere between 85 million and 90 million barrels of oil a day. That means somebody has to stop consuming 10 million to 15 million barrels of oil a day. But while the oil market needs demand destruction, politicians have other plans because they want to be re-elected. For example, German Chancellor Friedrich Merz said that gasoline and diesel taxes will be cut by 17¢ per liter for two months to cushion the blow to drivers.

The market has a very efficient way to get to this reduced level of demand. It raises the price, forcing marginal buyers to stop consuming oil. But if government subsidize the current high price of oil, the demand does not change and the market price has to go even higher in order to get that demand destruction.

Will US shale drillers step up to solve the crisis? Nope. We’ve now had more than a month of elevated oil prices, yet the Baker Hughes Oil and Gas Rig Count has not budged, with the number of active rigs actually ticking down by three to 545 for the latest available week (ending April 10).

In my view, here is the biggest misconception in the oil market today. Generalists are looking at it from Strait of Hormuz traffic flows while oil specialists are looking at production shut-ins. Generalists are saying, “Well, if there’s a peace agreement or tanker starts to come back, everything will be fine.”

Oil specialists are saying, “No, shut-in barrels are barrels that will be replaced via lower storage volumes elsewhere. Tanker availability delays production shut-in returning by one or two months. Over one billion total barrels are lost.” I don’t think it’s anything more complicated than that, so the only way to change sentiment is for widespread fuel outages. Coming soon to Europe and Asia, ex-China.

The September 2027 Crude Oil Futures (CLU7.NYM – $72.27) are a Buy under $75 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $49.70) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $12.46) announced strong first quarter 2026 production, an asset acquisition and the award of new land concessions in Germany, and the divestment of a non-producing asset in Croatia.

March quarter production averaged approximately 125,000 barrels of oil equivalent per day (boe/d), above the top end of their quarterly guidance range of 122,000 to 124,000 boe/d. Production was comprised of approximately 59% Canadian gas, 13% European gas, and 28% liquids. European gas production realized an average sales price of approximately $16 per million British thermal units (MMBtu). They are on track to bring on new production from the first Wisselshorst well in Germany by mid-2026, spud the next Netherlands well in the second half of 2026, and spud follow-up Germany Wisselshorst wells on the Bommelsen license in early 2027.

They are acquiring assets in Germany that are currently producing approximately 1,000 boe/d of low decline production (85% natural gas) with an effective date of January 1, 2025. These assets are adjacent to their existing operations and offer future European natural gas development upside. The acquisition is expected to close in the second half of 2026.

In addition, they added three concessions in the North German Basin that offer potential upside for their deep gas exploration program. These new concessions are adjacent to existing Vermilion acreage in Germany and double Vermilion’s acreage in the country to well over 1 million net acres.

Finally, they are selling their remaining 60% interest in a block in Croatia for $24 million. The asset has no production. The proceeds will be primarily used for incremental debt reduction, with the sale expected to close in the second half of 2026. They continue to produce and generate excess free cash flow from their SA-10 block (100% natural gas) in Croatia.

VET is a buy under $11 for a target price of $24 or more.

Primary Risk: Oil and natural gas prices fall.

Energy Fuels (UUUU – $20.93) moved up on barrage of uranium news. Rolls-Royce secured $814 million from Britain’s national wealth fund to develop the U.K.’s first small modular reactors. The U.K. government approved the development of three SMRs at the Wylfa site in North Wales. The BBC reported that the three units have a total output capable of powering ~3M homes for over 60 years.

Amazon-backed X-Energy, a designer of small modular reactors and manufacturer of nuclear fuels, said Wednesday it is targeting a valuation of up to $7.5 billion in its IPO.

The US government unveiled the National Initiative for American Space Nuclear Power, a sweeping initiative to bring nuclear energy technology into space. It is a joint NASA–Pentagon strategy to develop nuclear power systems capable of supporting future lunar and interplanetary missions. The initiative aims to deploy a 20 kilowatt space reactor, code named “SR-1 Freedom,” for interplanetary propulsion and surface power.

Canaccord Genuity issued a bullish report on the uranium sector as a “high-beta sector [that] should be a beneficiary of the increased focus on energy security which is not being reflected in stocks.”

CEO Mark Chalmers, who has done a great job of repositioning the company, is retiring. He will be a uranium and rare earth consultant to the company for two year. Ross Bhappu, Energy Fuels’ President since August 2025, is the new CEO. He is totally qualified to execute Chalmers’ vision for the company. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

EQT (EQT – $58.39) expects to report a total loss on derivatives of $238 million for the March quarter. They were unhedged as of the end of last year, so this must be some first quarter gas sales that got squeezed by the war.

The North American rig count is sitting near decade lows (outside of Covid-19), 15% to 20% of the global supply of LNG has been more or less blocked for a month, and AI compute along with energy usage continues to go vertical. Yet here we are with natural gas prices across the futures curve at four-year lows. Pretty remarkable and not something anyone would have predicted.

Yet EQT will be a bigger beneficiary of the Mideast energy disruption than any oil company, for two reasons. First, the Strait of Hormuz is the main export route for liquefied natural gas from the South Pars-North Dome field, a reservoir shared by both the nations of Qatar and Iran that contains nearly one-fifth of the world’s discovered natural gas. It is the single most important gas basin on Earth. About 20% of all LNG from the South Pars-North Dome field goes through the Strait of Hormuz.

Second, over the past 30 years, Qatar has invested $200-$300 billion to build the Ras Laffan Industrial City, fed by gas from the South Pars field. It is the largest gas liquefaction complex in the world. A month ago, Iran’s missiles hit 2 of the 14 liquefaction units at Ras Laffan, taking out 17% its capacity or 12.8 million tonnes a year. QatarEnergy’s CEO has indicated that these units will likely be offline for three to five years.

Why so long? Because before it can be transported, natural gas has to be liquefied in a cryogenic brazed aluminum heat exchanger. QatarEnergy’s two destroyed heat exchangers can’t be repaired, but must be replaced. All five heat exchanger manufacturers are back-ordered two to four years due to the existing demand for the largest LNG buildout in history. It will take even more time to install them and get them running.

While global gas prices have spiked due to the shutdown of the Strait of Hormuz, shale drillers have insulated the US economy from an energy crunch. With US gas production up 4% year-over-year, abundant supply has kept prices contained at just $2.60 per thousand cubic feet (mcf), while Europe and Asia are paying closer to $20 per mcf. This is not only shielding US consumers from higher energy costs, but it’s also boosting American industry by providing cheap feedstock for producing fertilizers, plastics, and other petrochemicals. EQT is a buy under $70 for a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

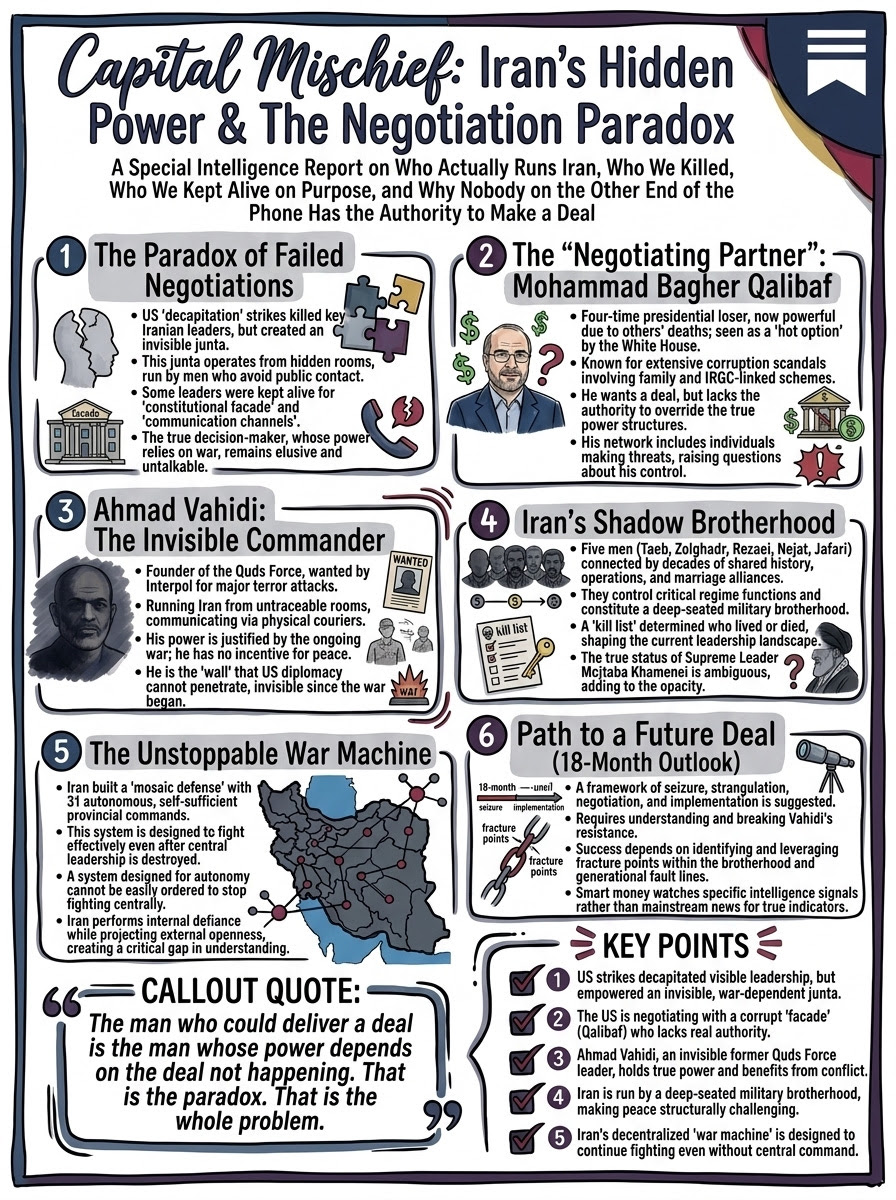

One quote that explains the entire Iran war. The negotiating partner who cannot negotiate. The invisible commander who will not. The brotherhood nobody elected. The war machine nobody can turn off. And the 18-month path to a deal that does not exist yet.

Click for larger graphic h/t Capital Mischief – Charlie Garcia

Click for larger graphic h/t Capital Mischief – Charlie Garcia

* * * * *

Click for larger graphic h/t Tom Kane

Click for larger graphic h/t Tom Kane

Your reading the most important medical story of the decade Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 4/16/26. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $263.40) – Buy under $205

Gilead Sciences (GILD – $138.55) – Buy under $115, first target price $150

Meta (META – $675.87) – Buy under $705 for a long-term hold

Nvidia (NVDA – $198.35) – Buy under $200 for a long-term hold

Onsemi (ON – $79.93) – Buy under $60, first target price $130

Palantir (PLTR – $142.76) – Buy under $160 for $200 first target price

PayPal (PYPL – $49.81) – Buy under $50, target price $150

Snap (SNAP – $6.02) – Buy under $11, target price $17+

Small Tech

Enovix (ENVX – $6.54) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $65.92) – Buy under $75; 3- to 5-year hold

Fastly (FSLY – $24.88) – Buy under $10 for a 3- to 5-year hold to $50+

PagerDuty (PD – $6.41) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $12.40) – Buy under $10, target price $40

ARK Venture Fund (ARKVX – $50.03) – Buy for SpaceX IPO

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.83) – Buy under $6, target $30+

Akebia Therapeutics (AKBA – $1.35) – Buy under $4, target $20

Compass Pathways (CMPS – $6.66) – Buy under $10, hold a long time for a 20x return

Editas Medicines (EDIT – $3.35) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $1.16) – Buy under $5, hold a long time

Medicenna (MDNAF – $0.44) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.05) – Buy under $2.50, target price $20, then $50

TG Therapeutics (TGTX – $34.30) – Buy under $30 for buyout at $40+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($78.89) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $80.29) – Buy under $50, target price $75

Sprott Junior Gold Miners ETF (SGDJ – $95.43) – Buy under $60, target price $100

Sprott Physical Gold and Silver Trust (CEF – $49.61) – Buy under $35, target price $60

Global X Silver Miners ETF (SIL – $97.18) – Buy under $60, target price $100

Coeur Mining (CDE – $19.51) – Buy under $10, target price $20

Paramount Gold Nevada (PZG – $1.79) – Buy under $1, first target price $10

Royal Gold (RGLD – $262.13) – Buy under $180

Cryptocurrencies

Bitcoin (BTC-USD – $75,146.29) – Buy

iShares Bitcoin Trust (IBIT – $42.73) – Buy

Ethereum (ETH-USD – $2,351.92)– Buy

iShares Ethereum Trust (ETHA- $17.82) – Buy

Commodities

Crude Oil Futures – September 2027 (CLU7.NYM – $72.27) – Buy under $75; $200+ target

United States 12 Month Oil Fund, LP (USL – $49.70) – Buy under $40; $100+ target

Vermilion Energy (VET – $12.46) – Buy under $11; $24+ target

Energy Fuels (UUUU – $20.93) – Buy under $18; $30 target

EQT (EQT – $58.39) – Buy under $70; hold for much higher prices ($100+)

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

SoftBank (SFTBY – $14.87) – Hold

Dakota Gold (DC – $5.83) – Hold for higher gold prices

First Majestic Mining (AG – $21.05) – Hold for higher silver prices

Freeport McMoRan (FCX – $68.28) – Hold for higher copper prices

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2026

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1st

That’s fast!

MM the word on the street is that Butler from akba wants to throw out another couple hundred million shares wants to up share count to 500 million,hopefully he doesn’t get approval from share holders but you know he will,hopefully it’s just hear say