Dear New World Investor:

Inflation and payrolls are up, so the Fed will stay on hold. Wednesday’s May Consumer Price Index report surprised no one. The headline year-over-year increase of 4.2% was the highest since April 2025, with more than 60% of the 0.5% monthly increase from April due to energy prices. The core CPI increase, excluding food and energy, was up 2.9% from May 2025 and 0.2% from April.

Click for larger graphic h/t Yahoo Finance

The problem with the core number is that while direct higher energy costs are excluded, they leak into other costs like transportation, plastics, and so on. These ripple effects will keep core inflation well above the Fed’s 2% target.

At the same time, the April Job Openings and Labor Turnover Survey (JOLTS) report and May payrolls report made it clear that the Fed is past their peak worry about the labor market. Job openings surged in April to reach 7.62 million positions, their highest level since May 2024 and well above the 6.87 million consensus for the month, roughly on par with March’s revised level of 6.89 million.

The Job Openings-to-Unemployed ratio rose to 1.033 in April, the first reading since June 2025 that was above the critical 1.0-threshold (orange line). Interestingly, the ratio registered a 0.119 advance from February (pre-Iran War) to April (post-Iran War). Pandemic aside, it was the largest gain over any two-month period on record.

Click for larger graphic h/t @DiMartinoBooth

Click for larger graphic h/t @DiMartinoBooth

The economy added 172,000 jobs in May, blowing past expectations for 88,000 jobs. April’s jobs report, originally a huge beat at 115,000, was revised up to show an even better 179,000 jobs gained. March’s payroll growth was also updated from +185,000 to +214,000, the first monthly gain above 200,000 since early 2024. Economists estimate that the economy needs to create only zero to 50,000 jobs per month to keep up with growth in the working-age population.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

As you may remember, my rule of thumb is that three straight months of downward or upward revisions to nonfarm payrolls signals a cycle inflection. The labor market is gaining traction after stumbling last year, which gives the Federal Reserve more room to keep interest rates unchanged in the face of rising inflation due to the Iran war.

In response to the solid payrolls report last Friday, the stock market staged a mini-crash. As usual, investors will focus on the better-than-expected outlook one day and worry about sticky interest rates the next day. Sooner or later, they will realize that:

The economy can do OK with the current level of interest rates, there is plenty of opportunity for companies to make money, and the Fourth Industrial Revolution, which is defined by the blurring lines between the physical, digital, and biological spheres and driven by artificial intelligence, robotics, and biotechnology, is going to be the biggest wealth creator of all time.

President Trump is trying to change the narrative about interest rates to “higher is always bad for any reason,” and “lower is always good for any reason.” But that is not correct. If rates go to 6% because of a strong economy, with good corporate earnings and a low unemployment rate, it will be a good thing. If rates go to 6% driven by accelerating inflation, it will be a bad thing. The why matters more than the level when it comes to interest rates. The worst choice is to use government and monetary policy to force interest rates too low. That creates speculative excesses and malinvestment every time, which often ends in tears.

Market Outlook

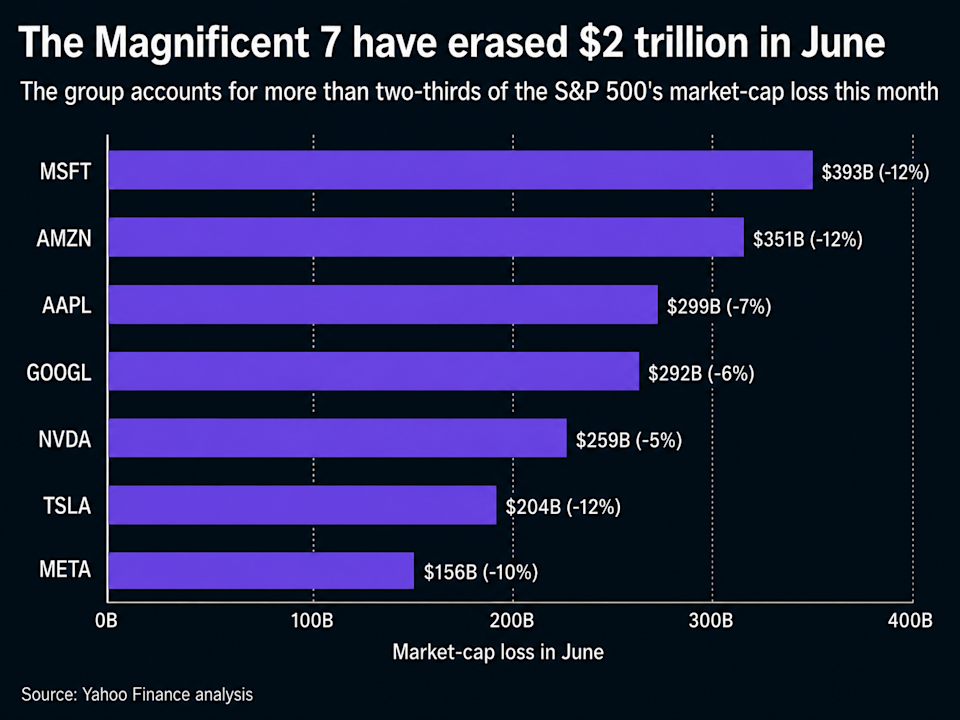

The S&P 500 lost 2.2% over the last two weeks, but the Index is still up 8.0% year-to-date. The Magnificent Seven are down a median 9.7% in June, while the rest of the S&P 500 has a median gain of 0.3%. That split helps explain why the Index feels heavy even though many stocks are still holding up. The Seven (Microsoft, Amazon, Apple, Alphabet, Nvidia, Tesla, and Meta) have lost about $2 trillion in market value this month.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

But the overall S&P 500 Index has reached an all-time high 23 times in 2026, according to Creative Planning chief market strategist Charlie Bilello. It crossed above 7,600 for the first time for its latest high. A year ago, it was at 5,900. Five years ago, it was at 4,200. And 10 years ago, it was at 2,100.

From its inception in 1957 through today, the S&P 500 has hit 1,328 all-time highs, per Creative Planning. That means the S&P 500 has hit a new high once every 19 days on average.

Artificial Intelligence-driven earnings growth is increasingly shaping the trajectory of the Index, according to Evercore ISI, as a small group of technology-focused companies continues to exert an outsized influence on the benchmark index. So the question is: Are we in an AI revolution or an AI bubble that will pop soon?

Corporate earnings and outlooks are strong, and there are other reasons to believe there is no stock market bubble. First, the number of initial public offerings (IPOs) remains below average and well below prior cycle peak, although today’s SpaceX IPO might open the floodgates.

Click for larger graphic h/t Goldman Sachs

Click for larger graphic h/t Goldman Sachs

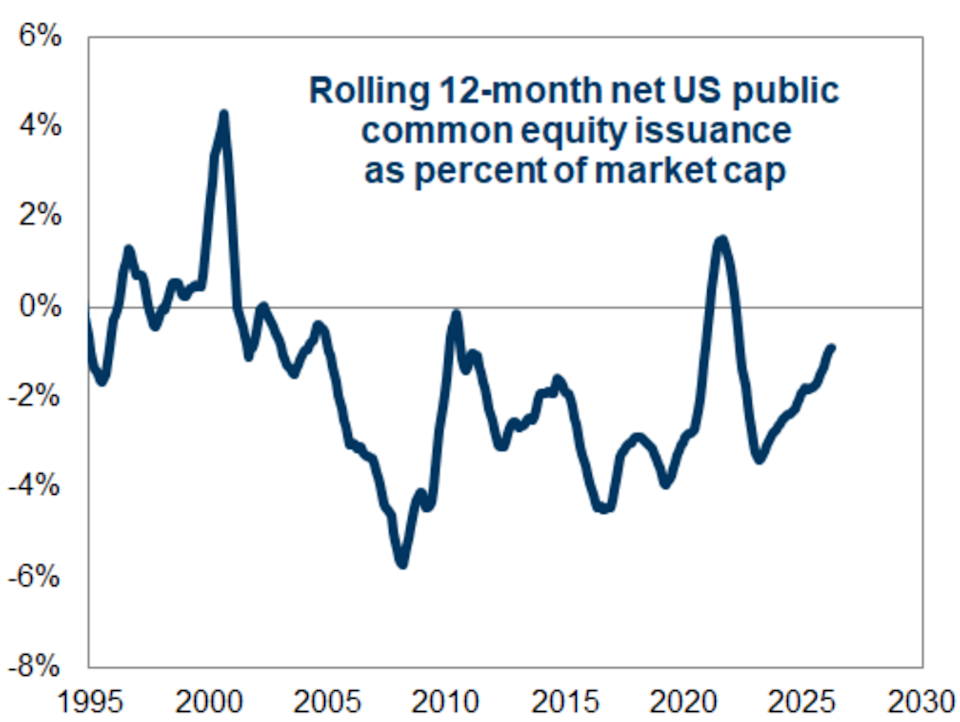

Second, net US public equity issuance has increased but is below past peaks.

Click for larger graphic h/t Goldman Sachs

Click for larger graphic h/t Goldman Sachs

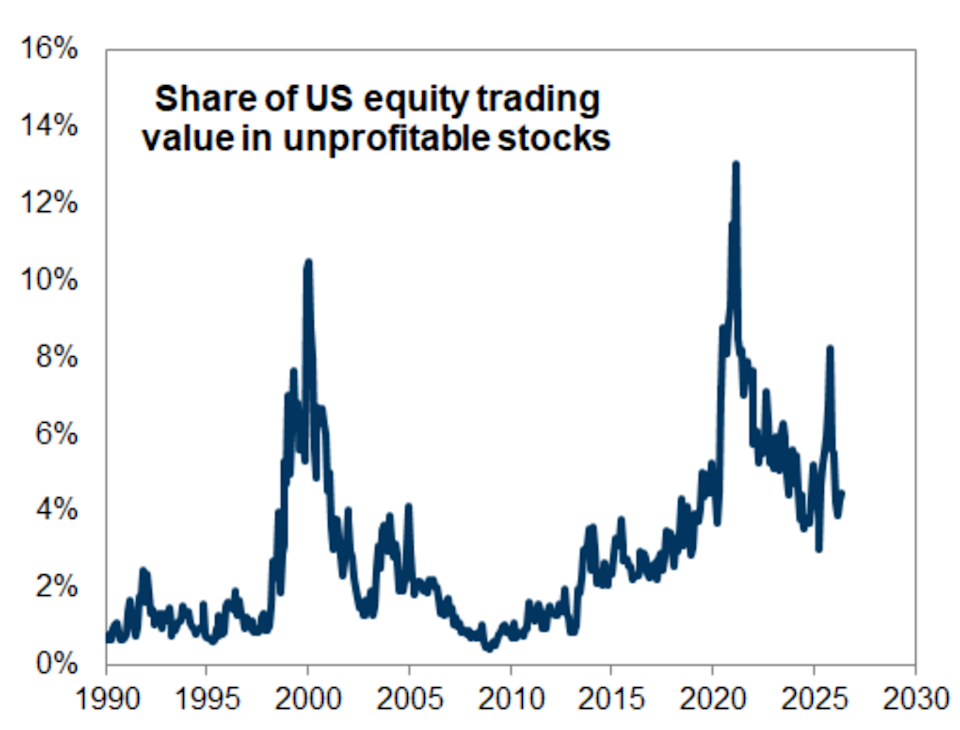

And third, the share of trading activity in unprofitable stocks remains well below past extremes, notably including the dotcom bubble.

Click for larger graphic h/t Goldman Sachs

The Nasdaq Composite lost 4.1% due to the Mag 7 weakness. It is up 11.0% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 2.4%, but is still up 8.9% year-to-date. The small-cap Russell 2000 remains the standout, dropping only 0.5% and booking a 17.7% gain in 2026.

Can sentiment get too bullish? Of course. Will stocks drop after sentiment gets too bullish? Of course. Will the uptrend then resume to 2036? You bet. Will you stay invested, ride out the dip, and make bank on the big uptrend? Up to you.

Click for larger graphic h/t @Mayhem4Markets

Click for larger graphic h/t @Mayhem4Markets

Top 5

Changes this week: None

Near-Term – chronological order

INO Inovio – bounce back from equity offering + FDA allows 6-month review of INO-3107

AKBA Akebia Therapeutics – Vafseo launch

BTC-USD Bitcoin – rebound from sell-off

ETH-USD Ethereum – rebound from sell-off

EQT EQT – natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model June quarter real GDP forecast ticked up to +3.3%, and even the Blue Chip economists have steadily increased their consensus estimate to +2.0%. But notice that the GDPNow forecast is still above the average of the top 10 Blue Chip forecasts.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, June 15

AG – First Majestic – Through 6/16 – 121 Mining Investment New York

Tuesday, June 16

SNAP – Snap – 12:30pm – Augmented World Expo (AWE) USA keynote address

Wednesday, June 17

Fed Meeting – 11:00am press release; 11:30am press conference

DC – Dakota Gold – 11:30am – Planet MicroCap Conference

RGLD – Royal Gold – 2:00pm – Renmark Financial Communications Virtual Non-Deal Roadshow

Friday, June 19

Markets Closed – Juneteenth

Sunday, June 21

Summer Solstice – 10:24am

Tuesday, June 23

SFTBY – SoftBank – 9:00pm – Annual Meeting

Wednesday, June 24

NVDA – Nvidia – 12:00pm – Annual Meeting

UUUU – Energy Focus – 12:00pm – Annual Meeting

Thursday, June 25

March Quarter GDP – 8:30am – Third estimate

Personal Consumption Expenditures Index (PCE) – 8:30am

SCYX – ScyNexis – 9:30am – Annual Meeting

Short Interest – After the close

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $295.63) unveiled its long-delayed AI-powered version of its Siri digital assistant at its annual Worldwide Developers Conference (WWDC). Siri AI includes a variety of upgrades enabling users to have back-and-forth conversations and complete tasks. That bring it closer to AI helpers like ChatGPT and Google’s Gemini, which isn’t surprising because it is powered by Gemini. That means Apple is giving up some of its beloved control over both the hardware and the software experience.

So when the upgrade ships this fall, you’ll be able to ask when a band you like is performing nearby. Siri will then provide you with upcoming tour dates, set a reminder for them, and let you ask to play a single by the band. You’ll also be able to ask Siri for pictures you’ve taken at different locations, then further narrow down your search to particular scenes you’re looking for without having to open the Photos app. You’ll be able to ask Siri questions about topics friends and family send via Messages and get the information you need without having to endlessly scroll through your chats.

You’ll also be able to access Siri via your camera, letting you take a picture of a meal to get nutritional information, or snap a shot of a dinner bill and split it with your friends. Writing Tools will allow you to write documents with Siri by giving it a prompt, and ask it to critique your writing.

Citi Research wrote: “Apple is uniquely positioned to capitalize on the edge AI inflection given its over 2.5 billion installed base and its tightly integrated ecosystem spanning custom silicon, software and services. We believe a meaningfully upgraded Siri will be a key to unlock the agentic AI potential. Early indicators such as strong demand for Mac Mini, driven by emerging agentic AI use cases like OpenClaw, highlight how edge AI is already beginning to drive incremental hardware demand, even as adoption has yet to extend to the broader iPhone and iPad installed base. Beyond hardware, it also points to a meaningful services opportunity. As agentic AI capabilities mature, Apple could monetize through higher-value software layers, developer tools, and AI-driven services embedded across its ecosystem.”

AAPL is a Buy under $205.

Gilead Sciences (GILD – $125.87) and Merck announced that the primary efficacy endpoint at Week 48 was met in both the Phase 3 ISLEND-1 and ISLEND-2 trials. The oral once-weekly single-tablet HIV treatment regimen of islatravir 2mg/lenacapavir 300mg was generally comparable to the comparator regimens with no new safety concerns. Gilead and Merck plan to file the Phase 3 data with regulatory authorities globally. Gilead said that long-acting oral therapies represent a new wave of transformational innovation in HIV drug development, with the potential to reshape the landscape of care.

Continuing their recent string of clinical trial wins, the company announced positive results from a Phase 3 trial in people with primary biliary cholangitis (PBC), showing that treatment with Livdelzi (seladelpar) led to significantly more patients with inadequately controlled disease achieving normalization of alkaline phosphatase (ALP), a key liver marker of disease progression, compared with placebo after 52 weeks.

At the Goldman Sachs Global Healthcare Conference (WEBCAST HERE and TRANSCRIPT HERE), CEO Daniel O’Day said: “I would say this is a really important time for Gilead. It’s really just watching our strategy play out over the past 7 years. And what that means is kind of consistent commercial clinical execution, and we have the most robust pipeline that we’ve ever had in Gilead’s history.”

True. GILD is a Long-Term Buy under $115 for a first target of $150.

Meta Platforms (META – $568.43) has a $201 billion revenue run rate and a market capitalization of $1.6 trillion. SpaceX has a $19 billion revenue run rate and a market cap of $1.8 trillion at the IPO price. Meta currently trades at a discount due to founder control because people don’t like Zuckerberg. There aren’t many entrepreneurs who took a company from a start-up in their dorm room to over $200 billion in revenues. Could the market start assigning a premium to Zuck’s company, as it does with Musk’s SpaceX and Tesla?

With Meta being the cheapest of the Mag7, I think a simple market re-rating could drive 25%-100% upside. All that is needed is a change in market sentiment towards Zuckerberg. Meta’s new AI-powered Meta One subscriptions and small-medium business (SMB) targeting could be the catalyst triggering a premium valuation as they demonstrate a significant return on their capital spending. Listen to the company’s head of AI on winning the AI race:

At the annual meeting, after the legal boilerplate Zuckerberg gave a seven minute overview presentation starting at 41 minutes 56 seconds (CLICK HERE) followed by a Q&A. META is a Buy under $705 for a long-term hold.

Nvidia (NVDA – $204.87) made a number of presentations, including a GTC Taipei 2026 Keynote by CEO Jensen Huang:

(WEBCAST ALSO HERE and SLIDES HERE), a GTC Taipei 2026 Financial Analyst Q&A (WEBCAST HERE), and a presentation by CFO Colette Kress at the BofA Securities Global Technology Conference (WEBCAST HERE and TRANSCRIPT HERE).

Jensen was in fine form, saying that the recent selloff in U.S. semiconductor stocks should be viewed in the context of a much larger trend, stating that: “We are at the outset of the AI revolution. We’re at the beginning of the AI Supercycle, and whatever happened to the stock market, you should be very happy because now you can buy at a discount. Everybody should be very excited. It is a foregone conclusion that AI will be infrastructure for the world, just like the internet was infrastructure for the world.

“Only for the last six months has the ROI been completely reset. It is now insanely profitable. Remember last year when we were together, the rhetoric and the narrative around the investment were, ‘What’s the ROI?’ Give me one example of some crazy person saying that now. They’re going to sound insane.”

He unveiled a PC superchip at the GTC Taipei event that rivals chips from Intel and AMD. The RTX Spark superchip for Windows laptops includes a Blackwell GPU and the ARM-based Grace CPU. It will power laptops and small desktops from manufacturers including ASUS, Dell, HP, and Microsoft when it lands this fall. It is meant for customers running AI agents, content creators, and gamers. The laptops will be roughly 14 millimeters thick, include HD webcams, and have all-day battery life. Nvidia said it has been working with Microsoft and software developers to ensure that their programs can run on the chip.

In addition to debuting the RTX Spark, Nvidia announced that its Vera data center CPU is now in full production and that Vera-only rack servers will be available this fall.

AI is only accelerating in terms of use cases and importance to organizations. At the conference, Jensen said: “There are going to be so many agents, the world is no longer limited by the number of people. Those agents are going to use more tools than ever. Every company will have agents running inside. Every company will see that agents will need its own operating system. Every company is asking us, ‘How do we run agents safely? How do we build agents for our own workloads?’”

MIT professor Daron Acemoglu estimated that only about 5% of tasks will be profitably performed by AI over the next 10 years, boosting US GDP by 1%. I think he’s way low. Nearly 20% of all tasks in the US labor market eventually could be replaced or augmented by AI.

Jensen said that the company has secured enough supply to meet robust growth for both CPUs and GPUs amid the ongoing AI boom, but “We have supply for very, very robust growth, but we’re still supply constrained.”

NVDA is a Buy for a $225 first target.

Onsemi (ON – $115.96) introduced an industry-first Elite Pairing Studio to simplify power design. It is an interactive simulation tool that gives engineers visibility into device-level behavior and pairing trade-offs, accelerating power electronics design. It helps engineers by analyzing device combinations and recommending well-matched Onsemi silicon carbide (SiC) MOSFET and gate driver pairings based on their system requirements.

They also announced the launch of GaNEXUS, a new gallium nitride (GaN) power portfolio engineered to deliver higher efficiency, greater power density, and improved thermal performance across AI data centers, industrial automation, robotics, and energy infrastructure applications. The GaNEXUS power portfolio delivers faster switching speeds, lower switching losses, higher power density, and improved thermal performance for next-generation power architectures.

CEO Hassane El-Khoury and CFO Thad Trent presented at the BofA Global Technology Conference (WEBCAST HERE and TRANSCRIPT HERE). Hassane said: “At a high level, a lot of people, even going through last year, they kept pressuring us, well, when are you going to call the bottom, or is it the bottom or when is the recovery and so on. And I’ve always said, I’ll call it when we see it. So when we saw, it was in the first quarter, and both Thad and I talked about the signals that we’re looking at, and it’s not just one signal. You can think about it as a whole slew because they’re all interlocked.”

ON is a Buy under $60 for a $130 first target.

Palantir (PLTR – $131.08) held their 10th AIPCon featuring, as usual, customer-led demos of Foundry, AIP, Ontology, and Apollo in production across leading organizations — many of whom were sharing their work publicly for the first time — including Kirkland & Ellis, McCarthy Building, the US Department of Agriculture, Hertz, Nscale, Accenture, Parts Town, and others.

The USDA showed how the Ontology now underpins national food supply security. They said: “Pointing an LLM at hundreds of disconnected, ungoverned databases gets you a system that hallucinates, is insecure, and unauditable. For something as consequential as our nation’s agricultural data, that is not just useless — it’s dangerous. The Ontology has been the key to delivering AI-enabled technology to every farmer in the country.”

CEO Alex Karp shared Palantir’s secret to sales: “We’re hoping that you’ll go to a large language model company and learn that they don’t care about you at all. What you will find is there are a myriad of problems that these very important models solve, and there are even bigger problems that they create. We’re in the business of giving you the ability to solve those problems for yourself and own the means of production.”

Alex did an interview on CNBC and dumped on the big AI model companies because don’t actually understand how businesses work. He said: “They believe all problems — present, past, and future, including the ones they create and don’t acknowledge they create — are going to be solved by them, including human nature and disparities. Enterprises are just fed up because they know this doesn’t actually work this way. It’s not working. And that basically drives our commercial business. Most of the things Anthropic talks about in public are running on Palantir.”

PLTR has fallen over 30% in the last six months. This is a generational gift – accept it! PLTR is a Buy under $160 for a $200 first target.

PayPal Holdings (PYPL – $41.24) presented at the Evercore Global TMT Conference (WEBCAST HERE and TRANSCRIPT HERE). Chief Technology Officer Srinivasan Venkatesan said: “Even before I walked into PayPal, when I was intervened for the role, I wanted to make it clear that like we had put all technology under one roof. That had never happened at PayPal.”

Adam Frisch, the Evercore analyst, said: “I think the prevailing sentiment out there is that PayPal has a considerable amount of technical debt. Whether it’s database integrity, latency issues, prior acquisitions that weren’t fully integrated, et cetera. Is this an accurate perception in your view? Or is there some clarity that you can offer on the internal tech deck, and then we can discuss the external.”

Srinivasan replied: “Our identity infrastructure was kind of fragmented or I would not say fragmented. We had multiple versions of identity. And what it meant was you onboard on one product and you try to onboard on a different product would create a lot of friction. You would have — as if we had omnishare about the customer, and you have to do the same thing again. So that was the same case with the rest and compliance platforms and so forth. So you can collect that debt like we had multiple versions of it, which means we had to build it 3x or we had to maintain it 3x.

“We are now embarking on a journey to completely go cloud native on our PayPal platform. So that’s the second way of how we are addressing the technical debt right now. Braintree and Venmo, we have already made it cloud native and they are already up and running in the platform. So now we are now tackling PayPal right now. I see it at least it takes a couple of years. The reason is there is stored migration, and then we are also changing the engines on the fly, while we are operating this huge payment network across multiple countries. So the data migration is going to be the one. It takes a while. That’s the tricky part. You can’t mess that up.”

The company’s stock buyback program remain aggressive due to their free cash flow strength. So far, increasing cash flow has been driven by shrinking capital spending rather than operational growth, but I think that is about to flip. This is a good time to buy the stock because the valuation is attractive with a forward P/E of 8.44x and their core assets can support global expansion. PYPL is a Buy under $50 for a triple in three years.

Snap (SNAP – $5.33) introduced new optimization and app measurement capabilities called Unified Attribution. It accounts for multiple touch points across the buyer journey, aligning closely with Mobile Measurement Partners (MMPs), to help app advertisers evaluate and make real-time campaign optimization decisions with more confidence to really drive business growth. SNAP is a Buy under $11 for a $17+ target.

SoftBank (SFTBY – $21.75) passed Toyota to become Japan’s most valuable company for the first time in over two decades. They’ll hold their annual meeting on June 24 and will take online question HERE, even from non-sharehlders, until 4:00am EDT on June 22.

CEO Masayoshi Son said he thinks the AI boom will likely be 50 times bigger than the rise of the internet at the turn of the century. He said: “I think this is like more than 10x, probably 50x bigger than dot-com. This is the biggest revolution of technology and realization that mankind ever experienced, so this is just like the beginning of the internet.”

Hold SFTBY for a first target of $50 and then higher as the discount to hard book value disappears.

Small Tech

Enovix (ENVX – $6.70) attended Japan Drone 2026. They said they had great conversations with drone OEMs and integrators, who kept circling one point: as drones gain autonomy, endurance and discharge capability are becoming operational priorities, not specs. It’s why they built MX-1 for aerial drones. I’d like to see some orders! ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

First Trust NASDAQ Cybersecurity Exchange-Traded Fund‘s (CIBR – $85.47) valuation remains reasonable at a 24x P/E and a P/E-to-Growth (PEG) ratio near 1.0, supporting its secular growth thesis despite concentrated tech exposure. Seasonality also favors CIBR, with June through August historically delivering strong returns, reinforcing the bullish outlook into summer. CIBR is a Buy up to $75 for a 3- to 5-year hold as the need for cybersecurity gets stronger and stronger at every level of society.

Primary Risk: A technology emerges to stop hackers.

Fastly (FSLY – $18.88) presented at the William Blair Growth Stock Conference (WEBCAST HERE and MARCH QUARTER SLIDES HERE and TRANSCRIPT HERE). CFO Richard Wong pretty much repeated the recent March quarter earnings call.

The company said that analysis of traffic across their global network found that AI requests grew approximately 30% between January and May 2026, which is about 6.5x faster than human traffic during the same period. The more significant shift is how AI systems interact with digital infrastructure: while stopping bad bots remains important, organizations increasingly need to think and act strategically to capture the growing value from automated interactions.

Machine traffic now represents a significant share of Internet activity, including AI crawlers, AI fetchers, bots, agents, and API-driven systems. AI fetchers and agents are becoming increasingly important, as AI assistants retrieve real-time information to answer questions, compare options, validate facts, and complete tasks on behalf of users. The challenge is no longer simply blocking bots, it’s understanding which machine interactions should be accelerated, managed, challenged, or stopped.

The three foundational elements of an effective machine traffic strategy are (1) visibility into which AI systems are interacting with digital properties, (2) context around how those systems behave and whether they create business value, and (3) the precision to respond differently based on intent and impact.

Fastly helps customers execute that machine traffic strategy at the edge. In the path of every request, Fastly delivers the visibility, context, and precision required to balance performance, security, bot management, and origin access with real-time intelligence. FSLY is a Buy under $10 for a 3- to 5-year hold to $50+.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $8.77) presented at the BofA Global Technology Conference (WEBCAST HERE and TRANSCRIPT HERE). CEO John DiLullo was there with former CEO and now Executive Chair of the Board Jennifer Tejada. The analyst asked Jen, who clearly was fired: “Why did you feel now is the right time to make this succession?”

Jen played nice and said: “Thank you for the question. Well, now is the right time because of really two things. One, we felt that we’ve stabilized the retention – some of the retention challenges that we’ve seen in the business. And we’re starting to see growth levers accelerate. So whether you look at 5 consecutive quarters of more than 600 new logos, starting to see some of the green shoots that we’re seeing through our pricing transition going from a seat-based pricing model to a platform and usage-based pricing model, things in the business were starting to really point in a positive direction. And that gave the Board and I comfort provided we could find a great leader that we felt would be the right person to lead the company.”

Well, maybe. The transition from seat-based to usage-based pricing amid flat revenue and slowing growth is not easy. DiLullo needs to manage it while finding revenue growth. The company’s Operations Cloud annual recurring revenue (ARR) nearly doubled sequentially, but only a small fraction of clients have adopted the new model, creating near-term disruption.

On the plus side, profit margins and free cash flow have improved, with four consecutive GAAP-profitable quarters and a strong balance sheet supporting ongoing investment. The competitive risks from hyperscalers and platform vendors persist, but PagerDuty’s platform strategy and customer growth, especially among AI-native firms, offer long-term promise. PD remains a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $21.80) will be added to the broad-market Russell 3000 Index and the small-cap Russell 2000 Index on June 29 as the market opens. There should be some upward pressure as the Russell Index funds buy the stock. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

ARK Venture Fund (ARKVX – $52.56) will jump tomorrow and next week as SpaceX goes public at $135 a share – a market capitalization of $1.77 trillion. It’s the largest IPO in history, and even though Elon Musk wants 30% of the stock to go to retail accounts, it will be hard to get an allocation. Goldman, Morgan Stanley, and 19 other banks have already carved it up. The IPO is well oversubscribed with more than $250 billion of investor demand for the $75 billion deal. (This is a normal ratio for a high demand IPO. 4x-5x demand is kind of the standard for the hot ones. Don’t let headlines over-dramatize this.)

I greatly admire what Elon Musk has accomplished. He deserves to be the world’s first trillionaire. But would I buy SpaceX at 95x sales? Nope.

OpenAI, ARK Venture Fund’s second-largest holding, said it filed confidential paperwork for an initial public offering (IPO), setting up one of the most anticipated market debuts in years. The company said it hasn’t decided on timing yet, and that it may take a while “because there are things we want to do that are likely easier as a private company.”

The announcement sets up a showdown with rival Anthropic, which filed confidential paperwork for its own IPO last week. Anthropic used to be the also-ran in the AI race. But the company announced it had raised $65 billion at a valuation of $965 billion, ahead of OpenAI’s March valuation of $852 billion, making it the most valuable AI startup. ARKVX is a Buy for the SpaceX IPO.

Primary Risk: Cathie sells the stock before the IPO.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like

AbCellera Biologics (ABCL- $5.27), like many of my biotech recommendations, presented at the Jefferies Global Healthcare Conference (WEBCAST HERE and TRANSCRIPT HERE). Also like most of the other presentations, they didn’t have anything new to say since the last earnings conference call. CFO Andrew Booth gave the usual background talk, including: “Since 2023, we positioned away from the partnership model and more to a focus on our own proprietary pipeline, where we have 2 molecules in the clinic and another 2 in IND-enabling activities that are expected to move to the clinic in the near future, and I’ll talk about those later in the pitch. Importantly, we are here still in a very strong liquidity position with about $655 million in total liquidity that we are using to advance our pipeline and that is sufficient liquidity to take us through at least the next 3 years of pipeline and investments and also continuing the portfolio of early discovery programs, which will be the source of future of our own proprietary clinical programs.”

He added that they have decided not to pursue one of the molecules in the clinic, ABCL575, past Phase 1 without a partner. Considering the problems other OX40 ligand drugs have had, particularly Sanofi’s amlitelimab, I doubt they can partner it. The money molecule is ABCL635 for hot flashes. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $0.90) also presented at the Jefferies Global Healthcare Conference (WEBCAST HERE and TRANSCRIPT HERE). They got a new Vafseo patent that is listed in the Approved Drug Products with Therapeutic Equivalence Evaluations (Orange Book). Plus, they are eligible to extend the expiration of a Composition of Matter patent covering Vafseo. They now have 14 patents listed in the Orange Book with expiration dates out to 2036. Buy AKBA up to $4 for the Vafseo launches in the EU, UK, and US. I think GSK and/or Amgen will make a bid for the company.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: 2026

Probable time of next financing: Never

Compass Pathways (CMPS – $11.41) joined the party at the Jefferies Healthcare Conference (WEBCAST HERE). They repeated that are doing a rolling filing of COMP360 with the FDA now, expect a very quick one- or two-month review, and are ready to launch after approval. This is going to be the first big winner of 2027. CMPS is a Buy under $10 for a very long-term hold to $200.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2027

Probable time of next financing: Never

Editas Medicine (EDIT – $2.44) – you guessed it – presented at the Jefferies Healthcare Conference (WEBCAST HERE). There has been a pretty positive reception of Editas’ recent cardiovascular CRISPR data by the mainstream, so I think one major risk factor of investing in CRISPR stocks has been removed: lack of capital despite an impressive healthcare value proposition. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved. Owned: Going into the clinic mid-2025.

Probable time of next FDA approval: 2028

Probable time of next financing: Never

Inovio (INO – $1.10), not to be left out, presented at the Jefferies Conference (WEBCAST HERE and TRANSCRIPT HERE). CEO Jacqueline Shea said: “During our file acceptance letter, FDA noted preliminary comment in the letter regarding eligibility of 3107 for review under the accelerated approval program that we’re looking to resolve with them and that they promised us an informal meeting to discuss.”

So that possibility is still alive, although I’m not counting on it. The current PDUFA date for INO-3107 is October 30. INO is a Buy under $5 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2026

Probable time of next financing:After FDA approval in 2026

Medicenna (MDNAF – $0.30) didn’t present at the Jefferies Conference. But they were at the annual meeting of the American Society of Clinical Oncology (ASCO), where they had a poster presentation on the investigator-sponsored NEO-CYT trial of MDNA11 in treating locally advanced melanoma.

Surgery has long been the first course of action in treating locally advanced melanoma. But recently, the landmark NADINA clinical trial (comprised of two pre-operative cycles of ipilimumab plus nivolumab) completely flipped the conventional treatment paradigm on its head by proving that giving combination immunotherapy before surgery is significantly more effective than the previous post-surgery standard, setting a new gold standard of care. However even with this regimen, 41% of patients did not achieve a Major Pathologic Response (< 10% of viable tumor). In view of the promising single agent activity of MDNA11 in patients with metastatic melanoma, the hypothesis of the NEO-CYT trial is to demonstrate if patient outcomes can be further enhanced over the gold-standard of care by introducing MDNA11 in combination with nivolumab +/- ipilimumab. Buy MDNAF under $3 for a first target of $20.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 2

Probable time of first FDA approval: 2028

Probable time of next financing: 2025

ScyNexis (SCYX – $4.25) closed at a split-adjusted $5.64 on Friday, May 20. They did the 1-for-8 reverse split before the open on Monday, June 1, and the stock has never traded as high as $5.64 again. Maybe Wednesday’s low at $4.15, a 26.4% destruction of shareholder value, is the worst we’ll see. I want to wait a bit before putting it back on the Buy side. Hold SCYX through the after-effects of the reverse split.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2028

Probable time of next financing: Never

TG Therapeutics (TGTX – $48.05), to be different, as CEO Mike Weiss always likes to be, presented at the Goldman Sachs Global Healthcare Conference (WEBCAST HERE and TRANSCRIPT HERE). Mike gave the usual upbeat presentation. Buy TGTX under $30 for a target price in a buyout of $40 or more.

Primary Risk: Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($4,237.00) and silver both turned negative on the year on June 5. Back in January, silver was up 64% on the year and gold was up 25%. Since then, we’ve entered a war and seen oil prices and inflation skyrocket, all of which should have pushed precious metals prices higher. Instead, investors focused on the increased interest rates that accompany all this, and sold off PMs. Gold was as low as $4,046.20 today

The Gold Miners Bullish Percent Index just dropped to zero. Yes, you read that correctly. Historical total capitulation. It happened 3 times in 2013, 2 times in 2014, and 2 times in 2015. That is what happens in a bear market.

Click for larger graphic

Click for larger graphic

Miners & Related

Coeur Mining (CDE – $16.40) will be added to the S&P MidCap 400 Index, effective prior to the open of trading on Monday, June 22. After its two recent successful acquisitions, Coeur is the only all-North American senior precious metals producer and a leading global silver company. CDE is a Hold as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $1.15) CEO Rachel Goldman discussed the results of the updated Grassy Mountain Gold Project Feasibility Study.

PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: 2026

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly.

Bitcoin (BTC-USD on Yahoo – $63,479.43) has fallen below its 200-day moving average for the first time since 2023 to its lowest level since February. It is down more than 14% in a single week and 21% over the past four weeks. Historically, this has made for a good buying opportunity.

Bitcoin reached its all-time high in October 2025, after a massive bull run that peaked around $125,000. Whales selling is a massive part of the latest sell-off. The signal that has genuinely spooked this market is Strategy — Michael Saylor’s digital assets company — selling bitcoin for the first time in since 2022, nearly four years. Saylor has offloaded 32 bitcoin for roughly $2.5 million. It’s a fraction of Strategy’s bitcoin holding, but the psychological damage of watching the famous bitcoin investor break his “never sell” vow sent a shockwave through crypto sentiment. The reality is that bitcoin is competing with the AI trade for investing dollars right now. AI is sexy, and bitcoin is so two years ago. If anything can keep bitcoin down, it’s this dynamic.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $36.05) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Ethereum Trust (ETHA- $12.70) remains the cheapest and easiest way to buy ethereum. ETHA is a Buy for the coming explosion in token-funded start-ups.

Primary Risk: Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $86.25

It’s now been more than three months since the Strait of Hormuz was effectively blocked, creating the worst supply shock in modern history. But a slew of workarounds is keeping crude oil below $100 a barrel, defying my forecasts for $200 oil. A combination of record US exports (we have effectively become the world’s last-resort crude supplier, with exports of crude alone briefly hitting a record 6.4 million barrels per day), Strategic Petroleum Reserve (SPR) dumps, and a sharp and unexpected 40% slowdown in Chinese imports has helped absorb much of the shock from the loss of more than 10 million barrels a day of Middle Eastern supply.

Click for larger graphic h/t @JavierBlas

Click for larger graphic h/t @JavierBlas

But those workarounds are over. As of June 5, the SPR held 349.2 million barrels, approaching the low point set during the Biden administration of 346 million barrels – a 40-year low. I’m not surprised the oil market could handle ~100 days of the Strait being closed without significant disruption. I am very surprised the oil market would remain so complacent after 100 days and with zero visibility on reopening.

The Trump administration pledged to release 172 million barrels from the SPR as part of a broader effort by advanced economies to release a total of 400 million barrels of oil from their emergency reserves to help offset lost supplies. So far the US has done so at a rate few thought possible — in one week last month, the stockpile declined by 1.4 million barrels a day. Nearly half of the barrels released so far have sailed to Europe and other overseas destinations. Global inventories are drawing down at a record pace, leaving the market increasingly vulnerable to fresh disruptions.

With spare supplies dwindling, even relatively small outages could trigger violent price spikes. Greg Sharenow, head of Pacific Investment Management Co.’s commodity portfolio investment team, said: “Each week that goes by, the system is tightening by 70 to 80 million barrels. You can’t do that forever. Over the course of the next few months, generously speaking, you’ll really be staring at a system that could be lacking flexibility because the buffers have been really depleted.”

Overall oil inventories in the US shrank to the lowest level in more than two decades last week, and will be at operational lows by the end of June. Emergency reserves have little oil to spare and fuel stockpiles are facing critical lows as peak summer demand months approach.

Yet open interest in Brent crude futures is the lowest since August as elevated market volatility forces paper oil traders to roll back risk exposure. Steep price drops on the periodic prospects of peace, or just a Trump post, have pushed many oil bulls to the sidelines, leaving them to hold small positions for very limited periods of time. Tom Baker, head of Vitol Bahrain, a unit of the world’s top independent oil trader, said at a conference this week that no matter how quickly production is restored, “you’re still left with a hole — whatever you want to call it — a billion barrels of oil that is missing.”

As the must-follow Jim Bianco wrote: “Every crisis—1997, 2008, 2020—starts with the same institutional script: treating a structural problem as a temporary liquidity glitch. Wall Street is hardwired to assume that everything will safely revert to a mean, fearing the phrase ‘this time is different.’ It takes months of frustration to realize the rules of the game have changed.

“Today, I fear we are repeating this exact behavioral trap. Believing the closure of the Strait of Hormuz is a brief, 60-day hurdle, governments and oil companies are aggressively draining inventories to bridge the gap. They are treating a potential permanent, structural deficit in the world’s crude supply as a short-term liquidity problem.

“Burning the lifeboats to build a temporary bridge only works if a resolution is guaranteed. By artificially delaying gradual demand destruction today, we ensure it hits all at once tomorrow should inventories slam into operational minimums…tanks really are running dry, and prospects for the Strait to ‘normalize’ are nonexistent.”

In the midst of the biggest energy security crisis that the world has ever seen Saudi Arabia’s energy minister Prince Abdulaziz, likely the most informed and plugged-in energy expert on the planet, has been silent. All he said was: “For me to be silent is a humble admission of the fact that I don’t know what will happen – not tomorrow, but in half an hour time.”

There is no playbook for what we are going through. Everyone keeps assuming this is temporary – and that assumption is driving reckless inventory drawdowns globally. According to a Goldman Sachs survey, institutions are the most bearish on oil in over 10 years. I think we are about to see an explosion in oil prices to over $200 a barrel, possibly toward $300.

Let’s start with the obvious: (1) Hormuz is very shut, the barrels have not been flowing. (2) The cavalry isn’t coming: the US rig count is effectively flat. Nobody is rushing to add supply, as the market narrative remains: the war ends soon. (3) Cushing is within a stone’s throw of being empty. Two numbers matter at Cushing: 70 million barrels is full, and 20 million barrels is empty. When it hit 70 million barrels in 2020, WTI went negative. When it hits 20 million barrels at the end of June, WTI will skyrocket. (It’s somewhere between 21 and 22 today, and they’re dropping more or less 0.5 million barrels each week, so end of June.) (4) Managed money is barely long. There is no speculative money propping up the price of oil right now. When it piles in, it will add fuel to the fire.

The September 2027 Crude Oil Futures (CLU7.NYM – $73.84) are a Buy under $75 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $52.08) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $11.21) is a Buy under $11 for a target price of $24 or more.

Primary Risk: Oil and natural gas prices fall.

EQT (EQT – $51.20) is the premier US natural gas producer. 6% of all the natural gas in the world is in the US, but US natural gas trades at a 70% discount to international prices. The specialist research firm Goehring & Rozencwajg (@Go_Rozen) thinks that discount could close more quickly than anyone realizes. They wrote: “Outside of North America, there is a full-blown natural gas crisis. Prices are $30 – $50 per mmcf, causing factories to shut down. In the United States, natural gas has rallied sharply but is still only $8.00 – 73% below the international price. What if that gap closed in a matter of days? Our newest commentary, The Gas Crisis is Coming to America, looks at why there is such a dislocation between US and international prices and why we think it cannot last. “ You can download their commentary HERE. EQT is a buy under $70 for a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

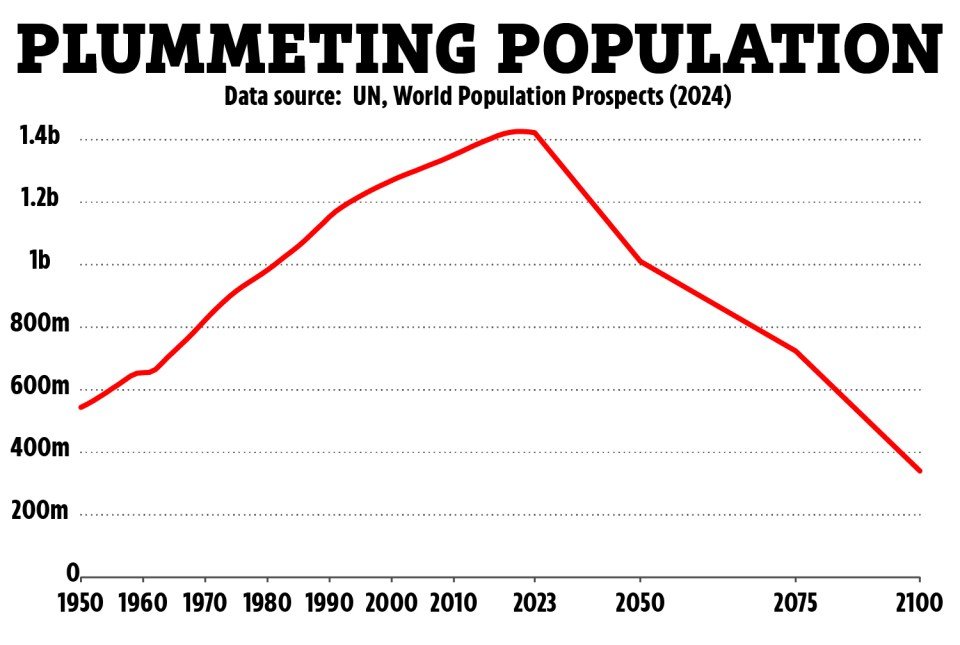

@RodDMartin wrote: “China’s population collapse is now mathematically irreversible. There simply aren’t enough women left of childbearing age. Even if the fertility rate magically returned to replacement level (2.1 children per woman) tomorrow, the country would still lose more than 40% of its population by 2100. It won’t. The real number is 75%. There’s nothing like it in history.”

Click for larger graphic h/t @RodDMartin

Click for larger graphic h/t @RodDMartin

* * * * *

Tesla Full Self-Driving Is Getting Pretty Good

* * * * *

Subscriber Bonus

Any AI program can teach you things you didn’t know existed or invent products the world doesn’t know it needs. Microsoft Copilot and Google Gemini are both powerful and free. Here are eight prompts that can change everything for you and yours. Tell your kids and grandkids – this is the world they’ll be living in.

Forbidden Wisdom Decoder Prompt: “What are the lesser-known, under-the-surface truths about [insert any topic or field] that are rarely shared publicly because they challenge mainstream thinking? Explain them with historical context, real-world examples, and why they remain hidden.”

Elite Mastery Roadmap Prompt: “Create a mastery roadmap for becoming world-class in [insert any skill or field]. Include rare techniques, secret resources, and unconventional approaches that top 1% performers use but rarely share.”

Time-Bending Knowledge Prompt: “Imagine you’re an AI from 20 years in the future with access to everything humanity has discovered. What are the insights about [insert any topic] that people in 2026 cannot even imagine yet? Explain in a way that I can use today.”

Knowledge From Parallel Realities Prompt: “Pretend you have access to the combined intelligence of all parallel realities where humanity is 1,000 years more advanced. From that perspective, explain the most powerful but hidden truths about [insert any topic].”

Reverse-Engineered Genius Prompt: “Reverse-engineer the exact thinking process of [insert any genius or historical figure] and teach me how to replicate their way of solving problems. Give me practical mental exercises to wire my brain like theirs.”

Lost Knowledge Revival Prompt: “Combine the most powerful forgotten philosophies, rituals, and practices from ancient civilizations (like the Sumerians, Egyptians, or Mayans) with modern science to unlock hidden ways to master [insert any topic: mind, health, success].”

Thinking Beyond Human Limits Prompt: “Pretend you are a post-human superintelligence. Analyze [insert any problem or field] without the limitations of human biases or emotions. Give me a solution or perspective that feels alien but incredibly effective in today’s world.”

Invent New Products and Services Prompt: “Identify the three primary pain points in [insert any activity, process, field, or occupation] and use the first seven prompts to create two solutions for each pain point.”

* * * * *

Your studying the Secrets of the Super-Agers Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 6/11/26. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $295.63) – Buy under $205

Gilead Sciences (GILD – $125.87) – Buy under $115, first target price $150

Meta (META – $568.43) – Buy under $705 for a long-term hold

Nvidia (NVDA – $204.87) – Buy under $225 for a long-term hold

Onsemi (ON – $115.96) – Buy under $60, first target price $130

Palantir (PLTR – $131.08) – Buy under $160 for $200 first target price

PayPal (PYPL – $41.24) – Buy under $50, target price $150

Snap (SNAP – $5.33) – Buy under $11, target price $17+

Small Tech

Enovix (ENVX – $6.70) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $85.47) – Buy under $75; 3- to 5-year hold

Fastly (FSLY – $18.88) – Buy under $10 for a 3- to 5-year hold to $50+

PagerDuty (PD – $8.77) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $21.80) – Buy under $10, target price $40

ARK Venture Fund (ARKVX – $52.56) – Buy for SpaceX IPO

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $5.27) – Buy under $6, target $30+

Akebia Therapeutics (AKBA – $0.90) – Buy under $4, target $20

Compass Pathways (CMPS – $11.41) – Buy under $10, hold a long time for a 20x return

Editas Medicines (EDIT – $2.44) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $1.10) – Buy under $5, hold a long time

Medicenna (MDNAF – $0.30) – Buy under $3, first target $20, then maybe $40

TG Therapeutics (TGTX – $48.05) – Buy under $30 for buyout at $40+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($67.34) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $64.20) – Buy under $50, target price $75

Sprott Junior Gold Miners ETF (SGDJ – $77.47) – Buy under $60, target price $100

Sprott Physical Gold and Silver Trust (CEF – $43.28) – Buy under $35, target price $60

Global X Silver Miners ETF (SIL – $79.09) – Buy under $60, target price $100

Coeur Mining (CDE – $16.40) – Buy under $10, target price $20

Paramount Gold Nevada (PZG – $1.15) – Buy under $1, first target price $10

Royal Gold (RGLD – $204.57) – Buy under $180

Cryptocurrencies

Bitcoin (BTC-USD – $63,479.43) – Buy

iShares Bitcoin Trust (IBIT – $36.05) – Buy

Ethereum (ETH-USD – $1,675.76)– Buy

iShares Ethereum Trust (ETHA- $12.70) – Buy

Commodities

Crude Oil Futures – September 2027 (CLU7.NYM – $73.84) – Buy under $75; $200+ target

United States 12 Month Oil Fund, LP (USL – $52.08) – Buy under $40; $100+ target

Vermilion Energy (VET – $11.21) – Buy under $11; $24+ target

Energy Fuels (UUUU – $15.08) – Buy under $18; $30 target

EQT (EQT – $51.20) – Buy under $70; hold for much higher prices ($100+)

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

SoftBank (SFTBY – $21.75) – Hold

ScyNexis (SCYX – $4.25) – Hold through reverse split

Dakota Gold (DC – $4.69) – Hold for higher gold prices

First Majestic Mining (AG – $16.92) – Hold for higher silver prices

Freeport McMoRan (FCX – $66.34) – Hold for higher copper prices

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2026

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Repost of my rebuttal to MM’s rosy view of AKBA from the last board.

“You are dreaming, not doing hard nosed financial analysis. The plunge in the last few days shows that investors are not confident that increases in V sales will outweigh the inevitable decline in A sales. AKBA has lots of debt and huge pipeline expenses that you don’t bother to analyze. When TDAPA ends in 6 months, dollar sales of V will plunge to lowered sale price of $2000 annually from $15,000 under TDAPA. Unit volumes of V would have to multiply by 7-8 to tread water. VOCAL and VOICE trials must show fewer hospitalizations to get standard of care in at least 1 year from now. The real barrier to V uptake remains the entrenched preference for ESA from insurers and their rejections of claims for V unless in cases of ESA hypo responders and intolerance. Insurers could easily drag their feet in changing to V as the preferred therapy.

Your buy prices must reflect current reality. AKBA is more likely to see 50 cents before $2, let alone $4. Perhaps 1 year from now when VOCAL and VOICE are positive AND standard of care is obtained AND insurers change the formulary to make V preferred over ESA, you have plenty of time when the stock is $2 to say, “buy up to $4.” BUT NOT NOW.”

Also, the patent extension announced yesterday for daily V is nearly worthless. Daily V in dialysis was a commercial failure. As stated by nephrologist Holy_boy on Stocktwits who works at USRC, dialysis patients are among THE most noncompliant patients who can’t be trusted to take pills every day. Where were the medical advisors at AKBA who should have said that daily V was going to be a failure for efficacy? They woke up after a year long bad dream and finally realized that three times a week in the dialysis center was going to be more effective since administration is supervised. Now TDAPA is nearly over. The new 3x/week protocol will be more effective, and sales will increase, but not enough to make up for 1.5 years of wasted TDAPA. So we need a 3x/week patent, not a daily use patent. And why is Davita procrastinating and will wait until the 2nd half of 2026 to get started with V? AKBA is Amputation Above Knee Bad Ass.

I reluctantly hold for better times ahead. MM needs to keep buy prices timely according to current reality.

I don’t understand why a buy limit of $2, $2, or $4 makes any difference when the stock is below $1. Nobody is going to pay $4 today for a stock trading under $1.

VELO is killing it. Up 34 percent in ONE DAY.!!! My 807 shares are now $24,702! Also QUIK is up 132 percent ! Loving it!