Dear New World Investor:

The venerable Dow Jones Industrial Average went over 45,000, the S&P 500 and Nasdaq Composite hit new record highs, and bitcoin cleared $100,000 – so all is right with the world? Well, not quite. Inflation is enough above the Fed’s target and the labor data is not that bad, so the Fed is not going to be in a rush to cut interest rates. I still think the odds slightly favor another quarter-point cut on December 18, but the CME FedWatch shows 70.1% thinking we get the 25 basis point cut and only 29.9% thinking no cut. There’s a fair amount of wishful thinking in there.

Assuming tomorrow’s November payrolls number is not a disaster and the December 11 Consumer Price Index is more or less in line, the quarter-point cut on December 18 is likely. But then we have to get through another Personal Consumption Expenditures Index (PCE) report on December 20, December payrolls on January 10, and the Consumer Price Index on January 15 before the January 29 meeting, Even if all of them are neutral to positive, I think the Fed won’t cut again just to keep us on our toes. Powell can say the economy is OK and inflation is slowly declining, so there’s no need to cut “at this time.”

In the short term, whether that knocks stocks down because FedWatch is disappointed or puts stocks up because Powell says the economy is OK (December quarter real GDP will be reported the next day, January 30) I don’t know. Get your Buy wish-list ready in case stocks dump or enjoy the upswing and you will win either way.

The October Personal Consumption Expenditures Index (PCE) rose 2.3% year-over-year, an increase from the 2.1% seen in September. The month-over-month increase was 0.2%, the same as September.

The core PCE – the Fed’s favorite inflation indicator – rose 2.8% YoY and 0.3% MoM, the same as September. Core PCE inflation is running at a 2.8% annualized pace over the past three months, the highest since April. On a six-month annualized basis, core PCE inflation ran at a 2.3% rate, the same as September. Further progress on inflation has stalled which is why I think it’s possible that the Fed doesn’t do another quarter-point cut on January 29.

The October nonfarm Job Openings and Labor Turnover (JOLTS) report beat the consensus estimates, posting a 7.744 million reading versus the consensus 7.519 million. The 372,000 advance was the largest in 14 months. September was revised down slightly from 7.443 million to 7.372 million, the lowest level since January 2021. It looks to me like labor demand is soft but not collapsing – probably just what Fed Chairman Powell wants to see.

Market Outlook

The S&P 500 added 2.1% since November 21 to another all-time high yesterday. The Index is up 27.4% year-to-date as inflows into US stocks are on track to reach an all-time high in 2024, double the total investment of the previous two years. Wall Street is doing what it always does: Raise the forecast to keep writing Buy tickets. Three weeks ago, both Goldman Sachs and Morgan Stanley forecast the Index could touch 6,500 by the end of 2025. Two weeks ago, both Barclays and RBC Capital Markets issued a 2025 yearend target price of 6,600. Barclays wrote that “For U.S. equities, we think macro positives outweigh the negatives heading into next year” and with “inflation continuing to normalize, resilient macro, and Big Tech maintaining EPS growth leadership” the S&P should continue its march higher. RBC wrote: “The story the data tells us is that another year of solid economic and earnings growth, some political tailwinds, and some additional relief on inflation (which should keep the S&P 500’s P/E elevated) can keep stocks moving higher in the year ahead.” Uh huh.

Deutsche Bank said they’d see your 6600 and raise you an even 400 points to 7000 by the end of next year. They said from a demand-supply perspective the U.S. equity market remains solid, with drivers of the last two years – large inflows and strong buybacks – continuing into 2025. Wells Fargo topped them all at 7007.

The Nasdaq Composite gained 3.8% and also booked a new all-time high yesterday. It is up 31.2% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 3.2% during a spate of brokerage firm healthcare conferences (see below). It is up only 9.0% year-to-date. The small-cap Russell 2000 gained only 1.4% as the small-cap rally lost steam and is up 18.2% in 2024.

The fractal dimension stopped consolidating over the last two weeks and may be about to trend again, even though that would be highly unusual. The healthiest pattern would be a churning market through January to get the fractals over 55.

Top 5

Changes this week: Revised the Near-Term order. Raised bitcoin target.

Near-Term – chronological order

SCYX – ScyNexis – Announce resolution of the manufacturing problem, lifting of clinical hold, restart of MARIO trial, maybe GSK files for hospital use approval

EQT EQT –natural gas price rebound

AKBA Akebia Therapeutics – Vafseo launch in January

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000 $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Economy

This morning’s Atlanta Fed’s GDPNow model raised the December quarter real GDP growth estimate to a stronger +3.3%. They see strength in both personal consumption expenditures growth and private domestic investment growth.

Click for larger graphic

Click for larger graphic

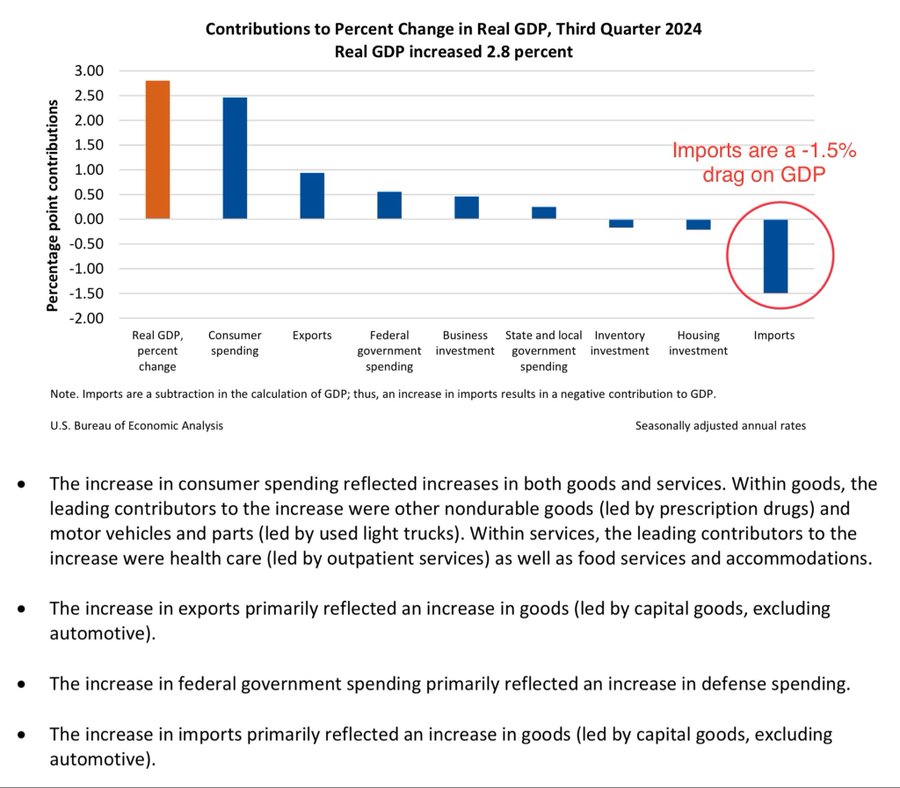

Nothing seems to stop Americans from growing consumer spending insatiably. It was most of the September quarter GDP increase. When it slows down – recession.

Click for larger graphic h/t @ecommerceshares

Click for larger graphic h/t @ecommerceshares

The increase in consumer spending reflected increases in both goods and services. Within goods, the leading contributors to the increase were other nondurable goods (led by prescription drugs) and motor vehicles and parts (led by used light trucks). Within services, the leading contributors to the increase were healthcare (led by outpatient services), food services, and accommodations.

The increase in exports primarily reflected an increase in goods (led by capital goods, excluding automotive). The increase in Federal government spending primarily reflected an increase in defense spending. The increase in imports primarily reflected in increasing goods (also led by capital goods, excluding automotive).

Dollar Death Watch

From @TheLastRefuge2:

“Everyone who is a pragmatic critical thinker knows that China will devalue their currency to lower the impact of exports to the USA. Beijing controls the banks and they did this before. As a result, the dollar value increases and imports cost less. The Chinese imports then enter the USA at a lower price consistent with their cost estimate as a tariff offset. China takes in a lower price, but retains access.

“That’s just how it works. The importers pay the tariff with a lowered price and a higher valued dollar. Essentially stasis for the time being. Then….. EU industrial products to Chinese manufacturing plants start to contract, due to China’s aggressive cost cutting initiatives. The EU gets angry about the impact to their economy. The EU then follows the same path and devalues their central bank currency, further pressuring the dollar to an upward price. Exports to the EU are now more expensive, and imports from the EU to the USA are now cheaper. Again, the EU goal is stasis.

“Both scenarios create cheaper USA imports despite the tariffs. However, on the EU side Trump then ends the Marshall plan and executes ‘tariff reciprocity’ against the EU. More frustration and gritted teeth by Brussels. [NOTE: Avoiding this squeeze also explains why U.K Prime Minister Starmer was all snuggly to Trump at Trump Tower a few weeks ago – he’s hedging.]

“Exports from the USA ultimately cost more because the dollar is stronger against EU and Asia currencies. However, a stronger dollar is an offset to BRICS leverage and allows Trump to play economic chess. Trump uses part of the tariff income to underwrite agriculture exports, but… here we have fun… if agriculture exports are impacted, domestic foodstuffs drop in price.

“Into this dynamic, Trump turns to Mexico. We have a strong dollar, all those Western Union transfers to Mexico are more valuable. Leverage is created. The economic situation then overlays the secure border dynamic and if Mexico wants to retain trade access within the USMCA agreement, the part that no one discussed comes into play. Unbeknownst to all those except those who watched Robert Lighthizer do it, the USA has first right of refusal to any trade agreement made by Mexico or Canada.

“That’s correct, Trump now controls a veto on trade agreements within USMCA partnered countries. Suddenly Xi Jinping is vulnerable in Mexico if Trump nixes the EV production. Beijing is financially exposed and vulnerable. Big Panda not happy. How do we know this will happen? Good question. Answers: (#1) This is what Trump did in 2017; and, (#2) Because he said this is what he is going to do.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, December 6

November payrolls – 8:30am – +200,000 expected; October was only +12,000 due to strikes and hurricanes

Saturday, December 7

Pearl Harbor Day

Midway is a 2019 movie on Netflix, Amazon, and YouTube about the decisive Battle of Midway in the Pacific. The hard-to-watch Pearl Harbor attack is from the 9-minute mark to the 15-minute mark. RIP my uncle Thomas Joseph Murphy, Jr. SK1c, who was on the Arizona.

Tuesday, December 10

GILD – Gilead Sciences – Unspec. – HIV Analyst Day

Short Interest – After the close

Wednesday, December 11

Consumer Price Index – 8:30am

Thursday, December 12

PZG – Paramount Gold – 11:00am – Annual meeting

MDNA – Medicenna – 1:00pm – poster at San Antonio Breast Cancer Symposium (SABCS), the world’s largest breast cancer conference

Friday, December 13

MDNA – Medicenna – 8:30am – Another poster at SABCS

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $243.04) was reiterated a Buy with a $273 target by Morgan Stanley as they expect artificial intelligence to be a key catalyst for iPhone sales in 2025. I agree – this is where much of Wall Street is missing the impact. AAPL is a HOLD – I expect to move back to Buy under $175 for new iPhones.

Gilead Sciences (GILD – $93.39) CFO Andy Dickinson presented at the Piper Sandler Healthcare Conference (AUDIO HERE and TRANSCRIPT HERE) and also at the Evercore HealthCONx Conference (AUDIO HERE and TRANSCRIPT HERE).

He summarized the investment case: “We now have all three of our franchises growing substantially and we have no major patent cliffs through 2033 unlike many of our peers. So we’ve substantially invested in our pipeline, both internally and externally. We have a number of either recent approvals or expected near-term approvals that will drive additional growth and diversification of the business. And whether you look at our HIV business, our liver disease business, or our oncology business, all of them are growing and expected to grow for the foreseeable future.”

Barron’s wrote: Gilead Sciences Is Turning Itself Around. Why Its Stock Can Keep Rallying. The stock ended eight consecutive uptick sessions on Monday and GILD remains a Long-Term Buy under $80 for a first target of $120.

Palantir (PLTR – $71.87) is the model for Enterprise Resource Planning (ERP) software in the future. Enterprise AI goes beyond simple automation to use AI to solve complex business problems that require human-like intelligence, such as understanding customer behavior, optimizing logistics, or detecting fraud. The ERP business is dominated today by Oracle and SAP. Oracle has partnered with Palantir in specific use cases, and I’d bet Larry Ellison would like nothing more than to buy Palantir. But Wall Street would kill his stock even if he just paid the current market capitalization of the company.

We might see a dip in the stock just ahead. Professional money managers need to show it in their yearend portfolios that clients look at. Wall Street is really good at knocking stocks down briefly, hoovering up as much stock as they can shake loose, and then calling the institutions to write Buy tickets. I noticed they got several Palantir insiders to sell small portions of their stock to start this process.

If you’re in, don’t let them shake you out. If not, just watch the fun or even buy a small starter position – a placeholder, really. The stock is far above my original recommendation and buy limit. PLTR is a Buy under $22 for a $100+ target.

PayPal Holdings (PYPL – $89.04) EVP and CFO Jamie Miller presented at the UBS Global Technology and AI Conference (AUDIO HERE and TRANSCRIPT HERE). She said their top priority is branded checkout – Pay With Venmo, Braintree, PayPal Everywhere, and Buy Now Pay Later. All those have raised merchants sales by 4%, so they are happy. About 5% of US merchants use it now, so there’s lots of headroom. On top of that, PayPal is very strong internationally and adding branded checkout there will drive 2025 and 2026.

PayPal Everywhere is a debit card that offers a 5% cash reward on spending in a category of the cardholder’s choice. Fastlane is designed to give merchants a sales uplift and over 1,000 use it today. PayPal wants to dramatically expand the user base before they monetize it in 2026. Venmo has more than 60 million monthly active users, mostly young consumers that merchants want. Pay With Venmo is up 30% year-over-year.

The headcount is down 10% from last year and they reinvested those savings in R&D and marketing. Expenses overall will be up low single digits in 2025. PYPL is a Buy under $68 for a double in three years.

Small Tech

Enovix (ENVX – $9.30) made a great hire – Dr. Hongwei Yan as Chief Technology Officer. As Board Chairman T. J. Rodgers said: “We all know that Korea and China lead the world in lithium-ion batteries. Now, we have a top scientist who has worked at both Korea’s No. 1 battery company, Samsung SDI, and China’s No. 1 battery company, Amperex Technology Limited (ATL) where he led over 30 battery qualifications with a 100% success rate for a Tier 1 US mobile customer [That would be Apple, folks.]. He brings us deep technical relationships with the battery experts at our top customers, an in-depth understanding of their qualification processes, and a successful track record in working with them to scale their production.”

He holds eight patents and has 21 peer-reviewed publications. This is a guy that could have gone anywhere and is not going to be fooled by vaporware. It’s a huge vote of confidence in Enovix’ technology and market position. If you’ve been on the fence about this stock, now is the time! ENVX is a Strong Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $9.93) CEO Todd Nightingale and CFO Ron Kisling presented at the UBS Global Technology and AI Conference (AUDIO HERE and TRANSCRIPT HERE). Todd said said the goal since he became CEO has been to broaden the functionality of the Compute@Edge platform and unify it into one cohesive easy-to-use edge solution. That has to include content delivery (like Akamai), edge security and web application programming interface (API) protection, easy observability, and edge compute. Each of those features allows them to land and expand at different customers with different needs.

In 2024 they saw a lot of variability among the biggest media customers, due in part to price cutting by Edgio. Edgio finally went bankrupt and Akamai bought their customer accounts at the courthouse door. Fastly has already won some of those accounts and is tracking every one as the traffic migrates elsewhere over the next 12 months. Oppenheimer thinks they’ll win anywhere from $20 million to $60 million of incremental revenue. Plus, it makes the pricing environment better for everyone – Akamai is not a price cutter.

In the meantime, Fastly focused on the much larger market of non-media customers to build a company that can grow at double digits with less variability. Outside of the Top 10, Fastly grew year-over-year revenues 20% in the September quarter. These customers don’t want multiple edge vendors and they need the security and programability of Compute@Edge. They are beta testing Fastly’s AI Accelerator to speed their chatbot responses with really useful feedback.

Ron Kisling said after their $150 million convertible stock sale on Monday they’ve paid debt down from about $1 billion to less than $200 million and have a solid balance sheet. Their profit margin on incremental revenue is 35% to 40%. FSLY is a Buy up to $10 for a 3- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $20.99) reported September quarter revenues up 9.4% from last year to $118.95 million, nicely above the $116.39 million Wall Street estimate. Pro forma earnings per share of 25¢ also beat the 17¢ estimate.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Jennifer Tejada said: “PagerDuty delivered a solid quarter with revenue and non-GAAP operating income results well above third quarter guidance ranges with annual recurring revenue increasing to $483 million, growing 10% year-over-year. Consistent performance over the past four quarters has led to stabilization across all business segments, and along with improving leading indicators, positions the business on a strong upward trajectory.”

Their pro forma gross profit margin of 86%, operating margin of 21%, and free cash flow margin of 16% were all pretty much right on their long-term financial model.

Click for larger graphic

Click for larger graphic

Forrester did a survey of PagerDuty customers and reported an average payback on their investment of less than 12 months with a Return On Investment of 249% over three years. The market research firm GigaOm recognized PagerDuty as a leader in AIOps for the third year in a row.

Click for larger graphic

Click for larger graphic

They guided for December quarter revenues of $118.5 million to $120.5 million, slightly below the $121.6 million consensus. Pro forma earnings guidance of 15¢ to 16¢ was in line with estimates.

For the full year, they raised revenue guidance from $463.0 million – $457.0 million to a range from $464.5 million to $466.5 million, with earnings guidance raised from 67¢-72¢ to 78¢-79¢. PagerDuty has a huge market opportunity:

Click for larger graphic

Click for larger graphic

They finished September with $542 million of cash . PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Rocket Lab USA (RKLB – $23.92) hit a record high Monday after announcing two successful launches and closing a $23.9 million award from the Department of Commerce under the CHIPS and Science Act of 2022. The money is to be used to increase its compound semiconductor manufacturing capability and capacity at its Albuquerque, New Mexico plant.

The second of the two launches, their 56th successful launch, put five satellites in low-earth orbit for Kineis, the French Internet of Things (IoT) constellation operator. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $2.85) made their third recent presentation at the Piper Sandler Healthcare Conference (AUDIO HERE), this time by Senior Director of Strategic Finance Martin Hogan. He discussed how they make a decision on what antibody programs to pursue for drug development. He repeated their four-step process:

1. Do they like the science – is the target clear and derisked?

2. Is there a big commercial opportunity, which means an unmet medical need?

3. Is there a clear opportunity for differentiation?

4. Is there a feasible development path that they can afford to take it to a point of value inflection?

The sweet spot often is in very difficult targets for an antibody, simply because they have the world’s best antibody discovery and development science. They expect to find one to three new programs a year, so in a few years they’ll have a dozen or so programs in preclinical or clinical development. They think carefully about the best value point in each program to bring in a capable partner for further development. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $2.02) CEO John Butler also presented at the Piper Sandler Healthcare Conference (AUDIO HERE). It was the usual presentation. John said they have 340,000 or 65% of dialysis patients under contract, and by the end of the year they expect to have 100%. For a fast launch, the sales force is focused on doctors treating those who will use Vafseo first – the 80,000 home dialysis patients and 150,000 high erythropoiesis-stimulating agents (ESAs).

John said they are close to agreeing with the FDA for another trial of Vafseo in non-dialysis patients, a market 4x-5x the dialysis market in dollar terms. They expected to be one of three products approved for dialysis, but now they are one of one. GSK is withdrawing Jesduvroq (daprodustat) from the US in a couple of weeks. Akebia also will be one of one in non-dialysis if they get approval. Buy AKBA up to $2 for the vadadustat launches in the EU, UK, and US.

Primary Risk: Vadadustat doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: NM

Probable time of next financing: Never

Compass Pathways (CMPS – $4.10) was another presenter at the Piper Sandler Healthcare Conference (AUDIO HERE). There are 17 million to 21 million US adults with clinical depression. About one-third of them have treatment-resistant depression (TRD), which the FDA defines as being failed by at least two drugs or other treatments. The only marketed drug for TRD is ketamine, so most TRD patients cycle through drugs approved for Major Depressive Disorder one after another, with a very small likelihood of benefit. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2027

Probable time of next financing: Late 2025

Editas Medicine (EDIT – $1.91) presented at the Evercore HealthCONx Conference (AUDIO HERE and TRANSCRIPT HERE). CFO Erick Lucera said there will be an update on the reni-cell trials including 28 patients (10 with one-year follow-up data and one with two-year data) at the American Society of Hematology (ASH) meeting next week. Partnering discussions continue. Reni-cell looks like a best-in-class sickle cell drug and a deal probably will include their second-generation in vivo sickle cell program.

They expect an appellate court ruling on the Cas9 and Cas12 patent suit before the end of the year. Editas won in the lower court and if that is affirmed, the opponents are done. If it is remanded to the lower court, that starts a two-year process to re-litigate. There are about 100 programs in development that need a license, and about 50 of them are at 8 to 10 companies. Editas expects a low single-digit royalty on all of them through the 2033-2035 patent expirations.

BofA downgraded Editas from Buy to Underperform and slashed their target price from $13 to $1(!). They wrote: “Deprioritizing reni-cel does make sense from a cash burn perspective but removes a significant portion of our valuation with partner interest remaining to be seen. Given the increasingly competitive nature of SCD and thalassemia development, we see the potential value of reni-cel waning as the field looks to in vivo therapies as the next logical step.”

Ignoring the fact that Editas has one of the best in vivo programs. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2026

Probable time of next financing: 2026 or never

Inovio (INO – $4.02) said data from a retrospective trial of INO-3107 showed that the number of Recurrent Respiratory Papillomatosis (RRP) patients meeting the criteria for a Complete Response increased from 28% at the end of Year 1 to 50% by the end of Year 2 and 54% at the end of Year 3. 95% of patients maintained or enhanced their original Overall Response Rate two years following initial treatment with INO-3107. In year three, 86% of patients had maintained or enhanced their initial response to INO-3107.

This new durability data will help to establish a re-dosing strategy focused on long-term elimination or reduction in the need for surgery to treat RRP disease. Inovio will present the data at future scientific conferences and submit it for publication in peer-reviewed journals. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Early 2026

Probable time of next financing: March 2025 or after FDA approval in 2026

Medicenna (MDNAF – $1.40) jumped 19.7% today after they announced the first Complete Responder in the combination dose escalation arm of their ABILITY-1 trial of MDNA11 and Merck’s Keytruda. A 70-year-old patient with advanced chemo-refractory anal cancer achieved a complete response in just 8 weeks. In addition, in the monotherapy arm of MDNA11 alone, they are seeing complete regression of all tumors in a patient with melanoma remaining tumor-free at week 63. Another patient with pancreatic cancer remains off all anti-cancer therapy for 11 months after completing the study. The company will present additional monotherapy and combination clinical data at medical conferences in the March and June quarters. Buy MDNAF under $3 for a first target of $20.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

TG Therapeutics (TGTX – $33.65) CEO Michael Weiss presented at the Evercore HealthCONx Conference (AUDIO HERE). Mike said the reception to Briumvi has been well above their expectations. They’ve had to raise revenue guidance twice, and there are lots of hospitals and doctors left to get on board.

They expect new patient starts to accelerate into 2025 and repeat patient volumes to make a bigger and bigger impact. The six-month continuation rate is around 85%. I am moving TGTX to a Hold for a target price in a buyout of $40 or more, an increase of $10 over my previous target.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,655.00) is trading near its all-time highs, but I am debating whether we should ring the cash register or not. If the US dollar is going to get stronger and stronger in spite of our large fiscal deficits, we should move to the sidelines. But if inflation also is about to re-accelerate, as seems likely with tariffs and illegal alien deportation, we should stay in. Stay tuned.

The fractal dimension continues to consolidate, driven for now by the stronger dollar. A few weeks of churning or a couple of sharp down weeks would get to 55. This little downturn is not a new trend.

Click for larger graphic

Click for larger graphic

Miners & Related

Coeur Mining (CDE – $6.80) presented at the Scotiabank Mining Conference (SLIDES HERE). They focused on the pending SilverCrest acquisition.

Click for larger graphic

Click for larger graphic

Coeur is becoming a premiere way to invest in silver, which is dramatically undervalued compared to gold. Even if we decide to sell some of the gold positions, we’ll probably keep all the silvers – the Global X Silver Miners Exchange-Traded Fund (SIL), Coeur, and First Majestic.

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Dakota Gold (DC – $2.23) said that their step-out drilling north of the JB Gold Zone has nearly doubled the known strike-length of the Homestake iron-formation hosted gold mineralization at the Maitland Gold Project. The Maitland drill program has delineated four distinct ledges, each of which has yielded high-grade Homestake Mine-style gold intercepts analogous to the gold mineralization found in the “West Ledge” system that produced approximately 6 million ounces of gold at the historic Homestake Mine. To date, their drilling program at Maitland has generated 49 intercepts from 73 holes at an average grade of 10.11 grams per tonne of gold over an average thickness of 3.8 meters. DC is a Buy under $2.50 for a $6 target as gold goes higher.

Primary Risk: Robert Quartermain doesn’t find enough gold. Secondary risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $6.20) will hold a special shareholder’s meeting on January 14 to approve the Gatos Silver acquisition. Vote Yes. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.77) said SSR Mining reported that engineering studies and site preparation activities continue at its Hod Maden project in Türkiye, as they continues to advance the project through to a construction decision. You may remember that SAND stock was hit last year when SSR had a problem at a different mine and investors were afraid they would put Hod Madden on hold.

In the September quarter, SSR spent about $10.9 million at Hod Maden. They will provide guidance on their expected 2025 capital spend at Hod Maden with their annual 2025 guidance.

Sandstorm holds a 2.0% NSR royalty and a 20% gold stream on the Hod Maden project. Under the terms of the gold stream, Sandstorm has agreed to purchase 20% of all the gold produced from Hod Maden for 50% of the spot price of gold until 405,000 ounces of gold are delivered. Sandstorm will then receive 12% of the gold produced for the life of the mine for 60% of the spot price of gold. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Stephen McBride of RiskHedge wrote a provocative piece on cryptocurrencies after President Trump’s reelection. He called bitcoin, ethereum, and other “serious” cryptos “newly legalized investments.” He wrote:

“You know Dogecoin (DOGE), the speculative crypto token with a fluffy dog mascot? It’s now worth more than Target (TGT)… America’s oldest bank, BNY Mellon (BK)… and America’s largest homebuilder, D.R. Horton (DHI). Some investors look at this and conclude crypto is just one giant casino. I get it. One crypto token called “AI Prophecy” has surged 3,000% since Election Day. Many other “memecoins” with silly names are doubling and tripling.

“But here’s what most people miss: This memecoin circus wasn’t an accident. It was engineered by regulators. They purposely created a twisted system where joke tokens flourished while real innovation froze. The good news is crypto just broke free from its regulatory prison. We’re entering a new era where quality crypto businesses solving real problems can shine. Now, these cryptos can appreciate 500% or more not because of gambling… but because they truly deserve it.

“For the past four years, America’s crypto rules created the worst possible incentives. Anyone could make a worthless token named after their pet hamster. But trying to build a platform that allows anyone to seamlessly send money across borders? That could land you in jail. The US Securities and Exchange Commission (SEC) would hunt down and sue innovators who built something useful.

“We lived in a bizarro world where the only projects regulators allowed were cryptos that obviously had no underlying value. It’s as if trading GameStop (GME) meme stocks was fine but investing in Amazon (AMZN) or Apple (AAPL) was illegal. Crypto banks were shut down by the government. Founders and funds were sued. Protocols were subject to constant surveillance sweeps.

“This wasn’t an accident. Their plan: create a circus atmosphere filled with joke coins. Then point at it and say, “See? Crypto is nothing but a giant casino. Let’s ban it.” Thankfully, they failed. Crypto just got its “get out of jail free” card. The US presidential election results freed crypto from its regulatory handcuffs.

“The incoming Congress will be the most pro-crypto we’ve ever seen. And Gary Gensler, the SEC chairman who made it his mission to strangle crypto innovation, exits on inauguration day. For the first time in years, entrepreneurs can build without fear of a lawsuit landing on their desk. Think of it as crypto’s legalization day.

“The market already smells this freedom. Just look at the charts of small, quality cryptos that were under the SEC’s thumb. VitaDAO (VITA), a project revolutionizing biotech funding, jumped 300%. Render Network (RNDR), “Uber for AI chips,” surged 100%. The Graph (GRT), which works like “Google of blockchain,” shot up 100%.

“These aren’t memecoins. They’re real businesses solving real problems. And now they can operate in the daylight instead of regulatory shadows. The next Amazon, Uber (UBER), or AirBnB (ABNB) might not be a traditional tech company. It might come from a crypto project that was just too legally risky to build until now. Get ready for an explosion of innovation and wealth creation in crypto markets. The wave of innovation that was bottled up for four years is breaking free…the coming wave of regulatory clarity will once again give ordinary investors the chance to get in early on quality projects. Get ready for the return of ICOs.”

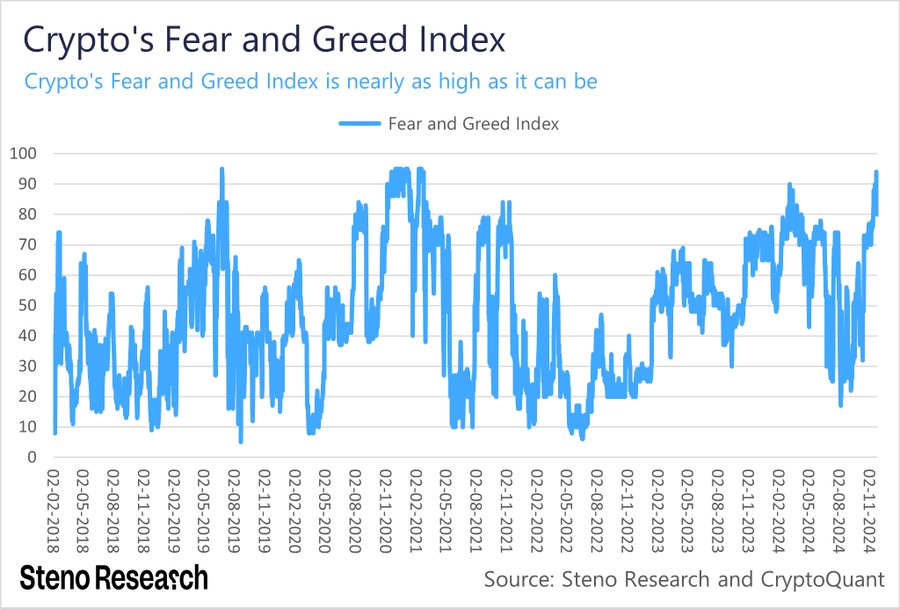

Bitcoin (BTC-USD on Yahoo – $99,423.96) cleared $100,000 before yearend, as I’ve been predicting all year in the Top Buys table, after Fed Chirman Powell said bitcoin is “not a competitor for the dollar, it’s really a competitor for gold.”

President Trump’s pick for the next head of the SEC, Paul Atkins, has previous experience at the SEC and is strongly pro-crypto. He founded Potomak Global Partners, an advisory for digital finance companies.

The Crypto Fear & Greed Index is sky-high, but as we know that is not a sell recommendation. It is a “keep your sneakers laced” recommendation because when the buyers run out of money there will be another patented bitcoin swoon. It’s just that the swoon might come from much higher levels.

Click for larger graphic h/t @AndreasSteno

Click for larger graphic h/t @AndreasSteno

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $56.40) and the other exchange-traded bitcoin funds just surpassed $100 billion in assets. There’s much more to come. IBIT remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $68.49

Oil has been flat under $70 for the last couple of weeks, even though the US expanded sanctions on Iranian oil exports, we saw Chinese factory activity growth, and this morning OPEC+ further delayed its planned output hike. The Treasury Department sanctioned 35 entities and vessels used to transport illicit Iranian oil to foreign markets in an effort to disrupt the use of oil revenue for the country’s nuclear program. As for the OPEC+ meeting this morning:

Click for larger graphic h/t @chigrl

Click for larger graphic h/t @chigrl

There are three tranches of the cuts. The unwinding of the first 2.2 million barrel layer has been pushed back by three months, and will be gradually returned over not 12 months but an 18-month period. The UAE agree to not only delay the start of its gradual quota increase by three months, but also see that increase come over 18 months versus the prior 9 months.

This agreement is HUGE. Ask yourself: Does this really look like a group fraying at the seams? As HFI Research wrote in The Narrative That The Saudis Will Launch An Oil Price War Should Go Right Out Of The Window After This OPEC+ Meeting: “The risk of an oil price war has gone down significantly, so if you see anyone spew this nonsense, you know they are not changing their opinion based on the changes in facts.”

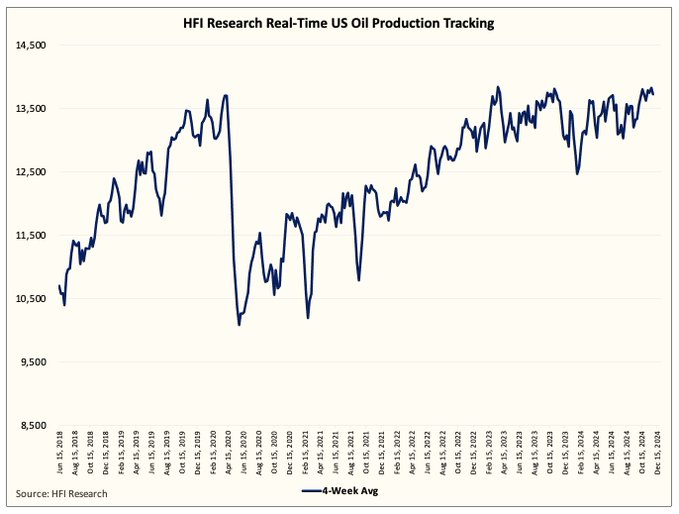

Meanwhile, November US oil production is done. There was NO uptick from October. We are going to exit 2024 closer to ~13.4 million barrels a day. People are literally not paying attention to this chart on US oil production. Why? Because the Energy Information Administration deliberately fed them bad data since 2022, and so they thought growth was super high. It’s not. Reality check? Flat since 2019.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

As Eric Nuttall wrote on the state of the oil market:

* * Global oil demand is at an all-time high

* * Global oil inventories are at an all-time seasonal low

* * US shale is growing at its slowest pace since its rise, other than during COVID or the Saudi spanking of 2016, and is clearly in its twilight

* * OPEC+ cohesion is strong as evidenced by the UAE concession, and they just proved that they will not “push” barrels onto the market, instead waiting for market conditions to allow for them to be “pulled”

* * EVERYONE is bearish due to 2025 non-OPEC growth projections, yet Brazil just disappointed by 350,000 barrels a day this year, or 30% of 2025 growth expectations. US ’25E too high as well?

* * After next year, non-OPEC supply growth will be less than global demand growth…forever…and will effectively stop growing in 2028

* * OPEC spare capacity is likely only ~4MM Bbl/d in a 104MM Bbl/d market, and is largely held by one sophisticated actor who can (and is) play the long game

* * Trump becomes President in ~1.5 months and his “maximum pressure” campaign could lower Iranian exports by 1.4 million barrels a day using existing sanctions, whose effectiveness (when actually enforced) is proven

* * Net speculative length remains low

“Remind me again…why is oil heading to $40/barrel and why is everyone so extremely bearish???”

The July 2026 Crude Oil Futures (CLN26.NYM – $67.17) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $36.46) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $10.03) is a Buy under $11 for a target price of $24 or more.

Primary Risk: Oil prices fall.

Energy Fuels (UUUU – $6.75) said the Madagascar Council of Ministers has lifted the suspension of the Toliara critical minerals project that was imposed in November 2019 on Base Resources. In October 2024, Energy Fuels acquired Base Resources and the Toliara Project.

CEO Mark Chalmers said: “The lifting of the suspension by the Malagasy Government is a very significant step in the development of the Toliara rare earths, titanium, and zirconium project. The Company can now re-commence development and other technical activities on the ground, which are expected to include the re-establishment of the Company’s social programs, additional mine planning and engineering, expanding the critical mineral resource base, as well as progressing any other legal activities necessary to progress the Toliara Project and achieve a positive financial investment decision.

“Having closely evaluated countless mining projects around the world during my 45-year career, I believe the Toliara Project is truly a ‘generational’ mining project, having the potential to provide the U.S. and the rest of the world with large quantities of critical minerals for many decades, including rare earth elements which we plan to process at our existing facility in the US.”

This was especially timely as China on Tuesday banned exports to the US of the critical minerals gallium, germanium, and antimony that have widespread military applications, escalating trade tensions the day after Washington’s latest crackdown on China’s chip sector. The curbs strengthen enforcement of existing limits on critical minerals exports that Beijing began rolling out last year, but apply only to the US. A Chinese Commerce Ministry directive on dual-use items with both military and civilian applications cited national security concerns. The order, which takes immediate effect, also requires stricter review of end-usage for graphite items shipped to the US. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

EQT (EQT – $44.45) will benefit from US data centers’ energy needs, which could boost gas demand by between 3 billion and 6 billion cubic feet per day (bcfd), according to S&P Global Ratings estimates. The agency expects US data center power demand to increase 12% annually until the end of 2030.

Virginia’s “Data Center Alley” alone hosts more than 3 gigawatts of data center capacity with 94 facilities connected since 2019, making it the world’s largest data center market. Projections suggest an additional 11 GW of capacity by 2030—equivalent to more than 40% of Virginia’s current peak demand.

Click for larger graphic

At the same time, President Trump’s transition team is preparing a sweeping energy plan for Day One in office, focusing on lifting restrictions on LNG exports. EQT has supply agreements in place for LNG exports. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

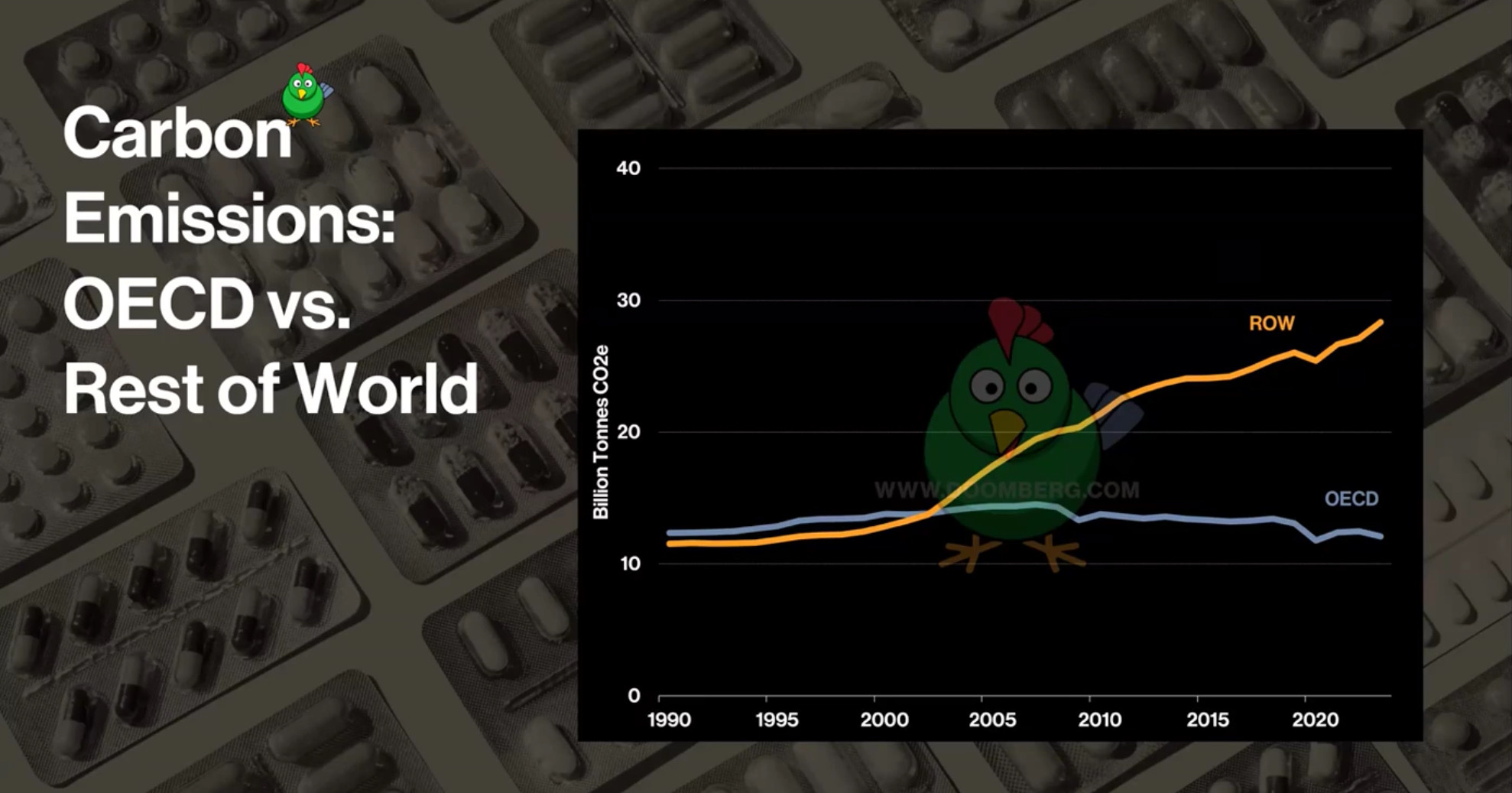

The West cannot materially impact global carbon emissions

Click for larger graphic h/t Doomberg

Click for larger graphic h/t Doomberg

* * * * *

HOW SMALL ARE WE?

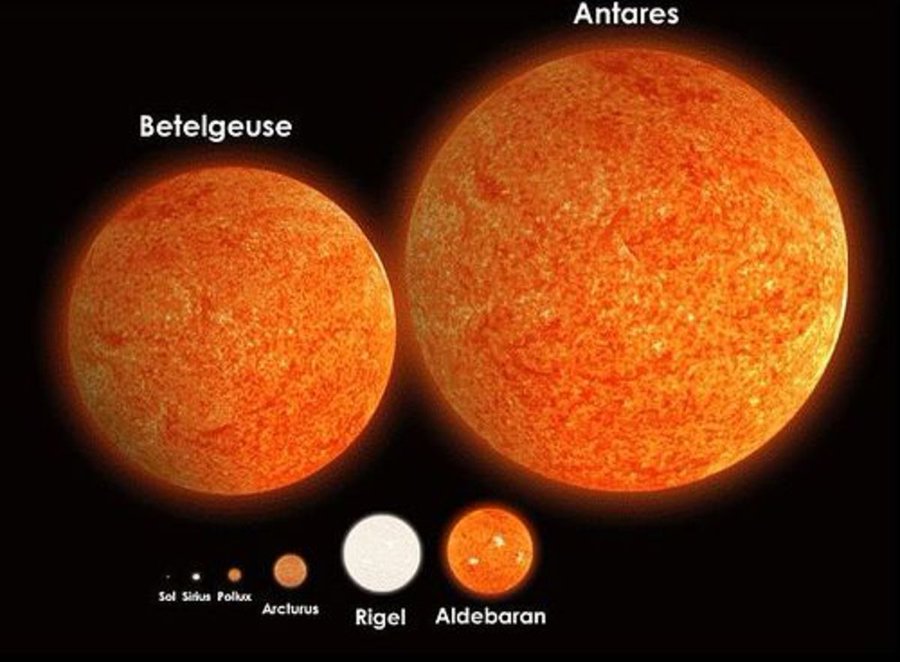

A human is minuscule compared to Earth—about 17.5 sextillion humans (17.5 × 10²²) would match its size (about 23 million people to go around the circumference of the Earth and over 7 million to reach the distance of the diameter). But Earth shrinks in comparison to the Sun, which is 109 times wider and so massive it could fit 1.3 million Earths inside. Even the Sun pales in comparison to Aldebaran, a red giant located 65 light-years away. Aldebaran is 52 times larger than the Sun and 150 times brighter. In a universe with 30 billion trillion stars, humanity is barely a speck in the grand cosmic scale.

Click for larger graphic h/t @MarioNawfal

Click for larger graphic h/t @MarioNawfal

* * * * *

Your reading over 300 pages of evidence from the CDC that show vaccines cause autism Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 12/5/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $49.76) – Buy under $33, target price $60

Gilead Sciences (GILD – $93.39) – Buy under $80, target price $120

Palantir (PLTR – $71.87) – Buy under $22, target price $100+

PayPal (PYPL – $89.04) – Buy under $68, target price $136

Snap (SNAP – $12.17) – Buy under $11, target price $17+

SoftBank (SFTBY – $30.02) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $9.30) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $64.87) – Buy under $60; 3- to 5-year hold

Fastly (FSLY – $9.93) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $20.99) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $7.31) – Buy under $10, target price $40

Rocket Lab (RKLB – $23.92) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $2.85) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $2.02) – Buy under $2, target $20

Compass Pathways (CMPS – $4.10) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $1.91) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $4.02) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.40) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.20) – Buy under $3, target price $20, then $50

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($31.80) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $30.10) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $38.87) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $24.58) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $39.97) – Buy under $30, target price $50

Coeur Mining (CDE – $6.80) – Buy under $5, target price $20

Dakota Gold (DC – $2.23) – Buy under $2.50, target price $6

First Majestic Mining (AG – $6.20) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.37) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.77) – Buy under $10, target price $25

Sprott Inc. (SII – $43.74) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $99,423.96) – Buy

iShares Bitcoin Trust (IBIT – $56.40) – Buy

Ethereum (ETH-USD – $3,835.83) – Buy

iShares Ethereum Trust (ETHA- $29.01) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $67.17) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $36.46) – Buy under $40; $100+ target

Vermilion Energy (VET – $10.03) – Buy under $11; $24 target

Energy Fuels (UUUU – $6.75) – Buy under $8; $30 target

EQT (EQT – $44.45) – Buy under $35; $70 first target

Freeport McMoRan (FCX – $42.79) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $243.04) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $608.93) – Expect to move back to Buy

TG Therapeutics (TGTX – $33.65) – Hold for buyout at $40+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

Much respect and appreciation goes out to your uncle Thomas who was on the Arizona. I have been there twice now over the years and each time it is a somber event. I can only imagine what those servicemen went thru those horrible hours of that attack. And it was even more impactful because I was serving on a Navy destroyer escort during my first trip to the Arizona. RIP

Check out the movie on NFLX. The only movie about Midway that I knew about was the star-studded one from the 1970s in Sensurround. That was a good flick, but this one from a couple years ago might be even better. The battle very easily could have gone the other way which would have given the Japanese supremacy in the Pacific. I have often wondered if the Creator made have had a hand in the outcome

Thanks Steve. Love to see it. Maybe over Christmas holidays when I visit my sister. I am too cheap to pay for Netflix!! Lol

TO: M. Murphy

In the bottom of your letter, where you summarize all the investments, you list SANDSTORM (Under inflation) with a target of $2538.87. I started to load up, but decided it might be an error (I’m joking). I thought you may want to fix this as it was there in the last newsletter also.

No, $2536.87 is right (also joking), Thanks! The right target is just $25. Thank you – fixed

MM and all – there are 3 HUGE secular growth segments of Crypto, Quantum computing, AI Tech – we can all make once in a lifetime gains with the right picks in these segments. Why cant this newsletter haveva section dedicated to these opportunitues?

MM let me say that differently as a question – can you/we dedicate a section of this newsletter to these 3 growth sectors while we are in early stages? Lets not miss the boat

I’ll ask again: Does anyone have any good recommendations in quantum computing? Are there specific companies with an edge or is it better to play the whole field with an ETF (QTUM)?

And add that I heard Keith Fitz-Gerald in a brief TV segment push his “buy the best; ignore the rest” thesis with a mention of IONQ following NVDA, TSLA and PLTR. (I picked up a few shares as a starter position and readily admit it was FOMO.)

MM? Anyone?

I like everything about IONQ except they can’t seem to make any money. I’d like to see the losses getting smaller, at least.

Thanks, Steve. Bitcoin has been the best crypto stock with ethereum #2. I’m looking at several altcoins with real businesses now that Gensler is on his way out.

Quantum computing is way too early.

AI tech – We’ve done OK with Meta and Palantir. It’s going to drive the next round of growth at Apple. Both Snap and Softbank are AI investments that should pay off big. So is PagerDuty.

I recommended Intel in Boomberg for the AI PC upgrade coming, but I strongly disagree with the Board firing Gensler. If they name a competent new CEO I’ll recommend it here.

The other huge secular growth segment is nuclear. I’d like to buy BWXT at a reasonable price, but for now UUUU is our only toehold.

MM- heres an exerpt from an article on cryptos with real businesses and utility, are any of these on yiur radar screen because tge time to act is now: VitaDAO (VITA), a project revolutionizing biotech funding, jumped 300%. Render Network (RNDR), “Uber for AI chips,” surged 100%. The Graph (GRT), which works like “Google of blockchain,” shot up 100%.

MM – nuclear seems like a much longer term bet and I wanna make profit before I die (joke) so wouldnt EQT and NG be a better near term bet?

They are a better near-term investment, but SMR nuclear is going to happen fast as the big data centers lock in power.

BTC now at $101,826.68. I am up 951 percent, ETH is $3838.65 up 86 percent and XLM (Stellar Lumens) moon shot is up 282 percent . 30K. Thank you for that recommendation. And a very merry Christmas to you too!!!

MM when will you have your alt coin recommendations and research ready?

AKBA–what are estimates for sales/marketing expenses for the rollout of Vafseo in 2025 and beyond? Who pays–dialysis organizations or AKBA? 50/50 or what? AKBA has already done a lot of marketing during the last 6 months to prepare for the launch.

MM, anyone–how does a strong dollar affect the outlook for oil, natural gas? You are already questioning whether we should hold or sell gold related investments. Although miners have leverage to gold prices, when inflation rises, their costs also rise, so gold itself may outperform miners.

Butler said they are using the current Auryxia sales force with only a few additions, so selling, general, and administrative expenses should stay around $27 million a quarter.

The dollar doesn’t really affect oil and natgas prices. It’s all about supply and demand. I think the traders are overestimating 2025 oil supply and undrestimating demand. Natgas demand depends on the weather, LNG exports, and data center electricity demand,

US $ relative to other fiat currencies is pure noise. It’s purchasing power is all that matters. Maybe not in my life time but at some point a new denomination will be issued…call it the Trump $….one of these or its equivalent for $1,000,000 current fiat. My grandfather bought a beach house in NC for $500 in 1931…it appraises today for $3 million and cost $30,000 a year to own and maintain….ridiculous.

Should that $500 over 94 years growing to $3 million is a CAGR of 9.69%.

9.69% compounded is an excellent steady rate of growth, tax free while you own it. But, $30K annual cost to own and maintain is 1%, equivalent to over 10% annual taxation, reducing the net tax free growth to 8.6%. That doesn’t count emotional costs of worries about hurricanes and other risks. Damn taxes cutting into growth. And that’s in a fairly low tax state, NC. What capital gains taxes do you face when you sell the house? Left coast states suck.

EDIT – MM cherry picked the BofA’a downgrade announcement to indicate the analyst was “Ignoring the fact that Editas has one of the best in vivo programs.”

The portion of the sentence left off from the downgrade announcement that addressed the in vivo program is in bold below:

Deprioritizing reni-cel does make sense from a cash burn perspective, but it removes a significant portion of the firm’s valuation with partner interest remaining to be seen. Given the increasingly competitive nature of SCD and thalassemia development, the firm sees the potential value of reni-cel waning as the field looks to in vivo therapies as the next logical step, adds the analyst, who notes that Editas’ in vivo HSC program is still “several years from prime time.”

EDIT’s pivot to focusing on in vivo may be promising but it also presents yet another delay for EDIT in getting a drug approved. It’s a little like APTO’s pivots & delays. Analysts aren’t going to assign much value to EDIT at this point for an in vivo program that is many years away from getting a drug approved.

Brent – I left that off because it is irrelevant. The reni-cell partnership is sure to include the in vivo follow-on drug.

EDIT issued a press release today that they were transitioning to an in vivo company, which we already knew. In connection with Editas Medicine’s transition to an in vivo company, the Company initiated a reduction in headcount that will eliminate approximately 65% of its workforce over the next six months.

What wasn’t mentioned in the press realease but came out in the associated conference call after the market close was that after an extensive search since late summer they were unable to find a partner for reni-cel and as a result they are shutting the program down. Hence the huge workforce reduction as they let go the folks associated with that program & try to right-size the company back to an earlier stage company.

Their cash burn will slow but also no reni-cel deal revenue. They are 2 years away from the start of any human clinical trials.

Thanks for the information. For BOF A to go from a buy at 13 dollar target to a sell at 1 dollar target is unreal. What changed ,they want a partner. I have 2000 shares and am down big. What target is reasonable?

Well worth reading.

https://www.crescat.net/the-history-of-the-us-dollar-cycles/

Just when you think it can’t get any worse. Why are they doing this at these prices?

INOVIO Announces Proposed Public Offering

4:01 PM ET 12/12/24 | Dow Jones

INOVIO Announces Proposed Public Offering

PR Newswire

PLYMOUTH MEETING, Pa., Dec. 12, 2024

PLYMOUTH MEETING, Pa., Dec. 12, 2024 /PRNewswire/ — INOVIO Pharmaceuticals, Inc. (Nasdaq: INO), a biotechnology company focused on developing and commercializing DNA medicines to help treat and protect people from HPV-related diseases, cancer, and infectious diseases, today announced that it intends to offer and sell shares of its common stock and accompanying warrants to purchase shares of its common stock, in an underwritten public offering. All of the securities in the proposed offering will be sold by INOVIO. The proposed offering is subject to market conditions, and there can be no assurance as to whether or when the offering may be completed, or the actual size or terms of the offering.

Oppenheimer & Co. Inc. and Citizens JMP are acting as joint book-running managers for the offering. Stephens Inc. is acting as lead manager for the offering.

A shelf registration statement relating to the shares of common stock and accompanying warrants offered in the offering described above was filed with the Securities and Exchange Commission (SEC) on November 9, 2023 and declared effective by the SEC on January 31, 2024. The offering will be made only by means of a written prospectus and prospectus supplement that form a part of the registration statement. A preliminary prospectus supplement and accompanying prospectus relating to and describing the terms of the proposed offering will be filed with the SEC and will be available on the SEC’s website at http://www.sec.gov. Copies of the preliminary prospectus supplement and the accompanying prospectus, when available, may also be obtained by contacting: Oppenheimer & Co. Inc., Attention: Syndicate Prospectus Department, 85 Broad Street, 26th Floor, New York, NY 10004, by telephone at (212) 667-8055, or by email at EquityProspectus@opco.com; or Citizens JMP Securities, LLC, 600 Montgomery Street, Suite 1100, San Francisco, California 94111, by telephone at (415) 835-8985, or by email at syndicate@jmpsecurities.com.

It’s the inherent risk in these biotechs, which often turns them into bio-wrecks. They take many years to bring a product to market and often encounter setbacks along the way extending the timeline even further. That results in a series of capital raises and the associated dilution only drives the price ever lower.

INO is burning $25M to $30M a quarter. They had $82M at the end of Q3, enough to get them into Q2 next year. But companies always try to raise capital a couple quarters before the runway end date. Companies low on cash don’t have the luxury of waiting for a better stock price. Many of these earlier stage biotechs that don’t yet have an approved drug trade based on their cash position, so their stock price drops as their cash position drops.

I would expect at least a $50M raise, which would get them two additional quarters of cash based on their current cash burn rate. But at today’s aftermarket price of ~$3 that’s 16.7M additional shares (and there will be warrants on top of that) or 63% dilution.

At least INO isn’t at APTO’s stage yet, which just sold 40M shares, plus 20M warrants, for a measly $8M. Through their recent reverse split they’d gotten the share count down to 19.5M shares only to incur another massive dilution.

New World Investor for 12.12.24 id posted.