Dear New World Investor:

Before the Fed meeting decision next Wednesday, we get November payroll growth tomorrow morning and the November Consumer Price Index next Tuesday morning. This week we found out that US job openings dropped to more than a 2½-year low in October. The Labor Department’s Job Openings and Labor Turnover Survey (JOLTS) showed that there were 1.34 vacancies for every unemployed person in October, the lowest since August 2021. That’s a strong sign to the Fed that demand for labor is cooling.

Click for larger graphic h/t @YahooFinance

Click for larger graphic h/t @YahooFinance

I expect the Fed to continue to pause – high, but no higher, for longer. And longer than the “rate cut is coming” crowd thinks.

Market Outlook

The S&P 500 lost 0.4% since last Thursday, even after posting a new 2023 closing high on Monday. A close above 4,796.56 on the S&P, 20% above the October 12, 2022, bear market low, would unleash a flood of articles and posts that the Index has been in a bull market since then. But for the last 50 years, the S&P 500 has logged average gains of only 0.2% and 2.0%, in the one-month and three-month period after a new bull market is confirmed. The Index is up 18.5% year-to-date.

The bear market that began when the S&P 500 hit its previous record on January 3, 2022, wasn’t that bad, down 25.4% at its lowest point. It was the fourth shallowest bear market since 1928, according to Yardeni Research. At the same time, at 282 calendar days, it was shorter than the average bear market length of 341 days. The good news: Over the past 50 years, the S&P had an average gain of nearly 260% during the six bull markets that occurred.

In contrast to the S&P, the Nasdaq Composite gained 0.8% and now is up 37.0% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 6.6%. Biotech stocks posted record gains in November due to the improving outlook. The XBI, representing over 130 biotech stocks, climbed about 14% while the S&P 500 added only about 9%. It still is down year-to-date, but only 3.0%.

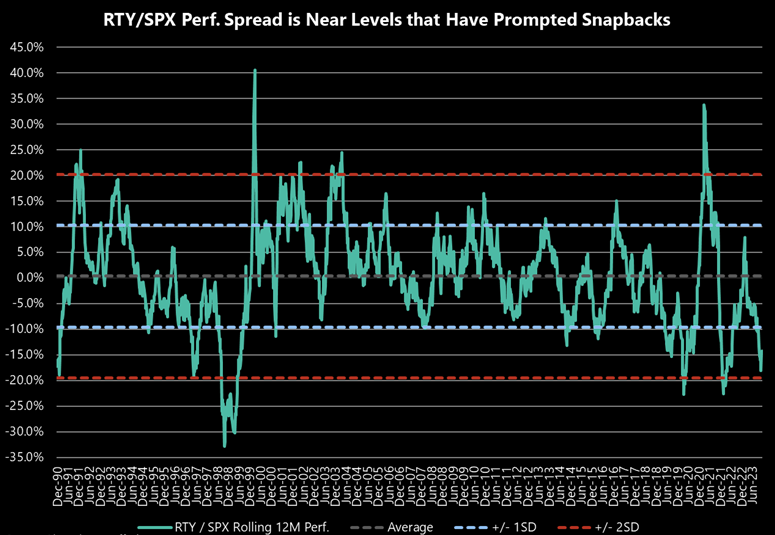

The small-cap Russell 2000 added 3.3% as the little guys rally continued. It is up 6.1% in 2023. Recent performance has been relatively terrible, with the rolling 12-month performance for the E-mini Russell 2000 Index Futures (RTY) relative to the S&P 500 reaching nearly -2 standard deviations. That has tended to be the level that has preceded extreme outperformance of small cap stocks, 2024 should be the Russell 2000’s year.

Click for larger graphic h/t @themarketear

Click for larger graphic h/t @themarketear

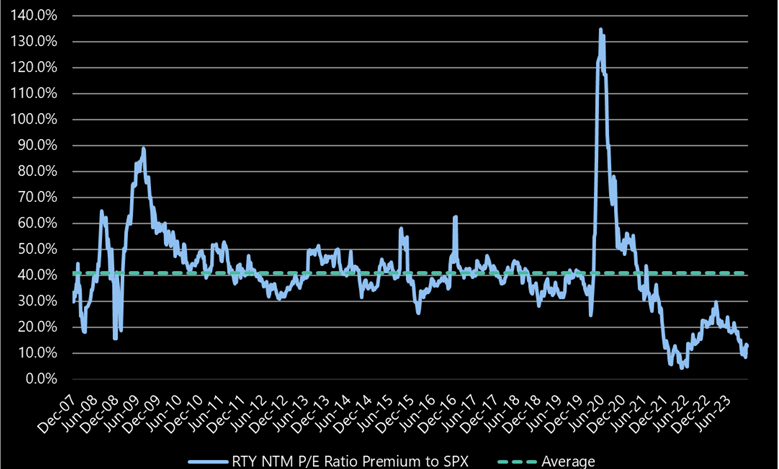

In addition to the standard deviation data, small-caps rarely get this cheap versus large caps. Using a simple next-12-months P/E ratio, the RTY is trading at just a 13% premium to the S&P 500. That level is near recent lows and well below where the relative valuation bottomed in the Great Financial Crisis. As a result – and unlike large caps – small caps are pricing in some pretty bad news already.

Click for larger graphic h/t @themarketear

Click for larger graphic h/t @themarketear

The fractal dimension stalled but still is signaling a major new uptrend is underway.

Top 5

Changes this week: Added SCYX and to get back to five recommendations I removed SFTBY, AKBA, and VLD (all still Strong Buys and all will be back)

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage this fall

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model forecast for December quarter real GDP growth has fallen shapely to +1.2%, the same as the Blue Chip economists. The main weakness is in personal consumption expenditures and private domestic investment growth, with a little from weak net exports.

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, December 8

November payrolls – 8:30am – +180,000 expected; October was +150,000

Saturday, December 9

APTO – Aptose Biotherapeutics – 6:15pm – American Society of Hematology (ASH) annual meeting

Monday, December 11

QUIK – QuickLogic – Unspec. – Oppenheimer 5G Summit: The Revolution Continues

Short Interest – After the close

Tuesday, December 12

Consumer Price Index – 8:30am

PZG – Paramount Gold – 11:00am – Annual meeting

Wednesday, December 13

Fed Meeting – 2:00pm press release; 2:30pm press conference

QUIK – QuickLogic – 9:20pm – International Conference on Field Programmable Technology, Yokohama, Japan

Friday, December 15

RKLB – Rocket Lab – Unspec. – Bank of America Virtual STARS Summit

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Meta Platforms (META – $326.59) is testing more than 20 new ways generative AI can improve user experiences across Facebook, Instagram, Messenger, and WhatsApp. They’ll apply it to search, social discovery, ads, business messaging, and more.

Meta and IBM formed the AI Alliance, a coalition of over 50 artificial intelligence firms and research institutes, advocating for an open-source model for AI development. Companies in the new alliance include AMD, Dell, Oracle, Intel, Sony, Fast.ai, the Mass Open Cloud Alliance operated by Boston University and Harvard, CERN, and more. The group’s stance differs dramatically from the closed approach of Google, ChatGPT-maker OpenAI, and Microsoft. META is a Buy under $150 for a $400 target in 2024.

Small Tech

Velo3D (VLD – $0.79) said their Sapphire 3D printers are the first to achieve the Department of Defense’s Green-level Security Technical Implementation Guide (STIG) compliance. This certification allows Sapphire printers to be connected to the DoD’s Secret Internet Protocol Router Network (SIPRNet). I didn’t even know there is a secret Internet protocol router network. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Aptose Biosciences (APTO – $2.68) presents the latest tuspetinib/venetoclax trial data on Saturday at the very important American Society of Hematology (ASH) annual meeting. I’m expecting another upside surprise, and I wouldn’t be surprised if a partnership or merger comes in the next few months. APTO is a Buy under $2.50 for a $300 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Compass Pathways (CMPS – $5.98) announced the publication of a paper in JAMA Psychiatry that demonstrates the potential for COMP360 psilocybin treatment in another disease, treatment-resistant bipolar type II disorder (bipolar II).

The primary endpoint of the study was the change in the Montgomery-Åsberg Depression Rating Scale (MADRS) total score from baseline to week three. All 15 participants had lower MADRS scores, with a mean change from baseline of -24.0 points at week three. Twelve participants met the response criteria and 11 met the remission criteria.

There was no increase in the suicidality score based on the MADRS, no manic symptoms and no unexpected adverse events or difficulties with the dosing sessions reported throughout the study. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Inflation MegaShift

Gold ($2,045.40) seems to have established a new price range above $2,000. It’s pausing before the push to new all-time highs. The fractal dimension stalled with this week’s spike and decline, but it’s within striking distance of 55, which will confirm a new uptrend.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

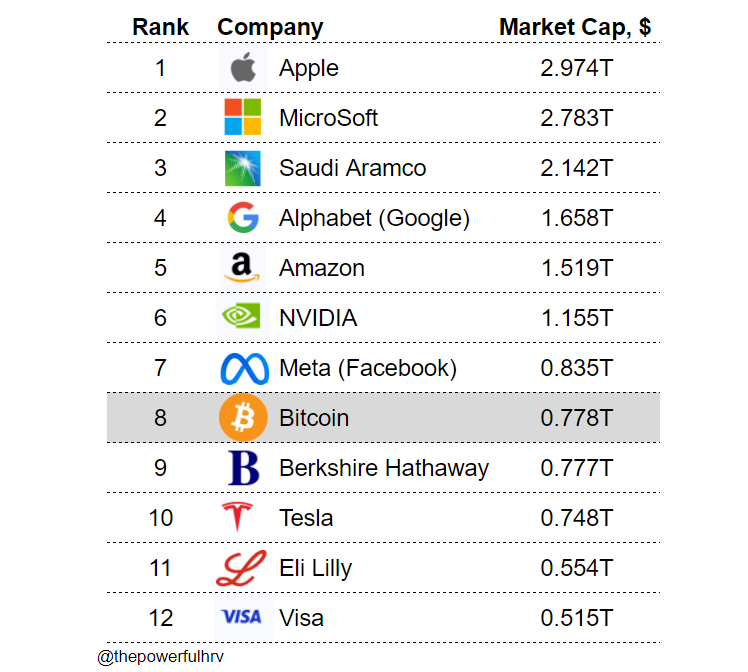

Bitcoin (BTC-USD on Yahoo – $43,340.03), according to Warren Buffett, is “rat poison squared” and “it is an asset that creates nothing.” This week, the market capitalization of bitcoin surpassed that of his company, Berkshire Hathaway.

Click for larger graphic h/t @thepowerfulHRV

Click for larger graphic h/t @thepowerfulHRV

With bitcoin solidly over $40,000 and on its way to $100,000, if I was a trader I’d sell it and wait for the SEC to go after Justin Sun and Tether. I might get back in close to $30,000, or I might miss the big move to $100,000 and beyond. So I’m not a trader.

Click for larger graphic h/t Bullion By Post

Click for larger graphic h/t Bullion By Post

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $33.90) is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $69.56

Oil has been weak and broke under $70 Wednesday in spite of extremely bullish news. As I predicted, US crude inventories fell a whopping 4.6 million barrels last week, far more than the expected 1.0 million barrels. It was the first draw in seven weeks as US refiners continued to raise their capacity use following the fall maintenance season. I do expect a big ~7+ million barrels build in crude this week due to low crude exports and high crude imports. Crude exports following this week are expected to be very high, so US commercial crude storage will be steadily lower into year-end. That should get oil back to $80.

Gasoline stockpiles increased by 5.4 million barrels last week. Analysts expected only a 700,000-barrel increase. Gasoline supplied, an indicator of demand, increased by 260,000 barrels a day, to 8.5 million barrels a day.

Geopolitically, over the weekend the Pentagon said that multiple US military and commercial vessels were attacked in the Red Sea, at time when the week-long truce between Israel and Hamas collapsed, sparking a resumption in the war.

ANZ Research wrote: “Crude oil prices near $80 a barrel look underpriced because the market is in deficit and inventories are low. Further, geopolitical risks are still looming, and a wider conflict in the Middle East will be a potential downside supply risk. If the US tightens its sanctions against Iran and Russia and OPEC+ voluntary cuts go as per plan, this severely tighten the market balance.”

Word. Yet Emotions Run Wild As Oil Bulls Question Their Existence.

The July 2026 Crude Oil Futures (CLN26.NYM – $65.38) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $34.49) is a Buy under $40 for a $100+ target.

International & Other Recommendations

It is important to hold some non-US assets, especially in China.

Acreage Holdings (ACRDF – $0.27) expanded its cultivation and processing facility in Egg Harbor Township, New Jersey. Thy said it was to support the ongoing demand for products at both the retail and wholesale levels, as well as the broadening of their brand and product offerings in the burgeoning New Jersey market. They had a record month of wholesale sales in August.

Although marijuana prices are very depressed at the grower level (welcome to farming), they said this new capacity lets them produce a larger and more diversified offering for two of the most popular segments in the market – premium flower and edibles – as well as top-selling concentrates for their Superflux line, which will reach consumers by year-end. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

* * * * *

Your Saving Wisdom Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 12/07/23. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $194.27) – Buy under $150 for new iPhones

Corning (GLW – $29.01) – Buy under $33, target price $60

Gilead Sciences (GILD – $78.05) – Buy under $80, target price $120

Meta (META – $326.59) – Buy under $150, target price $400

SoftBank (SFTBY – $19.51) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $11.28) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $50.65) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $16.84) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $21.90) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $11.30) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.70) – Buy under $13, target price $30+

Velo3D (VLD – $0.79) – Buy under $6, target price $50

$20-for-$1 Biotech

Akebia Biotherapeutics (AKBA – $1.17) – Buy under $2, target $20

Aptose Biosciences (APTO – $2.68) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $5.98) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.38) – Buy under $7, hold a long time

Invitae (NVTA – $0.58) – Buy under $10, first target $50, then $100+

Medicenna (MDNAF – $0.33) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.70) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $16.03) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($24.13) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $24.65) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $29.17) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.83) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $27.15) – Buy under $30, target price $50

Coeur Mining (CDE – $3.07) – Buy under $5, target price $20

First Majestic Mining (AG – $5.93) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.36) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.88) – Buy under $10, target price $25

Sprott Inc. (SII – $33.19) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $43,340.03) – Buy

Grayscale Bitcoin Trust (GBTC – $33.90) – Buy

Ethereum (ETH-USD – $2,350.966) – Buy

Grayscale Ethereum Trust (ETHE – $18.95) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $65.38) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $34.49) – Buy under $40; $100+ target

EQT (EQT – $36.99) – Buy under $35; $70 first target

Energy Fuels (UUUU – $7.31) – Buy under $8; $30 target

Freeport McMoRan (FCX – $36.37) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.61) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $20.63) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $11.78) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $26.97) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.27) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $0.99) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $9.50) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First

Three reasons why the FED will stop raising rates and then cut them. 1) the federal funds rate is now above treasury yields 2) the job market is weakening and the pace of inflation has continued to ease 3)Three of my newsletter editors are all saying the FED will stop/and lower rates. Some as early as January. Plus Powell is terrified he has gone too far and will trigger a recession in an election year.

John, I hope you and the newsletter authors your read is accurate!

Here is what one of them said. Gas prices have been down for 60 straight days. Indicators show the economy is doing great. Inflation is set to come under control without a recession or labor market destruction. A soft landing is the most plausible outcome. In the short term we will have a mild pull back which will be a buying opportunity. But markets will be up over the next year or two.

Stop raising rates, yes. But I doubt he’ll cut until he sees unacceptable weakness (anything that can’t be labeled a more-or-less soft landing). Also, he’s a Republican, although I doubt that influences his rate decision.

MM–please address my last post on VLD.

MM–on VLD, please critique this extremely bearish post from last PM.

6 hours ago (by ja)

“Been watching VLD crash now for the past 9 months.. great call option play on Ms Wood’s disrupter playbook.. Pretty sure it’s not going out of business.. They do need to start executing the $300 mil shelf as they will soon be out of $$.. So as a savvy investor it appears waiting till .30-.50 cent range a great play . this company market cap will fall below sales shortly.. Dilution will kill it further hence the 30 cent target.. Then I expect Elon Musk to ride in and buy it for nothing.. a pure gold mine for his companies.. First thing Musk does is fire the lame MGMT and start literally “printing bucks” at past shareholder expense.. Pathetic MGMT.

“You said their finances are not desperate, but the share price plunge is acting like 30-50 cents is a possible target. Normally, tax loss selling in a viable company is a buying opportunity, but there will be fear awaiting the next Q4 earnings or revenue news in several months.”

Yes, we know that VLD’s tech is wonderful. But how will the STIG certification build sales? As for the stock, Lazerator on YMB has a reasonable view of valuation. $100 million in 2023 sales divided by 200 million shares is 50 cents sales per share. At current share price of 78 cents, that’s a p/s of 1.6. That seems cheap, but it may be appropriate when sales continue to decline. (For rapidly growing companies like TGTX, p/s of 5-10 is appropriate.) But if Q4 and Q1 (2024) sales are poor, maybe a p/s of 1 is fair value, or a stock price of 50 cents.

So what do you view as a fair value with various sales projections? That includes the onerous new loan terms. Your buy price of under $6 is totally unrealistic at this vulnerable point.

No mention by MM that they are ISSUING stock for pennies ! And NO comment!

I thought the 11/30 issue covered it:

“The company exchanged the $70 million of senior secured convertible notes they sold on August 10 for $12.5 million in cash, 10 million shares of stock, and $57.5 million of new of senior secured convertible notes. This was expensive but necessary to cure the technical default to maintain minimum levels of quarterly revenue through the quarter ended June 30, 2026.”

Since 11/30, there have been announcements of share printing (selling) for severe dilutions. The YMB posters are thus predicting stock price bottoms of 30-50 cents. The stock has already plunged to 64 cents. It is trending much lower, and further tax selling could make it go much lower still. If Brent is right that 2024E sales will be $60-84 million, plunging sales means that an appropriate current p/s ratio could be 1.

Zweiter on YMB is wildly bullish based on DoD needs, but where are the orders from DoD?

To clarify, I was indicating what likely Q4 sales would be if multiplied by 4 quarters as contrast to MM’s expectations. I expect 2024 sales to somewhat exceed whatever VLD’s annualized Q4 sales turn out to be given how low the lower end of their Q4 guidance was.

I expect the next couple quarters to be rough due the customer service issues they called out in their Q3 call & lack of a sales backlog but currently expect the second half of next year to show some improvement. I think the analyst’s guidance if $104M is far more realistic then MM’s.

MM and Brent–future customer orders may be dropped if there is uncertainty about whether a financially shaky company like VLD will be around to service their concerns. VLD may not be the only company doing the high end of 3D printing and software.

What do you think about this?

MM – an abbreviated issue this week. Please give us some clarity on your bitcoin position. You’re not a trader as you say, but are you a long-term holder of bitty or GBTC? I’m trying to gauge your level of conviction on it as it has bounced around, how convinced are you it will hit $100k and what is your timetable? Lastly, what are your price projections and timetable on Ethereum and ETHE?

adding to the above almost all those closest to it say the BTC spot ETF will be approved in the first quarter (see chart attached forhow many have applied) so do you still expect a short term drop to $30k with ETFs being launched?

I more leery of it than expect it, as it’s what Wall Street does best: panic the unprepared and buy their stuff cheaply. I also am worried that the SEC will take out Tether before they approve spot ETFs. That would hit bitcoin hard. But I recommend just holding through whatever comes.

Yes, not much news during the holidays with the quarter-end approaching and brokerage firm conferences stopped. I am a long-term holder of bitcoin and think it could hit $100K before the 2024 halving. It will drag ethereum along, but as you know there is no cap on the number of ETH that can be created (negative) but it is easier to build other tokens on it (positive). For the raging bull case, see https://seekingalpha.com/article/4656966-grayscale-ethereum-trust-buy-this-nav-discount-opportunity.

Revenues

2021 $27.4 million

2022 $80,7 million

2023E $101.4 million (2 analysts)

2024E $112.7 million (2 analysts – I’m at $113-$120 million))

Tech companies don’t sell for 1x sales. I could see it at 3x ($1.50) until they show accelerating growth. That comes from two forces:

One of those 2 analysts obviously hasn’t updated their 2023/2024 numbers to reflect VLD’s Q4 guidance as their Q4 sales projection exceeds the top end of VLD’s Q4 revenue guidance range. The other analyst, who did update numbers, has a 2023E of $95.5 million, which reflects roughly the midpoint of VLD’s broad $15M-$27M Q4 guidance range. That analyst has a 2024E of only $104.2 million.

Your reasons for VLD to perform well in 2024 hold true for 2023 as well yet VLD sales have declined every quarter this year.

It’ll take a couple quarters minimum to reestablish a backlog cushion that will enable VLD to reestablish a positive sales trend.Your prediction of $113-$120 million to seems to be overly optimistic. If VLD comes in at the lower half of their $15M-$27M Q4 revenue guidance, which seems likely based on announced sales so far this quarter, that would equate to annualized revenue of $60 million to $84 million.

VLD plunged today only 10% vs the 21% in the previous session. Now Lazerator added that the SHORT TERM bottom could be 50 cents, whereas the long term bottom will depend on 2024 sales. I wonder if the extreme negative sentiment is already discounting poor sales.

MM–DoD would seem like the MAJOR LARGE customer of VLD. Where are their orders? Why is it taking so long–the usual slow moving bureaucracy? There’s been plenty of defense spending for Ukraine, Israel–why not VLD?

I don’t understand the latest dilution info and projections from after your 11/30 update. Can you clarify? The stock is plunging today as fast as on the previous trading day, Fri. Management has been selling shares lately–why?

MM–I congratulate you for your conviction that ARTH will succeed one day. Almost all of us sold out long ago, due to repeated failures to make even a few sales of AC5. A few people like Artbill and John Miller added at 60 cents and have mega-bagger returns on that, although if they held their 99% losing positions, they are still net down a lot from their original buy price. Probably NOT ONE worldwide investor out of several thousand waited patiently patiently patiently before buying for the first time at 60 cents, or 0.30 CENTS before the 200:1 reverse split.

So the key to investment success with NWI is to wait 5-10 years after a typical overoptimistic recommendation before buying. The companies are interesting speculations and can be financially life changing, but only if the investor pays attention to valuation, taking into account common risks of speculative businesses and financing. This applies to VLD, TGTX, SCYX, AKBA, which will be life changing investments after many years of huge losses, BUT ONLY NEAR CURRENT depressed prices.

So please address our concerns about valuation, using your expertise as a financial analyst. Thanks.

Well said,amen

Nvta,buy up to 50.00 dollars in 2021,now it trades at 56 cents

Not sure if arth even reported any numbers,but since the last time they stated they earned 1600,if they state they earned 4800 that’s huge,so I guess that’s enough for the share to be manualated like it has been,way to go TN

This illustrates that stocks can rise hugely when awful conditions improve to merely bad. If 4800 is true, it is not enough to let ARTH survive on its own, so hopefully there will be a buyout. NWI stocks must be bought only when conditions are awful, with reasonable prospects of improving, even a little.

4800.00 was just a guess,they never stated,just that it was substantial,compared to the previous quarter

Right. I also noticed that they didn’t specify the amount of sales. Compared to the nil last quarter, it was probably still small. It seems that the evasiveness of management hasn’t changed.

ACXP – for those following ACXP…

Acurx Announces Positive Phase 2b Results Showing 100% of Patients Who Had Clinical Cure with Ibezapolstat Also Had Sustained Clinical Cure

https://ir.acurxpharma.com/press-releases/detail/68/acurx-announces-positive-phase-2b-results-showing-100-of

Although the market doesn’t appear to recognize the significance of this latest news from AcuRx, any hospital administrator reading this would be VERY interested. Why? Because hospitals do not get reimbursement for a second round of treatment for C. Diff patients who have a recurring infection within 30 days. The hospital has to eat the cost of treating those patients again and this is a very significant expense. None of the patients who received ibezapolstat had a recurring infection within 30 days while 14% (2 of 14) of the vancomycin treated patients did. Although patients treated with vancomycin in this study did better than the 25% historically who have a recurrence after a first C Diff infection ( Kelly CP. Clin Microbiol Infect. 2012;18:21-27. doi.org/10.1111/1469-0691.12046. ; Cornely OA, Miller MA, Louie TJ, Crook DW, Gorbach SL. Clin Infect Dis. 2012;55:S154-S161. doi: 10.1093/cid/cis462. ) the SUSTAINED clinical cure rate has always been the biggest selling point for ibezapolstat. If it weren’t for the fact that recurrence is so common in C Diff cases, C DIff would not be the headache that it is for hospitals. Not having to worry about a patient returning in 30 days is a major selling point for ibezapolstat. Per Nestle (maker of VOWST) there are about 170,000 cases of recurrent C Diff annually.

Great info, thanks. I eagerly anticipate the update on sustained cure at 3 months. Even if hospitals will get paid for recurrences after 1 month, it still is a nuisance for patients to get recurrences at any time, even 6 months. I don’t know what are the average recurrence rates at various times after treatment for Vanco. I’ll read the paper soon.

BTW, are you the same Chris who said on YMB for VLD that he wouldn’t touch VLD with a ten foot pole? That expression dates us–I doubt young whipper snappers use that expression.

Different Chris, and though I share that Chris’s sentiments, I still am rooting for VLD. But if they can’t get their bookkeeping straight they are not investable by my standards. Also, I imagine the youngsters still use the “ten foot pole” expression, but “whipper snapper” is definitely old-school.

There seems to be exaggerated FUD going on about VLD. Today on YMB they said the CEO is dumping shares. On the website, I looked at SEC filings. There was a 12,000 share sale a week ago when the price was about $1. For about 5 sessions after that, only 2000 shares sold daily. I wouldn’t call that dumping as if there were an apocalypse. This looks like panic retail selling, aggravated by tax selling.

MM–please discuss the bookkeeping concerns of Chris. I am a novice at reading financial statements.

What do you think of today’s developments in ACHV? I didn’t see official news, but YMB is all abuzz over some FDA delay asking for more long term data? Does that justify today’s big haircut?

The 8-K left me with several questions, but I bought some ACHV 2.50 June Calls on the weakness. Perhaps we will get some clarity when the CEO talks Thursday at 10:30 at https://bit.ly/3tcvQkS

Oppenheimer price target lowered to $18.

When do you see dilution coming, and how much? We might learn more at 10:30 AM today.

Chris, where do you see AXCP stock price going over the next 3-6 months?

See my gloomy response to Chris just below.

I think they have a superior drug for C. DIff and believe several Big Pharma partners will compete for the drug. I think Acurx will try to sell the drug or company rather than conduct a Phase 3. Pfizer said their drug could be worth a billion dollars before it failed in Phase 3. So if ACXP’s drug will also be worth that amount after approval, you would have to value it far less at this pre-Phase3 stage. Is it worth $300M? $200M? Even at just $100M that’s 2.5x current market cap or $8.65/share. $200M would make it worth $17.30/share. Will that happen in the next 6 months? I think so, but if we have to wait, I will continue to buy on weakness just because I think they have a valuable asset that several companies will compete to acquire. Look at the options market. People are offering good money for the right to buy shares at $10 between now and April 19. For the past couple days someone has paid $.30 and $.55 for the right to buy shares at double today’s price. For the past week there have been buyers of options to pay $9 for shares between now and January 19! If you owned shares and were willing to accept over 100% profit in less than 6 months, you should sell some of those Calls. Of course you would also be leaving money on the table if a buyout occurs at an amount higher than your strike price, but a double in less than 6 months is not bad at all.

Option pricing seems convincing, but the crucial question is what are the odds of BP buying Ibeza before phase 3, based on a measly difference of 2 patients’ recurrence on Vanco vs 0 patients on Ibeza? 14 patients is too few to draw any firm conclusions. Of course, at this stage BP won’t pay much compared to what they would pay after a confirmatory phase 3. At this stage it is still a gamble for BP despite the great theoretical science of the microbiome. If phase 3 costs BP a few million bucks, that is a much cheaper gamble than 100 million bucks to buy it. So I guess funding a phase 3 is more certain than an early buyout of Ibeza. In that case, the stock could go to $5 or so, with a likely big payday for ACXP investors in a year or more. I’d be happy to be patient for that scenario.

I read a few papers by Kelly and Cornely. Most of the 25% recurrences of C Diff occur within 30 days. I don’t think the 94 day observation for recurrence will add anything. Most mild/moderate cases of C diff are treated with oral metronidazole, a cheap drug, but severe cases are treated better with Vanco. Oral Fidaxomicin has a somewhat lower recurrence rate than Vanco, so I wish the comparator trial had been done with Fidaxo rather than Vanco. While the 2/14 30 day recurrence with Vanco is worse than the 0/14 recurrence with Ibeza, it is only for a small number of patients. I guarantee that phase 3 will be required to generate more data before any Big Pharma buyout. The only hope for the stock is if a BP is interested enough to partner and fund phase 3. ACXP does not have the funding now to do phase 3 alone. They don’t have the ability to get the large phase 3 done in a timely manner. I am stuck holding my shares at an average cost of $4.44. If no partner is willing to step up, the stock could plunge to the fairly recent price of just over $1.

Ryan on YMB 1 hour ago posted a buyout is coming at $35. I strongly disagree. Many people are hoping for a buyout at this stage, before phase 3. RUBBISH. If BP wants to take a gamble before phase 3, they won’t offer more than $10. If they agree to fund phase 3, it could take until at least 2025. At that point, a buyout way over $!0 could happen. It is likely that phase 3 would confirm the theoretical superiority of Ibeza and the good phase 2B results to date.

Yep,I’m a holder of a lot of these like nvta,vld,what a Christmas,merry freking Christmas to me for being stupid and believing in MM,praying for a miracle some kind rebound,unbelievable

Hey Wendy if you are still out there,hope all is well,miss your input,

I fear she got swallowed up by one of her conspiracy theories. Before that she was a good and perceptive commentator, especially on things she knew something about. And then she dropped out. Like Show Me The Money, Drs Wayne and John Peterson, and oldster. Sometimes they say goodbye. Sometimes you never know. RIP Donald Galamaga. Miss your cheery good mornings.

The FED gods have spoken. Dow is up 500 plus points in one day. 3 rate cuts in play for 2024. My winners, SOFI up 35 percent, TGTX up 25 percent, SMCI up 330 percent, AAPL up 191 percent, WMMVF up 44 percent , INTC up 55 percent, QUIK up 44 percent and others. Lovin it!!

NVTA – Invitae Divests Ciitizen Health Data Platform and Implements Further Cost Cuts

https://ir.invitae.com/news-and-events/press-releases/press-release-details/2023/Invitae-Divests-Ciitizen-Health-Data-Platform-and-Implements-Further-Cost-Cuts/default.aspx

MM, please see the post below from Stocktwits regarding the independent consultant that NVTA hired.(especially the last sentence) What are your thoughts on this? Thanks!!

Jill Frizzley has been hired for a monthly fee of $40,000. I would like to believe that she was brought in for the company’s turnaround, but when looking at her work history over the past five years, she has served as a director at Proterra Inc. (since August 2023) and iMedia Brands, Inc. (since April 2023). She also held director positions at public companies such as Virgin Orbit Holdings, Inc., Surgalign Holdings, Inc., Avaya Holdings Corporation, Hudson Technologies, Inc., and Vivus, Inc. during the last five years. The commonality among these companies is that they all went bankrupt.

New World Investor for 12.14.23 is posted.