Dear New World Investor:

The recent catch-up rallies in German stocks, financial sector stocks, China technology, and even the ARK Innovation Exchange-Traded Fund (ARKK) mean we are in a “broadening bull.” This is when we suddenly and very quickly have an aggressive broadening of the rally. It could be a “buy the laggards” meme or just a general broadening, but it normally happens in just a fraction of the time that the overall bull has been in place.

So what are the next potential laggards to catch up? My guess is (1) junior miners catching up to record gold prices, and (2) biotech, driven by an acceleration in positive clinical results and increased FDA approvals under the Trump/Kennedy regime.

Market Outlook

After today’s drop, the S&P 500 is unchanged since last Thursday. The Index is up 4.0% year-to-date. The Nasdaq Composite also was flat and is up 3.4% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) gained 2.1%, perhaps beginning its catch-up move. It is up 3.0% year-to-date. The small-cap Russell 2000 dropped 0.1% and is up just 1.4% in 2025.

The fractal dimension almost – but not quite – signaled a new trend before flattening this week. If this really is going to resolve with another upleg, it should start soon. Otherwise, one of the regular 10% corrections probably looms.

Click for larger graphic

Click for larger graphic

Top 5

Changes this week: None

Near-Term – chronological order

AKBA Akebia Therapeutics – Vafseo launch

SCYX – ScyNexis – Announce resolution of the manufacturing problem, lifting of clinical hold, restart of MARIO trial, maybe GSK files for hospital use approval

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model for March quarter real GDP growth is down to +2.3% due to weakness in retail trade and industrial production.

Click for larger graphic

Click for larger graphic

The long-awaited credit crunch has arrived as credit card lenders wake to the sweet smell of BNPL in the morning.

Click for larger graphic h/t @DiMartinoBooth

Click for larger graphic h/t @DiMartinoBooth

Dollar Death Watch

Sometimes, things really are that simple.

Click for larger graphic h/t @eliant_capital

Click for larger graphic h/t @eliant_capital

You may remember that the dollar initially rallied up into January of 2017 following President Trump’s first victory before peaking and declining over 14% that year.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Sunday, February 23

INO – Inovio – 3:00pm – Poster at American Association for Cancer Research – Immuno-Oncology

AG – First Majestic – Through 2/26 – BMO Global Metals, Mining & Critical Minerals Conference

Tuesday, February 25

CDE – Coeur Mining – 8:00am – BMO Capital Markets Global Metals, Mining & Critical Minerals Conference

PYPL – PayPal – 8:30am – Investor Day

AAPL – Apple – 11:00am – Annual meeting

QUIK – QuickLogic – 5:30pm – Earnings conference call

Wednesday, February 26

QUIK – QuickLogic – 1on1s – Oppenheimer Emerging Growth Conference

Short Interest – After the close

NVDA – Nvidia – 5:00pm – Earnings conference call

Thursday, February 27

CMPS – Compass Pathways – 8:00am – Earnings conference call

December quarter GDP – 8:30am – Second estimate

RKLB – Rocket Lab – 5:00pm – Earnings conference call

ABCL- AbCellera – 5:00pm – Earnings conference call

TGTX – TG Therapeutics – 6:00pm & 6:45pm – Three poster presentations at Americas Committee for Treatment and Research in Multiple Sclerosis (ACTRIMS) annual forum

Friday, February 28

MDNAF – Medicenna – 1on1s – B. Riley Securities Precision Oncology & Radiopharma Conference

Personal Consumption Expenditures Index – 8:30am – The Fed’s favorite inflation indicator

TGTX – TG Therapeutics – 6:45 – Poster presentation at ACTRIMS

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $245.83) introduced the iPhone 16e at $599 or $24.95 a month for 24 months. It will be a smash hit because it uses the 16’s processor, battery, and camera and can run all the Apple Intelligence features. It only comes in black or white for now, but since almost everyone uses a case (my favorite HERE) that shouldn’t hurt sales.

Soccer is the most popular sport in the world. Major League Soccer kicks off its 30th season this Saturday on MLS Season Pass on Apple TV, with all 30 teams taking the pitch for “MLS is Back” weekend. Fans in more than 100 countries and regions can sign up for MLS Season Pass to access every MLS game with no blackouts. AAPL is a HOLD – I expect to move it back to Buy under $175 for new iPhones.

Gilead Sciences (GILD – $110.03) was granted priority review for its twice-a-year version of lenacapavir for the prevention of HIV as pre-exposure prophylaxis (PrEP). The Prescription Drug User Fee Act (PDUFA) target date is June 19. Lenacapavir got Breakthrough Therapy Designation for PrEP in October 2024. GILD is a Long-Term Buy under $90 for a first target of $120.

Meta Platforms‘s (META – $694.84) Instagram is introducing a new way for creators to work with brands to make money by recommending products. They introduced an addition to their Partnership Ads called Testimonials, which allows creators to get paid via written endorsements, shared as comments on the brand’s social media posts and advertisements. META is a Hold – Buy or add whenever it hits its lower Bollinger Band, now under $645.

Micron (MU – $103.18) announced its DRAM supply contract with Samsung for the Galaxy S25 phones that I told you was coming. Nothing like winning a contract with the sister company of your #1 competitor. Ouch! Look for the South Korean version of “heads will roll.”

They also introduced their next generation Solid State Drive (SSD) for PC manufacturers that doubles the performance of its predecessor. MU is a Buy under $102 for a $140 first target.

Nvidia (NVDA – $140.11) reports January quarter results after the close next Wednesday, and again the whole short-term direction of the stock market depends on the results. The consensus is expecting revenues up 72.5% to $38.13 billion with earnings of 85¢ per share. March quarter guidance should be for $42.0 billion and $91¢. I expect Nvidia to beat and guide above all four numbers, but…be ready for “didn’t beat by as much as last time” from traders hoping to shake some rubes out of their stock.

CEO Jensen Huang did a wide-ranging, hour-long on his vision for the future.

NVDA is a Buy under $125 for a $180 first target.

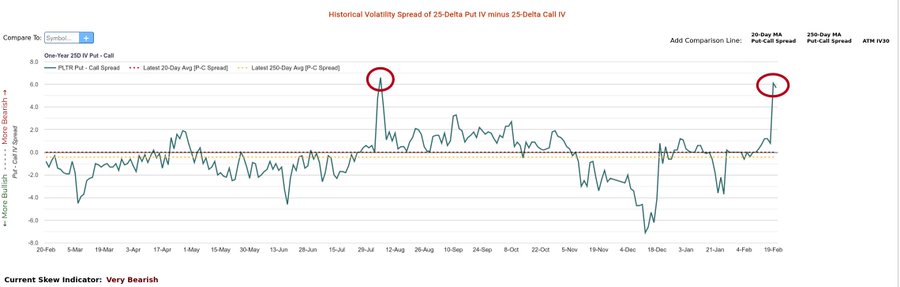

Palantir (PLTR – $106.27) dropped 10% on Wednesday and another 14.5% on Thursday to an intraday low at $95.80 before recovering to close down “only” 14.7% from Tuesday’s close. The stated reason was a Washington Post report that said Secretary of Defense Pete Hegseth sent a memo to senior leaders within the Pentagon and US military to slice 8% from the defense budget every year over the next five years, potentially equating to tens of billions of dollars in cuts. Hegseth wrote: “Our budget will resource the fighting force we need, cease unnecessary defense spending, reject excessive bureaucracy, and drive actionable reform including progress on the audit.”

Apparently a large number of people on Wall Street who must have no idea what Palantir does thought this cast doubt on a major source of PLTR’s revenue. As if! This will be great for Palantir because their software is great at cutting unnecessary spending and focusing resources where needed. Their revenues are about to go up, not down.

The bearish traders got way ahead of themselves again. Options skew towards put premium is blown out again. The last time options skew was this bearish on Palantir, the stock bottomed and then moved from a low of $21.23 to $125.

Click for larger graphic h/t @Mayhem4Markets

Click for larger graphic h/t @Mayhem4Markets

I am raising the buy limit to $100 and the target price to $150.

CEO Alex Karp did another talk on his book tour.

PayPal Holdings (PYPL – $77.63) holds their Investor Day next Tuesday. PYPL is a Buy under $68 for a double in three years.

Small Tech

Enovix (ENVX – $11.48) reported record December quarter revenues up 31.1% from last year to $9.70 million, soundly beating the $8.77 million estimate. The pro forma loss of 11¢ a share trounced the consensus expectation for an 18¢ loss. On the conference call (AUDIO HERE and PRESIDENT’S LETTER HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Raj Talluri said: “In the fourth quarter of 2024, we achieved key milestones in manufacturing, technology, and sales, setting the stage for a breakout year in 2025. We are focused on launching our first smartphone battery and converting our IoT pipeline into contracted backlog. Customers across multiple industries are acknowledging the readiness of our manufacturing capabilities, which are coming online at the perfect time to meet strong demand for our high energy-density solutions and diversified supply chain.”

Click for larger graphic

Click for larger graphic

They shipped early engineering samples to their lead smartphone OEM that are passing the critical safety tests. Enovix is on track for smartphone battery mass production in the fourth quarter. A new OEM customer submitted a purchase order for first samples, expanding their active engagements to seven of the top eight smartphone OEMs.

Enovix can deploy a new smartphone battery production line for $60 million. Each line produces 1,650 batteries per hour and generates $150 million in revenues a year. At a 50% gross margin, that’s $75 million in gross profit – a payback period on the capital spend of less than a year.

Click for larger graphic

Click for larger graphic

They also have a prepaid purchase order from a global technology leader in Artificial Intelligence and immersive technologies – probably Meta – reserving dedicated production capacity for their next-generation smart eyewear – probably the new Ray Bans I wrote about. Enovix made a new variant of EX-1M designed to fit within the confines of the glasses frames and shipped first samples from Fab2 earlier this month.

Click for larger graphic

Click for larger graphic

Market research firm IDC thinks the smart eyewear market will reach multiple tens of millions of units by 2028, driven by recent hardware and software advances, the growing adoption of AI applications, and the expanding use cases across consumer, enterprise and defense markets. A majority of America’s largest tech companies, along with several top-tier Asia-based OEMs, have announced smart eyewear products. Raj pointed out that no product today has a battery that can deliver all-day usage due to ever-increasing sensor, communications, and computing demands. Enovix’s high-energy-density battery makes them well-positioned to lead in this space.

Click for larger graphic

Click for larger graphic

Since the Presidential election, the company has seen increasing interest from drone manufacturers and defense suppliers seeking battery solutions that comply with allied country supply chain requirements, a.k.a., not from China. A significant portion of their 2024 revenue came from sales of conventional graphite battery products to defense customers.

Raj guided the March quarter to revenues between $3.5 million and $5.5 million with a pro forma loss of 15¢ to 21¢. The Street was at a loss of 17¢ but a revenue estimate of $6.21 million. Based on the revenue “shortfall” (I’m pretty sure Raj is sandbagging), the stock sold off after hours but recovered on Thursday.

Enovix finished the year with $272.9 million in cash, which gives them a cushion to install more high-volume production lines as required for future orders. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

QuickLogic (QUIK – $8.13) reports December quarter results after the close next Tuesday. The consensus is expecting revenues down 18.9% to $6.07 million with earnings of 3¢ per share. March quarter guidance should be for $6.15 million and 2¢. Those are low bars to beat. The next day they’re doing 1-on-1s at the Oppenheimer Emerging Growth Conference, and CEO Brian Faith probably wants to have some good news. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $25.26) reports their December quarter after the close next Thursday. Wall Street is looking for revenues up 117.65% to $130.57 million with a loss of 7¢ per share due to Neutron development expenses. March quarter guidance should be for $137.31 million and an 8¢ loss.

They successfully launched their 60th Electron mission to deploy the next satellite in the Earth-imaging satellite constellation of real-time space-based intelligence company BlackSky. This mission launched only ten days after Rocket Lab’s previous Electron launch, It was the ninth Electron launch for BlackSky since 2019. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $3.14) also is reporting December quarter results after the close next Thursday. Wall Street is looking for revenues down 17.62% to $7.58 million with a loss of 15¢ per share. March quarter guidance should be for revenues up 40.33% to $13.97 million and a 17¢ loss. But no one really caress about the numbers – it will be news on drug progression or new partnership deals that move the stock. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $1.91) has been weak. I keep buying a little more each week, looking forward to their comments on the Vafseo launch when they report December quarter results in mid-March. It’s back under my buy limit. Buy AKBA up to $2 for the Vafseo launches in the EU, UK, and US.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: 2026

Probable time of next financing: Never

Editas Medicine (EDIT – $2.06) closed last Thursday at $1.23 on 1.13 million shares. It usually trades 1.0 million to 1.5 million shares a day. On Friday it moved up 12% to $1.38 on a whopping 8.9 million shares.

Now, here’s the thing. Around 27% of float is sold short and it would take 8.7 days of volume to cover. Shorts were biting their nails the whole three-day weekend in case Astra Zeneca, Pfizer, or any other Big Pharma was about to bid. That didn’t happen, but on Tuesday some rushed to cover anyway. EDIT closed up 26% at $1.74 on another heavy volume day of 9.9 million shares.

That caused the shorts to panic. Wednesday volume hit 49,891,300 shares and the stock closed near its high at $3.20, up another 83.9% and up a total of 160% from last Thursday’s close. This was a short squeeze, pure and simple. It may have been deliberate, although I didn’t see any GameStop-style posts. Today, the stock fell back 35.6% to $2.06 on “only” 16.2 million shares. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2026

Probable time of next financing: 2026 or never

Inovio (INO – $2.22) said that peer-reviewed data from its Phase 1/2 clinical trial of INO-3107 as a treatment for recurrent respiratory papillomatosis (RRP) were published online in Nature Communications under the title DNA immunotherapy for recurrent respiratory papillomatosis (RRP): phase 1/2 study assessing efficacy, safety, and immunogenicity of INO-3107. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Early 2026

Probable time of next financing:After FDA approval in 2026

Medicenna (MDNAF – $0.86) reported December third quarter results. R&D was $3.4 million compared with $3.0 million last year. They had increased clinical costs related to the MDNA11 ABILITY-1 Study, which has expanded to new clinical sites and enrolled more patients in the current period relative to the prior period. R&D also included the combination portion of the MDNA11 study with KEYTRUDA during the current period, which had not commenced in the prior period.

They kept a tight grip on General & Administrative expenses at $1.7 million versus $1.8 million last year, and had a bottom-line loss of $5.0 million or 7¢ a share.

Their remaining milestones for 2025 include:

Click for larger graphic

Click for larger graphic

Medicenna finished the quarter with $30.0 million in cash, enough to get through the completion of the MDNA11 ABILITY-1 trial into mid-2026. Buy MDNAF under $3 for a first target of $20.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

Inflation MegaShift

Gold ($2,952.80) hit new all-time highs today as a hedge against President Trump’s tariff plans for cars, semiconductors, and pharmaceuticals, as well as – equally important – his plan to audit how much gold really is in Fort Knox. The fractal dimension clearly is in an uptrend that I expect to get over $3,000. The problem is it did not start with a full load of energy, so how much over and how long it can stay over are likely to be disheartening to the short-term traders.

Click for larger graphic

Miners & Related

Coeur Mining (CDE – $6.10) completed their $1.58 billion acquisition of SilverCrest Metals last Friday and held their December quarter results call this morning. Revenues rose 16.4% from last year to $305.0 million, missing the Street estimate for $314.32 million. They earned 11¢ a share pro forma, also below the 14¢ estimate. Free cash flow of $16 million in their second consecutive quarter of positive free cash flow brought total second half free cash flow to $85 million. The Rochester Mine’s fourth quarter free cash flow of $12 million was its first positive free cash flow quarter since the fourth quarter of 2019. Wharf generated its highest free cash flow in its 42-year history. Palmarejo delivered its highest free cash flow in seven years. Kensington increased its gold production by 13% while decreasing its unit costs by 8% year-over-year, and is targeting a return to positive free cash flow in 2025.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), management guided for March quarter production of 95,000 to 105,000 ounces of gold and 5.4 million to 6.5 million ounces of silver. For the full year they expect 380,000 to 440,000 ounces of gold, up 20% from 2024, and 16.7 million to 20.3 million ounces of silver, 62% above last year.

Coeur repaid an additional $30 million of their revolving credit facility during the quarter, reducing the outstanding balance by 29%, or $80 million, since mid-year to $195 million. In 2025:

Click for larger graphic

Click for larger graphic

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $5.76) also held their December quarter call this morning. Revenue was up 25.9% from last year to $172.3 million, beating the $160.55 consensus estimate. Pro forma earnings of 3¢ a share were in line with estimates. On the conference call (AUDIO HERE and TRANSCRIPT HERE), CEO Keith Neumeyer said they had a record $68.4 million in free cash flow in the quarter, more than double the September period. Total 2024 production hit 21.7 million silver equivalent (AgEq) ounces and they guided for robust production of 29 million AgEq ounces in 2025.

Consolidated cash cost of $13.82 per AgEq ounce for the quarter were 9% less than the $15.17 per AgEq ounce in the September quarter. Consolidated All-in Sustaining Cost (AISC) was $20.34 per AgEq ounce, a 3% decrease from $21.03 per AgEq ounce in the September period.

They finished the year with $202.2 million in cash and $106.1 million of restricted cash. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $6.19) reported December quarter revenues up 6.5% from last year to $47.4 million, above the $45.7 million estimate. Quarterly gold sales of 17,721 ounces were below last year’s 23,250 ounces.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Nolan Watson said that after taking on debt in 2022 to make significant investments in their long-term production base, in 2024 they focused on deleveraging the balance sheet. They made net debt repayments of $80 million in 2024 and an additional $15 million so far this year. As of February 18, $340 million remains outstanding on their revolving credit facility with an undrawn and available balance of $285 million.

In 2024 they returned over $28 million to shareholders with $17.5 million in dividends and $10.9 million in buying back 2.0 million shares. So far this year they’ve bought back another 319,000 shares for approximately $1.9 million. They plan to buy back a lot more than two million shares this year.

Nolan said development activities at their various gold streams are progressing, with Hod Madden in particular still on schedule for first production in 2028. You may remember that SAND took a hit when the Hod Madden operator, SSR Mining, had severe flooding at another mine and Wall Street guessed – wrongly – that SSR might slow the Hod Madden project.

For 2026, Nolan guided for 65,000 to 80,000 ounces of gold compared to 72,810 ounces in 2024. He increased the long-term production forecast to approximately 150,000 attributable gold equivalent ounces in 2030. Using prices of $2,600 an ounce for gold, $30 an ounce for silver, and $4,00 a pound for copper – all way low, in my opinion – Sandstorm will have $260 million in free cash flow. At $3,200 gold, they will have $300 million in free cash flow.

Click for larger graphic

Click for larger graphic

In 2025, they expect 59% of revenues to come from gold sales, 15% from silver, 20% from copper, and 8% other. In 2030 that will be gold 85%, silver 5%, copper 6%, and other 4%. So precious metals will go from 72% of sales to 90% of sales, which should earn them a higher price/earnings multiple. Right now, they are dramatically undervalued:

Click for larger graphic

Click for larger graphic

Nolan did a Bloomberg interview:

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sprott Inc. (SII – $43.38) launched the Sprott Active Gold & Silver Miners ETF (GBUG), the only actively managed ETF that invests in gold- and silver-focused companies that are engaged in exploring, developing, and mining; or royalty and streaming companies engaged in the financing of gold and silver assets.

John Hathaway CFA, Senior Portfolio Manager, said: “Gold and silver mining stocks have historically been correlated to bullion, but in recent years, they’ve lagged the price of the physical metals. Gold and silver mining stocks could offer significant catch-up potential.”

Yep. Buy SII under $40 for a $70 target price. And I might recommend GBUG, too.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly.

Bitcoin (BTC-USD on Yahoo – $98,358.97) has been consolidating over $95,000, getting ready for the next leg up. I think we’ll see $150,000 this year.

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $56.04) is up to $57 billion in assets. It was the world’s fastest ETF to get to $10 billion, $25 billion, and $50 billion. It’s already larger than the iShares Gold Trust and is closing in on the $80 billion SPDR Gold Shares (GLD) as the world’s largest commodity ETF. It remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Ethereum Trust (ETHA- $20.85) remains the cheapest and easiest way to buy ethereum. ETHA is a Buy.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $72.53

Oil closed near its high for the week as “total products supplied” – which is implied demand – over the last four weeks averaged 20.4 million barrels a day (Mbpd), up 3.7% from the same period last year. Motor gasoline product supplied averaged 8.4Mbpd, up 0.4% from the same period last year. Distillate fuel product supplied averaged 4.3Mbpd, up14.2% from last year. Jet fuel product supplied was up 4.3%. Demand across the board continues to steadily grow even as US shale production declines.

For 2025, I expect global oil inventories to decline by 0.5Mbpd, in stark contrast to the “oversupplied” narrative the International Energy Agency (IEA) and the consensus of paper oil traders have been pushing. At the end of 2024, the IEA wrote: “…our current market balances still indicate a 950 kb/d [thousand barrels a day] supply overhang in 2025. If OPEC+ does begin unwinding the voluntary cuts from the end of March 2025, this overhang would rise to 1.4 mb/d. A key uncertainty for the trajectory of OPEC+ crude supply remains the level of compliance with agreed targets, with our estimates showing collective output 680 kb/d above targets in November.”

IEA expected +950k b/d of surplus in 2025. This is one of the larger surpluses since the oil crash started in 2014. Aside from the Covid-19 demand destruction, IEA hasn’t forecast a surplus this large since the end of 2014. They’ve already backpedaled some, but not enough. In their latest February oil market report, they are still expecting about 0.5Mbpd of surplus. It’s going to be a deficit of 0.5Mbpd, and the only question is when they admit it and how high crude prices go.

Another cold event in March will wipe away most of the storage. March quarter inventory balances will show a decline of 0.5Mbpd versus the consensus traders estimate of an increase of 1.3Mbpd. So my answer to the question above is “real soon now” and “over $80.”

The July 2026 Crude Oil Futures (CLN26.NYM – $no trades) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $39.00) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $9.25) is a Buy under $11 for a target price of $24 or more.

Primary Risk: Oil prices fall.

EQT (EQT – $52.56) reported December quarter revenues down 20.1% from last year to $1.63 billion, a touch under the $1.81 billion estimate. But pro forma earnings of 69¢ a share clobbered the 53¢ estimate. Sales volume of 605 billion cubic feet equivalent (Bcfe) was at the high-end of their guidance, while capital spending of $583 million was 7% below the low-end of guidance. They had $588 million of free cash flow despite the Henry Hub price averaging only $2.81 per million British thermal units (MMBtu) during the quarter. For the full year it averaged $3.01 per MMBtu.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Toby Rice said: “This momentum is carrying forward into 2025, with continued efficiency gains and quicker-than-expected benefits from midstream compression investments driving production upside relative to our original outlook, while reserve development capital spending is expected to decline by approximately $200 million year-over-year. Our fourth quarter results and 2025 outlook showcase the power of the integrated, low-cost platform that we have strategically sculpted over the past several years.”

Toby guided for March quarter sales of 525 Bcfe to 575 Bcfe with 12 to 15 new wells. Full year 2025 sales will be 2,175 Bcfe to 2,275 Bcfe with 95 to 120 new wells. He expects $2.6 billion in free cash flow this year. Their free cash flow breakeven including hedging is all the way down at 90¢ per MMBtu. They are not hedged for 2026 production, when they expect substantially higher prices.

EQT is the best way to invest in natural gas.

Click for larger graphic

Click for larger graphic

It is a legitimate way to invest in the AI revolution until nuclear gets here after 2030.

Click for larger graphic

Click for larger graphic

And the Liquefied Natural Gas (LNG) export boom.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

Immediately ahead, natural gas prices are popping based on the latest weather outlook for another polar vortex in March. The Europeans are panicked and talking about putting price controls on LNG. Asia would love to buy all their gas at a premium to Europe’s price cap.

Click for larger graphic

Click for larger graphic

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

Anastasia Huppmann

* * * * *

Your using AI right now Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 2/20/25. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $51.87 – Buy under $33, target price $60

Gilead Sciences (GILD – $110.03) – Buy under $90, first target price $120

Micron Technology (MU – $103.18) – Buy under $102, first target price $140

Nvidia (NVDA – $140.11) – Buy under $125, first target price $180

Onsemi (ON – $55.74) – Buy under $60, first target price $100

Palantir (PLTR – $106.27) – Buy under $100, target price $150

PayPal (PYPL – $77.63) – Buy under $68, target price $136

Snap (SNAP – $10.68) – Buy under $11, target price $17+

SoftBank (SFTBY – $31.12) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $11.48) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $70.22) – Buy under $60; 3- to 5-year hold

PagerDuty (PD – $18.30) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $8.13) – Buy under $10, target price $40

Rocket Lab (RKLB – $26.26) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.14) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.91) – Buy under $2, target $20

Compass Pathways (CMPS – $4.54) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $2.06) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $2.22) – Buy under $14, hold a long time

Medicenna (MDNAF – $0.86) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.11) – Buy under $3, target price $20, then $50

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($33.46) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $34.29) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $40.37) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $27.13) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $37.09) – Buy under $30, target price $50

Coeur Mining (CDE – $6.10) – Buy under $5, target price $20

Dakota Gold (DC – $3.43) – Buy under $2.50, target price $6

First Majestic Mining (AG – $5.76) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.37) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $6.19) – Buy under $10, target price $25

Sprott Inc. (SII – $43.38) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $98,358.97) – Buy

iShares Bitcoin Trust (IBIT – $56.04) – Buy

Ethereum (ETH-USD – $2,735.40)– Buy

iShares Ethereum Trust (ETHA- $20.85) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – no trades) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $39.00) – Buy under $40; $100+ target

Vermilion Energy (VET – $9.25) – Buy under $11; $24 target

Energy Fuels (UUUU – $4.87) – Buy under $8; $30 target

EQT (EQT – $52.56) – Buy under $35; $70 first target

Freeport McMoRan (FCX – $38.96) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $245.83) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $694.84) – Expect to move back to Buy

Fastly (FSLY – $7.81) – Hold for March quarter results

TG Therapeutics (TGTX – $30.94) – Hold for buyout at $40+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2025

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

“New World Investor – 2.29.25″I always wanted stock prices from the future.

My call? There is no leap in 2025 but I augmented my position with a little PLTU when PLTR was below 100.

Thanks Chris for your input on 2/13 RR. Good to know. It’s been awhile since I have been to Florida and into Publix.

$6.17 for 12 Jumbo eggs today. 🙁 But jumbo frozen peeled deveined headless shrimp were just $17.99 for 3 lbs 🙂

Yes, and add 46 percent to that and you get $8.94 in 2025. Not to mention eggs are in everything. Bread. , pasta, snacks , etc. Try a menu of no bread and pasta and snacks. 108 million egg laying hens have been lost to bird flu just over the last four months. The latest news is now Turkey or Egypt? are going to step up and send eggs to the US. I can’t imagine what those shipping costs are going to be since they have to ship via refrigerated vessels. And the supply of those is limited. Not to mention that our friends in the Middle East don’t include Turkey and Egypt much anymore! I would hesitate to eat eggs from there!! Just saying!

Don’t eat bread, pasta, snacks. All junk food. Wheat gluten causes weight gain, worsening of diabetes and inflammatory diseases. I got cage free eggs for $4 a dozen at Trader Joe in NJ.

MM – curious why you dont have a gold or previous metal miner in the TOP 5 if a run is coming. Is SGDF the too recommendation? What about silver? Pls provide yiur too precious metal reco and target price and timeline for share price move

Akba sure isn’t trading like it has something worthy of becoming a blockbuster

I’m interested in how the launch is going as well…any update Mike?

For all the hype on AKBA, why only down days for the last week. what

are we not aware of? Did we get sold a bunch of hype here or when might we see more favorable results?

You would think if akba product were a hit the company would release some pr to help the stock price as it continues to be controlled by the shorts,we are at there mercy until they release earnings,and they better say something positive or this piece of shit will fall to a dollar

Hi Mike,

Do you have any indications on what ENVX is selling its initial batteries for i.e. EX-1 and EX-1M ? Just interested in the revenue / profit mix. Obviously they’re still losing (less) money but at what point does it look like they become profitable. Any ideas?

AKBA

For a stock that has the potential to be a blockbuster and the support of a TADPA why is the share price languishing. Why is this not north of $3 already on heavy volume. Hint:telling us that you bought shares under your price limit is not an answer.Nor does it inspire confidence. How about some factual information…..PLEASE. My God man, not another NVTA, SCYX (yes) We always seem to be left on our own to abandon these dogs, followed a few weeks later by a sell. SO SAD.

I am leading the discussion of AKBA on stocktwits regarding prior authorization for Vafseo. I am viber7 there. Nobody seems to know if TDAPA payment waits for insurance company approval using prior authorization procedures. If PA is denied, TDAPA is dead? Or does TDAPA pay the add-on anyway, even if PA is denied? Since the add-on is many times higher than the insurance payment, I wouldn’t care if PA is denied but we get the add-on. Probably wishful thinking on my part.

MM? MM? MM? Others?

Thanks for this JGMD. I will check this out and hopefully I can add.

Have contacted investor relations and as yet not recd a reply.

assuming pa refers to prior approval? going back over MM’s reports does almost 100% approval have this portion covered?

Thanks for your efforts. PA means prior authorization from the insurance company. Most expensive new branded drugs need PA before the insurance pays. PA is fraught with politics. It is a major factor in failure of sales of new drugs. AKBA Investor relations is nearly useless. On Stocktwits, poster Obviate showed a Texas PA procedure that is simple and should pose no problem. It doesn’t ask whether ESA drugs have been tried and failed. AKBA management should be posting a compendium list of PA organizations to give us confidence that PA won’t be a significant problem and to answer my question whether AKBA will at least get the TDAPA add-on payment even if PA is denied for the V in the ESRD bundle.

Still the numbers are astounding (if they are to be believed). 555000 PEOPLE ON DIALYSIS with chronic kidney disease in the US and the cost of vafseo on an annual basis is about $15500 which translates to roughly $8.6 billion. Shares outstanding fully diluted is 218.2 mil rev per share potentially is approx $40 and if we cut that in half ….$2O a modest multple of 3 translates to$5-6 intially and a much larger market with success of trial(s) that expand usage. A huge, “what the hell is going on” ?.

Michael, please chime in tonight .

AT the height of my concerns I see that the volume has picked up and share price as well. Lets see if it clears $2 by Monday. Still have not heard back from IR.

I would think that TDAPA would encourage prior approval. At $15500 annually this would be the cheapest of “expensive” drugs. Also with a large and growing population requiring dialysis for CKD is this not a cheaper and more convenient option?

Someone posted this on Stocktwits regarding SCYX: Does this mean we’re getting closer to the hold being lifted? Is it possible they would change the name as well??

NVDY is going for $17.99 now. This week it will pay $1.61 as its monthly dividend.

New World Investor for 2.27.25 is posted. New space recommendation: Redwire (RDW)