Dear New World Investor:

Last Friday’s Personal Consumption Expenditures Index report for January showed the headline number increasing 2.5% year-over-year, a tenth slower than December’s 2.6%. The month-over-month increase was 0.3%, the same as December and right on the consensus.

Stripping out the volatile food and energy components, the Fed’s favorite inflation indicator, the core PCE, gained 0.3% last month after an unrevised 0.2% rise in December. Year-over-year, core inflation increased only 2.6% after climbing 2.9% in December.

Click for larger graphic h/t Yahoo Finance

The 2.6% annual core inflation rate is still too hot for the Fed’s liking, but Treasury yields fell a bit because the bond vigilantes see a clear slowdown in the most recent core rates – the annualized three-month percentage change.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

I expect the first Fed funds rate cut as early as June 18. But even if they don’t cut this whole year, history tells us interest rates are low enough that the economy can do OK.

Click for larger graphic

Click for larger graphic

Market Outlook

The S&P 500 lost 2.1% since last Thursday as the correction rolled on. As we’ve all learned, buy corrections, don’t sell them. The Index now is down 2.4% year-to-date. The Nasdaq Composite lost 2.6% as investors sleepwalk into the AI era. It is down 6.4% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) was flat for the week and is down 3.3% year-to-date. The small-cap Russell 2000 dropped 3.4% and is down 7.3% in 2025.

Last week’s AAII sentiment indicator showed a new level of bearishness. This week wasn’t quite as bad, but still qualifies as overwhelmingly bearish.

Click for larger graphic

Click for larger graphic

Should you worry? Maybe – if you’re not buying. Studies show that buying when AAII bullish sentiment is extremely low and selling when it is extremely high gives superior returns. It’s a near perfect contrarian indicator. The herd is rarely right at market extremes

The fractal dimension still shows this downtrend as a consolidation of the last big uptrend. Another week or two of downward action would send it back down to or even through the 55 level, which would indicate a new trend down has started. I don’t think that’s how this will play out but it could happen.

Click for larger graphic

Top 5

Changes this week: None

Near-Term – chronological order

AKBA Akebia Therapeutics – Vafseo launch

SCYX – ScyNexis – Announce resolution of the manufacturing problem, lifting of clinical hold, restart of MARIO trial, maybe GSK files for hospital use approval

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Economy

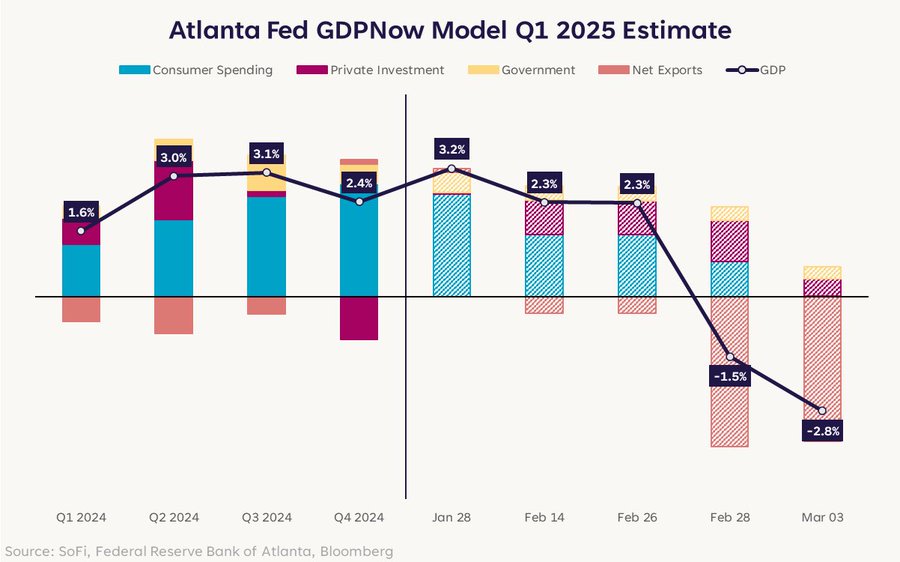

As you’ve probably heard, the Atlanta Fed’s GDPNow model forecast of March quarter real GDP fell to -1.5% on February 28. The big drag came from a surge in imports, which acts as a negative force on GDP, and may just be front-running tariffs. It fell further to -2.6% on March 3 due to a sharp drop to no growth in consumer spending or equipment investment, and a contraction in housing investment.

This morning’s update improved a bit to -2.4% thanks to wholesale inventories.

Click for larger graphic

Click for larger graphic

The decline in GDPNow is mostly from net exports as companies accelerate imports to try to beat any tariffs. There’s also weakness in housing-related consumption and housing-related investment that lingers from the December quarter.

Click for larger graphic h/t @LizThomasStrat

Click for larger graphic h/t @LizThomasStrat

This could be a growth scare, but more likely it’s signaling a slowdown.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, March 7

February payrolls – 8:30am – +160,000 expected; January was +143,000

Sunday, March 9

Daylight Savings Time – 2:00am your local time, set clocks ahead one hour

Monday, March 10

EDIT – Editas Medicines – 9:20am – Leerink Partners Global Healthcare Conference

RDW – Redwire – After the close – Earnings release; call tomorrow

Tuesday, March 11

RDW – Redwire – 9:00am – Earnings conference call

EDIT – Editas Medicines – 9:00am – Barclays Global Healthcare Conference

PYPL – PayPal – 10:30am – Wolfe Fintech Forum

GILD – Gilead Sciences – 10:40am – Leerink Partners Global Healthcare Conference

Short Interest – After the close

Wednesday, March 12

Consumer Price Index – 8:30am

Thursday, March 13

AKBA – Akebia – 8:00am – Earnings conference call

PD – PagerDuty – 5:00pm – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $235.33) introduced M3 Ultra, its highest-performing processor ever. It links two M3 Max systems-on-a-chip via 10,000 high-speed connections that allows the system to treat the combined dies as a single, unified processor with184 billion transistors. It powers a new top-of-the-line Mac Studio starting at $2,000 for the 96-gigabyte version. They also introduced a new iPad Air with a single M3 and a Macbook Air with an M4 for $1,000.

On the services side, Friday Night Baseball returns to Apple TV+ on March 28. AAPL is a HOLD – I expect to move it back to Buy under $175 for new iPhones.

Gilead Sciences (GILD – $116.04) presented at the TD Cowen Health Care Conference (AUDIO HERE and TRANSCRIPT HERE). Johanna Mercier, Gilead’s Chief Commercial Officer, said they grew about 8% in 2024 and would do about 5% to 6% in 2025 but for two headwinds. The first is the Medicare Part D drug price negotiations that will cost them about $1.1 billion in revenue, mostly (about $900 million) in HIV drugs. The second is adverse foreign exchange if the dollar stays strong. They will be back to 5%-6% growth in 2026.

Lenacapavir for HIV prevention has a June 19 PDUFA date and the launch will drive revenue growth in 2026. They expect 75% insurance coverage at six months and 90% at 12 months. They will price around $25,000 a year, in line with other pre-exposure drugs, and get market share on features. It offers 100% prevention with an every-six-months injection – a compelling marketing story. 95% of the market is on daily oral drugs today with only 50% to 55% compliance. 5% of the market is on an every-two-months injectable. Gilead thinks they can convert both groups to Lenacapavir. GILD is a Long-Term Buy under $90 for a first target of $120.

Meta Platforms (META – $624.93) Chief Product Officer Chris Cox presented at the Morgan Stanley Technology, Media & Telecom Conference (AUDIO HERE and TRANSCRIPT HERE). Chris was the #13 employee at Meta. He said he spends most of his time on AI, from basic research to their Llama foundational model, to building out the infrastructure. Most of their $65 billion in capital spending this year will be AI-related. It includes a new data center the size of Manhattan.

Chris said the new Ray Ban glasses are the best AI devices on the market. You can ask them anything about what you are looking at and get useful answers.

The company will debut a standalone Meta AI app, joining Facebook, Instagram, and WhatsApp, in the June quarter to compete with OpenAI’s ChatGPT and the rest of the mob, according to CNBC. The usual “people familiar with the matter” said Zuckerberg plans to make Meta the leader in AI by the end of the year, ahead of competitors such as OpenAI and Alphabet. They said Meta also plans to test a paid subscription service for Meta AI, similar to OpenAI’s monthly fees for access to more powerful versions of ChatGPT.

In the December quarter earnings conference call, Zuck said: “This is going to be the year when a highly intelligent and personalized AI assistant reaches more than 1 billion people, and I expect Meta AI to be that leading AI assistant,” and CFO Susan Li said that while the company’s Meta AI efforts are focused on “building a great consumer experience,” there are “pretty clear monetization opportunities here over time, including paid recommendations and including a premium offering.”

I’m recommending Meta for two major reasons. First, there are very few companies that started in a dorm room and grew to $200 billion in revenues with the founder running it the whole way. Second, they went earlier and bigger into AI than anyone, and those investments will generate huge returns over the next decade. META is a Buy under $655 for a long-term hold.

Micron (MU – $89.27) appointed two new heavyweight directors. Mark Liu had a 30+-year career with Taiwan Semiconductor, ending as Executive Chairman. Christie Simons is a senior audit and assurance partner of Deloitte & Touche and recently led Deloitte’s Global Semiconductor Center of Excellence to serve global semiconductor clients across consulting, advisory, tax, and assurance. MU is a Buy under $102 for a $140 first target.

Nvidia (NVDA – $110.57) Vice President: Healthcare Kimberly Powell presented at the TD Cowen Health Care Conference (AUDIO HERE and TRANSCRIPT HERE). She said Nvidia has been focused on accelerated computing for 20 years and some of the earliest users were in healthcare for image analysis and genomics. Now, of course, AI is dramatically increasing the areas it is used from drug discovery through clinical trials.

She made the point I’ve been harping on: Nvidia no longer is just a semiconductor company. They build full-stack data center solutions with GPUs accompanied with CPUs, networking, applications software, and pre-written applications for numerous industries. She didn’t say it, but that’s why the “competitors” can’t really compete.

She said healthcare globally is a $10 trillion industry and about 30% of that is operating expenses for labor, labs, and the physical infrastructure to deliver healthcare. There are many areas to deliver more and better healthcare using AI and GPUs, often in the form of agents or robots. Large Language Model technology can be applied directly to drug discovery, as both are built on understanding the sequence of events. Work that used to take three to five years can take a few months if a biotech company consistently puts their lab results in a proprietary database that informs the next round of lab work. That’s what Nvidia’s BioNeMo platform does.

Nvidia also presented at the Morgan Stanley Technology, Media and Telecom Conference (AUDIO HERE and TRANSCRIPT HERE). CFO Colette Kress said they just reported 18% sequential growth in data center revenue with the majority of revenue from the last generation Hopper chips, not the new Blackwell processors. She said many existing customers want to expand their capacity by adding to Hopper-based systems. Some new customers are not willing to wait for a Blackwell allocation and can build powerful systems with Hopper right now to get started, planning to build a Blackwell system later.

On the recent conference call, she said the post-training market was 10 times as large as the pre-training market we all thought was where Nvidia processors were needed. Pre-training is requiring more and more compute power to cope with other-than-text inputs like video and graphics. But it’s turning out that post-training to fine-tune the model for the reasoning part of the process. As Deepseek showed us, reasoning can be a key driver of a model’s quality for inferencing.

The stock closed today at its lowest level since September, but they are nowhere near the peak in demand for GPUs for AI. One driver investors are missing is the worldwide demand for sovereign AI models – every country will have one trained on its own data. It just takes a while for nation-state priorities to turn into enterprise budgets. NVDA is a Buy under $125 for a $180 first target.

Onsemi (ON – $43.88) presented at the Morgan Stanley Technology, Media and Telecom Conference (AUDIO HERE and TRANSCRIPT HERE). They said their working inventory is at 116 days, in their sweet spot. As soon as their major industries turn up, the growth will hit revenues right away, but they are not counting on that until 2026. No matter what, they will have a lot of free cash flow this year. They have a lot of new products that carry 60% to 70% gross margins and a substantial technology lead over their Chinese and European competitors.

After several private attempts at a merger, on Wednesday ON publicly bid $6.9 billion to acquire Allegro Microsystems (ALGM). Allegro is a leader in magnetic sensing and power integrated circuits for the automotive and industrial end-markets. Allegro’s Board called the offer “inadequate,” so we’ll have to see where the negotiations go. ON is a Buy under $60 for a $100 first target.

Palantir (PLTR – $80.46) announced a major contract with Societe Generale, a top tier European bank, for its international retail banking activities. The solution deployed relates to cutting-edge technologies ensuring the highest standards of security and data integrity. It uses Palantir’s state-of-the-art Anti Financial Crime solutions, built on Palantir Foundry, tailored specifically to address the challenges faced by international financial institutions to detect, prevent, and mitigate financial crime risks such as money laundering or fraud.

Palantir also announced a joint venture with TWG Global to redefine AI deployment in banking, investment management, insurance, and other financial services. By pairing Palantir’s AI infrastructure with TWG’s expertise in business operations and financial services, over the past year, TWG and Palantir have worked together to embed AI into TWG’s own companies, refining their approach and proving its impact. This is the next step in that effort — an operational AI offering designed to revolutionize financial services and insurance to integrate AI at scale and accelerate industry-wide adoption.

Palantir held their second developer’s conference with a keynote from Palantir Chief Architect Akshay Krishnaswamy:

PLTR is a Buy under $100 for a $150 target.

PayPal Holdings (PYPL – $68.08) presented at the Morgan Stanley Technology, Media and Telecom Conference (AUDIO HERE and TRANSCRIPT HERE). This was a don’t-miss presentation. CEO Alex Criss said the most important effort at the company is branded checkout. They’ve stabilized the technology and are rolling it out. The second most important effort is omnichannel – taking PayPal and Venmo everywhere. The third is leveraging consumer data with merchant data to redefine the checkout experience to include cross-sells.

Alex said PayPal has improved its checkout experience to be as good or better than the major competition, but that’s not good enough to take market share at the rate he wants to. So they are focused on creating a personalized experience with a choice of payment methods, including BNPL and crypto. The big change is letting the merchant recognize the customer when they come in and reconfiguring the website for them. That extends to creating personalized Buy Now buttons, like “Including Free Shipping” for Amazon Prime customers or “5% New Customer Discount.” PYPL is a Buy under $68 for a double in three years.

Small Tech

Fastly (FSLY – $6.50) presented at the Morgan Stanley Technology, Media and Telecom Conference (AUDIO HERE and TRANSCRIPT HERE). Management said their new go-to-market initiatives under the new Chief Revenue Officer are working, with the new enterprise customers in the December quarter, a strengthening pipeline, and increased bookings that let them guide 2025 revenues above the consensus estimates.

They also made a lot of progress on the product side and platform unification. They started 2024 with one security product and they are starting 2025 with three products. They introduced three new products in the December quarter, and platform unification makes it easier to cross-sell products.

They were surprised in 2024 when some of the top 10 customers who had a long history of consolidating vendors – to Fastly’s benefit – reversed to add new vendors offering lower prices (in some cases, for a bit slower or otherwise inferior services…looking at you, Amazon Prime). The top 10 accounted for 40% of 2023 revenue but only 32% of 2024. Fastly wanted to reduce their reliance on the top 10 by growing the below-top-10s faster, not by actually losing top 10 revenue dollars. They think with the Edgio bankruptcy the decline is over, pricing stability has returned, and Fastly will see a little increase in the second half of the year back to 35% or so.

Their growth drivers for the next 12 months also include the increase in enterprise customers, as they tend to add revenue over time, picking up Edgio customers, and easier comparisons that will let them exit 2025 at a 10% growth rate. Fastly is targeting profitability in 2026 and $800 million to $900 million in revenue in 2028 with a gross profit margin of 55% and an operating margin of 7%. FSLY is a Hold for March quarter results.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $17.27) reports January quarter results next Thursday. Wall Street is looking for revenues up 7.6% to $119.53 million with earnings of 16¢ a share. Guidance should be for $121.28 million and 19¢. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Redwire (RDW – $12.36) reports December quarter earnings next Monday with a conference call Tuesday morning. Analysts expect $74.55 million in revenues (five analysts) and a loss of 8¢ a share (one analyst). March quarter revenue guidance should be for $81.52 million, but there is no earnings estimate. One of the reasons I recommended RDW is that it is underfollowed.

The company has had an important role in recent space missions launched by Eli Lilly, ISS, NASA, the European Space Agency, and a couple of hundred more. It has contracts with big customers like Boeing, Lockheed Martin, and Jeff Bezos’s Blue Origin, including a deal to supply parts for Blue Origin’s space mobility platform. They just won a contract with the European Space Agency to design a spacecraft platform that could be delivered to Mars as a part of the LightShip initiative. LightShip is an electric propulsive tug that can carry passenger spacecraft to Mars and also offers navigation and communication services. Redwire’s solution is built around an adapted version of Hammerhead, its highly versatile small satellite platform, and its proven avionics capabilities that launched most recently on ESA’s Hera mission.

Redwire just called their warrants that are deep in the money. They will be exercised, bringing in $70 million by March 24. Including that, after the Edge Autonomy deal closes there ought to be something like 125 million shares of RDW outstanding. At today’s close, that’s a $1.545 billion market capitalization, 3.4x the 2025 revenue forecast of $459 million (three analysts). That’s cheap. RDW is a Buy under $18 for a $36 first target as space exploration grows.

Primary Risk: A new competitor emerges.

Rocket Lab USA (RKLB – $18.66) CFO Adam Spice did another excellent presentation at the KeyBanc Emerging Technology Summit (AUDIO HERE and TRANSCRIPT HERE). Adam said only 30% of revenues come from launch now, with 70% from Space Systems. They continue to expand that business targeting all the rocket components and then expanding into building a variety of payloads. He said the Electron launch business started as a negative gross margin business, then progressed to low 30% margins on the 16 launches in 2024. They’ll do over 20 launches in 2025 and as the cadence increases the gross profitability increases as they spread the fixed costs over more launches. They think they can get to mid-40% gross margins on 24 annual launches.

When they came public in 2021, the Neutron project had a $350 million budget and a development timeline of three to four years. They were hoping for a late-2024 first launch and it now will go in the second half of 2025.

The new alternative to land Neutron on a $50 million barge in addition to returning to the launch site is based on the available payload. A barge landing mission can carry 13 tons of capacity. A return to launch site mission can only carry 8 tons because it consumes so much fuel, but they save the cost of towing the barge several hundred miles downrange. The first test launch will be a soft splash-down into the ocean, after which they will recover the rocket. That’s because they don’t want to damage a $50 million barge if anything goes wrong.

Longer-term, launch is about a $10 billion total available market (TAM), making satellites and their components is about a $30 billion TAM, and the applications – communications, earth sensing, defense, and so on – are about a $300 billion TAM today and growing. That’s why Rocket Lab will evolve towards building its own constellation of satellites over the next three to five years. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL – $2.38) presented at the TD Cowen Health Care Conference (AUDIO HERE). They said 2025 is going to be a big year with two molecules going into the clinic. ABCL575 is targeted at atopic dermatitis and will be dosing the first patients in the September quarter. They will reveal the target for ABCL635 in their March earnings call in early May. They’ll also advance their next candidate into IND-enabling studies and complete the GMP plant to manufacture their own drugs and for others. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $1.92) reports December fourth quarter results next Thursday morning, Analysts expect revenues to be down 33.52% to $37.36 million as Auryxia goes generic with an 8¢ loss per share. What will move the stock is, of course, comments or guidance on the Vafseo launch this quarter. Analysts are looking for $37.41 million and a 5¢ loss. I don’t expect management to give full year revenue guidance, but in case they do the consensus is at $180.2 million, up 19.% from 2024.

The stock has been acting better than most biotechs. The market makers may have gotten the message to cover shorts before the earnings release – that happens. Buy AKBA up to $2 for the Vafseo launches in the EU, UK, and US.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: 2026

Probable time of next financing: Never

Compass Pathways (CMPS – $4.02) presented at the TD Cowen Health Care Conference (AUDIO & SLIDES HERE). Management said there are 21 million adults in the US with Major Depressive Disorder. Of those, 10 million are treated with drugs. 30% of those, or 3 million, fail at least two drug treatments and are classified as having Treatment-Resistant Depression.

Click for larger graphic

In the first COMP360 Phase 3 trial (005), we will get top-line data and a safety assessment from the Data Safety & Monitoring Board about suicidal ideation. After approval and launch in 2027, Compass already is working with a few hundred sites. Spravato, which is the closest comparable drug although not a substitute for COMP360, is currently in more than 5,000 sites being delivered by more than 4,000 prescribers. The majority of that is clustered in 600 to 800 sites. Compass is already working to change state laws where necessary.

Click for larger graphic

Click for larger graphic

CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2027

Probable time of next financing: Late 2025

Editas Medicine (EDIT – $1.78) presented at the TD Cowen Health Care Conference (AUDIO HERE and TRANSCRIPT HERE) and reported December quarter results two days later with no conference call. Revenues of $30.6 million missed the $37.17 million estimate and they lost $45.4 million, including $12.2 million of restructuring charges related to the discontinuation of the reni-cel program, or 55¢ per share in the quarter, also missing the 35¢ loss estimate.

CEO Gilmore O’Neill said: “Our objective and strategy to become a leader in in vivo gene editing accelerated in the fourth quarter after we achieved in vivo preclinical proof of concept ahead of schedule and shared positive preclinical in vivo data demonstrating the potential of our platform technology to achieve gene upregulation, or amplifying the expression of an existing protein to achieve clinically relevant levels that could potentially drive cures across tissues with a single dose.”

At the TD Cowen Conference fireside chat, management said one key difference they have is that they can functionally up-regulate genes, not just knock them out. Another is that their in vivo delivery system is superior to others, so they now are completely an in vivo company. A third is that they own the genetic editing patents expiring in 2033 that other CRISPR companies must license. There are about 100 programs in development that will require a license.

Editas is on track to declare two in vivo editing development candidates via gene upregulation, one in hematopoietic stem cells (HSCs) and one in liver, in mid-2025. They will present further in vivo HSC preclinical data and further in vivo preclinical data in one liver indication by yearend. They will establish one additional target cell type/tissue by yearend.

Editas finished December with $269.9 million in cash, enough to carry them into the June 2027 quarter, and will be in the clinic by mid-2026. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2026

Probable time of next financing: 2026 or never

TG Therapeutics (TGTX – $35.19) reported December fourth quarter Briumvi revenues up 141.6% from last year to $108.19 billion, solidly beating the $100.67 million consensus estimate. That brought them in at $310.0 million for the year, well above expectations early in 2024. GAAP earnings of 15¢ a share clobbered the 9¢ estimate.

On the conference call (AUDIO HERE and TRANSCRIPT HERE), CEO Michael Weiss guided 2025 sales to $540 million, a bit above the $534.45 consensus expectation. But Mike is wise to the game – guide a bit above the consensus, raise guidance every quarter or two, and then soundly beat expectations. TGTX jumped 14.4% after the report.

In 2025, TG will begin a pivotal trial of subcutaneous Briumvi and another pivotal trial of the 30-minute infusion that succeeded in the ENHANCE trial. Mike expects operating expenses of $300 million, which means earnings of $1.75 to $2.00 per share. I still think it’s likely they get bought out this year.

They finished the quarter with $311.0 million in cash, which they said is enough to “fund our business based on our current operating plan.” Translation: No more equity sales, thank you. Hold TGTX for a target price in a buyout of $40 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,919.80) has been buoyed by central bank buying. JPMorgan wrote: “While higher real yields have weighed on demand from other sources, central banks have increased their purchases by 11.5% annually since 2019 … With their share nearing a quarter of total demand, they have now become a dominant force in the market.”

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

Central banks don’t buy silver, but comparing the recent correction to the April 2024 correction, if silver repeats the May 2024 rally of 25%, it would hit $38.50 by the third week of March.

Unlike the S&P fractals, the gold fractal dimension decisively went back into trend mode, headed for the 30 level and a gold price north of $3,000 an ounce.

Click for larger graphic

Click for larger graphic

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly.

Bitcoin (BTC-USD on Yahoo – $90,534.26) fell nearly 17% in February to briefly trade under $80,000, its worst month since June 2022. It’s rebounding now after President Trump said a US strategic reserve of cryptocurrencies would include bitcoin, ether, XRP, solana, and cardano.

While retail pulls money out of the bitcoin exchange-traded funds, BlackRock added a 1% to 2% allocation to the $48 billion iShares Bitcoin Trust ETF (IBIT) in its target allocation portfolios that allow for alternatives.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $50.64) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Ethereum Trust (ETHA- $16.65) remains the cheapest and easiest way to buy ethereum. ETHA is a Buy for the coming explosion in token-funded start-ups.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $66.28

Oil had its lowest close in six months today as the market grappled with an uncertain demand outlook following President Trump’s sweeping tariffs on major US trading partners. US Gulf Coast refineries are placing fewer orders for crude from Mexico, and the Canadian province of Alberta is threatening to build pipelines to the coast to increase oil shipments to Asia and Europe.

President Trump’s call with Saudi Crown Prince Mohammed bin Salman was his first foreign leader call after being sworn in. Not surprisingly, OPEC+ decided to proceed with their long-delayed hike in oil production. They cited “healthy market fundamentals and the positive market outlook,” which could mean they expect oil prices to rise in the near future. The production increases will begin in April, although the countries noted they could change their minds in response to “evolving conditions.”

But OPEC is not “capitulating” by adding back 135,000 barrels a month. The market can absorb that increment easily, and I’m sure it depends on market conditions. If oil is under $70, fuggedaboutit. And no one will “Drill baby Drill” at these prices. US shale grew at its slowest pace since its inception (ex-COVID) in 2024. The twilight of shale is here, is widely underappreciated, and has massive implications. Even the Energy Information Administration figures show lower 48 oil production in December 2023 of 11.0 million barrels a day and December 2024 production of 11.18 million barrels a day – no growth.

To recap:

1) Global oil inventories, the barometer for market tightness, remain at multi-year seasonal lows

2) US shale company guidance corroborates no meaningful black oil supply growth

3) Demand is forecasted to grow by ~1.3 million barrels a day

4) Global tariff uncertainty – likely to remain, unfortunately

5) Iran/Venezuela/Russia oil sanctions – Iran is estimated to be exporting at/near max levels and Russia is bound by the OPEC+ voluntary agreement.

6) OPEC+ has begun the process of reducing spare capacity, which now is the largest overhang on sentiment

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

The July 2026 Crude Oil Futures (CLN26.NYM – no trades – June closed at $62.67) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $35.64) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $7.47) reported December quarter revenues down 3.6% from last year to C$504.35 million with fund flows from operations of C$263 million or C$1.70 a share.

Click for larger graphic

Click for larger graphic

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), management said in the quarter they returned $36 million to shareholders, including $18 million in stock buybacks and $18 million in dividends.

In Germany, Vermilion successfully tested the Wisselshorst deep gas exploration well, now estimated to contain 68 billion cubic feet of recoverable natural gas. It is Vermilion’s largest discovery in Europe over the past decade.

Click for larger graphic

Click for larger graphic

38% of expected net-of-royalty production is hedged for 2025. In particular, western Canadian gas hedges in 2025 and 2026 have been undertaken at pricing that locks in significant profits. Based on forward commodity prices, the company forecasts 2025 free cash flow of approximately C$400 million. Approximately 60% will be allocated to debt reduction with 40% allocated to shareholder returns, including dividends and more buybacks. VET is a buy under $11 for a target price of $24 or more.

Primary Risk: Oil prices fall.

* * * * *

* * * * *

Your increasingly interested in quantum computing Editor,

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 3/6/25. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $45.51) – Buy under $33, target price $60

Gilead Sciences (GILD – $116.04) – Buy under $90, first target price $120

Meta (META – $624.93) – Buy under $655 for a long-term hold

Micron Technology (MU – $89.27) – Buy under $102, first target price $140

Nvidia (NVDA – $110.57) – Buy under $125, first target price $180

Onsemi (ON – $43.88) – Buy under $60, first target price $100

Palantir (PLTR – $80.46) – Buy under $100, target price $150

PayPal (PYPL – $68.08) – Buy under $68, target price $136

Snap (SNAP – $9.60) – Buy under $11, target price $17+

SoftBank (SFTBY – $26.42) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $8.28) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $65.30) – Buy under $60; 3- to 5-year hold

PagerDuty (PD – $17.27) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $6.17) – Buy under $10, target price $40

Redwire (RDW – $12.36) – Buy under $18, first target price $36

Rocket Lab (RKLB – $18.66) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $2.38) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.92) – Buy under $2, target $20

Compass Pathways (CMPS – $4.02) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $1.78) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $1.96) – Buy under $14, hold a long time

Medicenna (MDNAF – $0.70) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $0.96) – Buy under $3, target price $20, then $50

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($33.15) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $33.73) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $39.00) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $26.81) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $36.14) – Buy under $30, target price $50

Coeur Mining (CDE – $5.50) – Buy under $5, target price $20

Dakota Gold (DC – $3.05) – Buy under $2.50, target price $6

First Majestic Mining (AG – $5.84) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.37) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $6.35) – Buy under $10, target price $25

Sprott Inc. (SII – $43.00) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $90,534.26) – Buy

iShares Bitcoin Trust (IBIT – $50.64) – Buy

Ethereum (ETH-USD – $2,115.98)– Buy

iShares Ethereum Trust (ETHA- $16.65) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – no trades – June closed at $62.67) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $35.64) – Buy under $40; $100+ target

Vermilion Energy (VET – $7.47) – Buy under $11; $24 target

Energy Fuels (UUUU – $4.19) – Buy under $8; $30 target

EQT (EQT – $46.16) – Buy under $35; $70 first target

Freeport McMoRan (FCX – $37.68) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $235.33) – Expect to move back to Buy under $175 for new iPhones

Fastly (FSLY – $6.50) – Hold for March quarter results

TG Therapeutics (TGTX – $35.19) – Hold for buyout at $40+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2025

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Numero uno?

AKBA

MM please answer similar questions posed by myself and jGMD on AKBA from the last RR ,thanks

“When is the TDAPA advanced? So with 555000 people requiring dialysis in the US at the moment and an annual cost of approximately $15,500 and well over a 100,000 new cases per year this translates to blockbuster potential of 8.6 Billion just in the US alone.”

The stated Wholesale Acquisition Cost is $15,500, but Akebia offers volume discounts to get that down to $2,500 a year – the same as Amgen charges – by the time TDAPA expires on December 31. 2026.

About 25% of patients with anemia due to chronic kidney disease fall below target hemoglobin levels. About 150,000 are on high ESA doses that are more dangerous to the patient and more costly to the dialysis provider. Another 80,000 are treated at home where injectable ESAs create extra costs that are avoided with oral Vafseo. So roughly half of all dialysis patients are the immediate target.

Akebia has done a good job of informing doctors of the benefits of Vafseo for these two groups, but it just takes time to get widespread adoption.

If they give March quarter guidance next Thursday morning, I’d like to hear $45 million to $50 million. If they give full-year guidance, which I don’t expect, they’ll probably lowball for $200 million so they can raise every quarter.

I don’t see how Amgen’s ESA general manager can’t buy them this year.

Thanks Michael, does the TDAPA renew for ’27? Still not sure how TDAPA works? Is it a program that provides an add on payment for all drugs or renal drugs and can AKBA apply to have it extended? Is it paid annually per patient? Does it appear that it could easily be or become a blockbuster drug?

What is the actual amount that is paid through TDAPA? Sorry Michael, so many questions.

Also, do all dialysis patients eventually develop anemia?

TDAPA is a 2-year designation, so ’25 and ’26 for Vafseo. It does not renew. It pays for all new diabetes drugs that qualify. The dialysis center pays Akebia when they order the drug and TDAPA reimburses the dialysis center when it is given to the patient.

The amount that the dialysis center pays for each dose depends on how much volume the center has done – it starts at roughly $15,500/year and drops to around $2,500/year at the end of 2026. Dialysis is a $1 billion opportunity and non-dialysis, which should be approved in late 2027, is a multi-billion dollar opportunity.

About 500,000 dialysis patients have anemia. 150,000 of them are on high doses of ESAs, which causes significant side effects including death. 80,000 of them are treated at home but must go to the center for their ESA infusion.

OK, but you did not address my post on this subject.

I am leading the discussion of AKBA on stocktwits regarding prior authorization for Vafseo. I am viber7 there. Nobody seems to know if TDAPA payment waits for insurance company approval using prior authorization procedures. If PA is denied, TDAPA is dead? Or does TDAPA pay the add-on anyway, even if PA is denied? Since the add-on is many times higher than the insurance payment, I wouldn’t care if PA is denied but we get the add-on. Probably wishful thinking on my part.

MM? MM? MM? Others?

MM–in this update, are you saying that prior authorization for patients on govt healthcare doesn’t matter and TDAPA pays anyway?

Michael, thanks for the clarity on some of the issues. Correct me if I’m wrong but it doesn’t seem to be the uptake you expected. The market slump bares that out. Hope to hear this evening where we go from here. As it stands, I am ready to pull the plug on this one and wait until 2027 for them to be granted vafseo for all CKD people, at this time it cannot be ignored.

MM, With all the discussions regarding “possibly” going back to Natural Gas and continuing the Natural Gas Pipeline we heard about earlier this week, is there any good reasons to look for a play in that category this year? Thanks MM!

EQT is by far the best nat gas investment. They are low-cost, highly integrated, and severely undervalued.

MM could you please explain the risks for Apple with its manufacturing dependencies for its products and the tariffs imposed by the Trump administration? Will this be the catalyst to move it under your $175 target to move it back to a Buy? Thanks!

While Apple is moving fast to source phones from other countries, they still are pretty dependent on China, as are some of their key suppliers. That probably was why Tim Cook made the pilgrimage to Mar-a-Lago and announced the plan to invest $500 million in the US. My best guess is they will work with the Trump rules to avoid disruption.

I think the stock comes back under $175 as Wall Street sours on high P/Es for slow growth.

Who is afraid of the big bad tariffs? Investors are falling all over themselves about the shock and awe of Trumps terrible tariffs. Canada is a joke. Who do they think they are fooling. Look at the numbers and don’t listen to the rhetoric from those Canadian politicians who love to blow smoke up everyone’s ass. Canada’s economy is highly dependent on the US buying their stuff. Over 70 percent of the goods they export is sold in the US!! Does anybody really think they are going to shoot themselves in the foot , keep those crazy tariffs in effect for very long and cause their fragile economy to go into a horrid recession because their newly elected PM is letting crap fall out of his mouth! Get real !! Same for Mexico. Mexico sends to the US way more goods than the US ships back. And if those US companies who now have plants operating there decide to bring them back to the US, that women who now rules Mexico will have an even bigger problem on her hands than Trumps tariffs!

That salt flats video of a 16 y.o. taking her first solo drive reminds me of this case of uncharged child endangerment last month where a first-grader died driving a junior drag racer at a track in Orlando.

https://www.msn.com/en-us/public-safety-and-emergencies/general/7-year-old-girl-dies-after-racing-accident-at-orlando-speed-world-pain-of-loss-is-immeasurable/ar-AA1yAfRE

Terrible.

RKLB. Michael, this from payloadspace.com. If this deal comes together, is it a good increase in shareholder value?..Good afternoon. Rocket Lab announced it was acquiring Mynaric, a struggling German-based laser comms provider, for $75M. $300M had been invested in Mynaric before the company began the process of filling for bankruptcy. Rocket Lab with the savvy prime play.

Thx is for the heads up on this. Also news release this week on RKLB, see paragraph below. Does this mean dilution on our stock which will drive down the price ?

Rocket Lab said it may fund the Mynaric deal and future acquisitions with proceeds from equity offerings. On Tuesday, the company also said it has filed a prospectus with the Securities and Exchange Commission to sell shares of its stock to raise up to $500 million to fund future growth, including potentially the Mynaric acquisition.

Michael, please advise on this !!

AKBA

It looks like Vafseo revenues will come in well below consensus in Q1. Am I reading this correctly? If I am, what are you expecting the stock to do in the immediate term Michael. You had also mentioned the possibility of a buyout? It’s looking like a possible Q2 story…..traction.

Does today’s news have any effect on the long term story for AKBA? For me, the answer is clearly “NO”. Therefore AKBA is on sale today. 15% off! It is a better value than yesterday.

New World Investor for 3.13.25 is posted.