Dear New World Investor:

Is the economy hot or not…and does the Fed care? The answer is that it is stronger than the Fed expected, but they don’t directly care. What they care about is inflation and unemployment – those are their two mandates.

Inflation

We got the March Consumer Price Index (CPI) inflation report, which is not the Fed’s preferred measure of inflation. They have repeatedly said that they look at the core Personal Consumption Expenditures Index (PCI) to get to their 2% target. The next PCE announcement comes April 26, before the May 1 Fed meeting. March’s CPI increase was driven by elements not included in the PCE.

First, the numbers. Headline year-over-year (YoY) inflation was 3.5%. That was up from 3.2% in February and a tick above the 3.4% expectation. The core YoY number, excluding food and energy, was 3.8%, the same as February but also a tick above the 3.7% consensus. Essentially, the markets panicked Wednesday over inflation topping the consensus estimates by a tenth of a percent. The deflation of core goods intensified, showing a YoY decrease of 0.7%, while the growth rate for core services accelerated, reaching +5.4%.

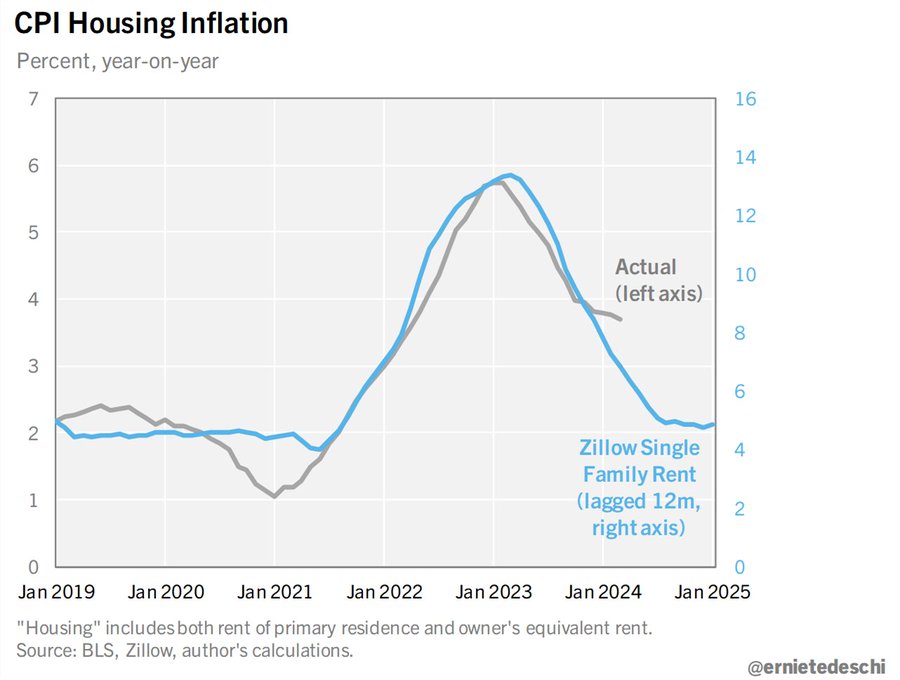

As usual, the lagging Cost of Shelter component contributed most to the slow CPI decline. Cost of Shelter includes the rent paid by tenants for housing and something called Owner Equivalent Rent, calculating the hypothetical amount homeowners would pay to rent their own homes, which obviously is affected by what renters actually pay. The “Rent of Primary Residence” component came in at 5.67% YoY, which was the lowest reading since May 2022, but still reflecting early 2023 rents rather than today’s generally lower reality.

@ernietedeschi, former Chief Economist at the White House Council of Economic Advisers, showed how the Zillow single family rent data leads the CPI shelter component by 12 months:

Click for larger graphic h/t @ernietedeschi

Click for larger graphic h/t @ernietedeschi

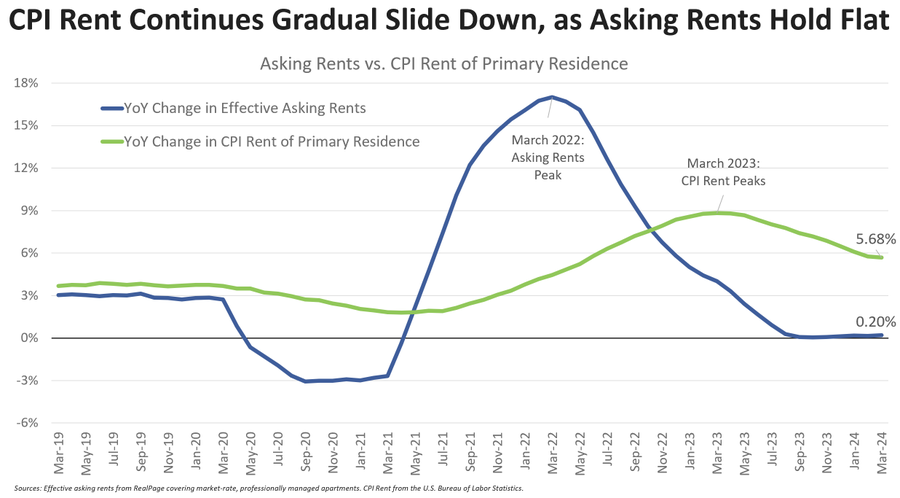

@jayparsons, a rental housing economist, showed this chart:

Click for larger graphic h/t @jayparsons

Click for larger graphic h/t @jayparsons

Cost of shelter – the two rent measures – accounts for 32% of the CPI and 43% of the core CPI. The blue line above shows real asking rents are up 0.20% YoY, not the 5.68% the Bureau of Labor Statistics used. If we multiply that 5.48 percentage point difference by the 32% that rents account for in the CPI, we get an overstatement of 1.75 percentage points. Subtract that from the 3.5% reported and annual inflation was just 1.75%. Using the same methodology, core CPI falls from 3.8% to 1.5% (hat tip @OphirGottlieb).

The month-over-month (MoM) increase was 0.4%, unchanged from February but a tick above economists’ forecast. The core MoM increase, which is a marginally useful number for figuring out what is really going on, was up 0.36%, also the same as February and also well above the consensus. A 0.36% monthly increase compounds to well over 4% annual inflation. Not good. The futures market has now pushed out the first rate cut into September. I think that the Fed will either cut by June or not at all to avoid looking partisan in the lead-up to the election. As I’ve been saying for months, “high – but not higher – for longer.” You heard it here first.

Unemployment

The Bureau of Labor Statistics said the US added 303,000 jobs in March, more than 50% above the consensus forecast for 200,000 and the largest gain in 10 months. The odds of all economists surveyed missing their nonfarm payrolls forecasts by such a wide margin for three straight months seem awfully low to me, but we’ll have to wait until after the election to see the final revisions.

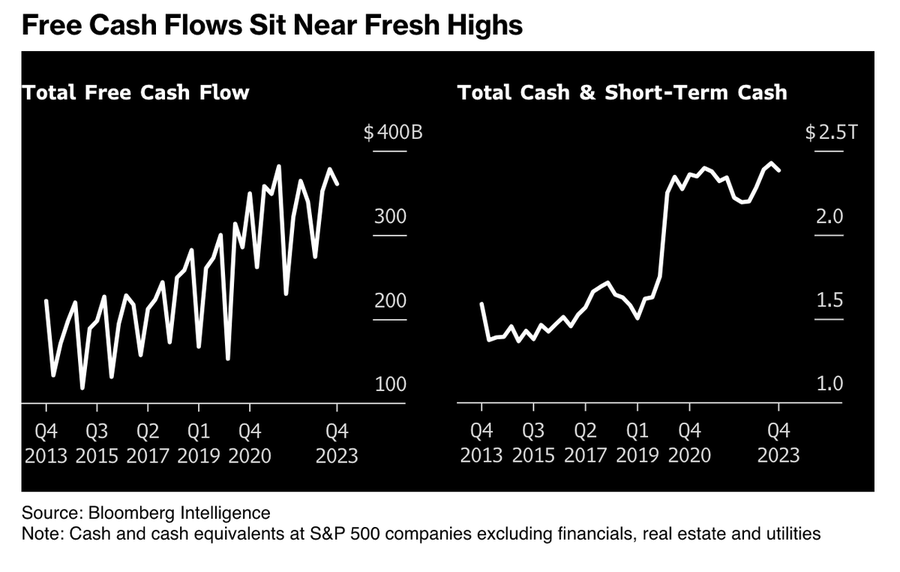

In the real world, corporate cash and free cash flow are at record high levels, supporting stock prices as we head into March quarter earnings results.

Click for larger graphic h/t @JessicaMenton

Click for larger graphic h/t @JessicaMenton

Market Outlook

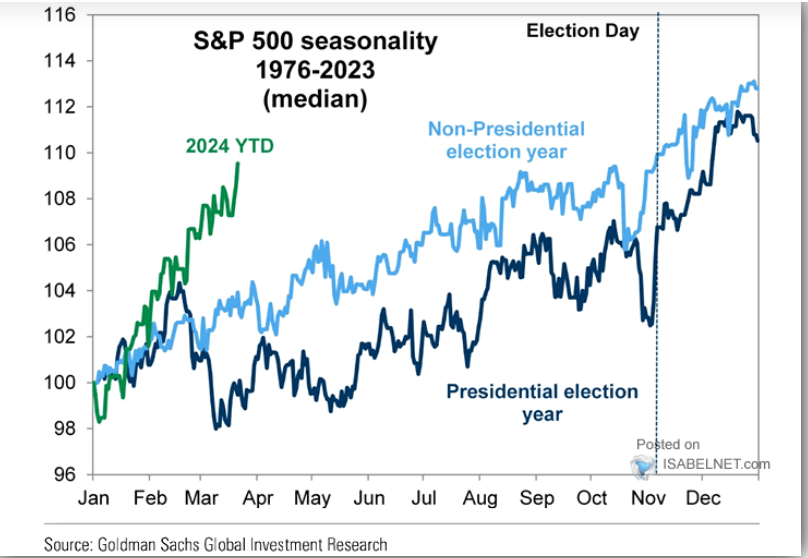

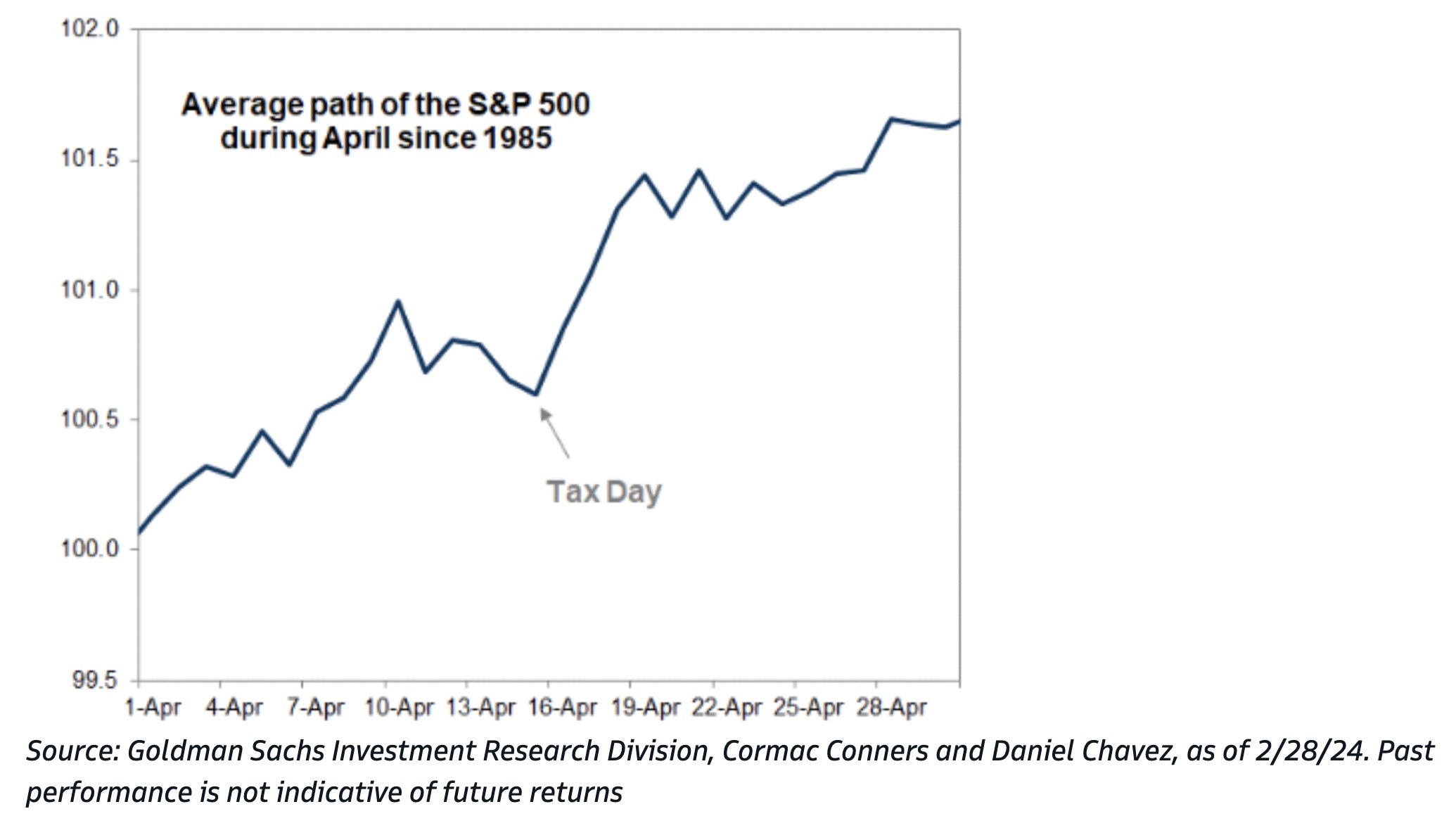

The S&P 500 added 1.0% since last Thursday as inflation reality came in not much worse than – maybe even a little bit better than – inflation fears. The Index is up 9.0% year-to-date, and has been much stronger seasonally that in a typical Presidential election year. You could argue that means (1) it’s ahead of itself; or, (2) that it’s a powerful sign of underlying strength. I think it’s both, so we’ll probably see high-level churning through the election.

Click for larger graphic

Click for larger graphic

Although April should get better after next Monday.

Click for larger graphic

Click for larger graphic

The Nasdaq Composite gained 2.4% as investors looked ahead to March quarter earnings, especially in technology. It is up 9.5% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 2.0% as riskier assets caught a bid. It is only up 2.2% year-to-date, though

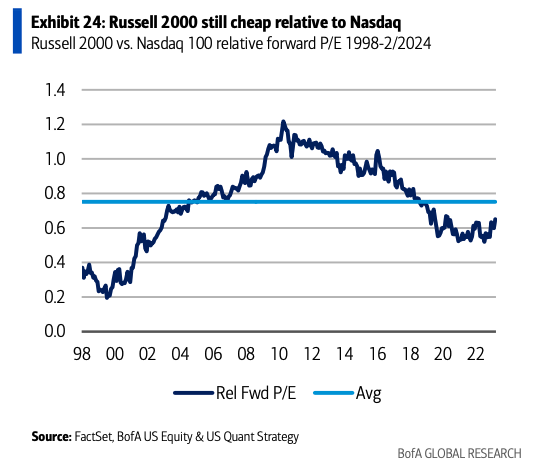

The small-cap Russell 2000 fell 0.5% and is (barely) up 0.8% in 2024. BofA said: “The Russell 2000 remains historically cheap vs. the Nasdaq, and as the overall corporate profits backdrop continues to broaden/accelerate, we see better trends for US small caps.”

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

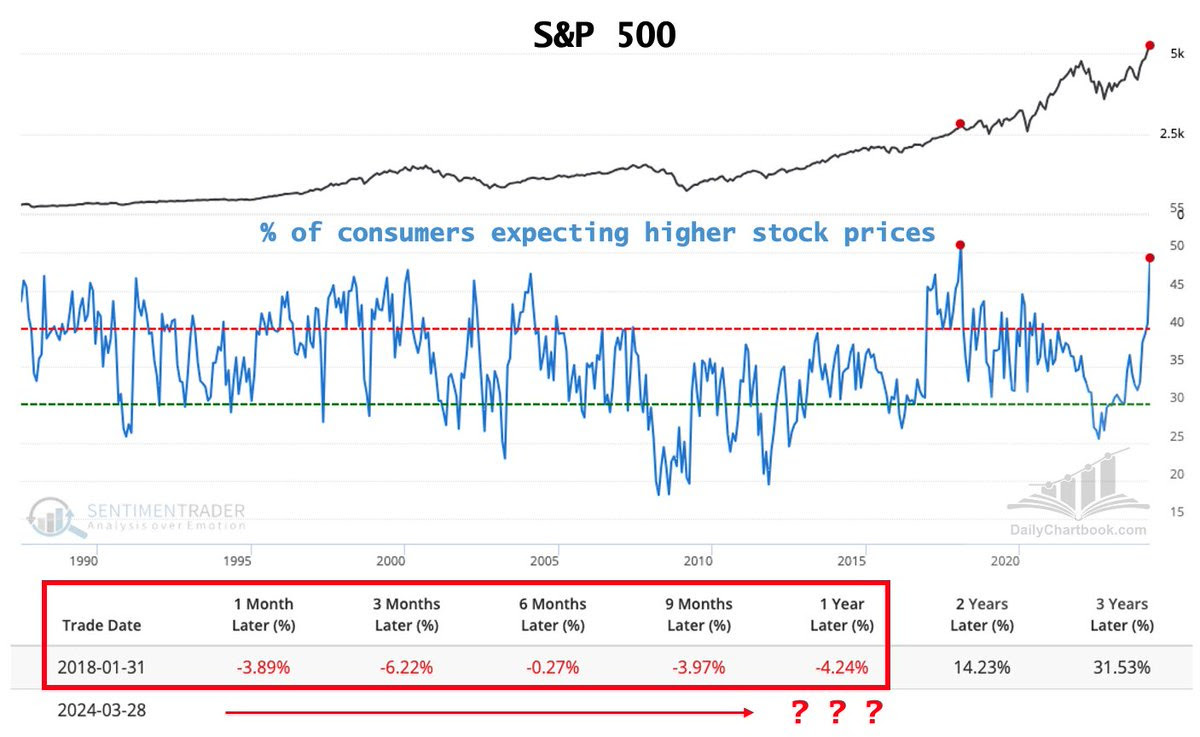

The newest Conference Board survey showed 49.3% of consumers expect higher stock prices. That number has only ever been higher once, in January 2018 at 51.0%. Following that instance, the S&P had mildly negative returns over the next 12 months, followed by a huge rally.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

The fractal dimension continues to grind out the necessary consolidation. As I said last week, this could continue for quite a while.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements at June WWDC and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model now is predicting March quarter real GDP growth of +2.4%, still a bit above the consensus for +2.1%. We get the first estimate in two weeks on April 25.

Click for larger graphic

Click for larger graphic

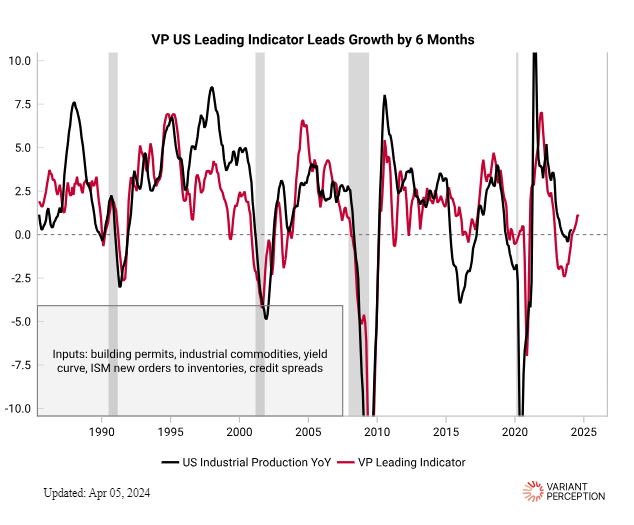

Variant Perception has a proprietary VP Leading Indicator of US economic conditions, and it is clearly inflecting higher:

Click for larger graphic h/t @VrntPerception

I may have to change my mild recession forecast if this keeps up.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Sunday, April 14

TGTX – TG Therapeutics – 7:30pm – Poster presentation at American Academy of Neurology annual meeting

Monday, April 15

INO – Inovio – 6:40pm – Festival of Biologics presentation “Advancing INO-3100 for the Treatment of Recurrent Respiratory Papillomatosis”

Tuesday, April 16

ABCL – AbCellera – 10:00am – Bloom Burton Healthcare Conference

MDNAF – Medicenna – 11:00am – Bloom Burton Healthcare Conference

Wednesday, April 17

TGTX – TG Therapeutics – 8:00am – 2 more poster presentations at American Academy of Neurology annual meeting

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $175.04) Vision Pro and spatial computing are going to change the way businesses operate. Workers can customize workspaces, collaborate on 3D designs, deliver specialized employee training, and guide remote fieldwork in entirely new ways.

According to Bloomberg, Apple already is assembling one out of every seven iPhones in India as they reduce their dependence on Taiwan and China. AAPL is a Buy under $175 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $32.27) was named to Goldman Sachs’ High Operating Leverage list. The company has said they can supply the next $3 billion in revenues without increasing their costs. Goldman said that they expect corporate profits to be the primary driver of forward equity returns. Stocks in the Goldman high operating leverage basket “are poised to benefit.”

They pointed out that high operating leverage stocks are trading near a record valuation discount to low operating leverage stocks. The median high operating leverage stock is expected to grow its earnings per share this year by 13% and is trading at 19x next-twelve-month earnings. The median low operating leverage stock is expected to grow its EPS by 7% and is trading at 24x next-twelve-month earnings. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

Meta Platforms (META – $523.16) introduced the next generation of their custom-made semiconductors designed for their specific AI workloads. These Training and Inference Accelerator processors wind up in custom-built computers to power their ranking and recommendation ads models on Facebook and Instagram.

Meta is one of the few companies large enough and smart enough to create the most efficient architecture for their unique workloads. AI compute requirements will only increase as the company’s new generative AI products, recommendation systems, and advanced AI research models get more sophisticated.

Piper Sandler said their latest Teen Survey showed

1) Facebook teen usage reach a four-year high

2) Year-over-year, Instagram’s usage lead over the next most popular app rose from 500 basis points to 800 bps

3) The largest observed improvement in teens voting Instagram as their favorite app since the debut of TikTok

Jefferies thinks Meta’s advertising will outgrow Amazon’s advertising in 2024 for the first time in a decade. Ads are 98% of Meta’s revenue, and the consensus expects 17.5% growth in 2024.The consensus 2024 ad revenue growth for Amazon is 22.4%. If Jefferies is right, or even close, there will be material upside to META earnings estimates. META is a Buy under $345 for a $400 target in 2024.

PayPal Holdings (PYPL – $65.80) teased their new innovations to revolutionize commerce, coming this year.

The new CEO, Alex Chriss, was on CNBC a couple of months ago, saying: “We will shock the world.”

Xoom, PayPal’s cross-border money transfer service, announced that US users now have the option to fund money transfers to friends and family abroad using US dollars converted from PayPal USD (PYUSD), a US dollar-denominated stablecoin. US Xoom users can easily convert the PYUSD in their linked PayPal Cryptocurrency Hub to US dollars and send money to recipients in approximately 160 countries globally with no transaction fees.

According to the World Bank’s September quarter 2023 report, the global average cost of sending $200 is just over 6%. With no Xoom transaction fees, cross-border money transfers funded using USD converted from PYUSD provides a lower cost option. PYPL is a Buy under $68 for a double in three years.

SoftBank (SFTBY – $27.98) sold 10.69 million shares of ValueCommerce back to the company for $70.8 million, reducing ValueCommerce’s position from “subsidiary” to “equity method associate,” which reduces SoftBank’s earnings volatility exposure. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Rocket Lab USA (RKLB – $3.86) won a $32 million contract from the US Space Force Space Systems Command to deliver the VICTUS HAZE Tactically Responsive Space Mission. Combining their launch and space systems capabilities as an integrated solution, Rocket Lab will design and build a rendezvous proximity operation (RPO) capable spacecraft, before launching it on Electron in 2025 with just 24 hours notice. After launch, they will operate it. The mission will be an exercise of a realistic threat-response scenario and on-orbit space domain awareness (SDA) demonstration.

The company is about to reuse a first stage fuel tank recovered during a January mission in a new launch. Reusability is one way to lower costs while maintaining or even increasing profit margins.

RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $0.33) has received purchase orders totaling $27 million since mid-December, with more than 50% of these orders from existing customers. The orders include the purchase of two Sapphire XC systems by Mears Machine, a leading global contract manufacturer, to supply parts for their defense and aerospace initiatives. The company ended the March quarter with $17 million in bookings and a $23 million backlog.

They did a “best efforts” public offering, which is the bottom of the barrel. They sold 34,285,715 units of stock and warrants at 35¢ each, raising about $11 million net of fees for about 14% dilution. The stock was clobbered and is climbing back.

There’s bad news and good news. The bad news is that the trouble with these deals is the low lifes that buy them sell their stock ASAP for 35¢ and keep the warrants as a free ride. So until most of the new stock gets sold, there’s a lid on the price.

The good news is they wouldn’t have done this if they were about to sell the whole company cheaply to someone. So I’m going to stick with them but slash my buy limit and target price, even though I still think they eventually will dominate the high-tolerance metal parts printing business. The buy limit goes to $1 and the target price to $10, although when it gets there I’ll probably raise it. VLD now is a Buy up to $1 for my $10 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $4.38) presented data on T-cell engagers (TCEs) against four tumor targets at this week’s annual meeting of the American Association for Cancer Research (AACR). The company’s VP: Translational Research said: “TCEs are among the most promising new modalities in cancer therapy, but limitations in efficacy and safety have been barriers to realizing their potential for solid tumor indications. Our data illustrate that we can repeatedly generate TCEs that maximize tumor-cell killing without inducing excessive cytokine release. Reducing the risk associated with CD3 engagement could improve efficacy both by widening the therapeutic window and by creating opportunities to further enhance potency through co-stimulatory modalities.”

“Widening the therapeutic window” is because the molecules were engineered using a specific set of rare CD3-binding antibodies that consistently show potent tumor-cell killing and low cytokine release across multiple targets, demonstrating their potential to expand the therapeutic window across solid tumor indications.

“Enhancing potency” is because AbCellera’s CD28-binding antibodies do not display superagonist activity, which is a property associated with toxicity. Integrating co-stimulatory building blocks should enable development of molecules with enhanced potency for difficult-to-treat cancers.

The SVP: Partnering said: “Our platform for creating precision TCEs to address indications in cancer and autoimmunity provides a strong foundation for both internal programs and strategic partnerships. We look forward to advancing these programs with the aim of delivering powerful new medicines for patients.”

Or, to put it bluntly: “License me! License me!” Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Compass Pathways (CMPS – $9.18) presented at the Needham Healthcare Conference (AUDIO HERE). The two Phase 3 trials are on track, the first for a top-line data release at the end of 2024 and the second for a data release in mid-2025. A Phase 2 study in PTSD will read out in the next couple of months.

Click for larger graphic

Click for larger graphic

Compass had $220.2 million in cash at the end of 2023 and raised another $31.4 million this year. They expect to burn $110 million to $130 million this year. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2026

Probable time of next financing: Late 2025

Invitae (NVTAQ – $0.00) is at $0 pending the outcome of the April 17 auction. The company presented new studies at the American Society of Breast Surgeons (ASBrS) annual meeting this week. They showed how machine learning can reduce variants of uncertain significance (VUS) in patients who have received genetic testing for breast cancer, in addition to results from real world data showing that uncertain results do not lead to an overuse of mastectomies for breast cancer patients. Hold NVTAQ.

Primary Risk: Current shareholders don’t own any of the restructured company.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Mid-2024.

Inflation MegaShift

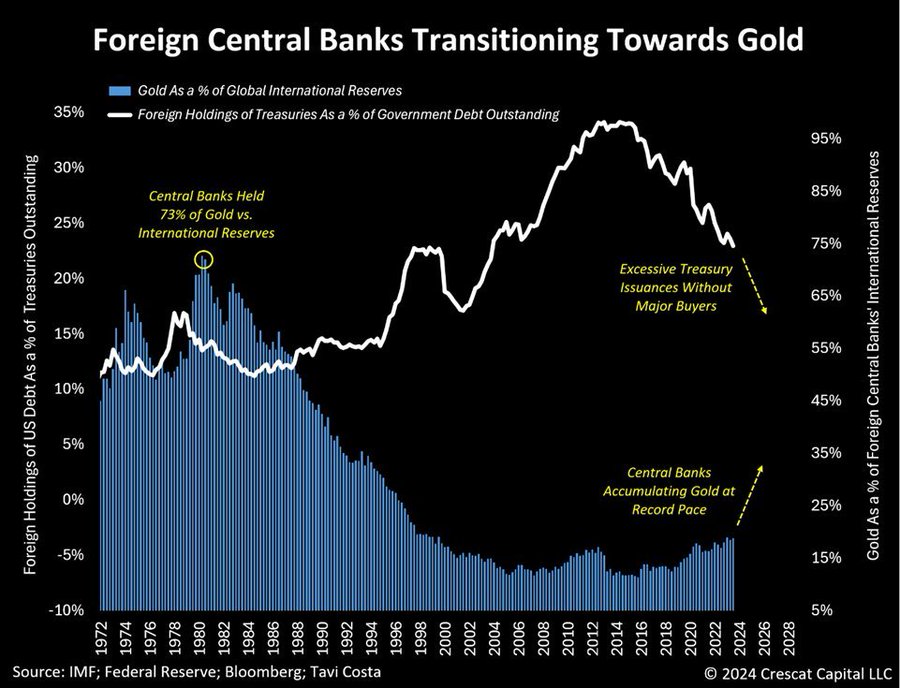

Gold ($2,390.60) has had 13 straight up days to all-time intraday and closing highs today. Foreign central banks are getting out of the way of Secretary Yellen’s firehose of Treasury paper by swapping into gold.

Click for larger graphic h/t @TaviCosta

Click for larger graphic h/t @TaviCosta

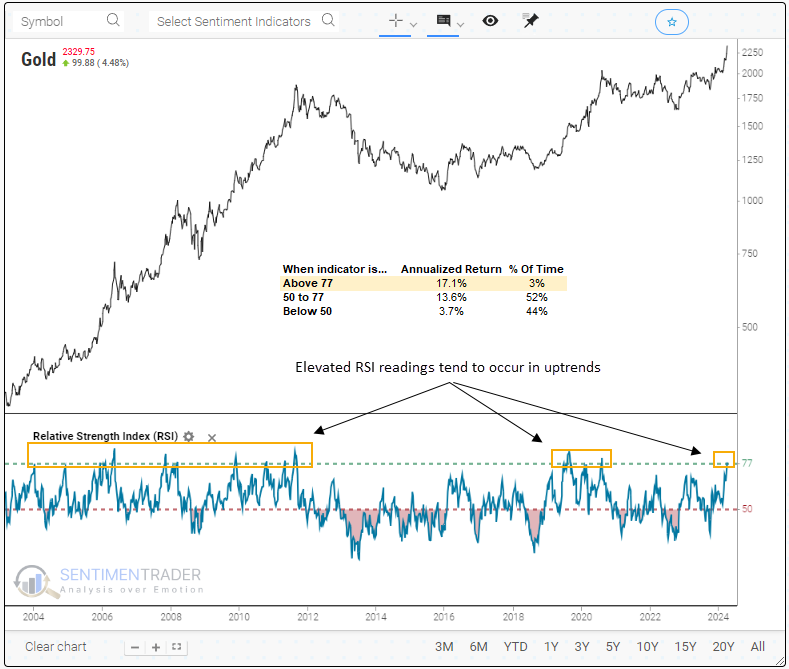

Gold’s weekly Relative Strength Index surpassed a reading of 77, a scenario observed in just 3% of precedents since 1973. Going forward, instances above 77 have yielded a remarkable 17% annualized return for the precious metal.

Click for larger graphic h/t @sentimentrader

Click for larger graphic h/t @sentimentrader

How will we know when this first breadth thrust is coming to a conclusion? I’m looking for a climax, and gold can’t fake it. I expect to see inflows into the metal exchange-traded funds. I’d like to see CNBC talking nonstop about gold. I want to see junior miners finally able to raise capital. Finally, I expect to see stories about gold starting to catch up with the price of gold.

Click for larger graphic h/t @hkuppy

Click for larger graphic h/t @hkuppy

For now, the fractal dimension has plenty of energy to push the price of gold higher.

Miners & Related

Coeur Mining (CDE – $4.79) presented at Gold Forum Europe (SLIDES HERE). It was their standard presentation.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.45) announced March quarter sales and revenue, although they won’t announce earnings until May 2. They sold approximately 20,300 attributable gold equivalent ounces and realized preliminary revenue of $42.8 million. Preliminary cost of sales, excluding depletion, was $5.7 million, resulting in cash operating margins of approximately $1,781 per attributable gold equivalent ounce.

CEO Nolan Watson posted another investor meeting:

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $70,734.71) fell below $70,000 as numerous day traders were liquidated and quickly bounced back.

The upcoming fourth bitcoin halving around April 20 is already priced in for the short term. It may follow a “buy the rumor, sell the news” pattern for a few months, mirroring the second halving in 2016. But this time around the bitcoin ETF holders are likely to buy more to capture the long-term impact of the supply shocks.

This halving will result in the smallest reduction in new issuance, in terms of bitcoins, in bitcoin’s history so far. But measured in dollars, the value of this issuance reduction is its highest ever, simply because bitcoin’s price is near its all-time high. At the time of the third halving on May 11, 2020, bitcoin was approximately $8,800. Today it’s over $70,000.

Click for larger graphic h/t @AndreasSteno

Click for larger graphic h/t @AndreasSteno

In the last month of high prices, most miners have not only sold off their entire mining rewards but also dipped into their reserves. The market has adjusted to a new equilibrium that accommodates all-time high selling activity by miners. When this selling pressure is reduced by half due to the halving, I believe the halving will push bitcoin up pretty quickly.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $40.17) is a Buy for the 2024 and 2028 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

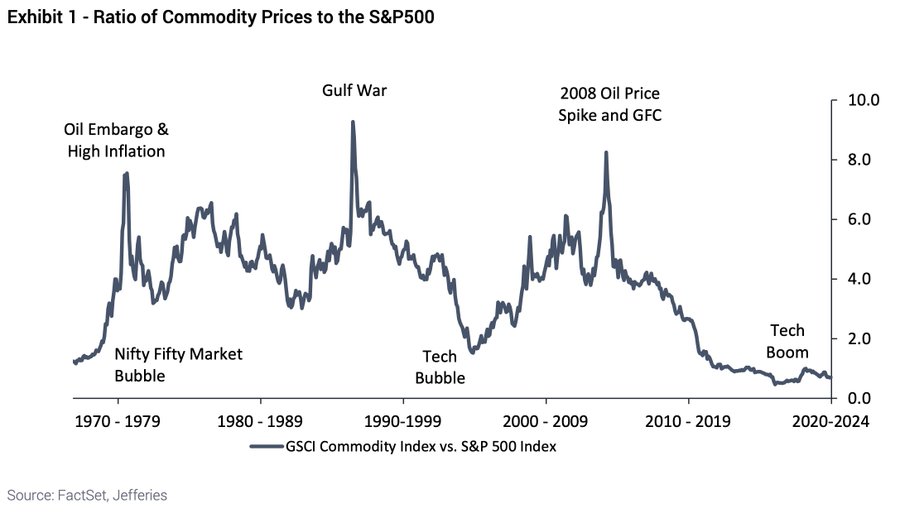

Commodities

The ratio of commodity prices to the S&P 500 is near all-time lows. Turnaround coming.

Click for larger graphic h/t @Schuldensuehner

Click for larger graphic h/t @Schuldensuehner

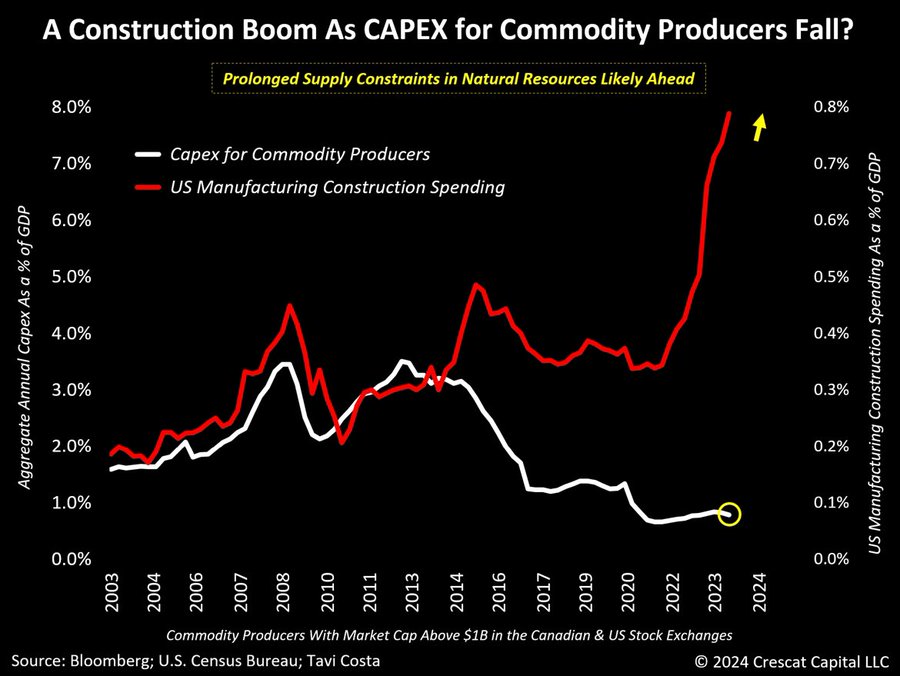

Despite the recent upsurge in construction spending, capital spending in natural resource industries has remained near historically low levels. Changes in the supply curve of commodities typically align with the capital spending behavior of the underlying producers, although with a significant lag. It takes time for investments to translate into increased supply. Substantially higher prices will be necessary to incentivize new capex investment, and it will take many years before these new supplies come on stream in a significant enough way to lower prices. It has been taking 10 years or more on average to bring a new discovery into production.

Click for larger graphic h/t @TaviCosta

Click for larger graphic h/t @TaviCosta

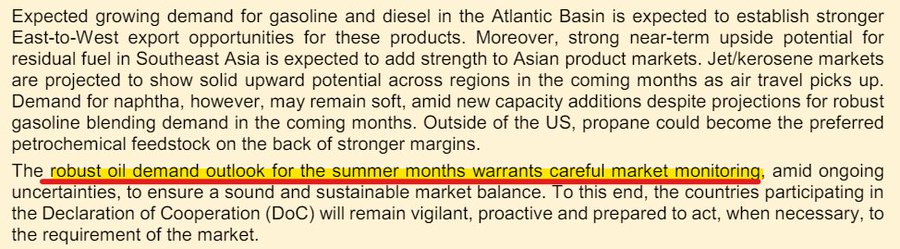

Oil – $85.57

With oil solidly bid at $85+, it’s probably time to pause the upswing to let everyone adjust to the new normal. I expect the Energy Information Administration to report crude builds for the next few weeks as they try to undo some of their weird 2023 adjustments. The Saudis want oil around $85 for now because they don’t want demand destruction. In fact, there was quite a change in tone from OPEC+, flagging the need to carefully monitor the “robust oil demand outlook for the summer months.”

Click for larger graphic h/t @JavierBlas

The July 2026 Crude Oil Futures (CLN26.NYM – $70.69) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $41.27) is a Buy under $40 for a $100+ target.

* * * * *

* * * * *

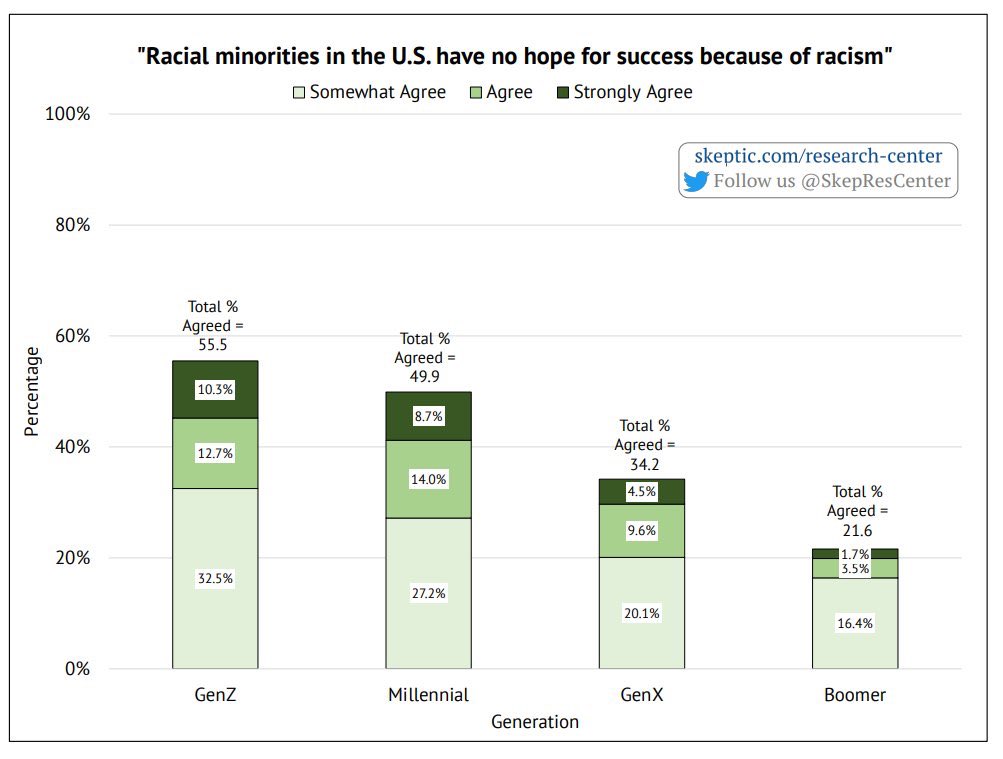

Perception: Almost 50% of Millennials and a majority of Gen Z think “Racial minorities in the U.S. have no hope for success because of racism.”

Click for larger graphic h/t @TheRabbitHole84

Click for larger graphic h/t @TheRabbitHole84

Reality: Some of the most successful groups in the United States are racial minorities.

Click for larger graphic h/t @TheRabbitHole84

Click for larger graphic h/t @TheRabbitHole84

Your reviewing The Battle of the BADS Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 4/11/24. Check out the complete Portfolio page HERE.

Portfolio Protection

April 30 SPY $505 put (SPY240430P00505000 – $3.91) swap for the June 21 SPY $505 put (SPY240621P00505000 – $6.42)

April 30 SPY $410 put (SPY240430P00410000 – $0.16) swap for the June 21 SPY $410 put (SPY240621P00410000 – $0.63)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $175.04) – Buy under $175 for new iPhones

Corning (GLW – $32.27) – Buy under $33, target price $60

Gilead Sciences (GILD – $68.65) – Buy under $80, target price $120

Meta (META – $523.16) – Buy under $345, target price $400

PayPal (PYPL – $65.80) – Buy under $68, target price $136

SoftBank (SFTBY – $27.98) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $7.34) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $55.97) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $13.74) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.82) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $13.86) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.86) – Buy under $13, target price $30+

Velo3D (VLD – $0.33) – Buy under $1, target price $10

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $4.38) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.53) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.38) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $9.18) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $11.76) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.41) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.60) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $14.76) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($28.60) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $27.01) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $33.74) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $22.23) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $32.19) – Buy under $30, target price $50

Coeur Mining (CDE – $4.79) – Buy under $5, target price $20

First Majestic Mining (AG – $7.96) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.47) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.45) – Buy under $10, target price $25

Sprott Inc. (SII – $42.02) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $70,734.71) – Buy

iShares Bitcoin Trust (IBIT – $40.17) – Buy

Ethereum (ETH-USD – $3,503.83) – Buy

Grayscale Ethereum Trust (ETHE – $25.73) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $70.69) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $41.27) – Buy under $40; $100+ target

Vermilion Energy (VET – $12.48) – Buy under $11; $24 target

EQT (EQT – $37.49) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.42) – Buy under $8; $30 target

Freeport McMoRan (FCX – $50.74) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $32.00) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $21.26) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.02) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $27.22) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.51) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.01) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.48) – Hold for buyout

Invitae (NVTAQ – $0.00) – Hold for April 17 auction

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1st

MM–on AKBA, there is talk about a 3 year extension of TDAPA at 65%. I interpret this as for 2 years, the add-on payment of 100% gives a total of 200%. Then for the following 3 years, AKBA gets 65% add-on for a total of 165%. Is this correct?

VLD, I think your bad news/good news assessment is realistic, especially with this AM’s announcement of hiring of legal VP Nancy Krystal to foster a favorable M&A if VLD cannot remain independent. But target share price over $10 if they can stay independent?

Thanks for your input. Yes, 27 million in purchase orders is some solid interest. And 23 million in backlog isn’t bad either. I don’t get the sell out narrative but either way it looks very promising at this point. IMO

VLD is DOA. Why is everyone chasing penny stocks on this board?

I doubt you have done much analysis on VLD. Its product is the ultimate in tangible real asset value like precious metals, with real industrial utility, unlike hyped crypto crap, a figment of the imagination. Don’t be cocky and think that your “safe” crypto wallet is bulletproof. When the electricity goes out, your slate can be wiped clean and gone forever. I have paper records of my online brokerage statements for backup.

AI is total garbage. Yahoo message board censorship is totally arbitrary AI. One typical example–I was discussing P/E ratios. The AI interpreted this as sounding like “pee ratio” and thought it was sexual, vulgar language. Anyone on YMB knows what P/E means, but Yahoo AI thinks it is vulgar, uncivil language. Many other factual posts of mine without any off color remarks are deleted for being “uncivil.” Many other posters have said the same thing. They spent lots of time trying to discuss things in depth, but their posts were blocked by Yahoo, and they gave up in frustration. This happens quite often. One of the biggest corrupt companies is NVDA. In an AI world, we are all doomed by AI robots which cannot be dealt with. Meanwhile, I do not buy products from any company that doesn’t have customer service people I can talk to. Chat boxes are depersonalized garbage and a waste of time.

It is true that subscribers who bought VLD around $10 will likely never break even. If it gets back to $1, highly likely, they will have a 90% loss, but I will have over a double.

Well BTC is around 68k. VLD is around 31 cents so there is that. If the electricity goes out, good luck with your stocks. Are you going to head into your brokerage waiving your paper receipts around and demand money? Good luck.

Just because the horrible yahoo message board has a horrible implementation of AI doesn’t mean AI is garbage. It means the developers at yahoo aren’t the best and brightest.

Paper records have value in court. Your blank slate of crypto has no value. Yahoo AI is totally bad. The best and brightest of AI developers anywhere can’t be trusted. For disputes, you can’t deal with any AI robot.

Your comment about racial perception vs reality is off the mark. Obviously when asked about racial inequality, we all know we are talking about African Americans. Nobody is even thinking about Indians, Chinese or Japanese Americans.

Your chart proves the point, African Americans are doing the worst. Nice try though.

MM, interesting article on MDNA11 results. Thoughts??

https://www.oncologypipeline.com/apexonco/aacr-2024-medicenna-looks-cytokine-renaissance

I am a buyer of this stock as well. I picked up 700 and change last week.

Hey John and Doyle, what’s your opinion on MDNA, when and how much will this stock appreciate? When I asked MM last week if this stock or SCYX had the best chance to double this year he said SCYX, your thoughts?

This is one of the few times that I agree with MM as I think SCYX has the better chance to double, especially when the hold is removed. I’m hoping MDNA doubles as well, but it may take a little time. I asked MM on the previous message board for his thoughts as it dropped on 4/9 from $1.32 to 1.09 on some preclinical data for MDNA113. (which didn’t make sense) Then it bounced back the next few days to $1.42 with the MDNA11 results.

I think it’s a good horse in the race. I am up 57 percent , my 4k is now 7k. And it was swimming upstream in the big selloff last Friday. For a high risk bio tech that’s a milestone in itself as they are usually the first ones to take a hair cut in a big market selloff. It’s up 358 percent in the past six months. Two of my advisors are saying that 2024 is going to be a lucrative place to be in biotech stocks .

It has promising cancer drugs and if you are over 50 what’s not to like about that? Not only does it have upside potential but it could also possibly save your life one day. That’s priceless. It had a high in 2020 of $4.50 ish. So with the current run up in the last six months and the history of once being at $4.00 and change, I am thinking other investors are thinking the same. That’s my short term target.

Just IMO

Hey John, do you see MDNAF at your $4 tsrget this year? What are the catalysts? Appreciate your insights.

If it does a double from here and goes up another 322 percent then the price will be $4.21.(if my math is correct?) That’s quite aggressive over that time frame. But these biotechs can be crazy. Who knows ? Depending on their trials and the whims of the FDA. (The FDA can fast tract their lead products if they feel a need for urgency and are confident they will succeed.) If not, I still think it can get there eventually. Just IMO

MM – thx for the insights. Can you clarify your Bitcoin comments, I’m not following what sounds contradictory? You first say the Bitcoin halving impact may be muted or priced in already, then you say the halving will move the price up rather quickly. What is your price target and timing?

MM, what’s your take on the Israel/Iran train wreck this weekend? How will it affect the markets in the short and long term?

So around 5:30 INO issues it’s Annual Report to shareholders which lists that they have cash runaway into the 2nd quarter of 2025. Then about a hour later they announce an offering and warrants at 7.69 when the stock closed at 10.99 today. WTF??

INOVIO POWERING DNA MEDICINES™ 660 W. Germantown Pike, Suite 110, Plymouth Meeting, PA 19462 Dear Shareholder, Phone:267-440-4200 Fax:267-440-4242 http://www.inovio.com The past year has been transformational for INOVIO. Today we are a company planning to submit a Biologics License Application (BLA) for our lead product candidate, INO-3107, in the second half of 2024 under the FDA’s accelerated approval program and preparing for the potential commercial launch of our first product in 2025. If approved, INO-3107 could become the first non-surgical therapeutic option for patients with Recurrent Respiratory Papillomatosis (RRP), a rare and debilitating HPV-related disease of the respiratory tract, and would be the first DNA medicine available in the United States. To achieve this transformation, we prioritized our product pipeline to focus on INO-3107 and other late-stage assets with strong commercial potential that are intended to treat diseases with high unmet medical need. We also remained committed to financial discipline, cutting our operating expenses by nearly half and maintaining a cash runway that we estimate will extend into the second quarter of 2025 without giving effect to any potential financing activities that we may undertake. But most importantly, we have focused on leveraging the advantages of our platform to deliver on the promise of DNA medicine for patients. Our strategic refocus also helped drive progress elsewhere across our product pipeline, including a clinical collaboration and supply agreement entered into with Coherus BioSciences in January 2024 to develop our product candidate INO-3112 in combination with LOQTORZI™ for HPV-related throat cancer. We also shared encouraging early-stage clinical results for our Ebola booster vaccine candidate, INO-4201, continued to advance other clinical-stage candidates through strategic collaborations, and made progress with promising preclinical next-generation candidates. We expect that the year ahead will provide ample opportunity to maintain our positive momentum. In addition to submitting our BLA, we plan to initiate a confirmatory trial of INO-3107 in the second half of 2024 while also continuing critical preparations for potential commercial launch. We also anticipate publishing important immunology data for INO-3107 in a peer-reviewed scientific journal later this year. As for our immuno-oncology candidates, we plan to finalize the trial design for the trial of INO-3112 in combination with LOQTORZI in patients with throat cancer, as well as to determine next steps for our candidate INO-5401 for the treatment of glioblastoma, a deadly form of brain cancer, with our strategic collaborator Regeneron. We also expect key development milestones for our infectious disease candidates, including determining next steps for INO-4201 and generating the first clinical data from our Phase 1 trial evaluating an anti-SARS-CoV-2 DNA encoded monoclonal antibody (dMAb) candidate. We have accomplished so much by focusing on the strengths of our DNA medicines platform and staying true to our renewed strategic vision, but our progress would not be possible without the continued support of our valued shareholders and the unwavering commitment of our talented team. I’m confident that together we can deliver on the potential of DNA medicine for patients around the world. Sincerely, Dr. Jacqueline Shea President and Chief Executive Officer

MM, thoughts on this? Amazingly, the price closed at $9.64 and actually hit a high of $10.21 yesterday.

Powell signals rates “HIGHER FOR LONGER” Did he tell you that MM?

hahaha The markets have absorbed this and are moving up today at least.About the only thing that I can figure is that now thist this is somewhat settled (cuts or nocuts) then some serious investing can take place. Call it the no uncertainty rally.

S&P: SEESAW

If anyone is interested in a short term catalyst, you might want to check out RAPT Therapeutics(RAPT) The stock was hammered in February as one of their trials was put on hold by the FDA due to 1 patient that had a SAE of liver failure.(there are 350 patients in the study and no liver toxicity was observed in any other patients) The stock went from $25.97 to as low as $6.86 on the news. It’s currently trading at $8.13. This particular patient had Covid at one time and took Herbal supplements and this is the likely cause of the event. RAPT recently releases promising results from a Phase 2 trial on Head & Neck Cancer patients. The hold should probably be lifted in the next few months and while the price may not go back to $25, it should go up significantly. They have a solid cash position of $158.9 million and they are not a 1 trick pony. There is no guarantee that the hold will be lifted, so invest at your own risk.

ACXP – Registration Statement Withdrawal

ACXP is withdrawing the Registration Statement that was initially filed on March 18, 2024.

“The Company has determined not to pursue, at this time, the public offering to which the Registration Statement relates. The Registration Statement has not been declared effective by the Commission and no securities have been issued or sold under the Registration Statement.”

Why would they do that?

ACXP- One of two things I can come up with. No one interested in the offering or there working on a deal.

The best scenario is #2. The stock rose 18% today, so maybe #2 is more likely, although the stock has had hyperactive spikes up to $8 many months ago.

Thanks. If they canceled the offering because nobody interested the stock falls back. If they canceled because they have other plans I think the stock will go up. Big question what are there plans? I don’t think they would cancel if they just had a partner. So a binary event. Either they canceled because no interest or a buy out in the works.

New World Investor for 4.18.24 is posted.