Dear New World Investor:

The Federal Reserve’s preferred inflation gauge showed prices heated up to the highest level in three years, likely keeping the central bank holding interest rates steady with an eye toward hiking if inflation doesn’t dissipate.

The year-over-year Personal Consumption Expenditures (PCE) index rose 4.1% in May, in line with expectations, and up from 3.8% in April. Month-over-month, inflation rose 0.4%, a tenth of a percentage point less than expectations and the same level as April.

The core PCE excluding volatile energy and food prices – the Fed’s favorite inflation gauge – was up 3.4% year-over-year, in line with expectations and up a tenth from 3.3% in April. Month-over-month, core inflation rose to 0.3% versus 0.2% in April – the highest level since October 2023.

The plunge in oil prices will keep a lid on the headline number for the next couple of months (June could be negative), but I don’t think the Fed will move rates down or up this year. Eight Fed members agree with me that rates will be steady, but you should know that nine of them expect one hike and six expect two. On average, they expect that headline PCE will end the year at 3.6%, and the core PCE will end at 3.3%. The CME Fed Watch Tool shows 48.5% expect a 25 basis point (¼ of 1%) increase in September.

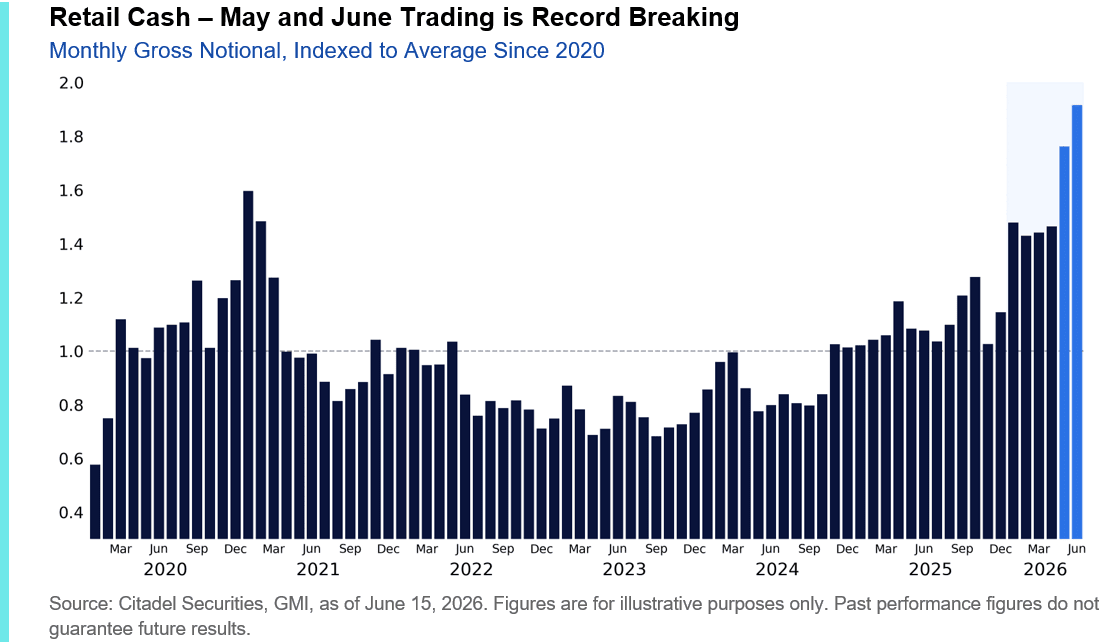

In this “muddle through” economic environment, some of the $9 trillion in sideline cash is coming back into the market. Some of that cash was built up by investors who feared a recession or depression, some feared runaway inflation, some thought the Iran war would widen, some thought AI was a bubble that would pop and cause a Crash. According to Citadel Securities: “May shattered previous activity records in cash equities. From this peak, activity has accelerated further in June, with volumes this month tracking 9% above May’s record. Nine of the ten largest retail trading days ever observed on our platform have occurred in just the last month, including seven during the first half of June alone.”

Click for larger graphic h/t Citadel Securities

Click for larger graphic h/t Citadel Securities

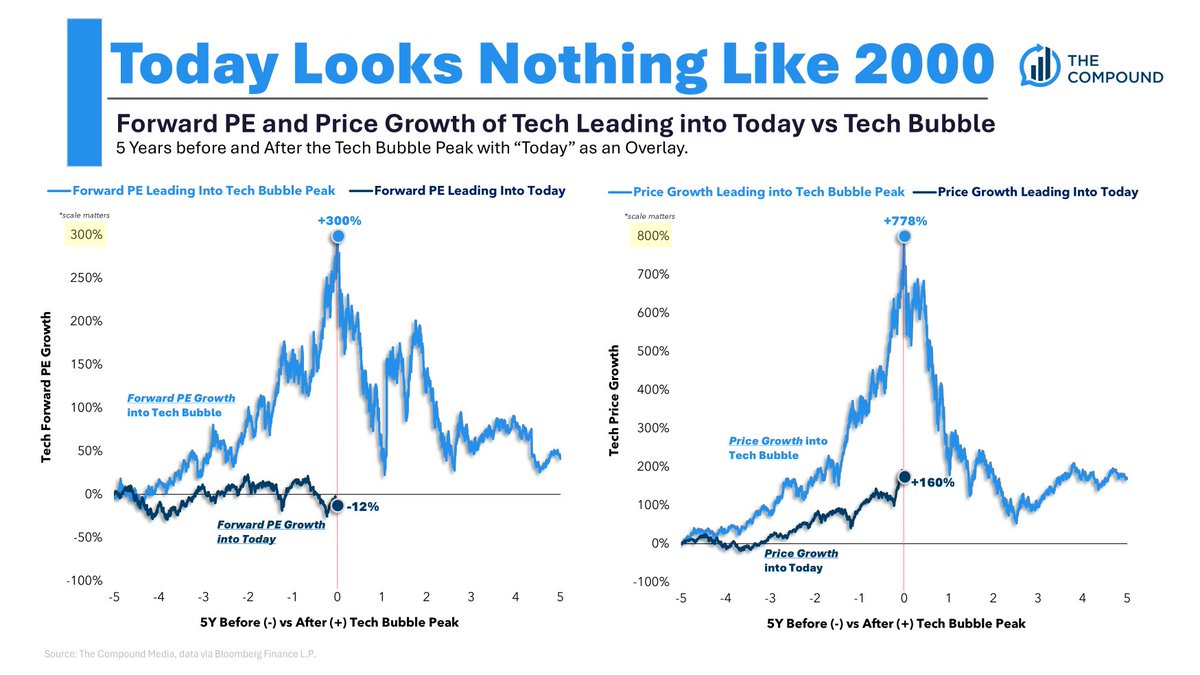

I am going to revive the California Technology Stock Letter as a standalone publication because I think we are in the Fourth Industrial Revolution, which is defined by the blurring lines between the physical, digital, and biological spheres and driven by artificial intelligence, robotics, and biotechnology. This will drive stocks up to the next 36-year cycle top in 2036.

Of course there will be pullbacks and maybe even shallow bear markets along the way. But we are starting from a good place. The forward Price/Earnings and P/E to growth (PEG) ratios of Big Tech today compared to the dotcom bubble show very different pictures.

Click for larger graphic h/t @mattcerminaro

Click for larger graphic h/t @mattcerminaro

AI stock prices have surged because their fundamentals are strong. This is the MegaShift of the next 10 years, and those who avoid it or exit too early will leave years of returns on the table. AI revenues already exceed the huge depreciation costs of giant data centers. Anthropic had its first revenue dollar in 2023. By the end of 2024, its annual recurring revenue reached $1 billion. By April 2026, it had annual recurring revenue of $34 billion. That jumped to $45 billion by May.

In the dotcom boom, telecom companies spent billions burying optical fiber. After the bubble burst, 95% of that fiber sat unused for years. But there are no dark GPUs. Nvidia is sold out and back ordered. The Nvidia A100 launched in 2020. Six years later, these still sell for nearly the same price as when they launched. Microsoft continued operating cloud machines based on Nvidia’s V100 until September 2025. That chip launched in 2017. Google says some of its seven- and eight-year-old TPUs still operate at 100% utilization. ChatGPT serves more than 900 million people every week.

Unlike the dotcom bubble, the biggest AI spenders are the richest and most profitable companies ever created: Microsoft, Alphabet, Amazon, and Meta Platforms. And they’re funding most of the AI buildout out of cash flow.

OK, OK, but aren’t the valuations insane? Not any more. In 2021-2022, Nvidia, which dominates AI hardware, traded near 70x forward earnings. Today, its forward P/E ratio sits in the low 20s. Palantir, which dominates AI software, is down 48.3% from its November 2025 high. And the AI boom has years left to run.

Market Outlook

After much hue and cry from both bulls and bears, the S&P 500 lost just 0.5% over the last two weeks. The Index is up 7.5% year-to-date. The Nasdaq Composite lost 1.7% as weak hands abandoned the AI trade. It is up 9.1% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) soared 14.3% on more merger announcements. It is now up 24.3% year-to-date. The small-cap Russell 2000 added 3.9% to an all-time high today and is up 21.2% in 2026, yielding the #1 spot to the XBI.

Top 5

Changes this week: None

Near-Term – chronological order

INO Inovio – bounce back from equity offering + FDA allows 6-month review of INO-3107

AKBA Akebia Therapeutics – Vafseo launch

BTC-USD Bitcoin – rebound from sell-off

ETH-USD Ethereum – rebound from sell-off

EQT EQT – natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model forecast for June quarter real GDP growth dropped sharply to +2.5% as the Blue Chip economists continued to adjust to various better-than-expected reports.

Click for larger graphic

Click for larger graphic

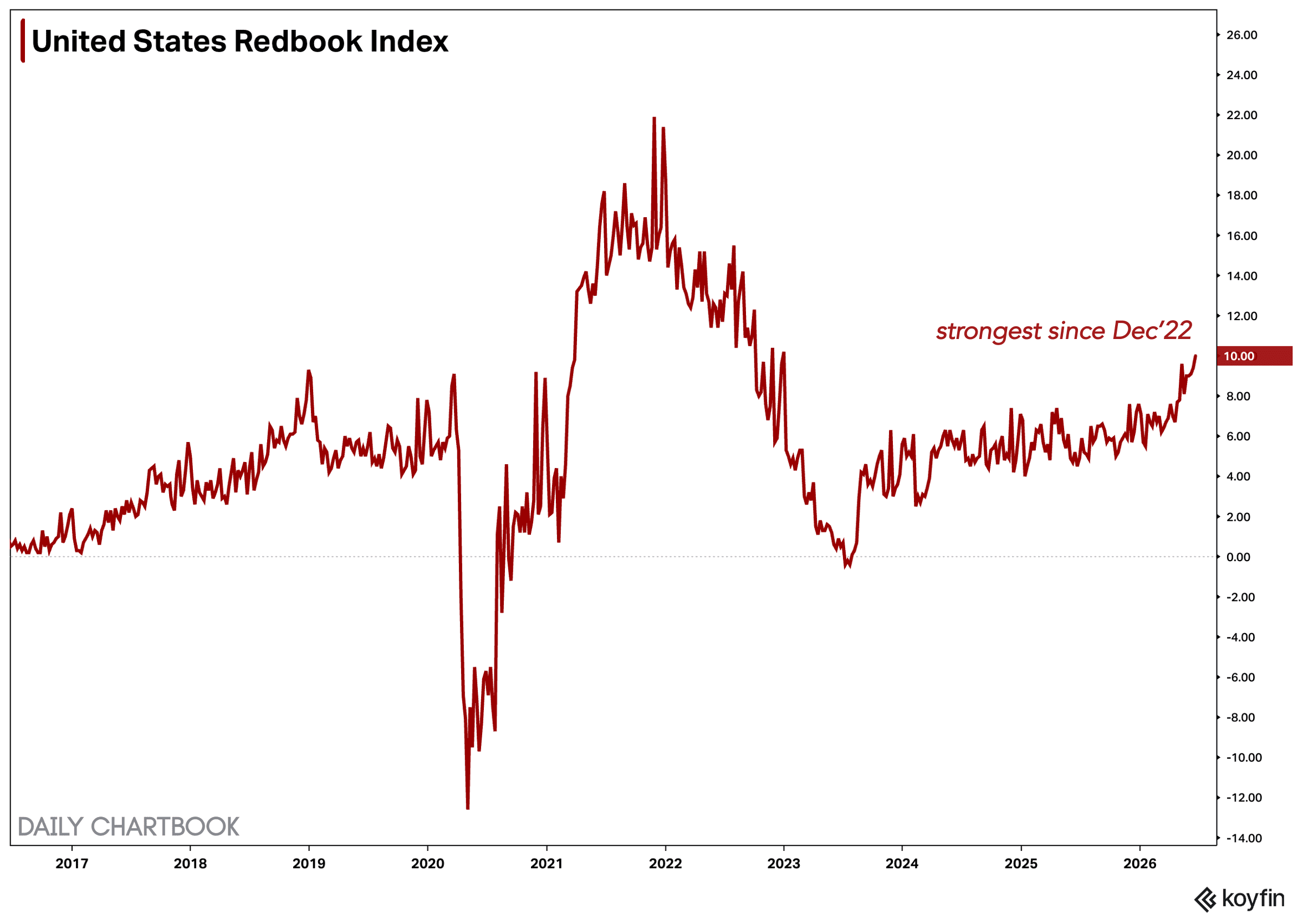

The US Redbook Index of same-store retail sales continue to flash exceptional strength: +10% year-over-year for the week ending June 20, up from +9.4% the previous week.

Click for larger graphic h/t Koyfin

Click for larger graphic h/t Koyfin

Dollar Death Watch

The US dollar broke out to a new 52-week high last Thursday. During the second half of the 1990s, investors around the world wanted exposure to American assets. They wanted US stocks, especially of US technology companies. They wanted dollars. Capital poured into the United States, and stocks and the dollar benefited. It looks like something similar is happening today in AI stocks, large and small.

Click for larger graphic

Click for larger graphic

Or maybe the dollar is just rallying on expected rate hikes. Ultimately, I don’t think they will happen. The market will re-rate the dollar lower when it realizes no hikes are coming any time soon. Until then, this is a headwind for precious metals prices.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, June 29

QUIK – QuickLogic – Before the open – Joins the Russell 3000 and the small-cap Russell 2000 Indexes

Tuesday, June 30

Job Openings and Labor Turnover Survey (JOLTS) – 10:00am

Thursday, July 2

June payrolls – 8:30am

Friday, July 3

Markets Closed – 250th Anniversary of the US

Friday, July 10

DC – Dakota Gold – 2:00pm – Rule Symposium for Natural Resource Investing

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $275.15) is on track to release an updated version of their AirPods and a second generation foldable iPhone in 2027, according to Bloomberg. Supposedly, the new AirPods will have cameras to become the company’s first AI wearable. If you are wondering why something in your ears would take pictures, fear not! The cameras will not take photos and videos, but will provide the new Siri AI with visual context. Users could ask questions about their visual environment, such as food ingredients, and have Siri come up with a dish.

The camera AirPods were initially set to ship in 2026, but have been pushed back because of issues with AI software. Bloomberg also said Apple is already working on the second-generation foldable iPhone, code named V78, even though the first-generation foldable is still set to arrive later this year, despite some reported hiccups.

I could say we will wait to see if John Ternus, the new CEO, can (1) actually ship the new AirPods in 2027, and (2) get people to buy a foldable phone when the second-generation model will obsolete it next year.

I could, but I won’t.

The problem here is that APPL is up 130% over the last five years, but largely from multiple expansion, not fundamental growth. It now trades at 34x forward earnings and a 2.5x Price/Earnings/Growth (PEG) ratio, with a free cash flow yield under 2.3%, making its risk/reward profile not that compelling. Worst of all, Apple lacks direct AI exposure and had to outsource the AI for Siri AI to Google’s Gemini.

We first bought Apple at $27.25 on December 17, 2015, and I’ve raised the Buy Limit from time to time to pick off transient declines. But at today’s close of $275.15, I think it’s time to book the 10x gain and move on. Yeah, I know it was clipped for $18 a share today, and probably will bounce back. There are core AI stocks we may own for the next 5 to 10 years – Nvidia and Palantir come to mind – but Apple is not one of them. I applaud them for not building huge data centers to sell time, but I fault them for not having a data center and an effective AI effort for internal use. Sell AAPL.

Gilead Sciences (GILD – $126.84) said that the European Commission has granted marketing authorization for Trodelvy as monotherapy for the treatment of adult patients with unresectable or metastatic triple-negative breast cancer who have not received prior systemic therapy for metastatic disease and are not candidates for PD-1 or PD-L1 inhibitor therapy.

The FDA accepted Gilead’s application for a once-weekly pill version of Yeztugo (lenacapavir) for pre-exposure prophylaxis (PrEP) of HIV. The sNDA has an FDA action date of February 2, 2027. Yeztugo is currently approved as an injection. After initiation dosing, subsequent doses are given every six months. GILD is a Long-Term Buy under $115 for a first target of $150.

Meta Platforms (META – $542.87) and EssilorLuxottica introduced Meta Glasses, which build on the technology and features of their current best-selling AI glasses. They have 26 styles across a range of colors, lenses, and frames, and are compatible with prescription lenses. They launch with Meta AI powered by Muse Spark, and start at just $299.

The glasses include a dedicated action button to quickly invoke Meta AI. They have open-ear speakers to deliver pristine audio quality without blocking your ears, so you can listen to phone calls, music, podcasts, and audiobooks while staying present and aware of your surroundings.

An advanced multi-mic array with advanced wind noise reduction means calls, messaging, and voice control are always crisp and sharp. You can take photos and videos hands-free to stay present in the moment. The glasses have over 8 hours of battery life. Pedestrian navigation is coming soon with turn-by-turn directions. Meta sells them through Best Buy, Amazon, Lenscrafters, Sunglasses Hut, and Meta.com.

Meta’s Advantage+ and upcoming Spark and GEM models are delivering superior Return On Ad Spend (ROAS) to advertisers, fueling 24%+ ad revenue growth and projected market share leadership over Google.

Despite a $1.5 trillion market cap, META trades at 17x 2026 estimated earnings and 15.6x 2027 earnings, supported by double-digit growth, robust operating leverage, and improving margins. META is the undeservedly cheapest Mag 7 stock with compelling risk/reward and a Buy under $705 for a long-term hold.

Nvidia (NVDA – $195.74) continues to widen and deepen its moat by adding more and more complex software that runs on its GPUs. They introduced the BioNeMo Agent Toolkit that includes more than a decade’s worth of NVIDIA life sciences libraries, tools, and open models.

The toolkit enables AI agents, scientists, and labs to work together by gathering evidence, reasoning across findings, running computational experiments, and recommending the next best steps to accelerate discovery. It gives any agent or AI platform — from general-purpose assistants to specialized scientific agents, software platforms and in-house biopharma systems — the tools needed to synthesize and summarize scientific knowledge, call models, evaluate results, reason, and execute next actions.

They made it almost impossible to raise capital for or run a life sciences company without it. More than 50 companies are already using it to advance scientific discovery, tapping into agent-callable skills for tasks including protein structure prediction, molecular docking, generative chemistry, genomic analysis, protein design, and biomarker discovery.

A record 35 Nvidia AI HPC supercomputers are in development across Europe, that continent’s largest one-year expansion of supercomputers, spanning national supercomputing centers, AI factories, and academic research institutions. CEO Jensen Huang said: “AI is the new instrument of science, and Europe is building the infrastructure to put it in the hands of millions of researchers. With Nvidia accelerated computing, researchers can simulate more complex systems, train scientific AI models, and build agentic AI workflows that turn Europe’s data and expertise into breakthroughs for the world.”

At yesterday’s annual meeting

(SLIDES HERE), Jensen said the AI debate is over. Useful AI has arrived, and it is profitable. Agents are doing real work. Physical AI – cars, robots, surgical – is the next frontier.

Click for larger graphic

Click for larger graphic

NVDA is a Buy for a $225 first target.

Onsemi (ON – $118.74) revenue growth is recovering, led by AI data center momentum and stabilization in their automotive and industrial segments. Profit margin expansion will be driven by utilization gains, with their gross margin projected to reach 54.4% by 2030. The company has scheduled an Investor Day for September 16 because the story will be clear by then.

Citi raised its target price from $100 to $120 but maintained its Neutral rating, although they said they see renewed momentum in its SiC {Silicon Carbide) business driven by the 800V DC transition led by Nvidia’s Vera Rubin Ultra GPU. They noted the recent price hikes and expect a stronger analog recovery, underpinned by ~30% compound annual growth rate (CAGR) from data center demand for analog and power semiconductors.

They also expect more than 70% CAGR for the power delivery market (800V-to-1V conversion) from about $2 billion in 2026 to around $12 billion by 2028, driven by rising power requirements for next-generation GPU chips and a shift toward more integrated designs, including increased use of Gallium Nitride, or GaN, and SiC – both areas on Onsemi’s strength. ON was a Buy under $60 for a $130 first target.

Palantir (PLTR – $107.27) said the US Army has established the Next Generation Command and Control (NGC2) common data layer baseline. The foundational data architecture for NGC2, its highest-priority modernization program, is built on Palantir’s Foundry as the cloud data layer and Anduril’s Lattice as the tactical data layer.

PLTR’s moat lies in its Ontology and AIP, enabling auditable, deterministic enterprise AI integration and commoditizing frontier models beneath its platform. The stock’s recent pullback is driven by valuation compression, not business weakness. They continues to post robust earnings and revenue momentum, and thanks in part to major defense programs, such as Golden Dome, and strategic partnerships with Oracle, Google, and Nvidia, I expect that to continue for years. 11 consecutive quarters of accelerating growth are hard to ignore.

Although their forward P/E ratio is over 97x, their Price/Earnings to Growth (PEG) ratio of 1.37x due to their 71% revenue growth rate actually makes PLTR relatively undervalued. Wolfe Research wrote: “Today, we see PLTR as the most applied enterprise AI software company, with the largest and fastest growth rates in the industry. While it is not ‘Too Big To Fail,’ for our coverage it is simply ‘Too Big To Ignore!’ The frontier models today have the intelligence to solve virtually any problem but are missing the context (which they are trying to build). The magic of infusing business context into the model for the most mission-critical use cases IS the product that PLTR delivers today, built on either Foundry or Gotham, using AIP, and delivered through a forward deployed engineer (FDE). The secret sauce is the Ontology, a highly proprietary database that ingests all the key dependencies of workflows, harmonizing and refactoring them to enable users to change them. Revenue has grown +85% Y/Y (and accelerating), backlog +97% Y/Y, all on just 1,000 customers and ~4,000 employees. Couple that with a massive Total Available Market at ~$385 billion across >100,000 enterprise companies, supporting a FY26-29 revenue CAGR of 39% in our base case, and 55% in our upside model.”

PLTR is a Buy under $160 for a $200 first target.

Snap (SNAP – $4.34) CEO Evan Spiegel unveiled their new augmented reality Smart Glasses in a keynote address at the Augmented World Expo.

Evan said: “SPECS are the beginning of a new era in computing. For decades, computers have asked us to look down, sit still, or step out of the moment. SPECS bring computing into the world around us where we live, work, learn, create, and connect.”

He’s probably right, but at a pricey $2,195, more than three times the cost of Meta’s Ray-Ban smart glasses, I doubt they’ll sell. It’s early days for these products and getting people to try them probably requires low prices and no profits. There’s an activist investor trying to get management to shut down the SPECS operation, because the real value is in AI-assisted advertising to the Snapchat user base. SNAP is a Buy under $11 for a $17+ target.

SoftBank (SFTBY – $20.08) held their annual meeting (WEBCAST HERE). The only real excitement was at the telecom unit’s annual meeting, where CEO Masayoshi Son said that Elon Musk’s space data center idea is dumb. Masa thinks the only advantage of orbital data centers is cheaper electricity, but power is a small fraction of data center costs compared to hardware. So whatever you save on the electric bill, you hand straight back in launch costs, maintenance, and communication delays.

After a shareholder asked if SoftBank planned anything similar to Musk’s plans, Masa said: “In the battle for AI, the next few years will be far more important than what might happen a decade or so from now.”

While calling Musk a “remarkable agent of change,” Son said that SoftBank will focus on building “formidable” data center capacity on Earth and: “He who strikes first wins.”

I think he’s wrong and public data centers will become the shopping malls of the 2030s – mostly empty. Companies are not likely to turn over all their data and know-how to a third party that can cut them off at any time. I’ve always said that Masa is smarter than me, but I’m much closer to selling the stock than buying more. Hold SFTBY for a first target of $50 and then higher as the discount to hard book value disappears.

Small Tech

Fastly (FSLY – $16.22) partnered with Skyfire to integrate its identity and payment-backed credentials into Fastly’s programmable edge cloud platform so enterprises can now securely identify, verify, and transact with AI agents in real-time and at global scale, without re-architecting existing infrastructure.

As AI agents increasingly browse, negotiate, and complete transactions autonomously, businesses must distinguish trusted, revenue-generating agents from malicious automation, in real time for billions of transactions. The Fastly/Skyfire partnership transforms AI agent traffic from a potential security risk into an accountable, monetizable channel. They uses enhanced intelligence to verify the AI agents to automatically identify which agents to trust and which to block.

Although the company reported 20% year-over-year revenue growth in the March quarter and posted its fifth consecutive quarter of positive free cash flow, the stock trades at a discounted 3.6x forward Price/Sales ratio, well below competitors Cloudflare and Akamai. Their expanding AI offerings and positive free cash flow trajectory make FSLY a Strong Buy under $10 for a 3- to 5-year hold to $50+.

Primary Risk:Content and applications delivery networks are a competitive area.

QuickLogic (QUIK – $18.41) has been on fire after being recommended by George Gilder’s Moonshots. The stock will be added to the Russell 3000 and 2000 before the open on June 29, and some specialty Russell index funds will have to buy it. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

ARK Venture Fund (ARKVX – $54.91) has gone up with the SpaceX IPO, with OpenAI and Anthropic probably next. Then we exit.

Click for larger graphic

Click for larger graphic

ARKVX is a Buy for the OpenAI and Anthropic IPOs.

Primary Risk: Cathie sells the stocks before the IPOs.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like

AbCellera Biologics (ABCL- $6.66) and Jazz Pharmaceuticals signed a deal that could be worth up to $848 million to AbCellera to develop next-generation T-cell engaging multispecific antibodies. AbCellera gets $56 million upfront (nice!) and up to $792 million in milestone payments and potential option fees to use their antibody discovery engine to discover candidates for gastrointestinal cancers and other solid tumors.

AbCellera will conduct discovery and early-stage research for two programs and has a commitment to begin a third program within a year. Jazz has an exclusive, worldwide right to commercialize those programs.

AbCellera’s antibody platform is an integrated, AI-driven discovery engine that mines millions of immune cells rather than designing molecules from scratch, backed by a decade of proprietary wet lab. The company has more than $650 million in liquidity against a roughly $2.1 billion market cap. Investors get the cash, platform, pipeline, two drugs in the clinic, and over 100 royalty positions. ABCL635, targeting hot flashes, is advancing to a Phase 2 trial with a key data readout expected in the December quarter, potentially derisking the program. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Inflation MegaShift

Gold ($4,039.10) is not going to recover, according to the options market. Call positions that gold will rise have become the cheapest they’ve been in nine years, a sign that almost no one thinks gold will recover. In fact, traders are loading up on protection against a further decline in the price of gold. The moves follow the metal’s 25% collapse from February’s record high to under $4,100 an ounce.

Gold prices have been struggling, as market expectations around US monetary policy have shifted dramatically since the Iran war began. Interest rate expectations have switched from a cut before the start of the conflict to fully pricing in at least a 25-bps rate hike by spring 2027.

But the structural factors supporting gold remain entirely intact, including eroding confidence in the US dollar as a reserve currency, which is likely to lead to further gold purchases by central banks. The high and rapidly rising levels of government debt are leading to monetary policy that is too loose when measured against inflation.

Miners & Related

Coeur Mining (CDE – $15.99) gave the standard presentation at the J.P. Morgan Natural Resources Conference (SLIDES HERE). I don’t know what CEO Mitchell Krebs said because they continue to block us from the webcast, in violation of SEC Rule FD. The company said they expect over $3 billion in earnings before interest, taxes, depreciation and amortization (EBITDA) and $2 billion of free cash flow in 2026, contingent on strong metal prices. The recent New Gold acquisition boosts reserves and future production, with the strongest quarters ahead as new mines contribute fully.

Coeur now has a strong balance sheet with a net cash balance after peak net leverage of 4.1x in 2023, and an expanded credit facility. They’ve implemented a $750 million buyback program and are buying back stock near current trading levels. Management plans record exploration investment in 2026, focusing on high-potential assets and leveraging capital inflows from New Gold to reshape the company’s future. CDE is a Hold as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Dakota Gold‘s (DC – $4.08) Senior Manager – Geology: William Gehlen presented at the Planet MicroCap Conference (NEW SLIDES HERE).

The new slide deck includes an overview of declining US gold production:

Click for larger graphic

plus the connection to data centers and cell phones:

Click for larger graphic

Click for larger graphic

and a better summary slide:

Click for larger graphic

All leading to the inevitable conclusion that Dakota Gold is very undervalued:

Click for larger graphic

Click for larger graphic

DC is a Hold for a $6 target as gold goes higher.

Primary Risk: Robert Quartermain doesn’t find enough gold. Secondary risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $16.50) said Sierra Madre completed the purchase of the Del Toro Silver Mine for $20 million and 10.87 million shares of Sierra Madre. Within 18 months, First Majestic gets another $10 million.

The company is enjoying surging cash flow from higher silver prices. Upcoming gold production at Jerritt Canyon, reopening in the second half of 2026, is expected to add over 100,000 ounces of gold annually, diversifying the company’s revenue and reducing the silver price risk. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $1.11) announced positive results of an Initial Assessment prepared in accordance with S-K 1300 for its 100%-owned Sleeper Gold Project, their past-producing gold mine located in Humboldt County, Nevada. It showed an after-tax net present value (NPV) of $402 million at an 8% discount rate compared to the company’s total market value of $96 million, with an internal rate of return (IRR) of 45% at a gold price of $3,600 an ounce.

Just to throw some red meat to the wolves, they also said at $4,700 an ounce the after-tax NPV jumps to $867 million and the IRR to 66%. Over a 17-year mine life, the Assessment projects average annual gold production of approximately 65,000 ounces and total payable gold production of approximately 1.1 million ounces. PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: 2026

Royal Gold (RGLD – $204.62) did yet another Renmark Financial Communications Virtual Non-Deal Roadshow (WEBCAST HERE and SLIDES HERE and TRANSCRIPT HERE) in their much-appreciated effort to get the stock up to a fair valuation similar to Franco-Nevada and Wheaton Precious Metals.

The company derisked its portfolio by converting Hod Maden equity into a royalty, aligning with its core streaming model and reducing capital commitments. With a robust pipeline—79 producing properties and a strong balance sheet—they are positioned for sustained growth and further acquisitions. The stock is attractively valued, offering leveraged gold exposure without the risks of physical ownership. It’s selling for only 16x the 2027 earnings estimate—well below its peers—offering compelling value for a high-margin, dividend-growing royalty business leveraged to gold prices. RGLD is a Buy under $180.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly.

Bitcoin (BTC-USD on Yahoo – $59,520.07) is in the tank, trading down with both gold and oil, and probably for the same reason: a fear that the Fed will start increasing interest rates. The good news is that it has bottomed in the past about halfway through the four-year halving cycle, which is where we are right now.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $33.52) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Ethereum Trust (ETHA- $11.74) remains the cheapest and easiest way to buy ethereum. ETHA is a Buy for the coming explosion in token-funded start-ups.

Primary Risk: Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $71.46

Oil fell sharply. The International Energy Agency is up to its old tricks, crying their version of “Wolf! Wolf!”:

IEA Sounds The Alarm: Oil Market Headed For Massive Glut By 2027 As Gulf Supply Returns After US-Iran Deal

“The agency said global oil supply could rise sharply in the coming years as Gulf producers gradually restart shuttered oilfields following the Iran-related conflict resolution. The forecast suggests production could climb by around 8 million barrels per day, reaching roughly 110 million barrels per day by 2027, while demand growth is expected to lag at a much slower pace. This imbalance could create a “significant overhang” in global markets, potentially easing tight inventories and rebuilding strategic reserves, the IEA noted in its latest Oil Market Report.”

Emphasis added. On the other hand, demand to rebuild Strategic Petroleum Reserves, the inevitable return of China to the buying table, and the very possible delay in normalizing flows through the Strait of Hormuz might – just might – mean prices just ahead are going up, not down. The Cushing terminal is at its operational low right now, today. Hypothetical future oil flows don’t create barrels to refine today. The IEA is still projecting a 1.8 million barrel-per-day shortfall through 2026, with inventories drawing at a record pace. Calling this oversupplied because futures dropped is like calling a drought over because someone called the weather service. Tanks don’t refill on announcements.

We have record low inventories that will continue to fall further (regional tank bottoms + US SPR at/near operational minimum levels). And about 0.45 million barrels a day of new demand for the next three years to restock depleted inventory, plus the likelihood that some countries will increases their SPR targets. 80% of most Mideast production will come online within one to four months, but OPEC has said “the last 20% is the hardest” – that’s over two million barrels a day. A Strait of Hormuz under IRGC control will never return to pre-war levels, and partial workarounds will take years.

The Cushing stocks are down to 21.64 million barrels, dropping by ~800,000 barrels a week. The absolute operational bottom is 20 million. Below that, pipeline pressure fails and tank roofs literally collapse. Mathematically, the hub hits technical failure in less than two weeks. US midstream companies are already panic-shifting pipeline flows from Texas export docks north to save Cushing, but it’s a zero-sum game. You don’t create new oil by changing its GPS destination. Fixing Oklahoma just means starving the Gulf Coast. The entire system has zero margin for error.

Even if the diplomatic talks go perfectly, you can’t teleport oil. Reopening Hormuz means mine-sweeping and re-insuring stranded tankers. More important, transit time around Africa to Europe and the US takes 35 to 40+ days. Global refiners cannot stop buying US exports yet; they have a five-week physical gap to survive. The drain on US tanks isn’t stopping.

Bears have piled into USO shorts thinking the geopolitical risk premium just evaporated. But when the next EIA data drops and shows Cushing is still a ghost town because physical ocean transit takes a month, those paper shorts are trapped. I think the drop to $70 isn’t a structural reversal—it’s a massive bear trap. Physical logistics can’t move as fast as a news ticker. Expect a violent, forced short squeeze pushing paper WTI back toward $105–$115 over the next 10 days as paper liabilities collide with an empty physical bucket.

Click for larger graphic h/t @BisonInsights

The September 2027 Crude Oil Futures (CLU7.NYM – no trades – August closed at $67.71) are a Buy under $75 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $46.18) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $9.42) is a Buy under $11 for a target price of $24 or more.

Primary Risk: Oil and natural gas prices fall.

Energy Fuels (UUUU – $14.42) said it expects to achieve its 2026 uranium production target from its fully-owned White Mesa Mill in Utah by mid-year, putting the company in position to exceed its guidance. It expects to reach output of ~1.6 million pounds of uranium by the end of June, which falls within its previously stated guidance range of 1.5-2.5 million pounds for the year, from the processing of ores mined at the company’s Pinyon Plain mine in Arizona and La Sal Complex in Utah.

After completing the current uranium ore processing campaign at White Mesa by the end of June to rebuild ore stockpiles, they will resume ore processing in the December fourth quarter, subject to continued strong ore production at the conventional mines, uranium market conditions, and the potential for a rare earth element processing campaign.

They also said permitting for the planned Phase 1 modifications and Phase 2 rare earth expansion in Utah is proceeding on schedule, with Phase 1 expected to become operational in late 2027 to early 2028.

The Trump Administration signed a $725 million conditional loan to Energy Fuels. In April, the US government launched a program called “Nuclear Dominance — 3 by 33.” The initiative, overseen by the Department of Energy, is designed to rebuild and secure the domestic nuclear fuel supply chain in the US by 2033 The program targets the full fuel cycle, including mining, milling, conversion, enrichment, and recycling. The goal is to align workforce development, financing, innovation, and industry collaboration toward a broad nuclear buildout. Policy support has framed nuclear fuel as both a national security priority and a critical minerals supply chain issue.

Energy Fuels is acquiring Vacuumschmelze GmbH & Co. KG, a German advanced magnetics company with over 100 years of production expertise, more than 400 patents, over 1,000 customers, and operating magnet production facilities in North America, Europe and Asia, including a state-of-the-art facility in Sumter, South Carolina, with capacity to produce 2,000 tonnes per annum (tpa) of permanent magnets, scalable to 12,000 tpa. They did a (WEBCAST HERE with SLIDES HERE and TRANSCRIPT HERE).

Click for larger graphic

Click for larger graphic

Over the last decade, VAC has produced and shipped more than one billion rare earth permanent magnets. Approximately 85% of VAC’s output is produced to customer specifications, reflecting deep design-in relationships built over decades, including customer partnerships averaging over 30 years with their largest accounts.

Energy Fuels is paying $1.9 billion ($718 million in cash and 65.853 million shares of stock), and expects the deal to be immediately accretive to their cash flow and profit margins. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

65 or Older? Watch This.

* * * * *

RIP Walter Parazaider of Chicago

Flute Solo Below

Your THINKING THE OCEANS ARE NEXT Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 6/25/26. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $275.15) – Buy under $205

Gilead Sciences (GILD – $126.84) – Buy under $115, first target price $150

Meta (META – $542.87) – Buy under $705 for a long-term hold

Nvidia (NVDA – $195.74) – Buy under $225 for a long-term hold

Onsemi (ON – $118.74) – Buy under $60, first target price $130

Palantir (PLTR – $107.27) – Buy under $160 for $200 first target price

PayPal (PYPL – $42.38) – Buy under $50, target price $150

Snap (SNAP – $4.34) – Buy under $11, target price $17+

Small Tech

Enovix (ENVX – $6.05) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $83.66) – Buy under $75; 3- to 5-year hold

Fastly (FSLY – $16.22) – Buy under $10 for a 3- to 5-year hold to $50+

PagerDuty (PD – $8.56) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $18.41) – Buy under $10, target price $40

ARK Venture Fund (ARKVX – $54.91) – Buy for SpaceX IPO

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $6.66) – Buy under $6, target $30+

Akebia Therapeutics (AKBA – $1.04) – Buy under $4, target $20

Compass Pathways (CMPS – $13.58) – Buy under $10, hold a long time for a 20x return

Editas Medicines (EDIT – $2.74) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $1.08) – Buy under $5, hold a long time

Medicenna (MDNAF – $0.28) – Buy under $3, first target $20, then maybe $40

TG Therapeutics (TGTX – $53.63) – Buy under $30 for buyout at $40+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($57.59) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $62.52) – Buy under $50, target price $75

Sprott Junior Gold Miners ETF (SGDJ – $75.62) – Buy under $60, target price $100

Sprott Physical Gold and Silver Trust (CEF – $39.80) – Buy under $35, target price $60

Global X Silver Miners ETF (SIL – $77.09) – Buy under $60, target price $100

Coeur Mining (CDE – $15.99) – Buy under $10, target price $20

Paramount Gold Nevada (PZG – $1.11) – Buy under $1, first target price $10

Royal Gold (RGLD – $204.62) – Buy under $180

Cryptocurrencies

Bitcoin (BTC-USD – $59,520.07) – Buy

iShares Bitcoin Trust (IBIT – $33.52) – Buy

Ethereum (ETH-USD – $1,565.49)– Buy

iShares Ethereum Trust (ETHA- $11.74) – Buy

Commodities

Crude Oil Futures – September 2027 (CLU7.NYM – no trades – August closed at $67.71) – Buy under $75; $200+ target

United States 12 Month Oil Fund, LP (USL – $46.18) – Buy under $40; $100+ target

Vermilion Energy (VET – $9.42) – Buy under $11; $24+ target

Energy Fuels (UUUU – $14.42) – Buy under $18; $30 target

EQT (EQT – $51.65) – Buy under $70; hold for much higher prices ($100+)

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

SoftBank (SFTBY – $20.08) – Hold

ScyNexis (SCYX – $3.81) – Hold through reverse split

Dakota Gold (DC – $4.08) – Hold for higher gold prices

First Majestic Mining (AG – $16.50) – Hold for higher silver prices

Freeport McMoRan (FCX – $62.80) – Hold for higher copper prices

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2026

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Thanks very much for the William Li link.

Paramount Gold Nevada’s ($PZG) Sleeper Gold Project Demonstrates Strong Economics

PZG provided another update – glad to see they are making the effort to get the word out after years of radio silence. You may want to fast forward to the 19th minute where CEO Rachel Goldman discusses the future path: “capital is a consideration” , open to all opportunities…

The takeaway for me is they will sell the company – they only have a handful of employees so they either get bought out or partner with an actual mining company.

The longevity video on 6 habits for longer life was great…thanks