Dear New World Investor:

Welcome to August! The Fed held the Fed funds rate steady in a range of 5.25%-5.50% and all but announced they will cut in September. They will, too. As leakee-in-chief @NickTimiraos pointed out:

* * Policy looks more restrictive now than it did earlier this year.

* * The recent inflation news is better than last year’s swift decline because it is more broadly based.

* * No tolerance for much labor market softening: “I would not like to see material further cooling in the labor market.”

* * A July cut was debated, but there was broad support for waiting until September.

September is the last Fed meeting before the Presidential election, so assuming Powell doesn’t go off the rails at the August 22-24 Jackson Hole meeting, it won’t be until November 7 and December 18 that we have to wait with bated breath to see what the wise overlords will do.

We are within seven weeks of the first Fed interest rate cut this cycle, but it’s too late to avoid a recession. Why? Because the Fed is always late. Last Friday’s University of Michigan survey showed the median income expectations for the middle of the income distribution. That’s about as typical as you can get. In each of the following graphics, the blue line is the middle-income median income expectations.

Middle income people are being squeezed by high interest rates:

Click for larger graphic h/t @DiMartinoBooth

Click for larger graphic h/t @DiMartinoBooth

And worried about increasing layoffs:

Click for larger graphic h/t @DiMartinoBooth

Click for larger graphic h/t @DiMartinoBooth

So they are cutting back on services spending that now accounts for 70% of the economy:

Click for larger graphic h/t @DiMartinoBooth

Click for larger graphic h/t @DiMartinoBooth

And not buying big stuff like houses (and, increasingly, $70,000 pickup trucks):

Click for larger graphic h/t @DiMartinoBooth

Click for larger graphic h/t @DiMartinoBooth

The US national debt now exceeds $35 trillion for the first time in history. These days, politicians of both parties spend like drunken sailors to boost the economy so they can get re-elected. This may be the first time in history that older generations enjoy life by callously burdening younger people with so much debt. Disgusting.

Click for larger graphic h/t usdebtclock.org

Click for larger graphic h/t usdebtclock.org

Treasury Secretary Yellen estimates $1.3 trillion in borrowing needs for the remainder of 2024. Nothing stops this train.

Market Outlook

The S&P 500 added 0.9% since last Thursday even though the Fed euphoria vanished like water on sand. The Index is still up 14.2% year-to-date. The Nasdaq Composite eked out a 0.1% gain and is up 17.0% for the year.

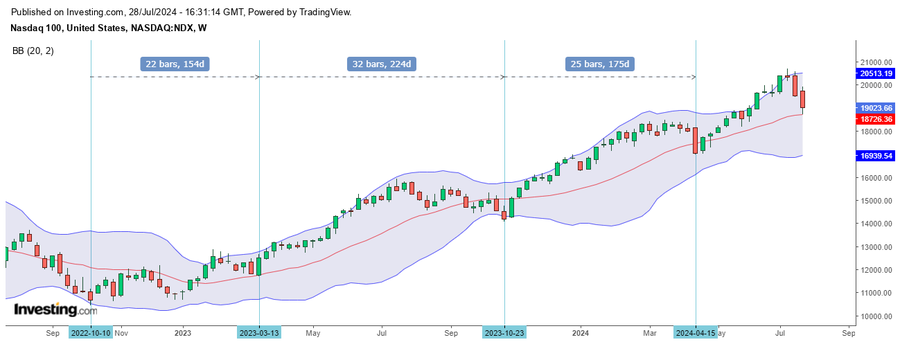

How long will the Big Tech correction last? The July top in the Nasdaq 100 (NDX) probably was an intermediate-term top that will lead to a 12% to 15% correction. The low is likely to occur in late September to late October. Last week’s low at the 20-week moving average probably was the end of the first down leg, the equivalent of the August 2023 low. I expect to move Apple and Meta Platforms back to Buys in four or five weeks, possibly before the iPhone 16 introduction and after we are through the bulk of the decline.

Click for larger graphic h/t @CyclesFan

Click for larger graphic h/t @CyclesFan

The concentration risk of the Mag 7 compared to the overall S&P 500 index, which worried many before this selloff began, has already been lessened considerably. I think there is more to go through a combination of the Mag 7 coming down some more and the S&P 493 going up.

Click for larger graphic h/t @jimwpaulsen

Click for larger graphic h/t @jimwpaulsen

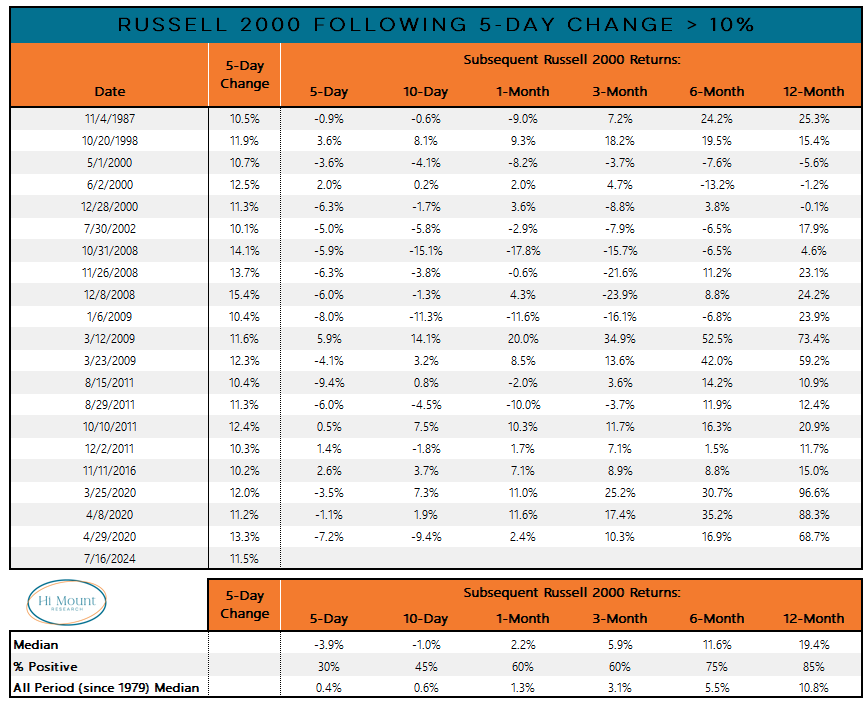

The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 2.3% even though biotech stock valuations are supposed to be a major beneficiary of lower interest rates. It is up 10.9% year-to-date. The small-cap Russell 2000 reversed and dropped 1.7%. It is up 7.8% in 2024. After a five-day gain of 10% or more, the Russell often flattens or retreats for a few weeks and then takes off.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

The fractal dimension looks like it wants to consolidate, Fed or no Fed. A red candle in a week the Fed signals a coming cut is unusual, to say the least.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

CMPS – Compass Pathways – Phase 3 data release and rebound from negative AdCom review of MDMA

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements at June WWDC and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

AKBA Akebia Therapeutics – Vafseo TDAPA approval in January

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model estimate for September quarter real GDP growth ticked down a bit to +2.5%, but it’s early days.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, August 2

July payrolls – 8:30am – +175,000 expected; June was +206,000 before revisions

SAND – Sandstorm – 11:00am – Earnings conference call

Monday, August 5

UUUU – Energy Focus – 12:00pm – Earnings conference call

PLTR – Palantir – 5:00pm – Earnings conference call

Tuesday, August 6

AKBA – Akebia – 8:00am – BTIG Biotechnology Conference

ABCL – AbCellera – 5:00pm – Earnings conference call

Wednesday, August 7

SFTBY – SoftBank – 3:30am – Earnings conference call

EDIT – Editas – 8:00am – Earnings conference call

CDE – Coeur Mining – After the close – Earnings release; call tomorrow

FSLY – Fastly – 4:30pm – Earnings conference call

Thursday, August 8

ENVX – Enovix – Grand Opening of Fab2 in Malaysia

CDE – Coeur Mining – 11:00am – Earnings conference call

GILD – Gilead Sciences – 4:30pm – Earnings conference call

INO – Inovio – 4:30pm – Earnings conference call

RKLB – Rocket Lab – 5:00pm – Earnings conference call

Friday, August 9

Short Interest – After the close

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

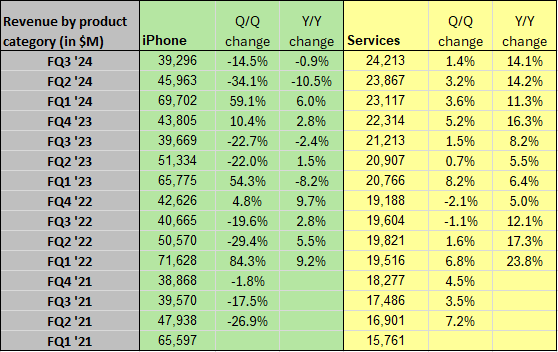

Apple (AAPL – $218.36) reported record June quarter revenues and earnings after the close today. Revenues rose 4.9% from last year to $85.78 billion, above the $84.38 billion consensus estimate. They reported $1.40 earnings per share, above the $1.34 consensus. iPhone sales of $39.296 billion were almost flat with last year’s $38.669 billion. Mac sales showed a good uptick from $6.840 billion last year to $7.009 billion. iPad also grew from $5.791 billion to $7.162 billion. Wearables, Home, and Accessories were about flat at $8.097 billion versus $8.284 billion last year. The all-important Services sector grew 14.1% from $21.213 billion to a record $24.213 billion.

Click for larger graphic h/t Seeking Alpha

Click for larger graphic h/t Seeking Alpha

On the conference call (AUDIO HERE and TRANSCRIPT HERE), CEO Tim Cook said: “During the quarter, we were excited to announce incredible updates to our software platforms at our Worldwide Developers Conference, including Apple Intelligence, a breakthrough personal intelligence system that puts powerful, private generative AI models at the core of iPhone, iPad, and Mac. [emphasis added] We very much look forward to sharing these tools with our users, and we continue to invest significantly in the innovations that will enrich our customers’ lives while leading with the values that drive our work.”

Apparently, they will not include Apple Intelligence in the September iOS 18 and iPadOS 18 update that will accompany the iPhone 16 introduction. According to Bloomberg, the new AI features will be rolled out to customers as part of software updates coming by October. That probably means that engineers need more time to fix bugs.

TD Cowen said optimism around Apple Intelligence should help the company report iPhone revenue growth in the December quarter, so they raised their sell-in forecast to 240 million iPhones for the January 2025 fiscal year. They reiterated their Buy rating and raised their target price from $220 to $250.

Baird also kept their Outperform rating on the stock and raised their target from $200 to $240, citing the opportunity to boost iPhone sales due to Apple Intelligence. They wrote: “We estimate that close to 95% of iPhones globally, even with the initial focus on the US, will need to upgrade at some point to take advantage of Apple Intelligence. With smartphone upgrade cycles lengthening for years, resulting in a much older iPhone base, the 1+ billion iPhones globally could be primed for an upgrade catalyst. Of course, other Apple devices like Macs and iPads, should also benefit.”

They noted that upgrade rates at AT&T and Verizon have been low, suggesting consumers may be waiting for AI to come to smartphones. So they raised their fiscal 2025 iPhone estimates by 20 million units and now expect iPhone revenue to be $216.1 billion, up 9% year-over-year and above the consensus estimate of 6% growth. For the full year, they now expect Apple to report $418.1 billion in revenue and earn $7.30 per share, up from their previous estimates of $394.6 billion and $6.73. AAPL is a HOLD – I expect to move back to Buy under $175 for new iPhones.

Corning (GLW – $40.04) reported June quarter revenues up 3.4% from last year to $3.6 billion, a return to year-over-year sales growth and meeting the $3.58 billion consensus estimate. Pro forma earnings per share of 47¢ also matched the consensus. Remember that on July 8, Corning said that their above-guidance performance in the quarter was driven by the “strong adoption of our new optical connectivity products for Generative AI.”

Click for larger graphic

Click for larger graphic

But on the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Wendell Weeks guided September quarter results to $3.7 billion in core sales and 50¢ to 54¢ earnings per share. Wall Street was at $3.78 billion and 55¢, so they took the stock to the woodshed on Tuesday, knocking it down 6.9%.

Corning and Lumen Technologies reach an agreement to reserve 10% of Corning’s global fiber capacity for each of the next two years to interconnect AI-enabled data centers.

Click for larger graphic

Click for larger graphic

They repeated that the March quarter was the low for this year and provided a forecast through 2028. This is very unusual behavior for this normally conservative company. If you think they can do it, as I do, it’s a perfect retirement portfolio stock with a great entry point and a 2.8% yield while you wait.

Click for larger graphic

Click for larger graphic

Deutsche Bank upgraded the stock from Hold to Buy with a $46 12-month target. They wrote: “Our estimates call for accelerating growth in 2H24, with Corning’s Optical segment growing at a 13% CAGR between 2024E-2027E. The drivers here are twofold, and include generative AI, with very strong uptake of Corning’s newer optical connectivity products for GenAI. A ramp in carrier activity (fiber deployments), following a prolonged ‘digestion’ phase, dampened by elevated inventory levels in recent periods.”

GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025.

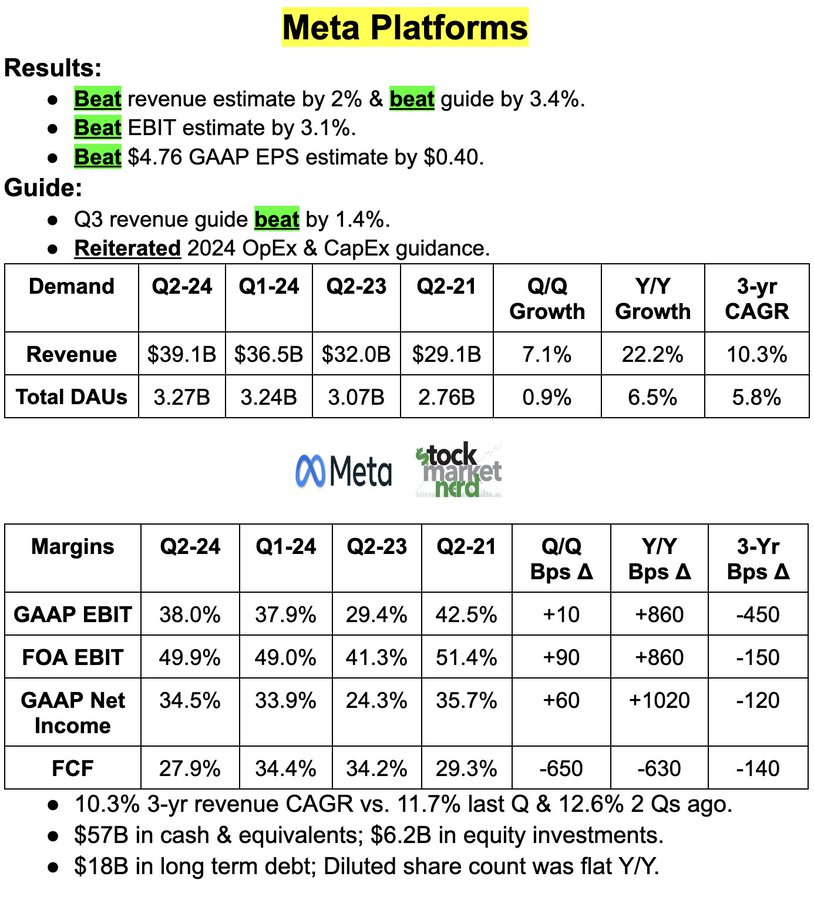

Meta Platforms (META – $497.74) reported after the close yesterday. Revenues rose 22.1% from last year to $39.07 billion, well above the $38.34 billion consensus estimate. They reported $5.16 pro forma earnings per share, clobbering the $4.72 billion consensus. It was a double beat and a strong quarter: Family daily active people increased 7% from last year to 3.27 billion. They said growth in the US has especially been a bright spot. WhatsApp now serves more than 100 million monthly actives in the US. Ad impressions increased by 10% and average price per ad also increased by 10%, both year-over-year.

Click for larger graphic h/t @StockMarketNerd

Click for larger graphic h/t @StockMarketNerd

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Mark Zuckerberg said: “I’m particularly pleased with the progress that we’re making with young adults on Facebook. The numbers we are seeing, especially in the US, really go against the public narrative around who’s using the app. A couple of years ago, we started focusing our apps more on 18 to 29 year olds and it’s good to see that those efforts are driving good results. Another bright spot is Threads, which is about to hit 200 million monthly actives. We’re making steady progress towards building what looks like it’s going to be another major social app.”

Zuck spent a lot of the conference call talking about AI, and I strongly recommend you listen to it or read the transcript. He focused on what AI means for their family of apps and core business, what new AI experiences and opportunities they see, and how AI is shaping their metaverse work. They are way ahead of other companies. For example, Mark said: “It used to be that advertisers came to us with a specific audience they wanted to reach, like a certain age group, geography, or interests. Eventually, we got to the point where our ad systems could better predict who would be interested than the advertisers could themselves.

“But today, advertisers still need to develop creative themselves. And in the coming years, AI will be able to generate creative for advertisers as well. And we’ll also be able to personalize it as people see it. Over the long term, advertisers will basically just be able to tell us a business objective and a budget, and we’re going to go do the rest for them.”

Then he added: “Business AIs are the other big piece here. We’re still in Alpha testing with more and more businesses. The feedback we’re getting is positive so far. Over time, I think that just like every business has a website, a social media presence, and an email address, in the future I think that every business is also going to have an AI agent that their customers can interact with. And our goal is to make it easy for every small business, eventually every business, to pull all of their content and catalog into an AI agent that drives sales and saves them money.”

They guided the September quarter revenue to $38.5 billion to $41.0 billion, with the midpoint of $39.75 billion fractionally above the $39.16 billion consensus estimate. The stock moved up 4.8% today. I get it, but META still is a Hold – I expect to move back to Buy under $400.

Nvidia CEO Jensen Huang and Meta CEO Mark Zuckerberg did a joint keynote at the big SIGGRAPH conference:

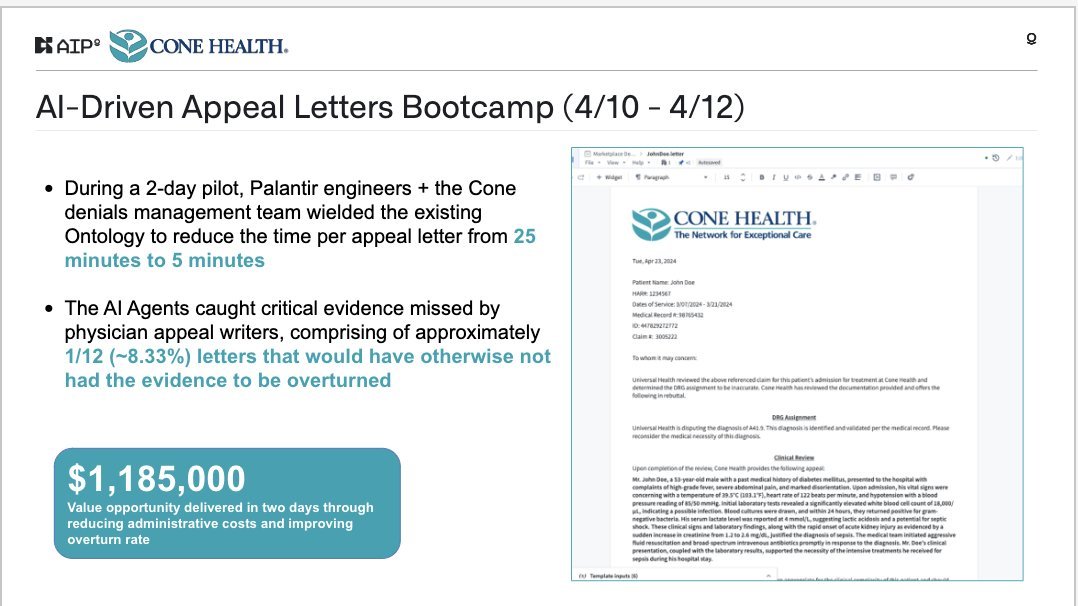

Palantir (PLTR – $26.08) reports June quarter results next Thursday. Wall Street expects $652.1 million in revenues and 8¢ earnings per share. September quarter guidance should be for $679.12 million and another 8¢.

Their AI software now is used by almost 20% of US hospitals, for many reasons. The Cleveland Clinic saw a 39% increase in daily hospital transfer volume. Nebraska Medicine increased patients sent to discharge from 15 per month to 14 per day. Lifepoint Health reduced the delays of treatment starts from 90 minutes to 5 minutes. HCA Healthcare reduced the time spent on manual processes by 80%. These are significant improvements that provide better care, reduce costs, or both.

Click for larger graphic h/t @arny_trezzi

Click for larger graphic h/t @arny_trezzi

Mount Sinai generated $1.5mn in annualized savings.

Click for larger graphic h/t @arny_trezzi

Click for larger graphic h/t @arny_trezzi

A two-day pilot of Palantir’s AIP at Cone Health identified a $1.185 million value opportunity.

Click for larger graphic h/t @arny_trezzi

Click for larger graphic h/t @arny_trezzi

Jefferies raised their target price to $28, less than $2 above where it closed today. They called it “Overhyped On AI” back in January and it’s up 64% since then. They wrote: “Palantir stock is priced for perfection but can continue to trade on AI enthusiasm…PLTR has had back-to-back quarters of solid execution, and we view the company as a rare blended AI apps/infrastructure asset with next-12-months revenue momentum.” But, of course, no Buy recommendation. PLTR is a Buy under $22 for a $100+ target.

PayPal Holdings (PYPL – $65.31) reported an excellent quarter, with revenue, earnings, and transaction gross profit all above the consensus estimates. Revenues rose 8.2% from last year to $7.9 billion, above the $7.82 billion consensus. They reported pro forma earnings per share of $1.19, well above the 99¢ estimate.

Click for larger graphic h/t @StockMarketNerd

Click for larger graphic h/t @StockMarketNerd

Payment transactions increased 8% from last year to 6.6 billion while total payment volume increased 11% to $416.8 billion. Transaction margin dollars – a key metric for PayPal to track to know how durable their profit compounding can be beyond cost cuts – increased a solid 8% to $3.6 billion.

Click for larger graphic h/t @StockMarketNerd

Click for larger graphic h/t @StockMarketNerd

As expected, active accounts decreased 0.4% from last year to 429 million, but as not expected, they increased 1.4% or 1.8 million from the March period. The turnaround is underway.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), management guided the September quarter to mid-single-digit growth in revenues and earnings, and raised their full-year guidance to earnings growth in the low- to mid-teens. They now expect EPS of $3.88-$3.98 compared to previous guidance of $3.83. CEO Alex Chriss said: “We delivered our best transaction margin dollar growth since 2021, and we are making steady progress on our strategic transformation while investing in innovation and operating more efficiently. Given the strength of our business, we are raising our 2024 guidance and increasing share repurchases.” They now expect to buy back $6 billion of stock in 2024, up from their prior guidance of at least $5 billion.

Argus upgraded the stock from Hold to Buy, saying efforts to reignite growth are proceeding faster than originally expected: “We view the company as making steady progress on its turnaround plan, which includes a new CEO and CFO, improved on-line checkout experiences, and revived growth from Venmo. In our view, the company has several competitive advantages as it seeks to grow payment volumes. These include a strong international presence, with 100M non-U.S. users in more than 200 countries.”

The stock is still below my buy limit. PYPL is a Buy under $68 for a double in three years.

Small Tech

Enovix (ENVX – $11.65) reported after the close today. Revenues of $3.8 million were just above the $3.65 million consensus estimate. They reported a loss of 14¢ per share, much less than the 23¢ loss expected.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE and LETTER TO SHAREHOLDERS HERE), CEO Raj Talluri said they expect significant revenue growth in the second half of the year from the first half. He guided for September quarter revenue between $3.5 million and $4.5 million with a pro-forma loss of 17¢ to 23¢. The Street was at $3.1 million and a 20¢ loss, so they knocked the stock down 19% today.

Enovix began production of the first batteries in Malaysia on the Agility Line, which recently completed site acceptance testing. They also completed factory acceptance testing for the high-volume Gen2 Autoline for all key modules. Raj said they are on track to over $35 million in annualized savings based on relocating high-cost California manufacturing to Malaysia.

Raj said that the 4,000 milliampere-hour (mAh – a measure of the capacity of a battery) to 5,000 mAh battery in smartphones today will soon go to more than 6,000 mAh and beyond due to AI and other enhanced features. Six of the top eight smartphone manufacturers are getting samples of the EX-1M battery:

Click for larger graphic

Click for larger graphic

The company announced a collaboration agreement with a Fortune 200 company to provide silicon batteries for a fast-growing Internet-of-Things (IoT) product category that already has tens of millions of users globally. Enovix will receive milestone payments for building and testing prototype batteries for this IoT device along a path toward mass production.

They also announced their second Memorandum of Understanding with a high-performance, global automotive OEM aimed at scaling the Enovix cell architecture for the EV market. The agreement is focused on cell design, performance validation, and optimization at the cell, pack, and vehicle levels. Enovix’s technology enables an order of magnitude improvement in cell thermal distribution, leading to faster charging, improved lifetime, and simplified pack assemblies, due to a smaller cooling system required.

Click for larger graphic

Click for larger graphic

42 million shares of the 140 million float are still sold short, in spite of the company’s progress. I’m not sure what they’re waiting for to cover, but that’s their problem. Maybe they’ll take advantage of today’s drop to cover before the grand opening of Fab2 in Malaysia next Thursday. ENVX has bounced off the $12 area, so this should be an excellent buying opportunity.

They ended the quarter with $249.9 million in cash. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $7.68) reports June quarter results next Wednesday. Wall Street expects $121.5 million in revenues and an 8¢ loss per share. September quarter guidance should be for $140.06 million and a 2¢ loss. FSLY is a Buy up to $14 for a 3- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $20.01) expanded their generative AI offering with PagerDuty Advance, which is embedded across the whole PagerDuty Operations Cloud platform, including Incident Management, AIOps, Automation, and Customer Service Operations customers. PagerDuty Advance empowers responder teams to work faster and smarter by using generative AI to surface relevant context or automate at every step of the incident lifecycle. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $10.12) signed a distribution agreement with Astute Electronics. Astute specializes in international electronic component procurement, distribution, and supply chain management. They will support QuickLogic customers across Europe and in Australia, Israel, Turkey, and New Zealand. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $4.96) reports June quarter results next Thursday. Wall Street expects $105.46 million in revenues and a 10¢ per share loss. September quarter guidance should be for $108.41 million and another 10¢ loss.

They have completed the integration and testing of two spacecraft destined for Mars orbit. Rocket Lab built the twin spacecraft for the University of California Berkeley’s Space Science Laboratory and NASA to enable the Escape and Plasma Acceleration and Dynamics Explorers (ESCAPADE) mission, scheduled to launch from Cape Canaveral this year. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $2.36) registered 1.65 million shares issuable on the exercise of warrants. This is not an offering by the company. VLD is a Buy up to $10 for my $100 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $3.05) reports June quarter results next Tuesday. Wall Street expects $10.15 million in revenues and a 14¢ loss per share. September quarter guidance should be for $10.89 million and another 14¢ loss.Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Compass Pathways (CMPS – $6.88) reported after the close today. The net loss was $38.1 million or 56¢ per share. On the conference call (AUDIO HERE), CEO Kabir Nath said the top-line COMP005 trial data for the first of their two Phase 3 pivotal program in treatment-resistant depression is expected in the December quarter, with the second trial data still on schedule for mid-2025. These are the largest randomized, controlled, double-blind psilocybin treatment clinical program ever conducted.

They expect to use $32 million to $38 million in cash in the September quarter and $110 million to $130 million for the full year 2024.

Nicholas Fabiano, MD did an excellent Twitter thread on how psilocybin leads to a profound shift in brain connectivity patterns.

Click for larger graphic h/t @NTFabiano

Click for larger graphic h/t @NTFabiano

Compass finished the quarter with $228.6 million in cash, enough to carry them past the top-line results into 2026, and $29.4 million in long-term debt. They’ll have to raise more capital to get through FDA approval and the launch. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2026

Probable time of next financing: Late 2025

Editas Medicine (EDIT – $5.14) reports June quarter results next Wednesday. The consensus is looking for $5.08 million in revenues and a 70¢ loss per share. September quarter guidance should be for $5.47 million and a 69¢ loss. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2025

Probable time of next financing: 2026 or never

Inovio (INO – $10.02) reports June quarter results next Thursday. Analysts expect a $1.10 loss per share with September quarter guidance for a $1.08 loss.

The company said that the European Medicines Agency’s Committee for Advanced Therapies (CAT) has certified the quality and non-clinical data for INO-3107, Inovio’s lead candidate for the treatment of Recurrent Respiratory Papillomatosis (RRP). The certification confirms that the company’s chemistry, manufacturing, and controls (CMC) data and nonclinical results available to date comply with the scientific and technical standards that would be used for evaluating a European Marketing Authorization Application. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2025

Probable time of next financing: After FDA approval in 2025

Medicenna (MDNAF – $1.65) jumped 6.5% today after they announced the first melanoma complete responder (=“cured”) with MDNA11 monotherapy. A patient with melanoma who failed dual check-point inhibitor therapy who showed a Partial Response at week 12 following treatment with MDNA11 achieved a Complete Response at week 52, with 100% regression of all target and non-target lesions.

Also, updated scans from the previously-reported pancreatic cancer patient continue to show sustained 100% regression of target and non-target lesions at 115 weeks. The patient remains in remission six months after ending MDNA11 treatment. All other previously announced patients with partial responses remain on treatment.

The combination dose escalation with pembrolizumab (KEYTRUDA) continues to enroll patients.

The company also reported a June quarter loss of $3.6 million or five cents a share. They finished the quarter with $35.6 million in cash, enough to carry them for about two years through the completion of the ABILITY-1 trial into mid-2026. Buy MDNAF under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

Inflation MegaShift

Gold ($2,490.90) went over $2,500 today before backing off. The yellow metal is flying on the Fed meeting as it seems like a given that the cutting cycle will begin in September now that the focus is shifting to employment

As it turns out, the Chinese central bank (PboC) did not stop buying gold in May. The PBoC buys gold in London from Western bullion banks. Because the bullion banks take care of the gold transport for the PBoC, the shipments from London to Beijing are disclosed in UK customs data. The customs data reveals that the PBoC continued to buy gold in May – when it communicated to the market it discontinued buying – at a rate of 53 tonnes. The PBoC stated it stopped buying to dampen the gold price so it could acquire more gold.

The fractal dimension hit 55 and immediately reversed, signaling this week began a new trend. But my experience is that’s very unusual behavior for gold, which likes to consolidate for long periods before kicking off a trend. So I’m hopeful but suspicious – the next few weeks will tell the tale.

Miners & Related

Coeur Mining (CDE – $6.00) reports June quarter results after the close next Wednesday with a conference call Thursday morning. Wall Street expects $242.25 million in revenues and a two-cent per share loss. September quarter guidance should be for $281.7 million and a four-cent profit. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $5.35) previously reported their production numbers (5.3 million silver equivalent ounces, consisting of 2,104,181 silver ounces and 39,339 gold ounces, a 7% and 9% increase, respectively, from last year) and held a conference call. This morning they released the June quarter financial data.

Revenues of $136.2 million dropped 7% from last year’s $146.7 million primarily due to a 15% decrease in the total number of ounces sold due to higher silver inventory levels held at quarter-end. They held 712,539 silver ounces in finished goods inventory as of June 30, inclusive of coins and bullion. The fair value of this inventory, which is not included in revenues, was $20.9 million. They could have beaten the consensus if they sold all the silver, but the stock dropped 13.4% today anyway.

During the quarter, ramp-up activities continued at First Mint, with new coin presses and laser-engraving equipment received at the facility. Installation of the equipment has begun, and they expect to launch several new products, including coins, in the second half of 2024. These added capabilities will increase minting throughput by over 50% and provide new sales channels with an expected increase in retail sales.

Consolidated cash costs of $15.29 per silver equivalent ounce and all-in sustaining costs (AISC) of $21.64 per silver equivalent ounce represented an improvement of 2% and a slight increase of 1%, respectively, compared to last year. They continue to undertake a series of cost reduction initiatives across the organization aimed at improving efficiencies and lowering production costs and other expenses while also increasing production.

They announced the discovery of a significant new, vein-hosted gold and silver mineralized system at the Santa Elena property in Sonora, Mexico. This new high-grade discovery, the Navidad vein system, was made at depth adjacent to the Company’s 100%-owned and currently producing Ermitaño mine.

CEO Keith Neumeyer said: “We are very excited about the new high-grade gold and silver system, Navidad; this is the most promising discovery at the Santa Elena property since Ermitaño was discovered in 2016. Four drill rigs are currently focused on this area, which appears to have the potential to expand as it is open in all directions. The proximity of this new discovery to the producing Ermitaño mine is important from an operational standpoint, and very encouraging for the prospects of continued exploration success across the underexplored, 100,000+ hectare Santa Elena land package. We believe that Navidad has the potential to significantly increase Santa Elena’s estimated Mineral Resources and, ultimately, extend the Life of Mine at this operation.”

They finished the quarter with $269.7 million in cash, including $117.5 million in restricted cash. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.63) reported after the close today, but won’t hold a conference call until tomorrow morning. Revenues slipped 2.7% from last year to $42.8 million, but they beat the $41.4 million consensus estimate. They reported a penny a share loss, missing the consensus estimate for a penny a share profit.

Sandstorm signed a definitive asset purchase agreement to sell a collection of non-core, non-precious metals royalties for $21 million plus the retention of the next $10 million in proceeds from the Copper Mountain Royalty. Upon completion of the transaction, Sandstorm will have sold over $50 million of non-core royalty and equity investments since the September 2023 quarter, including approximately $40 million in cash consideration.

They maintained their 2024 production guidance of 75,000 to 90,000 gold equivalent ounces, still expected to increase to approximately 125,000 ounces within the next five years.

They renewed their stock buyback program to purchase up to 20 million shares, about 7% of the issued and outstanding common shares. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $63,328.48) has gone straight down after nearly touching $70,000.

Click for larger graphic

Click for larger graphic

Why? Because two days after President Trump pledged to not move them and floated the idea of a Bitcoin Strategic Reserve, the US Government just moved $2.02 billion of Silk Road-linked bitcoin to a new address (bc1qsl993y04xnq4fyhmrt6cnmctgjjv9ukdvrk0cd). That signals they are getting ready to sell them. It looks like someone really does not want the bitcoin vote. BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $36.07) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $3,173.45) hasn’t moved much as spot ether exchange-traded funds saw negative net flows in their first week, as massive outflows from the incumbent Grayscale Ethereum Trust (ETHE) overwhelmed interest in the competing products. The equivalent bitcoin funds, which debuted in January, raked in $1 billion in net inflows during the first four days, even as they too suffered sizable outflows from the previously existing Grayscale fund. Overall, the spot ether exchange-traded funds lost $340 million in net outflows, with more than $1.5 billion exiting from the Grayscale Trust. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform ethereum.

iShares Ethereum Trust (ETHA- $23.75) is the cheapest and easiest way to buy etherum. ETHA is a Buy.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $76.93

Oil saw yet another large weekly draw with crude down 3.436 million barrels, including Cushing down 1.106 million, and gasoline down 3.665 million. At the same time, demand is strong. The Energy Information Administration sharply revised upward its May estimate for US oil demand. Using new monthly data, it pegs May at 20.80 million barrels a day, the highest ever seasonally for May and a massive ~810,000 barrels a day higher than the old estimate using weekly data of 19.99 million barrels a day.

The revisions upward included a very strong reading for gasoline. Using monthly data, @EIAgov pegged May gasoline demand at ~9.4 million barrels a day, the highest since August 2019, and ~350,000 barrels a day higher than their previous estimate.

But at the same time, lower 48 (i.e., shale) oil production was roughly flat both month-over-month and year-to-date as of May. The era of US shale “hyper growth” is over, even if Trump wins.

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

Global oil inventories just hit a record deficit relative to a normal baseline (2017-2019).

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

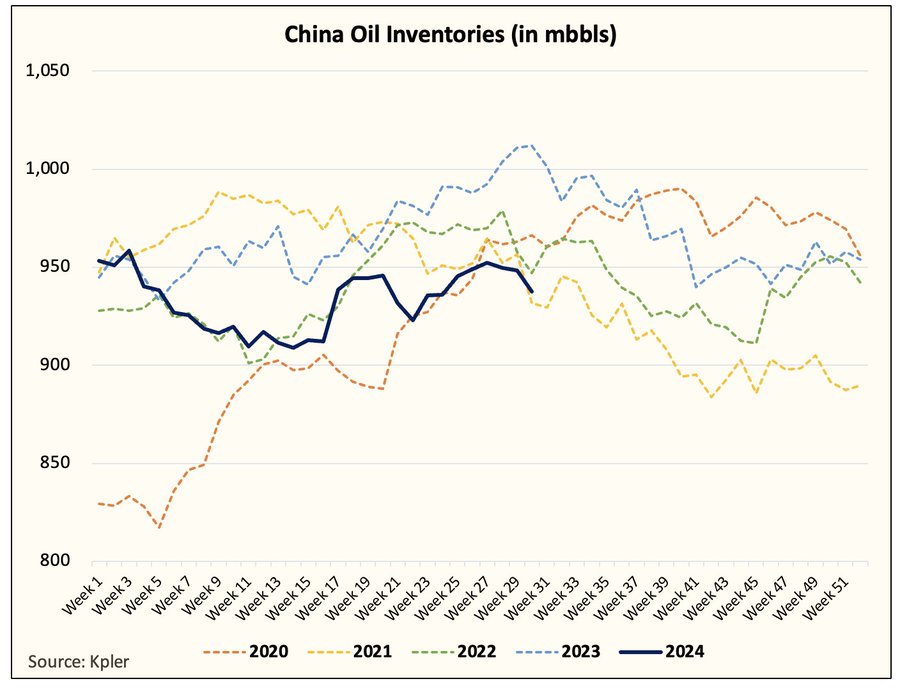

Chinese inventories are especially low. At some point, Chinese crude imports will have to increase.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

The Fibonacci 38.2% support level is at $75.63. The bottom of the trendline is $74.44. These suggest today’s prices are a relatively low-risk entry point.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

Hedge Funds’ net-long position in gasoline futures fell by 9,001 lots to 22,158 in the week ended July 23. They are now the least bullish on gasoline in more than four years.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

The July 2026 Crude Oil Futures (CLN26.NYM – no trades – June closed at $68.97) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $38.97) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $9.98) reported after the close today. Revenues rose 1.6% from last year to C$478.9 million or $345.13, below the $389.08 million consensus estimate. They lost 52¢ per share, far worse than the 45¢ consensus. But free cash flow was strong at $126 million.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Dion Hatcher said production averaged 84,974 barrels of oil equivalent per day (boe/d), 53% natural gas and 47% crude oil and liquids. Production increased 2% year-over-year and was at the upper end of their guidance range. They increased 2024 production guidance from 82,000-86,000 boe/d to 83,000- 86,000 boe/d, while maintaining capital budget guidance of $600 million to $625 million.

They returned $66 million to shareholders during the quarter, comprised of $19 million of dividends and $47 million buying back 2.8 million shares. So far this year they have repurchased and canceled 6.1 million shares, which is more than they repurchased in the full 2023 year. They believe the stock price is significantly undervalued – I agree! – and plan to allocate the majority of their shareholder returns to share buybacks.

Click for larger graphic

Click for larger graphic

VET is a buy under $11 for a target price of $24 or more.

Primary Risk:Oil prices fall.

EQT (EQT – $33.59) can make money at $2 natural gas – most can’t. People are forgetting that prices dictate just how fast Lower 48 gas production recovers. And with the prompt month below $2, the turn-in-line wells (TILs) the producers were expecting to bring on in August will be delayed. This will result in Lower 48 gas production remaining below ~102.5 Bcf/d, which will help keep the natural gas market in a small deficit.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $5.23) reports June quarter results on Monday. There are two publishing analysts. One expects $900.000 in revenues and the other expects $6.8 million. The average is $3.85 million, which is the meaningless number the computer bots will use to decide if the company beat or missed. Both analysts expect a 5¢ to 6¢ loss, with guidance for a 4¢ loss in the September period.

UUUU will benefit as long-term uranium contract prices hit over 16-year highs on supply uncertainty and higher demand from utilities scrambling to secure fuel to aggressively expand their capacity to power mushrooming AI data centers. Term prices are now around $79 per pound, the highest since 2008, and estimated to rise further in coming months. Spot prices, which rose nearly 88% last year and hit a 14-year high in February 2024, are now around $82 per pound.

In a May report, Goldman Sachs Research estimated global data center power demand, which now accounts for only 1% to 2% of overall power use, will grow 160% by 2030. The International Energy Agency says nuclear generation could roughly double by 2050 and so should supply. But in order to incentivize producers to invest in new projects, prices must exceed the marginal cost of production, currently at $90-$100 per pound, by at least 30%. So the market is expected to remain in deficit over the next 10 years at least.

Click for larger graphic

Click for larger graphic

Companies like Energy Fuels have limited volumes but know there’s high demand for their available pounds, so are increasingly looking for higher prices or are happy to run via spot sales. They will benefit from the US push for Big Tech to invest in climate-friendly energy generation to cater to surging AI needs. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

RIP Bob Newhart

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

Your considering The Bear Case for the Dollar Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 8/1/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $40.04) – Buy under $33, target price $60

Gilead Sciences (GILD – $76.49) – Buy under $80, target price $120

Palantir (PLTR – $26.08) – Buy under $22, target price $100+

PayPal (PYPL – $65.31) – Buy under $68, target price $136

SoftBank (SFTBY – $27.34) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $11.65) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $54.21) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $7.68) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $20.01) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $10.12) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.93) – Buy under $13, target price $30+

Velo3D (VLD – $2.36) – Buy under $10, target price $100

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.05) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.29) – Buy under $2, target $20

Compass Pathways (CMPS – $6.88) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $5.14) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $10.02) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.65) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.04) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $18.93) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($28.60) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $29.09) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $32.26) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $22.61) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $32.92) – Buy under $30, target price $50

Coeur Mining (CDE – $6.00) – Buy under $5, target price $20

First Majestic Mining (AG – $5.35) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.43) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.63) – Buy under $10, target price $25

Sprott Inc. (SII – $42.97) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $63,328.48) – Buy

iShares Bitcoin Trust (IBIT – $36.07) – Buy

Ethereum (ETH-USD – $3,203.73) – Buy

iShares Ethereum Trust (ETHA- $23.75) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – no trades – June 2026 last was $68.97) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $38.97 – Buy under $40; $100+ target

Vermilion Energy (VET – $9.98) – Buy under $11; $24 target

EQT (EQT – $33.59) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.23) – Buy under $8; $30 target

Freeport McMoRan (FCX – $43.63) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $218.36) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $494.74) – Expect to move back to Buy under $400

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

The FED should have cut and like you say are always late. Again they snatched a loss out of the jaws of victory. The severity of this upcoming recession could have been avoided. Powell should be fired. The probability of a 1/2 cut in September doubled today to 29.5%. I think a real shot of a cut in August especially if we get bad employment numbers tmrw.

The FED can’t and won’t fight market rates much longer. Powell and company are now at 5.3 percent while the yield on 10 year treasuries is 3.974. In addition the housing market is in a crisis. There is now a glut of homes available for sale. But interest rates are too high and lots of would be home owners are in debt up to their eyeballs with credit card debt. So their ability to qualify for financing on overpriced housing at high interest rates is quite limited. All that free money they got during the COVID nightmare is GONE. And all the people who refinanced at 3 percent are NOT selling to be jacked up to 5 plus rates. Powell is past the point of no return in my opinion. The big R as in Recession is looming. IMO

“All that free money”are you referring to those 2 small checks the Biden admin sent out during the covid crises?

Those were bad employment numbers. I still think the recession will be mild and short because Powell will panic and cut rates rapidly, setting up the next boom/bust cycle.

Here’s an example of censorship from Medscape, a leading news source for doctors. I was censored. An recent excellent article by a Yale professor detailed her experience treating covid illness using the medication, Paxlovid, plus her use of antioxidant and mitochondrial supplements. I commented and praised her integrative approach using drugs and natural supplements. I added a few other supplements not mentioned. I related how I have helped most patients recover quickly just with my use of natural agents, without drugs. BOOM–my comment wasn’t published, with Medscape citing how it violated community standards. What garbage–Medscape is funded by Big Pharma and serves as a mouthpiece for drugs. My comment went against their agenda, not community standards. Most community doctors in clinical practice want to hear about anything that can be done to help treat difficult conditions. This is typical verbiage utilized by censors. This is AI being used to efficiently eliminate free exchange of different viewpoints. It matters WHO programs the AI to serve a particular point of view. AI sabotages human desire for freedom and independence. I regard investing in AI with the same disdain as investing in processed food, beverage, tobacco and marijuana companies whose products poison most users.

Investing in AI is more like investing in hammers. It can be used for good or bad purposes.

Please repost your censored Medscape comment here, verbatim, thx.

Ae you equating AI with the greed of big pharma ?

AI magnifies the good and bad of people and companies. Big Pharma can help with incurable conditions like cancer, but for common “lifestyle” conditions like diabetes, high cholesterol which are mainly caused by overweight from bad eating and lack of exercise, BP is a detriment. My Medscape comment was censored in a nanosecond by AI. It would have been better to let it get published. If others disagreed, they could have presented their reasoning. Many readers would have benefited from hearing about natural and BP approaches.

Why not post your censored post here?

Don’t remember my exact words in the post. The essence is contained in my previous posts about this.

I think this is a hick-up.

This is a correction to a very hot market. I am surprised it took this long to happen. I believe a small correction is what we are looking at. Nothing more. Perhaps you can call it a mild recession.

Not falling off the cliff like some are predicting.

how long will it last?

Warren Buffet is pissed off and in a selling mood .(and he has big bucks that can swing the markets both ways).As is evident with the markets these last several days. He probably thinks there is doom ahead as well.

From what it looks like, it’s definitely a correction in the market. If I knew how long it will last I would be a zillionaire….

New World Investor for 8.8.24 is posted.