Dear New World Investor:

The July Producer Price Index (PPI) rose only 0.1% month-over-month from June, matching the consensus expectation. PPI was up 2.2% year-over-year, versus 2.7% in June. Core PPI, which excludes food and energy, was flat versus the consensus for +0.2%. It is up 2.4% year-over-year, down from 2.9% in June.

Then the headline July Consumer Price Index (CPI) came in at 2.9% year-over-year, the lowest annual reading since spring 2021 and a tick below the 3.0% expectation. It was up 0.2% from June with the badly lagging housing inflation statistics accounting for nearly 90% of the monthly increase. The core CPI was equally well-behaved, up 0.2% month-over-month and 3.2% year over year (June was +3.3%).

Inflation is above the Federal Reserve’s 2% target on an annual basis, but they know disinflation (not deflation) has enough momentum to keep the headline number falling, if only from the housing figures catching up to reality. The 12-month shelter rate of inflation fell to 5%, the lowest level in 2½ years.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

So they think they should cut rates sooner rather than later. According to the CME FedWatch tool, traders are aligned on a Fed cut next month — the question is by how much. Just over half of their bets are on a bigger, 50bp (basis point) cut, while the rest remain on a 25bp cut. I’m at 25bp.

We get the next core Personal Consumption Expenditures (PCE) index – the Fed’s favorite inflation indicator – on August 30. According to Goldman Sachs, based on the PPI and CPI reports the core PCE price index rose 0.14% in July, corresponding to a year-over-year rate of +2.65%. Additionally, the headline PCE price index increased 0.14% in July or +2.53% from a year earlier.

After the PCE we get the next payrolls report from the Bureau of Labor Statistics on September 6 and then the Fed meets on September 17-18.

After this morning’s July retail sales figure of +1.0% more than doubled expectations for +0.4%, I may have to give up on my short, mild recession forecast and admire J. Powell for pulling off a soft landing. US business fixed investment is accelerating and the corporate sector is running a financial surplus to the tune of ~2.6% of GDP – both of which are unheard of ahead of a recession.

Click for larger graphic h/t TS Lombard

Click for larger graphic h/t TS Lombard

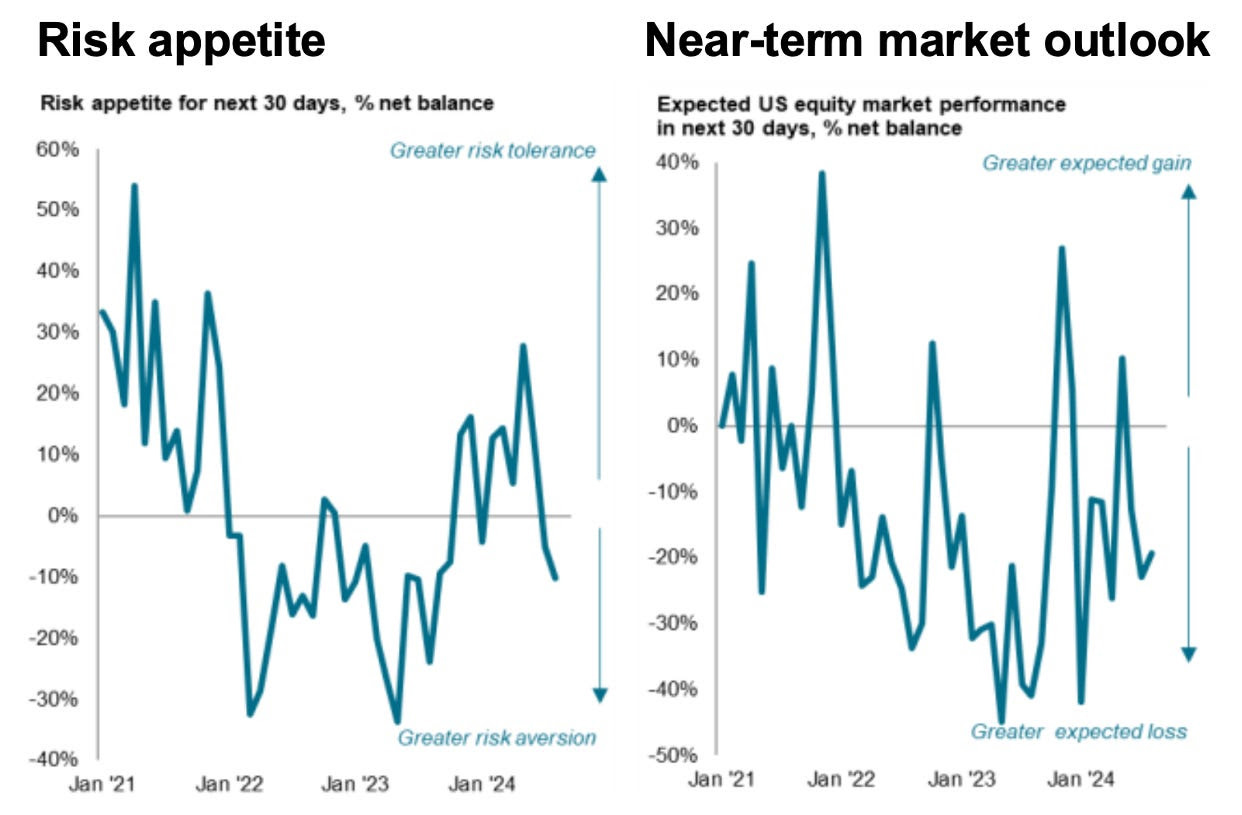

The good inflation data put the S&P 500 over 5400 for the first time since August 1 just as wrong-footed money managers’ risk appetite fell for a third successive month in August, down to a one-year low of -10% in August from -5% in July.

Click for larger graphic h/t S&P Global

Click for larger graphic h/t S&P Global

Market Outlook

The S&P 500 added 4.2% since last Thursday to back over 5500 as lower inflation eased the way for a September Fed rate cut. The Index is up 16.2% year-to-date. S&P earnings sentiment (upgrades – downgrades) in the US has improved sharply in recent weeks.

Click for larger graphic h/t Goldman Sachs via @mikezaccardi

Click for larger graphic h/t Goldman Sachs via @mikezaccardi

The Nasdaq Composite gained 5.6% and is up 17.2% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 2.9% as even biotech caught a bid. It is up 9.4% year-to-date. The small-cap Russell 2000 edged up 2.4% and is up a measly 5.3% in 2024.

The fractal dimension stopped consolidating with this week’s move up. It shouldn’t be possible for a new trend to start from such a low fractal dimension, but…

Top 5

Changes this week: Swapped the positions of EQT and USL to reflect Near-Term timing. Removed VLD from Long-Term.

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – September iPhone 16 introduction

USL United States 12 Month Oil Fund, LP – crude should rise quickly

EQT EQT –natural gas price rebound

CMPS – Compass Pathways – Rebound from negative AdCom review of MDMA and Phase 3 data release in December quarter

FCX Freeport McMoRan – copper shortage

AKBA Akebia Therapeutics – Vafseo TDAPA approval in January

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model forecast for September quarter real GDP growth fell from +2.9% on August 6 to +2.4% this morning due to their forecast of third-quarter real gross private domestic investment growth decreasing from 2.8% to 0.0%.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Wednesday, August 21

QUIK – QuickLogic – Through 8/22 – Needham Semiconductor & SemiCap 1×1 Conference

Thursday, August 22

Jackson Hole Fed Conference – Through 8/24

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple‘s (AAPL – $224.72) iPhone 15 builds were stronger than expected in July, and that momentum seems to be building into the iPhone 16 launch, according to Morgan Stanley. They said that based on the latest checks from their Greater China Tech Hardware team, they revised up their September quarter iPhone build estimate to 54 million phones, up +8% year-over-year and 2 million higher than their prior forecast. The 54 million iPhone builds is an all-time September quarter build record, 4 million units higher than the previous record, and implies September quarter iPhone shipments of 55 million units, up 10%year-over-year. They noted that is 5% above Morgan Stanley’s current September quarter shipment forecast of 52.5M units and 10% above consensus expectations of 50 million phones. They believe that the July iPhone build upside increases the odds of a September quarter beat.

They said that the upward revision for the September quarter reflects continued late-cycle iPhone 15 strength, as builds for all other iPhone models are unchanged, though it was not clear if this trend reflects upgrades due to the anticipation of Apple Intelligence or other factors. Their estimates for the second half of calendar 2024 for iPhone 16 builds remain unchanged at 85 million to 90 million units. and likely closer to around 87 million units. Morgan Stanley has an Overweight rating and a $273 target price for Apple. AAPL is a HOLD – I expect to move back to Buy under $175 for new iPhones.

As I expected, Gilead Sciences (GILD – $74.34) got FDA approval for Livdelzi (seladelpar) for second-line therapy in primary biliary cholangitis, an autoimmune liver disease mainly affecting women that causes decreased liver function, debilitating itching, and fatigue. Gilead estimates there are approximately 130,000 people in the US with primary biliary cholangitis, of whom 30,000 to 40,000 don’t respond to first-line therapy.

Before the approval, Gilead paid Johnson & Johnson $320 million to buy out J&J’s 8% royalty on Livdelzi net sales. GILD is a Long-Term Buy under $80 for a first target of $120.

Palantir (PLTR – $31.22) and Microsoft partnered to deliver AI to classified networks for critical national security operations. Palantir will deploy their suite of products – Foundry, Gotham, Apollo, and AIP – in Microsoft Azure Government, Azure Government Secret (DoD Impact Level 6), and Top Secret clouds.

Integrating Microsoft’s Azure cloud compute and powerful language models (GPT-4 and others) with Palantir’s Foundry data integration and ontology capabilities, and AIP’s use-case building capabilities, will enable operators to build AI-driven operational workloads across defense and intelligence verticals, from logistics, to contracting, to prioritization, to action planning and more.

Third Bridge wrote: “The performance tells us that Palantir’s value proposition for AI and generative AI solutions continues to resonate with customers despite a crowded and opaque market landscape. We’ve heard from experts that downsizing an initial deployment of Palantir’s Foundry platform could significantly broaden the company’s addressable market, and the introduction of AIP and the Bootcamp sales model appears to be successfully facilitating that transition.”

Wedbush wrote: “With this marquee deal solidified and Microsoft leveraging Palantir for AI and Large Language Model capabilities to the US government, the company can now increase the pace of AI implementation while Palantir continues to accelerate AIP adoption within the federal sector. We believe this will be a launching pad for the Palantir AIP story to hit the Department of Defense and broader Beltway ecosystem over the next 12 to 18 months.” They rate the stock Outperform with a $38 target price.

Citigroup raised their target price from $28 to $30 and said government contracts were a key factor in Palantir’s June quarter earnings beat. They wrote: “Results show that Palantir’s approach, potentially helped by AIP, is able to tap into emerging AI pools of spend with record net additions of large eight-figure customers and a 15-point reacceleration in US Commercial that helped offset some softer international market performance.”

Palantir also won an $8 million contract with the Air Force for commercial AI mission control software and integration services to be performed primarily in South Korea. And they sent the first AI-fueled TITAN prototype to the Army. PLTR is a Buy under $22 for a $100+ target.

PayPal Holdings (PYPL – $67.94) picked up a new bullish brokerage firm as Daiwa Capital Markets upgraded the stock from Neutral to Outperform and raised their target price from $68 to $72. They said some of the company’s initiatives are “quickly generating visible results,” such as the improving profitability for Braintree that I already noted.

High Growth Investing wrote: “PayPal Stock : The Sleeping Giant Awakes, subtitled “Why the unloved payment provider is one of my high-conviction buys at current prices.” They wrote: “PayPal is suffering from the expectation, shared by many analysts, that the PayPal platform could become less important in the age of Apple Pay and Generative AI. I think these fears are overblown. PayPal’s massive user base of over 220 million monthly users provides a good basis for the new management to create significant value for long-suffering shareholders in the coming years…Patience is now required to give the new management time to confirm the positive fundamental trend. Then it should only be a matter of time before the stock price leaves the valley of tears.”

I couldn’t agree more. PYPL is a Buy under $68 for a double in three years.

SoftBank (SFTBY – $28.40) finally got a Seeking Alpha June quarter TRANSCRIPT HERE. CEO Masayoshi Son is making a big bet on AI. In the June quarter SoftBank 10x’d its stake in Nvidia (NVDA) from 1.05 million shares to 10.5 million shares. They also established a new 5.41 million share position in Tempus AI (TEM). SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $10.66) was teased by the Green Zone Fortunes newsletter as

“RIP: Apple iPhone 2007—2024? Why Apple (The World’s Most Innovative Tech Company) Has The Guts to Kill Its iPhone Starting September 10… And Launch The Next Big Thing In Its Place.”

The “Next Big Thing” is the AI iPhone – sounds more like an evolution than a death to me – and the stock he is teasing? “It’s a tiny company making what I believe is an indispensable part for the iPhone Killer. On the low side, I believe this company could double in price…On the high side — i.e. if shares follow the same trajectory as Apple — you could pocket up to 20x your investment over the next several years.”

Nope – just Enovix. While I appreciate the enthusiasm of his copywriters, the odds that Enovix is about to become a supplier of a critical part of the iPhone 16 are somewhere between no way and zero. Now the 18, 19, or 20 – maybe. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $6.27) announced an 11% reduction in force as part of their restructuring effort. They will take a charge of $9.5 million to $10 million in the September quarter for severance payments. FSLY is a Buy up to $10 for a 3- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

QuickLogic (QUIK – $8.94) reported June quarter revenues up 41.3% from last year to $4.1 million, below the $4.5 million consensus estimate. The pro forma loss of 5¢ per share also was disappointing compared to expectations for breakeven. On the conference call (AUDIO HERE and TRANSCRIPT HERE), management said they had $3 million in scheduling push-outs that caused them to lower their full-year growth projection from 30% to 15%. They did not lose any contracts to competitors that they expected would contribute to the 30% growth. And none of the push=outs were due to delays caused by QuickLogic.

They expect September quarter revenue to be up only slightly from the June quarter, followed by a very sharp rebound in the December to hit their revised full-year growth projection. They have deliverables scheduled to support the majority of the implied revenue outlook for the December period.

In addition, they have increased their two-year sales funnel to $189 million. Within this, there are numerous outstanding proposals including three new RFPs with major customers totaling approximately $8 million that they submitted during July alone. Management said: “All in all, the things that are most important for our long-term success are going extremely well and even with a lower growth outlook for 2024, our four-year CAGR is 30%. We believe we are well positioned to maintain or exceed that rate of growth during the coming years.”

They guided for September quarter revenues of $4.2 million, ±10%, with a 2¢ to 9¢ pro forma loss. They will use less than $500,000 of their $23.3 million available cash, which includes their $20 million line of credit.

The stock dropped 12.7% yesterday and bounced back more than half of that today. It could have been worse, but CEO Brian Faith gave a superb presentation at yesterday’s Oppenheimer Technology, Internet, & Communications Conference (AUDIO HERE and REALLY GOOD SLIDES HERE). Brian went through the whole repositioning strategy in detail and made it clear that quarterly fluctuations and push-outs are trivial compared to the revenue ramp ahead of them, much of which is baked in. They have a tiny piece of a $1 billion market where they are the technology leader.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

They will be profitable with positive cash flow in the second half of the year, and profitable for the year as a whole. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $5.83) successfully hot fired its new Archimedes rocket engine for the first time, which was a critical technical milestone toward the first launch of Neutron, their new medium-lift rocket. Neutron’s first flight is scheduled for mid-2025.

Rocket Lab has begun installation of the largest automated fiber placement (AFP) machine of its kind into their Neutron rocket production line in Middle River, MD. The custom-built 99-ton, 39-ft. tall AFP machine will enable Rocket Lab to automate production of the largest carbon composite rocket structures in history. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $1.30) reported a really bad June quarter with revenues down 59.0% from last year to $10.3 million, far short of the $13.7 million I used in my May 16 spreadsheet – and even that did not lead to an annual estimate as high as the company’s guidance. Not surprisingly, they said: “Given the uncertainty of timing of the company’s deferred orders and other factors, the company is withdrawing its previously announced financial guidance for fiscal year 2024.”

The pro forma loss was $2.57 a share. They said second quarter cash flow, excluding financing activities, was in line with their forecast and improved more than 70% on a year-over-year basis. That’s all well and good, but they ended the quarter with only $3 million in cash. In an SEC filing on August 9, they said they are laying off 63 employees or about 30% of the company.

What’s next? The Board has to sell the company. They probably have low-ball offers on the table, and since they are effectively out of money they’ll have to take one. Somebody is going to make a lot of money out of this technology – SpaceX? – but it’s not Velo3D or us. I misjudged how quickly demand for their advanced technology would arrive as well as former CEO Benny Buller’s ability to manage and grow the company. Sell VLD.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $1.44) presented at the Canaccord Genuity Growth Conference (AUDIO HERE). CEO John Butler said they have two products in development to follow Vafseo.

Vafseo enters a market of half a million dialysis patients with anemia, a $1 billion market. Akebia is (1) driving physician demand, (2) contracting with clinics so doctors can prescribe it, and (3) generating additional clinical data to make Vafseo the standard of care after the TDAPA period expires in January 2027, when Vafseo will cost $2,500 a year.

For their first target market, a once-a-day oral product fits the 80,000 home dialysis market perfectly. For the second target, about 150,000 or 25% of patients are not in the target range for hemoglobin, and doctors spend a large part of their time managing these more difficult cases. They are the most expensive patients for dialysis organizations – they use the most ESAs (Erythropoiesis-Stimulating Agents) – and are the most at risk of a heart attack. Vafseo solves that problem.

The company is funded through the TDAPA period and should never need to raise more equity. Buy AKBA up to $2 for the vadadustat launches in the EU, UK, and (after TDAPA approval in December) the US.

Primary Risk: Vadadustat doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: TDAPA January

Probable time of next financing: Never

Compass Pathways (CMPS – $7.05) Chief R&D Officer Mike Gold and SVP: Medical Affairs Steven Levine presented at the Canaccord Genuity Growth Conference (AUDIO HERE). They did an excellent job of showing how COMP360 differs from the Lykos Therapeutics’ MDMA drug that the FDA turned down on August 9. Their two Phase 3 trials are designed to answer the “functional unblinding” issue that sunk Lykos’ drug.

On August 10, the journal Psychopharmacology retracted three articles related to the use of MDMA for PTSD. Psychopharmacology cited protocol violations as well as failing to disclose potential conflicts of interest in its retraction notice. Scientists who worked on the pieces are affiliated with the Multidisciplinary Association for Psychedelic Studies, which incubated Lykos Therapeutics, the company behind midomafetamine, the drug the FDA just rejected. Lykos CEO Amy Emerson is a co-author. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2026

Probable time of next financing: Late 2025

Inovio‘s (INO – $7.80) earnings call transcript finally posted HERE. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2025

Probable time of next financing: After FDA approval in 2025

ScyNexis (SCYX – $1.73) reported a June quarter GAAP loss of 30¢ a share, 10¢ worse than the 20¢ estimate. In the press release they said: “Third-party manufacturing of new batches of ibrexafungerp for use in clinical trials is in progress, and SCYNEXIS looks forward to restarting the Phase 3 MARIO study in invasive candidiasis.”

As I said on the Comments, there would be no point in manufacturing new batches unless the FDA has blessed the manufacturer and the process, and there is no way to restart MARIO without the FDA lifting the clinical hold. I think an announcement is imminent.

Today, ScyNexis closed with a total market capitalization of $65.5 million, with a deal worth hundreds of millions of dollars in place with GSK. Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2024

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,403.90) continues to rise, punctuated by occasional drops as the high-frequency computer bots decide the Fed is a little less likely to cut 50 basis points in September. It’s kind of pathetic that grown men focus their energy on picking up nickels when a steamroller is bearing down on them.

OK, OK. the fractal dimension clearly is signaling a new trend after this week’s jump in gold prices. New all-time highs lie just ahead, with a full load of energy to go higher. A run at $3,000 is not out of the question. We’re going to need a new graphic.

Miners & Related

Sandstorm Gold (SAND – $5.33) posted their sixth Shareholder FAQ:

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sprott Inc. (SII – $41.11) June quarter earnings call transcript finally posted HERE. Buy SII under $40 for a $70 target price.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $56,817.93) fell as the “Harris/Biden” administration moved another 10,000 Silk Road bitcoins to Coinbase. Presumably, they want to sell them before a Bitcoin Strategic Reserve can be created.

Seeking Alpha wrote: Crypto bill can be passed this year, Schumer says, as Democrats woo industry. They said: “Senate Majority Leader Chuck Schumer (D-NY) said passing a bipartisan cryptocurrency regulation this year ‘is absolutely possible,’ reassuring crypto advocates that want to back the Democratic presidential candidate Kamala Harris.

Seeking Alpha added that while Harris hasn’t formally shared her views yet, senior Democrats shoring up industry support indicates that she may pivot away from the Biden/Harris Administration’s harsh stance on crypto.

Crypto has become a significant topic in the upcoming presidential election, with Republican nominee Donald Trump calling for the US to be “the bitcoin superpower of the world.” His running mate, Sen. J.D. Vance (R-OH), is also pro-crypto, and their campaign has been accepting crypto donations.

Click for larger graphic

Click for larger graphic

Matt Hougan, CIO at Bitwise, said: “If you look at most assets in the world, institutions own at least half of them. In order for that to happen, we’re going to need to see institutions add a trillion dollars. We’re like a few percentage points into that trade. That’s a multi-year trade. It’s not going to take place overnight, but a very small fraction can even buy these. That’s going to change in the second half of the year, and I think you’ll start to see that in the flows as we get into October and November and December.”

Morgan Stanley just began allowing wealth advisors to begin selling Bitcoin ETFs. How fast are BlackRock’s bitcoin and ethereum exchange-traded funds accumulating?

Click for larger graphic h/t @zerohedge

Click for larger graphic h/t @zerohedge

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $32.50) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $2,575.94) will benefit from the ethereum exchange-traded funds, but not as rapidly as happened with bitcoin. According to the above-mentioned Matt Hougan, excluding the outflows from Grayscale’s converted Ethereum Trust, all of the Ethereum ETFs have attracted more than $2 billion in inflows. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

iShares Ethereum Trust (ETHA- $19.35) is the cheapest and easiest way to buy ethereum. ETHE is a Buy under net asset value.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $77.94

Oil closed at $80.06 on Monday but sold off a bit from there after the Energy Information Administration reported a crude build of 1.357 million barrels. Crude exports are jumping, so we should see a draw in next week’s report. Gasoline fell 2.894 million barrels as the summer driving season rolls on.

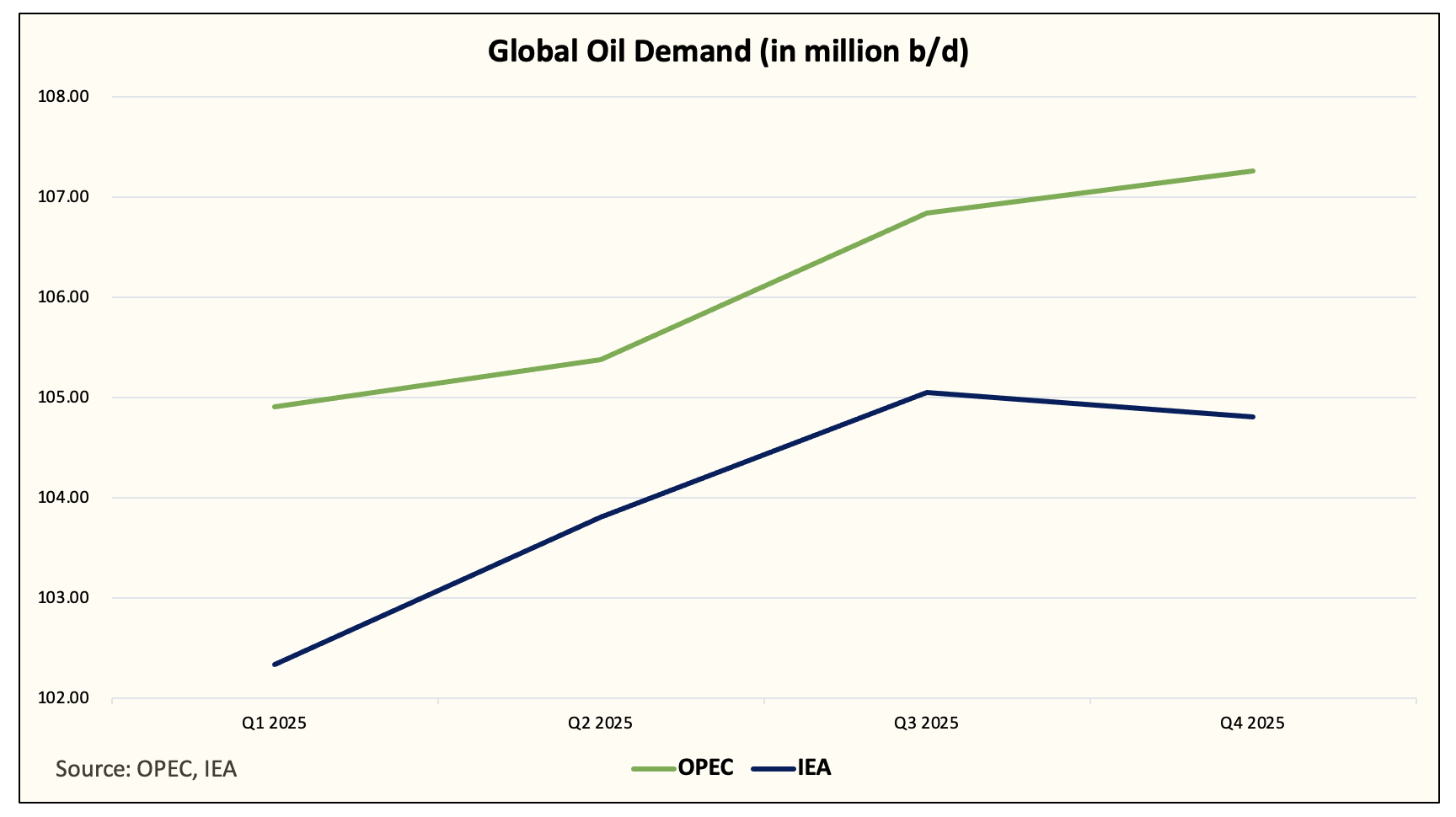

There is a dramatic difference between OPEC’s and the International Energy Administration’s forecasts of oil demand. I think the IEA’s forecast is closer to right, in part because I still think we’re in for a recession.

Click for larger graphic h/t HFI Research

Click for larger graphic h/t HFI Research

But in either case, prices should be supported with global oil inventories very low because demand so far has held up:

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

The July 2026 Crude Oil Futures (CLN26.NYM – $68.56) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $39.21) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $10.29) is a Buy under $11 for a target price of $24 or more.

Primary Risk:Oil prices fall.

* * * * *

Your Moving On from the Anthropocene Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 8/15/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $40.26) – Buy under $33, target price $60

Gilead Sciences (GILD – $74.34) – Buy under $80, target price $120

Palantir (PLTR – $31.22) – Buy under $22, target price $100+

PayPal (PYPL – $67.94) – Buy under $68, target price $136

SoftBank (SFTBY – $28.40) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $10.66) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $57.73 – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $6.27) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $19.43) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $8.94) – Buy under $10, target price $40

Rocket Lab (RKLB – $5.83) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $2.62) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.44) – Buy under $2, target $20

Compass Pathways (CMPS – $7.05) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $4.00) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $7.80) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.70) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.73) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $20.94) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($28.42) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $29.33) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $33.70) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $22.65) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $31.95) – Buy under $30, target price $50

Coeur Mining (CDE – $5.90) – Buy under $5, target price $20

First Majestic Mining (AG – $5.50) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.43) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.33) – Buy under $10, target price $25

Sprott Inc. (SII – $41.11) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $56,817.93) – Buy

iShares Bitcoin Trust (IBIT – $32.50) – Buy

Ethereum (ETH-USD – $2,543.71) – Buy

iShares Ethereum Trust (ETHA- $19.35) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $68.56) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $39.21) – Buy under $40; $100+ target

Vermilion Energy (VET – $10.29) – Buy under $11; $24 target

EQT (EQT – $31.78) – Buy under $35; $70 first target

Energy Fuels (UUUU – $4.567 – Buy under $8; $30 target

Freeport McMoRan (FCX – $43.58) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $224.72) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $537.33) – Expect to move back to Buy under $400

Sell

Velo3D (VLD – $1.30)

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

MM–on VLD, in addition, you seriously misjudged the financial state. Amateurs on YMB were on target. Where were you? I repeatedly called you out on this, but you ignored the market and my warnings. As recently as last week, you had a buy price below $10 and target of $100. This parallels the demise of NVTA which you seriously misjudged. Up until the end, you had a low lottery ticket buy on that.

Right

I sold VLD today for a total 90% loss from an average cost of 44 cents pre RS, or $15.40 after RS. Most subscribers have suffered nearly 100% losses.

MM–you cannot go on like this. With frequent 99% losses, it takes a 100 bagger to make up losses like that. With 99% losses on each of 10 stocks, it takes a 1000 bagger with the same dollar investment to break even on the combined 11 stocks. I bet you have almost never had a 1000 bagger.

Your introductory market analysis is excellent, but your due diligence on current financial status of each stock is the total opposite. I suggest you sell this newsletter, or confine your comments to overall market analysis, and leave it up to a younger analyst to make stock recommendations. Your market analysis can be used to trade major indices like SPY, and ultra safe blue chips like Berkshire H.

MM – While I generally concur with the overall sentiment expressed above by JGMD, I would suggest this newsletter reduce its focus on general market analysis, since this information is readily obtainable from other sources, so that much more time/attention can be devoted to materially improving the quality and timeliness of the stock recommendations, updates and underlying analyses (with input from other analysts and subject matter experts in your professional network, as appropriate).

Your recommended approach does make sense.

so was Arth, APTO,, ACRDF etc

MM–AKBA seems like one of the few NWI stocks with good promise. How can analysts compiled by Yahoo project only $177 million for 2025 sales? Auryxia sales for 2024 are projected at $172 million, probably $155 million or so for 2025. That leaves $22 million for Vafseo. What is your estimate for 2025 sales for Vafseo? Even tiny sales for Q1 and Q2 could cause a renewed plunge in the stock in the first half of 2025.

I expect $70 million to $100 million in Vafseo sales in 2025. Yahoo is reporting only 3 analysts, one of whom is at $129.31 million, one at $170.85 million, and one at $232.50 million. In short, with a $100+ million spread between high and low, nobody knows.

But from only a $300 million total market capitalization today, the potential reward looks way higher than the potential risk to me. That’s because I think the company is doing everything right for a strong launch, a very profitable TDAPA period, and continued success thereafter.

I saw the Yahoo 3 analyst revenue estimates. These are total Auryxia and Vafseo revenues. YMB poster Paul R says that A loses its patent March 2025, but will retain some revenues due to the bundling of A and V from TDAPA. Do you have estimates on total A sales for 2025 and future years? How will the stock react to only $70-100 million in V sales in 2025, when blockbuster sales are expected in several years?

I think TGTX is the safest NWI stock. It just got cashflow positive after less than 2 years of Briumvi sales. Which will obtain blockbuster ($1 billion sales) in the shortest time, AKBA or TGTX?

MM. should we chase Palantir? It seems to be way above your buy limit?

The following stocks are above my Buy limit or so far above they’ve been moved to Hold:

AAPL, GLW, META, PLTR, SFTBY, CIBR, TGTX, SGDM, CEF, SIL, CDE, and SII.

At these market levels and stages of the economic and political cycle, I don’t think it’s a good idea to chase.

Instead, if you need more exposure, focus on stocks under the Buy limit, e.g.:

– – Instead of (AAPL, META, PLTR, SFTBY) buy PYPL or the new recommendation I am working on.

– – Instead of CIBR, look at stocks that are down ENVX, QUIK, or RKLB.

– – Instead of TGTX, AKBA, CMPS, SCYX, or INO for the next 12 months, or ABCL, EDIT, or MDNA for public VC risk/reward.

– – Instead of chasing (SGDM, CEF, SIL, CDE, and SII). go for SGDJ, AG, or SAND

– – And there’s still time to catch the commodity supercycle with USL, VET, EQT, UUUU, and FCX.

ARTH followed by the VLD disaster amply justify the anger and frustration of many subscribers.

BUT, imho, MM’s fortunes as a stockpicker may be starting to turn, provided one has had the fortitude to accumulate some of the names regularly after his initial recommendation. Example: RKLB!!!

With the long-term perspective of having been a subscriber for more than 3 decades, I can tell that part of the problem has been his migrating towards Biotech and Medtech instead of remaining with his original focus on hardware and software with the Caltechnology Letter. Had he been able to do both maybe he would have had a very early position in NVDA with which to offset the ARTH debacle for example.

I feel badly for the subscribers who have lost so much on VLD, NVTA, ARTH, APTO and ACRDF. Always keep in mind that when Murphy recommends an investment he has a tendency to accept the bull case and reject the bear case. Although he has been aware of NGENF for many years, he has never recommended it. Even after it began its Phase 2 trial in chronic spinal cord industry and fell from a high of $2.99 in February to a low of $1.30 in June, he passed on it. Now at $2.20, it has a catalyst coming up in the next 7 weeks as the CEO announced several times in the past couple of weeks that they expect to reach full enrollment before the end of September. An even bigger catalyst will come between February and May when the results of the Phase 2 trial will be announced. Although I greatly greatly increased my holdings last year, I added more between April and June. If you don’t yet have NGENF, I would add here for a minimum 100% gain between now and next May. Another 100% gain in 2 months (the NAT Oct 3.5 Call under .30) looks like it is on its way and the window to buy appears to have closed.

What do you think the odds of clinical trial results matching pre clinical? I have some,Would like more. The upside is huge.

Let’s put it this way … The biggest investment I have in a publicly traded company is in NGENF

Thanks Chris,Now if ACXP could partner up in the next few weeks I could get some more NGENF. At this point highly unlikely. It’s been so long. I really thought he could do it quickly. He probably will sometime in the distant future.

Chris,

I share your enthusiasm for NGENF. I have read much of the preclinical work by Dr. Jerry Silver’s lab, heard him speak in online presentations and private meeting. His discovery that CSPGs inhibit nerves from growth and repair following injury is key to the NGENF approach to healing spinal cord injury. There is a video online from his labshowing recovery of mice including ability to climb a ladder using hind legs effectively. This has been confirmed in recently injured mice as well as in mice who sustained injury a year prior to treatment. Thus the current trial has an arm recruiting patients with injury over a year old and is starting to enroll another arm with patients who have sustained more recent injury. I have a very large position in shares and look forward to the announcement that the first arm of 20 patients is fully enrolled, as the dosing and PT period is a measurable 12 weeks with a 4 week followup. I was now aware that calls are available, will need to look into that.

I agree that Jerry Silver sounds convincing. I don’t understand your last sentence–“calls are available.”

KAREN, I was referring to the NAT 3.5 Oct Call. There are 10 offered and bid at .20, .25. If you put in an order for 10 contracts at the market, you will double your money in lass than 7 weeks

Adding to the disasters, MM’s two gold stock picks are pathetic with First Majestic being widely regarded as a management piggy bank vs a shareholder focused legitimate corporation like AEM or AGI. The best miners are souring.

The persistent lack of fundamental stock research shared and explained amazes. Massive losses for those who acted on most recommendations.

Not sure I will ever read another issue of my lifetime subscription.

I only have two gold stock picks? And AG is silver, not gold.

Thanks MM I had nice a move today in TGTX my 3erd biggest holding rolled half of my PCYC house $ another great bio MM pick.

from YMB

Briumvi will be a Blockbuster drug, ie, over $1B in revs. That means $750M to $850M in profit or more than $5+/share earning. The PE on a newly emerging blockbuster product will result in a PE of at least 20 and a minimum price over $100/share

MM–on AKBA, what is the cost of generic ESA’s like darbepoetin, epopoetin? I suspect much cheaper than Vafseo at $15,500 annually during TDAPA. After TDAPA expires, V will be $2500 annually, probably competitive with generic ESA. Of course, V is medically superior to generic ESA’s, but will much cheaper ESA’s greatly reduce numbers of patients prescribed V? How does bundling of Auryxia and Vafseo compare in costs to existing bundling of ESA’s with other drugs?

MM–Darbepoetin doesn’t seem to be available as a generic, so what are the prices for Brand Aranesp, the ESA used today? Look at goodrx. Medicare effectively doesn’t cover it. I don’t know about other insurances. Put another way, the co-payment cost to the patient on Medicare is roughly $1400 monthly. For the initial dose of 0.45 mcg/kg body weight given weekly or 0.75 mcg/kg given every 2 weeks, assume typical body weight of 90 kg. That’s 40 mcg weekly or 160 mcg monthly. Or 67 mcg every 2 weeks, 135 mcg monthly. The cash goodrx cost of four 1 ml vials of 40 mcg/ml is $1200-1300 monthly. Darbe comes in higher concentrations with slight lowering of the total costs, but those are approximate numbers to consider. These Darbe costs are much higher if higher doses are needed, and the same may apply to V if higher doses are needed.

I don’t know the IV administration costs by the clinic/dialysis center, but it can be given by a patient himself subcutaneously without cost. I don’t know the bundling deals, but it appears that Darbepoetin is much cheaper than Vafseo during TDAPA, and even after TDAPA when the cost of V drops to $2500 annually, still double what Darbe costs. When will generic Darbe be available? Then it will be even cheaper.

How is Butler going to deal with these facts that V will be much more expensive than Aranesp during TDAPA, and even after TDAPA when V will still be double the price of Aranesp?

Further info from goodrx. The cash price of 30 tablets of 150 mg of V is $650-700. The clinical trials used 150-600 mg daily to titrate the hemoglobin to the appropriate level. It didn’t say what was the average dose. So the V monthly price is $650-700 for lowest dose, $1300-1400 for middle dose, $2600-2800 for highest dose. I don’t know how insurance coverage affects these numbers. I don’t know typical doses of Darbe currently used. My Darbe numbers in my previous post are for starting doses. In the worst case of no insurance coverage for V, which is the case for Darbe, for middle daily dose of 300 mg V, the cash costs are comparable for V and Darbe. All I can say confidently is that the 2 year TDAPA provides a revenue bonanza for AKBA. They better have a great launch to bank the most money by Jan 2027. After that, the numbers aren’t great for V, unless V is declared standard of care and it dominates over ESA’s. I now better understand the desire for bulls to sell the stock in about 2 years from now. It may not be a great long term hold.

MM?

New World Investor for 8.22.24 is posted. I removed TGTX from Near-Term because we got the recovery from the overdone pullback.