Dear New World Investor:

From the Fed minutes of their February meeting, released yesterday: “Almost all participants observed that slowing the pace of rate increases at the current juncture would allow for appropriate risk management.”

It looks to me like the economy is stronger than expected (good news), which will require the Fed to raise interest rates a little higher than expected for a little longer than expected (bad news). If the economy slows faster than now expected (bad news), the Fed will slow, pause, end, or cut interest rates (good news). Either way, as long as Powell et. al. stay data-driven and move incrementally, it no longer matters much what the exact path is. Stocks will move based on fundamentals, particularly growth in sales and earnings.

In the December quarter, the stock market expected many bad things: a European power crisis, rising unemployment, slowing GDP with a risk of recession, no China reopening, profit margin declines, credit defaults, bankruptcies rising, and continued geopolitical tensions. Very few materialized, yet most market participants sat on their hands – and their cash. As Goldman Sachs wrote: “No one is positioned for a rally and everyone wants it to roll over, rather than be forced to chase.” That means the pain trade remains up.

I still expect another 25-75 basis points of rate hikes, followed by a long pause starting in the June quarter. Inflation and economic output data are cooling faster than the employment market is weakening, and the Fed knows it. This gives the Fed permission to pause in the near future rather than having runaway inflation force it to hike us beyond a mild (if any) recession and into a depression.

“What has been missing throughout the Fed’s tightening cycle is a clear narrative as to what rate hikes will achieve. Rates were never going to influence the durable goods inflation of 2021. Rates are a clumsy way of tackling profit-led inflation.” – UBS

Market Outlook

After Tuesday’s drop, the biggest so far this year, the S&P 500 lost 1.9% since last Thursday. The Index is up 4.5% year-to-date. The Nasdaq Composite lost 2.2% but still is up 9.8% for the year. The small-cap Russell 2000 dropped 1.8% and is up 8.3% in 2023.

The fractal dimension consolidated a little more this week. The next trend could start anytime.

Top 5

Changes this week: None

Near-Term – chronological order

INO Inovio – VGX-3100 HPV Phase 3 results any day

EQT EQT – cold March coming

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Virus Update

There has been an amazing drop in COVID-19-related deaths. The seven-day moving average peaked at 3,499 deaths per day on January 17, 2021. About a year later, on January 31, 2022, the average peaked at 2,797 a day. Fast forward a year to January 15, 2023, and it peaked at only 597. Today, it is down to 138 deaths per day.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, February 24

Personal Consumption Expenditures Index – 8:30am

Monday, February 27

AG – First Majestic – Through 3/1 – BMO Global Metals & Mining Conference

SII – Sprott – 10:00am – Earnings conference call

Short Interest – After the close

QUIK – QuickLogic – 5:30pm – Earnings conference call

Tuesday, February 28

CDE – Coeur Mining – 9:45am – BMO Global Metals & Mining Conference

NVTA – Invitae – 4:30pm – Earnings conference call

RKLB – Rocket Lab – 4:30pm – Earnings conference call

Wednesday, March 1

INO – Inovio – 4:30pm – Earnings conference call

Thursday, March 2

GLW – Corning – 1on1s – Susquehanna Technology Conference

VLD – Velo3D – 5:00pm – Earnings conference call

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Algernon Pharmaceuticals (AGNPF – $1.42) has dosed the first patients in their trial of DMT for stroke recovery. This week they announced a new research program with DMT for traumatic brain injury (TBI). They’ll start a Phase 2 trial in the December quarter.

Up to 50% of mild TBI patients have symptoms that have not resolved after six months. Millions of mild TBIs occur each year, and that number is expanding with increased access to motor vehicles in the developing world and the associated increase in accidents. There are currently no drugs approved for the treatment of TBI of any severity.

Algernon appointed a global TBI expert, Dr. Andrew Maas, as a scientific and medical advisor to help guide the TBI research program. He is Emeritus Professor of Neurosurgery at the Antwerp University Hospital and University of Antwerp. He holds positions as past Chairman of the Neurotraumatology Committee of the World Federation of Neurosurgical Societies (WFNS) and the International Neurotrauma Society, and is Co-Chairman of the European Brain Injury Consortium. He said: “There is a great need to improve the recovery potential in patients after TBI, and the role of neuroplasticity is a promising target, for which DMT holds potential.”

AGNPF is a Hold for the Phase 2b IPF/chronic cough results.

Primary Risk: Ifenprodil fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2024

Probable time of next financing: 2023

Graphite Bio (GRPH – $2.55) discontinued their sickle cell program, presumably because they couldn’t figure out how to modify their gene correction drug to avoid the serious side effects. They will continue research to identify another development candidate.

To cut the cash burn, they are laying off 50% of the workforce. At the end of December they had $283.5 million in cash. We’ll get more details when they report earnings in March. GRPH is a Hold until the conference call.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Pre-clinical

Probable time of first FDA approval:Unknown

Probable time of next financing:Unknown

Inovio (INO – $1.32) reports December quarter results next Wednesday. As usual, the real news will be any updates on their various clinical trials. INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: Mid-2024

Invitae (NVTA – $2.08) reports earnings next Tuesday. The consensus is expecting revenues to fall 3.8% from last year to $121.28 million with a 53¢ loss per share, much better than the December 2021 quarter loss of 81¢. There is a wide range of loss estimates, from -27¢ to -91¢.

For the March quarter, Wall Street expects sequentially flat guidance for $122.17 million in sales (Range: $112.18 to $127.92) and a loss of 44¢ (Range: -30¢ to -54¢). For the full 2023 year, the consensus expects sequentially flat revenues of $516.11 million (Range: $480.29 to $527.03) and a loss of $1.63 (Range: -$1.03 to -$2.00). Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

Medicenna (MDNA – $0.63) set up a $10 million At-The-Market facility with Oppenheimer. These sales do weigh on the stock price, but if they are carefully handled they don’t hurt much. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

Biotech MegaShift

Akebia Therapeutics (AKBA- $0.74) got a second interim response from the FDA that it had to change the person reviewing Akebia’s appeal, so a response will be delayed. Sigh. AKBA is a Hold for the results of the FDA meeting on vadadustat.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Vadadustat NDA filed; CRL

Probable time of next FDA approval: Unknown

Probable time of next financing: Unknown

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $149.40) said their Apple Watch can measure heart health features, including high and low heart notifications, cardio fitness, irregular rhythm notifications, an ECG app, and atrial fibrillation history. Researchers, clinicians, and developers are using the watch to study, track, and treat a broad range of conditions.

Bloomberg reported that Apple has a moonshot-style project underway that dates back to the Steve Jobs era: Noninvasive continuous blood glucose monitoring. The goal of this secret endeavor — dubbed E5 — is to measure how much glucose is in someone’s body without needing to prick the skin for blood. After hitting major milestones recently, Apple now believes it could eventually bring glucose monitoring to market, according to people familiar with the effort. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products. And healthcare, too!

Gilead Sciences (GILD – $82.54) said Trodelvy produced both rapid and durable responses for patients across a range of hard-to-treat types of metastatic urothelial cancer, including platinum-ineligible and rapidly progressing, post-platinum metastatic urothelial cancer. Platinum-ineligible patients had 13.5 months overall survival while the rapidly progressing, post-platinum patients had 12.8 months overall survival.

The company also said three retrospective real-world studies covering more than 500,00 COVID-19 patients in 800 hospitals showed which that initiation of Veklury (remdesivir) within the first two days of hospital admission reduced mortality and hospital readmission rates among all patients, regardless of disease severity. A reduction in mortality was also observed in vulnerable populations, such as people living with cancer or HIV. GILD is a Long-Term Buy under $70 for a first target of $100.

Meta Platforms (META – $172.04) announced a paid subscription service for Facebook and Instagram. A Meta Verified blue check account will cost $11.99 a month on the web or $14.99 a month on iOS. The subscription lets users verify their account with a government ID, get a blue badge, get extra impersonation protection against accounts claiming to be them, and get direct access to customer support. It’s launching in Australia and New Zealand this week ahead of a wider rollout.

The Silicon Valley rumor mill is saying Meta will announce more job cuts in March, probably in the middle management layers that Zuck talked about removing to streamline decision making. The payroll savings could be even larger than with the first round of cuts.

Meta seems to be launching a competitor to Discord via its planned “Broadcast Chat Channels.” And while Tencent is cutting its VR hardware program (they’re too far behind), McKinsey have called the metaverse a more than $1 trillion market opportunity. Meta will be a – maybe the – leader. META is a Buy under $150 for a $400 target in 2024.

Other Tech

QuickLogic (QUIK – $5.74) reports December quarter earnings Monday after the close. Wall Street expects $4.33 million in sales and a five cents per share loss. For calendar 2023, the Street is forecasting sales up 36.8% to $22.47 million and a five-cent profit. Management is likely to guide higher. And why is this stock selling for less than 3.5x sales? QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets and wearables.

Primary Risk: New sensor hub competitor emerges.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $4.55) reports their December quarter Tuesday after the close. The consensus is looking for $49.24 million in sales and a seven-cent loss per share.

The new investor relations guy gave a good fireside presentation at the Cowen Aerospace/Defense & Industrials Conference (AUDIO HERE). He said the market for systems and components is larger than the $10 million to $20 million launch business. Eventually, Rocket Lab wants to own some of its own satellites – first time I’ve heard that.

Rocket Lab was named again to Via Satellite’s 10 Hottest Satellite Companies list. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Velo3D (VLD – $3.21) reports December results next Thursday after the close. Expectations are for $25.93 million revenues and a loss of 13¢ per share. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,832.00) held up pretty well despite the broad-based selloff in assets and bonds over the last week:

Click for larger graphic

Click for larger graphic

The same is true over the last five years, which included vastly different macro dynamics while the dollar has been essentially flat.

Click for larger graphic

Click for larger graphic

Gold broke down below the 38.2% retracement level at $1,842 and was rejected each time it tried to get above that level. That’s not good, especially with such a large load of fractal energy to power a big trend. The next couple of weeks will be critical for gold.

Miners & Related

Coeur Mining (CDE – $3.01) reported December quarter revenues up 1.1% from last year to $210.11 million, beating the consensus for $204.82 million. But the pro forma loss of six cents a share missed the four-cent loss estimate. They had solid production results, particularly from the Rochester mine.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said inflationary pressures on key consumable costs hurt their profit margin.

Coeur expects 2023 gold production of 320,000 to 370,000 ounces and silver production of 10.0 to 12.0 million ounces. That’s driven by strong expected second half silver and gold production increases from the planned ramp-up at Rochester plus higher expected gold production from the Wharf mine.

They continue to drill aggressively.

Click for larger graphic

Click for larger graphic

And it’s been successful. Proven & Probable gold reserves increased 12% from last year and silver reserves increased by 3%.

Click for larger graphic

Click for larger graphic

Coeur has $62 million in cash but total potential liquidity of $504 million, if needed.

Click for larger graphic

Click for larger graphic

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $4.80) reported their December quarter and full-year results. In 2022 they had a record 82,376 attributable gold equivalent ounces, up 22.0% from 2021. Revenues grew 29.4% to a record $148.7 million. They had record cash flows from operating activities of $109.8 million and record net income of $78.5 million, up over 180% from 2021. Their average cash cost per attributable gold equivalent ounce was $284, resulting in cash operating margins of $1,511 per ounce.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), they forecast attributable gold equivalent ounces for 2023 between 85,000 and 100,000 ounces just based on their existing royalties. They expect attributable gold equivalent production to be approximately 140,000 ounces in 2025.

Click for larger graphic

Click for larger graphic

CEO Nolan Watson said: “When I look at our potential acquisitions, there’s only one small gold stream that we are looking at, which we could do without raising any equity. And outside of that potential gold stream for which I believe the probability of landing is low, we plan on aggressively paying down our debt so that we can both save on interest, but also so that over time, we can recharge our balance sheet. If 2022 was the year of aggressive transformation, I think 2023 and perhaps 2024 will be the years of calm consolidation, where we take time to pay down our debt.”

Sandstorm is valued at 90% of its net asset value. Its two mid-tier royalty competitors are Osisko (OR) at 120% of NAV and Triple Flag (TFPM) at 125% of NAV. SAND is well-run with excellent, growing assets, plenty of liquidity, and it’s cheap!

The Chief Financial Officer did an interview on how Fed tightening may lead to more resource sector mergers and acquisitions.

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $23,983.62) is consolidating its recent move from the $22,000 area to over $25,000. As we’ve seen many times before, these consolidations take time and may even include a quick drop-and-recovery to the $22,000 level.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

The Grayscale Bitcoin Trust (GBTC- $11.89) now holds 0.00091017 bitcoin per share worth $21.78 per share. The Trust closed at $11.89, a 45.4% discount. GBTC is a Strong Buy at this large discount to net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $75.67

Oil fell almost $3 since last Thursday due to the continued build in crude inventories. They’re up 55.431 million barrels so far this year, although the total liquids stockpile remains low whether you are looking at it including the Strategic Petroleum Reserve or not.

h/t HFI Research Click for larger graphic

h/t HFI Research Click for larger graphic

Total liquids are up because of crude. Gasoline, distillates, and jet fuel are very low going into the global refineries maintenance period and driving season.

h/t HFI Research Click for larger graphic

h/t HFI Research Click for larger graphic

China really is reopening and Morgan Stanley raised their 2023 oil demand growth estimate by 36%, from 1.4 million barrels a day to 1.9 million bpd. They cited growing momentum in China’s reopening and a recovery in aviation – “Mobility indicators for China, such as congestion, have been rising steadily,” while “flight schedules have firmed-up the outlook for jet fuel demand.”

In the US, the Strategic Petroleum Reserve has been cut in half from its high down to 346 million barrels, its lowest level since August 1983. President Biden will release more of the Reserve starting April 1. Russia plans to cut oil exports from its western ports by up to 25% in March versus February. This is a 1800 from the other day when they announced that March exports would remain the same even with the 500,000 bpd production cut. The world is about to experience an oil shortage and $100+ oil.

The July 2026 Crude Oil Futures (CLN26.NYM – $65.43) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.87) is a Buy under $36 for an $80+ target.

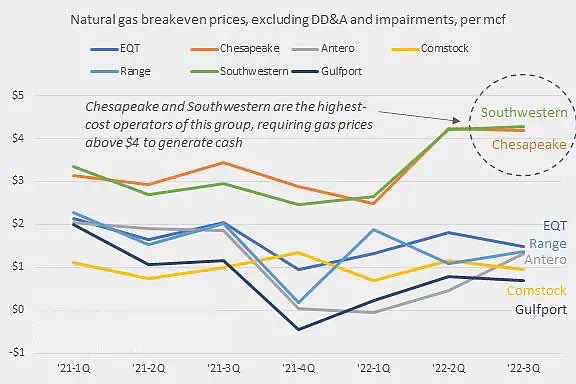

EQT (EQT – $32.49) will benefit as Chesapeake Energy (CHK), the second-largest producer of natural gas, plans to reduce production due to low prices. As I showed you in the February 9 Radar Report, Chesapeake is a high-cost producer. EQT is fine.

Click for larger graphic

Click for larger graphic

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

Click image

Click image

* * * * *

* * * * *

Your always learning more Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.66) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $1.36) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $8.57) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $1.32) – Buy under $7, hold a long time

Invitae (NVTA – $2.08) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.63) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.50) – Buy under $3, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $16.45) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $149.40 ) – Buy under $150 for new iPhones

Corning (GLW – $34.70) – Buy under $33, target price $60

Gilead Sciences (GILD – $82.54) – Buy under $70, target price $100

Meta (META – $172.04) – Buy under $250, target price $400

SoftBank (SFTBY – $20.51) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $41.82) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $14.74) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $29.56) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $5.74) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.55) – Buy under $13, target price $30+

Velo3D (VLD – $3.21) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Hold

Bag of Junk Silver – ($21.32) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $23.63) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $27.47) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.09) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $26.70) – Buy under $30, target price $50

Coeur Mining (CDE – $3.01) – Buy under $5, target price $20

First Majestic Mining (AG – $6.80) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.31) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.80) – Buy under $10, target price $25

Sprott Inc. (SII – $36.71) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $24,470.21) – Buy

Grayscale Bitcoin Trust (GBTC – $11.89) – Buy

Ethereum (ETH-USD – $1,649.31) – Buy

Grayscale Ethereum Trust (ETHE – $7.54) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.86) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $26.75) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $14.94) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $30.03) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.84) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.10) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $65.43) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.87) – Buy under $36; $80+ target

EQT (EQT – $32.49) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.62) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $1.42) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.74) – Hold for FDA decision

Arch Therapeutics (ARTH – $3.53) – Hold for buyout

Graphite Bio (GRPH – $2.55) – Hold until they resolve the clinical hold

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Does anyone know why I have an entry in my TD Ameritrade account for a small amount of money shown as a proceed for GBTC on 12/31/2022? I have not sold any of my small holding of GBTC. I ask because I am starting my taxes using TurboTax and it does not know what to do with this small proceed since I have no actual sell date because I have not sold any shares. Thanks for any insight you can share with me.

There are now a lot of ways they charge for fees. In this case, there is likely some sort of end of year payment for some small even ant up for the tax year disbursements. Usually this will show up somewhere in your statement. Forexample you may get issuance of some stock (might be a spinout) You part calculates with some partial shares in additions to whole shares exactly. So you get credit for XXX.YYY shares where YYY is a partial share which get pait to you with a the fraction part as CASH (say 225,31 shares where $..31 is taxable into last year.

Looking at their web site might sho you how to that on the statement for that year. If you can;t find that contact the brokers help file for the details. You will eventually get the years tax revenue forms.

Two bad for once

Michael M, you don’t pick good stocks anymore. For the original Cal Tech Letter guy, picks like AAPL and META are so pedestrian and have not worked for you. Biotechs are just biowrecks. How about going back to doing some research on cutting edge small – medium cap technology stocks? Big new trends in AI, haptic technology, etc. Remember the term 10 bagger? Time for your thinking to go back to the future!! Good Luck.

Bill D.

Well said Bill,so many of us are down significantly from the mm recommendations,hopefully mm sleeps as well as I do,nvta down over 80 percent or more from his recommendation to buy up to 50 dollars a share,I was a guible follower ,now that I know he didn’t purchase that high,all he kept saying was Sean George was doing everything right,I for one helped pump this disaster up,all we can do is hope for a short squeeze after the earnings come out to halt this piece of from dropping further,you don’t need a college degree to pick losers like this

Hey Bill, on the bright side nvta only has to go 20 to be a 10 bagger. This is as bad as arth,have agreat day..

“Biotechs are just biowrecks.” TRUE. Keep in mind that narrow focused treatments are just bandaids which don’t address the root causes of disease. Maybe Medicenna will have the best cytokine platform. Who knows? These academic theoreticians are fools if they think they can outwit Mother Nature. I have seen this phenomenon many times. Dealing with menopause, a drug called medroxyprogesterone was considered to be a valid proxy for natural progesterone. The WHI trials of 2002 claimed that hormone replacement caused increased breast cancer and heart disease. But that was using medroxyprogesterone, not natural (real) progesterone. But medroxyprogesterone causes vasoconstriction of the coronary arteries, opposite to natural progesterone. These foolish academic physicians indoctrinated doctors in the field to believe that medroxyprogesterone is the same as the real thing–natural progesterone. This is indoctination coming from Big Pharma to doctors who have forgotten their basic biochemistry knowledge. But I could show a child the structural formula of the 2 versions, and he would easily recognize the difference. It’s as simple as seeing the difference between a square and circle. This young child knows you can’t put a round plug into a square whole, and has more intellectual honesty than most researchers for Big Pharma.

The best of NWI bios, TGTX has a lymphocyte depleting drug for MS. It is likely after a few years of followup, this immunosuppression will lead to increased rates of cancer, worse prognosis for covid, etc.

The pure tech companies like VLD have some hope, but be suspicious of all spec bios.

TGTX–a hit piece today on Seeking Alpha. Probably FUD (fear, uncertainty, doubt), but it illustrates alternate views of the prospects for this new drug. Don’t buy at these prices. FUD could get the stock to correct to $10 or so.

QUIK–MM said, “And why is this stock selling for less than 3.5x sales?” The reason is that they still haven’t shown a profit after several generations of new products. Promises and excuses, BS so far. The P/S of 3.5 would be fair value if they had stable profits. At this stage, if profits don’t materialize as now promised, the P/S could fall to 1, with a further 70% decline in the share price over 1-2 years.

“Dilbert” dropped by Washington Post, others, after cartoonist’s racist rant:

https://www.washingtonpost.com/media/2023/02/25/scott-adams-dilbert-canceled/

That guy is off the rails. Wow. I believe MM was a fan of Adams.

If the stars align and we are lucky we may be able to sell NVTA, INO, VLD, ARTH and GRPH with what we have invested in them. VLD may be able recover to $10 but there is no news that seems to get investors excited. The rest look like a haircut to me.

Y’all might want to take a look at NAT, a stock I have followed for years and re-purchased last year. NAT owns and operates 19 Suezmax tankers with 15 of them rented out at spot market prices and 4 longer term. After 2 years of steadily losing money and cutting their quarterly dividend to a penny, in December they raised it to 5 cents and said they expected to pay a 10 cent dividend in March. I poured more money into the stock in January when shares were priced below $3. This morning they announced the March dividend will be $0.15. This quarter they are charging even higher daily rates than last quarter with most of their short-term rates averaging over $60,000 per day per chartered vessel and operating expense of about $8000 per day. This is mostly attributable to Russia’s attack on Ukraine and the re-opening of China. How long will these earnings stay high?

“the supply of Suezmax tankers will remain at historic low levels for at least the next two or three years. Only 14 new ships are currently on order, representing only 2% of the existing fleet. This is a 30 year low. Environmental regulations, increased steel and production costs, and higher interest rates make investing in new ships challenging. A small order book for new tankers has always been positive for our industry.”

So if they keep paying 15 cents a quarter or 60 cents per year, at today’s closing price of $4.25 (up 11.8%) the dividend yield will be 14.12%.

And you can sell options against your shares 😉

All because 60 percent of the US production of natural gas is being shipped to Europe via tankers. China is preparing to provide “lethal support “ for Russia’s war in Ukraine. Meanwhile, Joe, is promising lethal action if they do. Can you see WWIII in sight? Japan’s Fumio Kishida is raising its country’s wages and stoking worldwide inflation in his aftermath. Joe finally admits that inflation is a bigger hemorrhoid on Powell’s little hinny than he previously anticipated as he was spending 31 TRILLION of our great grandchildren’s future incomes!! Get a clue at the Oval Office. It is NOT going away with the FED raising rates until interest rates are HIGHER than the inflation rates. And Powell knows that if he does that he will break something. So here we are. IMO

NAT’s tankers are for petroleum, not gas. China and Russia are doomed by their demographics.

Thanks for NAT info. Unfortunately, it is selling at a high, and its recent parabolic rise will correct. With no earnings, too much optimism is reflected in the stock price. Dividends are a way to mislead investors. A company pays the dividend, but the share price goes down by that amount, so net asset value is unchanged. It is just a ploy to mislead investors who don’t understand elementary math. And dividends are taxed at higher rates, but long term capital gains tax rates are lower. Buffett said to invest in top quality companies that don’t pay much dividends, going for long term capital gains.

When’s the JGND newsletter starting? I will subscribe.

JGMD. Sorry.

I support Joe’s response to Putin’s war on Ukraine. Time to step up boys and meet the aggression with lethal force. Don’t want to follow in Nevelle Chamberlain’s footsteps. We have already seen this show and can only prevent WW3 with a unwavering show of force which is all this guy will understand.

Thanks, Chris a real nice 50% gain and that Y’all reminds of Mississippi.

Man, this board has died. RIP

i miss last year’s rambunctious, say it as it is, Michael. You have been mellow this year. What’s up?

Apparently the author has bailed on this newsletter. All his picks have been a disaster. Nothing to see or invest here.

Plus Everybody is shell shocked after the beating we took in 2022.

Earnings are out for nvta,he’ll of an improvement,could be the start of a turnaround,did jump on a few shares,good luck all ,have a nice day

Down 17%. This is a 70% wipeout for me. Fortunately it’s only a few shares. Another MM disaster.

You and I both Micheal,what a f. King disaster,held too many shares ,won’t buy another recommendation from this newsletter though he has failed

Count me as the third member of this latest NWI disaster. NVTA – The Amazon of genetic testing? Yeah right.

More like the Napster of genetic testing.

Another terrible equity raise. Deerfield got MM on one years ago too. Can’t remember if it was Arena or Dendreon. These guys go max short and then cover on the back end with a private placement or some hideous convertible with the company. I don’t know why they fall for it every time. They should at least squeeze their nuts first.

MM- why the massive and awful dilution for NVTA? Can you break down this deal with your old friend Deerfield? I thought no financing was needed.

I agree with Michael. MM picks have been horrible. No consistent winners in 5+ years resulting in a dead comments board.

MM needs his mojo back!

SCYX +25% anyone find news as there an outbreak somewhere?

Samuel,it looks like guggenhiem upgraded scyx with a buy rating and an 8.00 price target today,hope that answers your question,have a great day

thanks

NVTA- Huge collapse today. Waiting for MM to comment on what may be causing it. Anyway, I dodged that bullet, do not own at present.

Unfortunately I do own VLD which is also having a very rough day. I suppose tomorrows’ EPS report could be the reason. Not a favorable environment for MM’s small caps.

I am looking for an entry point on VLD. Do they have a sufficient number of customers?

Well they have SpaceX which makes it worth a flyer IMO. Very small investment as this is a nasty environment for spec stocks.

VLD- The stock has done very well since the bottom in December at $1.50. It sort of preannounced a good quarter and traded near $4. It is correcting since then and it is hard to say how it will handle the actual news after the close. All of these microcaps are suffering in this stagflationary environment with a very hostile Fed. Continuous declines in Bonds and higher rates are making investing in anything a losing proposition until the Fed changes direction. Not to mention the very high geopolitical risks, with China dumping its US Treasuries holdings.

Great day for AXON .. formerly TASR. They have built a moat around their police cams and the government funding just keeps coming on and on. Now my largest position. ENPH is another fantastic company that is hitting it on all cylinders.

MM picks Oil over solar. Way behind the curve for a supposed tech newsletter.

META: Not a fan, but when you get a couple US Senators writing a letter to you asking you not to sell your product to kids, you know you have a high-demand gizmo.

The new Radar Report for 3.2.23 is posted.