Dear New World Investor:

Well, the Fed finally broke something. This morning, Yahoo Finance wrote: “The once-difficult job now facing Federal Reserve chair Jay Powell and his central banker colleagues just became a seemingly impossible dilemma — continue its fight against inflation by raising rates and tightening credit markets even further or battle a new banking crisis that poses systemic risk.”

I call BS. There is no “systemic risk” because the Fed or the ECB is totally able to bail out any overleveraged banks without impacting inflation a bit. The idea that Chairman Powell will not raise the Fed funds rate another quarter- or half-point next week is just Wall Street trying to suck in latecomers to the rally by shorting stock to them this week and covering lower next week. Gotta pay the kids’ summer camp bill!

There is no doubt the banks have substantial unrealized losses in their Treasury notes and bonds. But I’ve seen this game before. Four or five major banking crises ago, I did a detailed analysis of the big banks’ balance sheets and could show they were all broke. I recommended shorting the worst of them. During a lunch with my first Director of Research, I presented my work and he said: “Yeah, but the Fed will never let major banks fail.”

He was right. The Fed simply changed the rules to allow banks to carry their losing assets at cost, the bank stocks rallied, I covered all my shorts at a loss, and life went on. The Fed literally is owned by the banks – do you think they want to go out of business?

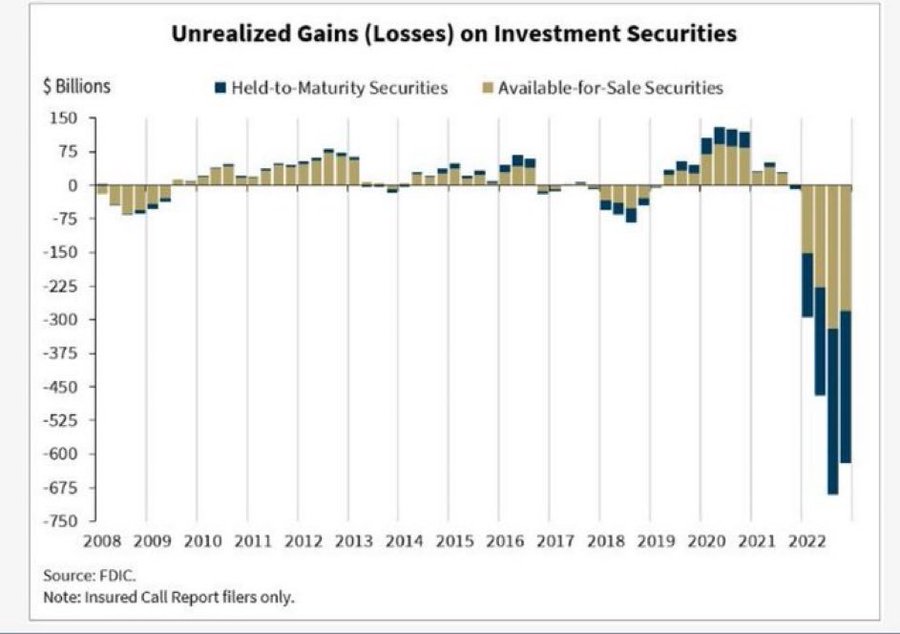

Yes, there are a lot of losses to paper over. FDIC Chairman Martin Gruenberg profiled the banking industry last week. He highlighted the following chart, showing banks’ unrealized losses:

Click for larger graphic

Click for larger graphic

Everyone wants their money right NOW to move to higher-yielding money market funds. Bank deposit rates are too low, so there is a slow-motion run on the entire low-yielding banking system. This is especially true of small/regional banks.

The fix is simple – raise deposit rates to attract capital. That stops outflows as bank deposit accounts are again competitive with other higher-yielding options. If they raise deposit rates enough, it could even reverse the flows back into banks.

Sure, raising deposit rates hurts banks’ profitability, but it’s better than selling bonds and realizing massive losses. Banks have about $652 billion in unrealized losses, up from only $3 billion a year ago. But most banks are not facing a solvency problem. They didn’t lose money on bad loans. They are facing liquidity/profitability problems that are easy to solve.

Silicon Valley Bank was different. They did lose money on bad loans, although they may not have booked those losses yet. We know this because it is proving to be very difficult to sell a lot of those loans. “What am I bid for this loan to a software company with no hard assets that makes the 27th most-popular dog-walking app in Southern California?”

Crickets.

Meanwhile, in the real world, inflation is going in the direction the Fed wants, but slowly. The slowdown in the housing market finally is starting to affect rents, although Tuesday’s Consumer Price Index data for February showed housing costs accounted for the majority of inflation pressures in the economy last month. The shelter component is one-third of the CPI and rose 0.8% from January and 8.1% from last year.

The headline CPI was up 6% year-over-year, its lowest increase since September 2021, and 0.4% month-over-month. Core inflation, excluding food and energy, was up 5.5% from last year and 0.5% from last month. The shelter category accounted for over 60% of the total increase in core inflation.

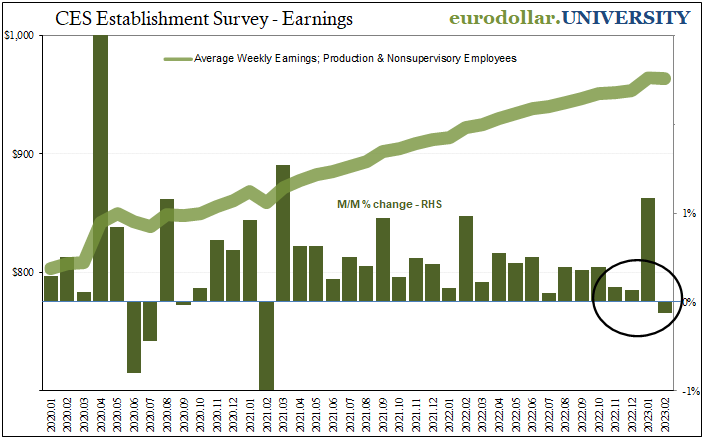

We know that Chairman Powell also is watching the payroll data. Last Friday’s February jobs print blew past expectations yet again with 311,000 new jobs, less than January but way more than the 225,000 jobs expected. However, weather boosted payrolls by about 65,000 in February, and Powell knows it.

Another important factor in February payrolls was average weekly earnings, which grew the least in a year and actually fell compared to January. That’s highly unusual for the past five years. Monthly declines only happened five prior times during those years – three of them in the 2020 lockdowns. It could just be a blip or, like hours worked, it most likely is an indication of the start of a cyclical turn.

Click for larger graphic h/t @JeffSnider_AIP

Market Outlook

In spite of (or maybe because of?) the bank drama, the S&P 500 added 1.1% since last Thursday, bouncing off the 3850 level yesterday. The Index is clinging to a 3.1% gain year-to-date. The Nasdaq Composite gained 3.3% as technology caught a bid. It is up 12.0% for the year. The small-cap Russell 2000, in contrast, dropped 3.0% and is barely up 0.6% in 2023.

The fractal dimension still is consolidating at high levels. If stocks can continue to climb, it will quickly turn into a major trend up.

Top 5

Changes this week: None

Near-Term – chronological order

EQT EQT – cold March

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is moving up quickly

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model is now estimating +3.2% for March quarter real gross domestic product growth. That’s still far above the Blue Chip consensus of 0.9%, but at least the consensus finally is moving up. Wall Street still is going to be surprised by the strength when the first estimate is announced on April 27.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, March 20

Spring Equinox – 5:24pm

Wednesday, March 22

Fed meeting – 2:00pm – Press release; News conference at 2:30pm

ACRDF – Acreage Holdings – After the close – Earnings release; call tomorrow

Thursday, March 23

ACRDF – Acreage Holdings – 10:00am – Earnings conference call

APTO – Aptose Therapeutics – 5:00pm – Earnings conference call

Friday, March 24

Short Interest – After the close

The $20-For-$1 Stocks

None of our stocks had any significant exposure to Silicon Valley Bank, and none lost any money as a result of the bank’s failure.

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Aptose Biosciences (APTO – $0.56) CEO Bill Rice gave a fireside chat at the Oppenheimer Healthcare Conference ( VIDEO HERE). They have completed the dose escalation part of the Phase 1/2 trial of tuspetinib in acute myeloid leukemia (AML) patients that have failed numerous therapies with some complete responses and a remarkably good safety profile.

They are directing tuspetinib development towards an accelerated approval path with a single Phase 3 trial starting in 2024.

The competitors offer either highly selective molecules that inhibit one kinase or a dirty kinase inhibitor that inhibits many. The problem with highly selective drugs is they must fully inhibit their intended target – 85% to 100%. That can lead to toxicities in normal cells or the rapid emergence of drug resistance as the cancer cells quickly find an alternative path.

The dirty kinase inhibitors do block many paths, but at the cost of severe side effects.

Tuspetinib is uniquely balanced between the single agents and the dirty kinase inhibitors. It hits a handful of clinically-validated myeloid kinase targets and avoids the others. This is going to be the AML drug – a blockbuster with well over $1 billion in sales. Aptose is very likely to be bought out, probably before approval. APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Compass Pathways (CMPS – $8.68) did an excellent fireside chat at the Oppenheimer Healthcare Conference ( VIDEO HERE) with four members of the management team. They said they’ll enroll 900 to 1,000 patients in their two Phase 3 trials just getting underway. First data from the first trial comes in mid-2024 and from the second trial in mid-2025.

They did a combination study of COMP-360 with SSRIs and there was the same positive reaction they had with COMP-360 alone. They are not worried about bad data due to patients who already are on SSRI therapy.

They finished 2022 with $143 million in cash and have guided for a 2023 cash burn of $85 million to $115 million, so they can get into 2024. But they already are looking at ways to extend their cash runway past the mid-2024 data readout. They are looking at a set of biotech equity investors or debt. I expect a private placement of stock before the end of the year.

Compass is going to be one of the – maybe the only – winners in psychedelic medicine for treatment-resistant depression, and possibly anorexia and PTSD, too. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2023.

Inovio (INO – $1.13) also did a fireside chat at the Oppenheimer Healthcare Conference (VIDEO HERE and TRANSCRIPT HERE) with the new CEO. She said she’s looked at the tremendous amount of data that Inovio has generated over the years to see where they really have a clinical sweet spot, a clear regulatory path, and a promising market. The big advantage of DNA medicines is they generate a balanced immune response – antibody responses, cellular responses, and – crucially – CD8 or killer T-cell responses. That’s really what is causing the viral clearance in their HPV-related indications, the promising data for INO-5401 in brain cancer, and for INO-3112 in head and neck cancer. Those killer CD8 T-cells that are antigen-specific underpin their mechanism of action across those indications.

They are currently in discussions with the FDA about the design of the Phase 3 trial of INO-3107 in recurrent respiratory papillomatosis. It will be a global trial that starts later this year. INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: Mid-2024

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $155.85) won an Academy Award for Best Animated Short Film for The Boy, the Mole, the Fox and the Horse. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences‘ (GILD – $79.85) Chief Medical Officer did a wide-ranging fireside chat at the Barclays 2023 Global Healthcare Conference (TRANSCRIPT HERE). They have a number of molecules in human trials for both HIV-infected patients and HIV prevention. We’ll start seeing lots of data this year,

In oncology, he said the biggest competitor Trodelvy has still is chemotherapy, not any competing drug. Their biggest challenge right now is awareness and getting the caregivers to transition from chemotherapy to Trodelvy. Their next big program is in lung cancer, where we’ll also see data this year. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $204.93) CEO Mark Zuckerberg issued an Update on Meta’s Year of Efficiency that included firing 10,000 more people and canceling 5,000 open job opportunities. Zuck is doing exactly what he should and what Wall Street wants, at least the cutting costs part. He’ll save over $2 billion in costs, representing well over a 5% upside to the consensus earnings estimate. He’s not backing down on the metaverse, which is what I want.

Google killed their Glass Enterprise Edition yesterday, removing a major competitor to Meta’s Ray-Ban augmented reality glasses. META is a Buy under $150 for a $400 target in 2024.

SoftBank (SFTBY – $18.53) was nicked by the Silicon Valley Bank failure not because they had any exposure to the bank but because they are central to the global venture capital ecosystem. That’s silly, and SoftBank said they see little impact from SVB’s failure on its portfolio companies or on its own finances. Most Vision Fund portfolio companies are cash-rich.

SoftBank is selling for a 38% discount to the net asset value of its publicly-traded investments. This is a level that has caused CEO Masayoshi Son to announce large stock buybacks. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Other Tech

PagerDuty (PD – $31.95) reported an excellent January fourth quarter with revenues up 28.7% from last year to $101 million, just ahead of the $99 million consensus estimate. Pro forma earnings of eight cents a share clobbered the two-cent estimate. They had $15.6 million of free cash flow.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said they added 379 new customers last year and now have 68 of the Fortune 100 and nearly half of the Fortune 500. They win because they offer a very fast payback on the cost of their software:

Click for larger graphic

Click for larger graphic

Their “land and expand” sales model is working. They get an initial small order for a specific problem and then the customer finds additional uses for the software.

Click for larger graphic

Click for larger graphic

They have an 85% gross profit margin and as revenues grow they can steadily reduce expenses as a percent of revenues until they are very, very profitable.

Click for larger graphic

Click for larger graphic

They guided April quarter revenues to a range of $102 million to $104 million, or 19% to 22% growth, with pro forma earnings of 9¢ to 10¢ per share. Wall Street was expecting $104.82 million and only three cents a share.

For the January 2024 fiscal year, they guided for revenues of $446 million to $452 million, 20% to 22% growth, and pro forma earnings of 45¢ to 50¢. The consensus was expecting $451.43 million and only 20¢, in a wide range from 8¢ to 34¢. The low end of their guidance was above the highest Street estimate.

Needless to say, Wall Street loved the report and marked the stock up 14.8% today. Don’t chase it, but on any retracement PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Rocket Lab USA (RKLB – $3.96) launched their second Electron from the Virginia launch pad today at 6:38pm. This is a mission for Capella Space. Blast-off is at the 24-minute mark.

RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $2.51) was upgraded by Morgan Stanley to a Strong Buy with a 12-month target price of $27. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Inflation MegaShift

Gold ($1,923.80) broke above its 50-day moving average as nervous investors sought a safe haven from the possible economic impact of bank failures.

Click for larger graphic

Click for larger graphic

Although the fractal dimension is moving in the right direction, it hasn’t dropped below 55 yet to signal a real new trend finally is underway. When it happens, that trend will easily result in significant new highs.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $24,946.60) shot up 18% in 24 hours to over $26,000 after the Silicon Valley Bank follies. Over last weekend bitcoin facilitated about 600,000 transactions, issued 2,037 new bitcoin at a steady and predictable 1.8% inflation rate, and paid miners $43 million for producing 326 blocks. About one million new addresses were generated while banks were closed and the Fed was not needed – or wanted. See how this works?

Click for larger graphic

Click for larger graphic

After bouncing exactly off its 200-day moving average, bitcoin easily cleared its 50dma. That pattern has been the start of some big moves in the last five to seven years.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

The Grayscale Bitcoin Trust (GBTC- $14.05) still is the best way to buy bitcoin. There’s a very good chance they win their lawsuit against the SEC and convert to an exchange-traded fund with no discount. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

International & Other Recommendations

It is important to hold some non-US assets, especially in China.

Acreage Holdings (ACRDF – $0.83) postponed their earnings report to next Thursday due to the time and effort of yesterday’s special shareholder meeting. As I expected (but voted against), the floating shares voted in favor of the merger. We’ll hold our Canopy Growth (CGC) shares until Constellation Brands buys us out. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

Oil – $68.24

Oil was smacked down Tuesday and Wednesday as hedge funds exited their inflation hedges to cover their two-year Treasury note shorts. It stabilized today after Saudi state media reported that the country’s energy minister, Prince Abdulaziz bin Salman, and Russian deputy prime minister Alexander Novak met in the Saudi capital to discuss the OPEC+ group’s efforts to maintain market balance. Another production cut coming?

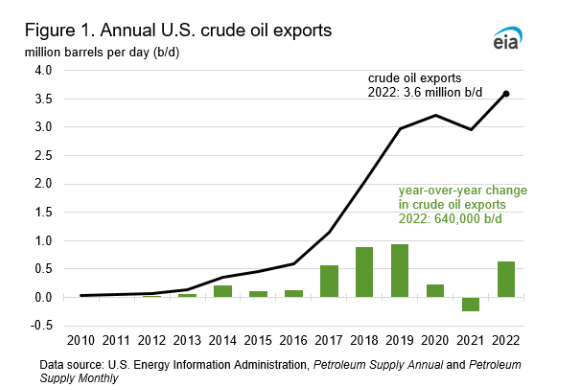

Although the American Petroleum Institute showed yet another weekly increase in crude oil inventories, adding 1.16 million barrels, there were very large product draws: gasoline -4.59 million barrels and diesel -2.89 million barrels. And US crude oil exports increased to a new record of 3.6 million barrels per day in 2022.

Click for larger graphic

Click for larger graphic

The Biden Administration’s decision on Monday to break his campaign promise to ban all drilling on federal lands and approve a massive drilling project in Alaska also weighed on the market, even though it will face legal challenges and we won’t see any more oil from it before 2030, if ever.

Goldman Sachs’ global head of commodities research said that oil prices could climb back above $100 a barrel this year due to rising demand for oil from China while sanctions against Russia will reduce their oil exports. He said: “Right now, we’re still balanced to a surplus because China has still yet to fully rebound.” But he added that by May, the oil market could swing to a supply deficit. And then: “Are we going to run out of spare production capacity? Potentially by 2024, you start to have a serious problem.”

The ever-reliable contrarian indicator of an Economist wrong-way cover story hit this week:

Click for larger graphic

Click for larger graphic

They wrote: “Oil fueled the 20th century—its cars, its wars, its economy, and its geopolitics. Now the world is in the midst of an energy shock that is speeding up the shift to a new order.

“As COVID-19 struck the global economy earlier this year, demand for oil dropped by more than a fifth and prices collapsed. Since then there has been a jittery recovery, but a return to the old world is unlikely.

“Fossil-fuel producers are being forced to confront their vulnerabilities. ExxonMobil has been ejected from the Dow Jones Industrial Average, having been a member since 1928. Petrostates such as Saudi Arabia need an oil price of $70-80 a barrel to balance their budgets.”

The last couple of times The Economist proclaimed the end of the oil age:

Click for larger graphic

Click for larger graphic

The July 2026 Crude Oil Futures (CLN26.NYM – $62.09) have come down with the spot price of crude, but still are above my buy limit. So I am raising the Buy limit to $65 for the $200+ target. Only buy futures for all-cash; do not use margin.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $26.19) is a Buy under $36 for an $80+ target.

EQT (EQT – $30.12) moved up today as US natural gas prices rose 7% on forecasts for demand to rise next week with the amount of gas flowing to US liquefied natural gas (LNG) export plants on track to hit a record high for March. Prices jumped despite forecasts for less cold weather over the next two weeks than previously expected. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $5.30) reported 2022 revenues up 293.7% from 2021 to $12.52 million with a GAAP loss of 38¢ per share. The three publishing analysts are expecting 2023 revenues to grow 238.6% to $42.37 million in a range from $32.2 million to $51.7 million. The one analyst with a 2024 estimate is looking for 140.9% growth to $102.06 million. The per-share loss is expected to drop to two cents this year (in a huge range from a loss of 17¢ to a profit of 44¢), followed by a two-cent profit in 2024.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said they are preparing multiple uranium mines for production and developing enough rare earth refining capacity to power up to one million EVs per year by late-2023 or early-2024.

Click for larger graphic

Click for larger graphic

They are unique in producing both uranium and rare earths.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

The first new nuclear reactor in the US in seven years, Georgia Power’s Vogtle Unit 3 reactor, started up last week. The future of electricity production has to be nuclear.

Energy Fuels finished the year with $75 million in cash and no debt. They also had $38.16 million in inventory valued at cost that has a current market value of $62.48 million.UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

Eric Del Monaco, the former Chief Risk Officer of American Life & Security Co. and the former Head of Global Markets for Natixis Securities Americas, wrote an excellent analysis of the Silicon Valley Bank implosion.

The Real Silicon Valley Bank Bailout

The popular narrative is that Silicon Valley Bank went bust because it owned long-duration assets, mainly treasuries and agencies, against overnight deposits in search of yield. This explanation is far too simplistic and hides what was really going on.

Banks usually hedge all or part of their fixed-rate asset exposure using interest rate swaps. These instruments effectively turn a fixed rate asset into a floating rate asset, thereby immunizing its value from rate movements. SVB apparently used to do exactly this. In fact, according to the latest 10-K filing, in 2021 the notional of interest rate swaps was $10.7BN and in 2022 that number fell to $550MM. The real question is why did they do this?

Hedging would indeed reduce your return; however, it seems unlikely that yield enhancement is the sole or primary driver. For starters, the yield curve has been flat to inverted, so they would have gained little in yield terms for increasing duration.

It appears that the Available for Sale (“AFS”) book only grew by $1.3BN, but the losses swelled by approximately $2.2BN year over year. Given that hold-to-maturity (“HTM”) investments are carried at amortized cost, this does not appear to be a result of new investments in 2022.

All this does indicate that a decision was made to remove the hedges, implicitly betting interest rates would go down. This action is more of a directional bet on interest rates than a stretch for yield. A very curious thing to do given Jerome Powell seemed resolute on the direction of rates as recently as last Tuesday.

For another explanation, you need to look at SVB’s loan book. That’s where the yield stretch really was. SVB wasn’t your typical regional bank. They catered to Silicon Valley and the VC community at large. Based on filings they had a loan book of $74BN. Of which, $41BN was in loans like “capital call facilities” which help private fund managers juice returns through borrowing.

In addition, they had $10BN in private bank loans which were things like high-end real estate mortgages and margin loans against private shares. Yet another $15BN were loans to various types of venture companies. (Those of us who remember “SIVs” from the last crisis, can think of SVB as an SIV for the VC industry with the benefit a federal backstop.)

The real kicker here is that they only provisioned $636MM or 0.85% for losses. This seems impossibly small, especially given the general carnage in the sector. It is no wonder that regulators have struggled to find a buyer as of Sunday night.

It is plausible, if not likely, that credit risk in the loan book is what SVB was really trying to offset all along. They were hoping that as they realized losses on these loans, the Fed would need to ease and cut rates to avoid a recession. They could then take the loan write-downs, which would be offset by a gain on the interest rate bet. All they needed was time. While historically this is exactly what the Fed had done, it now clearly backfired in spectacular fashion.

So here we all are in full bailout mode again, and it is a bailout despite what the Treasury Department says. Given the balance sheet profile of the bank, I find it inconceivable that there are sufficient assets to cover deposits at current values.

The duration mismatch story is a red herring designed to distract the public from what is happening right under our noses. To understand that you need to ask: Who we are really bailing out?

SVB was largely a wholesale deposit bank with some retail deposits which FDIC insurance is designed to protect anyway. The very Silicon Valley customer base that benefited from the aggressive lending SVB engaged in, is by and large the same group of people who started to pull the money out thereby causing the failure. Being lending customers they would be, after all, in the best position to know the financial shape of the loan book.

Now some those same customers want someone else to make up the difference under the guise that it will save the economy from contagion.

SVB is not 150-year-old Lehman with trillions in OTC swaps that entangled the global financial system. Also, given that regional banks can borrow from the Fed’s discount window at will, real systemic contagion is only a possibility to the extent that the others were irresponsible enough to run risk in the same manner.

A solid institution should be able to survive a bank run given modern safeguards. Nonetheless, if that is the case then imprudence has become a systemic risk perpetuated by nearly two decades of bailouts and irresponsibly reactive monetary policy.

The bailout also implicitly assumes that SVB’s customers, the VC portfolio companies, are worth saving. It is unclear that is the case. If so, that determination should be the responsibility the investors in those companies. They should come up with the additional capital, not consumers or taxpayers.

Also, if VC capital is trapped at SVB, they should be forced to explain this astonishing breach of fiduciary duty, or at least oversight, to their investors.

All Americans should be angry over this bailout. It is far worse than what happened at Lehman or AIG. If there ever was a “Bank of the Elites”, Silicon Valley Bank was it. I do not find it credible that the VCs who were hyperventilating about contagion were really worried about the employees at their portfolio companies, and not their private jets.

These fund managers all benefited greatly (and disproportionately) from the upside when rates were zero and average Americans were just getting by. Fair enough, but it is deeply immoral and irresponsible to let them off the hook on the way down, especially as what remains of the middle-class struggles with inflation. Whatever that is, it’s not traditional American capitalism.

The worst part is that this will do nothing to solve the problem. Not only will inflation remain high despite these interventions, it will add fuel to the fire. With the expectation of bailouts, risk-takers will be more aggressive in their perpetual game of chicken with the Fed.

That is not a deflationary dynamic nor does it bode well for long-term financial stability. What it will mean is higher rates and higher inflation for longer, and a lot more pain for all of us who will still fly commercial airlines when this crisis is finally over.

* * * * *

* * * * *

Your studying the US dollar Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.56) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $6.78) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $8.68) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $1.13) – Buy under $7, hold a long time

Invitae (NVTA – $1.39) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.55) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.28) – Buy under $3, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $14.66) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $155.85 ) – Buy under $150 for new iPhones

Corning (GLW – $33.33) – Buy under $33, target price $60

Gilead Sciences (GILD – $79.85) – Buy under $80, target price $120

Meta (META – $204.93) – Buy under $250, target price $400

SoftBank (SFTBY – $18.53) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $40.92) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $16.11) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $31.95) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $5.37) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.96) – Buy under $13, target price $30+

Velo3D (VLD – $2.51) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Hold

Bag of Junk Silver – ($21.82) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $25.51) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $28.85) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.81) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $27.41) – Buy under $30, target price $50

Coeur Mining (CDE – $2.92) – Buy under $5, target price $20

First Majestic Mining (AG – $6.92) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.31) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.36) – Buy under $10, target price $25

Sprott Inc. (SII – $35.27) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $24,946.60) – Buy

Grayscale Bitcoin Trust (GBTC – $14.05) – Buy

Ethereum (ETH-USD – $1,675.22) – Buy

Grayscale Ethereum Trust (ETHE – $7.89) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.97) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $25.46) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $14.23) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $28.95) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.83) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.04) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $62.09) – Buy under $65; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $26.19) – Buy under $36; $80+ target

EQT (EQT – $30.12) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.30) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $0.37) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.71) – Hold for FDA decision

Arch Therapeutics (ARTH – $3.60) – Hold for buyout

Graphite Bio (GRPH – $2.47) – Hold until they resolve the clinical hold

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Numero Uno?

Me two, but only due to typing with one finder.

If you have any smarts, don’t retweet Scott Adams. This guy is a fascist and now is trying to tap dance away from his view for his book.

Racist not fascist. Watch his interview with Chris Cuomo, he lays out all his cards.

Did you watch the video? Looks to me like he is trying to end systemic racism. I’m in favor of that.

Hotep Jesus interview https://www.youtube.com/watch?v=oeFA-n3SMRw

Chris Cuomo interview https://www.youtube.com/watch?v=U_bv1jfYYu4

I think Scott Adams was 100% correct when he said at 9:50 “We’re doing everythig wrong and it’s making me crazy.”

I did watch it. He claimed he was intentionally gaslighting and that his audience and the “blacks” he know knew he was just kidding. Also, claiming that systemic racism starts in the schools is complete nonsense.

He then tried to distance himself from his “get away from black people” statement. Nobody is buying it.

MR. MICHAEL MURPHY

AC5 is approved, not investigational. AC5-G for endoscopic mucosal resection and AC5-V for vascular reconstruction are investigational, but who cares? AC5 is entering a huge market and the next big one is the internal surgery application.

MR. GEORGE PETERSON

Reply to Michael Murphy

Dearest Michael, what are your projections for stock price by the end of this year? In addition, when do you think the internal testing and approval process be completed?

Thank you and GOD Bless you!

George

some positive news at last !

Complete BS. Positive hype, not news. Read my post on the last board.

I think Norchi will either uplist to the Nasdaq National Market or sell the company by the end of this year. The internal trial should start late this year or early next. It’s a small, relatively inexpensive, quick trial. Only one needed to expand the label.

Big Pharma has been looking at ARTH for YEARS. Until significant sales are actually reported, this company is worth ZERO. No, the patents are worthless if they don’t generate sales.

“TG Therapeutics (TGTX – $14.66) – Buy under $7, target price $25+”

MM do you believe TGTX can drop bellow $7? Isn’t TGTX is a buy at current $14.66 price?

It probably won’t go under $7 again, but I’d say Hold instead of Buy until we see how strong the Briumvi rollout is.

On SVB…This is not a political post, just factual…MOST, I repeat MOST ( possible ALL) of the 10 members of the Board of Directors of SVB has either a financial or banking background! This is astounding…What they are mostly are large Democratic donors. Take Garen Staglen, a 10 year member of the SVB Board. He is a winemaker, albeit a very successful one. He donated substantial sums to Democratic politicians including Prez’s Obama, candidate Clinton and Joe Biden, another is a social media “influencer’, and the list goes on…so is there any wonder why the bank made the fatal error of getting upside down off their investments vs deposit yields…Oh and a huge depositor at SVB, who may have broken California law by lobbing Biden and Yellen directly to cover all deposits > $250K ??? None other that Governor Gavin Newsome ! look it up…

Point of correction: Most do NOT have either a financial or banking background.

I have to be honest Mike, this feels very political. And since you had to announce it wasn’t, that most likely confirms that it is.

Snake: But it is totally factual and that was my point.

MM… do you have a link to the Eric Del Monaco piece ?

I’ve not been able to find it.

get the comment thing off my screen

SVB- MM, a very good analysis and explanation of what has happened here. However, I disagree with your expectation of higher rates for longer. Many other institutions are in trouble, look at FRC. So the FED is looking at systemic risks and will inevitably do a 180 regardless of what happens next week when we may have a bi-polar decision of massive cash injections for bailouts while still pursuing QT. So the Fed is done, here comes the cash fire hydrant and hyperinflation.

Long GDX, GDXJ, SA, NUGT.

The cash fire hydrant results in hyperinflation which leads to higher market rates of all time maturities. Then the Fed raises rates to match market rates. J Powell is the reincarnated P Volcker. Agree?

He wants to be Volcker but people weren’t so wedded to the stock market back in the late 70s/early 80s. 401ks replaced pensions over the years so market hits aren’t tolerated anymore and there isn’t the political will to finish the job.

Powell is going to be forced to pivot. Buckle up.

No pivot if more banks are hydrant hosed with printed money, causing hyperinflation.

Pivot is the same as money printing.

Totally agree with your posting. The FED is out of ammo. Powell is paralyzed with fear that if he raises interest rates too high, he will break something else. And rightly so. There are some 200 other banks that are in deep do do. If Powell pivots now or soon, inflation will come back with a vengeance. Just like it did in the 70/80’s and the FED raised rates to 18 percent to finally put it to bed. So he is in a catch 22. Damned if he does, and damned if he doesn’t. Also several vocal billionaires have been fanning the flames of doom and gloom while doing the exact opposite with their own $$$$. Carl Ican , Ray Dalio, Grantham, and Bill Ackman. (Who netted 2 billion in the last few months ) after he publicly called a crash and later shorted the market. Paul T. Jones made some 2.5 million in buys after stating the woes of the markets and causing a sell off.

Sentiment is bad, for good reason. This is not a contrarian buy signal, especially for spec stocks. Would be partners won’t take risks on companies with failed management. Chris has the best picks of the crap spec collection we know about, but they are still risky in this bad political economic environment.

Have to disagree. Sentiment always is worst at the bottom, and extremes of sentiment always are contrarian signals.

If political/economic fundamentals are bad, sentiment is correct and NOT a contrary signal.

Thanks MM – great RR & summary of the SVB crisis.

MM .. looks like I might have been wrong on GBTC. Regardless, BTC ain’t no tulip. I prefer it offline as I almost lost a fortune on the BlockFi Bk ( I happy removed all funds months before when they were offering 8% interest on USDC/too good to be true category).

For everyone else, UCLA will win the NCAA big dance. You read it first here.

NVTA

trying to unravel the terms of this deal with Deerfield. While not dilutive immediately, it sure looks like it will be after 2024. It definitely feels like it already is. The market sure doesn’t like it. Yet Michael you do and maintain a buy under $10 for $50. Please explain the dilution potential and why you think it sets them on the correct path.

I guess zman he is to busy writing is book than to give you the common curiosity of answering your question on nvta as it sinks to 1.20

They had $340 million in 2% converts due in 2024. The new deal replaces 90% of them with 4.5% convertible notes due in 2028. The remaining 10% converts to equity now, plus NVTA sold another $30 million in the new converts.

The 90% or ~$305.7 million that was exchanged for new notes took a haircut to get $275.3 million of new notes, plus 14.2 million shares of stock or roughly 5.5% of the 260 million shares outstanding.

The new notes are convertible at $2.574 per share, a pretty hefty premium. They convert into 118.6 million shares, which is a 45.6% dilution in March 2028 if the company doesn’t buy them back.

Invitae also fully repaid their $135 million senior secured loan, so in total they cut 2024 debt payments from $485 million to $14 million while reducing total debt on the balance sheet by over $165 million.

They burned $510 million in 2022 and will slash that to $250-$275 million in 2023 while growing revenues at low double digits, below their long-term path of 15% to 25% growth. It was the conservative revenue guidance that is weighing on the stock.

I think NVA is doing exactly what Wall Street wanted them to. As they execute quarter-by-quarter, I think the stock will go up dramatically. I still think using genetics to personalize medicine will be a huge winner and Invitae will dominate it.

ThanksMichael

In a nutshell they’ve got almost 5 yearsto demonstrate they desrve a hefty premium over today. If they can dominate in a growing health segment they will deserve a higher stock price much sooner.

One thing that has been an understanding on wealth and inflation over our individual lifetimes. Here are two abreviated format,

And a much higher hourly wage.

Prime number + verbal delusion = bitcoin =ponsi scheme

a typo just above. The price listed as “$0.90″ should read ‘$9.00 plus taxes”.

Sorry, trivia like a few hundred dollars today Is easy to goof……..

Is there any information on BLPH. It’s up 400% in 2 weeks.

People are coat-tailing on the Kevin Tang investment.

That was my thinking when I bought some more on 3/9. Now up 38 percent.

So what is going on with NVTA, VLD, and RKLB plus most other NWI recommendations especially today? WTF ????

Maybe we should just use all of the NWI recommendations to sell everything short?

QUIK also–quicksand. YMB posters say lack of growth in orders despite promises of innovative products. Can’t compete with giants like TXN. Common theme of most NWI spec stocks–Great ideas, lousy execution, pie in the sky hopium.

“On the strength of our numerous eFPGA IP-based opportunities, our sales funnel now is over $118 million, the largest in QuickLogic’s history…The increased diversity of our funnel and the magnitude of the deals makes us confident of exceeding our organic sales growth target of 30% in 2023…we will continue to grow faster than the market, achieving positive quarterly non-GAAP operating income by midyear, as well as annual profitability for fiscal 2023.”

I think Brian Faith is the most underrated CEO in tech.

All talk, but promises of profitability have been broken for YEARS AND YEARS.

Have a look at ACHV. On the quarterly call last week, they said they have results of two major trials coming up in Q2. In the first half of Q2 (by mid-May) they will have results of their Phase 2 trial in e-cigarette nicotine vaping. In the second half of Q2 (by the end of June) they will have the results of their second Phase 3 in cigarette smoking. The first Phase 3 produced outstanding results with minimal side-effects and this trial is identical. They have already begun work on their FDA submission for approval as well as talks with potential Big Pharma partners. I was surprised when the first Phase 3 in smoking cessation didn’t create a bump in price, but maybe that was because everyone knew they still had to do a second.

SCYX – appears to be benefiting a little from recent Candida auris news…

Candida auris fungus spreading in U.S. hospitals – CDC

https://www.reuters.com/business/healthcare-pharmaceuticals/candida-auris-fungus-spreading-us-hospitals-cdc-2023-03-21/

“A little” = +26.3% today.

Original Recommendation: June 23, 2016 @ $21.90

Come on dude. The stock is at 2 bucks.

Mike, how does the approval of Cidara Therapeutics drug rezafungin effect Scynexis going forward, if at all?

It’s a better echinocandin but still just fungistatic – stops it – and not fungicidal – kills it – like ibrexafungerp. It is not effective against candida auris.

Bought more NVTA.

Number one rule: don’t add to losers. Once or if NVTA changes from a double black diamond ski slope to a nike swoosh, I might add some.

So you’re against dollar cost averaging?

Only in investments I believe in .. BTC for example. NVTA has been a disaster.

It has been. But I don’t think it will be in the future. The new CEO is executing beautifully.

Any Views on BLPH ? some action – loss reduced -so should I sell though a loss …

Top-line results of the Phase 3 trial are due in midyear. I expect total success and a filing for approval this year, with approval in 2024. I’m adding it to near-term buys this week.

First Majestic (AG) dropped from $7.44 Monday to $5.53 yesterday before closing at $5.76. The reason? They announced Monday evening they “would be temporarily suspending all mining activities and reducing its workforce at Jerritt Canyon in northern Nevada, effective immediately.

The company said over the past 22 months since it acquired the Jerritt Canyon Gold Mine it has “been focused on increasing underground mining rates in order to sustainably feed the processing plant at a minimum of 3,000 tpd in order to generate free cash flow as our plans suggested.”

However, “mining rates have remained below this threshold and cash costs per ounce have remained higher than anticipated primarily,” citing ongoing challenges such as contractor inefficiencies and high costs, inflationary cost pressures, and multiple extreme weather events affecting northern Nevada.

Keith Neumeyer, the company president and chief executive, said, “the decision to temporarily suspend mining activities at Jerritt Canyon, which represented approximately 21% of the company’s 2022 revenue, was driven by our goal to produce profitable ounces across the company.”

Sounds like a prudent move to me. The weather will change. The out of work contractors will adjust and inflation is dropping. Some of my biggest wins have come from absurdly cheap miners. AG still has the same amount of metal in the ground as they did a week ago and now they will be getting it out of the ground at a lower average cost. Went long AG this morning. On September 27, 2018, Murphy first recommended Buy AG under 6 for a first target of $12, probably in the next 12 months. He was not far off as it hit $12 in December of 2019. As he often does, however, he forgot to hit the “SELL” button when it reached his target. The beginning of the pandemic knowcked it back to $5 and in early 2021 it hit $24. Another great selling opportunity missed. Here, I am buying but will be realistic about selling as it bounces off this solid support and metals prices rise.

So Powell basically said that all money in all banks would be backstopped regardless of the FDIC limit of $250k.

The market says bullshit.

Powell looked like a deer in a headlight today.

Bailing out many banks is ‘MORAL HAZARD.” Ignorant people want bailouts and regulation to save their ass, but this lets banks take on more risk since they know DADDY FED will bail them out. Short term, bailouts make people happy, but long term this leads to more bank failures and more victims. Regulation fails because there aren’t enough regulators to micromanage the financial steering wheel of all the banks and their customers. The only solution is NO regulation but instead, individual fiduciary responsibility.

Contrary to the rest of the tech world which is in the toilet bowl, SMCI (Super Micro Computer) is on fire. My original position went over $10K this week. Up 79 percent over weeks. Just FYI

The Radar Report for 3.23.23 is posted. Sell AGNPF.