Dear New World Investor:

While the unemployment rate remains below 4%, the number of permanent job losses has begun to rise significantly. The latest two-month increase was as steep as in every recession for the last 30 years. Layoffs in higher-paying jobs has been increasing, causing a rise in the loss of permanent jobs. The current headline strength of the labor market has been disguised by the ongoing demand for workers to perform jobs of a lower skill level in hospitality and travel. The overall labor market is not as healthy as it seems.

Click for larger graphic h/t @TaviCosta

Click for larger graphic h/t @TaviCosta

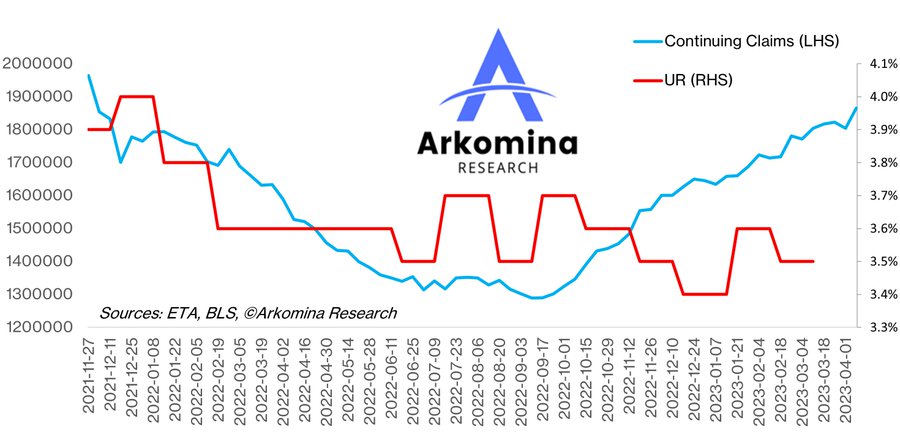

Also, while the Fed keeps talking about the tight labor market, continuing jobless claims reached a new 17-month high of 1,865,000. The last time continuing claims were this high was in November 2021 when the unemployment rate was closer to 4%.

Click for larger graphic h/t @MBjegovic

Click for larger graphic h/t @MBjegovic

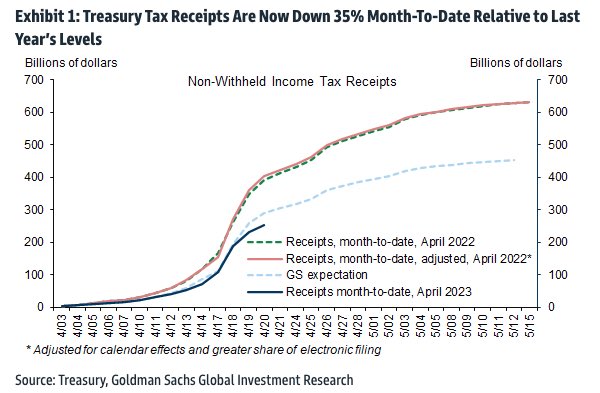

If employment drives tax receipts, why would tax receipts be down this much with employment still strong? California was given a six-month extension for the rains, but that’s not enough to produce such a shortfall.

Click for larger graphic h/t @DisruptorStocks

Click for larger graphic h/t @DisruptorStocks

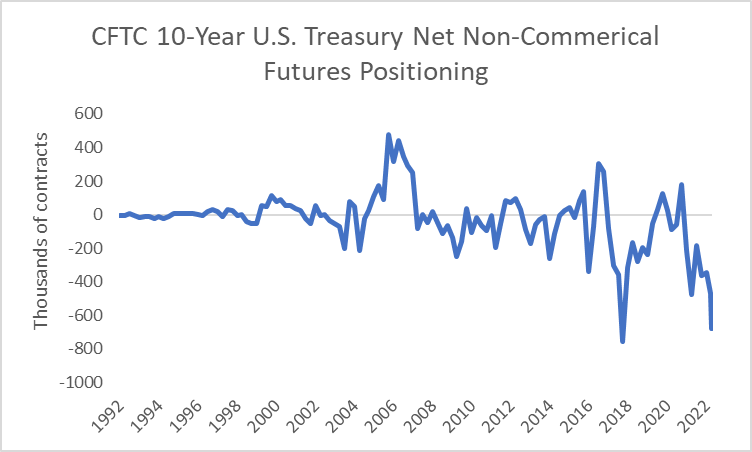

Check out the positioning of hedge fund speculators in 10-Year Treasury futures according to the CFTC’s Commitment of Traders (COT) report. Short bets are at an all-time high as the Fed closes in on ending the rate-hike cycle – exactly the opposite of how they should be betting.

Hedge funds were net long Treasury Bond futures through 2021 and the first half of 2022 – despite the inflationary spike, despite the ending of QE and starting of QT, and despite the well-telegraphed Fed’s hiking policy. That was a terrible trade as long-term interest rates sharply spiked in 2022. Hedge funds were deeply wrong on that trade, as I think they are on this one. T-bonds should rise as interest rates slowly fall.

Click for larger graphic

Click for larger graphic

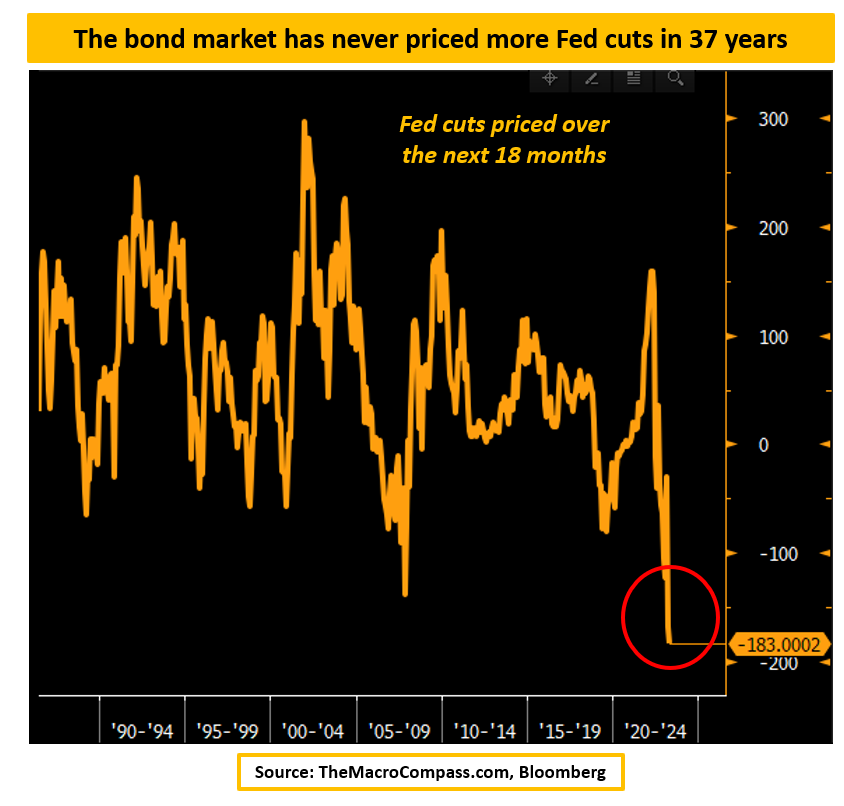

The bond market is pricing almost 200 bps worth of Fed cuts over the next 18 months. This is by far the biggest amount of cumulative Fed cuts the bond market ever priced in over the last 37 years.

Click for larger graphic h/t @MacroAlf

Click for larger graphic h/t @MacroAlf

Market Outlook

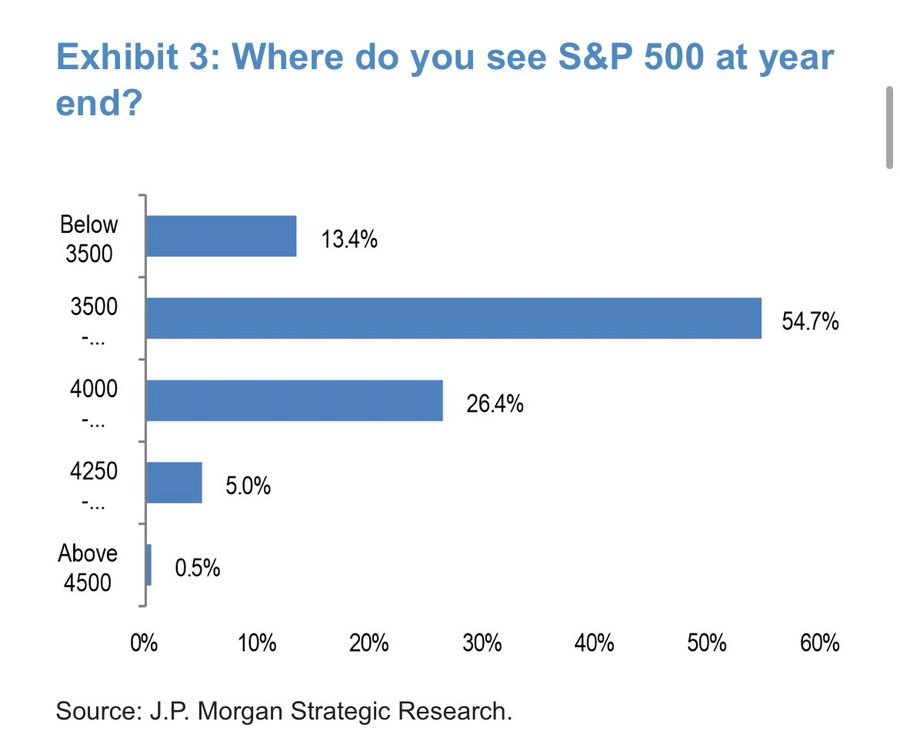

The S&P 500 added 0.1% since last Thursday thanks to today’s rally. The Index is up 7.7% year-to-date. A recent JPMorgan survey showed that most respondents expect the S&P 500 to be at 3500 by yearend. Hardly anyone thinks it will be above 4000.

Click for larger graphic

Click for larger graphic

The Nasdaq Composite gained 0.7% and is up 16.0% for the year. The small-cap Russell 2000 dropped 2.2% and is back to a year-to-date loss, down 0.6% in 2023.

The fractal dimension barely moved last week and still needs a couple of decent up weeks to signal a new uptrend.

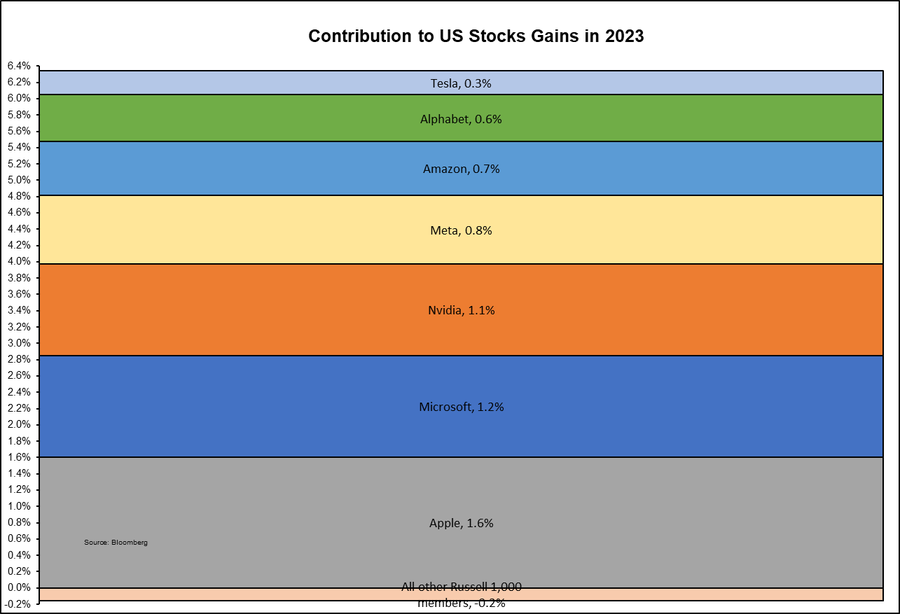

Market breadth is very weak. The top 1,000 US stocks are up 6.2% in 2023. All of these gains came from the 7 platform stocks: Apple, Microsoft, Nvidia, Meta, Amazon, Alphabet, and Tesla. We own two of them. The remaining 993 stocks had a small negative contribution and the next 2,000 stocks also are down. The question is whether the strength broadens out or the market drops.

Click for larger graphic

Click for larger graphic

Top 5

Changes this week: Added ENVX to Near-Term

Near-Term – chronological order

ENVX Enovix –bounce back to ~$13 on coming research reports

EQT EQT –natural gas price rebound

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

BLPH Phase 3 results mid-2023

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

Economy

This morning’s first estimate of March quarter real Gross Domestic Product growth was only +1.1%., well below the +1.9% consensus estimate published by Bloomberg. That continued the slowing trend from +3.2% growth in the September quarter and +2.6% in the December quarter.

The Atlanta Fed’s GDPNow model slashed its March quarter estimate from +2.5% to +1.1% in advance of this morning’s report. They sharply reduced their estimate of personal consumption expenditures growth and gross private domestic investment growth (housing). From the mid-March peak, their estimate plummeted as data came in, even as the consensus was rising..

Click for larger graphic

I think this still is compatible with my shallow recession thesis if the Fed stops raising rates. They may do another 25 basis points (¼ of a percentage point) next week, or they may not, but that should be the end of it. It’s time to pause and let the impact of the past increases work through the economy.

Incidentally, a recession fixes three things that bother investors:

1. High inflation: Sticky, high prices have weighed on stocks. A slowdown would alleviate this.

2. Aggressive Fed rate hikes: Stocks will look more attractive once policy loosens up.

3. Falling productivity: Recessions stop companies from hoarding workers, which improves profit margins.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, April 28

Personal Consumption Expenditures Index – 8:30am – The Fed’s favorite inflation measure

Monday, May 1

VLD – Velo3D – 5:00pm – Earnings conference call

Wednesday, May 3

Fed Meeting – 2:00pm – News release; presser at 2:30pm

FSLY – Fastly – 4:30pm – Earnings conference call

Thursday, May 4

AG – First Majestic – Earnings release, no conference call

AKBA – Akebia Therapeutics – 10:00am – Special shareholders meeting

AAPL – Apple – 5:00pm – Earnings conference call

Friday, May 5

April Payrolls – 8:30am – +181,000 expected vs. +236,000 in March

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $168.41) will report March fourth quarter earnings next Thursday. Analysts are expecting revenues to drop 4.4% from last year to $92.98 billion, with earnings down 5.9% to $1.43 per share.

The company is getting ready to unveil its latest software and hardware updates at its Worldwide Developers Conference starting June 5, which may include their new app designed to aid people’s mental and physical health. It would allow users to track and record their daily efforts, and have access to a user’s texts and phone calls. It will analyze a person’s behavior, understand what their typical day looks like, and offer personalization features, including journaling suggestions. Analysis would take place on the device, continuing Apple’s privacy efforts.

In another of its many mistakes, GM is dropping Apple CarPlay even though it is supported on 800 vehicles, including all of GM’s competitors. GM is going to use a new built-in infotainment system developed with Google. Good luck with that!

AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $32.75) reported March quarter revenues down 9.9% from last year to $3.37 billion, a skotch above the $3.5 billion consensus estimate. Pro forma earnings of 41¢ a share beat the 39¢ consensus. On the conference call (INFOGRAPHIC HERE and TRANSCRIPT HERE), management said: “Last quarter, we told you that markets constituting about half of our sales were experiencing recession-level demand and that our first quarter sales would decline by greater-than-normal seasonality due to pandemic-related disruptions. China – that we would raise prices again to offset additional inflation and also begin to restore our productivity ratios to pre-pandemic levels. And as a result, our margins would increase one to two percentage points sequentially despite lower sales. And that is exactly how the first quarter played out.”

Display Technologies sales slipped 3% from the December quarter as both volume and glass price declined slightly. But they added that volume increased in March as conditions in China improved and panel maker utilization resumed its recovery. They expect volume in the second quarter to increase significantly from the first quarter, in part due to very low inventory levels.

Optical Communications sales decreased 6% sequentially as better pricing partially offset a greater-than-normal seasonal volume decline caused by the pacing of customer projects. That revenue is delayed but not lost. Environmental Technologies sales increased 9% from the December quarter, mostly thanks to increased gasoline particulate filter adoption.

They guided for June quarter sales of $3.4 billion to $3.6 billion, below the $3.6 billion consensus, with pro forma earnings of 42¢ to 49¢ a share, also below the 48¢ consensus. The second half of 2023 should rebound nicely as Display, Optical, and smartphones recover.

GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2024.

Gilead Sciences (GILD – $83.55) reported March quarter revenues down 3.6% from last year to $6.35 billion, right on the $6.33 billion estimate. But pro forma earnings of $1.37 missed the $1.54 consensus estimate.

Total product sales, excluding Veklury, increased 15% to $5.7 billion, but Veklury sales decreased by 63% to $573 million driven by lower rates of COVID-19-related hospitalizations. HIV product sales increased 13% to $4.2 billion, driven by favorable pricing, higher demand, and lower inventory draw-downs.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), they guided for total 2023 product sales between $26.0 billion and $26.5 billion, a bit below the $26.73 billion consensus. That includes total Veklury sales of approximately $2.0 billion, unchanged from prior guidance.

They guided for diluted earnings per share between $4.75 and $5.15, compared to $5.30 and $5.70 previously. Pro forma diluted earnings per share were guided between $6.60 and $7.00, about equal to the $6.84 consensus.

They have numerous data releases coming this year:

Click for larger graphic

Click for larger graphic

In the quarter, they paid $969 million in dividends and bought back $400 million in stock at an average price of $82.29. The stock slipped about 2% in after-market trading. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $238.56) blew away the March quarter consensus estimates. For the first time in a year, revenues were up 2.7% from last year to $28.65 billion. The consensus thought they would be down to $27.66 billion. Thanks to Zuckerberg’s “Year of Efficiency” job cuts, earnings of $2.20 a share clobbered the $1.97 estimate.

Facebook daily active users were 2.04 billion, an increase of 4% year-over-year. Monthly active users were 2.99 billion, an increase of 2% year-over-year.

Family daily active people was 3.02 billion, an increase of 5% year-over-year. Family monthly active people was 3.81 billion, an increase of 5% year-over-year.

Ad impressions delivered across the family of apps increased by 26% year-over-year, offsetting a 17% drop in the average price per ad.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), Zuckerberg said they now expect full-year total expenses in the range of $86 billion to $90 billion, including $3 billion to $5 billion of restructuring costs related to facilities consolidation charges, severance, and other personnel costs. Capital expenditures still are expected to be in the range of $30 billion to $33 billion, which includes their ongoing build-out of AI capacity to support ads, Feed, and Reels, plus an increased investment in capacity for their generative AI initiatives.

They said integration of A.I. helped drive their first revenue increase in three quarters. Reels monetization is up over 30% on Instagram and over 40% on Facebook on a quarterly basis as A.I. plays a larger role in the platforms. Time spent on Instagram went up by 24% since Meta launched A.I.-powered Instagram reels.

Zuckerberg went out of his way to say he is not ditching the metaverse. He said: “A narrative has developed that we’re somehow moving away from focusing on the metaverse division. So I just want to say upfront that that’s not accurate. We’ve been focusing on both AI and the metaverse for years now, and we will continue to focus on both…I think there’s an opportunity to introduce A.I. agents to billions of people.”

“A.I. Agents” are avatars. More than one million Meta avatars have been created. Half of the people who use their Quest VR headset every day spend more than one hour in virtual reality.

We laugh today at the people who said no one needs a personal computer or smartphones would never catch on. In the future, those who thought the metaverse was unimportant will join them. It’s going to change everything.

The company guided for a strong June quarter, expecting revenues in a range from $29.5 billion to $32.0 billion, above the $29.47 billion consensus. The stock was up 13.9% today. META is a Buy under $150 for a $400 target in 2024.

Small Tech

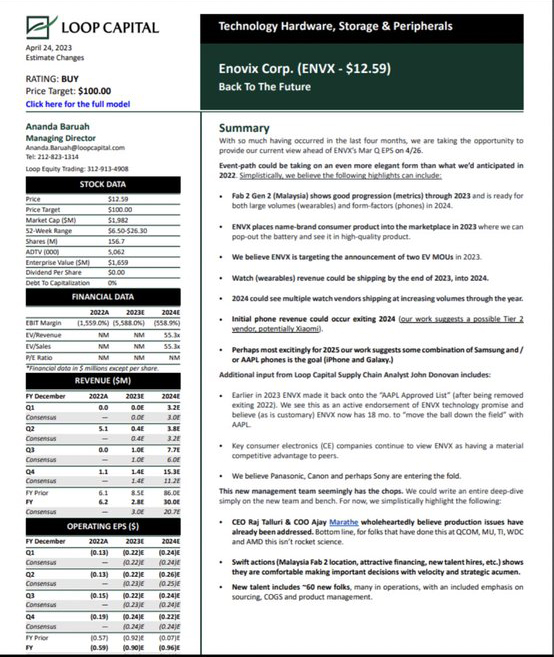

Enovix (ENVX – $10.54) reported a March quarter pro forma loss of 20¢ a share compared to the consensus for a 16¢ loss. The stock dropped 15.7% to $10.54 today. I was waiting to recommend ENVX under $12, but I was worried that if they reported a very good quarter – as they did – it might run away from us. As it turned out, the shortsellers did a great job of knocking the stock down as low as $9.06 intraday. The CEO took advantage of today’s dip to buy 5,000 more shares at $10.10, bringing his total holdings to 2,010,000 shares. I want you to do the same.

On the conference call, (SHAREHOLDERS LETTER HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Raj Talluri said: “We are making substantial progress across all fronts. Fab 1 delivered units above our forecast, and we are moving quickly on Fab 2 in Malaysia with a site selected and are in the process of closing non-dilutive financing to largely fund our first Gen 2 Autoline in Fab 2. We additionally raised $172.5 million of marginally dilutive capital to fund Gen 2 Autolines 2, 3 and 4.”

The made 12,500 batteries from Fab 1 in the quarter, well ahead of their forecast for 9,000. They are forecasting 18,000 for the June quarter. I expect 20,000 to 25,000. They are still forecasting 180,000 cells for the full year. The second-generation production line has a much higher throughput.

Click for larger graphic

Some investors have wondered if the batteries really are manufacturable at high volumes. The CEO said: “If we can do this for chips at the 9-nanometer scale, we can surely do it for batteries at the 50-nanometer scale.” The high-volume Gen 2 production line design approval is done and purchase orders issued.

Enovix Gen 2 Manufacturing from Enovix on Vimeo.

They’ve chosen a site for Fab 2 in Malaysia and hired a management team plus 25 engineers. The Malaysia plant with four autolines will be paid for in a low-dilution way. It will produce samples next April. By the end of 2024 or early 2025, it will produce 36 million to 76 million batteries worth $5 each, or $180 million to $380 million in revenues at a 50% gross profit margin.

I wanted to review Enovix’s customer funnel to show you where they are and how fast they are progressing. The graphic below shows where each customer was at the end of 2021. The horizontal axis shows:

* * ES10 – These customers are buying Engineering Samples to qualify the technology, which takes three to nine months.

* * CS10 – These customers have requested a Custom Sample battery for a specific need, which might be a different form factor or include a special component. This takes six to nine months.

* * QS100 – These customers are buying Qualification Samples, a few hundred to 1,000 batteries to qualify both the technology and the fab (fabrication facility) to test production quality. That process takes four to six months.

* * P1K – These customers are buying a thousand batteries for Product Integration to put in their product and then do extensive quality testing of the final product, not just the battery. This can take three to six months.

* * P10K – These customers are placing Pre-production orders for 10,000 batteries for release (or limited release) of a product for sale. That process takes two to six months.

* * FM$ – this is the First $1 Million order. That process takes four to six months.

The letter is the account code. On the right, you can see that S* is a strategic account and a mega-cap customer. The color denotes whether the application is wearable, mobile phone, laptop/tablet, or other (medical, industrial). On the left, I’ve marked customer S*14. It is Samsung.

Click for larger graphic

Only about 20% of customers will let Enovix name them. As you can see, Canon, Panasonic, Casio, Nintendo, the US Army, Genius (Chinese watch company), and OPPO (Chinese cell phone company) were early customers.

One year later, this is what the funnel looked like at the end of 2022. Enovix went from 43 accounts to 78 accounts, including 21 at or through the qualification phase. That included Samsung and OPPO.

Click for larger graphic

The plan for 2023 is to bring in new customers and move existing customers through the funnel. You can see on the right the color-coded Sales Responsibility of each of their three current salespeople to move customers forward. Customer L05, a wearable, is expected to be their first $1 million order.

Click for larger graphic

They said they are up to 106 customers with a $718 million potential market. The Chief Commercial Officer said: “All the cells we’ve been shipping over the last few quarters are now in qualification and take numerous quarters ’till those qualifications are done. But we’re still on schedule exactly how we thought that in the back half of this year we’ll start seeing customers put products into the market with our batteries in them.”

On Monday, Loop Capital recommended buying ENVX with a $100 target. They said the company is targeting the announcement of two EV customers in 2023. They think Samsung, Apple, or both could announce phones with the Enovix battery in 2025.

Click for larger graphic

Click for larger graphic

ENVX is a Buy up to $13 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

For a quick Enovix introduction, watch this:

Fastly (FSLY – $15.10) will report March quarter results next Wednesday. Wall Street wants to see sales up 13.4% to $116.09 million and the per-share loss cut from 15¢ last year to 10¢ this year. Fastly should be able to beat that.

Morgan Stanley raised their recommendation from underweight to equal weight as better gross profit margins offset “incremental weakness” in cloud infrastructure spending. They added: “In the near term, we expect share gains in Fastly’s core content delivery to continue given Fastly’s performance advantage and large players such as Akamai less interested in competing on price.” FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Rocket Lab USA (RKLB – $3.90) holds a news conference tomorrow to let media people ask experts about the upcoming launch of the TROPICS satellites for NASA. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $2.20) will report March quarter results Monday. Consensus expectations are for revenues up 119.1% to $26.77 million with the loss reduced from 13¢ a share last year to 10¢. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $0.91) held their shareholder information meeting last Friday (AUDIO HERE) to try to persuade more people to vote for their proposed reverse split. Credit to them, they said they realized it might hurt shareholder value. If it isn’t approved, they’ll ask Nasdaq for another extension. I doubt that would be granted. I continue to recommend you vote NO.

As expected, the European Commission granted marketing authorization for Vafseo (vadadustat), for the treatment of symptomatic anemia associated with chronic kidney disease in adults on chronic maintenance dialysis. The approval is applicable to all 27 European Union member states plus Iceland, Norway, and Liechtenstein. Vadadustat is now approved in 32 countries with a decision from the FDA due any day. AKBA is a Hold for the results of the FDA appeal on vadadustat.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Vadadustat NDA filed; CRL

Probable time of next FDA approval: Unknown

Probable time of next financing: Unknown

Aptose Biosciences (APTO – $0.47) filed the proxy statement for their annual meeting on May 23. Proposal #4 is for permission to do a reverse split between 1-for-10 and 1-for-20. As always, vote NO. APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Arch Therapeutics (ARTH – $3.00) is at the Symposium on Advanced Wound Care (SAWC) Spring 2023 meeting through Sunday. This is the first clinical conference opportunity for Arch to present AC5 since the Centers for Medicare and Medicaid Services established the new AC5-dedicated Level II Healthcare Common Procedure Coding System (HCPCS) code, “A2020”, effective April 1. They’ll present two clinical case studies. ARTH is a Hold for a buyout.

Primary Risk: AC5 fails to sell or the internal trial fails.

Clinical stage of lead product: External approved. Internal trial 2023

Probable time of first FDA approval: External done. Internal 2024

Probable time of next financing: March or June 2023 quarter

Inovio (INO – $0.78) got a positive recommendation from the European Committee for Orphan Medicinal Products (COMP) on their application for orphan drug designation in the European Union for INO-3107 for Recurrent Respiratory Papillomatosis. The recommendation now goes to the European Commission, which will provide a final decision on the application within 30 days, around the end of May.

They’ll also present the safety and immunological data from both cohorts of the recently completed Phase 1/2 trial of INO-3107 on May 5 at the American Broncho-Esophagological Association program at the Combined Otolaryngology Spring Meetings (COSM) in Boston. INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: Mid-2024

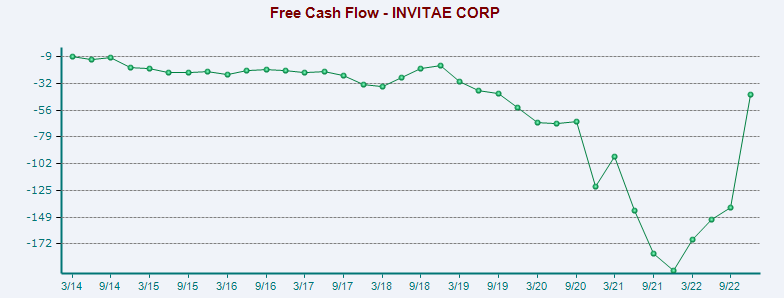

Invitae (NVTA – $1.36) is selling at a 0.5x price/sales ratio with a 40% gross margin and 10% to 15% revenue growth of a critically important product and service to personalized medicine.

Click for larger graphic

Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

Medicenna (MDNA – $0.70) did a fireside chat at the Bloom Burton Healthcare Conference (VIDEO HERE). They have seen tumor control in five of 14 heavily-pretreated patients.

Click for larger graphic

They have several milestones coming this year.

Click for larger graphic

They continue to pursue a partner for MDNA 55. It’s hard to convince Big Pharma to invest in a glioblastoma drug after all the failed programs of the last 20 years, but they are accumulating data on payer reimbursement and other factors. The Phase 3 trial will cost $40 million to $50 million to enroll 150 patients on the drug, 50 on standard of care, and 100 from hospital registry that will not receive the drug. This is the first time the FDA has allowed hospital registry to serve as the standard of care.

Nasdaq granted them a second 180-day extension to meet the $1 minimum bid rule. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

TG Therapeutics (TGTX – $23.33) presented data from the Phase 3 trials evaluating Briumvi in patients with relapsing forms of multiple sclerosis at the American Academy of Neurology (AAN) annual meeting that ended today. They also got their reimbursement code from the Centers for Medicare & Medicaid Services. Under the Healthcare Common Procedure Coding System (HCPCS), the Briumvi J-Code (J2329) will become effective July 1. Hold TGTX for a target price in a buyout of $25 or more now that the MS drug is approved.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Second half of 2023

Inflation MegaShift

Gold ($1,997.50) is consolidating just under $2,000 for what should be a move to new record highs. According to The Wall Street Journal, “How to Buy Gold” hit a Google record as crypto investors chase the world’s oldest asset. They said: “The old-school precious metal has new allure for a generation seeking a respite from the cryptocurrency roller coaster.”

Well, maybe. I think there is substantial buying of gold by OPEC as they sell oil to China for yuan and then quickly turn it into gold. The fractal dimension still shows an uptrend has begun.

Sandstorm Gold (SAND – $5.84) got a good write-up on SeekingAlpha. The author pointed out that Sandstorm has been one of the worst-performing royalty/streaming companies over the past two years, sitting over 30% below its April 2022 highs despite a higher gold price. The underperformance can be attributed to significant share dilution related to two major transactions, a follow-on equity raise that surprised the market, and timelines being pushed at some assets.

However, he said, the company has transformed its portfolio, which seems to be ignored by the market, and 2024/2025 should be catalyst rich with multiple new assets coming online. So, with Sandstorm trading at a massive discount to its peer group (barely 9x the 2025 cash-flow estimate) and gearing up for significant per-share growth after 2024, it is the best value in the royalty/streaming industry. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $29,741.64) dipped below the $28,000 to $30,000 range and quickly snapped back as $113 million of short positions were liquidated. It and gold are both benefiting as safe haven trades, although bitcoin also acts like a risk-on asset and does better when the Nasdaq 100 is rallying, while gold does better when the US dollar weakens.

Standard Chartered Bank said bitcoin could reach $100,000 by the end of this year, as they believe the recent banking-sector crisis helped to “re-establish bitcoin’s use as a decentralized scarce digital asset. Against this backdrop, bitcoin has benefited from its status as a branded safe haven, a perceived relative store of value, and a means of remittance.”

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

The Grayscale Bitcoin Trust (GBTC- $16.44) is at a 38.5% discount to net asset value, which easily makes it the best way to buy bitcoin. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $74.83

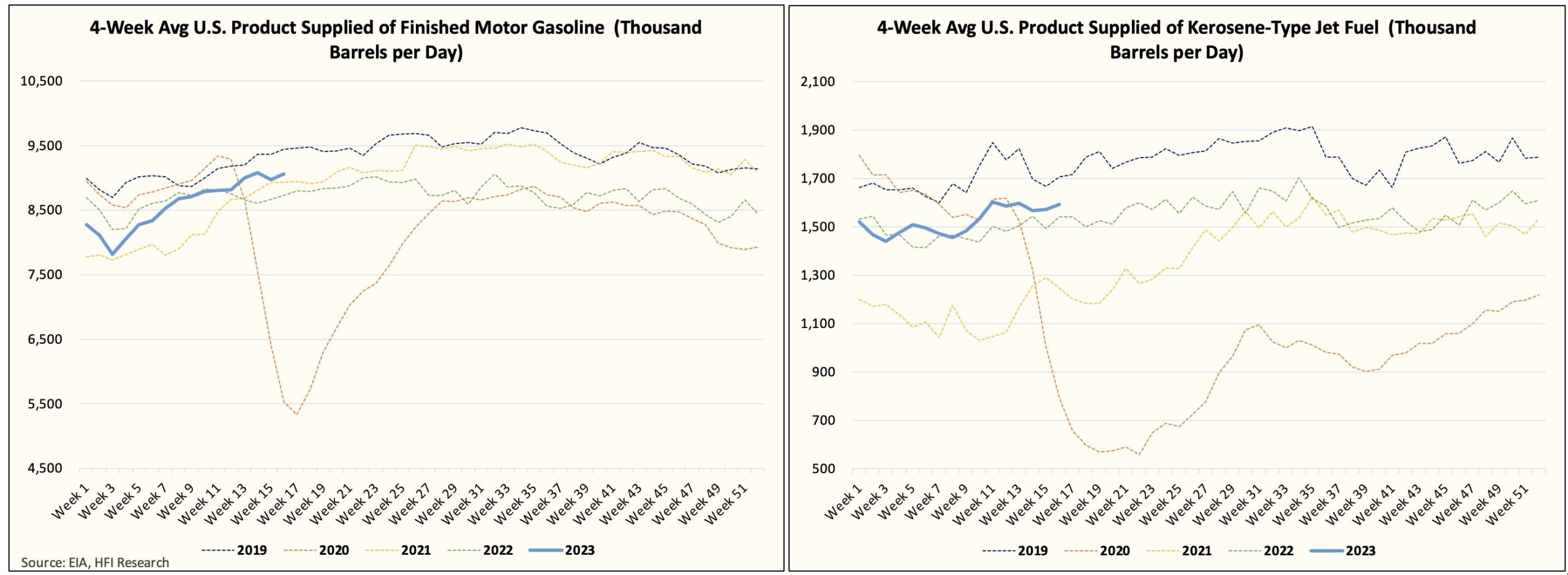

Oil dropped $4 a barrel this week as recession fears outweighed another US inventory draw, even though the physical market is getting tighter and tighter. Energy Information Administration data showing US crude inventories fell last week by 5.1 million barrels to 460.9 million barrels, far exceeding analyst forecasts of a 1.5 million drop. Gasoline stocks fell by 2.4 million barrels to 221.1 million barrels. Distillate stocks also drew down by almost 600,000 barrels to 111.5 million barrels.

US oil demand is much better than meets the eye.

Click for larger graphic h/t HFI Research (full article)

Click for larger graphic h/t HFI Research (full article)

I expect a gradually increasing oil deficit starting in May when the OPEC+ cuts begin.

Click for larger graphic

And after telling President Biden and Fed Chairman Powell to stick it, OPEC now is specifically calling out the International Energy Administration.

Click for larger graphic

Click for larger graphic

Who will win? Well, OPEC has over a trillion barrels of oil reserves – 1,241,820,000,000, to be as precise as possible. The IEA has 0 barrels of oil reserves. Hmm…

The July 2026 Crude Oil Futures (CLN26.NYM – $64.26) are a Buy under $65 – where they are now! – for a $200+ target. Only buy futures for all cash; do not use margin.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.56) is a Buy under $36 for an $80+ target.

EQT (EQT – $33.54) reported March quarter results that solidly beat on the top and bottom lines. Revenues hit $2.66 billion, far better than the $1.77 billion estimate. Pro forma earnings hit $1.70 a share, also much better than the $1.32 estimate. March quarter gas sales of 459 billion cubic feet were 2% above the middle of their guidance range.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said EQT has among the best hedge books of any natural gas peer in 2023 with 62% of their production covered via floors with an average strike price of $3.38 per MMBtu.

Click for larger graphic

They repurchased $200 million of stock in the quarter at an average price under $34. They also retired $210 million of debt at an average cost of 96% of par. They still had over $2.1 billion of cash at the end of the quarter.

They see supplying LNG export plants as a huge opportunity:

Click for larger graphic

The CEO said: “Our free cash flow generation has significant durability and duration with our internal forecast projecting cumulative free cash flow from 2023 and to 2027 of greater than $12 billion at strip pricing and excluding the benefit of Tug Hill [acquisition].

“This equates to more than 105% of our current market capitalization and greater than 80% of enterprise value underscoring the significant value proposition embedded in EQT shares even after the recent decline in strip pricing. Our free cash flow outlook gives us tremendous confidence in being able to achieve our absolute debt target of $3.5 billion pro forma for the Tug Hill acquisition, while also being able to continue to opportunistically retiring our stock via our $2 billion share repurchase authorization.”

EQT is best positioned to weather the natural gas price glut that developed after a key US LNG export facility was shut by a fire and abnormally mild winter weather gutted heating demand. The Raymond James US energy team says a recovery is unlikely prior to 2025. They are modeling $3.25 for 2024.

But the Golden Pass LNG export terminal in Port Arthur, Texas, was expected to start up in the December 2024 quarter, taking 2.3 billion cubic feet of natural gas a day. On their conference call, Range Resources (RRC) said they now expect Golden Pass to be taking feed gas by mid-2024. Antero Resources said the timeline is “accelerated,” EQT said the March quarter. The clear consensus is that Golden Pass is going to be taking feed gas early. This is a big deal because six extra months of Golden Pass operations takes 420 billion cubic feet of gas or 10% out of the 2024 domestic supply.

At the same time, depressed gas prices are pushing drillers to curtail production growth in the interests of cash preservation. Managements will take lower production growth over having to reduce dividends to shareholders. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $5.42) will benefit from rising uranium prices, even though the Sprott Physical Uranium Trust (SPUT) has been out of market for last two months. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $37.47) reported March quarter revenues down 18.3% from last year to $5.39 billion, slightly ahead of the $5.25 billion consensus estimate. Proforma earnings of 52¢ soundly beat the 46¢ estimate. On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said production and sales were impacted by heavy February rains at the Grasberg mine in Indonesia but they achieved a full recovery in March.

First quarter copper production fell 4% to 965 million pounds from 1.01 billion pounds last year due to the lower operating rates at Grasberg. Their average realized price of $4.11/lb compared to $4.66/lb a year earlier, while unit net cash costs climbed to $1.76/lb from $1.33/lb a year ago.

First quarter gold production slipped 2% to 405,000 ounces at an average realized price of $1,949/ounce.

They trimmed their 2023 capital spending forecast from $5.2 billion to ~$5.1 billion, and now guide for full-year copper production of 4.1 million pounds, down from its prior outlook of 4.2 million pounds, 1.8 million ounces of gold, and 79 million pounds of molybdenum, including 1.1 billion pounds of copper, 500,000 ounces of gold and 20 million pounds of molybdenum in the June quarter.

Click for larger graphic

Click for larger graphic

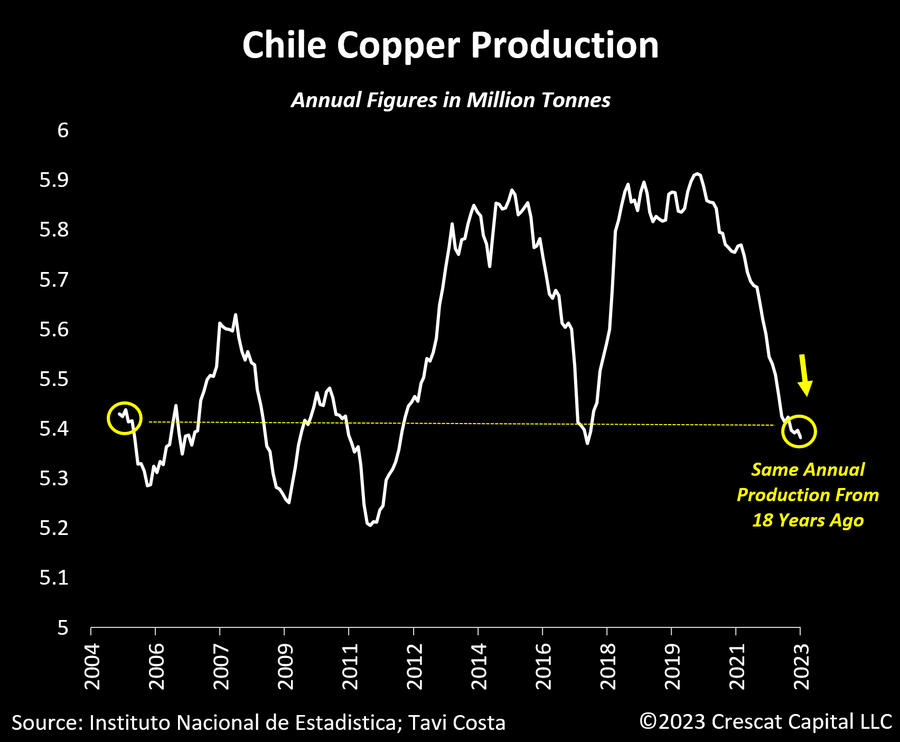

Chile’s overall copper production is currently as low as it was 18 years ago, nearly down 10% from its recent peak. It is important to note that Chile holds a dominant position in the supply of this metal, accounting for nearly 30% of the total global production, akin to the OPEC of the copper market.

The potential transition to a green economy relies on an ample and accessible supply of metals, which is unattainable today. High-grade copper discoveries are becoming increasingly challenging as most deposits found in the last decade are characterized by having low-grade mineralization that would not be economically viable at the current metal prices.

Additionally, the potential nationalization of Chile’s lithium industry raises critical questions about the stability of the country’s copper market, which could further complicate the global supply of this metal. These factors are among the main reasons for such a compelling demand and supply case for copper in the long-term.

Click for larger graphic h/t @TaviCosta

The company expects to return ~50% of free cash flow to shareholders this year. In addition to the 30¢ base dividend, there will be a 30¢ variable dividend, and they have $3.2 billion available in their stock buyback program. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

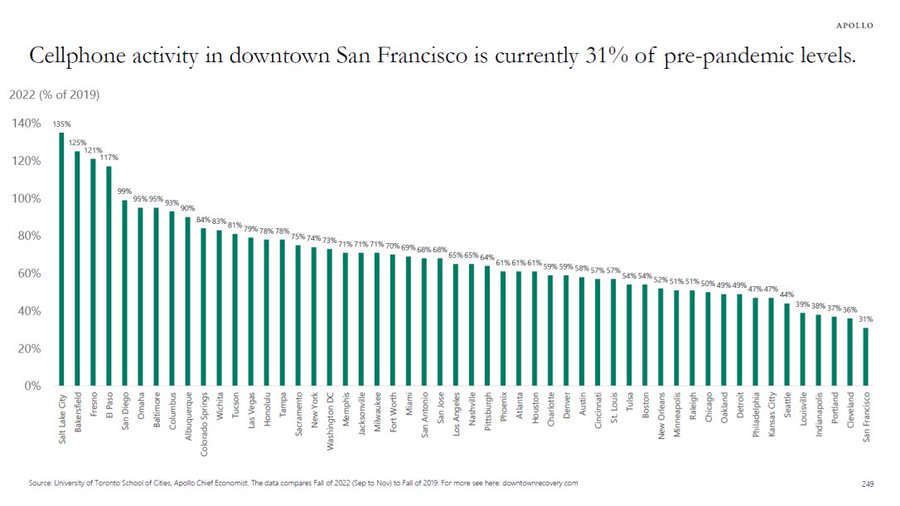

Data from downtowns show that cellphone activity in San Francisco is at 31% of pre-pandemic levels. New York is at 74%, Chicago is at 50%, Boston is at 54%.

Click for larger graphic h/t @carlquintanilla

Click for larger graphic h/t @carlquintanilla

* * * * *

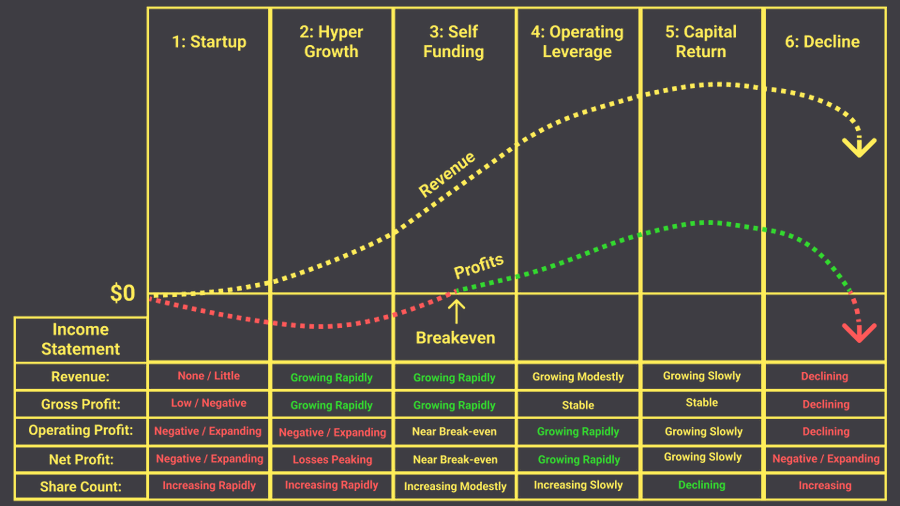

You can tell which stage a business is currently in by watching revenues, gross profit, operating profit, net profit, and share count.

Click for larger graphic h/t @BrianFeroldi

Click for larger graphic h/t @BrianFeroldi

* * * * *

Your studying Shopify Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.47) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $7.57) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $8.08) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.78) – Buy under $7, hold a long time

Invitae (NVTA – $1.36) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.70) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $3.06 – Buy under $2.50, target price $20, then $50

Tech Dominators

Apple Computer (AAPL – $168.41 ) – Buy under $150 for new iPhones

Corning (GLW – $32.75) – Buy under $33, target price $60

Gilead Sciences (GILD – $83.55) – Buy under $80, target price $120

Meta (META – $238.56) – Buy under $250, target price $400

SoftBank (SFTBY – $18.70) – Buy under $25, target price $50

Other Tech

Enovix (ENVX – $10.54) – Buy under $13; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $40.05) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $15.10) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $31.00) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $5.50) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.90) – Buy under $13, target price $30+

Velo3D (VLD – $2.20) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Hold

Bag of Junk Silver – ($25.19) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $29.24) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $33.33) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $19.22) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $30.13) – Buy under $30, target price $50

Coeur Mining (CDE – $3.49) – Buy under $5, target price $20

First Majestic Mining (AG – $7.06) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.33) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.84) – Buy under $10, target price $25

Sprott Inc. (SII – $36.00) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $29,741.64) – Buy

Grayscale Bitcoin Trust (GBTC – $16.44) – Buy

Ethereum (ETH-USD – $1,906.29) – Buy

Grayscale Ethereum Trust (ETHE – $9.04) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.48) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $25.31) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.77) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $27.69) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.68) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.00) – Buy under $1.30; long-term hold

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $64.26) – Buy under $65; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.56) – Buy under $36; $80+ target

EQT (EQT – $33.54) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.42) – Buy under $8; $30 target

Freeport McMoRan (FCX – $37.47) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Akebia Biotherapeutics (AKBA – $0.91) – Hold for FDA decision

Arch Therapeutics (ARTH – $3.00) – Hold for buyout

Graphite Bio (GRPH – $3.06) – Hold until they update their strategy

TG Therapeutics (TGTX – $23.33) – Hold for buyout at $25+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

I’m confused as to why you are so pessimistic on TGTX. The long term analysis values the stock at just over $65; you state $25 plus. Am I missing something ?

I’m far from pessimistic. I expect a buyout offer at something over $25.

MM :You are my hero, really! I bought 10K shares of TGTX back in late 2016 & early 2017 @ $5.70/share when YOU 1st started recommending it, and held… Thank You, Thank You, Thank You . I now hold more shares @ an average of $6.35. So,Michael you have helped make me very comfortable financially and I truly appreciate it ( even if another large holding of mine, ARTH is a write off at this stage, I am way ahead ! ). What I admire most about you and your recommendations is your in depth financial analysis. So, what I would like is YOUR analysis on what a reasonable RANGE is here for a Buy Out AND WHEN. Setting aside the 2 other drugs in their pipeline completely ( pessimistic on my part) , at a long range

( low ball IMO) 35% market share of the rapidly expanding GLOBAL CD20 class of drugs ( up 19% BTW YOY) , Briumvi on a DCF over say 12 years is about $21.8 BILLION, assuming their OPEX stays in check. This excludes any terminal value at all, which I think is unlikely. Assuming a risk adjusted discount of even 50% to the above revenue forecast, the the NPV drops to about $14.3 Billion and an upside scenario to a 50% market share boosts the NPV to ( a WOW ! ) of $41.2 Billion thru 2035. So I would like YOUR insightful analysis on same or please shoot holes in my SWAG above please. Again Michael Many Thanks for the initial recommendation. Enjoying the ride …

Congratulations!

That is amazing. You caught it at the very bottom and held on when it went to 52 in 2020 and dropped to 4 bucks in 2022.

I would have probably sold it in 2020 but hindsight is 2020. No pun.

Ok so TGTX has done well but I could pull out dozens of clunkers that have dropped 90% or more. Just sayin …

Michael: Biotechs are what I call ” High Risk; High reward” investments. They are not for Milk Money IMO. Every once in a while lightning strikes. TGTX is my 1 lightning strike.Thanks.

Thanks for those promising recomendations on Enovix batteries and FCX copper,I think I will try to buy a bit.

Thanks MM, great RR. Also several advisers are calling for a massive run up in the stock market the rest of the year. With the FED basically hobbled to raise rates any further due to the fragile banking sector, housing market killed,automobile markets killed off, consumers backing off spending and the risk of a bigger recession than anticipated. IMO

Either the Fed backs off because the economy is weak, which hurts earnings, or the economy accelerates, improving earnings, but the Fed starts raising again. Either scenario probably allows a stock market that moves up, but I don’t see “massive.”

great report Michael. I am expecting to see significant RIFs over the next 3 quarters as Consumer demand declines. CapX is also flattening if not declining over the same time period. I am also seeing continued outsourcing of transactional and technical jobs to offshore locations. Overall job market will get worse as the year progresses.

True. Employment is a lagging indicator.

Thanks for the ENVX update. How does solid state batteries (e.g. QS) and / or CATL’s high density batteries impact ENVX’s offering? Is it superseded by either / both or do they co-exist?

CATL is more real than QS. ENVX has the capacity plus the quick charge and better safety, but CATL has the existing market share and size. ENVX just has to start reporting design wins and then revenues.

No comments on TGTX movement! WOW!

Strong hold.

Are we selling TGTX at $39.00 ? Or still holding for a buyout?

Hold for a buyout.

I agree. However, today’s trading reflects extreme optimism that Briumvi is the greatest thing since sliced bread. $8 million in sales beat $4 million expectations, but these are small numbers. Next quarter will have to show continued glorious growth to justify further advances in the stock price. You can start doing modeling of sales, time to breakeven so they won’t need to do capital raises, projections of stock price as time goes on, etc.

MM could you please comment on the answer M. Weiss gave regarding partnership? Thanks.

TGTX. Q1 2023 CC

Matthew Lee Kaplan

Can you elaborate a little bit more on your ex U.S. plans. And how you’re thinking about partnering versus going alone?

Michael S. Weiss

Yes. So I mean, again, we’re just continuing to do the analysis of what the ex U.S. market looks like. I mean we’ve kind of narrowed it down that if we’re going alone, we’d probably focus primarily in Germany, where we think the vast majority of the ex U.S. market resides. There’s obviously more global opportunity than that. But again, if it’s going to be a go-it-alone strategy, we’ll probably be more focused and we start there. And obviously, there’s other European countries we could add on pretty easily.

On the partnership side, look, we continue to evaluate potential partners. Obviously, one of the biggest concerns we have is doing a partnership when we recognize the value we can achieve for a partnership is going to be less than we probably get for the ex U.S. rights in a strategic relationship. So it’s important to us to manage that, make sure we have flexibility with the ex U.S. territory. So I think, again, we’re looking into and we’re evaluating the opportunities available to us, both alone and with partners.

And we’re getting close. Hopefully, we’re going to make that decision in the coming months. And again, like we said in the prepared remarks, hopefully, to be prepared to launch later this year.

I was totally confused by this – “the value we can achieve for a partnership is going to be less than we probably get for the ex U.S. rights in a strategic relationship.” What? A partnership IS a strategic relationship. I assume this is bafflegab, and I think he is defining “strategic relationship” as a buyout.

The main direct competitors are Roche (ocrelizumab) and Novartis (ofatumumab), so any of the others would have no antitrust issues. Sanofi and Merck seem likely to me.

Love “bafflegab.” Hadn’t encountered it before.

The market is down 270 at the close. But, SMCI is up 28.27 percent, TGTX is up 11.91 percent (overall up 142.51 percent in holdings) BLPH is up 11.48 percent (overall up 62.26 percent) today. Just FYI

NVTA

MM can we expect next Tuesday’s reporting to demonstrate that they are definatly turning the corner. What kind of price action would you be looking for?

The new Radar Report for 5.4.23 is posted.