Dear New World Investor:

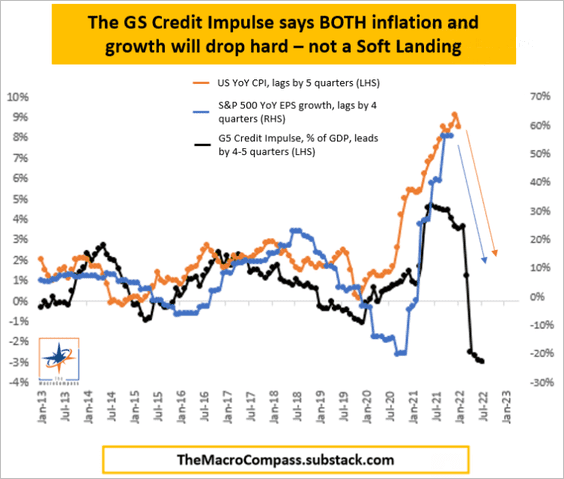

The Fed minutes indicate they are full speed ahead on interest rate increases until either inflation cracks or unemployment shoots up. The Goldman Sachs Credit Impulse Index shows a hard landing coming for the economy with a stock market decline likely. Fed tightening takes seven to nine months for impact, so the likely hit is mid-2023.

Click for larger graphic

Click for larger graphic

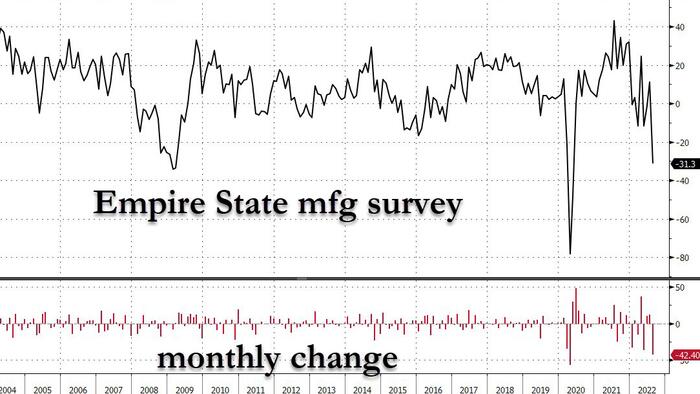

The New York Empire State Manufacturing Index cratered, down -31.3 vs +0.5 estimate. It was the lowest reading since May 2020 and the second largest monthly decline on record.

Click for larger graphic

Click for larger graphic

It was led by a remarkable -29.6 for new orders, which are forward-looking and gauge how fast and steep the industrial decline may be in the December quarter.

And the market has been short-term overbought since mid-July. Plus the weakest month of the year, September, is coming at us. Scary, hey?

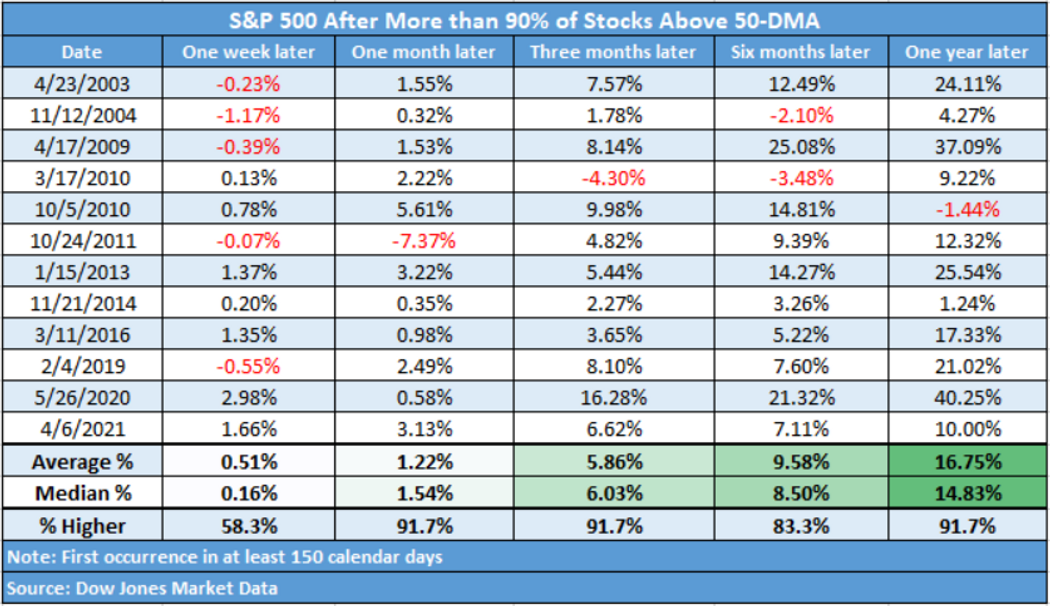

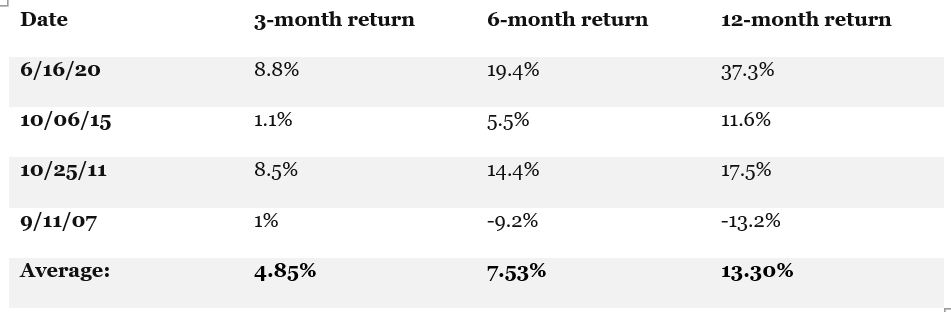

But we can’t turn negative yet. For starters, the number of S&P 500 stocks trading above their 50-day moving averages reached 93% last Friday — the highest level since June 2020. This is important because in recent decades, once the number of S&P 500 stocks trading above their 50-day moving average topped 90%, the market was almost always higher one year later — usually substantially so.

On average, after reaching this market-breadth milestone, the S&P 500 has gone on to gain more than 16% over the next 12 months. Near-term returns were a tossup, but every major market low over the past 50 years or so has been followed by that metric exceeding the 90% threshold.

Click for larger graphic

Click for larger graphic

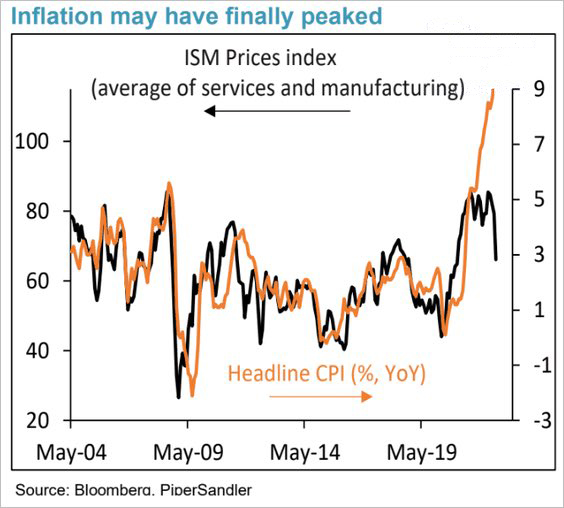

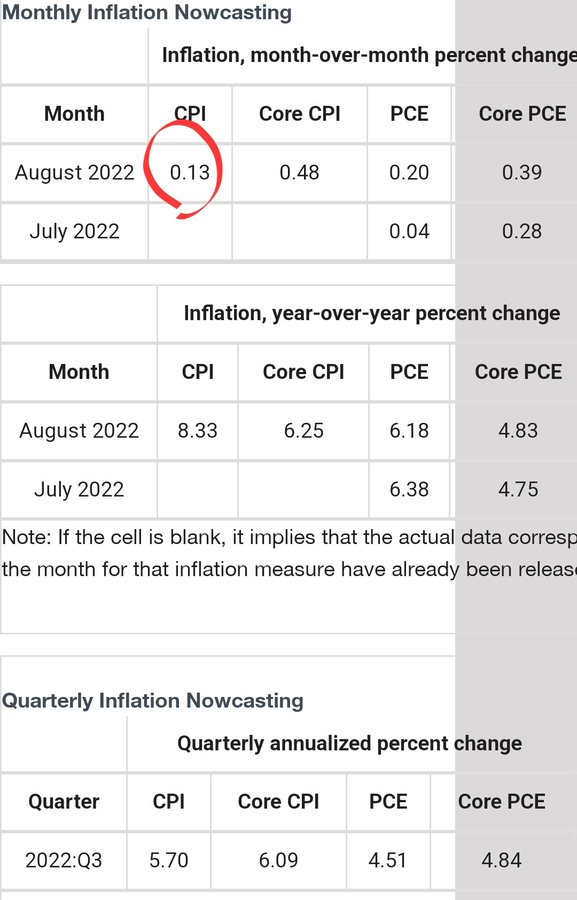

Second, I think my call that inflation has peaked is correct.

Click for larger graphic

Click for larger graphic

The August inflation nowcast from the Cleveland Fed reflecting oil price drops looks good:

Click for larger graphic

Click for larger graphic

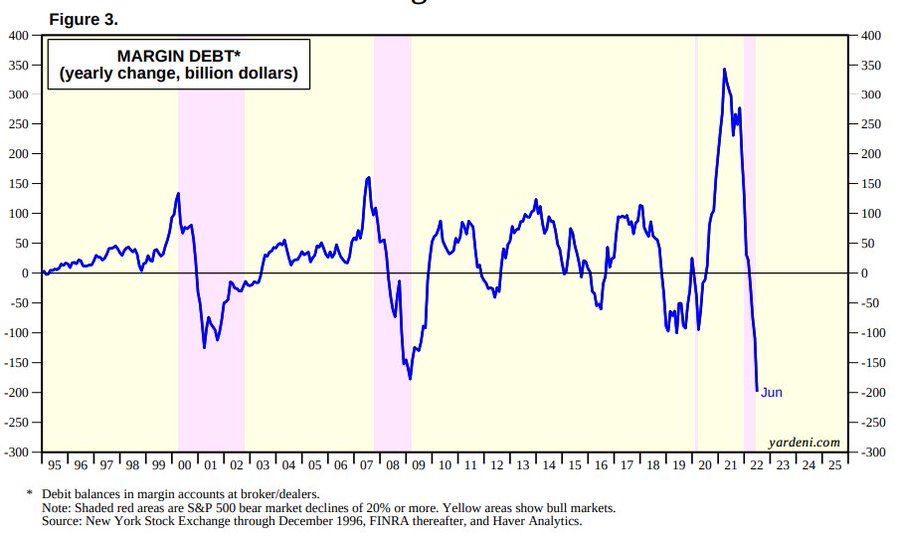

Third, we’ve been through one of the deepest peak to trough deleveraging episodes in history: margin debt quite literally collapsed during this bear market.

Click for larger graphic

Click for larger graphic

Fourth, corporate insiders have been buying. This could signal an upward trend for stocks over the next one to two years.

Click for larger graphic

Click for larger graphic

Fifth, there still are too many bears. From June 16 to August 12, short interest in the US stock market increased by $125.7 billion, or roughly 14%, according to technology and data-analytics firm S3 Partners.

Click for larger graphic

Click for larger graphic

Check out the long-term S&P 500 Index returns generated (dividends reinvested) since 2000 when the E-Mini S&P 500 Index Futures short interest has been this extreme:

Click for larger graphic

Click for larger graphic

Institutions are a little bit more invested, but nowhere near bullish:

Click for larger graphic

Click for larger graphic

Fifth, Goldman Sachs says they are seeing $13.3 billion in equity demand every day as the hedge funds scramble to reduce their losses before the withdrawals window opens on November 1.

Sixth, the American Association of Individual Investors bulls nudged up to 33.3%, which isn’t much but is the highest reading in 2022. But the bears nudged up as well to 37.2%. The four-week moving average of bears is back to April levels. Last week, the S&P 500 rose more than 3%. And yet…small options traders bought FEWER calls to open and bought MORE puts during the week. This is the first week since 2009 when retail traders fought a >3% weekly rally to this degree.

Markets top when everyone is bullish and fully invested. Institutions, hedge funds, retail – none of them are on board. That means the path of least resistance is up.

Market Outlook

The S&P 500 added 1.8% since last Thursday and now is back over the 50% retracement level from the January all-time high to the June bear market lows. There has never been a “bear market rally” that bounced back above the 50% retracement level and then went on to make lower lows. The Index is down just 10.1% year-to-date.

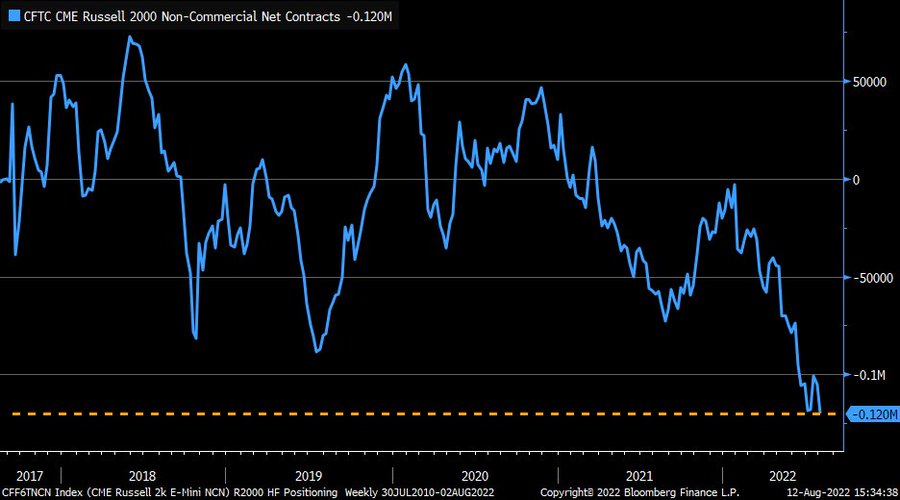

The Nasdaq Composite gained 1.5% and is down 17.1% for the year. The small-cap Russell 2000 rose 1.3% and is down 10.9% in 2022. Small caps have had a strong rally in the recent move higher for the broader market, but hedge funds are betting against them with a multi-year high in Russell 2000 futures short positions:

Click for larger graphic

Click for larger graphic

The fractal dimension is heading towards the full consolidation level at 55. That provides enough energy to power the next trend, which should be up into early next year.

Top 5

Changes this week: None.

Near-Term – chronological order

AAPL Apple – September new iPhone introduction

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphite Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model estimate for real GDP growth in the September quarter dropped to 1.6%, about the same as the Blue Chip consensus, on lower real personal consumption expenditures growth.

Click for larger graphic

Click for larger graphic

Business execs see a recession coming.

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Wednesday, August 24

Short Interest – After the close

QUIK – QuickLogic – 3:00pm – Rosenblatt Virtual Technology Summit

Thursday, August 25

June quarter real GDP – 8:30am – Second estimate; -0.9% expected, unchanged from first estimate

Friday, August 26

Personal Consumption Expenditures Index – 8:30am

Fed Chairman Powell – Jackson Hole banking conference

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations are typically very low. At the same time, Initial Public Offering valuations had moved very high. We were seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors make 5x to 10x in a reasonable, three- to four-year period if they buy at those valuations. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Algernon Pharmaceuticals (AGNPF – $3.09) privately placed $1,402,125 of units at an issue price of $3.75 per unit. Each unit includes one share and one 5-year warrant exercisable at $4.25. The stock was down less than 2% today – no harm, no foul.

The had a lengthy update in Medical Gold that they probably paid for. AGNPF is a Hold for the Phase 2b IPF/chronic cough results.

Primary Risk: Ifenprodil fails in clinical trials.

Clinical stage of lead product: Phase 2/3

Probable time of first FDA approval: 2023

Probable time of next financing: 2022

Bellerophon Therapeutics (BLPH – $1.45) reported a June quarter loss of $4.1 million or 43¢ per share, better than the 60¢ loss expected. Management said enrollment is steadily proceeding in their 300-patient Phase 3 trial in fibrotic interstitial lung disease.

They recently got FDA clearance to conduct a follow-up exploratory Phase 2 double-blinded, placebo-controlled chronic treatment clinical trial of INOpulse in pulmonary hypertension associated with sarcoidosis patients, a disease with no approved therapies and a median survival of approximately five years after diagnosis.

At the end of June, they had $16.3 million in cash, enough to carry them into 2023Buy BLPH under $5 for a $30 first target and $100 someday.

Primary Risk: The Phase 2b PH-ILD trial fails or the FDA turns down the INOpulse.

Clinical stage of lead product: Phase 2 transitioning to Phase 3 in March quarter

Probable time of first FDA approval: 2021

Probable time of next financing: March 2023 quarter

CohBar (CWBR – $0.17) reported a June quarter loss of $2.7 million or three cents a share, a penny better than the four-cent loss estimate. On the conference call (TRANSCRIPT HERE), management said the Investigational New Drug filing to put CB5138-3 for idiopathic pulmonary fibrosis into human trials is on track for the second half of 2023.

CohBar finished the quarter with $20.1 million in cash, enough to fund them through mid-2023.

They have approval for up to a 1-for-30 reverse stock split by November 7. I have lost confidence in this management team’s ability to get a drug to the finish line. It’s a great technology, and we may come back to it on the future, but for now, I’m changing my Hold recommendation to Sell. SELL CWBR

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 1

Probable time of first FDA approval: 2025

Probable time of next financing: March 2022 quarter

Medicenna (MDNA – $1.02) reported a June first-quarter loss of $4.2 million or seven cents a share, right on the consensus. On the conference call (SLIDES HERE and TRANSCRIPT HERE), they said new MDNA11 data from the Phase1/2 trial showed tumor control in four of ten evaluable patients, including two sarcomas, a metastatic melanoma, and an unconfirmed partial response in a pancreatic cancer patient. This may be confirmed by the required second scan in the next few weeks.

The trial is enrolling the fifth dose-escalation cohort with no dose-limiting toxicities so far. We will get more data from the fourth cohort in late September and initial data from the fifth cohort before the end of this year.

Click for larger graphic

Click for larger graphic

They finished the quarter with $19.3 million in cash and raised another $20 million in August, enough to carry them into 2024. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: mid-2022

ScyNexis (SCYX – $2.82) reported June quarter revenues of $1.32 million, up 88% from the March quarter but below the $1.64 million consensus expectation. They lost $13.3 million or 31¢ per share, much better than the -59¢ consensus. On the conference call (TRANSCRIPT HERE), management said Brexafemme prescriptions increased to 5,141, up 29% from the March quarter. It was prescribed by over 2,200 individual healthcare professionals in the quarter, an increase of 25% over the March period.

Brexa now is covered by plans representing more than 109 million or 60% of commercially-insured lives, a 17% increase over the 93 million covered lives as of the end of March. The company will advertise on the Oprah Winfrey Super Soul podcast for three months. This podcast is expected to deliver 4.2 million impressions. They also have partnered with national and local pharmacies and grocery stores to place Brexafemme shelf display ads where women are shopping for over-the-counter products like Monistat, and will drive consumers to ask their doctors about Brexa.

They are rolling out a new patient video that will be placed on Hulu, YouTube, and other programmatic partners as well as on targeted OB/GYN waiting room monitors. This initiative will garner over 19 million impressions and activate women to ask their doctors if Brexa is the right treatment option for them.

ScyNexis hit its target enrollment of 200 patients for the Phase 3 trial evaluating oral ibrexafungerp for the treatment of patients with severe fungal infections who are either intolerant to standard antifungal therapy or experience refractory fungal infections despite treatment, including those caused by Candida auris.

They began enrollment in two Phase 3 trials. One is evaluating oral ibrexafungerp as a step-down treatment for invasive candidiasis, and the other is evaluating ibrexafungerp for vulvovaginal candidiasis patients that have failed treatment with fluconazole.

They finished the quarter with $118.7 million in cash, enough to carry them into the March 2024 quarter. Buy SCYX under $2 for a first target price of $20 now that Brexafemme is approved and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: mid-2022

Probable time of next financing: second half of 2023 or newer

Biotech MegaShift

TG Therapeutics (TGTX – $7.31) is the subject of numerous shareholder class-action lawsuits. Don’t worry about them. TGTX is insured and the only point is to get the lawyers a payday in time for their Christmas in Aspen. Buy TGTX under $7 for a target price in a buyout of $25 or more after the MS drug is approved.

Primary Risk: FDA turns the MS drug down.

Clinical stage of lead product: Filed for approval.

Probable time of next FDA approval: September 28, 2022

Probable time of next financing: March 2023 quarter

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $174.15) will introduce iPhone 14 on September 7. Credit Suisse upgraded Apple to overweight from neutral and raised their target price to $201. How brave of them! The analyst noted Apple’s growing services business and large customer base as bullish drivers for the stock. Ya’ think? AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $65.18) announced statistically significant and clinically meaningful results from the second interim analysis of the key secondary endpoint of overall survival in their Phase 3 trial of Trodelvy in patients with HR+/HER2- metastatic breast cancer who received prior endocrine therapy, CDK4/6 inhibitors, and two to four lines of chemotherapy. They already filed an application with the FDA to approve Trodelvy for this group of patients. They also said they expect to present full data from this trial soon.

The stock hit a six-month high on the news. The company announced an agreement with Everest Medicines to transfer all remaining worldwide development and commercialization rights to Gilead for Trodelvy, including Greater China, South Korea, Singapore, Indonesia, Philippines, Vietnam, Thailand, Malaysia, and Mongolia. GILD is a Long-Term Buy under $70 for a first target of $100.

Other Tech

PagerDuty (PD – $27.48) did a fireside chat at the Canaccord Genuity Growth Conference (ZOOM HERE). It was a worthwhile basic introduction to the company and its position in the market. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk:Digital operations management is a competitive area.

Probable time of next financing: None needed

QuickLogic (QUIK – $7.35) reported June quarter revenues up 57.6% from last year and 10.9% from the March quarter to $4.54 million with a loss of only four cents a share. Analysts were expecting $4.47 million and a three-cent loss. New product revenue increased 148% from last year.

On the conference call (TRANSCRIPT HERE), management said their new $7 million eFPGA contract “has the potential to increase to tens of millions of dollars.” They had their best bottom line performance since 2010 and have an increase in their sales funnel and large design wins currently approaching $100 million over time.

QUIK said they are being designed into several new models of phones that will ship well into 2024, giving them good long-term visibility. In the near term, the start date for the $7 million contract was pushed out to the December quarter, so they now are expecting September quarter revenues of $3.4 million, ±10%, with an 11¢ to 14¢ per share loss. They still expect 2022 revenues up 35% from last year and to be profitable in the December quarter.

They finished the June quarter with $18.5 million in cash and don’t need to raise any money. They did update their mixed shelf registration for up to $125 million, but I expect this would only be used for an acquisition. QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets, and wearables.

Primary Risk: New sensor hub competitor emerges.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $6.00) said their mid-September Electron launch (their 30th) will deliver their 150th satellite to space – a quarter of those delivered to space in the past three months alone.

Next: LOXSAT. Electron and Photon will conduct a flight demonstration of a complete cryogenic fluid management system in orbit for NASA, essentially building, launching, and testing a cryogenic fuel depot in space.

After that they are sending their Photon spacecraft to Venus in search of life. Supported by a science team at MIT, this is the first private mission to Venus and the first opportunity to probe the Venusian clouds in nearly 40 years. You can read the full mission details HERE. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,771.70) weakened as the dollar strengthened again after the Fed minutes showed they are going to increase interest rates into a recession. The fractals still are extremely consolidated and can power a very large move.

Miners & Related

Sandstorm Gold (SAND – $5.98) held their conference call last Friday morning (TRANSCRIPT HERE). As I wrote last week, SAND easily beat estimates and set quarterly records for net income, revenues, and production. But management was even more excited about the Nomad Royalty acquisition that closed last Monday. Existing Sandstorm and former Nomad shareholders now own approximately 73% and 27% of the outstanding shares of the new pro forma Sandstorm, respectively. CEO Nolan Watson said: “We believe that the new Sandstorm will become an even more attractive investment vehicle for large institutional investors looking for high quality, high upside, lower risk exposure to gold.”

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offers a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $23,345.41) traded over $24,000 and seems to have strong support at $23,000. Ethereum (ETH-USD) hit a new three-month high last Friday and is up about 100% from its June lows.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

International & Other Recommendations

It is important to hold some non-US assets, especially in China.

Acreage Holdings (ACRDF – $1.04) made a really good presentation at the “Pot to Public” investor series (ZOOM HERE). I couldn’t find CEO Peter Caldini’s slides on their website, but I grabbed the key ones.

First, the company has been completely transformed by the new management team.

Click for larger graphic

Click for larger graphic

They are focused on their core Northeast market, a $13 billion opportunity by 2026, and getting vertically integrated.

Click for larger graphic

Click for larger graphic

They have four primary markets, the most important being New York and New Jersey.

Click for larger graphic

Click for larger graphic

The other two are Ohio and Connecticut. Maine is a secondary focus.

Click for larger graphic

Click for larger graphic

As are the other markets.

Click for larger graphic

Click for larger graphic

In each market, they want to have enough growing operations to be wholesalers to other companies while building their retail operations to sell their higher-end and others’ products.

Click for larger graphic

Click for larger graphic

The Canopy Growth merger will be at a minimum of $6.41 per share and happen as soon as the Feds make it legal for US banks to provide services to marijuana companies. I think that happens within 12 months. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

Mongolia Growth Group (MNGGF – $1.28) posted their June quarter shareholders letter. All is well. MNGGF is a buy under $1.30 for a long-term hold.

Primary Risk: Harris Kupperman makes bad investments.

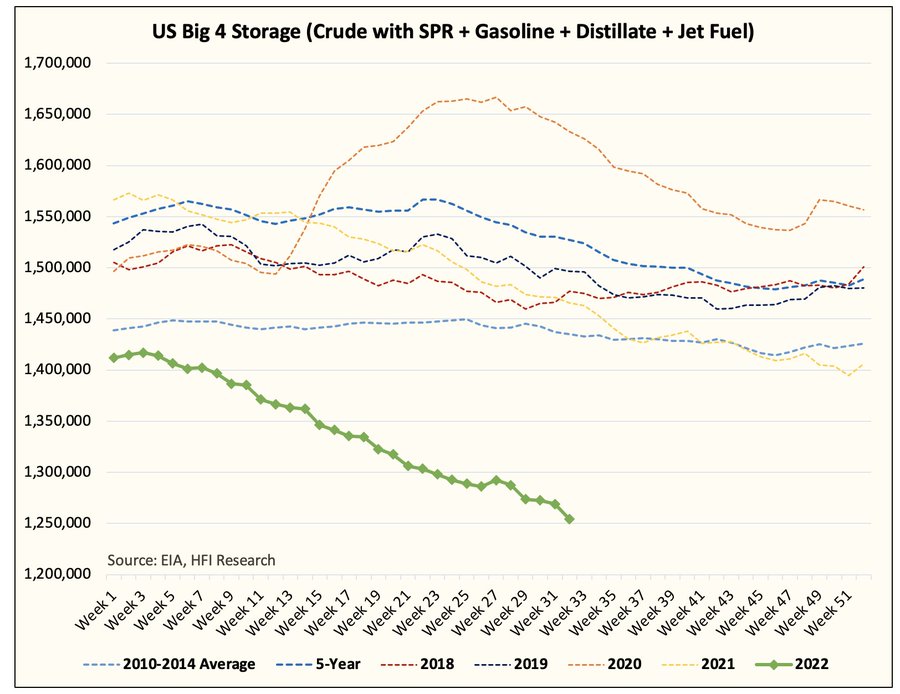

Oil – $90.55

Oil was hit as everyone pretended there’s an Iran nuclear deal, but that looks likely to fade over the next few weeks. Meanwhile, four-week gasoline demand rose to 9.06 million barrels a day, the highest this year.

Click for larger graphic

Click for larger graphic

Gas stations owners did their part and went on a buyers strike that “depressed” demand until they ran out of fuel, and now are scrambling to refill their tanks. This week’s Energy Information Administration data showed a huge draw on crude oil (-7.1 million barrels) and gasoline. The Strategic Petroleum Reserve draws are being exported according to Vortexa estimates, based on winning bids from Shell, Unipec, Glencore, Vitol, Equinor, Mercuria, Macquarie, and others. US crude oil exports hit 5 million barrels, a record high, last week.

At the same time, you can see the impact of the demand losses in the total liquids storage charts. But as demand rebounds into yearend, we are going to be back on track (downtrend).

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

OPEC Secretary-General Haitham Al-Ghais said global oil markets face a high risk of a supply squeeze this year as demand remains resilient and spare production capacity dwindles. Fears over slowing consumption in China and the wider world – which have pushed crude prices 16% lower this month – have been exaggerated. He said: “We are running on thin ice, if I may use that term because spare capacity is becoming scarce. The likelihood of a squeeze is there.”

The financial market appears to be ignoring how tight the physical market for oil is. Even sanctioned Iranian oil is now selling at a premium instead of the historic extreme discount. Longer term, when looking at Russia, many oil service companies have left due to the sanctions. What happens when winter arrives, arguably the most dangerous time as most of their production already is in areas of permafrost such as Siberia. If they have to shutter these wells we are talking years to recover.

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $32.17) is a Buy under $36 for an $80+ target. Now is the time!.

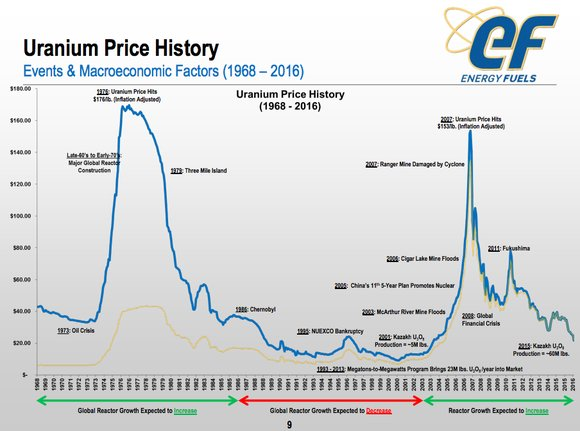

Energy Fuels (UUUU – $6.29) is in the right place at the right time. Germany is keeping their last three nuclear reactors online. Japan now supports a restart of its reactors. The Inflation Production Reduction Act supports nuclear. Energy Fuels is signing contracts and ramping up its uranium portfolio.

Click for larger graphic

Click for larger graphic

UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

Map showing the location of US and Chinese bases in the region with a range of different weapon systems, including Chinese H-6K bombers and F-35 fighters from a US carrier group.

Click for larger graphic

Click for larger graphic

* * * * *

New to me: Meral Guneyman

* * * * *

Your agreeing with American Hustle: Microchip Edition Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.86) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $1.45) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $17.61) – Buy under $20, hold a long time for a 10x return

Graphite Bio (GRPH – $3.82) – Buy under $9, hold a long time

Inovio (INO – $2.51) – Buy under $7, hold a long time

Invitae (NVTA – $3.85) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $1.02) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.82) – Buy under $2, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $7.31) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $174.15) – Buy under $150 for new iPhones

Corning (GLW – $36.86) – Buy under $33, target price $60

Gilead Sciences (GILD – $65.18) – Buy under $70, target price $100

Meta (META – $174.66) – Buy under $250, target price $400

SoftBank (SFTBY – $21.58) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $46.08) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $11.11) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $27.48) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $7.35) – Buy under $10, target price $40

Liberty Media Acquisition Corporation (LMACA – $9.86) – Buy under $10, target price $20 to $30

Rocket Lab (RKLB – $6.00) – Buy under $13, target price $30+

Velo3D (VLD – $4.86) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – $447,000 – Buy while fixed mortgage rates are low

Bag of Junk Silver – ($19.45) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $23.64) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $27.48) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $16.38) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $24.99) – Buy under $30, target price $50

Coeur Mining (CDE – $3.03) – Buy under $5, target price $20

First Majestic Mining (AG – $7.75) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.38) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.98) – Buy under $10, target price $25

Sprott Inc. (SII – $38.27) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $23,345.41 ) – Buy

Grayscale Bitcoin Trust (GBTC – $14.48) – Buy

Ethereum (ETH-USD – $1,822.08) – Buy

Grayscale Ethereum Trust (ETHE – $13.99) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.35) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $35.01) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $15.42) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $27.47) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $1.04) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.28) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $32.17) – Buy under $36; $80+ target

Energy Fuels (UUUU – $6.29) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $3.09) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.40) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.04) – Hold for buyout

Sell

CohBar (CWBR – $0.17)

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

2

First I guess: Another great Radar Michael 2 questions. With the recent passage of the Inflation Reduction bill by the Democrats, but enormous increases in expenditures (IRS. CLIMATe Change and lots of buying batteries and chips overseas so China can help he carbon with their Coal plants, excuse the sarcasm, would the models of inflation not be jarred a bit by this massive tax and spending?

2nd question: On the last radar board Could you please assess this issue of avoiding ESG impact on the energy stocks with the initiation of the ETF DRLL . My venture thus far has been OK with both TPL and DRLL with the latter being a source of capital for fossil fuel companies as the goal goes for this new line of ETF’s.?

Strive’s Flagship U.S. Energy Fund DRLL Exceeds $100 Million Within First Week of Launch (yahoo.com)

“Markets top when everyone is bullish and fully invested“

Wasn’t this the case when the markets topped at the end of 2021?

WOW, great RR, MM. So much great information, so little time. Just a note on APPL. Warren Buffet just made a big buy on the shares. And he historically doesn’t like investing in tech stocks.

Appreciate all the great market info this week.

SCYX – the 11/4/21 SCYX note included the following 2022 revenue guidance: The estimate … for 2022 is $28.56 million.

Revenues through the first half of 2022 are a meager $2.0M. SCYX will likely do, say, $6M to $7M for 2022 or just over 20% to 25% of that late 2021 estimate.

A year ago at this time in their investor presentations SCYX was forecasting $400 million to $600 million for vulvovaginal candidiasis alone in 2027 peak US sales. This year those presentations have been revised to just $400+ million.

Based on the very disappointing VVC sales ramp the likelihood of SCYX reaching $400+ million in VVC/rVVC revenues seems extremely unlikely. 2022 revenues will not even hit 2% of that forecast.

Revenues clearly aren’t ramping quickly enough to get them to cash flow positive before additional financing is needed in late 2023/early 2024 as may have been thought earlier.

It’s likely Merck, or its women’s health spinoff Organon, would be much more capable of optimizing the VVC/rVVC market potential. SCYX would benefit by selling off the VVC/rVVC indications & using the money to fund the remaining indications.

Could happen. They are more likely to build a broad-based antifungal portfolio where knowledge of one application leads to use for other applications.

Bought more ACRDF

MM is the ACRDF and Canopy Growth merger is a done deal, signed and definately happening or is it speculation?

A signed deal, but already revised once. Canopy (which is controlled by Constellation Brands) wants ACRDF for a US footprint as soon as possible.

What is going on with the recission of a tender offer for the OIL security? There is a deadline of 9/12/22 to respond thereto.

It is a settlement with the SEC. They will buy your shares purchased during the settlement period at your purchase price. . . . don’t do it, current market value should be higher.

Michael – what is your price target for ACRDF? When will it get there?

@Steve. This is in the portfolio link

Acreage Holdings (ACRDF) Buy Limit: $2 Target Price: Hold for CGC merger

Acreage Holdings is a US multi-state cannabis company.

Original Recommendation: October 24, 2019 @ $2.27

I’ll take the $6.41 per share. I think the SAFE banking act could pass in 2023 even with a Republican Congress, so late 2023 – early 2024 is me best estimate.

MM, can you update the financing part for MDNA?

hey finished the quarter with $19.3 million in cash and raised another $20 million in August, enough to carry them into 2024. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: mid-2022

Thanks for the nudge. March 2024.

MM, Do you think APTO will have to do a Reverse Split in order to remain compliant? It closed at .80 today. Thanks!!

There is a steady stream of data coming at scientific meetings in December, next June, and the following December. Today’s $77 million market capitalization for a coming successful oncology drug is ridiculously low. APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 1a

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Tiny numbers of patients–see Carol J’s posts on YMB for an extremely bearish view.

It’s a risk, but they have 6 months to get the stock up, which gets us well past the American Society of Hematology meeting and data December 10-13.

More fundamentally, go refute Carol J’s repeated observations that very few patients have been enrolled in trials. ASH will be a yawn.

Go UUUU. Japan decides to bring its nuke plants back online. Plus OPEC is cutting back on production because of the future’s market action. Citigroup warned that inflation (in Europe) is on course to hit 18.6 percent by next year as energy prices soar.

Note that UUUU is technically a Canadian firm also listed on the exchanges there and here but with domestic locus in California. They do have extensive locus to US Nuclear ratings, although having interests in other rare earths, too.

You can look at the firms USA (and Canadian) filings for more details associated with this dual existance and business reporting.

Thus where you hold the stock(s) may impact your tax situation and other legal aspects depending on your locus vs. the share type(s) you might hold.

Note that Germany is teetering at holding back closing their last nuclear plants, while France is but one country that still has functioning facilities. Will the US government clamp down on their US business ?

I just want to note that the perennially, decades long recommended ARTH is now down below 3 cents. A fair chunk of money down the drain.

On YMB, someone recently posted a story about the many offerings in the high end bandage field. We were led to believe that AC5 is by far the best. Maybe not, but even if AC5 is the best, there are plenty of good alternatives backed up by major companies. Who wants to do business with a company like ARTH whose major business activity is getting funding to pay the few insiders and fleece 99+ percent of shareholders.

MM: Could you comment on ARTH; it seems like their idea of getting the stock exchange-listed would require a 200 for 1 reverse split to get the price above $5.00; do you think they are actually going to do this? You have down hold for a buyout at $1.00 to $2.00 but the recent MM picks that were bought out (ATRS and BDSI) were purchased at a price far less than anticipated (at least by me). Although ARTH doesn’t have debt to force them into bankruptcy they seem to be diluting the stock at every turn. From my days at a Fortune 500 company I recall I had to do due diligence on vendors – if someone had a “going concern” warning it was just easier to pass on them rather than place an order and start a relationship.

The Radar Report for 8.25.22 is posted.