Dear New World Investor:

Oh, no! Fitch downgraded US government debt from AAA to AA+! I did not expect this! It dramatically affects…

Nothing.

Literally. Not. A. Thing. As Mohamed El-Erian said: “Why now? When you look at the reason, you scratch your head as to the timing of this. I don’t think that this Fitch rating changes anything.”

Warren Buffett says he’s not concerned about the Fitch downgrade, saying his company continues to buy $10 billion of Treasury bills each week. “There are some things that people shouldn’t worry about and this is one.”

After S&P did the same downgrade in August 2011, it made no difference to anything. Of course, the computerized trading bots and day traders jumped on this terrible negative news to knock stocks down.

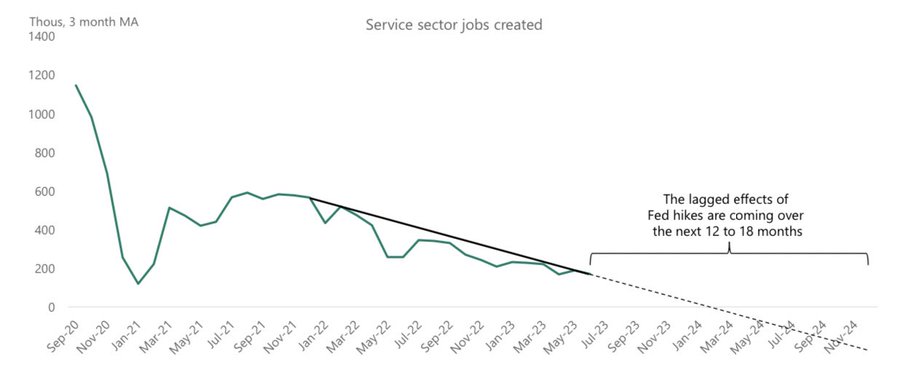

Tomorrow’s July payrolls report is expected to show +200,000 jobs, I will be paying special attention to the June and May revisions. Government forecasters tend to trendline the first reported number, and when you get three dramatic revisions in a row in the same direction, it usually marks an inflection point. I still expect a shallow recession starting in the December quarter and, as always, jobs are the key metric and services are where the adjustment will come. I expect weakness to start showing in the nonfarm payrolls report.

Click for larger graphic h/t @INArteCarloDoss

Click for larger graphic h/t @INArteCarloDoss

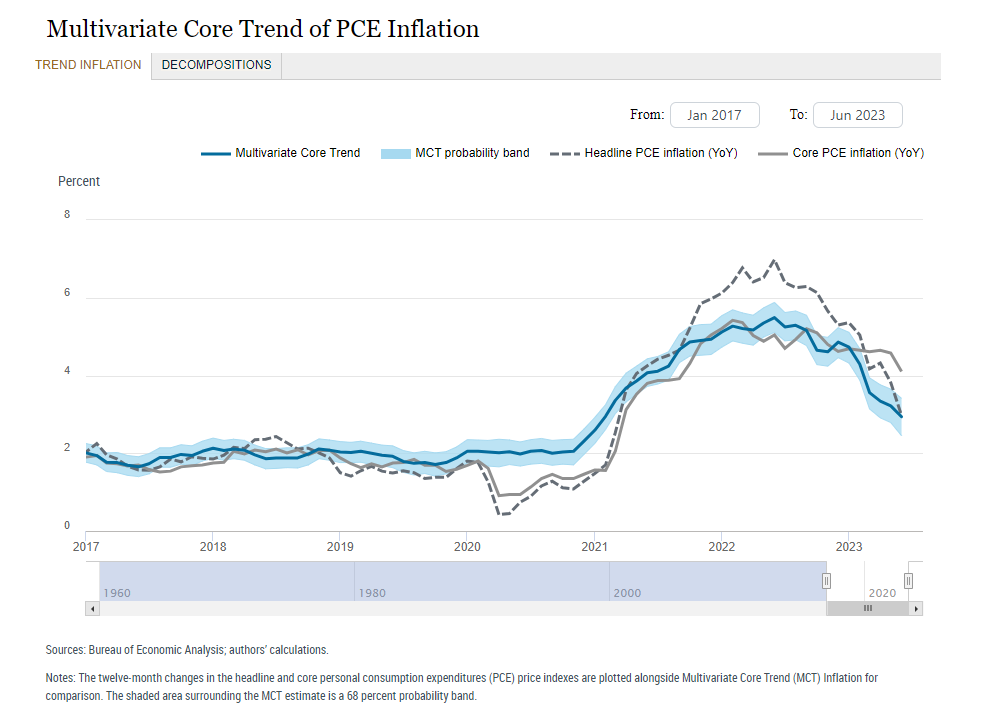

The New York Fed’s inflation gauge captures the underlying trend, called the “multivariate core trend” rate of inflation. It fell to 2.9% in June from a downward-revised 3.2% in May This is the lowest level since January 2021.

Click for larger graphic

Click for larger graphic

Last Friday’s Personal Consumption Expenditures report showed consumer prices rose in June at their slowest pace in more than two years. The June PCE was up 3.0% year-over-year compared to 3.8% in May. It was up 0.2% month-over-month.

The core PCE was up 4.1% YoY, down from 4.6% in May. It was up 0.2% month-over-month, down from 0.3% in May.

Chris Ciovacco did an interesting presentation on where we are in the longer-term outlook. I don’t think he knows about the 36-year cycle that last topped in 2000 and will top again in about 13 years in 2036.

And as long as we’re talking about the long term, what about interest rates? Critics of the Fed are unfamiliar with the big trend in rates that has been in place for over 700 years, since 1310. Could it be that the Fed doesn’t matter? The red box indicates the period before the Federal Reserve Bank.

Click for larger graphic h/t @WinfieldSmart CFA

Click for larger graphic h/t @WinfieldSmart CFA

Market Outlook

The S&P 500 lost 0.8% since last Thursday, including a 1.4% drop the day of the Fitch downgrade. The Index has climbed for five straight months and is up 17.3% year-to-date. The Nasdaq Composite lost 0.6%, including a 2.2% drop on Fitch downgrade day, its worst day since February. It is up 33.4% for the year. The small-cap Russell 2000 gained 0.3% and is up 200 points or 11.4% in 2023.

The fractal dimension shows this week to date as a pause in the uptrend, not a change in direction. But a lot of energy has been used up, and the usual late summer/fall correction probably will start in a few weeks.

Top 5

Changes this week: Added TGTX to Near-Term – see below

Near-Term – chronological order

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage this fall

SFTBY SoftBank – for ARM IPO this fall

AKBA Akebia – Vadadustat NDA filing 2023; approval 2024

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

Obviously, it’s early days, but the Atlanta Fed’s GDPNow model is looking for strong +3.9% real GDP growth for the September quarter.

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, August 4

July payrolls – 8:30am – +200,000 expected; was +209,000 in June

SAND – SandStorm – 11:30am – Earnings conference call

Tuesday, August 8

SFTBY – SoftBank – 3:30am – Earnings conference call

RKLB – Rocket Lab – 4:30pm – Earnings conference call

NVTA – Invitae – 4:30pm – Earnings conference call

Wednesday, August 9

SII – Sprott Inc. – 10:00am – Earnings conference call

CDE – Coeur Mining – After the close – Earnings release; call tomorrow

Short Interest – After the close

INO – Inovio – 4:30pm – Earnings conference call

Thursday, August 10

Consumer Price Index – 8:30am

CDE – Coeur Mining – 11:00am – Earnings conference call

APTO – Aptose Therapeutics – 5:00pm – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

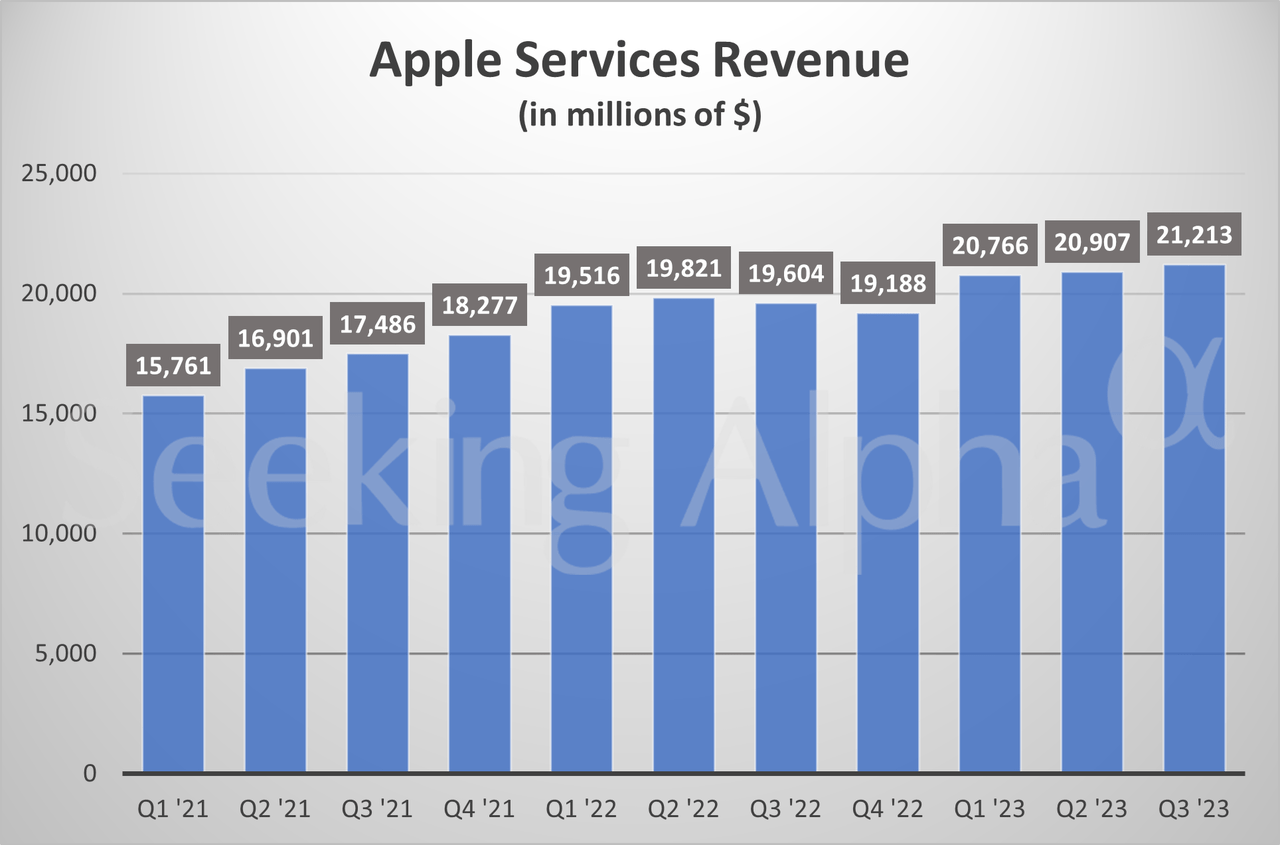

Apple (AAPL – $191.17) reported earnings after the close today. Revenues fell 1.4% from last year to $81.8 billion, in line with estimates. Earnings hit $1.26 a share, beating the $1.19 estimate. But on the conference call (AUDIO HERE and TRANSCRIPT HERE), CEO Tim Cook said: “We continue to face an uneven macroeconomic environment.” Consequently, they expect a September quarter year-over-year revenue drop similar to the June quarter. That is below analyst expectations of roughly flat fiscal fourth-quarter sales of $90.19 billion, so the stock is down 2% in after-hours trading.

In the June quarter, iPhone revenues were down for the third straight quarter, this time falling 2.5% from last year to $39.67 billion. That’s the longest stretch of falling sales in nearly seven years. Mac revenues were weak, down 7.3% YoY to $6.84 billion, although almost half of the buyers were new to the product. iPad was even weaker, down 19.8% to $5.79 billion. But Wearables, Home and Accessories grew 2.5% to $8.28 billion and Services came through with an 8.2% year-over-year gain to a record $21.21 billion. Apple ended the quarter with more than a billion paid subscriptions.

Click for larger graphic

They’ll announce the iPhone 15 on September 13 and I think people are nuts to sell before we see what surprises are in store. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $75.53) reported June quarter revenues up 5.3% to $6.59 billion, just above the $6.45 billion estimate. Pro forma earnings of $1.34 badly missed the $1.64 estimate. But that includes a $525 million or 32¢ charge related to HIV antitrust litigation settlements.

Sales of Trodelvy, Yescarta and Tecartus — Gilead’s cancer medicines — surged a combined 38% to $728 million. That beat analyst expectations for $709 million,

On the conference call (TRANSCRIPT HERE), management said they have 21 late-stage trials ongoing simultaneously and “We are going to be really disciplined about where we go from here … looking at our portfolio and making some tough decisions around what keeps going and what doesn’t.”

For the full year, they now expect total product sales between $26.3 billion and $26.7 billion, up a bit from $26.0 billion to $26.5 billion previously. Total product sales excluding Veklury (remdesivir) were increased a little more to between $24.6 billion and $25.0 billion, up from $24.0 billion to $24.5 billion previously.

But they trimmed their pro forma diluted earnings per share guidance from $6.60 to $7.00 down to between $6.45 and $6.80, a bit below the $6.73 consensus estimate. .

Wall Street liked the quarter and the stock held up in the aftermarket. The company declared a 75¢ quarterly dividend, giving us a 4% yield while we wait. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $313.19) introduced AudioCraft, an open-source generative AI tool for audio and music. Users can easily generate high-quality audio and music from text.

Click for larger graphic

META was up 11% in July, and as Evercore ISI said: “How could a stock that is now up 165% year to date possibly be one of our Top Picks?! Because valuation is still cheap. Meta remains much closer to a trough than a peak multiple, and we believe the Street woefully underestimates the EPS potential here.”

Meta currently trades at 19.2 x estimated 2024 earnings, below the S&P 500’s level of 21x. Yet, Meta is expected to grow profits significantly higher than the broader market in 2023 and 2024. Analysts are projecting Meta’s profits will increase by 30% in 2023, accelerating to 31% growth in 2024. META is a Buy under $150 for a $400 target in 2024.

Small Tech

Enovix (ENVX – $17.82) hosted a signing ceremony with YBS International Berhad to commemorate their new Fab-2 manufacturing facility in Penang Science Park, Malaysia. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $20.24) reported a superb June quarter. Revenues grew 19.8% from last year to a record $122.8 million, well above the $118.9 million estimate. The pro forma loss of four cents a share was much better than the 10¢ loss expected. Although the total customer count was down 28 from the March quarter to 3,072, 551 were enterprise customers, up 11 from the first quarter. And the average enterprise customer spend of $818,000 was up 3% quarter-over-quarter.

On the conference call (INVESTOR SUPPLEMENT HERE and TRANSCRIPT HERE), they guided for September quarter revenue of $125 million to $128 million compared to the consensus for $127.06 million. They expect a proforma loss of seven to nine cents a share, worse than the five-cent loss estimate.

For the whole year, they now expect revenues of $500 million to $510 million, above the consensus for $502.1 million. They are targeting a pro forma loss of 21¢ to 27¢ per share, a bit worse than the 26¢ consensus. But Wall Street focused on their strong Dollar-Based Net Expansion Rate (DBNER), which increased to 123% in the second quarter from 121% in the first quarter, and the stock was up 23% today.

During the quarter they repurchased $236.4 million of their convertible debt for $195.7 million, a 17% discount to par, resulting in a $36.8 million net gain.

KeyBanc Capital Markets said the results were solid and the company looks “well positioned to gain share in content delivery.” Piper Sandler said the turnaround from the new management team is going “fairly smoothly” and there are a number of initiatives the company is undertaking over the next 12-18 months that can drive growth. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Rocket Lab USA (RKLB – $7.03) has had to postpone the 40th Electron launch – the third for Capella Space – to August 6, due to strong winds at their New Zealand Launch Complex 1.

Rocket Lab announces earnings next Tuesday after the close. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $2.02) appointed Dr. Adrian Keppler to its Board of Directors. He has spent more than 15 years as a C-level executive in the additive manufacturing industry, including as CEO Of EOS, a German provider of 3D printing solutions. He will help Velo3D increase adoption of its Sapphire printers in Europe. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Aptose Biosciences (APTO – $3.66) was hit for a 94¢ per share loss on Monday on huge volume but no news, and is steadily bouncing back. They will announce June quarter results after the close next Thursday. Analysts expect a loss of $2.01 per share, in a pretty wide range from $1.50 to $2.33. APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Compass Pathways (CMPS – $8.98) said they lost 62¢ in the June quarter, better than the 70¢ loss expected. On the conference call (AUDIO HERE), they said the COMP360 Phase 3 pivotal program in treatment-resistant depression is underway and on track, while the Phase 2 trials in anorexia nervosa and post-traumatic stress disorder (PTSD) are ongoing.

For the September quarter, they expect to use up to $18 million in cash, and $80 million to $90 million for the full year. They finished the June quarter with $148.2 million in cash. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2023

Inovio (INO – $0.47) reports June quarter results next Wednesday, after the close. Analysts expect a 14¢ per share loss. As always, it will be news on the various clinical trials that moves the stock. INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: Mid-2024

Invitae (NVTA – $1.23) reports June quarter results next Tuesday, after the close. The consensus is expecting revenues to fall 12.0% from last year to $120.2 million due to discontinued businesses, with the per-share loss dropping from 68¢ last year to 37¢ this year, in a range from -31¢ to -45¢. All eyes will be on the cash burn, with a revenue beat a nice plus. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

Medicenna (MDNA – $0.37) reported a June quarter loss of four cents a share. The Safety Review Committee cleared the next MDNA11 Cohort 6 dose escalation in the Phase 1 ABILITY trial as there were no protocol defined dose-limiting toxicities. They’ll hold an MDNA11 clinical update next Wednesday with a conference call to discuss data from cohorts 5 and 6, the recommended dose for monotherapy expansion, and details on their Phase 2 trial design.

CEO Fahar Merchant said: “We are encouraged by the safety profile of MDNA11 to date, in addition to the prolonged and persistent single-agent activity in heavily pre-treated, end-stage cancer patients, even though the purpose of the Phase 1 ABILITY study was to evaluate the safety of MDNA11. We look forward to evaluating MDNA11 in a Phase 2 patient population in which the patients are less heavily treated in clinically relevant tumor types and may therefore be more likely to respond to immunotherapy treatments such as MDNA11.”

In the September quarter they will report initial anti-tumor activity data from Ability’s fifth and sixth dose escalation cohorts and begin the ABILITY trial’s MDNA11 Phase 2 monotherapy arm. In the December quarter they’ll give us a clinical update from the monotherapy arm and start the MDNA11 plus pembrolizumab combination arm.

Click for larger graphic

Medicenna has until October 23 to regain compliance with Nasdaq’s $1 a share minimum bid requirement. They finished the quarter with $29.6 million in cash, which is enough to get them through the MDBA11 trial and the September 2024 quarter. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

TG Therapeutics (TGTX – $11.20) reported Briumvi sales doubled from the March quarter to $16.07 million. But that missed both the Wall Street consensus for $17.95 million and the reckless Cantor Fitzgerald $24 million to $32 million estimate. They lost 34¢ a share versus the -25¢ expected.

On the conference call (TRANSCRIPT HERE), management said they have had over 1,200 Briumvi prescriptions since launch, including over 800 in the June quarter, from over 340 healthcare providers at more than 225 centers across the US. Their team now has payer coverage in place for approximately 80% of covered lives. It’s important to realize that there’s about a six-week lag between the prescription and the first infusion, so there is built-in revenue growth for the September quarter. Analysts are looking for $47.15 million in the September period and – get this – only $39.02 million for December!

TG signed a very nice European distribution deal with Neuraxpharm. The total deal size is $645 million with over $150 million in upfront and near-term milestones, tiered double-digit royalties up to 30%, and – most important – an option to buy back all rights under the commercialization agreement for a period of two years in the event of an acquisition of TGTX.

H. C. Wainwright raised their target price from $34 to $41 in a well-timed slap at Cantor. I’m moving TGTX back to a Buy under $12 for a target price in a buyout of $30 or more now that the MS drug is approved. I added it to the Top Buys Near-Term list.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Second half of 2024 or never

Inflation MegaShift

Gold ($1,969.30) continues to trade in a $1,940 to $1,970 range. The fractal dimension clearly is in a consolidation move towards the 55 level.

Bob Elliott is a smart guy. He wrote an interesting blog post: The Role of Gold In A Portfolio.

Miners & Related

Coeur Mining (CDE – $2.71) announces June quarter results after the close next Wednesday, followed by a conference call Thursday morning. The one publishing analyst with a revenue estimate is expecting $225.0 million. Five analysts with earnings estimates range from a loss of four cents to a loss of nine cents, with an average of a six-cent loss.CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $5.93) reported June quarter revenues down 7.0% from last year to $146.7 million, but that beat the $133.11 consensus. The pro forma loss of two cents a share was half of the expected four-cent loss. They finished the quarter with $160.2 million of unrestricted cash. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sprott Inc. (SII – $32.13) reports June quarter results next Wednesday morning. There are no consensus estimates. Buy SII under $40 for a $70 target price.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $29,206.49) saw the most concrete rules proposed yet from Congress for a framework to regulate cryptocurrencies. The bill passed by the House Financial Services Committee would define when a cryptocurrency is a security or a commodity and expand the Commodity Futures Trading Commission’s oversight of the crypto industry, while clarifying the Securities and Exchange Commission’s jurisdiction, as many crypto advocates including me complain of the agency’s overreach.

Representative Patrick McHenry, Chairman of the House Financial Services Committee, said:,”As other jurisdictions like the UK, the EU, Singapore, and Australia have moved forward with clear regulatory frameworks for digital assets, the United States is at risk of falling behind. We intend to change that today.” Bravo!

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $19.30) is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $81.73

Oil is over $80, gasoline prices are at a 2023 high, and the paper oil bears are getting crushed by the steady bullish news from the physical market. The Energy Information Administration just reported the largest U.S. weekly crude draw in history and the trend is expected to continue. Next week’s preliminary US crude storage figure shows a small build, but this quickly reverses the following week. US commercial crude storage could fall to 2022 level by the end of August.

Looking at Kpler tanker traffic over the coming weeks, US crude exports are expected to remain elevated, while US crude imports remain low. This combined with flat US oil production is a recipe for much lower crude storage.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

US oil production remains flat around 12.6 million barrels a day, slightly lower than the May production average of 12.65 million barrels a day. Typically, production starts to meaningfully grow by the end of the September quarter and into the December quarter. If we don’t see similar momentum this time, it implies that US oil production has already peaked for the year. Given the rig count drop, that is a very high possibility.

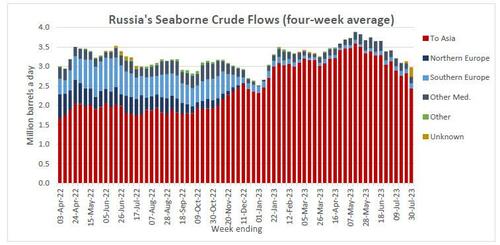

Russian crude shipments tumbled to the lowest since January as the Urals price jumped to $64.37 in July, far above the G-7 price cap for Russia’s oil, set at $60 a barrel. Moscow continues to cut supply to international markets. Russia’s four-week average crude shipments fell by 154,000 barrels a day (b/d) to 2.98 million b/d, down by 905,000 b/d from their peak in mid-May and 400,000 b/d below the level seen in February.

Click for larger graphic

Click for larger graphic

The July 2026 Crude Oil Futures (CLN26.NYM – $67.05) are a Buy under $65 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $37.22) is a Buy under $35 for a $100+ target.

Energy Fuels (UUUU – $6.07) will go up faster than the price of uranium goes up. Has there been a more impressive large-scale energy transition than France in the 1970s and ’80s? Almost as if they found some magic rocks that gave off energy.

Click for larger graphic

UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

Focus on what you can control:

Click for larger graphic h/t @BrianFeroldi

Click for larger graphic h/t @BrianFeroldi

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

Your learning ChatGPT Superprompts Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $191.17) – Buy under $150 for new iPhones

Corning (GLW – $33.57) – Buy under $33, target price $60

Gilead Sciences (GILD – $75.53) – Buy under $80, target price $120

Meta (META – $313.19) – Buy under $250, target price $400

SoftBank (SFTBY – $24.18) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $17.82) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $46.18) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $20.24) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $24.42) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $8.26) – Buy under $10, target price $40

Rocket Lab (RKLB – $7.03) – Buy under $13, target price $30+

Velo3D (VLD – $2.02) – Buy under $6, target price $50

$20-for-$1

Akebia Biotherapeutics (AKBA – $1.51) – Buy under $2, target $20

Aptose Biosciences (APTO – $3.66) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $8.98) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.47) – Buy under $7, hold a long time

Invitae (NVTA – $1.23) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.37) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.88) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $11.20) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($23.69) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $25.00) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $28.42) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.25) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $25.83) – Buy under $30, target price $50

Coeur Mining (CDE – $2.71) – Buy under $5, target price $20

First Majestic Mining (AG – $5.93) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.31) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.23) – Buy under $10, target price $25

Sprott Inc. (SII – $32.13) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $29,206.49) – Buy

Grayscale Bitcoin Trust (GBTC – $19.30) – Buy

Ethereum (ETH-USD – $1,831.82) – Buy

Grayscale Ethereum Trust (ETHE – $11.18) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $67.05) – Buy under $65; $200+ target

United States 12 Month Oil Fund, LP (USL – $37.22) – Buy under $35; $100+ target

EQT (EQT – $41.73) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.07) – Buy under $8; $30 target

Freeport McMoRan (FCX – $43.05) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $32.82) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $24.90) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.38) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $30.84) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.22) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $0.93) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.45) – Hold for buyout

Graphite Bio (GRPH – $2.57) – Hold until they update their strategy

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

ON TGTX:” an option to buy back all rights under the commercialization agreement for a period of two years in the event of an acquisition of TGTX.”

It seems like this would be fishing for a buyout bid; if another company is interested in TGTX by July 2025 that would really be the cutoff date to fish or cut bait. (Sorry about all the fishing metaphors). So I actually find that clause very encouraging.

Yes.

At $81.73 a barrel , how is the SPR going to get refilled if there is a cap on oil at $70.00? Just sayin. I am glad that Fitch lowered the US credit rating even if it did nothing. At least it brings attention again to the fact that the central government is on a path of self destruction. If we continue to kick the can

down the road and continue to just raise the debt ceiling because we have out of control spending eventually something is going to break and when it does it will get very ugly. IMO

Where was Fitch when Pres. Trump added 25% of entire national debt in just 4 years ?

TGTX: On your summary: Probable time of next financing: Second half of 2023; has this been moved back in view of the Neuraxpharm deal? Also I read somewhere that the CEO is on record as saying that he himself would finance any future cash needs; your thoughts please.

Thank you!

MM–similar question to mine above.

Now that’s my kind of CEO. Someone who has enough confidence in himself and the company he is navigating to put up his own money if the company needs future financing. Perhaps they should put that clause in every potential CEO’s contract. You run the company down , you finance future cash needs. That would hold their feet to the fire!! Thanks MM for your input. I bought some more today at $10.00 and change.

Right on! As for ARTH, you say to TN, “you ran ARTH down, now you pay personally to keep it going, instead of diluting the retail shareholders to pay your salary for producing almost no sales.”

Same goes for management of APTO whose salaries are way out of proportion to their accomplishments.

Yes, the second half of 2024 at the earliest, and probably never if Briumvi keeps growing at this clip. It isn’t easy to handle 50%-100% sequential growth. It’s not just about shipping the drug. Providers have to be onboarded, insurance dealt with, salespeople hired and trained, and so on. But I believe the demand is there.

I bought some more TGTX today

TG Therapeutics, Inc. (NASDAQ:TGTX) shareholders will have a reason to smile today, with the analysts making substantial upgrades to this year’s statutory forecasts. The consensus statutory numbers for both revenue and earnings per share (EPS) increased, with their view clearly much more bullish on the company’s business prospects.

After this upgrade, TG Therapeutics’ eight analysts are now forecasting revenues of US$126m in 2023. This would be a substantial 425% improvement in sales compared to the last 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 48% to US$0.65. Yet prior to the latest estimates, the analysts had been forecasting revenues of US$91m and losses of US$0.89 per share in 2023. So there’s been quite a change-up of views after the recent consensus updates, with the analysts making a sizeable increase to their revenue forecasts while also reducing the estimated loss as the business grows towards breakeven. from Simply Wall Street

It is useful to watch changing analyst estimates and consider the resulting sentiment. Buy when sentiment is low, sell when sentiment is highly optimistic. When TGTX was in the 30’s, sentiment was very optimistic as if the stock was going to the moon, over 100. Even the usually optimistic MM maintained a target buyout price of only 25. I got sucked into the optimism and didn’t want to sell, for fear of missing out on one of the few NWI picks that come once in a decade.

There will be more buying opportunities after a good but not great quarterly earnings report when sentiment will become pessimistic. Save cash.

I sold my TGTX just to clear I am not patient enough to wait I am 84 yrs old

Smart. No elderly person should be gambling with these spec stocks, unless he is wealthy and bored.

What is the common sales trajectory for blockbusters in the making?

Frank Christensen?

MM–on TGTX, with the Neuraxpharm distribution deal, do you still think TGTX will need to do a financing in 2nd half of 2023? That would be dilution. But with $150 million upfront and additional milestone cash and growing sales, they might not need any more financing. Wasn’t there some financing recently when the stock was $34? That was a good move. But financing at $10 would be seen as a negative if the next Q sales don’t show continued rapid growth.

Has anyone heard of VERSES, an up and coming Ai stock? Thinking of buying some soon. Only $1.10 at this point.

If I recall, rather than scraping and mining all of the internet, they only scrape and mine all of an enterprise’s data. Interesting concept and perhaps much more manageable than the internet. Supposedly they can send your robots or stock pickers around the warehouse in an optimal manner. Not sure they have a moat around their ideas. nor am I sure it is a viable business.

Had not heard of it but I bought a few shares. Up almost 20%.

Thanks!

William

Hi Guys, have a question on Uranium stock. I came across a OTC stock on uranium from Canada called “Traction Uranium Ltd” (TRCTF). I would like to know what do you guys think about it, pros and cons. Also would be great if you can recommend any other ones. MM, I would really love to have your thoughts on this. Thank you all.

https://tractionuranium.com/

NGENF (very long) I hope some of you have bought into NGENF. Up over 10% today on high volume based on last night’s press release. They got the FDA green light to begin giving their drug to Spinal Cord Injury patients. In less than a year, this stock will be a ten-bagger or a lot lower. And will have plenty of room to run after that,

https://nervgen.com/nervgen-pharma-to-proceed-with-landmark-phase-1b-2a-clinical-trial-for-nvg-291-in-spinal-cord-injury-having-completed-fda-review-and-received-irb-approval/

Chris, thx for the alert but Im confused by your statement that a year from now NGENF will be “a ten bagger or a lot lower” – what do you mean by a lot lower??

If the drug has good effects in SCI patients, it’s an easy 1000% gain. If it doesn’t, share price will be a lot lower than now.

If it works, I anticipate that after the 10x jump, it will continue to go up to $50 as it is tried in other diseases such as stroke, MS, ALS, etc.

Like you, I’m in on both NGENF & ACXP.

NGENF stated in your link above that “recruitment is anticipated to happen relatively quickly with results expected by mid-2024. Results from the subacute cohort (10-49 days post-injury) are expected in late 2024/early 2025.”

Given that not much news is expected for almost a year I’m anticipating the stock price to fall back from it’s pop & anticipate having plenty of opportunity to add in the $1.15 to $1.25 range that it has been trading at the last several months.

Totally agree about NGENF. There may be follow through buying tomorrow, but usually pullbacks occur when surprise good news dissipates. The risk is that preclinical (animal) good results don’t apply to humans as effectively. Whatever this risk is, buy low to maximize returns.

ACXP has a business update on 8/14. We want to know how many patients have enrolled in the new trial comparing ACXP’s drug to the standard of care, vancomycin. My average cost from a year ago is $4.44. I’m wondering whether to add now or wait until after 8/14. The stock plunge recently may portend bad news about enrollment.

Yes. I think you may well have the chance to buy it below $1.25 again, but I would buy some here just in case it doesn’t fall back. You can always add more if the price drops back. While chronic SCI results are expected by mid-2024 (less than a year), that doesn’t mean there will be no news until then. The news flow will be:

1st chronic SCI patient enrolled

Chronic SCI trial fully enrolled

1st Acute SCI patient enrolled

Dosing of chronic SCI patients begins (this will happen at the end of the 4-week baseline measurements and continue for 12 weeks)

Acute SCI trial fully enrolled

AND THE BIG ONE: News leaks out that some of the chronic patients who haven’t improved in years, are getting better.

If the chronic SCI trial begins at the end of this month, it will conclude around the end of this year. I think we will hear some results well before July of 2024.

Plus, just like the $3.2 M grant received from Wings for Life last Q, NervGen could receive additional grants from DoD, American Stroke Association or other organizations.

We don’t know whether the SCI patients will have a life-changing outcome where they can become independent and enjoy life, or merely have a slight improvement. Many cancer therapies merely prolong life by a few months, but make big money for Big Pharma. In like manner, a small improvement for SCI patients can make good money for NGENF.

I like both studies–recent SCI and chronic SCI. For recent SCI patients, it’s harder to get matched groups, since they may diverge without any treatment, so it is harder to judge whether the agent gives a better result than no treatment. But chronic SCI patients are stabilized at their level of disability, so matching groups is easier, and the trial should be more meaningful.

MM,

I noticed that you didn’t mention anything about INO announcing a 30% cut in staff as part of a restructuring effort. When are we ever going to see anything good from this company?

TGTX–think of the shorts as your friend. They are giving us more attractive buy prices. They know the great potential of Briumvi, and are looking to buy after they short it down to the lowest price.

There doesn’t seem to be much support until about the $8 level so that is where I’m looking to get in. I’ll be very happy with that if I can get it.

On FDA approval for Briumvi, the stock was about $10. There is some support just before approval at $8, but real long term support is at $5. If the next 2 quarters of sales are excellent but not outstanding, $8 may come, and will be a good buy point. But save money for the scenario where 4 quarters away the sales are good but not great, offering a $5 buy price and a buyout of $10-15. If the shorts are pessimistic in the extreme when sales are very good, we could still get a $5 buy price and a buyout of $25, MM’s target.

MM – Virtually all of your international recommendations were initially made 5+ years ago (with one exception) and are very China-focused. Given today’s global market context, do you still strongly believe that China and your recommended funds represent the most attractive international investing opportunities? If not, I would appreciate your current best thinking in this regard.

I’m not MM, but China is rapidly becoming irrelevant as other Asian countries are becoming more developed.

Let’s hope so. Doing business with a big tyrant is unsavory and ultimately dangerous. We need to build production in these other Asian countries.

Whats going on with ENVX the last 3 weeks. It’s been getting killed

Mm,do we have to assume a reverse split is in the near future for nvta

CDE: What happened today with CDE? Down 9%. Is this a good time to buy this? I have not heard the earnings and conf call. Please chime in to give an idea if it is a good time to DCA here. Thank you all.

The new Radar Report for 8.10,23 is posted.