Dear New World Investor:

One year ago, the Fed said interest rates would remain lower for longer, they were unlikely to raise rates until 2024, they believed a recession was unlikely, inflation was transitory and not a problem, and inflation should fall to 2% in 2022. Wrong on every count.

Yesterday, they raised the Fed funds rate by 75 basis points (3/4 of a percent) for the third consecutive time, bringing the funds rate to a new range of 3.0% to 3.25%, its highest level since 2008. Three 75-basis-point rate hikes in a row are unprecedented since the Fed explicitly started targeting the Fed funds rate to conduct monetary policy in the late 1980s. And Chairman Powell said they are split between raising another 100 basis points versus 125 basis points by the end of this year.

As I’ve said, they are driving at high speed with their eyes firmly fixed on the rearview mirror of employment and the housing component of the Consumer Price Index. Bizarrely, the Fed policy statement indicated a stronger economy, saying recent indicators point to modest growth in spending and production, while we already are in a Fed-induced recession.

Chairman Powell hammered home that the culprit is the labor market. Nothing to do with a war, supply chain disruption, ending virus lockdowns, record fiscal stimulus, or massive Fed Quantitative Easing. No, it’s all because too many people have jobs and wages. How dare they!

The Fed said they expect to raise interest rates three more times, twice this year and once in 2023. After that, they anticipate cutting rates in 2024 and 2025 as the economic growth and inflation outlooks improve. They raised their inflation projections for the core Personal Consumption Expenditures Index from ending the year at 4.3% and declining to 2.7% next year to ending the year at 4.5% and falling to 3.1% next year. We get the next PCE report on September 30.

The Fed increases strengthen the dollar, forcing other countries to raise rates or suffer severe inflation. Globally, 32 central banks, a record share, are in a hiking cycle. The Bank of England raised its policy rate today by 50 basis points, to 2.25%, in a 5-4 decision. Three officials wanted 75bps and one wanted 25bps. Norway’s bank raised 50bps, to 2.25%. Even Switzerland gave up on its eight-year, negative-rate era, raising 75bps to 0.50% in its most aggressive tightening action in two decades.

Stocks tanked.

Click for larger graphic

Click for larger graphic

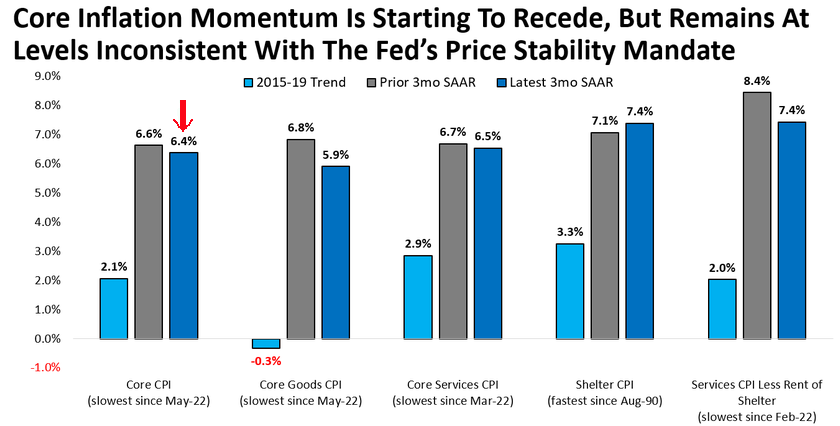

In Powell’s press conference, he said: “If you look at Core Personal Consumption Expenditures Index inflation on a three month, six month, and twelve month annualized basis, that’s a good indication of where inflation is today.” Right now that “blend” is 4.3% and we can assume they want that closer to 2.5%.

Click for larger graphic

Click for larger graphic

The yield spread between the two-year and ten-year Treasury notes now is more inverted than the last two major bear markets in 2000 and 2008. Things are already breaking – the housing market, the foreign dollar funding markets, the revolving debt markets, the venture capital market, etc.

The average bear market peak to trough decline is 37.3% over an average duration of 289 days. Those averages say this bear market ends next month on October 19, the 35th anniversary of Black Monday, with the S&P 500 at 3020. Of course, everyone will be maximum bearish at the bottom.

Click for larger graphic

Click for larger graphic

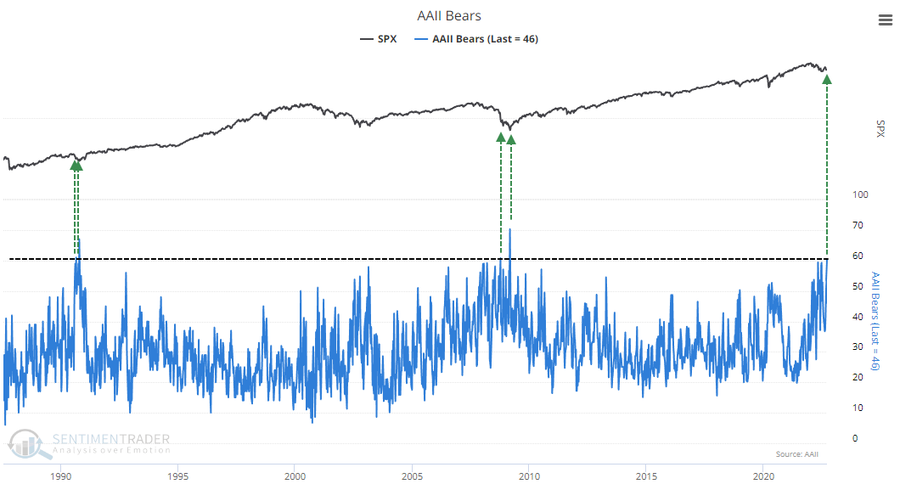

The American Association of Individual Investors bulls fell to 17.7%. The low so far this cycle is 15.8% in mid-April. The bears jumped to 60.9%, above the 59.3% in June. This is the highest reading since March 2009 when they were 70%. They got to 60% on October 8, 2008. They are above 60% for only the fourth time in the history of the survey. The one-year returns after the others: +22.4%, +31.5%, +7.4%, +56.9%.

Click for larger graphic

Click for larger graphic

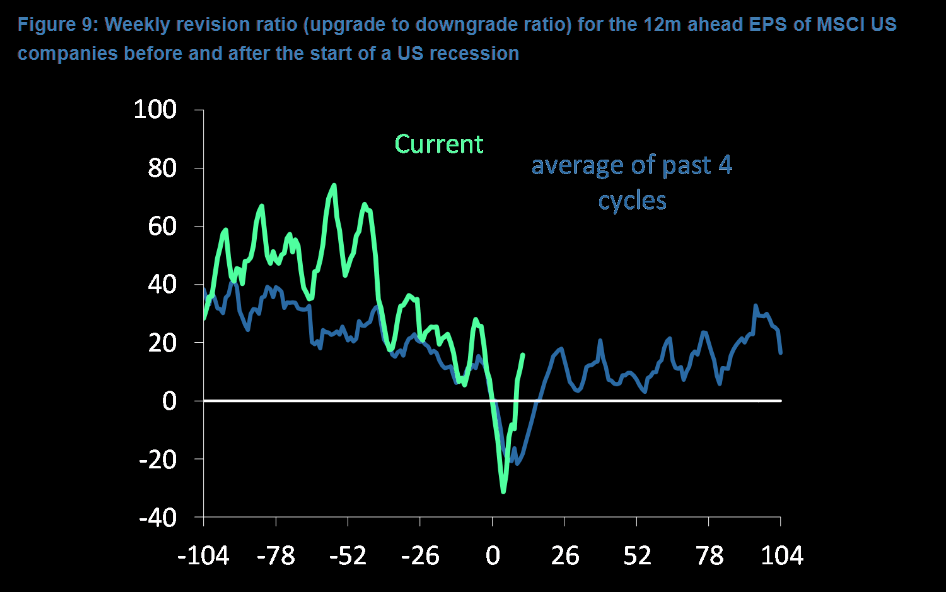

Even though a contraction in earnings has yet to materialize, analysts’ earnings revisions have been downshifting since last summer and turned negative this year. As you can see in the chart below, these earnings revisions have been tracking the pattern seen in previous recessions. Analysts have priced in the elevated recession risk. However, there are signs of bottoming out in the earnings revisions metric, which suggests that large earnings declines would likely be avoided.

Click for larger graphic

Click for larger graphic

During the previous period of stagflationary nominal growth from 1967 to 1980, commodities and gold outperformed equities and bonds. Everyone needs to own some gold, silver, oil, and uranium.

Market Outlook

The S&P 500 lost 3.7% since last Thursday and is just 120 points above the June 16 low. The Index is down 1,008 points or 21.1% year-to-date. The Nasdaq Composite lost 4.2% as tech stocks continued their freefall and is down 29.3% for the year. The small-cap Russell 2000 was hardest-hit, dropping 5.6%, and is down 23.3% in 2022.

The fractal dimension just touched full consolidation last week and down-ticked slightly this week. I wouldn’t call it a new downtrend yet, but another down week or a break of the June 16th lows probably will indicate a multi-week downtrend is underway.

Top 5

Changes this week: None

Near-Term – chronological order

AAPL Apple – New iPhone preorders

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphite Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model estimate for real GDP growth in the September quarter fell (again) from +0.5% to +0.3% after the most recent housing starts report cut the estimate for residential investment growth. The Fed seems to be targeting employment and housing, so I expect this to be a drag on the economy for quite a while.

Click for larger graphic

Click for larger graphic

The official first estimate of September quarter real GDP comes at 8:30am on October 27, 13 days before the midterm elections.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, September 23

RKLB – Rocket Lab – Unspec. – BofA Industrial Innovation Summit

Monday, September 26

Short Interest – After the close

Wednesday, September 28

SCYX – ScyNexis – 9:30am – Special Meeting of Shareholders

APTO – Aptose Therapeutics – 3:25pm – Cantor Oncology, Hematology & HemeOnc Conference

Thursday, September 29

June quarter GDP – 8:30am – Third estimate

SCYX – ScyNexis – 12:00pm – Ladenburg Thalmann Healthcare Conference

Friday, September 30

Personal Consumption Expenditures Index – 8:30am – Event

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations are typically very low. At the same time, Initial Public Offering valuations had moved very high. We were seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors make 5x to 10x in a reasonable, three- to four-year period if they buy at those valuations. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Algernon Pharmaceuticals (AGNPF – $4.30) decided to advance Ifenprodil for idiopathic pulmonary fibrosis with cough as its key indication. They filed a request for Orphan Drug Designation with the FDA for the use of Ifenprodil as a treatment for IPF. Orphan Drug Designation qualifies them for incentives including tax credits for qualified clinical trials, exemption from user fees, and a potential seven years of market exclusivity after approval.

CEO Chris Moreau did an update on the stroke program:

They also received C$450,000 from a refundable tax credit program from its clinical research work in Australia, bringing them to a total cash refund received of over C$3.0 million.AGNPF is a Hold for the Phase 2b IPF/chronic cough results.

Primary Risk: Ifenprodil fails in clinical trials.

Clinical stage of lead product: Phase 2/3

Probable time of first FDA approval: 2023

Probable time of next financing: 2022

Arch Therapeutics (ARTH – $0.02) will present AC5 at the “Innovation Spotlight: Shining a Light on Bold Ideas in Wound Care” session at the 2022 Symposium on Advanced Wound Care on October 16.

Under the terms of the recently issued Senior Secured Convertible Notes, Norchi has to uplist to the Nasdaq National Market by February 15. In order to do that he has to reverse split the stock and do an offering at the time of the uplisting to raise sufficient cash to support operations for at least one year and meet the minimum stockholders’ equity requirement.

This is a big gamble. I’ve seen this work IF he has really good news to announce after the uplisting. He’ll also need a much better stock market – this will be like an Initial Public Offering targeting institutional investors. That also means he needs a real investment banker, not one of these “best efforts” bucket shops. We’ll see what the prospectus filing looks like. ARTH is a Hold for a buyout.

Primary Risk: AC5 fails to sell or the internal trial fails.

Clinical stage of lead product: External approved. Internal trial 2023

Probable time of first FDA approval: External done. Internal 2023

Probable time of next financing: June 2022 quarter

Compass Pathways (CMPS – $12.48) has a very good updated presentation showing their expanded pipeline.

Click for larger graphic

Click for larger graphic

CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2024

Probable time of next financing: Mid-2023

Invitae (NVTA – $2.56) released a new study in JAMA Network Open, underscoring the clinical utility of the American Society of Breast Surgeons guidelines recommending universal genetic testing for patients with breast cancer, and showing universal testing improves patient outcomes. This is how genetic testing will become mainstream medicine. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

ScyNexis (SCYX – $2.46) has a special meeting of shareholders next Wednesday to increase their authorized shares from 100 million to 150 million. Vote Yes. Buy SCYX under $2 for a first target price of $20 now that Brexafemme is approved and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: mid-2022

Probable time of next financing: second half of 2023 or never

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Corning (GLW – $30.72) “is a much bigger company than it was five years ago, and has some business segments like optical communications with very positive outlooks. Despite this, shares are trading in the low $30s, the same price they were at almost five years ago. Trading with a 7.4x EV/EBITDA multiple, and a dividend yield significantly above its ten-year average, shares are looking quite attractive.” So says this article on Seeking Alpha, and I strongly agree. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My first target is $60 in 2023 .

Meta Platforms (META – $142.82) is going to cut costs by 10% , mostly from reduced employment. Meta has begun cutting a significant number of staffers by reorganizing departments and giving affected employees a limited window to seek other roles. Chairman Powell should like that! META is a Buy under $250 for a $400 target in 2023 or 2024.

Other Tech

QuickLogic (QUIK – $6.24) said current institutional investors bought 487,279 shares, or about 3.9% of the outstanding stock, at $6.57 each in a direct offering with no broker. This almost certainly means some firm came to them to buy a big position, and QUIK offered a few other funds the chance to get stock without running up the price. I don’t think they needed the money, but as the old saying goes:

They call it legal tender

That green and crackling stuff.

It’s tender when you have it

But when you don’t, it’s tough.

QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets, and wearables.

Primary Risk: New sensor hub competitor emerges.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $4.31) held their very good Investor Day yesterday (SLIDES HERE and presentation on YouTube).

They will build their Archimedes Test Complex at NASA’s John C. Stennis Space Center in Mississippi to test the engines for their reusable Neutron rocket. By leveraging NASA’s existing infrastructure and test stand Rocket Lab can fast-track Neutron’s first launch. The Mississippi Development Authority is investing in the project.

Yahoo Finance interviewed CEO Peter Beck HERE. Stifel reiterated their Buy recommendation and set a $15 target price. Everyone needs to own this stock. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Velo3D (VLD – $4.36) is another stock that everyone needs to own as manufacturing returns to the US. European companies are shifting manufacturing to the US because our energy costs are so much lower. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,680.00) is sitting at a critical level at its 200-week moving average at $1681.10. The Commercials – the miners – have their smallest short position in three years. The hawkish Fed could easily have dropped it another $100 yesterday but it went up instead, in spite of the dollar hitting a 20-year high. The fundamental setup is getting better by the day.

Miners & Related

Coeur Mining (CDE – $3.00) jumped after it sold its non-core Crown and Sterling holdings in Southern Nevada to AngloGold for $150 million at closing and $50 million deferred, to be paid when the mines attain a total resource of at least 3.5 million gold ounces. The holdings comprise approximately 35,500 net acres and are located adjacent to AngloGold’s existing gold projects. The deal will close by the end of the year. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $6.08) is my favorite way to own gold because it offers Industry-Leading Growth At An Attractive Valuation. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $19,381.53) slipped under $20,000 and the usual suspects were quick to say it’s a worthless Ponzi scheme. It behaves like a high-risk/high-reward asset in a risk-off environment. I still think the Grayscale Bitcoin Trust (GBTC- $11.74) is the best way to buy it, as the large discount to net asset value gives you a significant margin of safety.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $83.58

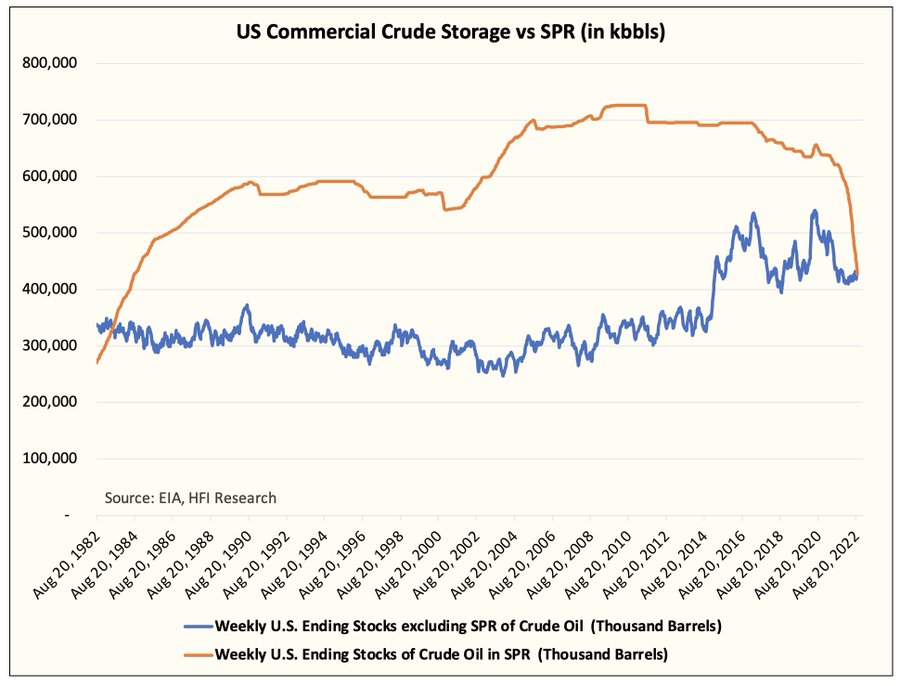

Oil is depressed in the low $80s even as gasoline prices start rising again due to refinery outages. OPEC+ missed their oil production target by a whopping 3.583 million barrels per day in August. But hefty Strategic Petroleum Reserve weekly releases – 6.9 million barrels last week, or~985,000 barrels a day – pressured crude prices. Over the last four weeks, the SPR has injected nearly 950,000 b/d into the market. It now is at its lowest level since August 1984 and for the first time since 1983, US commercial crude storage is now higher than SPR.

Click for larger graphic

The SPR releases are adding 1% of global demand to the market every day but they won’t last forever. They are scheduled to fall to 300,000 b/d in November and stop in December, after the midterm elections. A million barrels of daily supply goes poof. And China has begun running down its crude oil stockpiles, which could signal that refiners are getting ready to boost fuel exports as part of the government’s efforts to revive the economy. Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $29.88) is a Buy under $36 for an $80+ target.

Energy Fuels (UUUU – $5.98) will benefit from Ukraine just asking the US to sanction Russian uranium supplier Rosatom. Spot uranium hit $50 a pound at the open this morning for US nuclear fuel brokers. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

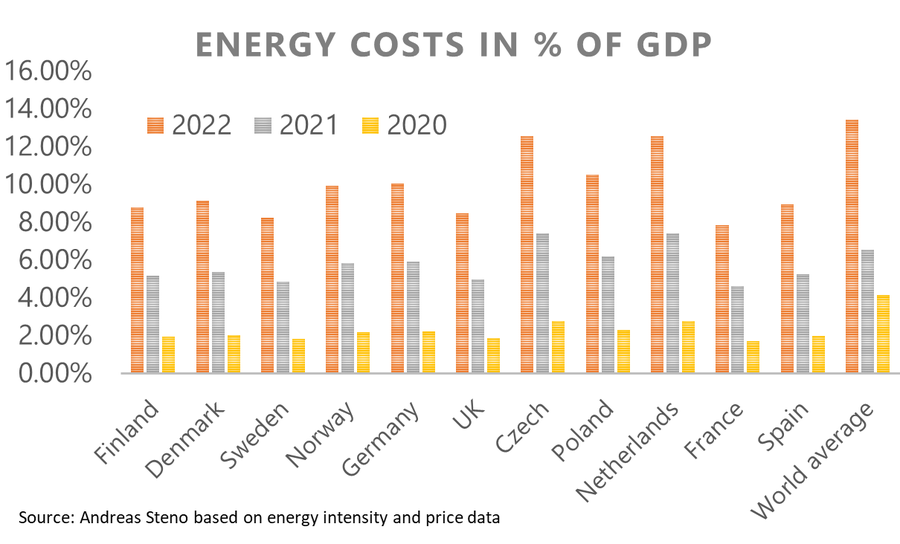

80% of annual European gas consumption happens between October and March

Click for larger graphic

Click for larger graphic

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

Mark Cuban started a company to provide low-cost drugs by mail. If you have any prescriptions that are not fully covered by insurance, his prices can be only 10%-20% of retail, and sometimes lower than your copay. https://www.costplusdrugs.com/medications/

* * * * *

Your listening to a Podcast Curriculum Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.61) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $1.11) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $12.48) – Buy under $20, hold a long time for a 10x return

Graphite Bio (GRPH – $3.01) – Buy under $9, hold a long time

Inovio (INO – $1.77) – Buy under $7, hold a long time

Invitae (NVTA – $2.56) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.86) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.46) – Buy under $2, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $6.09) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $152.74) – Buy under $150 for new iPhones

Corning (GLW – $30.72) – Buy under $33, target price $60

Gilead Sciences (GILD – $63.77) – Buy under $70, target price $100

Meta (META – $142.82) – Buy under $250, target price $400

SoftBank (SFTBY – $18.51) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $39.30) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $8.44) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.32) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $6.24) – Buy under $10, target price $40

Liberty Media Acquisition Corporation (LMACA – $9.85) – Buy under $10, target price $20 to $30

Rocket Lab (RKLB – $4.31) – Buy under $13, target price $30+

Velo3D (VLD – $4.36) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Buy while fixed mortgage rates are low

Bag of Junk Silver – ($19.45) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $20.72) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $24.38) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $15.81) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $23.63) – Buy under $30, target price $50

Coeur Mining (CDE – $3.00) – Buy under $5, target price $20

First Majestic Mining (AG – $7.34) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.31) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $6.08) – Buy under $10, target price $25

Sprott Inc. (SII – $33.41) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $19,381.53) – Buy

Grayscale Bitcoin Trust (GBTC – $11.74) – Buy

Ethereum (ETH-USD – $1,328.08) – Buy

Grayscale Ethereum Trust (ETHE – $9.81) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $27.71) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $30.97) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.95) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $25.56) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.96) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.19) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $29.88) – Buy under $36; $80+ target

Energy Fuels (UUUU – $5.98) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $4.30) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.33) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.02) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First!

2nd

3

@Michael Murphy. Another excellent RADAR. Again, very interesting data on bulls and bears. An interesting phenomenon has been the number of Wall Street Journal editorials dealing with the perils of being behind continued strong Climate change investments as Europe, particularly Great Britain and others taking a bath with their economies, giving very soft suport for continued investments in Windmills and solar panels and changing strategies to open up investments in fossil fuels. DRLL, the ETF whose target is 8000 oil and gas companies that values the equities using good old fashioned balance sheets and P&L statement to measure company health and for dealing with banks to agree to lend money for CAPEX.still having relative stability. I have been asking our very green state to consider this change of sentiment away from alternative energy (except Nuclear and Quebec Hydro) and describing the current Climate Change Gang as “Fossil Deniers” and trying to get a natural gas pipeline from the Marcellus Shale thru PA and NY to RI. Got some support but we don’t have the millions these Climate Change losers do. Say a prayer to St. Jude, patron Saint of lost Causes. Other topics. Would really like to see Gold and the group you mention make their run up. Any thought about Dollar Tree? GLTA

The price of lithium is going through the roof. So EV production is going to have a major struggle to get to the point of doing away with gas vehicles. Also the state of California is taxing heavily lithium production companies even tho they are all in on green energy. Go figure. And Putin is saber rattling by calling up more troops and hinting that he will use the big N word. Hallelujah, the Fed finally gets it. They took away the uncertainty of what exactly they plan to do. At least there is that, even if the pain in the economy is more of a reality now. When interest rates are on parity with the inflation rates we will gain some traction. IMO

This recession will drive oil below 50 bucks a barrel. Just sayin.

Excellent book. Fossil Future: Why Global Human Flourishing Requires More Oil, Coal, and Natural Gas—Not Less by Alex Epstein

Epstein is a funded by the Koch brothers petrochemical billionaires, and a leading climate change denier. Hardly an unbiased assessment. Just another far right comment by Murphy who claims he is “left of Bernie Sanders.” Meanwhile today FL continues to go underwater….

So what about Epstein and Koch? The reality is that there is not enough lithium to produce EV’s for all. How about environmental costs of disposing of all the batteries? You noted the problems with nuclear waste. Alt energy sources will continue to be a minor fraction of global needs. Fossil fuels are here to stay for a long time.

“…Human Flourishing Requires…” is propaganda. This book isn’t an investment book, or an educational book, its disinformation by the ultra rich Koch suckers for their own business. Akin to the tobacco companies “studies” demonstrating that personality types not tobacco caused cancer. BS.

For a New World Investment letter, this author is stuck in the past.

It’s quite amusing to see the right get all up in arms about the environmental impact of alternative energy after ignoring the horrible impact fossil fuels have had on the environment.

Not enough lithium .. give me a break. Do we really think that Elon is building out a future with no thought on batteries?

Come on.

Propaganda notwithstanding, alt energy will remain a minor part of total energy production. Manmade climate change is still debatable. There is very little hard science published–most of it is propaganda suited to specific political agendas. There is no way for laymen like us to know the real truth. That’s a big factor why financial analysts cannot know which speculative biotech will succeed–they get propaganda suited to each companies’ interests.

@Michael Murphy, Epstein is right on target. His conclusions are in sync with Steve Koonin, “Unsettled” and Michale Schallenberger, (several textxs on fossil fuel persistent as a major component of all wmajor energy systems, with an exhortation about the use of Nucklear packages. The impact, from a fiancial and equity point of view settles out with fossils dominating volume and therefor EPS done the line.

MM – you say that “Everyone needs to own some gold, silver, oil, and uranium” yet you don’t have any of these investments in your Top 5, why?

In a raising interest rate/strong dollar environment the LAST thing you want is gold and silver. Just sayin.

The top 5 are either near-term (usually event-driven) or long-term based on projected returns. I think of PMs, oil, and uranium more as uncorrelated holdings.

Hey Mike, what about CWBR? My $1000 turned into $100 on that pick.

Got QID?

Phase 1 trial failed.

I did buy QID options and cashed in for $1000 gain. Thanks.

I cleared out all my QID options this morning. It was a great September( for shorts) but I think we are headed up after the BOE blinked.

Earnings start in a couple weeks and I haven’t seen any negative pre-announcements. If earnings are at least decent, it’s up from here.

MM, You didn’t mention anything about this. I presume this was good news?

Medicenna Presents Preclinical Data Demonstrating Anti-Tumor Activity of its Anti-PD1-IL-2 BiSKIT and Long-Acting IL-4/IL-13 Super-antagonist at Cytokines 2022SEPTEMBER 22, 2022 AT 7:30 AM EDT

Download PDF

— Single agent Anti-PD1-IL-2 BiSKIT™ showed superior efficacy compared to a combination of an anti-PD1 antibody with an IL-2 Superkine in murine models of colon, skin, and breast cancer

–IL-4/IL-13 Super-antagonist displayed monotherapy activity in multiple cancer models and in synergy with an IL-2 Superkine, highlighting its potential to treat immunologically “cold” tumors

TORONTO and HOUSTON, Sept. 22, 2022 (GLOBE NEWSWIRE) — Medicenna Therapeutics Corp. (“Medicenna” or “the Company”) (NASDAQ: MDNA TSX: MDNA), a clinical stage immunotherapy company, today announced presentation of data from two preclinical programs that demonstrate the anti-tumor activity of the Company’s anti-PD1-IL-2 (aka MDNA223) BiSKIT (Bi-functional SuperKines for ImmunoTherapy) and long-acting IL-4/IL-13 super-antagonist (aka MDNA413). The data are featured in two separate poster presentations at the 10th Annual Meeting of the International Cytokine & Interferon Society (Cytokines 2022), which is taking place both virtually and in-person at the Hilton Waikoloa Village, in Big Island, Hawaii.

“Our presentations highlight the versatility of our Superkine platform in designing novel, highly selective immune modulators to treat cancer,” said Fahar Merchant, PhD, President and CEO of Medicenna. “We believe these programs complement our lead MDNA11 program, expand our pipeline of therapies and potentially drive collaborations given the increasing interest recently displayed in the cytokine space. Data from the MDNA223 program show that proliferation of cancer fighting immune cells with the IL-2 Superkine while simultaneously preventing their exhaustion with PD1 inhibition on the same immune cell leads to superior efficacy. In addition, data on our long-acting MDNA413 Superkine demonstrated its potential to reverse the immunosuppressive tumor microenvironment that are known to limit the efficacy of cancer immunotherapies.”

Poster P110: A Next Generation Bifunctional Superkine for Immunotherapy (BiSKIT) Encompassing the Combined Therapeutic Potency of IL-2 Super-Agonist and Anti-PD1

Poster P110 includes preclinical data from in vitro and in vivo studies of MDNA223, a next generation BiSKIT consisting of an anti-PD1 antibody linked to an IL-2 super-agonist (MDNA109FEAA). Anti-PD1 drugs, such as Keytruda® (pembrolizumab), have been approved for a number of cancer indications.

In vitro data presented at the meeting demonstrated MDNA223’s potency against the PD1/PDL1 checkpoint was similar to that of a control anti-PD1 antibody while displaying increased affinity for IL-2 receptor beta (IL-2Rβ) and no binding to IL-2 receptor alpha (IL-2Rα). This enhanced IL-2Rβ selectivity resulted in potent and preferential stimulation of anti-cancer CD8+ T cells over pro-tumor Treg cells. In vivo murine data showed MDNA223 exhibiting a prolonged pharmacodynamic response extending beyond the duration of pharmacokinetic exposure. In addition, the murine surrogate of MDNA223 showed superior efficacy compared to co-administration of anti-PD1 and long acting MDNA109FEAA in murine models of colon, skin, and breast cancer. These data demonstrate the therapeutic synergy resulting from the BiSKIT’s ability to concurrently target PD1 and the IL-2 receptor on the same immune cells (cis-binding approach).

Poster P69: Fc-MDNA413 is a Novel Long-Acting IL-4/IL-13 Super-Antagonist that Suppresses M2a TAM Skewing and In Vivo Tumor Growth Including Synergy with an IL-2 Super-Agonist.

Poster P69 includes preclinical data from in vitro and in vivo studies of Fc-MDNA413, a novel, long-acting IL-4/IL-13 Superkine. Fc-MDNA413 is designed to reverse the immunosuppressive tumor microenvironments (TMEs) of immunologically “cold” tumors by selectively binding to the IL-13 receptor alpha-1 (IL-13Rα1) with high affinity and blocking signaling via the Type II IL-4 receptor (IL-4Rα/IL-13Rα1) expressed on tumor associated macrophages (TAMs) and myeloid derived suppressor cells (MDSCs). It consists of an IL-4/IL-13 super-antagonist fused to the Fc domain for half-life extension.

Data presented at Cytokines 2022 showed Fc-MDNA413 blocking the pathways that induce M2a TAMs and MDSCs to promote cancer growth and demonstrated its potential to treat cold tumors. In vitro analyses showed that the Superkine is 300-times more selective for IL-13Rα1 over IL-13Rα2 (a decoy receptor) compared to a fusion protein consisting of Fc domain linked to wild type IL-13. This superior binding profile enabled Fc-MDNA413 to potently inhibit IL-4/IL-13 mediated functions as measured by pSTAT6 signaling, TF-1 cell proliferation, and M2a polarization of macrophages. In murine studies, Fc-MDNA413 demonstrated sustainable serum exposure at a dose that was well tolerated and inhibited tumor growth as a single agent in melanoma and colon cancer models. In addition, Fc-MDNA413 synergized with an IL-2 agonist in a murine melanoma model, highlighting the advantages of co-targeting suppressive and effector immune cells within an otherwise cold TME.

Copies of the two posters are available on Cytokines 2022’s virtual platform. They will also be posted to the “Events and Presentations” page of Medicenna’s website following the conclusion of the meeting

Yes, but preclinical activity doesn’t move stocks.

Press Releases :: Arch Therapeutics, Inc. (ARTH)

Arth confirms first shipments of AC5 under the company’s new reimbursement support program.

They don’t tell the dollar value but it will show up in the Q3 earnings.

Dear Michael, do you have the results on the following votes (ARTH):

The company filed a proxy statement for the September 29 annual meeting. There are seven items:

1. Elect four directors – vote Yes

2. Approve a reverse stock split of not less than 1-for-100 and not greater than 1-for-200 – vote No Way

3. Approve an increase the number of authorized shares of common stock – vote No

4. Approve, on an advisory basis, the compensation of Executive Officers – vote No

5. Approve, on an advisory basis, how frequently stockholders believe we should conduct an advisory vote on the compensation of our Named Executive Officers – vote No

6. Approve a proposal to grant discretionary authority to adjourn the Meeting, if necessary, to solicit additional proxies – vote No

7. Ratify the appointment of Baker Tilly as independent auditors – vote Yes

Thank you and GOD Bless you!

George

Vote is on Thursday.

MM – you said in a previous report that SCYX had a November 30 PDUFA date, and you said if approved a $20 first PT – is this still correct? Can you give an update? Is there still a 11/30 PDUFA? If not what are the catalysts that will move it to the $20 PT and when.

Yes, 11/30 PDUFA sate

what in your opinion are the chances of approval on 11/30?

MM and all: Is anyone investing in LABU – this 3X biotech sector is at $6, was $60 one year ago and all time low is $4, seems a good risk with limited downside

I have a few hundred shares that I just started to purchase.

I also think it’s a good risk.

William

how is TGTX not a top buy?

pdufa date 12/28 5x

Sam – can you share why you think TGTX is a 5X opportunity please?

@steve

best in class treatment in 10+B this year projected to grow to over 20B buy 2028, market segmented into something like 7 categorizes. we have 350M float IF we can get %5 of that 20+B or 1/3 of our segment of the ms market.

than —– check my math

1B / 350m = 2.8 * pe10 = sp$28

i might bat 300 on a good day so do your own DD

As I recall

Roch makes the drug Ocrevus (ocrelizumab) that Ubri was compared to in the Ultimate 1-2 trial and that drug is forecast to do B7 buy 2028. anti-cd20 is something like 1/3 $ of the MS market and is about 10B and growing. Ubri can get 1/3 of that 3 years out maybe more.

My # 3-5B on MS

Good News for NVTA. First Genetics company appointed to National Quality Forum on Delivery of Health Care for three years. This puts NVTA as part of standards determination nationally

Invitae – Invitae Appointed to National Quality Forum Committee on Quality Standards for Healthcare

So you would think,but if they don’t bring in any revenue from it,it means squat as reflected in the share price

MM, I’m still trying to see if this is good news. Why couldn’t they get 300 patients? Wasn’t the enrollment supposed to be done by Q4 2022 and now it’s going to Q1 2023. Do they have enough cash to make it till then? I’d appreciate your thoughts on these questions. Thanks!!

Bellerophon Announces FDA Acceptance of Change to Ongoing Phase 3 REBUILD Study of INOpulse® for Treatment of Fibrotic Interstitial Lung Disease

WARREN, N.J., Sept. 27, 2022 (GLOBE NEWSWIRE) — Bellerophon Therapeutics, Inc. (Nasdaq: BLPH) (“Bellerophon” or the “Company”), a clinical-stage biotherapeutics company focused on developing treatments for cardiopulmonary diseases, announced today that the U.S. Food and Drug Administration (FDA) has accepted the Company’s proposal to reduce the study size for its ongoing registrational REBUILD Phase 3 trial of INOpulse® for the treatment of fibrotic Interstitial Lung Disease (fILD). The new study size of 140 subjects does not impact the trial’s principal objective or endpoints and maintains power of >90% (p-value < 0.01) for the primary endpoint of Moderate to Vigorous Physical Activity (MVPA) based on the effect size observed in Phase 2.

Following the evaluation of baseline MVPA characteristics, as measured by actigraphy, compliance to treatment and review of safety data of the randomized subjects in the ongoing Phase 3 REBUILD study, the trial’s independent Data Monitoring Committee (DMC) supported reducing the target study size from 300 to 140 subjects.

“With this study size change, we believe that we are well-positioned to accelerate the completion of our Phase 3 REBUILD study,” said Naseem Amin, M.D., Chairman of Bellerophon’s Board of Directors. “With over 100 subjects randomized to date, we expect to complete enrollment in the first quarter of 2023, and anticipate the availability of pivotal top-line data in the third quarter of 2023.”

“The target of 140 subjects maintains a statistical power of greater than 90% for MVPA, which has been accepted by the FDA as the primary endpoint for the Phase 3 REBUILD study,” said Peter Fernandes, Bellerophon’s Principal Executive Officer.

Dr. Steven D. Nathan, M.D., F.C.C.P., Medical Director of the Advanced Lung Disease and Lung Transplant Program at Inova Fairfax Hospital and Chair of Bellerophon’s REBUILD Steering Committee, said, “The revised study size is based on an effect size generated from Phase 2 study data in 44 patients with the same primary endpoint being evaluated in the Phase 3 study, MVPA. The analysis presented to the FDA indicated that the trial remains adequately powered to demonstrate a statistically significant result on MVPA. We look forward to working with the Company to get this study over the finish line soon and build upon and validate the existing body of clinical evidence generated to date for INOpulse.”

The REBUILD study is a Phase 3, randomized, double-blind, placebo-controlled clinical trial evaluating the safety and efficacy of pulsed inhaled nitric oxide (iNO) in subjects on long-term oxygen therapy who are at risk for pulmonary hypertension associated with pulmonary fibrosis. The study plans to enroll 140 fILD subjects who will be treated with either INOpulse at a dose of iNO45 (45 mcg/kg ideal body weight/hr) or placebo. The trial’s primary endpoint is the placebo corrected change in MVPA, as measured by actigraphy.

For further details regarding the protocol and additional information on the REBUILD Phase 3 study of INOpulse for the treatment of fILD, please visit ClinicalTrials.gov and reference Identifier NCT0326710.

The reason this is good news is that “the trial’s independent Data Monitoring Committee (DMC) supported reducing the target study size from 300 to 140 subjects…The target of 140 subjects maintains a statistical power of greater than 90% for MVPA, which has been accepted by the FDA as the primary endpoint for the Phase 3 REBUILD study.”

In other words, INOpulse works well enough that they only need 140 patients to prove it, not 300.

They have enough cash to get to mid-2023. They expect to complete enrollment in the first quarter of 2023, and give us top-line data in the third quarter. So they probably will announce full enrollment, do an offering, and then announce results.

Thanks MM. So in other words, we’re probably not going to see any meaningful price appreciation until they announce complete enrollment in Q1 2023.

Delays in enrollment are a major cause of biotech crapouts. The most important biotech of all, NGENF, enthusiastically recommended by Chris for treatment of major neurologic disease, has had delays in enrollment in Australia due to stupid politics there. Partial clinical holds for unpublished reasons is another example of political sabotage. Great news of funding pushed that stock up to $2, but it has plunged to $1.20.

Looks like the bank of England blinked. Melt up?

What will Joe do now? Gas is rising and the SPR is getting pumped out!!

MM, How come this didn’t move the stock considerably? Is there something I’m missing?

Medicenna Reports Confirmed Partial Response in Pancreatic Cancer and Clinical Update on MDNA11’s Monotherapy Dose Escalation Portion of the Ongoing Phase 1/2 ABILITY StudySEPTEMBER 28, 2022 AT 9:25 AM EDT

Download PDF

TORONTO and HOUSTON, Sept. 28, 2022 (GLOBE NEWSWIRE) — Medicenna Therapeutics Corp. (“Medicenna” or “the Company”) (NASDAQ: MDNA TSX: MDNA), a clinical stage immuno-oncology company, today announced new clinical data on anti-tumor activity from the Phase 1/2 ABILITY study of MDNA11, the Company’s “beta-only” long-acting IL-2 super-agonist. These data include a confirmed partial response (PR) in a fourth-line metastatic pancreatic ductal adenocarcinoma (PDAC) patient that had previously failed chemo and checkpoint inhibitor therapies. The confirmatory scan for this patient continues to show further tumor reduction compared to prior scans, suggesting durable anti-cancer activity following MDNA11 monotherapy. Overall, five of fourteen evaluable patients in the ABILITY study’s low and mid-stage dose escalation cohorts have achieved tumor control (PR or stable disease (SD)) with MDNA11 monotherapy.

“We are excited to report confirmation of a partial response in a patient with late-stage pancreatic cancer, one of the most aggressive tumors that rarely responds to single agent immunotherapy,” said Fahar Merchant, PhD, President and CEO of Medicenna. “Furthermore, four additional patients have experienced tumor control despite the advanced stage of cancer in all patients enrolled in ABILITY’s dose escalation cohorts. This outcome provides early evidence supporting our belief in MDNA11’s single-agent anti-tumor activity and underscores its therapeutic potential as a best-in-class IL-2 agonist. Given that the dose-escalation portion of the trial is designed primarily to evaluate the safety and pharmacokinetics and determine the phase 2 dose, these early signs of potential clinical benefit are particularly impressive as we continue to dose escalate and advance towards the trial’s dose expansion phases early next year.”

The ABILITY study’s dose escalation cohorts are evaluating MDNA11 monotherapy administered intravenously once every two weeks to patients with advanced solid tumors, with the primary objective of evaluating the safety and pharmacokinetics and determining the recommended Phase 2 dose (RP2D). Once the RP2D has been established, a key secondary objective of the trial will be to evaluate the anti-tumor activity of MDNA11 alone and in combination with the checkpoint inhibitor KEYTRUDA® (pembrolizumab) in the trial’s dose expansion phases.

The ABILITY study’s first three dose escalation cohorts evaluated MDNA11 at doses of 3,10 and 30 µg/kg. Patients in the fourth and fifth dose escalation cohorts receive two 30 µg/kg “priming” doses of MDNA11 before stepping up to receive fixed doses of 60 and 90 µg/kg, respectively. The trial is currently enrolling patients in the fifth dose-escalation cohort, with no dose-limiting toxicities, dose interruptions, dose de-escalations, or treatment discontinuations due to safety issues observed to-date. A summary of demographic and therapeutic activity data from all evaluable patients in the first four dose escalation cohorts is provided below.

Patient Demographics

Prior to enrolment in the ABILITY Study, patients in Cohorts 1 to 4 (n=14) had failed up to four lines of systemic therapy.

Prior to enrolment in the ABILITY Study, eleven of fourteen patients (89%) in Cohorts 1 to 4 had relapsed on, could not tolerate, or did not respond to at least one immunotherapy with a checkpoint inhibitor.

Therapeutic Activity

Five of fourteen evaluable patients (36%) have achieved tumor control as defined in the study

To date, MDNA11 has demonstrated a favorable tolerability profile in the monotherapy dose escalation segment of the ABILITY study. New data on MDNA11’s safety, pharmacokinetic and pharmacodynamic profiles are expected to be presented at a major medical meeting in the fourth quarter of the calendar year.

About the Phase 1/2 ABILITY Study

The ABILITY (A Beta-only IL-2 ImmunoTherapY) study is designed to assess the safety, pharmacokinetics, pharmacodynamics, and anti-tumor activity of various doses of intravenously administered MDNA11 in patients with advanced, relapsed, or refractory solid tumors. The trial includes an MDNA11 monotherapy arm, as well as a combination arm designed to evaluate MDNA11 with KEYTRUDA® (pembrolizumab). Approximately 80 patients are expected to be enrolled into the ABILITY Study. Following establishment of the recommended Phase 2 dose (RP2D) and optimal treatment schedule in the study’s dose escalation phase, Medicenna plans to conduct a dose expansion phase that will enroll patients with renal cell carcinoma, melanoma, and other solid tumors in monotherapy and combination settings. For more information, see ClinicalTrials.gov Identifier: NCT05086692.

KEYTRUDA® is a registered trademark of Merck Sharp & Dohme LLC, a subsidiary of Merck & Co., Inc., Rahway, NJ, USA.

The new Radar Report for 9.29.22 is posted.