Dear New World Investor:

What a week! After last Friday’s mini-crash (see below), the S&P 500 entered a bear market on Monday, the Fed raised the funds rate 3/4 of a point yesterday, the biggest increase since 1994, and stocks closed today at their lowest since December 2020. Investors are worried that a more aggressive Fed will cause a recession – wants to cause a recession – while inflation stays high because the factors driving it are not affected by the Fed. That’s the “perfect storm” outlook and I think it’s too negative, although there’s no doubt the economy is slowing quickly and the Fed will keep increasing rates for a while.

The Fed’s increase was widely expected, as is another 3/4 point on July 27 and either 1/2 or 3/4 on September 21. But that should be about it. Their hawkish talk started slowing things down even before the first Fed funds increase, as shown by the negative GDP print for March, May’s 0.3% drop in retail sales as car sales plunged and some supply chain-caused pricing problems eased (lumber, cardboard), The University of Michigan’s preliminary consumer sentiment survey slumped to 50.2 in June, the lowest level ever recorded by the survey that started in the mid-’70s, and this morning’s announcement of 229,000 new unemployment claims was higher than expected. Claims have climbed steadily to the highest level in five months after notching a more than 50-year low in March and are slightly above pre-pandemic levels.

Monday’s selling that put the S&P 500 in bear market territory, down 20% from its all-time high, was the fifth-largest sell program in history. It was a 92:1 down day, the worst Declining Volume / Advancing Volume day since November 18, 2011. Goldman Sachs Prime Brokerage, which services hedge funds, said those worthies sold US stocks for a seventh straight day Monday with the dollar amount of selling on Friday and Monday exploding to levels not seen since April 2008, which means a more frenzied liquidation than what took place in the immediate aftermath of the failure of Lehman Brothers.

Furthermore, much of the action was putting on new shorts. Goldman said that hedge fund short sales climbed “aggressively,” with broad-based investing strategies like exchange-traded funds dominating the flows. Between outright liquidations and shorting, hedge fund net equity exposure is near five-year lows.

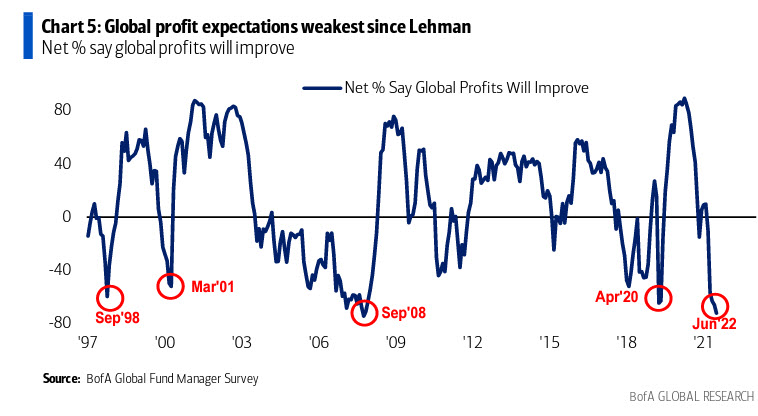

The most recent BofA June survey of professional managers backs this up. Their optimism on global growth fell to a new low of -73%, the lowest since 1994. Global profit expectations fell to -72%, the weakest since September 2008. Major lows in profit expectations also occurred in other Wall Street crisis moments like the failure of Long Term Capital Management, the dotcom bubble burst, the Lehman bankruptcy, and the COVID-19 low.

The most popular description of what the economic backdrop will be for the next 12 months was “stagflation” by 83% of the respondents, the highest level for that outlook since June 2008. And their expectation for global profits:

Click for larger graphic

Click for larger graphic

Not surprisingly, these fund managers are very bearish and already sold:

Click for larger graphic

Click for larger graphic

Individuals are equally negative, with the CNN Fear & Greed Index in “Extreme Fear” territory at 13 and the American Association of Individual Investors overwhelmingly bearish.

Click for larger graphic

Click for larger graphic

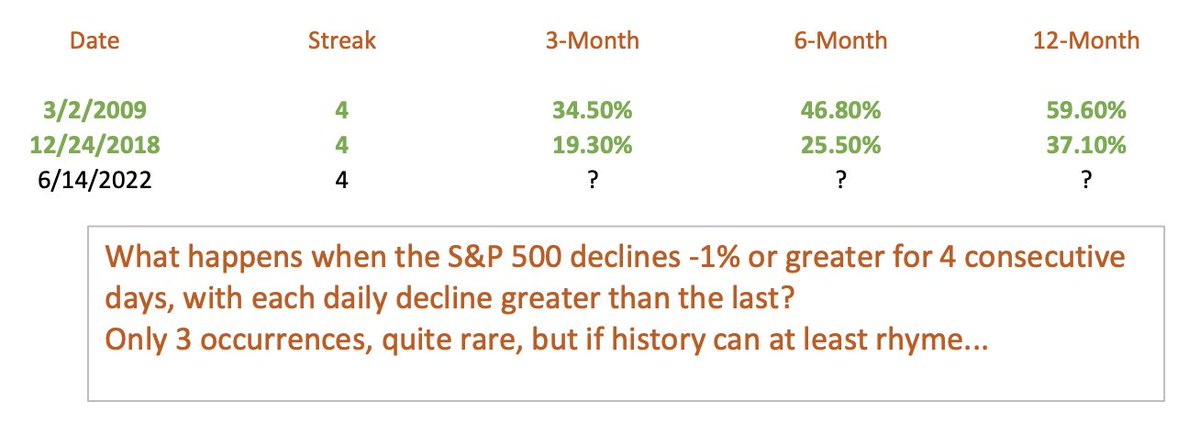

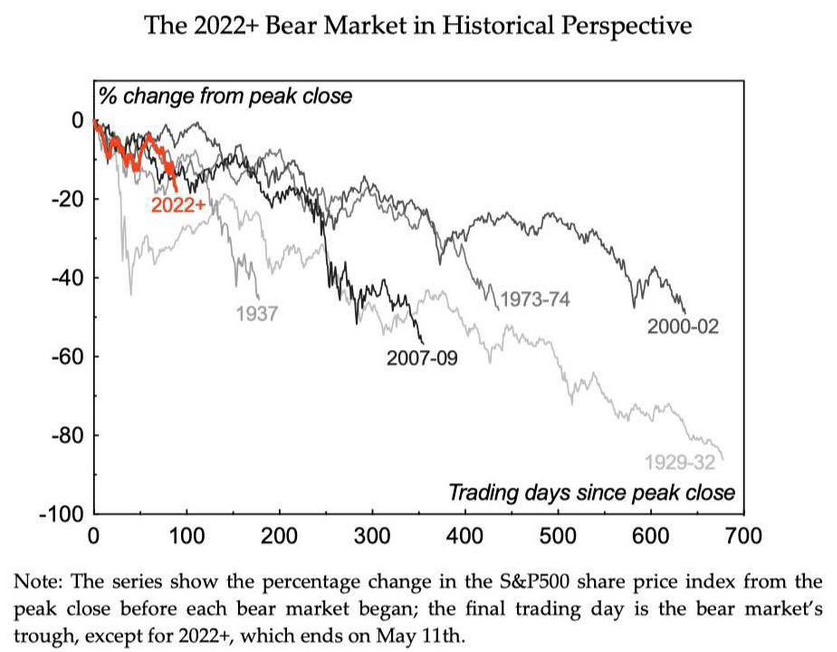

So in a “sell everything” market with stocks, bonds, and cryptocurrencies all getting hit at the same time, what do you do? Keep calm, hold what you’ve got, and look for opportunities to pick up good stocks at low-ball prices. What don’t you do? Panic or short stocks after a bear market has started. We may have just seen the panic bottom. Through Monday, the S&P500 fell by more than than 1% for four consecutive days, with greater declines each successive day. This had only previously happened in March 2009 and December 2018. Both marked the lows in the market.

Click for larger graphic

Click for larger graphic

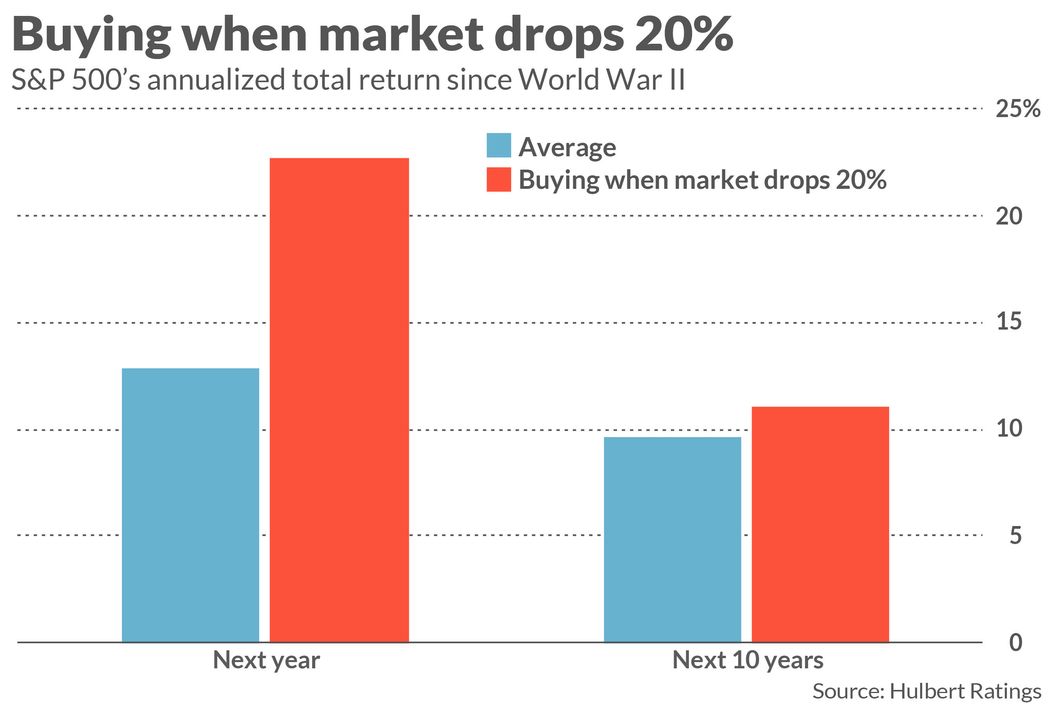

As Mark Hulbert pointed out:

Click for larger graphic

Click for larger graphic

For the last few years, we have been investing in especially volatile times:

Click for larger graphic

And it’s possible this will continue for a while:

Click for larger graphic

Click for larger graphic

But those who buy stocks the day the S&P 500 enters a bear market have made an average of 22.7% in 12 months. That’s more than double the stock market’s long-term average. In only two of the 12 major declines since World War II in which the S&P 500 fell by more than 20%, you would have been sitting on a loss 12 months subsequent to buying on the day the 20% loss threshold was violated. But even in those two cases, you eventually came out ahead — it just took longer than a year. In any case, notice that this means that in 10 of the 12 cases since World War II you were sitting on a profit in a year’s time. Those aren’t terrible odds.

I have adjusted all the buy limits and target prices to reflect current realities – some up, some unchanged, many down. That includes recommendations not covered in this issue, so check “All Recommendations” at the bottom of the newsletter.

Market Outlook

The S&P 500 lost 8.7% since last Thursday and is down 23.1% year-to-date, the second worst start to a year in history (1932 was the worst). The Nasdaq Composite lost 9.4% and is down a whopping 32.0% for the year. The small-cap Russell 2000 dropped 10.9% and is down 26.5% in 2022.

The fractal dimension is plunging towards the 30 level that will tell us the downtrend is over. It will take two to four weeks to get there, depending on how strong the move is.

Top 5

Changes this week: None

Near-Term – chronological order

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphic Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model estimate for real GDP growth in the June quarter has fallen to 0.0%, down from 0.9% on June 8. Weakness in real personal consumption expenditures growth, real gross private domestic investment growth, and real government spending growth drove the decline. The Blue Chip economists are much more positive at +3.1%. I expect the real number will be somewhere in the middle.

Click for larger graphic

Click for larger graphic

Virus Update

Worldometers now shows 542,705,206 worldwide confirmed infections, of which 524,341,023 have run their course. Of those, 518,003,832 recovered and 6,337,191 died – matching the last three week’s all-time low case fatality rate of 1.2%.

In the US, there have been 87,759,180 confirmed infections, of which 84,542,775 have run their course. Of those, 83,505,111 recovered and 1,037,664 died– the eighth week in a row at the all-time low case fatality rate of 1.2%.

Hospitalizations are still ticking up.

Click for larger graphic

Click for larger graphic

But daily deaths have flattened under 300, with today’s reading at 274.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most of the presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, June 20

Market Closed – Juneteenth

Tuesday, June 21

Summer Solstice – 5:13am

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations typically are very low. At the same time, Initial Public Offering valuations have moved very high. We were seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors that pay that much can make 5x to 10x in a reasonable, three- to four-year period. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out of favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Algernon Pharmaceuticals (AGNPF – $3.39) treated their last patient in the Phase 2 chronic cough and idiopathic pulmonary fibrosis trial on May 5. On Monday they said they have locked the database and we will see results on schedule in July.

The stock fell 22.7% today after they announced a public offering of units – stock plus a five-year warrant – but did not specify the size or pricing. The sole underwriter is Research Capital Corp, which probably means it’s essentially a “best efforts” underwriting. They expect to close the deal next week. AGNPF is a Hold.

Primary Risk: Ifenprodil fails in clinical trials.

Clinical stage of lead product: Phase 2/3

Probable time of first FDA approval: 2023

Probable time of next financing: 2022

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $130.06) will present all Major League Soccer games around the world for 10 years beginning in 2023. The Apple TV app will have no local blackouts, but most of the games will require an MLS subscription. Apple TV is available on iPhone, iPad, Mac, Apple TV 4K, and Apple TV HD, of course. But it’s also available on Samsung, LG, Panasonic, Sony, TCL, VIZIO, and other smart TVs; Amazon Fire TV and Roku devices; PlayStation and Xbox gaming consoles; Chromecast with Google TV; and Comcast Xfinity. Fans can also watch on tv.apple.com.

JPMorgan said Apple’s revenue from gaming and music will jump 36% to $8.2 billion by 2025. The two services will have a subscriber base of 180 million by 2025, 110 million for music, and 70 million for gaming. Apple Music already is the second-biggest music-streaming service after Spotify and will account for about $7 billion by 2025. Apple Arcade, their gaming subscription service, will pull in $1.2 billion. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $57.72) did an excellent fireside chat at the Goldman Sachs Global Healthcare Conference (AUDIO HERE). Management said their pipeline has increased by 50% in the last few years, but that is understating the real impact because it almost all is oncology. They already have a $1 billion-a-year oncology business and expect it to be 30% of revenues by 2030.

Most Wall Street analysts are modeling declining HIV revenues from 2025 to 2030. They couldn’t be more wrong. Biktarvy, their one pill, once-a-day treatment for the infection continues to grow and is patented to 2033. The infection prevention drugs and patent estate will grow significantly. There are a number of programs in process for long-acting alternatives.

Gilead pays a 5% dividend and can grow 5% to 10% a year for the next five to ten years. It’s a gift for the conservative part of your portfolio. GILD is a Long-Term Buy under $70 for a first target of $100.

Meta Platforms (META – $160.87) announced virtual reality for Meta Horizon Home. When users put on their Meta Quest headset they can invite friends to their Meta Horizon Home environment, hang out with them, watch movies together, and launch multiplayer games. I cannot tell you how much teens are going to love this. It’s a big step into the metaverse, which is the next big technology to sweep the world. Don’t miss it!

META is a Buy under $250 for a $400 target in 2023.

Other Tech

Rocket Lab USA (RKLB – $4.14) finally posted the link to their Stifel Cross Sector Insight Conference presentation and fireside chat (AUDIO HERE and SLIDES HERE). I covered the presentation last week, but you may want to listen to CEO and Founder Peter Beck tell the story. Rocket Lab is one of my five best long-term holdings.

The company was just selected by Ball Aerospace to manufacture the Solar Array Panel to power NASA’s Global Lyman-Alpha Imager of Dynamic Exosphere (GLIDE) mission spacecraft planned to launch in 2025. GLIDE is a heliophysics mission intended to study variability in Earth’s atmosphere.

The GLIDE spacecraft will launch with another Rocket Lab-powered spacecraft, also built by Ball Aerospace, the National Oceanic and Atmospheric Administration’s (NOAA’s) Space Weather Follow On-Lagrange 1 (SWFO-L1). SWFO-L1 is another heliophysics mission that will collect solar wind data and coronal imagery to meet NOAA’s operational requirements to monitor and forecast solar storm activity.

The CEO said: “Rocket Lab has become the ‘go-to’ provider of space solar power and space systems products throughout the space industry.” Rocket Lab will be added to the Russell 3000 Index on June 27. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Velo3D (VLD – $1.64) announced a new addition to its Sapphire family of printers, the Sapphire XC 1MZ. The new printer allows customers to print parts one meter in height, with a total build volume twice that of the Sapphire XC and nine times larger than the original Sapphire. This increases the addressable use-cases of Velo3D’s end-to-end metal additive manufacturing solution. First shipments go out late in the September quarter to several aerospace companies. VLD is a Buy up to $6 for my $30 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,855.00) continues to consolidate. It opened the week right on the 38.2% retracement level, explored a break below, and rejected that idea. Tom Palmer, the CEO of Newmont Mining, the world’s biggest gold producer, said there is a higher floor forming under the market as years of stimulus devolve into a fight to contain inflation. He said previously the floor was about $1,200 and now it’s probably more like $1,500 or $1,600.

Miners & Related

Coeur Mining (CDE – $3.48) posted their presentation at the RBC Global Metals & Mining Conference, although not the webcast (SLIDES HERE). The key slide:

Click for larger graphic

Click for larger graphic

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

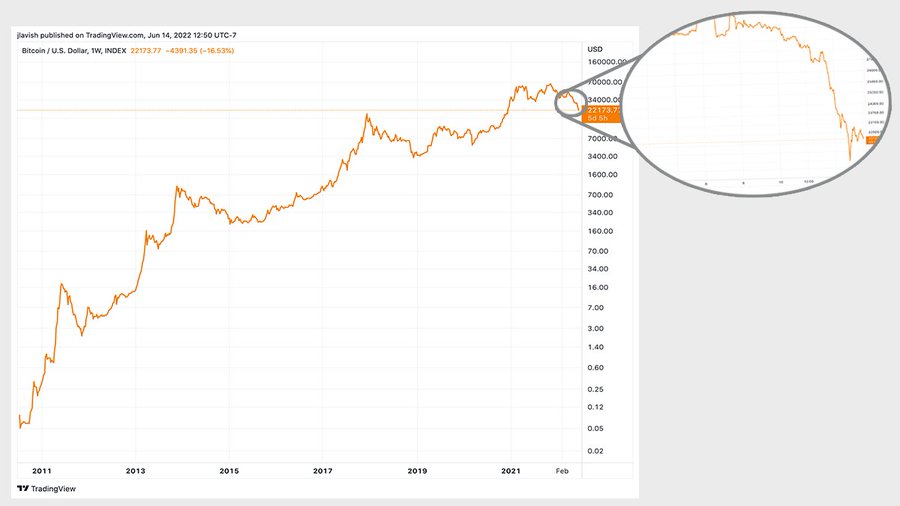

Bitcoin (BTC-USD on Yahoo – $20,565.41) slid towards $20,000, a level it hasn’t traded at since 2020. It dropped for nine straight days, a record losing streak going back to the early 2010s.

Click for larger graphic

Click for larger graphic

But….in 2018, Bitcoin fell around 84% peak to trough. Bitcoin has fallen 70% from its November 2021 peak. In 2018, ether fell 92% peak to trough and has fallen 75% from its November 2021 peak. Everything you are feeling right now… is in here.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $12.73) has applied to convert to an exchange-traded fund. The SEC has to issue a decision by July 6. GBTC is a Buy under net asset value.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

International & Other Recommendations

It is important to hold some non-US assets, especially in China.

Acreage Holdings (ACRDF – $1.22) made a very strong (and rare) presentation at the Benzinga Cannabis Capital Conference (VIDEO HERE and SLIDES HERE). Management addressed investors perception head-on:

Click for larger graphic

Click for larger graphic

It’s the Coeur Mining or SandRidge Energy problem. People remember the old management that ran the company into the ground and it just takes a while – and some good results – to get interest again. The new management has made some tough decisions, like exiting Florida, and relentlessly built back the balance sheet to support a concentrated effort, mostly in the Northeast.

Click for larger graphic

Click for larger graphic

The company is completely changed and Wall Street doesn’t get it yet. They will.

Click for larger graphic

Click for larger graphic

They said their relationship with Canopy Growth is strong and close, with cooperation on introducing new products. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

Oil – $117.14

Oil fell after the CPI inflation surge and China imposed some new COVID-19 lockdown measures, but it’s bouncing back. According to AAA, nationwide gasoline prices now average $5.009 a gallon. California is in the lead at $6.428 while Georgia is the low bidder at $4.497.

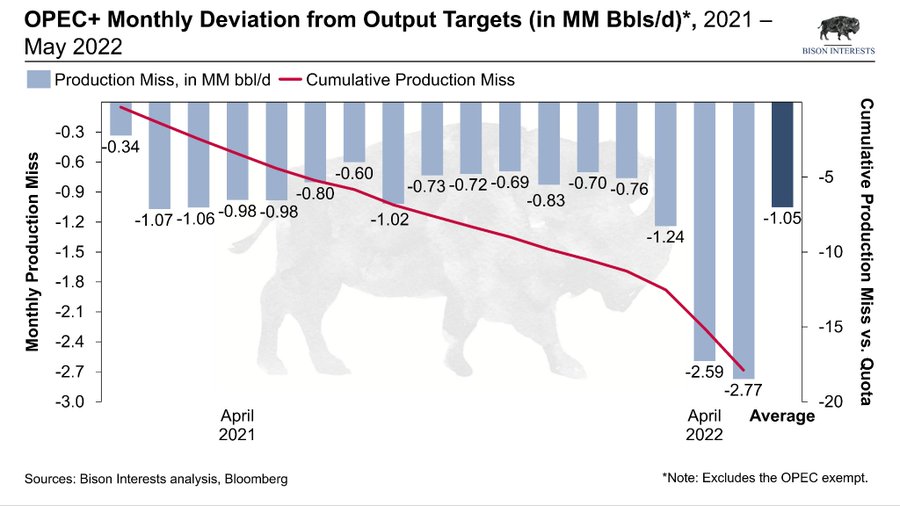

It’s just supply and demand. On the supply side, despite a mild bounceback in Russian output, OPEC+ missed their oil output target even more in May. Total production was 37.60 million barrels a day, falling short of the 40.37 million barrels quota by 2.77 million barrels a day.

Click for larger graphic

Click for larger graphic

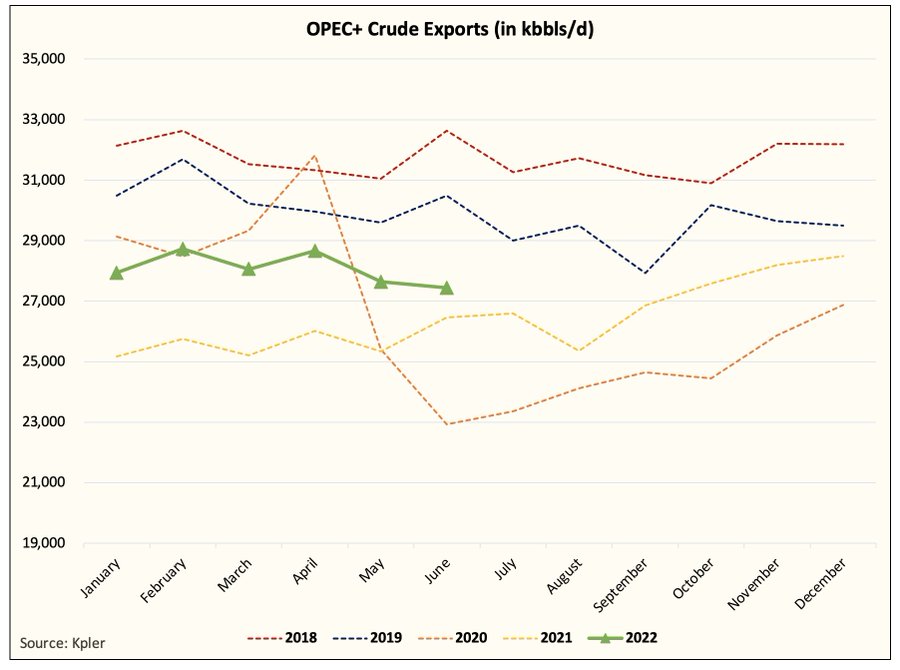

In the US, we have a flat rig count. OPEC+ crude exports so far in June are at the lowest level year-to-date. It’s a hot summer over there, and they burn oil to generate electricity for air conditioning.

Click for larger graphic

Click for larger graphic

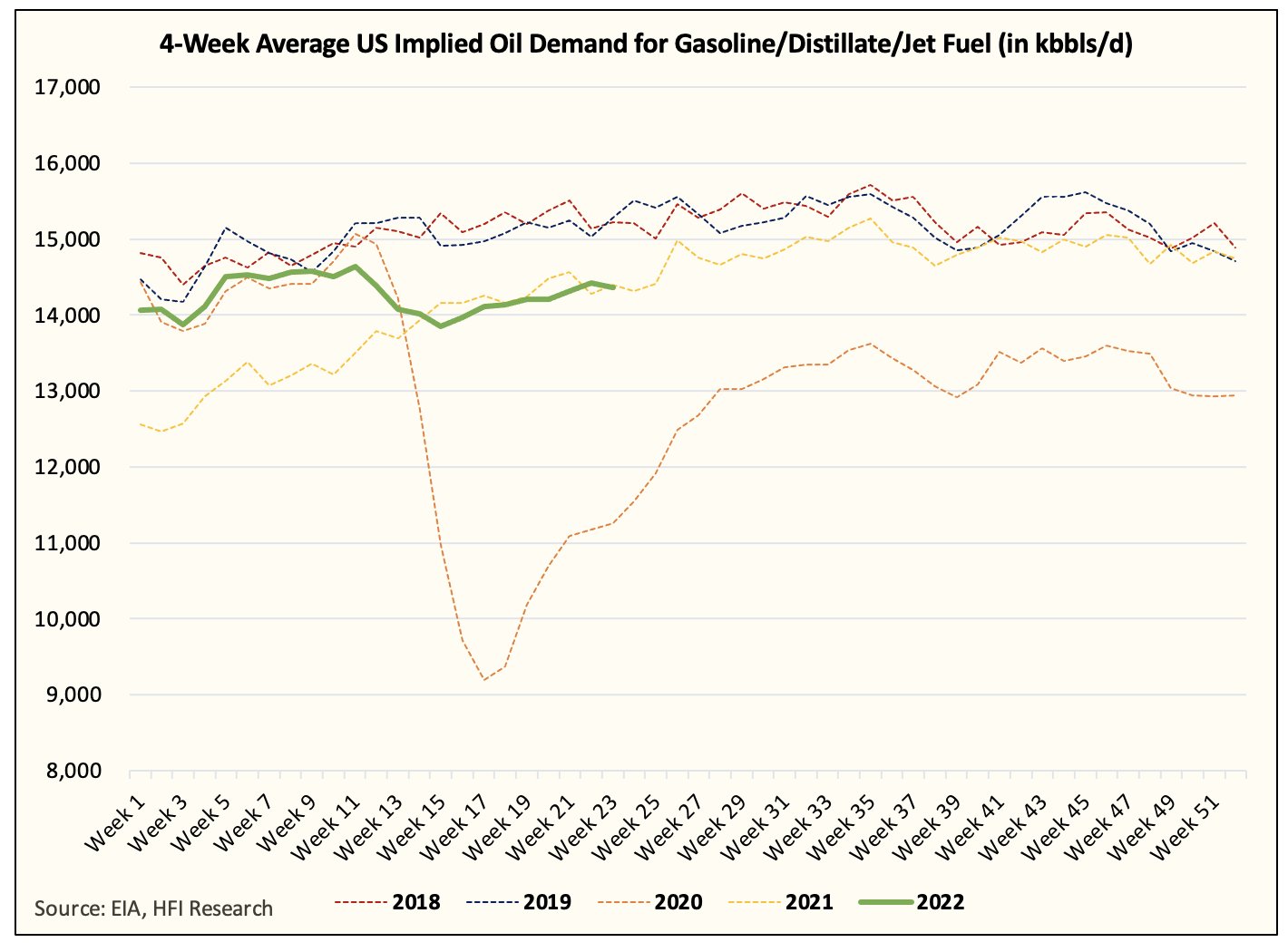

On the demand side, high product prices finally are hitting oil demand. The data is rather clear:

Click for larger graphic

Click for larger graphic

People don’t use oil, they use gasoline and diesel. With oil around $120 a barrel and crack spreads at $60, the real impact of high energy prices is not 5% of global GDP, it’s 7%. Energy at 7% breaks things, not to mention $9 natural gas prices that drive up the price of drying crops and fertilizer – and therefore everything else.

Click for larger graphic

Click for larger graphic

Eric Peters, Chief Investment Officer of One River Asset Management, wrote: “Climate change is an urgent priority. But policies around ESG were introduced before economies and consumers were provided a sufficiently wide off-ramp away from fossil fuels. Policy is discouraging oil production. US output is well below its highs and oil and gas rig counts, which would normally be in the 1000s at current prices, are sitting at 733. A timely alternative has not been provided. Panicked policies can worsen the disorientation – price caps, soliciting foreign production, and taxing profits of oil producers reduce investment capital, compounding the emergency.”

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $37.66) as a new, higher buy limit. Buy OIL under $36 for an $80+ target.

Energy Fuels (UUUU – $5.22) was nicked when the price of uranium fell 20% in five days. That gives you another entry point for the inevitable growth of nuclear power. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

Edward O. Thorp — Beating Blackjack and Roulette, Beating the Stock Market, and More

* * * * *

Your avoiding logical fallacies Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.78) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $0.92) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $9.41) – Buy under $20, hold a long time for a 10x return

Graphite Bio (GRPH – $2.14) – Buy under $9, hold a long time

Inovio (INO – $1.48) – Buy under $7, hold a long time

Invitae (NVTA – $2.13) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.80) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.82) – Buy under $2, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $3.74) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $130.06) – Buy under $150 for new iPhones

Corning (GLW – $31.37) – Buy under $33, target price $60

Gilead Sciences (GILD – $57.72) – Buy under $70, target price $100

Meta (FB – $160.87) – Buy under $250, target price $400

SoftBank (SFTBY – $18.03) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $38.28) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $10.25) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.68) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $7.321) – Buy under $10, target price $40

Liberty Media Acquisition Corporation (LMACA – $9.82) – Buy under $10, target price $20 to $30

Rocket Lab (RKLB – $4.14) – Buy under $13, target price $30+

Velo3D (VLD – $1.64) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – $391,200 – Buy while fixed mortgage rates are low

Bag of Junk Silver – $21.80 – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $26.82) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $33.270) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.85) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $28.99) – Buy under $30, target price $50

Coeur Mining (CDE – $3.48) – Buy under $5, target price $20

First Majestic Mining (AG – $8.02) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.50) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $6.43) – Buy under $10, target price $25

Sprott Inc. (SII – $36.28) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $20,565.41) – Buy

Grayscale Bitcoin Trust (GBTC – $12.73) – Buy

Ethereum (ETH-USD – $1,099.33) – Buy

Grayscale Ethereum Trust (ETHE – $7.16) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.39) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $35.87) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $15.61) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $30.25) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $1.22) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.28) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $37.66) – Buy under $36; $80+ target

Energy Fuels (UUUU – $5.22) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $3.39) – Hold for chronic cough results

Akebia Biotherapeutics (AKBA – $0.32) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.05) – Hold for buyout

CohBar (CWBR – $0.18) – Hold for human trials of CB5138-3

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

2

3rd. A timely and outstanding Radar Report, Michael Murphy. The 12 month overall 22.7% improvement of our portfolios for a prudent husbandry of our assets is very interesting and gives good motivation to stay with the solid ones and look for strong opportunities with patience. I saw an interesting piece in economics early this week that stated that our view of the inflation numbers are much too understate, due to what the author saw as the “degree of Stick-iness” in many catetegories of products and programs, government and private sector, as government gets larger and more complex in the private sector, so that it is taking longer for competition to have a downward move over time. In teh government sector, as the population gets larger and older and thsoe, government benefits get larger(social security, pensions, Medicare, Medicare, Obamacare, retirement pay civil service and military, etc, etc)and less efficient as silos exist in more and different specialties that grow with their naturaladvocacy for more reources. In any event, this administration, to me, may get a more sticky inflation as the seek to satisfy more jobs of a regulatory nature and etc. Just sayin’

sure hop we get some slack on fossil fuel production to meet both US demand and export demand and international needs. Hope we see a glimmer of seeing a nice bounce tomorrow. GLTA

Social security and Medicare are the best investments our government makes for it’s people and that is what it supposed to do. Thank God for FDR and LBJ.

You are unaware of the low quality of Medicare coverage for good health care. Absolutely the worst are Medicare Advantage Plans, which are heavily advertised. The sales pitches are “money back in your benefits”, deals on peripherals like OTC items, etc. But important things like access to quality MD’s, expensive MRI/CT scans is a nightmare. The best MD’s do not accept Medicare Advantage, because the pay rates are abysmal. Many chiropractors withdraw from all Medicare plans because the paperwork required to get the measly pay isn’t worth the time and money spent by the professional.

You don’t understand that all guaranteed socialistic programs eventually fail, since the public thinks they are freebies, everyone takes advantage of the “services” so the limited money to provide services is diluted among many more claimants.

As for social security, my friend died suddenly at 58 before he could collect any benefits, and all his years of paying taxes for SS was money stolen from him. So the SS system is a theft scheme to get benefits at the expense of others. Everyone except the truly handicapped would be better off keeping their tax money for benefits, and doing very conservative investing.

Govt debt would be much lower without entitlement spending. Interest rates would be lower. Extreme booms and busts are caused by govt money printing to cover debts, not the free market, as wrongly claimed by socialists. In the glory days of 19th century free market capitalism, there were much smaller fluctuations in economic conditions. Learn about the Austrian school of economics, founded by Ludwig von Mises.

“Everyone…would be better off…doing very conservative investing.” Uh, why are you here at this site, doing what is certainly the opposite of conservative investing??

Very few people do any conservative investing besides those who buy a house and hold on to it long-term. Most people don’t save for retirement. 49% of adults ages 55 to 66 had no personal retirement savings in 2017. Forty percent of older Americans rely solely on Social Security for income. A large segment of the population can’t afford to save anything for retirement. Sixty-four percent of Americans live paycheck to paycheck.

https://www.cnbc.com/2022/03/08/as-prices-rise-64-percent-of-americans-live-paycheck-to-paycheck.html

Some spend every cent they have, no matter how much they earn. Nice big house in suburbia, two new cars, debts and no savings, until the layoff happens. Even those who win big lotteries often blow it all within a few years, and end up broke. Your dream of everyone investing conservatively isn’t realistic at all. Even you are here at the New World Investor casino.

So what do you do when this large segment of the population doesn’t have money to buy food, shelter and medical care? These “socialistic” programs are one solution, what’s yours? Claiming everyone would save if Social Security taxes were eliminated isn’t realistic, and I think you know that.

Most large corporations deleted their retirement pension programs for employees during the Raygun era, and justified huge pay increases for top executives for “cost-cutting” measures like eliminating pensions and other employee benefits. Typical CEO salaries went from $500,000 to $15 million in a decade. My uncle (and the father who lived next door to me growing up) got no pension when the machine shop owner decided to close his business when many of his long term employees were getting close to their 20-year company retirement pension benefit. So they got nothing, and the owner retired to Switzerland. That trick was so common that the pension laws were changed to require five year vesting for company pensions.

Social Security is a forced retirement savings program. Sure, your friend failed to get his retirement payout, but most people don’t die at 58. My father died at 53. And my mother received Social Security benefits from his account, and my youngest brother and sister indirectly received Social Security benefits paid to my mother to support them after his death. Your worst case scenario is the only one you discussed, and its not the typical case by far. Its rare. But you use that to generalize about how without Social Security, people would invest for their own retirement conservatively. Equally rare. Get real.

And you conveniently forgot to mention that businesses also pay 6.2% of wages into their employees Social Security retirement program, to help increase the benefits to working employees. Social Security is not an entitlement program paid out by the government general fund. It was funded by employees and businesses. So your tax money can go to wars, roads, and Congressional trips.

So its not as ugly as you paint it. Its just your hatred for any government program you can label “socialist.” Even if the fund isn’t actually socialist at all. The government doesn’t pay the benefits, employees and employers are paying into the Social Security Trust Fund, so its a forced retirement program since businesses rarely offer them anymore, and people rarely save sensibly for their retirement.

Ever look up the total cost of invading Iraq (twice!)? Or Nam? Isn’t Social Security more prosocial and a better investment than that spending in dollars and blood?

Everyone knows that Medicare Advantage programs are terrible. That’s why the vast majority of people go to Medicare supplement programs. I’ll bet the chiropractors who don’t accept Medicare have trouble staying in business. Who would pay for voodoo medicine out of pocket?

Your argument against social security is a red herring. Just because you know a person that died before receiving benefits doesn’t mean the program is flawed. Many elderly are staying out of poverty ( barely) with their SocSec check.

The real reason the US is in such a mess is the blank check given to the war machine every year for the past 50+. The only president who dared cut back a TINY bit was Clinton and he was roasted for it. Spending trillions to “defend” a country is insane given the fact that we can’t even “defend” an elementary school.

Let’s cut that trillion dollar defense budget by 2/3. Medicare and social security would be safe for years and the country wouldn’t notice the difference. There would be a lot of out of work servicemen though, many of which currently spend their days playing ping pong on a base somewhere.

BTW, if you are so anti socialism I guess you won’t be collecting social security and medicare right?

Compare with other countries where rationing is done differently.

FDR noted that with the SSA in place, the peons would be so pleased that they would vote for the Democratic Party in thanks.

And so it was. Maybe?

Thanks Michael Good job I must say summarizing it all.

Halalouya. Finally the FED gets it. Powell needs to get some hubris and pull a Paul Volcker and take sufficient action to kill runaway inflation. Recession be damn. Yes, there will be some short term pain and volatility in the stock market. We all need to get over it , take our licks and get on to a better place. IMO

Michael Murphy – why has NVTA fallen so far?

Just read my posts on NVTA. It is a small niche company. The business model is to sell everyone on genetic testing, which will necessitate providing tests at a reasonable price. But oncology and hepatitis treatments are also niche services. The difference is that these treatments cost well over $100,000 per year. Even though there are relatively few such cases, the very high payments mean that profits are high. NVTA’s tests don’t make much of a difference to patient outcomes. Much of what MM has written on NVTA is just promotion from the company, and isn’t reality.

Chris your comments on the the last radar report really was good about acxp. I bought 600 shares. It only traded 5000 shares today. Why do you think it’s traded so thinly? Very strange. Just not known yet? Even being traded so lightly the price moves quite a lot. 52 week low 2.33 high 8.74.It really looks like a fun play. Please keep us enlightened.

Right. I have the same question to Chris–why is it so thinly traded? I am concerned about the lack of interest. If the phase 2B trial is successful, will any more interest develop? That means a Big Pharma buyout. I hope this isn’t another ARTH situation where the product is great, but almost no sales were made. I have a good amount of ACXP shares and am looking to buy more when it settles down after the recent jump.

when will the ACXP phase 2B results be published, anyone know?

They expect to complete trial enrollment late this year, so probably June-Septemner 2023.

I think the price moves a lot BECAUSE it is thinly traded. Why is it thinly traded? It is an unknown micro-cap with a chart that scares people. I think Big Pharma is aware of ACXP and just waiting on results to make an offer (or bidding war). Look at the BoD. The company is well-connected. While they expect to enroll the last subject in the trial before the end of the year, the data lock should occur in January. I think we will have data 2 or 3 months before Mr. Murphy says 2B results will be published. Maybe a peek even earlier.

Chris,

What happened to explain the big decline on high volume in NGENF today? No news on YMB. I am itching to buy this, but there is plenty of time before real news on human trials.

After my caustic assessments of most small biotechs for investment, why am I interested in NGENF and ACXP? NGENF seems to have the best mitigating treatment for several common, severe neurological diseases. Even though they are still not addressing the root causes of diseases, their treatments can be repeated when the inexorable disease rears its ugly head. It is a much better concept than TGTX’s drug, which merely depletes lymphocytes overactive in autoimmune MS. So there will be depression of other functions of the immune system. My strategy with TGTX is to take profits (hopefully) on approval, cut and run before the inevitable appearance of other diseases like cancer years later, when that drug will collapse. I took nice profits twice on DNDN, before its total wipeout. NEVER BUY AND HOLD NWI STOCKS.

For ACXP, they have the best antibiotic for C diff, a limited and worthwhile goal. They aren’t trying to deal with complex diseases like cancer, MS and other autoimmune diseases, where most companies such as NWI hopefuls will fail.

The current low price is a gift. Despite that, I have looked in NGENF’s mouth and the teeth are not too long and sans caries. It is my biggest position (or at least was before the recent price drop — I haven’t recalculated, but it probably is still my biggest).

Whats your biggest position? NGENF OR ACXP? I feel really stupid. I don’t get the analogy, looked in mouth and the teeth are not too long and sans caries.

Chris looked in NGENF’s mouth and didn’t see any caries (cavities) or dirty laundry or smell bad odor. “Long in the tooth” means something that has been going on too long and is about to collapse/reverse, like the bull market from 2008 which finally reversed a few months ago. Actually, adult teeth don’t grow like hair, so long teeth are just fantasies.

NervGen is my biggest position. Ever heard the phrase, “Don’t look a gift horse in the mouth”? When you are buying a horse, you usually check it’s teeth to see if it is “long in the tooth”. While the size of the tooth doesn’t change, the gums recede as one ages and so the visible part of the tooth appears longer. If someone gives you a horse for free, do you care whether it is 3 or 20 years old? It’s free! Even if you don’t want a 20 year old horse, you might be able to trade it for something you want. I have never understood why people like to buy things after the price has gone up. I prefer to buy before the price goes up. So NervGen is up 10% this morning. Is it too late to buy? Just think about what the company will be worth if its drug works in any of the three Phase 2 trials that will begin at the end of the year. It was trading 100% higher just 6 months ago, but could be much higher a year from now. Some people would rather wait until NervGen proves its drug works in people like it does in animals. Those people will pay more than today’s buyers, but they will have less risk. I am willing to tolerate the risk of failure for the additional profits.

Thanks Chris and JGMD.

You gave a better explanation for “long in the tooth” than I.

What’s happening with QUIK?? Is it catching fire?

ARTH (as if it matters, or too little too late): Arch Therapeutics Provides Update on Reimbursement Strategy in Additional Selling Channel:https://ir.archtherapeutics.com/press-releases/detail/578

Yep, I saw it this morning. Steph Kam. This is really a last gasp strategy. I like it though. Get a code approved by Medicare and Medicaid to get the revenue accelerated. Makes sense, The end of the KOL phase is just a stoppage of paying them and move into second quarter expansion of potential codes for closing the wounds near internal action is a good try for an expanded AC5. Where they will get the cash to do this will probably be borrowing against early revenue expectations from a supportive bank, We can’t dilute any more, IMHO. GLTA

This is an example of what’s wrong with relying on insurance coverage. People are programmed by the system to not get anything worthwhile unless insurance covers it. If I had a wound or chronic ulcer, I would gladly pay lots of cash for AC5 or its variants to prevent amputation. I wouldn’t care whether Medicare covers it or if it is bureaucratically damned as an “investigational” agent. People blow big bucks taking vacations or on home improvements. What’s more important–those things, or saving your limb?

I sold the stock, but for the sake of saving people’s limbs, I am routing for ARTH.

And (on Seeking Alpha) somebody else still likes NVTA:

https://seekingalpha.com/article/4519650-invitae-stock-out-of-cash-burn-speculative-strong-buy?mailingid=28135874&messageid=2800&serial=28135874.8244&source=email_2800&utm_campaign=rta-stock-article&utm_medium=email&utm_source=seeking_alpha&utm_term=28135874.8244

Thanks again Steph Kam. The article hits the button on the head, if we can survive this inflation nationally in this cycling bear market. BTW, top news is NY Post article by Michael Goodwin, their big editor. He essentially says it’s time for Biden to go now. I don’t have a link.

Here is that link from the NY Post:

Joe Biden has nothing to offer (nypost.com)

Thanks Don. That says it all. When the most hated man in the world (Putin) has a better approval rating then Biden (the leader of the free world) that’s a very telling statistic. Not political. Just facts from our media.

I know of several MD’s and DO’s with all cash practices who don’t accept insurance. They serve patients who want the very best care and advice and don’t live by the sabotage of the insurance system. These docs use genetic testing which impacts their choice of nutritional therapies and assessment of risks of serious diseases. They would use NVTA services. Unfortunately, they are in a small minority of the universe of docs. At the current stock price, NVTA is a highly speculative bet on whether the company can become profitable.

You may recall Nixon’s infamous secret audiotapes to record his own Presidency for history. Unfortunately for Nixon, those tapes held evidence that led to his resignation when his Republican party would no longer tolerate Nixon’s wrongdoing, documented on audiotape.

There is a Presidential photographer that is typically present during meetings in the White House and elsewhere. They tend to become ignored over time, as important business is transacted. Today we have video rather than audio recordings of just about everything. But there’s just photography not video footage from that Presidential photographer. But there was a British videographer who was documenting the Trump re-election campaign, that had access to the Trump family during the re-election campaign through January 6. Today the January 6 committee will feature testimony from that videographer, and maybe some video clips that could be rather enlightening.

You won’t see this story on Fox News or OAN. You’ll just hear Tucker’s opinions about it. So you might want to tune into the hearings today starting at 3PM Eastern, noon Pacific time. Or watch a real news channel tonight. Could be some interesting video documenting Ivanka contradicting her recent testimony to the Jan 6 committee, and other video shedding light on Trump family re-election activities.

Testimony is one thing. Nothing quite like video to document history.

Note that during the Nixon Watergate era, there was high inflation, and a bear market with the S&P500 falling about 50%:

https://www.yahoo.com/news/heres-stock-market-watergate-133736317.html

However, inflation was double digits before that political (and criminal) scandal broke, and there also was an Arab oil embargo seriously affecting the US. Perhaps similar to the Russian Ukraine invasion oil/gas situation today? Certainly for Europe. The article warned about political risk affecting the economy. Trump is likely to face DOJ criminal charges IMHO. That would be unprecedented, much like the Nixon saga but worse.

Trump should have taken this page from the Nixon playbook:

Resign and let the new President (your loyal VP) pardon you.

A little late for that now.

MM, what is the fair value of SandRidge Energy, Inc. (NYSE:SD) in your opinion? Thanks.

The new Radar Report for 6.23.22 is posted.