Dear New World Investor:

I spent this week looking at Snap (SNAP), hoping I could recommend it as a first step towards taking advantage of the bear market in high tech, but – nope. I really like the way they are getting ready for the metaverse, which I think will cause dramatic changes in the way people learn, work, and play. But…

Snap was founded 11 years ago as Snapchat on the simple idea that users would like to send pictures to others knowing the pictures would disappear after a certain period of time. In the first year, they processed one billion photos as it really caught on with kids. In the US, 90% of the 13- to 24-year-olds and 75% of the 13- to 34-year-olds use it. When they refused a buyout offer from Mark Zuckerberg, Facebook started Instagram to sort of compete, and now TikTok is the new shiny object for teens.

On Snap’s investor overview page, they define themselves this way:

Click for larger graphic

Click for larger graphic

A camera company, not a photo-sharing site? Interesting. I’ve been intrigued by the filters they introduced several years ago that were quickly copied by Instagram and then everyone else – even Zoom.

Click for larger graphic

Click for larger graphic

Like Pokémon Go, these filters are an early example of augmented reality, or AR. A picture is static, but as the girls move their heads around in a video, the ears, nose, and tongue move quickly to stay in the proper relationship to the face. This technology is the basis for Gucci’s ad campaign that lets women see what a pair of shoes will look like on their feet. It let SmileDirectClub show my youngest daughter how great her smile would look if she signed up for their clear plastic braces to straighten her teeth – and that worked! Or look at Accuvein, which makes blood draws or IV starts simple:

Click for larger graphic

Click for larger graphic

The first generation Snap glasses had cameras that could take still pictures or up to 70 10-second videos on a single charge.

Click for larger graphic

Click for larger graphic

Then Snap made three acquisitions to do the hard work of developing their own AR hardware. In May 2021 they bought WaveOptics, which specializes in displays for AR glasses. Most glasses project the AR data onto the glasses. WaveOptics uses photonic crystals and hologram physics to create a sharp image on a very transparent display showing the wearer’s complete field of view.

Last January they acquired Compound Photonics and merged them into WaveOptics. They make video drivers for high definition, lifelike images. Then in March, they acquired NextMind, which lets users control the glasses with their thoughts. Sounds woo-woo, I know. But Elon Musk’s Neuralink does the same thing, except Neuralink requires the user to have a hole drilled in their skull and a chip implanted. NextMind puts all the electronics in a headband so the user doesn’t have to touch the glasses or use voice commands – they can just think what they want to do.

The new generation of Snap’s glasses, called Spectacles, have dual waveguide displays capable of superimposing AR effects made with Snap’s software tools. The frame features four built-in microphones, two stereo speakers, and a built-in touchpad. Front-facing cameras help the glasses detect objects and surfaces you’re looking at so that graphics more naturally interact with the world around you. They are quite complex and for sale only to developers.

Click for larger graphic

Click for larger graphic

I think Snap will be a leader in the metaverse, competing with Meta’s Oculus and Apple’s forthcoming product, plus whatever Google does. So why not recommend the stock, which is down 83% from its all-time high?

Click for larger graphic

Click for larger graphic

Because after guiding below consensus for the June quarter, three weeks later they said they wouldn’t even hit the low end of their guidance. I don’t know if they’re losing digital advertising market share to Meta, Google, and TicTok, or if digital advertising is collapsing for everyone, or if the Apple privacy changes are biting them harder for some reason, or what. But I do know this: Bad quarters are like cockroaches. You rarely see just one of them. I’d rather pay $20 for SNAP when I know they can stop the cash burn than pay $14 today and see it slide into single digits. So, love the company, wait and see on the stock.

Economy

The Atlanta Fed’s model for June quarter real GDP growth has fallen to just +0.9%, due in part to companies selling off inventories (looking at you, Target). If it goes negative, the newsreaders will all bleat “Recession! Recession!” But the second half of 2022 was always going to be stronger than the first half, so this would be the shortest “recession” on record. We’re more likely to see a real downturn in 2023.

Click for larger graphic

Click for larger graphic

There’s no doubt the economy currently is in a stall. Federal tax collections plunged in May, withholding taxes in particular. Those worried about a slowing economy now have real data to back them up. But the Bureau of Labor Statistics reported that in May the US added 390,000 jobs, which was a drop from last month’s upward-revised 436,000 and the lowest since April 2021 but was well above the 320,000 consensus expectation. It is puzzling that the ADP survey is so weak while the government’s numbers are surprisingly strong, especially when new claims for unemployment insurance have been steadily climbing for weeks.

+0.9% is below the stall rate, but Real Final Sales are the true bottom line number for the economy. The rest is inventory adjustment which nets to zero over time. The Commerce Department’s advance retail sales reports are strong, but reports by Target and Walmart suggest weakness. Car sales in April also were poor. We’ll get the first look at June quarter GDP, real final sales, and inventories on July 28.

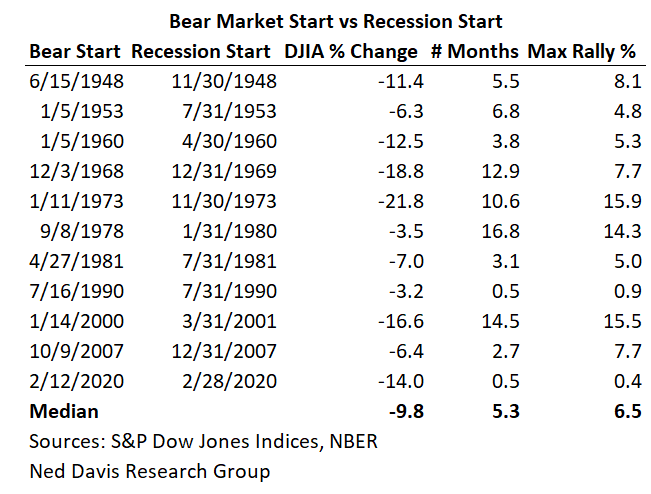

The stock market has led post-war recessions by five months, on average. I think recession risks are low in 2022, so either that means a strong second-half stock market rally or an unusually long lead time. The few cases with long lead times had big counter-trend rallies, including a 15.5% rebound in 2000.

Click for larger graphic

Click for larger graphic

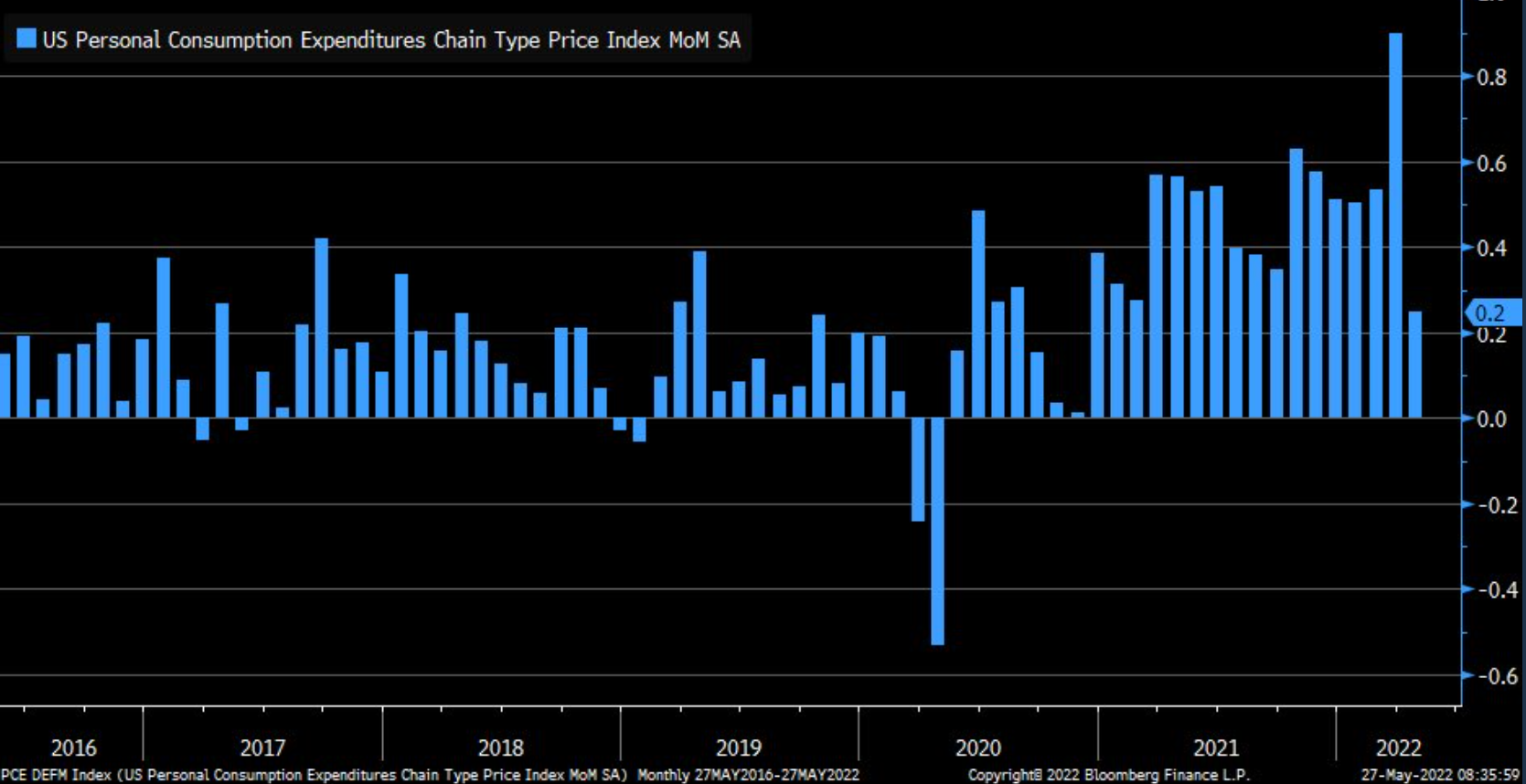

On inflation, the key number is not tomorrow morning’s year-over-year headline number (expected to be 8.3%) for the Consumer Price Index, but the month-over-month change in the core Personal Consumption Expenditures Index. Why? Because that’s what the Fed is looking at. In February, March, and April, the month-over-month change was just +0.3%, the lowest level since November 2020, versus+ 0.5% in December and +0.4% in January. A month or two at or under the +0.2% level and the Fed will decide their job is done with no need for further Fed fund increases.

Click for larger graphic

What is the worst possible way to “fight” inflation caused in part by supply line shortages? Why, it would be to helicopter drop more money for people to spend – inflation stimulus. No one would do that, right? Wrong. The rulers of our fiat system, in their infinite wisdom, may soon decide to fight inflation with more inflation.

It’s already happening in Canada. Quebec has announced that they will give a $500 stimulus check to everyone that makes $100,000 or less. This handout to 6.4 million Canadians, will “help Quebecers cope with the sharp increase in the cost of living that we have seen in recent months,” according to Finance Minister Eric Girard.

Some US congresspeople have just introduced a bill to hand out “gas price stimulus checks” of $100 a month to all citizens who live in areas where gas prices are above $4 per gallon – an annual bill of $168 billion. Yeah, that ought to bring gas prices down.

CNN said: “The administration should ask Congress to authorize a payment of $1,100 per household to pay for four months of higher prices going forward, and provide an option for the president to provide a second or even third check to low- and moderate-income families for an additional four months in the event that prices remain high. We don’t know when this crisis is going to end or when prices for essential goods and services will return to more affordable levels.”

Will we end up with a mind-blowing system in which the government is forever printing up the currency to compensate people for the consequences of previous money printing? That’s the Weimar Republic hyperinflation playbook. I think hope they’re not that stupid.

Market Outlook

The S&P 500 lost 3.8% since last Thursday as the market worries one day that the economy is too strong, so the Fed will tighten (stocks down!), and the next day that the economy is too weak, so there will be a recession (stocks down!). The Index is down 15.7% year-to-date. The Nasdaq Composite lost 4.6% and is down 24.9% for the year. The small-cap Russell 2000 soared 2.5% and is down 17.6% in 2022.

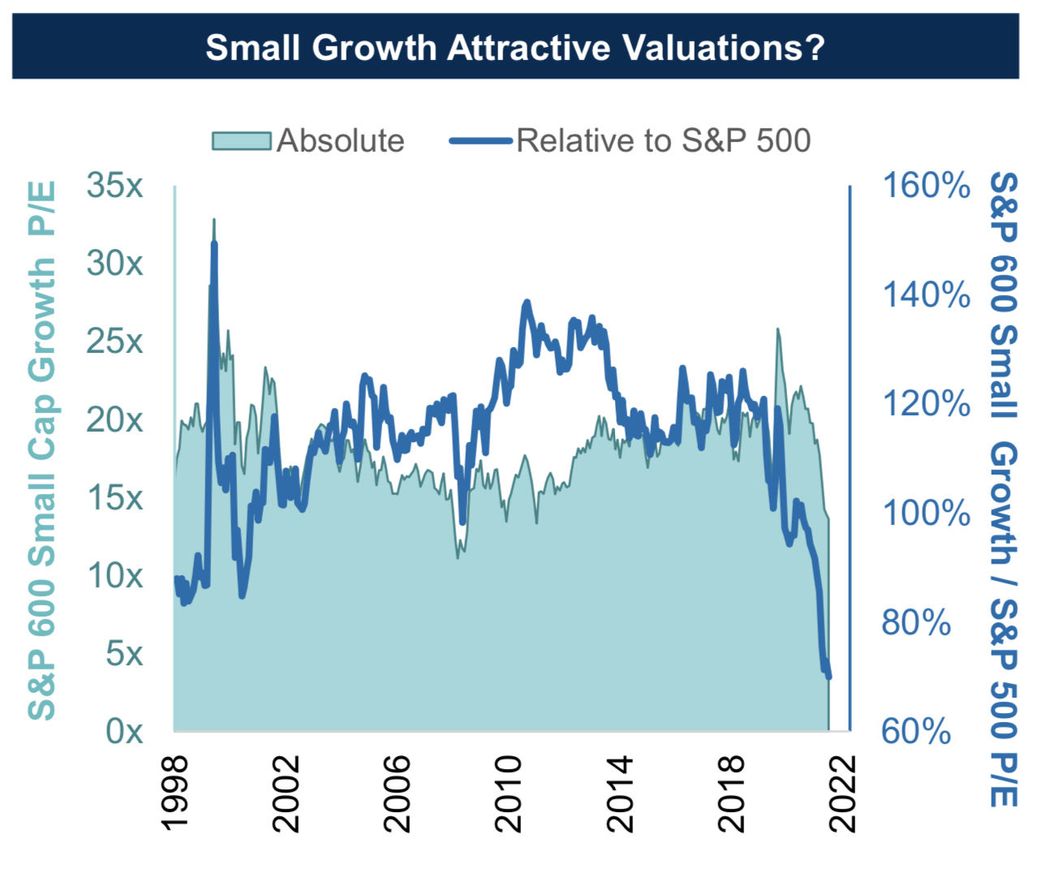

I know it doesn’t feel like it, but this is a time to buy small-cap growth stocks, The weighted forward Price-to-Earnings ratio for the S&P Small Cap 600 Growth Index, 12.16x, is low both absolutely (10-year average 19.15x) and relative to that of the S&P 500 (69% versus 10-year average of 112%). This is the cheapest that the S&P Small Cap 600 Growth Index has been, relative to the S&P 500, since FactSet started tracking the data in 1998.

Click for larger graphic

Small-cap growth stocks are less expensive than small-cap value equities, yet they generally have higher operating margins, return on capital and stronger balance sheets.

The fractal dimension is treating the last two weeks as a consolidation of the big jump the week before that. My guess is that unless the Fed raises the funds rate on Wednesday more than half a percent (50 basis points) or otherwise throws a spanner in the works, we’ll have an uptrend to end next week.

Top 5

Changes this week: None

Near-Term – chronological order

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphic Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Virus Update

Worldometers now shows 538,352,631 worldwide confirmed infections, of which 517,908,770 have run their course. Of those, 511,581,559 recovered and 6,327,211 died – matching the last two week’s all-time low case fatality rate of 1.2%

In the US, there have been 86,988,671 confirmed infections, of which 83,861,030 have run their course. Of those, 82,825,999 recovered and 1,035,031 died – the seventh week in a row at the all-time low case fatality rate of 1.2%.

Hospitalizations continue to creep upwards.

Click for larger graphic

Click for larger graphic

While daily deaths are stalled around 250.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most of the presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, June 10

Consumer Price Index – 8:30am – +8.3% headline, +5.9% core expected

APTO – Aptose – 10:30am – European Hematology Association

Monday, June 13

AG – First Majestic – Through 6/15 – PDAC- Prospectors & Developers Association of Canada

Tuesday, June 14

CWBR – CohBar – 5:00pm – BIO International Convention

Wednesday, June 15

Fed meeting – 2:00pm – 50 basis point increase expected

CWBR – CohBar – 1:30pm – Annual meeting

GILD – Gilead – 2:20pm – Goldman Sachs Global Healthcare Conference

NVTA – Invitae – 5:40pm – Goldman Sachs Global Healthcare Conference

Thursday, June 16

SCYX – ScyNexis – 9:30am – Annual meeting

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations typically are very low. At the same time, Initial Public Offering valuations have moved very high. We are seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors make 5x to 10x in a reasonable, three- to four-year period. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out of favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Graphite Bio (GRPH – $2.62) presented at the Jefferies Healthcare Conference (AUDIO HERE and CORPORATE PRESENTATION HERE). Graphite truly is the future of gene editing because they can not only find dysfunctional genes and cut them, they can replace the bad genetic sequence with the proper sequence.

Click for larger graphic

Click for larger graphic

This precision gene repair can fix up to 4,000 base pairs at a time – far more than any competitor.

Click for larger graphic

Click for larger graphic

They will prove the power of “find and replace” with their sickle cell program, where they’ll dose the first patient this year and have proof of concept results next year. I expect rapid FDA approval – this is a life-saver.

Click for larger graphic

Click for larger graphic

If you’ve been hesitant about buying GRPH, I urge you to listen to this 26-minute presentation. It’s about the best 26 minutes your portfolio could ever have. GRPH is a Buy under $26 for a $50 target in 2022, $100 in 2023, and then higher.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 1

Probable time of first FDA approval: 2025

Probable time of next financing: 2023 or 2024

Inovio (INO – $1.65) did a fireside chat at the Jefferies Healthcare Conference (ZOOM HERE). The new CEO was very competent but not exciting – perhaps a change that Wall Street will be more comfortable with. She joined Inovio in March 2019 as the Chief Operating Officer. Before that, she was the Chief Operating Officer and later the Chief Executive Officer of Aeras, a not-for-profit organization dedicated to developing new vaccines against tuberculosis. During her tenure, she oversaw two major clinical trial breakthroughs in the development of TB vaccines. She holds a Ph.D. from the National Institute for Medical Research in the UK, has been named as an inventor on more than 20 patents, and currently serves on the board of Trustees for the Sabin Vaccine Institute.

This summer, they will present the antibody data from the recently completed trial in China by their partner, Adavaccine. China really wants a vaccine that prevents people from getting infected, which INO-4800 does and their domestic Sinovac-CoronaVac vaccine does not.

The second Phase 3 trial of VGX-3100 for precancerous cervical dysplasia will read out at the end of this year. Inovio has a very deep pipeline, much of it funded by others.

Click for larger graphic

Click for larger graphic

INO is a Buy under $21 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2022

Probable time of next financing: Not needed

Invitae (NVTA – $2.66) partnered with an Australian patient organization, Pink Hope, to streamline and expand access to genetic information for breast cancer patients. They said up to 60% of Australian breast cancer patients with high risk, hereditary gene variants such as BRCA would not qualify for genetic testing due to the nation’s eligibility criteria and would be unable to access what can be life-changing knowledge.

Those who do receive a referral for genetic testing in New South Wales can face a 12-month,or longer wait time, during which they and their family members could develop cancer, have their cancer progress, or not get access to personalized treatment that could increase survival.

Pink Hope will help people navigate the genetic testing pathways available. Buy NVTA under $50 for a first target of $100 and eventually $200+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

Medicenna (MDNA – $0.91) got another important US patent covering composition and methods of treating degenerative diseases via administration of Interleukin -4 and Interleukin -13 empowered Superkines. “Composition of matter” are the strongest patents and this one gives them protection until 2038. Buy MDNA under $4 for a first target of $40, then maybe $80.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: mid-2022

ScyNexis (SCYX – $2.04) filed the supplemental New Drug Application (sNDA) with the FDA for Brexafemme for the prevention of recurrent vulvovaginal candidiasis. It will be the first and only oral non-azole treatment for the prevention of recurrent yeast infections, defined as three or more episodes of VVC in the previous 12 months.

Because Ibrexafungerp has been designated by the FDA as a qualified infectious disease product (QIDP), it gets a six-month priority review, so we will get approval by the end of 2022. Buy SCYX under $12 for a first target price of $27 now that Brexafemme is approved and a buyout at $85.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: mid-2022

Probable time of next financing: 2023 or never

Biotech MegaShift

Akebia Therapeutics (AKBA- $0.44) presented at the Jefferies Healthcare Conference (ZOOM HERE). I have to give credit to the CEO for not hiding after the Complete Response Letter. He slashed costs and is making the strongest presentation possible, plus getting ready to go to war with the FDA’s decision. Akebia has some fundamental strengths:

Click for larger graphic

Click for larger graphic

He said they are determined not to raise money. They had $174.6 million in cash at the end of March.

Click for larger graphic

Click for larger graphic

Auryxia was up 10% to $142.2 million in 2021 even as the overall phosphate market declined due to COVID-19-related deaths in dialysis patients. They are guiding for about $170 million this year.

They are expecting vadadustat approval in Europe in the March quarter. Then they will re-partner Europe, Australia, and China.

Click for larger graphic

Click for larger graphic

UT Health has completed the study of vadadustat for Acute Respiratory Distress Syndrome (ARDS) and should report data soon. This is a very big opportunity if it works, because nothing else does. AKBA is a Hold for the FDA meeting on vadadustat.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Vadadustat EMA filed

Probable time of EMA approval: March 2023

Probable time of next financing: June quarter of 2023

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $142.64) held their Worldwide Developers Conference this week and made a number of announcements. They previewed iOS 16, the latest software for the iPhone. They announced Apple Pay Later, a buy now, pay later (BNPL) product; their new and much faster M2 processor, a 13-inch MacBook Pro with M2, a new MacBook Air with M2, iPadOS 16, macOS Ventura, and watchOS 9 for the Apple Watch. The FDA approved a new Apple Watch atrial fibrillation feature just hours before the conference started.

AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $34.26) said they see Optical Communications having a multiyear significant growth environment because their customers and governments are funding large broadband network build-outs. They expect that will drive a significant amount of growth in 2022, 2023, and beyond.

Their cost reduction program is succeeding. They’ve stabilized profit margins and expect them to go up from here, in part by passing along price increases to customers and in part by continuing to reduce costs. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My first target is $60 in 2023.

At the American Society of Clinical Oncology (ASCO) meeting, Gilead Sciences (GILD – $61.18) presented final data from the Phase 3 ASCENT study of Trodelvy in patients with relapsed or refractory metastatic triple-negative breast cancer (TNBC) who received two or more prior systemic therapies, at least one of them for metastatic disease.

In a follow-up analysis from the final database lock, Trodelvy improved median progression-free survival versus physicians’ choice of chemotherapy (4.8 vs. 1.7 months) and extended median overall survival by almost five months (11.8 vs. 6.9 months). The two-year overall survival rate was 20.5% in the Trodelvy arm, compared with 5.5% for physicians’ choice of chemotherapy.

In yesterday’s fireside chat at the Jefferies Global Healthcare Conference (AUDIO HERE), the Chief Medical Officer said they now have three positive Phase 3s in different cancers. He did a deep dive into Gilead’s oncology program. There was a good article on SeekingAlpha: Gilead Sciences: Buy The Dip. GILD is a Long-Term Buy under $105 for a first target of $130.

Meta Platforms (META – $184.00) changed their name from Facebook to Meta today. The big Apple event made no mention of further tightening of privacy on iOS and no virtual reality headset – both good news for Meta shareholders. META is a Buy under $320 for a $400 target in 2022 or 2023.

SoftBank (SFTBY – $20.69) bought back 23.6 million more shares in May, bringing them to 106.9 million shares of the 250 million authorization. Masa has our backs and will keep buying stock as long as it is at this extraordinary 50% discount to the value of their net assets. SFTBY is a Buy under $30 for a first target of $60 in the next two years.

Other Tech

PagerDuty (PD – $26.73) reported April first quarter earnings last Thursday and I covered them in the Radar Report – revenues up 34.3% from last year to $85.4 million and a four-cent pro forma loss. Both were well ahead of the consensus estimate for $82.92 million and an eight-cent loss. On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said they see a strong demand environment with no impact from macro factors yet. Although 24% of revenues are international, their foreign exchange exposure is limited because all their deals are done in US dollars.

Their value proposition is automation. Given the tight market for developers, improving developer efficiency is crucial. PagerDuty now is essential infrastructure and their market is much larger than incident response.

Click for larger graphic

Click for larger graphic

They finished the quarter with 15,040 customers, up 8% from last year, including 655 with annual recurring revenue over $100,000. That number was up 43% from last year and a remarkable 10% from the December quarter. Their dollar-based net retention – how much a customer spent this quarter compared to the same quarter last year – was 126%, their sixth straight quarter over 120%. New customers included DocuSign, Cisco Systems, Genentech, Mattel, Shopify, and World Market.

They guided the July quarter revenues to an above-consensus $87 to $89 million, up 29% to 32%, with an eight- to nine-cent loss. For the January fiscal year, they raised guidance to $364 to $369 million in revenues, up 29% to 31%, with a 17¢ to 21¢ pro forma loss. Management said they will be judicious with their own expenses and expect to be profitable in the January fourth quarter and the next fiscal year.

Their non-GAAP operating model is to maintain their 85% gross profit margin, continue to invest 26% of revenues in Research & Development, somewhat reduce the percentage going to Sales & Marketing, and take a third out of the percentage going to General & Administrative.

Click for larger graphic

Click for larger graphic

On this afternoon’s fireside chat at the William Blair Growth Stock Conference (VIDEO HERE), the CFO gave a really thorough explanation of their strategy. If you have 30 minutes, this is highly recommended.

The company finished the quarter with $467.5 million in cash. PD is a Buy up to $40 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk:Digital operations management is a competitive area.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $4.44) presented this afternoon art the Stifel 2022 Cross Sector Insight Conference, but didn’t share the audio, just the slides HERE. It’s a good presentation, with sections on:

* * Launch – Electron is the second most frequently launched US rocket with 132 launch opportunities every year

* * Space Systems – more than 38% of global launches in 2021 had Rocket Lab technology, and their mission is “Everything that goes into space should have a Rocket Lab logo on it.”

* * Space Applications – their final move up the value chain is to provide data and services from space

Ken Fisher is buying RKLB. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Velo3D (VLD – $1.89) presented at both the William Blair Growth Stock Conference (ZOOM HERE) by the CEO and then a fireside chat by the CFO at the Stifel Cross Sector Insight Conference (AUDIO HERE). There are many things I like about Velo3D in addition to their very superior technology. If you listen to these two presentations you’ll hear the CEO inventor/founder of the company giving a very solid, easily understood description of what the company does and why it will win, followed by the CFO drilling down on their sales and customer qualification process. They have the company under very tight control:

Click for larger graphic

Click for larger graphic

Velo’s basic advantage is that they can make parts that no other additive manufacturing company can do, and even parts that CNC (Computer Numerical Control) can’t do. That means engineers can design things that previously couldn’t be manufactured – which has stunning implications.

Click for larger graphic

Click for larger graphic

Their launch customer (SpaceX) pricing was $2 million a system for 20 systems. Their $43 million yearend backlog included nine systems for SpaceX accounting for $18 million and nine other systems accounting for the remaining $25 million – an average price of $2.78 million. The list price now is $3 million. Each system includes one year of free maintenance, which costs $120,000 a year thereafter. This all means Velo3D’s profit margins will steadily expand. The new Sapphire XC already is a success.

Click for larger graphic

Click for larger graphic

Their average customer buys 1.3 additional printers every year to increase their production. These repeat orders plus their new customer acquisition are a “land & expand” strategy that builds the company in a thoughtful, predictable way. They have to manage their supply chain, of course, but as production shifts to the Sapphire XC, they will use the learning curve to reduce costs and improve profit margins.

Velo3D is going to dominate complex part manufacturing as production returns to the US. The opportunity to buy this company at a market capitalization under $400 million is a gift. VLD is a Buy up to $11 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,849.40) reluctantly gave a little ground up since last Thursday, but that’s pretty impressive given the strength in the US dollar against other currencies. This is obvious consolidtion and just increases the energy to power gold’s next uptrend.

Miners & Related

Coeur Mining (CDE – $3.78) presented today at the RBC Capital Markets Global Mining and Materials Conference, but they only shared the SLIDES HERE. It was their standard introductory presentation. The key slide:

Click for larger graphic

Click for larger graphic

CDE is a Buy under $10 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $0.49) said the permitting process for the Grassy Mountain gold mine took a major step forward at a recent public meeting of the Oregon State Technical Review Team’s water resource subcommittee. The subcommittee confirmed that the groundwater Baseline Data Report submitted by Paramount was accurate and complete according to the previously approved procedures and protocols. The subcommittee will recommend it for approval by the full Technical Review Team, which is comprised of all state agencies involved in the permitting process.

To date, 22 Baseline Data Reports have been accepted by state regulators. The remaining Geochemistry Baseline Data Report is expected to be approved later this month. PZG is a Buy under $5 for a $10 first target with gold over $1,600 an ounce.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: First half of 2022

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $30,087.75) has been range-bound since early May and should start moving up any day. A wide-reaching, bipartisan crypto bill emerged Tuesday from Senators Cynthia Lummis (R-Wyo) and Kirsten Gillibrand (D-NY). Lummis is on the Senate Banking Committee that oversees the Securities and Exchange Commission and Gillibrand is on the Agriculture Committee that oversees commodities and the Commodity Futures Trading Commission, so this could be a serious bill. It grants new powers and a clear regulatory role to the CFTC. It makes transactions less than $200 tax-free, potentially clearing a path for a cryptocurrency that acts more like a currency. And it would set new federal law for stablecoins, similar to a recent proposal by Senator Pat Toomey (R-Pa).

A coherent set of explicit regulations would help cryptocurrency adoption and prices, but I don’t expect anything to pass this year. At least this provides a framework to start talking.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $19.41) hired the former Obama Administration Solicitor General as an additional legal counsel to support its pending Exchange-Traded Fund application with the SEC. The SEC has a July 6 deadline to either reject or approve the conversion of GBTC to a spot Bitcoin exchange-traded fund. That would instantly jump the fund’s price by 15% or so. GBTC currently holds over 3.4% of all Bitcoin in circulation. GBTC is a Buy under net asset value.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

International & Other Recommendations

It is important to hold some non-US assets, especially in China. China Internet stocks took off yesterday on signs the regulators are easing up.

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $32.64) is a Buy under $38 for a $66 target in 12 to 18 months.

Primary Risk: China falls into a recession.

KraneShares Bosera MSCI China A Share Fund (KBA – $35.05) is a Buy under $34 for a three- to five-year hold.

Primary Risk: China falls into a recession.

Morgan Stanley China A-Share Closed-End Fund (CAF – $15.71) is a Buy under $24 for a three- to five-year hold.

Primary Risk: China falls into a recession.

KraneShares CSI China Internet Exchange-Traded Fund (KWEB – $31.59) is up around 50% from its mid-May lows. It is trading well above its 50-day moving average for the first time in months.

Click for larger graphic

Click for larger graphic

This is my favorite way to invest in Chinese technology. KWEB is a buy under $50 for a double over the next three years.

Primary Risk: China falls into a recession.

Acreage Holdings (ACRDF – $1.18) will benefit as the New York State Senate approved a bill that would require public health insurance to cover medical marijuana expenses. ACRDF is a buy under $4.49 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

Oil – $121.28

Yesterday we learned that US gasoline stocks fell for the 10th week in a row by a surprise 0.8 million barrels as demand rose despite sky-high pump prices. Analysts had expected gasoline stocks to rise 1.1 million barrels.

Gasoline hit $4.919 nationwide, with 15 states averaging over $5 a gallon and California at $6.24. I expect $6 nationwide by the end of August. All it will take is for exports to persist at this elevated pace and refinery runs – already near the top range for reasonable utilization rates – to slow slightly. Gasoline inventories will continue to draw to levels below the 2008 lows and retail gasoline prices will climb to $6 a gallon or even higher. As Chinese virus lockdowns ease, oil demand will surge, pushing up prices. The same will be true for natural gas prices, which in turn affect electricity and heating prices.

OPEC+ decided on a 648,000 barrels-per-day increase to production for July and August. Normally they would increase 432,000 each month in July, August, and September, a total of 1,296,000 barrels. Divide 1,296,000 by two months and you get 648,000. They packed three months of quotas into two. But as I’ve shown you, they can’t hit even their lower quotas – the quotas increase, but actual production doesn’t.

Click for larger graphic

Click for larger graphic

In all likelihood much of the production, even if is produced, won’t be exported because higher cooling demand during the summer means many OPEC producers experience a spike in domestic oil consumption as they burn oil to generate electricity. Global inventories are resuming their collapse, OECD inventories are falling at the same rate as 2021, and US inventories are falling faster than 2021.

So what happens to oil prices when the inventories run low? When record Strategic Petroleum Reserve releases slow down to preserve what’s left of a hollowed-out SPR? What happens when China restarts? What happens when seasonality spurs demand?

Commercial inventories will plummet, and oil prices…well, you get the picture. Got OIL?

Click for larger graphic

Click for larger graphic

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $39.26) is a Buy under $36 for an $80+ target.

Energy Fuels (UUUU – $6.46) will benefit from a new Biden Administration program to buy $4.3 billion of enriched uranium from domestic sources. UUUU is a buy under $11 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

RIP Jim Seals

* * * * *

Your thinking about the end of citizenship Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.92) – Buy under $4, ultimate target $45

Bellerophon Therapeutics (BLPH – $0.97) – Buy under $11, first target $30, then $300

Compass Pathways (CMPS – $9.79) – Buy under $36, hold a long time for a 10x return

Graphite Bio (GRPH – $2.62) – Buy under $26, hold a long time

Inovio (INO – $1.65) – Buy under $21, hold a long time

Invitae (NVTA – $2.66) – Buy under $50, first target $100, then $200+

Medicenna (MDNA – $0.91) – Buy under $4, first target $40, then maybe $80

ScyNexis (SCYX – $2.04) – Buy under $12, target price $27, then $85

Other Biotech

TG Therapeutics (TGTX – $4.10) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $142.64) – Buy under $150 for new iPhones

Corning (GLW – $34.62) – Buy under $33, target price $60

Meta (FB – $184.00) – Buy under $320, target price $400

Gilead Sciences (GILD – $61.18) – Buy under $105, target price $130

SoftBank (SFTBY – $20.69) – Buy under $30, target price $60

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $42.57) – Buy under $32; 3- to 5-year hold

Fastly (FSLY – $12.41) – Buy under $45; 2- to 5-year hold to $150+

PagerDuty (PD – $26.73) – Buy under $40; 2- to 5-year hold

QuickLogic (QUIK – $7.71) – Buy under $10, target price $60

Liberty Media Acquisition Corporation (LMACA – $9.92) – Buy under $10.50, target price $20 to $30

Rocket Lab (RKLB – $4.44) – Buy under $13, target price $30+

Velo3D (VLD – $1.89) – Buy under $11, target price $50

Inflation

A Short-Sale or REO House – $391,200 – Buy while fixed mortgage rates are low

Bag of Junk Silver – $21.71 – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $27.39) – Buy under $25, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $34.10) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.85) – Buy under $15, target price $30

Global X Silver Miners ETF (SIL – $29.80) – Buy under $30, target price $50

Coeur Mining (CDE – $3.78) – Buy under $10, target price $20

First Majestic Mining (AG – $8.36) – Buy under $15, next target price $23

Paramount Gold Nevada (PZG – $0.49) – Buy under $5, first target price $10

Sandstorm Gold (SAND – $6.57) – Buy under $10, target price $25

Sprott Inc. (SII – $37.52) – Buy under $30, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $30,087.75) – Buy

Grayscale Bitcoin Trust (GBTC – $19.41) – Buy

Ethereum (ETH-USD – $1,786.53) – Buy

Grayscale Ethereum Trust (ETHE – $11.41) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $32.64) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $35.05) – Buy under $34 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $15.71) – Buy under $24 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $31.59) – Buy under $50 for a double over the next three years

Acreage Holdings (ACRDF – $1.18) – Buy under $4.49 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.45) – Buy under $1.25; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $39.26) – Buy under $36; $80+ target

Energy Fuels (UUUU – $6.46) – Buy under $11; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $4.07) – Hold for chronic cough results

Akebia Biotherapeutics (AKBA – $0.44) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.04) – Hold for buyout

CohBar (CWBR – $0.22) – Hold for human trials of CB5138-3

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

OMG ONE

2

Can someone please explain how something like Bitcoin can be used as a routine currency when it’s value is all over the place? Wouldn’t somethong like Tether (if it is fully secure) be better to use to buy and sell stuff?

I mean, isn’t a huge benefit of our (boring, routine) dollar that it is stable?

Bitcoin’s volatility does have to go away before it can be used as a currency. I don’t think Tether is secure.

For AKBA: Probable time of next FDA approval: March 29, 2022

Probable time of next financing: June quarter of 2022.

It sounds like the CEO is saying they are determined not to raise money. Do they not have enough to get well past any FDA meeting?

Sorry, I should have updated this earlier. They’ve slashed costs and the next approval will be in Europe, unless their FDA meeting goes incredibly well. So:

<b>AKBA is a Hold for the FDA meeting on vadadustat.</b>

<b>Primary Risk:</b> Vadadustat not approved.

Clinical stage of lead product: Vadadustat EMA filed

Probable time of EMA approval: March 2023

Probable time of next financing: June quarter of 2023

Great Radar and new look at SNAP Michael Murphy. I was late getting up this AM and now just looked at the inflation numbers. They are all over the UP in the sky bad. 1% vs .7% est and 8.6% annual vs 8.3% est. and all of them looking very high. Stand by for a red day until something else arrives to tell us to turn on our fossil fuel in the United ststes or suffer until oil hits a gazillion dollars a teaspoon (of course a joke attempt) Let go see if TPL continues its ride to the moon. Good luck to all,

Doesn’t that tell you the FED doesn’t have a damn clue what is happening and going to happen in the future. First they say inflation is “transitory” , nothing to worry about, it will blow over like the last rain storm we created, then all the talking heads said inflation has peaked in March and is heading DOWN, wrong again. Let’s fire up the printing press again now and print up some more Monopoly money to hand out for the high price of gas because the greenies want fossil fuels to go away. Again CLUELESS, not only is NOT going away, even with all the political BS, OIL is one of the ONLY assets going UP in value. DAH. Flipping IDIOTS . Even Christine L, finally woke up to the fact that negative interests rates are a trip into the economic rabbit hole of hell. Who in their right mind is going to invest in government bonds paying didly squat , or worse negative interest rates when inflation is running at 8 plus percent!!!?? Where do these elected officials come from??Did the 2 year Dr.F. catastrophe/imprisonment cause everyone to lose their common sense and mind??

MM–good analysis of SNAP. All those “cool” camera tricks are merely hot entertainment for superficial kids. A good way to supercharge short term stock performance is to have a “cool” idea to market in a flashy way. The kids jump on it, then their short attention span leads them to the next fad. Then the stock crashes. What superficial idiot buys shoes for the way they look rather than how comfortable they feel on the feet? In my idiot 20’s, I bought pointy Italian shoes with thin soles that looked good, but were too tight and impractical to wear for any length of time.

Metrics may favor small cap growth stocks vs small cap value stocks now. However, any company that has no earnings is always risky. Don’t be so enthusiastic about VLD. It is a great small cap growth stock with great technology but with weaker than expected sales. That explains the drop from $10 to under $2 today. Where is the bottom? Will it see $1 before $4? That is, halving before doubling?

Agreed. This new SNAP idea is bullshit. Another example of what the best and brightest in this country are going after, a true waste of smarts, capital, time and energy. For all of its despicable failure, I still think ARTH and AC5 represent a “better” effort than this example of useless creative code writing. Some of MM’s ideas I currently like, with the caveat that we are in a Bear Market and you may have to extinguish positions at any time, VLD, RKLB, KWEB, Gold and Silver.

They will do about $150 million in sales in 2023 and currently are valued at 2.3x that number. Way too low for a company growing this fast.

Gary,

I wrote another lengthy response to you last PM on the last page, about gall bladders and uterine fibroids.

Where are the brilliant women like Wendy who seem to have disappeared?

What did happen to Wendy? I miss her. She suffered personal attacks from others still on this board so I don’t blame her for departing. She recommended ABBV a long time ago and I bought it then.

I miss her too.

No, she attacked me here for NO reason whatsoever years ago, so do not make it sound like she is some kind of victim; very bright and very nuts is probably more like it.

Also, FYI, I recommended ABBV here in 2017 upper $60s. It has been paying me 6% divvies ever since. Probably should have let some go at $172 but I guess I like/need the income. Currently suffering like most stocks/sectors under the weight of Brandon’s Bear Market.

I knew two young people that had their gall bladder removed and they had fatty food intolerance.

That’s sad, but gall bladder surgeons are oblivious to the negative digestive consequences. For these unfortunate people, I recommend bile supplements such as ox bile with each meal. The liver still makes bile, but it is slowly dripping into the intestine when it is not needed. The purpose of the GB is to store the bile. When food hits the upper intestine, the GB is signaled to contract, releasing the effective amount of bile for digestion. Analogy–if you let your shower drip slowly, you are wasting water, and it will take hours to shower. Dumb GB surgeons, but that’s the standard of care from authority figures who DO NOT follow the science.

When do you think the ARTH buyout will happen

Has to be soon, they are out of money.

MM–don’t you understand that no Big Pharma will buy out ARTH for their investigational products? There must be a reason that even the approved product AC5 didn’t sell. Some BP scientist probably figured out the flaws in the product that were not disclosed to investors. The patents are worthless if the product can’t generate any significant revenue, let alone make a profit. The BP will tell TN, “take my 5 cents or go F-CK yourself.” Buyouts NEVER occur at 20 times the current stock price. 2-3x, maybe. At today’s 4 cents, that’s 8-12 cents buyout at best.

All this 7 years of wasted mental anguish following this garbage stock. How about plunging APTO, MDNA? You have no expertise to claim that either of these has a leading strategy for fighting disease.

I never expected Big Pharma to buy ARTH for the investigational products. I expect them to buy it for FDA and EMA approval of AC5, which clearly works extremely well. The question is what is such a product worth in the hands of a large sales force.

APTO is a bet on Bill Rice, although the Phase 2 data on HM43239 certainly looks very strong.

MDNA data also looks great. Both have “a leading strategy for fighting disease” but I have lost confidence in my ability to predict how the Phase 3 trials will turn out.

ARTH–sure, AC5 is great. It may do well with a large, competent sales force. But why didn’t the BP acquirer make an offer years ago? One, maybe they did, but greedy TN turned them down. Now, TN can either take ZERO or an offer of 10 cents or so as BP says to TN, “take it or go live on the $millions you collected at the expense of your shareholders by running the company into the ground, and collect your social security benefits.” Two, BP did DD on AC5, found flaws that investors didn’t know about, and passed on it. Maybe the only flaw with AC5 is that TN priced it too high, and BP judged that a fair MSRP is much lower so that the expenses of effective marketing couldn’t be justified. (Incidentally, SCYX’s Brexa is priced too high for a few pills, so it is not being approved or selling that well now. Much of the fault underlying high prices is the inefficient, lengthy FDA process for getting approvals.)

APTO–there are a few posters like Carol J on YMB who know oncology better than you, I or Bill Rice. Case numbers enrolled are growing at a dinosaur pace, and there is little to show for all the time and money spent.

MDNA–as with APTO, nobody there has “a leading strategy for fighting disease.” There is no oncologist who knows what the hell they are doing, except on a superficial level. Fighting disease is much more complicated than any one model of magic bullet drug targeting of the “right” pathogenetic mechanism. I’ll say to Dr. Joe Onco to go ahead and think you know how to tailor your cytokine analog to the disease. You don’t care or pay attention to the fact that the cause of all disease is epigenetic modification by environmental toxicants, poor nutrition, etc. These are the true underlying causes of disease, which then secondarily result in biochemical anomalies. But targeting the biochemical anomalies is like treating symptoms, and will not cure the disease.

Read Dr. Dale Bredesen’s book, THE END OF ALZHEIMER’S for his indictment of the mainstream magic bullet approach in this field. Flawed theories of dissolving amyloid plaque–the drug trials have all failed. But the investigators never learn, and perpetually play the political game of getting grant money from federal agencies full of ignorant MD’s.

I told you–get out of the mainstream medical field for your investment ideas.

Well, the talking heads are now saying 1% for the Feds and sequential 50 50 50.and now looking closer to the big R show Note that SAND turned up as has gold. I always liked Wendy L and we also bet on some pennies. one for you. SGLDF Has had Sprott interest and will be operational this year with its Goldstone mine in Arizona as its partner Alaska mine is starting permits. Do your own due diligence.

I bought some SGLDF about 100% higher. Would love to see it move up as it’s my on;y PM play.

“Don’t fight the Fed!” Direxion has a 3x bear on the 7-10 year treasury notes (TYO). With the Fed having told us all that a couple half-point raises are to be expected and inflation showing its ugly head, shoulders and upper torso, this seems to be a no brainer. I watched it go to $12 a share in early May but then drop back under $11. On the way back up, I bought. With today’s inflation news the shares were in high demand. I don’t know if I would be a buyer here, maybe wait for a pullback or just nibble here, but I don’t see how this doesn’t work.

Was there any news or promotion on Acurx that explains its pop in the last 2 sessions? Usually the stock loses its gains soon after these promotions. I figure we can wait before adding, since enrollment in phase 2B could be delayed another 6 months or more. The only risk is FDA sabotage from Big Pharma.

There was a paid promotional piece comparing AcuRx to Seres’ poop pills and all the CDI failures with PFE, Summit, Sanofi and Finch. I don’t worry about FDA sabotage from BP, because I expect AcuRx to sell to BP next year after P2 results are revealed. TYO working quite nicely.

Thanks. Where did you find this info about the promotional piece–have a link? I just don’t understand why ACXP is always thinly traded, with little interest on YMB.

I confused ACXP with NGEN. The latter does promotions which pop the stock only briefly. NGEN granting of a few stock options exercised at over $2 isn’t significant to explain today’s plunge.

09-Jun-2022:07:51:00, Pfizer’s CDI Trial Miss Puts Acurx Pharmaceuticals Ibezapolstat In Front-Line Position, Here’s Why Big Pharma May Come Calling ($ACXP)

Finding an effective treatment against C. difficile has been challenging, with the past few decades serving up little more than short-term relief from CDIs debilitating symptoms. But, one micro-cap company, Acurx Pharmaceuticals (NASDAQ: ACXP), is on the right path to changing the treatment landscape with its CDI treatment drug candidate showing best-in-class front-line treatment potential.

In fact, data is more than good; its ibezapolstat candidate demonstrates things that others cant… overwhelmingly positive results that treat debilitating CDI symptoms and deliver a more vital interim result- it can cure the infection. And that distinction may have ACXP on the radar screens of several of the Big Pharma players.

From Under The Radar To Blinking Bright

That presence is well deserved and well-timed. Acurx Pharmaceuticals, after all, could be the last company standing in a race to capture the lions share of the estimated $1.6 billion CDI treatment market opportunity. The better news for ACXP to make that happen is that several potential competitors have dropped off the clinical radar over the past decade, with each relegated to potentially treating, at best, niche indications of the infection. The latest disappointing data came from Pfizer (NYSE: PFE), which missed meeting its primary endpoints in its Phase 3 CLOVER trial to treat C. diff. But they arent the only ones licking their wounds.

Sanofi (NYSE: SNY) missed its endpoints back in 2017, and more recently, Summit Therapeutics (NYSE: SMMT) published topline results that were far from impressive. In fact, that miss resulted in them trying to change the primary endpoints in its Phase 3 trial, something the FDA didnt accommodate. Those three werent the only ones disappointed to date.

Another pharmaceutical company, Finch Therapeutics (NASDAQ: FNCH), saw a setback when it received a clinical hold letter from the FDA about concerns over its SARS-CoV-2 donor screening protocols. While Finch announced that the FDA hold was lifted and that enrollment would resume in 2H 2022, they still lost considerable clinical momentum. Its appropriate to note that FNCHs Phase 2 data was impressive compared to Pfizer, Sanofi, and Summit. It showed that 80.3% of trial participants receiving a single administration of its candidate following standard-of-care antibiotics achieved sustained clinical cure through eight weeks. Promising, yes. Better than ACXP? No.

Better Data, Dual Action

Acurxs candidate published Phase 2a data that appears to be significantly better. The most significant advantage could be that compared to Finchs candidate, which focuses on the microbiome as a single dimension and has shown only a reduction in recurrent infection, ACXPs ibezapolstat is a dual impact drug that addresses the direct infection and, to date, avoids recurrent infection altogether. Not only that, it restores the microbiome, a critical consideration.

That difference alone endorses a persuasive and data-justified argument that ACXPs candidate is seemingly better than Finchs one-dimension drug in cases of multiple recurrent infections. If thats the case, ACXPs candidate checks additional boxes to become the preferred first-line treatment. And other than Finchs, no other candidate looks close to emerging as a serious threat to ACXPs ibezapolstats intended front-line position.

Thats potentially excellent news for ACXP. And its the reason why ACXP could already be on Big Pharmas shortlist for acquisition or licensing terms to earn the lions share of a lucrative market opportunity.

Big Pharma Dialing?

Speculation is that Pfizer could be the first to call. Investors are zeroed in on Pfizer clearly expressing their interest in pursuing the over one billion dollar market opportunity during its CLOVER trial update commentary. Still, interest and ability are two different clinical beings, and in the drug industry, only the latter matters.

With that said, dont think PFE is blinded by unwarranted optimism. They know its candidate failed to meet endpoints. Moreover, they likely know, at best, its candidate, if approved, would be relegated to treating fringe and niche CDI treatment indications. Therefore, spending potentially hundreds of millions of dollars more to advance an unpromising drug candidate makes little to no sense.

What does make sense is for deep-pocketed Pfizer to cozy up with the presumed CDI treatment drug frontrunner. In this case, with data supporting the presumption, Acurx is the likely recipient of their first call. Remember that PFE doesnt invest billions to earn a backstage pass. Instead, history indicates that what they cant produce, they acquire. And with ACXP showing evidentiary promise as one of the only companies left to bring an effective and comprehensive CDI treatment to market, it may be wise to consider a fair price for its lead asset.

Better news on that front for ACXP and investors is that the price point could be hefty, with ACXP bargaining from a position of strength. Remember, data supports the potential for ibezapolstat to become the front-line therapy to treat over 500,000 patients who get CDI each year. Of those 500,000, more than 20,000 patients per year die. So, while the term infection is used, dont underestimate its potential 4% outcome. CDI can be fatal.

Race For A CDI Cure

Its why the race to find a treatment, better yet, a cure for CDI, is a persistent pursuit. And thats precisely what ACXP may be serving up. So dont think Pfizer calling on Acurx is overly speculative. They would be dialing because ACXPs Phase2a data showed 100% cure after 10 days of treatment and 100% sustained cure after a 30-day follow-up. Thus, the totality of data, even noting Finchs one-dimensional eight-week sustained cure, shows ACXPs Phase 2a data to date constitutes the best clinical data seen in the CDI space.

Also strengthening its likelihood of earning front-line status, ACXPs CDI candidate demonstrates restoration of the patients microbiome during treatment, which is highly unusual for an antibiotic. Considering that, its reasonable to consider ibezapolstat as a potential “dual impact” therapy because it restores the microbiome while tending to the acute infection.

More in ACXPs favor and likely attracting industry attention is that the data from its Ph2a trial was so impressive that it led the Trial Oversight Committee and the Scientific Advisory Board to allow for early termination of its Phase 2a trial and advance straight into a Phase 2b study. Furthermore, that jump was allowed after data on just ten patients showed a 100% cure rate and 100% sustained cure after follow-up.

They save time and resources from that allowance. They benefit further from the FDA already granting ACXP a Qualified Infectious Disease Product (QIDP) and a fast-track designation for the companys ibezapolstat treatment. Interest in their getting a better drug to market faster could stem from knowing that Vancomycin, the current standard of care for CDI, has a recurrent infection rate of up to 40%, meaning it is not as effective in long-term treatment.

Dont Forget The Value From Massive Demand

Also, keep in mind that an approved ibezapolstat will likely meet overwhelming demand. A 2017 update of the Clinical Practice Guidelines for C. difficile infection by the Infectious Diseases Society of America (IDSA) and Society or Healthcare Epidemiology of America (SHEA) indicates that C. difficile infection presents a significant problem to those in healthcare settings and among the general population. The disease is so prevalent in hospitals and long-term care facilities that the New England Journal of Medicine called C. difficile one of the most common causes of health-care-associated infections in hospitals.

While there is already a plethora of company-published data to support and attract interest, theres more to consider. And its again favorable to ACXP. Data published from ACXPs Phase 2a trial in Clinical Infectious Diseases, one of the most respected journals in the medical community, indicates that ibezapolstat is well positioned to earn the front-line treatment crown. According to the article, ibezapolstat showed ideal traits as an oral antibiotics candidate, demonstrating a highly potent response against C. difficile, good tolerability, and limited gastrointestinal absorption. That resulted in very high fecal concentrations, which may reach three orders of magnitude above the MIC for C. difficile.

The article further noted that in addition to the ibezapolstat treatment being highly effective at killing C. difficile, it appears to do so while maintaining the populations of helpful bacteria in the gut microbiome. These signs indicate that the treatment may do more than cure CDI in the short term; it can significantly reduce the likelihood of recurrent infection.

Will Suitors Come A Callin?

Whats it all mean? Put simply, ACXP could be in play. Moreover, things could move quickly, noting that the cost to partner with a Phase 2 company over a Phase 3 company can amount to hundreds of millions of dollars. Yes, hundreds of millions. Just look at before and after market cap shots of companies making that leap. Its a valid indication of how valuable being a Phase 3 trial with compelling, best-in-class data can be.

The bottom line… Acurx is in the right place with the most promising CDI treatment drug to make a deal. And while several companies may be interested near-term to partner or license, the chatter centers around Pfizer being the ideal and most likely suitor.

If so, whether in Phase 2 or Phase 3, ACXP investors could be in for an exciting ride in 2022. Catching that action from the inside and looking out may be the better place to reside. After all, what may be considered chump change from Pfizer, or another pharma player, would be a windfall for Acurx Pharmaceuticals and its investors. And the way things could play out, both may get that benefit.

Well thought out and informative Chris thanks.

Thanks, Chris. Where did you find this article? Perhaps I can follow this analyst for updates.

It all sounds great, so why is ACXP so thinly traded?

Is there blood in the streets yet?

This week is going to be ugly, the Fed may increase rates by .75% on Wednesday? Recession here we come. Or is it stagflation here we come?

good evening all. Waiting for the Celtics-Golden Warrior Game. Started an exccellent book By Alex Epstein titled “Fossil Future, Why Global Humand Flourishing Requires Mor oil, Coal and Natural Gas- Not Less. Epstein’s premise is where most reputable books are going these days; after Steve Koonin’s very highly respected best Seller in Amazon, (not the condensed copy-too many agendas) titled “Unsettled” which acknowledges a striong need fo fossil for a long time for baseloading energy systems including distributed systems. Koonin is widely respected by more recent members of the IPCCC. My favorite Michael Schellenberger, author of Apocalypse Never and and SanFran sicko , a great physicist and climate researcher is impressed with Epstein’s energy density physics considerations. Epstein is founder of the Center for Industrial progress. Do your own due diligence. I am thoroughly convinced we are squeezing our fossil supremacy into a policy catastrophe and Michael Murphy is probably right closer to $200/bbloe.

Either someone shocks Biden and his team to sanity,or we are gonna have an enormous investment quandry, with ripples of alternative week short strategies, volatility, Recommend a prayer as well. Go Celtics.

“Do you own due diligence.”?

No, I don’t own it; I can barely rent it, a coupla minute at a time.

Prices for natural gas and coal are high amid a worldwide energy crunch, but renewables — powered by the wind and sun — have no fuel cost.

“Because the price of wind and sunlight hasn’t doubled in the past year like other resources, they are acting as a hedge against high fuel prices,” said Joshua Rhodes, an energy researcher at UT Austin.”

“Texans are cranking on the air conditioning this week amid an unusually early heat wave, setting new records for electricity demand in the state, which surpassed 75 gigawatts on Sunday and smashed the 2019 record. Texas grid operator ERCOT projects it could approach that peak again on Tuesday.

But unlike previous extreme weather events in Texas which led to deadly blackouts, the grid is holding up remarkably well this week…owed in large part to strong performances from wind and solar, which generated 27 gigawatts of electricity during Sunday’s peak demand — close to 40% of the total needed.

“Texas is, by rhetoric, anti-renewables. But frankly, renewables are bailing us out,” said Michael Webber, an energy expert and professor at the University of Texas at Austin. “They’re rocking. That really spares us a lot of heartache and a lot of money.”

Despite the Texas Republican rhetoric that wind and solar are unreliable, Texas has a massive and growing fleet of renewables. Zero-carbon electricity sources (wind, solar, and nuclear) powered about 38% of the state’s power in 2021, rivaling natural gas at 42%.

This is a relatively recent phenomenon for the state.

“Wind and solar would not have been available in years in the past, so the growing capacity helps to alleviate reliance on natural gas and coal,” said Jonathan DeVilbiss, operations research analyst at the US Energy Information Administration.

Not only have renewables helped keep the power on during a scorching and early heatwave, they have also helped keep costs low.

You need to add in the costs of building infrastructure and maintenance for windmills, solar panels, etc. Wind/solar are impractical in certain climates. Texas is favorable.

100 years ago, horsepower was sort of free, but you had to feed the horse and maintain his health. We used to briefly fan ourselves in the heat, but the act of moving your arms makes you warmer. Continuous exercise increases energy requirements (food) which costs money. Renewables are not free. Nuclear is the best alternative. Liberals who preach diversity should not sabotage fossil fuels. We could use several energy sources, best determined by market demand.

MM?

Also, you might think using renewables doesn’t deplete natural resources the way using fossil fuels does. Energy from horses is renewable, as long as you feed and care for the horses. But food production requires resources. Electric vehicles are attractive, but having most of the US utilize EV’s would deplete lithium and other materials for batteries, etc. The sun’s energy is free, but solar panel materials and maintenance consume resources. What if you need a new roof? You have to dismantle the solar panels and put them back after the roof is done–more costs.

Do your research about ALL the costs involved in any form of energy production. Is there any energy that is ACTUALLY zero carbon? To manufacture and install windmills, other forms of energy are used, like nonrenewables. A small % of people live on a mountain and can use waterfalls to generate electricity.

Texas is the most full of shit state in the country. Perhaps Beto can try to correct course but I doubt it.

Everyone knows that renewables are the only way out of this mess but no GOP member can get elected unless they have a gas line up their ass and a gun in both hands.

Instead of your left wing propaganda tirade, do the cost analysis I mentioned just above. EV’s are fine for a few people, but renewables (which are not really renewables due to their own environmental costs) will not meet the energy needs of most of the US.

TGTX–now at all-time (?) lows, down over 90% from one year highs. This AM, a YMB poster thought that similar to Roche’s Ocrevus in 2016, the reason for the 3 month FDA delay is a manufacturing issue which requires correction. Not quite the kiss of death, but close. What is disgusting is the CEO’s evasion and silence on this. Shareholders are angry, and they will be FUMING when a CRL comes out in Dec.

This is my sole NWI stock that has any chance of offsetting my huge losses in NWI bios. At the very least, MM needs to drop his unrealistic, pie-in-the-sky projections for the other bios which are rank high risk speculations. They should all be downgraded to holds, if not sells.

CDE

MM or any goldbugs out there, is there any value to be had in CDE as a takeover target with all the heavy activity in M&A in this sector?

https://www.spglobal.com/marketintelligence/en/news-insights/blog/gold-market-outlook………Good read

Also:out https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/gold-mining-m-a-poised-to-heat-up-in-2022-as-asset-pipeline-runs-bare-68503860

CDE and PZG are poor quality gold companies. MM projected they would skyrocketed when gold rose over $1600. Blue chip major gold companies have done MUCH better. Why are CDE and PZG such dreadful laggards?

I am buying the dip. NVTA today @$2.00 and change and SNAP. Call me crazy if you will.

Back up the hearse prices. These aren’t dips, they are death spirals.

Snap will not survive this bear market. TikTok and Google youtube shorts will stab it to death.

How about that nice head fake from the suits yesterday to suck retail in so they can be rug pulled? Scum of the earth.

IMO, this mess is just getting started. I own a bit of GOOG for the split run that probably won’t happen. The only things I own of interest are QID, GDX, SLV, TBT, and bit of OIL but a recession will kill oil prices.

I’d love to see TSLA go into the 200s. Maybe I’ll get lucky. Musk has completely lost his mind and needs to be replaced as CEO.

FYI .. this bubble was going to burst regardless of the color tie in the oval office. Everyone blaming Biden for the price of oil and inflation don’t understand how global money printing works. I think we are in the beginning stage of people losing faith in the FED. Invest carefully.

Thanks Michael for finally saying Elon sucks. I was getting worried about you for a minute. I know you’re a Tesla fan but you can’t separate the man from the company on that one.

I think Elon is brilliant but the combination of sleep deprivation and Adderall/wine has impaired his judgement. I still believe Tesla will become the largest company in the world mostly due to AI and robotics but I wouldn’t dare add here.

Biden’s huge spending caused the Fed to print money. Europe is worse with huge money printing and negative interest rates.

The new Radar Report for 6.16.22 is posted. Happy Father’s Day!