Dear New World Investor:

A big welcome to several new and returning subscribers! As you could tell from yesterday’s action, you’re just in time for the fun. Please read the Comments and make your own – there are a lot of smart people here.

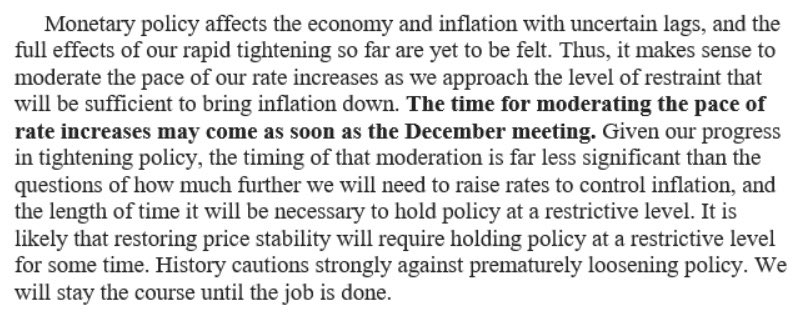

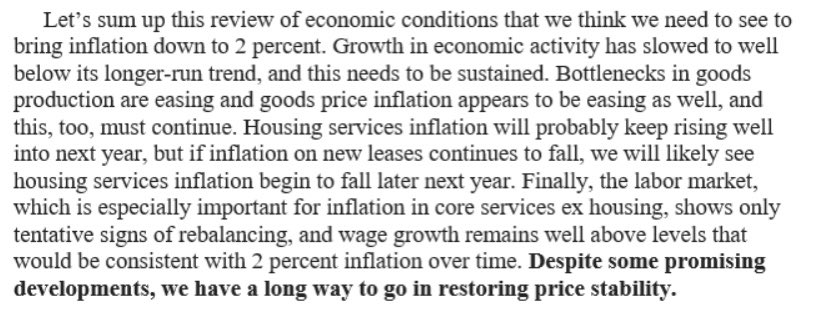

Fed Chairman Powell started the pivot I expected yesterday, signaling a 50 basis point (1/2 percentage point) increase in the Fed funds rate at the December 14 meeting, and the stock market loved it. He now thinks a recession is just as likely as not: “…risks to the baseline projection for real activity were skewed to the downside and viewed the possibility that the economy would enter a recession sometime over the next year as almost as likely as the baseline.”

He said: “It makes sense to moderate the pace of our rate increases as we approach the level of restraint that will be sufficient to bring inflation down.” Then he made it perfectly clear: “The time for moderating the pace of rate increases may come as soon as the December meeting.”

Click for larger graphic

Click for larger graphic

He acknowledged that the inflation components that have generated the largest rise now are expected to subside, perhaps significantly, as forecasts continue to anticipate. But he highlighted the labor market as a potential problem for getting inflation down:

Click for larger graphic

Click for larger graphic

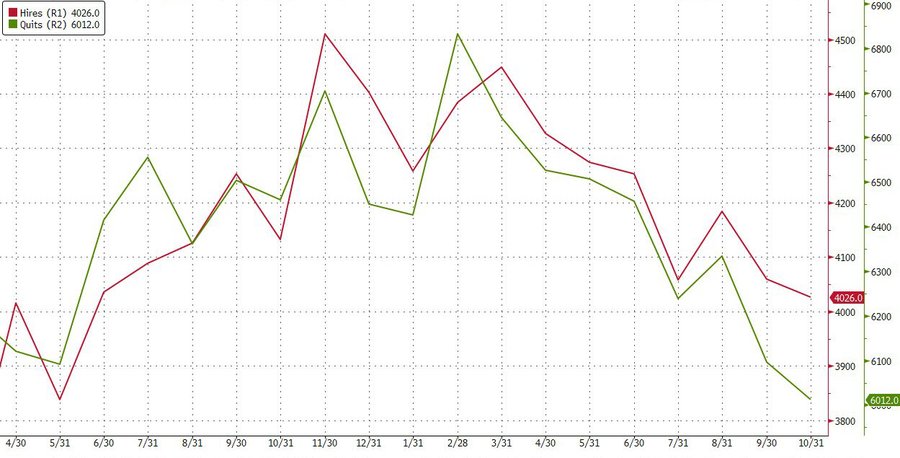

Powell said there’s been a shortfall in labor supply, primarily due to excess or early retirements and the slow growth in the working-age population. We get the November payrolls number tomorrow morning, with +200,000 expected. But the newest data shows the labor markets are softening fast. New hires have fallen to the January 2021 level. Quits, which indicate confidence to get a better-paying job, have fallen to the May 2021 level.

Click for larger graphic

Click for larger graphic

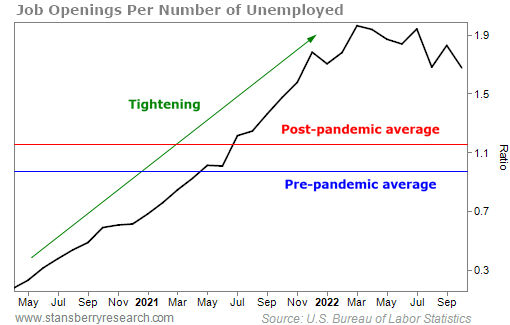

One month after the August Job Openings and Labor Turnover Survey (JOLTS) report showed an unexplained surge in job openings (following the 890,000 plunge in July), things are reverting back to normal. The August number was revised down to +407,000 and in September the trendline resumed its grind lower as another 353,000 job openings were gone, bringing the total openings to 10.3 million, down from the record 11.9 million in March. The ratio of job openings to the number of unemployed for October dropped back to 1.7. That’s the lowest ratio since the 1.6 in November 2021. It’s still above the pre-pandemic average but moving in the right direction.

Click for larger graphic

Click for larger graphic

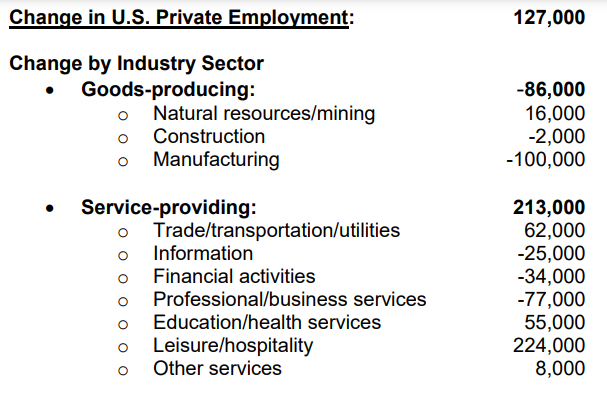

Yesterday’s ADP Employment Report showed job creation slowed by the most since January 2021. The data was not only weaker than expected but the shift in the makeup of the hires was to lower quality jobs. The manufacturing sector lost 100,000 employees, pointing to a weakening economy. If it wasn’t for 224,000 fast food workers, payrolls are now negative.

Click for larger graphic

Click for larger graphic

So the Fed is starting their pivot – remember, the pivot is a process, not a data point – because they can see the economy slowing quickly. They will keep raising rates at a slower and slower pace and, yes, we may wind up at a higher terminal rate than expected. But some companies will post strong earnings growth in 2023, others will advance important drugs or get FDA approval, and their stocks will go up regardless of the Fed funds rate.

This morning’s inflation news showed the Fed’s favorite indicator, the core Personal Consumption Expenditures Index, rose only 0.2% in October, less than the 0.3% expected. That’s an annual rate of 3.7% – not 2.0% yet, but getting there quickly.

This has been the worst Fed hiking cycle for equities. In 11 prior hiking cycles, nine saw equities go up (8% to 29%), one saw them down modestly (-2% in 1994) and one saw them down significantly (-13% in 1973). The current hiking cycle has equities down 25% peak-to-trough and 15.4% peak-to-current.

Click for larger graphic

Click for larger graphic

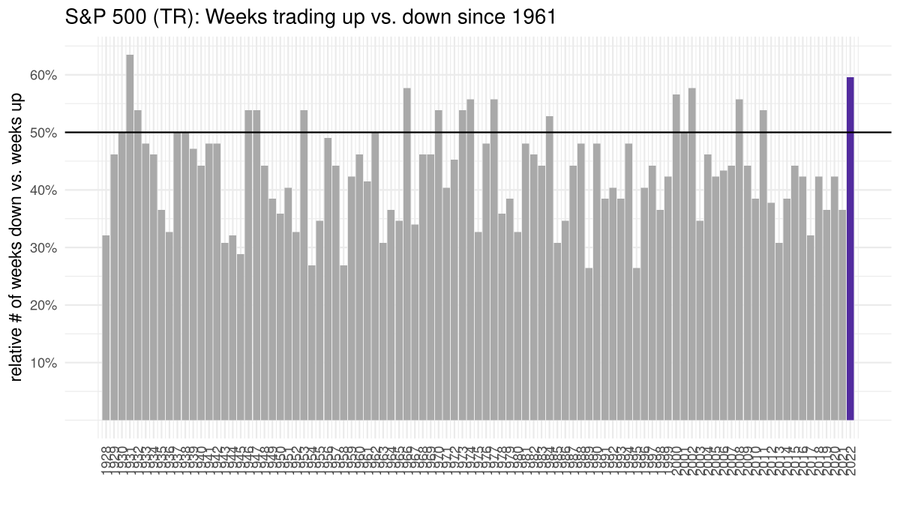

The S&P 500 has lost money in 59.6% of the weeks this year, the most since 1931. No wonder it feels so bad!

Click for larger graphic

Click for larger graphic

Both professional and retail investors are very negative. The Bears have outnumbered the Bulls in the American Association of Individual Investors sentiment poll for 35 consecutive weeks, since April 7. With data going back to 1987, that’s now the longest streak of negativity that we’ve seen.

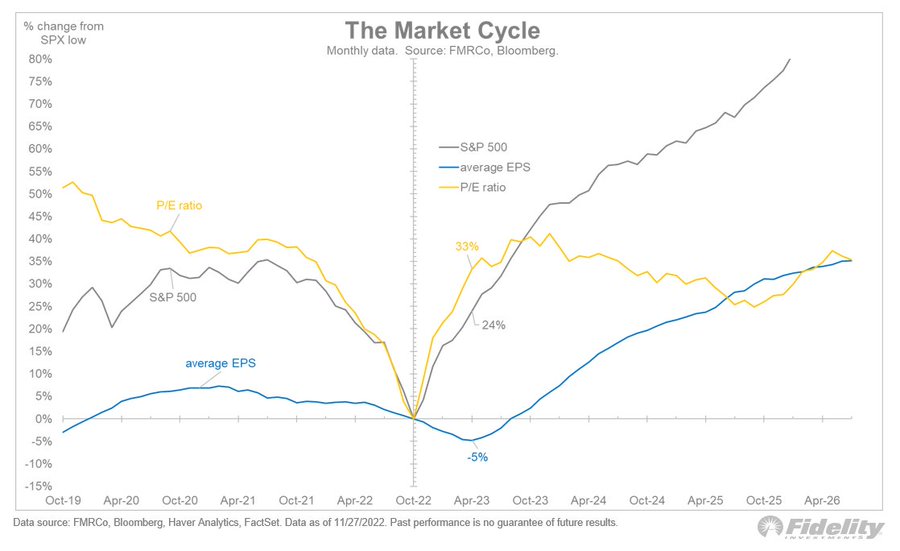

Whether the stock market’s low is behind us might hinge on when earnings growth hits bottom. This chart shows the average for all bear-market bottoms, indexed to the price low. There is a clear pattern of price bottoming several quarters before earnings.

Click for larger graphic

Market Outlook

The S&P 500 added 1.2% since last Wednesday, including yesterday’s 3.1% jump to close above its 200-day moving average for the first time since April 5. The Index is down 14.4% year-to-date, its worst performance through the first 11 months of any year since 2008.

The Nasdaq Composite gained 1.7%, including yesterday’s 4.1% jump, but is down 26.6% for the year. The small-cap Russell 2000 moved up 1.0% and is down 16.2% in 2022.

The S&P 500’s price/sales ratio has come down significantly from the peak. The orange circles highlight where the ratio was at major market lows in 2020, 2018, 2009, and 2002.

Click for larger graphic

Click for larger graphic

The fractal dimension is loaded with energy and will start dropping if the uptrend continues. It’s a long way from signaling the consolidation is over, but if it does there is plenty of power to have a bang-up start to 2023.

Top 5

Changes this week: None

Near-Term – chronological order

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Their bitcoin is safe; the discount is a gift

INO Inovio – VGX-3100 HPV Phase 3 results by yearend

TGTX TG Therapeutics – FDA approval on December 28

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphite Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

September quarter real GDP growth was revised up from +2.6% to +2.9%, but the Atlanta Fed’s GDPNow model for December quarter growth fell sharply to +2.8% due mostly to a decrease in real personal consumption expenditures.

Click for larger graphic

Click for larger graphic

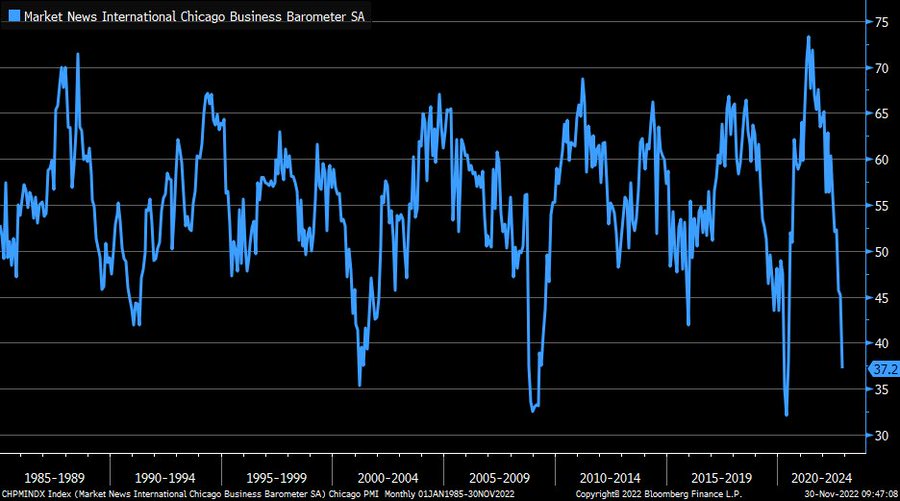

The Chicago Purchasing Managers Index doesn’t have the same weight as the ISM Manufacturing index, but it’s still a reliable indicator. The November Chicago PMI fell sharply to 37.2 versus the 47.0 estimate and 45.2 in October. It is now starting to flirt with the pandemic lows. Prices paid rose at a slower pace; new orders and production fell at a faster pace; inventories rose at a faster pace; and employment fell at a slower pace. In the last 55 years, this level of the Chicago PMI has always coincided with a recession.

Click for larger graphic

Click for larger graphic

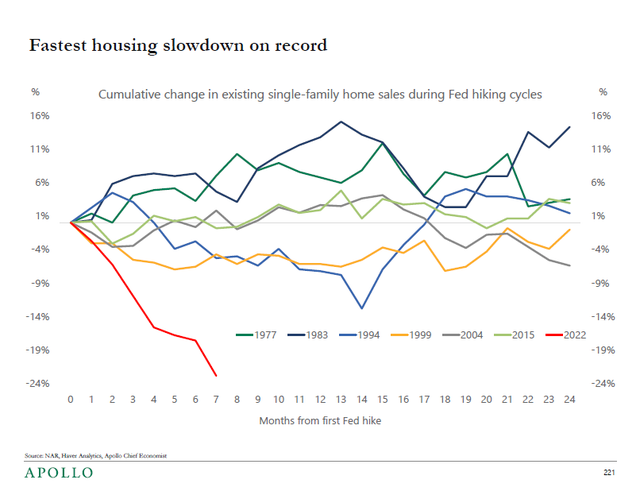

And a housing market crash is in progress:

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, December 2

November payrolls – 8:30am – +200,000 expected vs. +261,000 in October

Tuesday, December 6

ACRDF – Acreage Holdings – Unspec. – Cowen Cannabis Conference

Wednesday, December 7

GILD – Gilead – 8:00am – Nasdaq Investor Conference

Thursday, December 8

GLW – Corning – 12:50pm – Barclays Global Technology, Media and Telecommunications Conference

Friday, December 9

Short Interest – After the close

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations are typically very low. At the same time, Initial Public Offering valuations had moved very high. We were seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors make 5x to 10x in a reasonable, three- to four-year period if they buy at those valuations. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Compass Pathways (CMPS – $10.22) did a fireside chat at the Evercore ISI HealthCONx Conference (ZOOM HERE). There wasn’t a lot new – the Phase 3 trial still kicks off this year. There was a good general discussion about the problems of treatment-resistant depression, other drugs, and so on.

They have a cash runway into 2024. They will have two Phase 2 readouts in 2023, one in anorexia and one in PTSD. One Phase 3 readout in treatment-resistant depression is scheduled for 2024 and the other for 2025. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2024

Probable time of next financing: Mid-2023

Graphite Bio (GRPH – $3.43) CFO Alethia Young gave a very good presentation at the Evercore ISI HealthCONx Conference (ZOOM HERE). Alethia was a Wall Street biotech analyst – a good one – and she carries the sickle cell gene, so she has skin in this game. This was mostly a backgrounder on GRPH. GRPH is a Buy under $9 for a $50 target in 2023, $100 in 2025, and then higher.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 1

Probable time of first FDA approval: 2025

Probable time of next financing: Mid-2024

Invitae (NVTA – $2.97) launched a Rare Patient Network for patients with pediatric epilepsy and/or developmental delay, with plans to include other conditions in the coming months. By directly engaging with patients with rare neurodevelopmental conditions, they’ll make it easier to identify and recruit patients into clinical trials. Even before a diagnosis or without a diagnosis, families who are grappling with epilepsy or a developmental delay will have a way to help each other and themselves simply by using their own medical records as a resource. When a treatment comes along, this resource will already be there just waiting to be part of the solution. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

ScyNexis (SCYX – $2.12) got FDA approval of Brexafemme for recurrent vulvovaginal candidiasis (VVC), as I predicted. It is now the only FDA-approved therapy for both the treatment of vulvovaginal candidiasis and the reduction in the incidence of recurrent VVC. That should make partnering it easier and more lucrative. Buy SCYX under $2 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: late-2022

Probable time of next financing: second half of 2023 or newer

Biotech MegaShift

Akebia Therapeutics (AKBA- $0.29) gave a fireside chat at the Piper Sandler Healthcare Conference (AUDIO HERE). Management said the issue with the FDA is a difference of opinion on the risk/benefit profile. Akebia is arguing this should be a labeling issue to let doctors and patients decide if they want to use it. Right now, Akebia is expecting a decision by the end of the year.

They are expecting European approval for both dialysis and non-dialysis in the March quarter. They have several interested potential partners lined up. AKBA is a Hold for the results of the FDA meeting on vadadustat.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Vadadustat NDA filed

Probable time of next FDA approval: Unknown

Probable time of next financing: Unknown

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $148.31) slipped on reports that iPhone 14 Pro and Pro Max shipments in the December quarter could be 15 million to 20 million less than expected due to the Chinese lockdowns. No one is talking about a lack of demand. Bloomberg reported Foxconn’s massive iPhone factory in Zhengzhou, central China, is set to ease COVID control measures.

The December quarter is a big one for Apple, and I’m seeing numerous marketing campaigns. Six months from now, no one will care about Chinese lockdowns. AAPL is oversold and a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $34.24) presented at the Credit Suisse Technology Conference (SLIDES HERE and TRANSCRIPT HERE). The company is building a new optical cable factory in Arizona to meet record demand. In smartphones, they just introduced Gorilla Glass Victus2, which delivers improved drop performance on rough surfaces like concrete while preserving the scratch resistance of Gorilla Glass Victus. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2023 .

Gilead Sciences (GILD – $87.90) presented at both the Evercore ISI HealthCONx Conference (TRANSCRIPT HERE) and the Piper Sandler Healthcare Conference (TRANSCRIPT HERE). At Evercore, the CFO said: “When we look at the HIV business going forward, it’s a great setup for us in terms of the strength of the business and the performance and the long runway that we believe that we have, growth ahead of us. And then the oncology business is really performing. You saw that in the first three quarters of the year. The third quarter was fantastic. A number of shareholders have commented on the fact that the oncology business is now a bigger business than the HCV business and it’s growing substantially…

“So for this year for the base business, we’re guiding 5% to 6% growth for the year. And what we’ve said is that the growth we think that the pipeline is going to deliver, improved growth profile over time and that you should really see an inflection in the mid-part of the decade and that the growth should improve from that point on as well. So we like where we are and we think we have the pipeline that’s going to deliver improved growth.” GILD is a Long-Term Buy under $70 for a first target of $100.

Other Tech

Fastly (FSLY – $10.06) did an excellent fireside chat at the Credit Suisse Technology Conference (TRANSCRIPT HERE). The new CEO (from Cisco) said: “The biggest maybe positive surprise was the innovation roadmap, the velocity of innovation at Fastly and the way the roadmap is playing out, I think was in a lot better shape than I thought perhaps from the outside, especially in that there is sort of a core business in network services and content delivery and there is a growth engine – a growth business in security, especially with the Next-Gen WAF and Signal Science acquisition.”

Looking forward, he said: “I think in three years, if people think of Fastly as a Content Delivery Network business, we would have failed, like that would be a huge issue. We are an edge cloud platform. That’s where we deliver value to our customers. We are not trying to relieve load from people’s web servers. We are trying to deliver the best possible user experience and the edge cloud platform is going to be the answer for that for years and years to come.”

FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Probable time of next financing: None needed

PagerDuty (PD – $22.52) reported October third-quarter results after the close today (AUDIO HERE and SLIDES HERE). Revenues grew 31.3% from last year to $94.2 million with pro forma earnings of four cents a share. They guided the December quarter for revenues of $98 million to $100 million, in line with the $99.07 million consensus, with earnings of two to three cents a share, above the one-cent consensus.

For the January 2023 fiscal year, they guided for revenues of $368 million to $370 million, a skootch above the $367.82 million estimate. They expect pro forma earnings to breakeven to a penny a share, well above the consensus for a loss of 11¢.

It was a strong quarter, their sixth in a row with revenue growth above 30%.

Click for larger graphic

Click for larger graphic

PagerDuty sells a fast return on investment:

Click for larger graphic

Click for larger graphic

The stock is up over 4% in after-hours trading. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk:Digital operations management is a competitive area.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $4.22) decided to allow more time for final pre-launch preparations, and now is targeting December 9 for their first mission from Launch Complex-2 in Virginia.

Hurricanes are some of the most destructive weather events on Earth. To help study these powerful storms, NASA has selected Electron to launch TROPICS – a collection of small satellites designed to measure storm strength and help improve forecasting models. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,817.70) had a big day today, up 3.3%, as the Fed pivot caused the US dollar index to retreat to a three-month low. The fractal dimension is still at historic levels that could easily power this move to new all-time highs.

Miners & Related

First Majestic (AG – $9.51) sold a portfolio of its royalty interests to Metalla Royalty & Streaming (MTA) for $20 million in common shares of Metalla common stock, about 8.5% of the company.

The royalties include 100% of the gold from the La Encantacia silver mine, up to 1,000 ounces per year, and a 2% Net Smelter Return on the smaller mines. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $0.38) said the Federal Bureau of Land Management has accepted the Plan of Operations for the proposed Grassy Mountain gold mine in eastern Oregon as complete. The BLM will issue a Notice of Intent, thereby initiating the Environmental Impact Statement process that culminates in a Record of Decision that sets out the BLM’s decision regarding the proposed mining operations. That process should take a year. PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: Second half of 2022

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $16,960.37) had a very bad November, booking the fourth largest realized loss event for holders on record. As the fallout from the FTX fraud plays out, I expect less capital to flow toward the altcoins and more into bitcoin and ethereum. Brazil just passed a law to legalize cryptocurrencies and Fidelity has started opening retail bitcoin trading accounts.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $8.89) has all their bitcoin stored in offline or “cold” storage with Coinbase Custody Trust Company, a fiduciary under §100 of the New York Banking Law and a qualified custodian for purposes of Rule 206(4)-2(d)(6) under the Investment Advisers Act of 1940, not at an exchange or somewhere it can be hacked. The current fear-based discount of 42.7% from net asset value will go away fairly quickly, so now is the time to grab it. GBTC is a Buy under net asset value.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

International & Other Recommendations

It is important to hold some non-US assets, especially in China. China is easing its Zero-COVID policy in response to the protests. Chongqing, a provincial-level city I visited on a trek up the Yangtze River, has relaxed its COVID rules. When I was there I noticed many families with multiple children. When I asked about the one-child policy then in effect, my guide said that was just an idea from the Big Dogs in Beijing and they didn’t pay much attention.

Guangzhou, a China export hub, lifted most lockdowns after the state TV said: “Areas that meet qualifications to lift lockdowns should ease ASAP.” The official Xinhua news agency and other government-run sites are running multiple stories and commentaries emphasizing epidemic controls must be applied with “softness” and “greater precision,” ensuring daily life and healthcare continue. There has been a marked change of tone from the previous military-themed rhetoric and analogies to battling the epidemic, with a greater focus on resuming as much normality as possible. Like other governments facing unrest, China is pursuing a mixed strategy by arresting protesters and intensifying street policing, while selectively relaxing epidemic controls to reduce their social and economic costs and keep the majority of the population in line.

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.53) is a Buy under $38 for a $66 target in 12 to 18 months.

KraneShares Bosera MSCI China A Share Fund (KBA – $31.12) is a Buy under $40 for a three- to five-year hold.

Morgan Stanley China A-Share Closed-End Fund (CAF – $13.94) is a Buy under $18 for a three- to five-year hold.

Primary Risk: China falls into a recession.

KraneShares CSI China Internet Exchange-Traded Fund (KWEB – $28.08) is a Buy under $40 for a double over the next three years.

Primary Risk of all four: China falls into a recession.

Acreage Holdings (ACRDF – $1.60) is certain to grow. According to a new survey conducted by Pew Research Center, only 12% of US adults think marijuana use should not be legal. 88% said cannabis should be legal for either medical or recreational purposes, and 59% said it should be legal for both.

After November’s latest batch of state referendums, recreational marijuana is now legal in 21 states and DC but remains illegal under federal law. As a result, current federal rules force even legal marijuana businesses to use cash instead of normal banking services. Legislators in Congress seeking to free state-legal cannabis businesses to use the country’s banking system have high hopes of finally pushing legislation across the finish line during the upcoming lame-duck session. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

Oil – $81.27

It’s only taken 204.3 million barrels from the Strategic Petroleum Reserve, rolling lockdowns in China, and record-low open interest to get oil down to

Refining margins have held up despite the crude sell-off, meaing this is not an end-user, demand-led sell-off. This is a very crude-centric problem. China hasn’t been buying. Russia is trying to sell as much as possible. The headline risks out of China caused computer algorithms to dump oil, hitting some stop-losses.

But sentiment got a big boost today from easing concerns over China’s zero-COVID unrest after Vice Premier Sun Chunlan, a top government official, urged an “optimization” of the nation’s virus response as pathogenicity weakens.

It was a huge week for the drawdown in crude storage. Crude was down by a truly staggering 12.58 million barrels, the largest weekly crude draw since June 2019 and over 5x the 2.49 million barrels expected. The crude draw was partially offset by rising product stocks (+2.77 million barrels of gasoline and +3.58 million barrels of distillates). Another 1.4 million barrels came from the Strategic Petroleum Reserve. Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $30.64) is a Buy under $36 for an $80+ target.

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

RIP Christine McVie

and

* * * * *

Your reading Doomberg on the SPR Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.67) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $1.02) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $10.22) – Buy under $20, hold a long time for a 10x return

Graphite Bio (GRPH – $3.43) – Buy under $9, hold a long time

Inovio (INO – $1.92) – Buy under $7, hold a long time

Invitae (NVTA – $2.97) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.58) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.12) – Buy under $3, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $8.02) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $148.31) – Buy under $150 for new iPhones

Corning (GLW – $34.24) – Buy under $33, target price $60

Gilead Sciences (GILD – $87.90) – Buy under $70, target price $100

Meta (META – $120.44) – Buy under $250, target price $400

SoftBank (SFTBY – $22.10) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $42.02) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $10.06) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.52) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $6.16) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.22) – Buy under $13, target price $30+

Velo3D (VLD – $2.04) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Buy while fixed mortgage rates are low

Bag of Junk Silver – ($22.92) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $25.47) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $31.10) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.60) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $29.49) – Buy under $30, target price $50

Coeur Mining (CDE – $3.50) – Buy under $5, target price $20

First Majestic Mining (AG – $9.51) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.38) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.47) – Buy under $10, target price $25

Sprott Inc. (SII – $36.58) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $ 16,960.37) – Buy

Grayscale Bitcoin Trust (GBTC – $8.89) – Buy

Ethereum (ETH-USD – $1,276.28) – Buy

Grayscale Ethereum Trust (ETHE – $6.78) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.53) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $31.12) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.94) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $28.08) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $1.60) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.12) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $30.64) – Buy under $36; $80+ target

Energy Fuels (UUUU – $6.75) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $1.86) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.29) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.04) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First!

Christine McVie – “Everywhere” a top 10.

She was a very good songwriter and singer. She will be missed.

i will take 3erd

MM is WAY OFF BASE on SCYX. I repost what I said at the end of the last board. All investors in SCYX should study what I wrote carefully.

SCYX–what a dumbass company, from the CEO MD who speaks broken English, to the scientific team doing trials. The recurrent VVC trial reported yesterday compares Brexa monthly to placebo. Brexa was only slightly better than placebo, at 65% reduced recurrence vs 53%, respectively. Why didn’t they study Brexa against the CHEAP standard of care, which is weekly single dose fluconazole (F). Here’s an article on F.

https://www.nejm.org/doi/full/10.1056/nejmoa033114

If the link doesn’t work, it is easily found by searching “fluconazole recurrent candida infection” or similar terms.

At 6 months, F reduced recurrence by 90%, much better than Brexa. Since F is much cheaper than Brexa, almost nobody is going to use Brexa for recurrent VVC. For acute VVC, Brexa had a comparable small margin of superiority to F, and yet the sales after a year were piss poor. Expect to see the same for recurrent VVC, so I doubt SCYX will find a partner for VVC uses.

Now I am worried that Brexa isn’t a wonder drug for serious hospital cases either. In that case, SCYX will go bankrupt in a few years. But if it is a far superior and safer drug than the current drugs for serious cases, SCYX has a chance as a highly speculative company with questionable or unknown potential. It deserves a low market cap at this early stage for serious cases. That’s why the stock plunged today.

Watch MM report the news as a positive and promote a back up the truck buy strategy. I will repost this on the new RR as a reality check for all to see.

0

Reply

JGMD

Reply to JGMD

December 1, 2022 7:48 pm

Instead of “reduced recurrence” I should have said “remained in remission” as reported in the article on F and the current news on Brexa for recurrent VVC. My points remain the same.

I was critical of the original trial for acute VVC. The scientific board is still thoughtless, and the new trial for recurrent VVC is equally mediocre and meaningless. I was correct that the sales for Brexa would be poor for acute VVC, and I will be proven correct again for recurrent VVC.

Also, MM said, “It (Brexa) is now the only FDA-approved therapy for both the treatment of vulvovaginal candidiasis and the reduction in the incidence of recurrent VVC.”

Incorrect. The NEJM article I linked shows better results with fluconazole (F) for both indications. In that article, the remission rate was worse for F at 9 months than for 6 months. Possibly the remission rate for Brexa would be worse at 9 months than it was at 6 months, possibly comparable to placebo, but this wasn’t studied. Another failure of the scientific board. Trials and dealing with the obstructionist FDA are both too expensive.

It is only prudent to invest in these risky speculative bio startups IF and only IF the scientific and marketing management is competent. SCYX has neither. Most of us are down about 90% from the original buy price on NWI. The stock was basing recently, and I considered adding at this much lower price. However, in the light of my reassessment, I will hold at best.

Thanks for your insight. However, I went against your opinion and bought some more last week after the FDA approval. I think women are desperate for something/anything that is approved by the FDA and will spend whatever to try it out. Not to mention, a better/smarter company could buy them out at this point and run with what they have. A lot of companies now have a war chest of money on their books getting beat up by inflation and more motivation to do something with it. Case in point, recent biotech buyouts. Just IMO

Sorry, you made a comparable mistake “bottom” fishing in ARTH at much higher prices than the current ARTH price. I just look at the ho-hum data, and compare it with the standard of care, fluconazole. The fact is that Brexa is a mediocre product, that a better marketing partner couldn’t do much better with. Such a partner could put prettier lipstick on this pig, but a pig is a pig. Inflation sucks, but it is better to sit on your cash than to squander it on crappy companies like SCYX. And, all the desperate women didn’t drive sales on Brexa for VVC.

Look at today’s stock dump, many times greater than the general market decline. No, this isn’t just tax loss selling. My real worry is that Brexa isn’t a great drug for C. auris, maybe no better than its activity against the common C. albicans of VVC. This company has been hyped up by ignorant financial analysts who are just promoters and wishful hopium characters.

Some women fail fluconazole treatment. Some strains of candida are azole-resistant. What is the alternative for these cases?

All true, but the sales numbers are poor. Overall, cheap fluconazole has a much better record than Brexa in published trials for VVC. The number of cases where Brexa cures the amole-resistant is small. Read the NEJM article I linked. There are others. But the latest recurrent VVC trial against placebo was a stupidly designed trial which will not sell Brexa. Placebo? So what!!! Why wasn’t a head to head trial against fluconazole done? Stupid management. Nobody is going to partner for VVC after that trial. A would-be partner will let SCYX run its finances into the ground. If the trial succeeds, the partner can pick up Brexa for VVC or the whole company in a fire sale just like the coming attractions for deadbeat ARTH or Algernon.

Brexa is DEAD for VVC as far as making money goes. C. auris human trials are beginning–how much data is there so far, just in vitro or animal trials?

Bearish YMB post by “Far” 20 hours ago on SCYX.

“Ceo leaving discontinued sales right before leaving doesn’t even have a conference call after their biggest indication is approved..now no sales no revenues no business partner..it’s becoming obvious they want this to end in bankruptcy and the insiders with their crony backers will then will

Probably come back buy the drug privately for Pennies…it all makes sense now..anyone remember the synergy scam face it folks small cap bios is pure theft.”

Never mind that Far may be a short seller with that motive. I don’t psychoanalyze financial manipulators. But my medical analysis fits with that post.

CLW: Can you think of a company with stellar products and position against any competitors – except it never got over about $44 and mostly sits down in the $30s. At least they did not drop in the $20s.

And the wonders of Bit Coin for those who got in at almost 4X the present quote. Just wait to a few visits by 88,000 IRS folks with guns come visiting..

I think people that have lost as much on Bitcoin as you say have nothing to worry about from the IRS.

Why are you people so worried about replacing 50k retiring agents and adding 30k more over the next 10 years?

Seems odd, unless of course …..

Quick Inlation Beater play for 4% in 10 days (and possibly more thereafter). Buy NAT at $3.55. You may have missed the December $0.05 dividend (went ex-div Monday and price turned downward after that. You can still sell the Dec 16 $3.50 call for .20, bringing your cost down to 3.35. If called away in ten days you get 3.50 for what cost you 3.35 and make 15 cents or 4% in just 10 days. Or maybe it doesn’t get called away and you can turn around and sell Jan calls against your stock. NAT will likely announce in February that a 10 cent dividend will be paid in March.

Get yourself out of GBTC as soon as possible. There’s a reason it’s selling at such a huge discount to BTC. Don’t ride this to zero.

https://www.coindesk.com/markets/2022/12/06/crypto-markets-today-fir-tree-suit-against-grayscale-adds-to-industrys-growing-woes/

“Fir Tree wants to use the information it’s seeking to pressure Grayscale to resume redemptions”

The discount would amortize instantly if GBTC did that. The reason GBTC sells at such a huge discount is fearmongering. In order for their bitcoin NOT to be there, the following would have to happen:

1. The signers of the SEC filings would have to not care that they certainly would go to jail.

SIGNATURES

Pursuant to the requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned in the capacities* indicated, thereunto duly authorized.

Grayscale Investments, LLCas Sponsor of Grayscale Bitcoin Trust (BTC)By: /s/ Michael Sonnenshein

Name: Michael Sonnenshein Member of the Board of Directors

and Chief Executive Officer

Title: (Principal Executive Officer)*By: /s/ Edward McGee

Name: Edward McGee Chief Financial Officer

Title: (Principal Financial Officer and Principal Accounting Officer)*

Date: November 4, 2022

*The Registrant is a trust and the persons are signing in their capacities as officers or directors of Grayscale Investments, LLC, the Sponsor of the Registrant.

2. Friedman LLP, the auditor of the 10-K, would have to be in on the fraud with partners ready to go to jail. In September, Marcum LLP acquired Friedman and would at least have had to miss the fraud in its due diligence.

3. The custodian, Coinbase Custody Services, would have to be willing to risk its entire business, lose its licenses, and again) have several officers ready to go to jail.

https://www.sec.gov/ix?doc=/Archives/edgar/data/1588489/000119312522053501/d289251d10k.htm (10-K)

“The Trust’s Digital Asset Account is a segregated custody account controlled and secured by the Custodian to store private keys, which allow for the transfer of ownership or control of the Trust’s Bitcoin, on the Trust’s behalf. Private key shards associated with the Trust’s Bitcoin are distributed geographically by the Custodian in secure vaults around the world, including in the United States. The locations of the secure vaults may change regularly and are kept confidential by the Custodian for security purposes. The Custodian requires written approval of the Trust prior to changing the location of the private key shards, and therefore the Trust’s Bitcoin, including to a different state. The Digital Asset Account uses offline storage, or cold storage, mechanisms to secure the Trust’s private keys. The term cold storage refers to a safeguarding method by which the private keys corresponding to digital assets are disconnected and/or deleted entirely from the internet.

Bitcoin in the Digital Asset Account are not treated as general assets of the Custodian. Rather, the Custodian serves as a fiduciary and custodian on the Trust’s behalf, and the Bitcoin in the Digital Asset Account are considered fiduciary assets that remain the Trust’s property at all times.

4. Oh, also – GBTC’s bitcoin is insured by an outside company.

Now, if you think all those companies and corporate officers are in on a massive fraud, you certainly should stay away from GBTC.

But if you think this is just Wall Street BS designed to separate the rubes from their money by buying GBTC in the open market and then pushing for redemptions at face value, buy GBTC.

Nobody saw Voyager, BlockFi, or FTX going BK. SBF thought he could get away with fraud but he is certainly going to jail.

Signers of SEC filings go to jail all the time. Fraud happens all the time. This thing is so disconnected from BTC at this point it has to raise eyebrows.

So far this Wall Street BS has driven this thing down 75%, it’s down 7% today while BTC is only down 1%.

Very sketchy to me. If you want to own BTC, buy it on an exchange and store it in your own personal cold wallet.

There is magic in the Webb:

https://as.cornell.edu/news/webb-telescope-shows-exoplanet-atmosphere-never-seen?utm_medium=email&utm_content=learnmore-link&utm_campaign=alumni-newsletter-december-2022&utm_source=alumni

The Radar Report for 12.8.22 is posted.