Dear New World Investor:

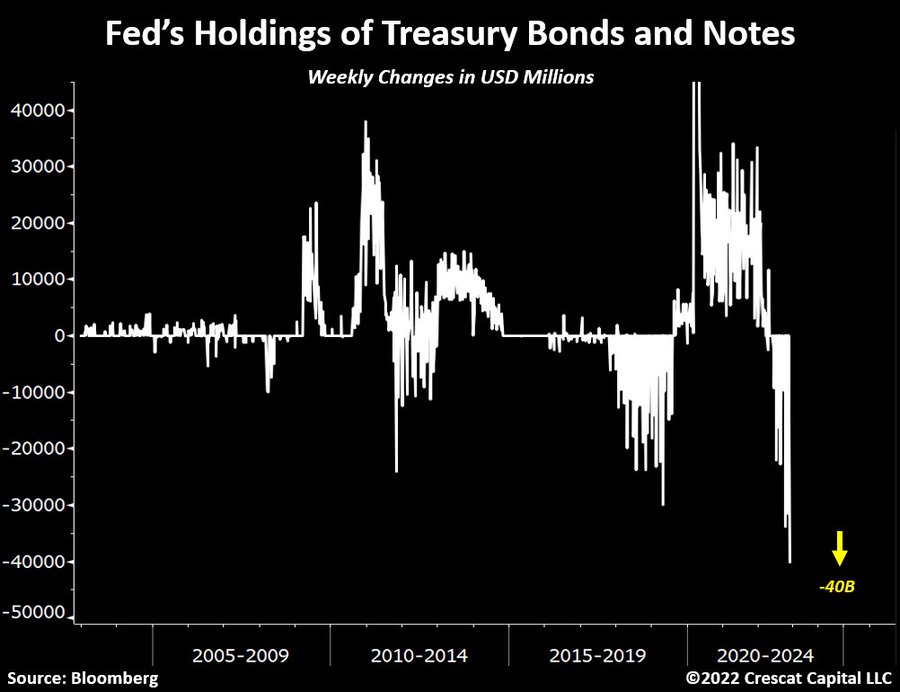

The latest Fed minutes, released today, said a “number of participants” said it would “become appropriate to slow the pace of increase in the target range for the federal funds rate.” That, I hope, comes as no surprise to you, as I’ve run this graphic for the last three weeks:

Click for larger graphic

Click for larger graphic

The Fed pivot never was going to be a sudden 180 degtees. The pivot is a process, not an event. Chairman Powell has been saying for months it will be data-driven – not inflation-driven, but data-driven. That means all the data.

Powell knows this inflation isn’t a wage-price spiral. It is a money-price-wage spiral.

Click for larger graphic

Click for larger graphic

To end it:

1) There is a monetary deceleration, then

2) Prices across the economy fall, then

3) Wages/core inflation fall

The Fed has to stay the course until they check all three boxes. Right now, they have checked #1 and #2. They are close to checking #3.

Click for larger graphic

Powell is deliberately raising rates and shrinking the Fed’s balance sheet in a recession, and he knows it. He wants to crush the inflation he financed, exacerbated by supply chain shortages that are now resolved or rapidly headed that way. But he does not want to cause a deep recession because he knows he doesn’t have to in order to achieve his objectives.

Already, the economic numbers mostly are pretty bad. September quarter GDP growth was inflated by oil sales from the Strategic Petroleum Reserve and the lower trade deficit due to the strong dollar lowering import prices.

Recently, the Kansas City Fed Manufacturing Index came in at -6 in November after -7 in October. The negative numbers mean contraction, and they said: “Manufacturing activity declined at a similar pace compared to last month.”

The Philadelphia Fed Manufacturing Index for November was expected to be -7, a slight improvement from October’s -8.7. Instead, it plunged to -19.4. They said: “The general activity index declined further, the new orders index remained negative, and the shipments index remained positive but low.”

Overall US industrial production, including manufacturing, mining, and utility output, fell 0.1% in October. That follows a downward September revision from +0.4% to +0.1%. The consensus expected a 0.2% gain in October.

Yesterday, S&P Global said its flash US Composite PMI Output Index, which tracks the manufacturing and services sectors, fell to 46.3 this month from a final reading of 48.2 in October. A reading below 50 indicates a contraction in the private sector. It was the fifth straight month of contraction and the worst number since 2009, with new orders dropping to the lowest level in 2 1/2 years as higher interest rates slowed demand.

This morning’s weekly jobless claims showed 240,000 new filings for unemployment insurance were made last week, the most since mid-August and well above the consensus for 225,000. The Conference Board’s leading indicators are flatlining:

Click for larger graphic

Click for larger graphic

The recession is accelerating, and Powell knows it. Headline inflation will stay high into 2023 due to oil prices and Powell knows it – so he is focused on the month-to-month change in core inflation, ex-food, and energy. The Fed can’t do anything to increase the supply of food or oil.

Meanwhile, hedge funds are still very bearish even after the ongoing short squeeze forced them to unwind short trades at one of the fastest paces in years. They are betting their careers that this is a bear market rally, with the lows ahead of us, most likely in the March quarter:

Click for larger graphic

Click for larger graphic

Maybe they’re right and will all keep their jobs…or maybe not. This is where individual investors have a huge advantage over Wall Street, because whether October 13 was the bottom or it lies ahead, stocks are cheap right now. No one is going to fire you for not buying the absolute low and three years from now it won’t matter whether you bought in October, November, December, January, February, or March.

JPMorgan said hedge funds have reversed all the risky exposures that they had taken on between late August and the end of September. Goldman Sachs data indicated hedge funds believe the recent equity bounce is nothing but a bear-market trap. This sets the stage for a Santa Claus rally into yearend.

Market Outlook

The S&P 500 added 2.0% since last Thursday in light trading. The Index is down 15.5% year-to-date. The Nasdaq Composite gained 1.3% and is down 27.9% for the year. The small-cap Russell 2000 also went up 1.3% and is down 17.0% in 2022.

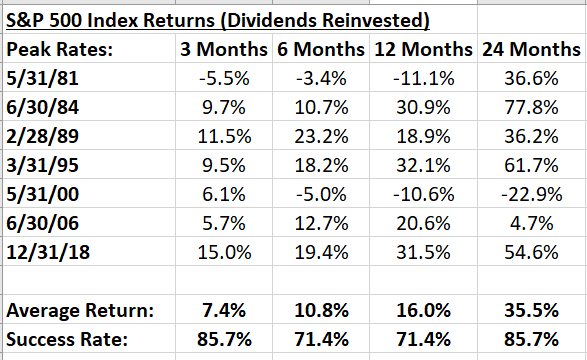

Fed policymakers have said they want to see a positive real Fed funds rate before pausing interest-rate hikes. That could happen as soon as the March quarter. Previous rate-hike cycle peaks have produced outsized S&P 500 Index returns.

Click for larger graphic

Click for larger graphic

The fractal dimension continues to consolidate to extreme levels. The bulls and bears are in a standoff. When it breaks, there will be a huge move. I still think it’s up as the Fed slows its increases, seasonality turns positive, and pension fund contributions hit at the end of the year.

Top 5

Changes this week: None

Near-Term – chronological order

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

INO Inovio – VGX-3100 HPV Phase 3 results by yearend

TGTX TG Therapeutics – FDA approval on December 28

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphite Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

This morning’s Atlanta Fed GDPNow model estimate for December quarter real GDP increased slightly to +4.3%. The Blue Chip consensus has not started increasing yet. It will.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Thursday, November 24

Markets Closed

Friday, November 25

Markets close early – 1:00pm

Short Interest – After the close

Tuesday, November 29

GLW – Corning – 8:15am – Credit Suisse Technology Conference

FSLY – Fastly – 10:55am – Credit Suisse Technology Conference

GLD – Gilead – 1:00pm – Evercore ISI HealthCONx Conference

AKBA – Akebia – 2:30pm – Piper Sandler Healthcare Conference

Wednesday, November 30

CDE – Coeur Mining – Unspec. – Bank of America Leveraged Finance Conference

CDE – Coeur Mining – Unspec. – Scotiabank Mining Conference

September quarter GDP – 8:30am – Second estimate

GLD – Gilead – 11:30am – Piper Sandler Healthcare Conference

SCYX – ScyNexis – Around 5:00pm – FDA decision

Thursday, December 1

Personal Consumption Expenditures Index – 8:30am

GRPH – Graphite Bio – 11:45am – Evercore ISI HealthCONx Conference

PD – PagerDuty – 5:00pm – Earnings conference call

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Meta Platforms (META – $112.24) is expanding ways people can find, message, and buy something from a business on WhatsApp. People in Brazil, Indonesia, Mexico, Colombia, and the UK can browse businesses on WhatsApp by category – such as travel or banking – or search by name to find them. They’re also testing secure payments right in a chat in Brazil with multiple payment partners.

A rumor went around that Mark Zuckerberg would retire in 2023 and the stock went up. I get it that people don’t like him, although I can’t think of many entrepreneurs that started a company in their dorm room and led it to over $100 billion in revenues. I also get that people don’t believe in the metaverse. In my career I’ve heard smart people say no one needs a personal computer, the iPhone would never be anything, and the Internet was a passing fancy.

Everything is going to be affected by the metaverse, and Zuckerberg plans to dominate it. I don’t think retirement is even in his vocabulary. META is a Buy under $150 for a $400 target in 2024.

Other Tech

Rocket Lab USA (RKLB – $4.40) said it has completed the final launch rehearsal and is ready for lift-off as early as December 7 for its first mission from US soil at their Launch Complex 2 in Virginia. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Velo3D (VLD – $2.18) got a nice write-up in Seeking Alpha: Velo3D: Proprietary PBF Technology Sets It Apart From Competitors. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

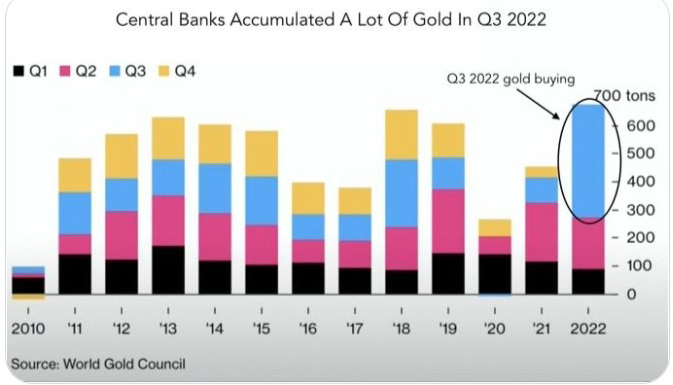

Gold ($1,754.70) has been around this price for two years, causing the most consolidated market I’ve ever seen. New all-time highs are a lock, it’s just a question of when.

The September quarter was a record quarter for central bank gold purchases. Go thou and do likewise.

Click for larger graphic

Click for larger graphic

Silver demand will hit record levels in 2022, driven by new highs for physical investment, industrial demand, jewelry, and silverware production, according to the Silver Institute’s Interim Silver Market Review. Global silver demand is projected to increase 16% from 2021 a new high of 1.21 billion ounces, in large part due to a near-doubling of Indian demand as it recovers from a slump last year.

Industrial demand makes up more than 60% of silver usage each year and is on track to set a new record of 539 million ounces in 2022. More and more silver is used to produce solar panels and in EVs.

Demand for silver jewelry production will increase by 29% to about 235 million ounces. Silverware fabrication will consume another 73 million ounces, a 72% increase.

Silver mine output will only increase by 1% in 2022. The 194 million ounce shortfall will be a multi-decade high and will likely come in at four times the deficit seen in 2021. Got silver?

Buy A Bag of Junk Silver ($21.64) for a hold until 2024-2025.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Global X Silver Miners Exchange-Traded Fund (SIL – $28.87) is a Buy up to $30 for a first target of $50 when silver gets back over $40. The silver miners should outperform both the large and junior gold miners in the next upleg for precious metals that will run until 2024-2025.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $9.62) is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying assets that offers a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $16,462.50) still is depressed from the FTX exchange collapse fraud

Click for larger graphic

Click for larger graphic

But CoinShares reported that institutional investor sentiment was “deeply negative” last week as short product inflows represented 75% of the total inflows—the largest inflow on record. These Johnny-come-latelys are piling on after bitcoin and ethereum already dropped and bottomed.

The collapse of FTX spread fears of contagion across the whole $830 billion industry, driving the discount to the net asset value of the Grayscale Bitcoin Trust (GBTC- $9.23) to a whopping 45%. Rumors spread that they did not actually own as much bitcoin as they claimed, or that they had lent it out, and there would be a “run on the bank.”

Those rumors are ridiculous. GBTC is a public entity reporting to the SEC, and the CEO and CFO would go to jail if they lied about their bitcoin holdings. Also, the $10.6 billion Trust generates about $200 million a year in management fees – would they really risk that?

And GBTC is a closed-end trust – there can’t be a run on the bank because investors can’t redeem shares. Last Friday, Coinbase Custody Trust Company, a subsidiary of crypto exchange Coinbase Global, testified to the security of Grayscale Investments’ digital assets products held at Coinbase Custody.

In a letter signed by Coinbase Chief Financial Officer Alesia Haas, Coinbase said the cryptocurrencies underlying each Grayscale product are segregated, in cold storage, and can’t be lent by Coinbase Custody. “We will never, directly or indirectly, lend, pledge, hypothecate or rehypothecate any of the digital assets underlying any Grayscale products,” Coinbase said in the letter.

GBTC is a Buy under net asset value.

BTC-USD, ETH-USD, GBTC and ETHE all are very Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $77.45

Oil was hit hard this week on fears that China’s zero-COVID lockdown policy will never end (it will, and soon) and rumors Saudi Arabia will increase oil production by 500,000 barrels a day in return for President Biden granting Saudi Crown Prince and Prime Minister Mohammed bin Salman Al Saud (MBS) immunity in a civil lawsuit filed by the former fiancée of Jamal Khashoggi who was murdered and dismembered inside the Saudi consulate in Istanbul in 2018. (Quid pro quo, anyone? They won’t, they already denied there was a deal.)

Crude oil prices fell today, even after the Energy Information Administration reported inventories of oil fell 3.7 million barrels over the week to November 18. This compared with a decline of 5.4 million barrels for the previous week. The EIA said that at 431.7 million barrels, US crude oil inventories were 5% below the five-year seasonal average.

Some have suggested that the OPEC+ two million barrel quota cuts that just started “didn’t work” because oil hasn’t spiked yet. This ignores the roughly six weeks lag time between the cuts and the data. OPEC+ meets on December 4 to set production plans for January. That’s just one day before the effective date of both the EU’s Russian oil embargo and the G7 oil price cap.

By mid-December, the EIA will show lower imports. Russian barrels also will drop over one million barrels. Demand is fine and prices are headed much higher. Russia said they won’t sell any oil to price-cap nations, a scenario which JPMorgan said could lead to $380 per barrel. Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $29.33) is a Buy under $36 for an $80+ target.

Energy Fuels (UUUU – $6.88) had two good articles on Seeking Alpha: Going Nuclear With Cameco And Energy Fuels and Energy Fuels: Alta Mesa Deal Should Help The Stock. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

* * * * *

Your using TIKR Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.67) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $1.02) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $10.48) – Buy under $20, hold a long time for a 10x return

Graphite Bio (GRPH – $3.50) – Buy under $9, hold a long time

Inovio (INO – $2.05) – Buy under $7, hold a long time

Invitae (NVTA – $2.82) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.43) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.45) – Buy under $3, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $8.17) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $151.07) – Buy under $150 for new iPhones

Corning (GLW – $33.92) – Buy under $33, target price $60

Gilead Sciences (GILD – $85.42) – Buy under $70, target price $100

Meta (META – $112.24) – Buy under $250, target price $400

SoftBank (SFTBY – $21.84) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $40.89) – Buy under $40; 3- to 5-year old

Fastly (FSLY – $8.59) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.00) – Buy under $30; 2- to 5-year old

QuickLogic (QUIK – $6.17) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.40) – Buy under $13, target price $30+

Velo3D (VLD – $2.18) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Buy while fixed mortgage rates are low

Bag of Junk Silver – ($21.64) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $24.62) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $29.22) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.08) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $28.87) – Buy under $30, target price $50

Coeur Mining (CDE – $3.41) – Buy under $5, target price $20

First Majestic Mining (AG – $9.62) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.36) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.40) – Buy under $10, target price $25

Sprott Inc. (SII – $37.04) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $16,462.50 ) – Buy

Grayscale Bitcoin Trust (GBTC – $9.23) – Buy

Ethereum (ETH-USD – $1,181.69) – Buy

Grayscale Ethereum Trust (ETHE – $6.89) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $27.34) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $29.61) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.17) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $25.10) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $1.43) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.15) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $29.33) – Buy under $36; $80+ target

Energy Fuels (UUUU – $6.88) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $2.00) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.26) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.04) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment advice or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Happy Thanksgiving

A Happy and Peaceful Thanksgiving to all!

Thank You Michael for the outlook on the market To everyone here Have a very grateful

THANKSGIVING TIME hopefully with friends and family.

Happy Thanksgiving, MM and all.

MM, just a gentle reminder that, more than a month ago, you told us that you were working on your top-10 list of “forgotten growth + value stocks” for putting cash to work in the current environment. As you pointed out in the current Radar Report, there’s no telling how soon the market might turn definitively positive. For those of us still holding some cash on the sidelines, your insights on this subject could prove valuable right now.

Read this. Why is there a third party Custodian for GBTC?

https://twitter.com/mikeburgersburg/status/1595398437549359108?s=61&t=GrvE–BxpfpwQwsV1SbjiA

You always want a third-party custodian to hold investors’ assets so they can’t be embezzled or misused.

Didn’t you say that you couldn’t understand why anyone would hold their BTC in an exchange? Doesn’t Grayscale hold their BTC in an exchange?

Am I misunderstanding?

A custodian is very different from an exchange.

Coinbase is an exchange. Now they may be serving as a custodian for GBTC but they are still an exchange.

They have a separate company, Coinbase Custody Services. When I ran mutual funds, all the assets were custodied at State Street. Goldman was our prime broker. Fund purchases and redemptions were all handled by State Street, Our trades through Goldman were all settled between Goldman and State Street.

The GBTC discount is a huge opportunity because all the assets are safe.

MM – you don’t have SCYX in your near-term movers despite a 11/30 PDUFA date for recurrent yeast infections. Is approval just a given and baked into the price?

11/30 approval matters little. Brexa for VVC is a money loser, so the best outcome is how much cash SCYX can get for VVC licensing to another party.

MM–You must address the real meat and potatoes here–approval for serious hospital infections. When would that occur? Before or after cash raising/dilution in 2024? Please respond to these concerns which are of interest to many subscribers, which I have asked many times without response from you.

11/30 approval is important to make Brexa an easily partnered asset. My guess is ~$50 million upfront and low double-digit royalties.

The Phase 3 trials for invasive candidiasis, refractory invasive fungal infections, and candida auris all end at the end of 2023, with FDA approval in the second half of 2024. They might raise money after they file in early 2024 but before approval unless a Brexa deal carries them through. That raise should be at a much higher price than current levels, as they’d have the Brexa deal done, three successful Phase 3s reported, and the IV formulation filing and approval coming in 2025.

Good, thanks. OK, when and if $59 million occurs, we can divide that by the number of fully diluted shares to figure the share price bump at that time. However, maybe the 11/30 approval is widely anticipated, and then there will be only a brief spike in the share price. This happened at the original approval with a steady decline in the share price until now.

I meant ~$50 million (typo, fixed). The real impact on the stock price will be the discounted current value of the expected royalties, which largely depends on who the partner is.

MM–how do you figure $50 million plus recurrent royalties for the VVC Brexa business? What are the recent sales revenue numbers? A good partner will have better marketing to increase sales for VVC. With $74 million present market cap, there would be a big increase in the stock price, but so far the market doesn’t care. Possibly the market doesn’t see a partner emerging for VVC.

Did they get FDA approval today?

SCYNEXIS Announces FDA Approval of Second Indication for BREXAFEMME® (ibrexafungerp tablets) for Reduction in Incidence of Recurrent Vulvovaginal Candidiasis :: SCYNEXIS, Inc. (SCYX)

Why is the stock down with approval ?

Thank you sir. I am assuming MM will have his take on the stock in the RR this week. Also Don B, wondering as well.

MM et al – seems like there is some serious doubt about SFTBY. The 1st article is from Kuppy’s group, so there should be some believability. Please comment, especially whether or not we should still be buying Softbank.

https://capitalistexploits.at/hold-my-beer/?utm_source=email&utm_medium=Social&utm_campaign=sitebuttons

https://on.ft.com/3OuVKX8

Happy Thanksgiving to all

That article is from 2019. Softbank’s value comes from its holdings in publicly traded subsidiaries. The Vision Fund is the frosting on the cake. I think it will be very successful over the next five years.

Most of the debt is held by the operating companies and is nonrecourse to the Softbank parent.

TY. My bad. I didn’t notice that Kuppy’s article was from 2019, as it came in a current email. Not sure why he’s sending it now. I hope you’re right about the nonrecourse debt.

Happy Thanksgiving! ! !

MM and Board anyone Following Kintara Therapeutics?

There Cancer Drug just got fast tract thinking about

Starting a position any insights? ((-:

Donald Galamaga,

I hope you are well. Miss your wisdom.

MM, I had put this on the previous 2 message boards. Please share the thoughts. Thanks!!

MM, as I write this Medicenna is at a 52 week low of .46. Ever since they did that horrible offering back in August, it’s been in a free fall, even with the good news of MDNA11. Thoughts?

This might explain some of the weakness in the last few weeks. This company is discontinuing their IL-2 Development.

Neoleukin Therapeutics Announces Third Quarter 2022 Financial Results and Corporate UpdateNovember 14, 2022

PDF Version

— Development of NL-201 to be discontinued for strategic reasons —

— Company to focus on next-generation de novo proteins and core technology —

— Company restructuring to extend cash runway into the second half of 2025 —

SEATTLE, Nov. 14, 2022 (GLOBE NEWSWIRE) — Neoleukin Therapeutics, Inc., “Neoleukin” (NASDAQ:NLTX), a biopharmaceutical company utilizing sophisticated computational methods to design de novo protein therapeutics, today announced financial results for the third quarter ended September 30, 2022 as well as a strategic decision to discontinue development of NL-201, a fully de novo IL-2/IL-15 agonist, and focus on advancing next-generation de novo protein therapeutics based on Neoleukin’s expertise in designing and testing novel cytokine mimetics and experience with advanced machine learning.

“We will be using the information we have learned from the development of NL-201 and advances in protein design to build the next generation of de novo protein therapeutics,” said Jonathan Drachman, M.D., Chief Executive Officer at Neoleukin. “We expect to focus on technology that widens the therapeutic window, such as the development of targeted and conditionally activated molecules to create potent immune agonists. We believe we are well positioned to do this work based on our expertise in de novo protein design combined with our experience in advanced machine learning and neural networks, which allows us to predict and create structures for de novo proteins with more sophisticated and dynamic structural elements than was previously possible.”

“This coincides with a strategic decision to discontinue development of NL-201, which we believe was the first fully de novo protein to be evaluated in clinical trials,” said Dr. Drachman. “We are grateful to the patients and families that participated in this Phase 1 trial and to the investigators and study personnel who enabled rapid testing of NL-201 during a global pandemic.”

Discontinuation of NL-201 Development

Neoleukin announced today that it is discontinuing development of NL-201, its first de novo cytokine mimetic to be tested in patients. Preliminary monotherapy data from the Phase 1 study of NL-201 demonstrated engagement of the target receptor, expected pharmacodynamic changes for a potent IL-2/IL-15 agonist, and did not demonstrate significant immunogenicity even after multiple cycles of therapy—an important de-risking of the potential for de novo proteins that may be administered over many weeks and months. However, based on a review of the preliminary data, the expected benefit to risk ratio for patients, and recent developments in the field of IL-2 therapeutics, Neoleukin determined that the resources required to continue development would be better applied to advancing the next generation of de novo protein therapeutics.

They really need to partner MDNA55. Otherwise, it’s just the bear market hitting development-stage companies especially hard. Tax loss selling could be next, although many of these are going to run out of sellers.

They have been saying that they are close to partnering MDNA55 for the last 2 years!! If the PH3 results were so good, why are they having such a hard time finding someone?

I’m also curious about your thoughts about the Neoleukin news? I guess you could look at it as good and bad. It’s 1 less competitor, but it also shows how hard it is to be successful in the IL-2 space.

The lack of a partner is very frustrating. I don’t know what the problem is, but there obviously is one.

The Neoleukin failure is good news because MDNA has an IL-2 replacement that clearly works with much, much lower side effects. My friend who died of liver cancer at 42 was one of the first IL-2 patients. Ran a temperature of 107.50 for a while.

Sorry for your friend with liver cancer. Cancer is a disorder of the immune system. Unless root causes of cancer are addressed, such as infections, bad lifestyle habits like smoking, alcohol and obesity, the prognosis in the majority of patients is grim. It is folly to think that an isolated super-duper manmade cytokine analog will do much to overcome the jungle of stresses on the immune system that caused his cancer. There are 100’s, 1000’s of cytokines involved in immune disorders, and addressing any isolated single one like IL-2 is doomed to failure.

A simple example of the nearly useless benefits of drugs–high triglycerides with high trig/HDL ratio is caused by eating too much carbs. The drugs used to lower trig show at best a 50% reduction. That’s yields minimal benefit. But a strict low carb or even keto diet to become slender will reduce trig and trig/HDL by 95% to become normal. Huge benefits, no side effects of drugs.

MM, you referenced below about BLPH raising money soon. With the price currently trading at $1.12, the SP would be decimated if they did it any time soon. You previously mentioned that they would probably raise money once they announce the trial being fully enrolled.

At the end of September they had $11.3 million in cash, and I still expect them to raise money soon.

The full enrollment announcement should come in January or February. They burn about $5 million a quarter in cash and no one wants to get below six months of cash for long. They could do a convertible offering that wouldn’t hit the stock much.

The latest presentation is really good

https://investors.bellerophon.com/static-files/d2ffa433-af84-44d5-9402-00f75ed68d43

SCYX–what a dumbass company, from the CEO MD who speaks broken English, to the scientific team doing trials. The recurrent VVC trial reported yesterday compares Brexa monthly to placebo. Brexa was only slightly better than placebo, at 65% reduced recurrence vs 53%, respectively. Why didn’t they study Brexa against the CHEAP standard of care, which is weekly single dose fluconazole (F). Here’s an article on F.

https://www.nejm.org/doi/full/10.1056/nejmoa033114

At 6 months, F reduced recurrence by 90%, much better than Brexa. Since F is much cheaper than Brexa, almost nobody is going to use Brexa for recurrent VVC. For acute VVC, Brexa had a comparable small margin of superiority to F, and yet the sales after a year were piss poor. Expect to see the same for recurrent VVC, so I doubt SCYX will find a partner for VVC uses.

Now I am worried that Brexa isn’t a wonder drug for serious hospital cases either. In that case, SCYX will go bankrupt in a few years. But if it is a far superior and safer drug than the current drugs for serious cases, SCYX has a chance as a highly speculative company with questionable or unknown potential. It deserves a low market cap at this early stage for serious cases. That’s why the stock plunged today.

Watch MM report the news as a positive and promote a back up the truck buy strategy. I will repost this on the new RR as a reality check for all to see.

Instead of “reduced recurrence” I should have said “remained in remission” as reported in the article on F and the current news on Brexa for recurrent VVC. My points remain the same.

The new Radar Report for 12.1.22 is posted.