Dear New World Investor:

My annual holiday vacation is next week, so the next Radar Report will be on January 5. I may post a Flash Alert after the December 28 FDA decision on TG Therapeutics’ drug to treat multiple sclerosis. We end this annus horribilis with one of the best investment opportunities I’ve ever seen.

Toby, Derek, and Daniel Rice IV, three brothers from Pittsburgh, started Rice Energy in 2009 to acquire, explore, and develop natural gas and oil properties in the Appalachian Basin. Their strategy was to be an early entrant into the core of a shale play by identifying the core of the play and aggressively executing their acquisition strategy to establish a largely contiguous acreage position. They were an early identifier of the core of both the Marcellus Shale in southwestern Pennsylvania and the Utica Shale in southeastern Ohio.

They started as conventional frackers, completing their first horizontal well in October 2010, but then developed the technology to drill exceptionally long wells, which reduced their cost per foot while increasing production per well. Their average net daily production, measured in million cubic feet per day (Mmcf/d), grew rapidly:

Average Net Daily Production (MMcf/d)

Click for larger graphic

Click for larger graphic

They went public in January 2014. In November 2017 they sold the company to EQT Inc., a badly-managed natural gas behemoth, for 7,782,819 million shares of stock, or 3.1% of EQT. Rice Energy CEO Daniel Rice IV went on the board. The merger made EQT one of the largest natural gas companies in the US, and the plan was to use Rice’s long horizontal well technology to cut EQT’s costs while boosting production. In the joint proxy statement, the first listed benefit of combining Rice Energy with EQT was that the “substantial contiguity in the acreage footprints should allow for a significant increase in the average lateral lengths of future Marcellus wells of the combined company, thereby significantly reducing well costs on a per horizontal foot basis and increasing the present value of development.”

When the merger was announced, EQT said $1.9 billion of its projected base synergy cost savings of $2.5 billion would be attributable to capital efficiencies resulting from reduced well costs. Following the announcement of the merger, Rice Energy’s leadership team spent five months with EQT’s management team laying out the blueprint that led to Rice Energy’s operational success. Alas, after the merger closed, EQT ignored what the two companies had spent months discussing and decided to move forward with its own existing internal systems, and without the critical personnel responsible for Rice Energy’s success.

Following EQT’s disastrous 2018 operational performance, the Rice brothers staged a successful proxy fight and took over the company in July 2019. The improvement was immediate. In about a year, they transformed it into America’s leading producer of natural gas via massive increases in drilling efficiency and huge, very attractive acquisitions.

Click for larger graphic

Click for larger graphic

Over the last five years, EQT’s proven reserve base has almost doubled to 23 trillion cubic feet while its capital spending has fallen 50% from around $2 billion to around $1 billion. Plus, they are sitting on a lot more gas that hasn’t been developed yet. They have over a million acres of land in the Marcellus that remains undeveloped, double their 500,000 developed acres.

To expand even further, EQT has offered $5.2 billion, half in cash and half in stock, for Tug Hill and its associated pipeline infrastructure. The deal is under review by the Federal Trade Commission. Tug Hill is a privately held, mid-sized producer in the Marcellus whose assets and pipelines are adjacent to EQT’s.

EQT gets 800 million cubic feet a day of additional production from 300 drilling locations – a 15% increase from their current daily production of 5.5 billion cubic feet per day (BCF/D) to about 6.3 BCF/D, nearly 20% of the total dry gas output in the Appalachian Basin. Tug Hill also owns 100,000 acres in the core of the Marcellus basin. This acreage has enough proven reserves to provide 11 years of continuous production with only maintenance-level amounts of capital spending.

EQT also gets 95 miles of pipeline gathering systems, which will allow them to reduce their capital spending for gathering systems by 75%. And they are only paying 2.3x next 12 months’ estimated operating profits. The acquisition reduces EQT’s production cost basis by 15¢ per million British Thermal Units, which both increases its profit margins and drives down its breakeven price of gas.

Why would Tug Hill sell out? They said: “EQT is the face of the new energy paradigm. Toby Rice’s vision around US LNG is something we believe in and because of our significant ownership position, are excited to be a part of that vision.”

EQT doubled their share buyback forecast to $2 billion and their debt repayment through 2023 increased to $4 billion. Most important, the Tug Hill acquisition increases their cash flow per share by 10% and their long-term free cash flow forecast to $5 billion a year. This for a company with less than a $14 billion market capitalization today!

After the deal closes early next year, in 15 years three brothers from Pittsburgh will have built America’s largest producer of a super-clean, carbon-based energy source – natural gas. They’ll have the gas and the pipelines. Next, they’ll build, buy, or invest in a liquefied natural gas facility to ship LNG to Europe at 4x to 10x times the US price. That deal will create the first new energy major to emerge from America’s shale resources, which are among the largest ever discovered. The resource is so big and EQT is growing production so much that it could become the world’s largest and most important energy company over the next 10 years.

The Rice brothers believe the future of the world’s economy depends on unleashing US-sourced natural gas. Their plan is to lead the US to produce an additional 50 billion cubic feet (BCF) of natural gas a day, enough to power the world. Recently, Toby Rice, now the CEO of EQT, said: “The Marcellus as a whole has more gas reserves than Russia. So it’s an absolute powerhouse…this is like the Saudi Arabia of energy…With a $3.75 gas price, the Marcellus shale has the opportunity to increase natural gas production an incremental 35 BCF a day and be able to do that over a 10-year period of time and hold that ball, hold those lines flat for over 30 years. The biggest gas field in the world can be the biggest gas field in the world two times over. And the only thing that needs to make that happen is pipelines. And then also the LNG facilities to create the demand for incremental volumes.”

Valuation

EQT raised its free cash flow estimate for 2022 by 50% to $2.35 billion. With the Tug Hill acquisition, higher natty prices, and more drilling they will be at $5 billion a year soon. Free cash flow of $5 billion annually with a proven growth strategy should be worth at least 12x or $60 billion. EQT’s current market capitalization is only $12.9 billion. Higher natural gas prices are inevitable as more and more of the world’s electrical generation switches from coal to natural gas, which gives EQT even more upside. As you know, Russia has officially halted all natural gas exports to Europe – 40% of EU natural gas supply is now offline indefinitely. As Goldman Sachs wrote: “In our view, the market continues to underestimate the depth, the breadth and the structural repercussions of the crisis…We believe these will be even deeper than the 1970s oil crisis.”

EQT is a unique situation, a once-in-a-generation kind of business that can grow production for the next 30 years without having to acquire any additional resources. The growing backlash against ESG trends will most likely keep pressuring oil and coal but embrace natural gas in the near term and Gen IV nuclear in the long term. If a third of the cars on the road by 2030 are electric – which I strongly doubt due to the expense and unavailability of rare earth metals – the electricity to charge them has to come from base load power. Unless we want to follow Europe and China in building coal-fired power plants, that means natural gas. It is the most logical bridge fuel to get us to a greener future over the next 20 years.

The consensus of 15 analysts’ earnings estimates for 2023 is $9.80 a share, in a wide range from $7.03 to $12.54. The stock is priced at only 5.0x the lowest estimate and 3.6x the consensus. EQT is cheap but this is a bet that natural gas prices at least won’t fall dramatically. I expect them to increase substantially.

Here’s how EQT’s stock price has matched the ups and downs of natural gas prices over the past six months, using the standard Henry Hub price:

Click for larger graphic

Click for larger graphic

The energy sector as a whole performed well this year, and EQT is well positioned to take advantage of the long-term trend to much higher prices. They have a solid management team, a healthy balance sheet, and a clear strategy for growth, which should continue to drive shareholder value. Buy EGT under $35 for a first target of $70 and a long-term hold for much higher prices. I am adding EQT to the list of Top Long-Term Recommendations.

Click for larger graphic

Click for larger graphic

Market Outlook

The S&P 500 lost 1.9% since last Thursday, mostly due to today’s drop on the “terrible” news that September quarter real GDP was revised up from +2.9% to +3.2%. The Index is down 17.7% year-to-date. The Nasdaq Composite lost 3.1% and is down 33.0% for the year. The small-cap Russell 2000 won the week, dropping 1.2% to finish down 21.9% in 2022.

Tomorrow morning, the Commerce Department will release the Personal Consumption Expenditures price index for November. The year-over-year PCE inflation rate should cool to about 5.5% from October’s 6.0%, with the month-over-month index up 0.2% versus October. The annual core PCE is expected to slow to 4.6% from 5%, with month-over-month core prices also up 0.2%.

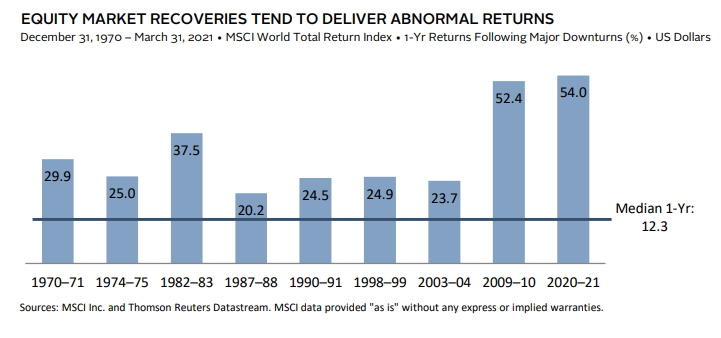

The fractal dimension continues to consolidate in this one-for-the-record-books bull/bear war. The next move is going to be wild.

After the market puts in a long-term bottom, the returns from that ultimate low should be quite impressive if they are like other periods of recovery.

Click for larger graphic

Click for larger graphic

Top 6

Changes this week: Added EQT to Long-Term

Near-Term – chronological order

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

INO Inovio – VGX-3100 HPV Phase 3 results by yearend

TGTX TG Therapeutics – FDA approval on December 28

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphite Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

EQT EQT – largest US natural gas company

Economy

The Philadelphia Fed just revised jobs lower by 1.2 Million (!) for the June quarter. In the aggregate, only 10,500 net new jobs were added during the period rather than the 1,121,500 jobs estimated by the sum of the states. The Bureau of Labor Statistics’ Current Employment Survey estimated net growth of 1,047,000 jobs for the period. The monthly survey covers 5.7% of all employers while the Philly Fed’s revisions are based on 95% of all employers. Payroll jobs actually remained essentially flat from March through June 2022.

The Current Employment Survey we know as the monthly jobs report is timely, but it’s often inaccurate, substantially revised later, and grossly inaccurate at economic turns. Yet the Fed makes decisions based on the monthly data even when the Household Survey shows major discrepancies. As I’ve always said, the Household Survey is more likely to be accurate at the turns.

For months on end, the Fed has been saying: “Jobs are too strong for there to be a recession,” despite knowing that jobs are a lagging indicator, and despite the Household Survey differing sharply. As Gary Friedman, CEO of Restoration Hardware (RH) said: “People keep saying, are we going to be in a recession? We’re in a recession. Anybody who thinks we’re not in a recession is crazy.”

Over to you, Chairman Powell.

The Atlanta Fed’s GDPNow model forecast for December quarter GDP dipped another 0.1 percentage point to +2.7% after the low housing starts report.

Click for larger graphic

Click for larger graphic

There is now a record divergence between “hard” and “soft” economic data. Using the St. Louis Fed methodology:

– Hard Data Economic Index = +1.6 (+.6 on average at a recession’s start)

– Soft Data Economic Index = -2.5 (-.6 on average at a recession’s start)

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, December 23

Personal Consumption Expenditures Index – 8:30am – see above for expectations

Sunday, December 25

Monday, December 26

Markets closed

Tuesday, December 27

Short Interest – After the close

Wednesday, December 28

TGTX – TG Therapeutics – After the close -PDUFA date for MS approval

Thursday, December 29

NO RADAR REPORT THIS WEEK!

Sunday, January 1

Happy New Year! Let’s Make It A GREAT One!

Monday, January 2

Markets closed

Thursday, January 5

Next Radar Report

Friday, January 6

December payrolls – 8:30am – +57,000 expected; November was +263,000

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations are typically very low. At the same time, Initial Public Offering valuations had moved very high. We were seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors make 5x to 10x in a reasonable, three- to four-year period if they buy at those valuations. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Invitae (NVTA – $1.90) sold some non-core assets to Integrated DNA Technologies for $48 million. Wall Street wants to see them focus, cut costs, and conserve cash. This does all three. It’s only a question of time until the Street flips from glass-half-empty to glass-half-full and moves the stock up. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

Biotech MegaShift

Akebia Therapeutics (AKBA- $0.41) met with the FDA in November to discuss their appeal of the complete response letter they got in March for vadadustat. Subsequently, they received a request for additional clarifying information from the Office of New Drugs, Center for Drug Evaluation and Research, which will decide the appeal. Akebia will submit the requested information in January and expects to receive a response 30 days later. AKBA is a Hold for the results of the FDA meeting on vadadustat.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Vadadustat NDA filed

Probable time of next FDA approval: Unknown

Probable time of next financing: Unknown

TG Therapeutics (TGTX – $8.58) has a December 28 PDUFA date for FDA approval of ublituximab for multiple sclerosis. It could hit $1 billion in annual sales – a blockbuster drug – by the end of 2024. Buy TGTX under $7 for a target price in a buyout of $25 or more after the MS drug is approved.

Primary Risk: FDA turns the MS drug down.

Clinical stage of lead product: Filed for approval.

Probable time of next FDA approval: September 28, 2022

Probable time of next financing: March 2023 quarter

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $132.23) will broadcast every Major League Soccer game in the 2023 season on the Apple TV app, starting February 1 for holders of the MLS Season Pass. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $85.28) got FDA approval for Sunlenca as a first-in-class, twice-yearly treatment option for people living with multi-drug resistant HIV. GILD is a Long-Term Buy under $70 for a first target of $100.

Meta Platforms (META – $117.12) reviewed their progress in augmented reality (AR) and virtual reality (VR) in 2022. The Meta Quest Pro’s most innovative features are its mixed reality capabilities (Meta Reality) and its advanced optical system (Infinite Display).

I have no doubt that Meta will be a (maybe the) leader in the virtual reality metaverse IF CEO Mark Zuckerberg ignores the naysayers and short-term thinkers that don’t get it. The metaverse will be as big a change as the Internet. It will change everything: business, education, entertainment, travel – you name it.

The FTC is suing Meta to stop its acquisition of Within Unlimited and their virtual reality fitness app. Zuckerberg testified that Meta is helping to build the nascent virtual reality industry, not dominate it.

He said that owning Within Unlimited is “not that critical” to Meta’s ambitions, because they primarily aim to build communications tools and a platform for apps from different developers.

Zuckerberg said: “It’s less important that we own the experiences than that they exist.” He said he wants to see other firms build key productivity and gaming apps to draw a mass audience to virtual and augmented reality.

FTC lawyers kicked off the proceedings by asking Zuck about an internal email he wrote in 2015 where he said he expected Meta to build “most of the apps and software services” for the VR industry. Zuckerberg replied that major platform owners tend to build the most popular apps in their area of expertise, likening Meta’s emphasis on communications to Microsoft’s focus on productivity. Platform companies have built “the key apps, what they call the killer apps,” Zuckerberg said, “but they’re not the only apps available.”

Senator Marco Rubio(R), Representative Raja Krishnamoorthi(D), and Representative Mike Gallagher(R) introduced bipartisan legislation in the Senate and House to ban TikTok in the US. Nobody is against banning TikTok, so maybe it will happen. If so, Meta and YouTube Shorts will be big beneficiaries.

JPMorgan just raised their rating to overweight, raised their target to $150, and wrote: “Heading into 2023, we believe some of these top and bottom line pressures will ease, and most importantly, Meta is showing encouraging signs of increasing cost discipline, we believe with more to come.”

He added that Meta shares have bounced more than 30% off their lows as the company has taken initiatives to cut costs, both in terms of headcount and spending, and there is likely more to come: “We believe Meta is building the muscle for more sustainable financial discipline that can help drive further upward earnings revisions, and we believe the risk-reward is attractive at current levels.”

META is a Buy under $150 for a $400 target in 2024.

Other Tech

Fastly (FSLY – $8.11) is trading for just 2x next year’s revenue and growing 25% a year. Opportunities don’t get much better than that. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $3.73) had to push their first Virginia launch into January due to persistent strong upper-level winds. As a result, they reduced their December quarter revenue guidance from a range of $51 million to $54 million to $46 million – $47 million. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,801.50) dropped today on the higher September quarter real GDP estimate, which boosted the dollar and might pressure the Federal Reserve to raise interest rates faster or further.

But it found solid support at $1,800 and may be starting to reflect Eric Sprott’s year-end wrap-up: “Big, Big, Big Things Happening in Gold and Silver.”

Miners & Related

First Majestic (AG – $8.74) closed the sale of its royalty interests to Metalla Royalty & Streaming for $20 million in MTA stock. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $16,813.41) is holding well as the FTX drama plays out.

Click for larger graphic

Click for larger graphic

It’s pretty clear that Alameda Research co-CEO Caroline Ellison and FTX co-founder Gary Wang have flipped on Sam Bankman-Fried. They both pled guilty to federal charges in the Southern District of New York and are cooperating with authorities. Meanwhile, SBF is “nearly broke” with only $100,000 in the bank, but he somehow posted a $250 million bail bond.

I don’t think he’ll plead guilty. He’ll go to trial and this will drag on for years. But that’s good for bitcoin and ethereum, because the message to investors is “don’t buy ishtcoins, buy the best” and the message to regulators is “get off your butts and put a structure in place.”

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys. The best way to buy bitcoin remains the Grayscale Bitcoin Trust (GBTC- $8.14), a Strong Buy at a 47.0% discount to net asset value.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $78.33

Oil rose after the Energy Information Administration reported a 5.9 million barrel drop in US crude inventories in the week ended December 16, in spite of another 3.7 million barrel draw from the Strategic Petroleum Reserve. Industry analysts blamed the drop on strong exports, as well as a drop in imports due to the Keystone pipeline outage. There’s a once-in-a-generation winter storm barreling across the US this weekend, bringing more than a foot of snow, possible blizzards, and whiteout conditions. The Denver weather service said: “This event could be life-threatening if you are stranded with wind chills in the 300 below to 450 below zero range.” Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $29.40) is a Buy under $36 for an $80+ target.

Energy Fuels (UUUU – $6.11) sold $18.5 million of uranium to the US National Nuclear Security Administration to establish a Strategic Uranium Reserve.

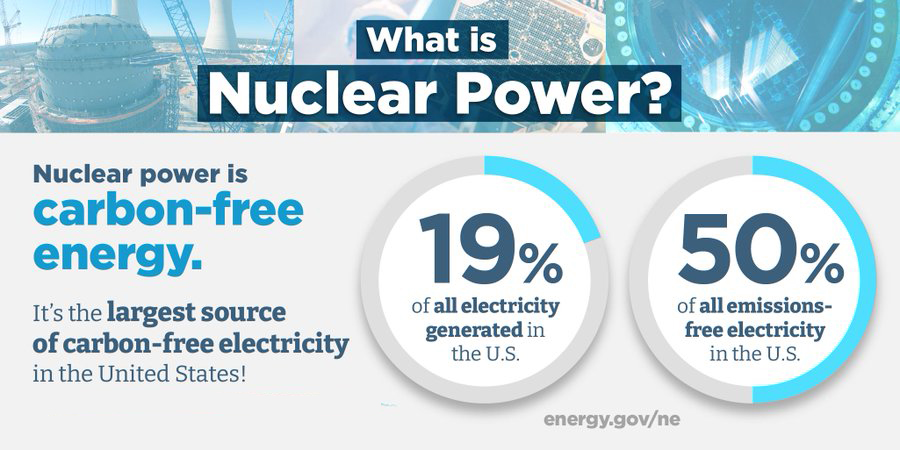

Nuclear energy is the largest source of carbon-free electricity in the US.

Click for larger graphic

Click for larger graphic

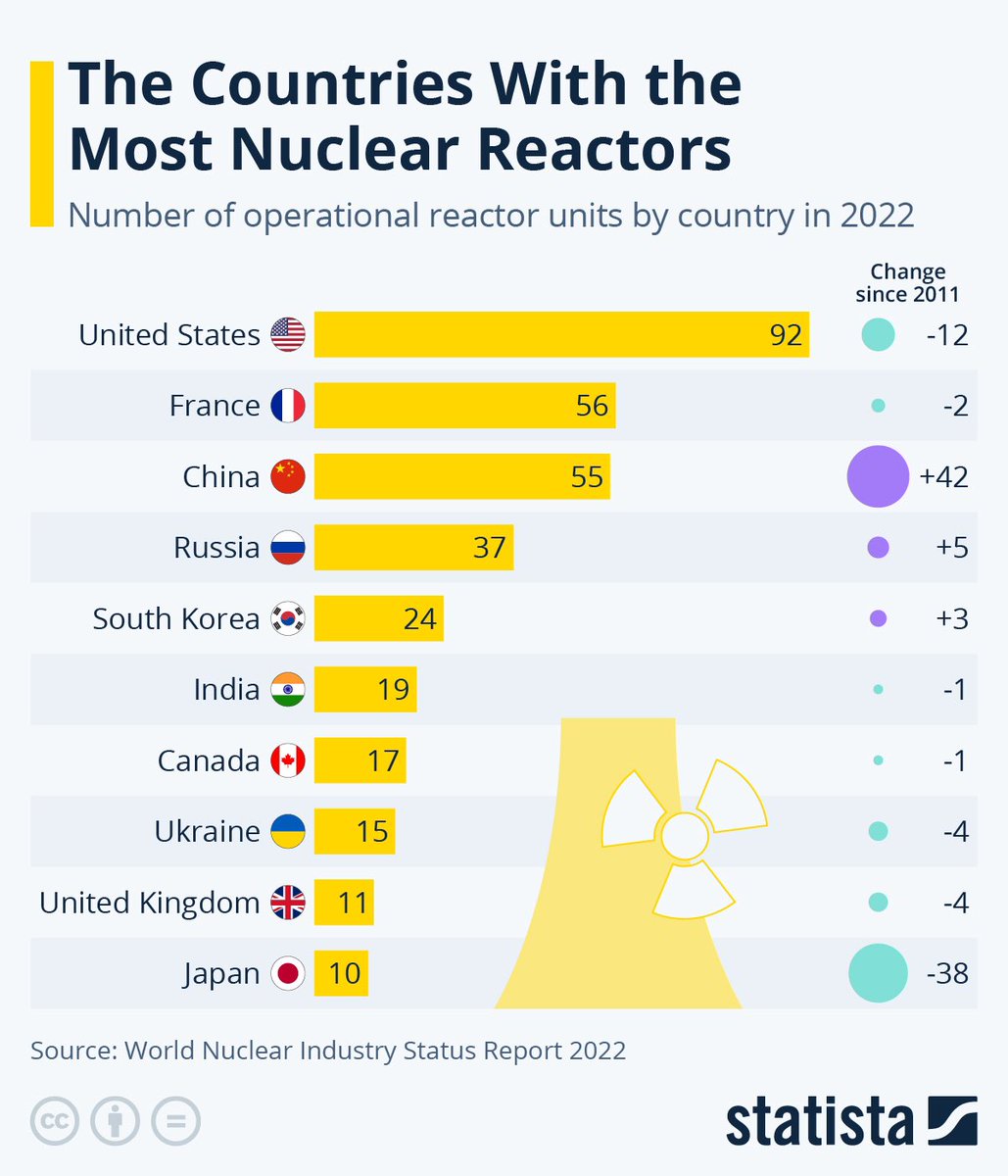

The US leads the world with 92 nuclear reactors. However, while we’ve been (wrongly) shutting down nuclear, China has built a whopping 42 nuclear plants since 2011. America must not lose its nuclear energy advantage.

Click for larger graphic

Click for larger graphic

In a dramatic 1800, Japan said it will adopt a new policy to “maximize the use of existing nuclear reactors” by accelerating restarts in a reversal of their post-Fukushima plan to phase out the use of nuclear power plants. Japan sourced about a third of its energy from 54 nuclear reactors before the Fukushima disaster. Now, only nine are operational, forcing the country to burn additional coal, natural gas, and fuel oil despite pledges to achieve net zero carbon emissions by 2050.

It also will extend the lifespan of nuclear reactors beyond 60 years and develop advanced – presumably Gen IV – reactors to replace those that are decommissioned. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

BofA Describes 2022 in 22 Numbers

9.1% – US CPI hit a 40-year high

45.8% – German PPI hit a 100-year high

2 – number of Fed rate hikes forecast for 2022 in the BofA Global FMS in December 2021

284 – number of central bank rate hikes YTD in 2022

5.4x – ratio of US private sector financial assets to GDP (vs peak of 6.2x)

1969 – US unemployment rate fell to 3.5%, lowest since 1969

34% – record YoY rise in Miami house prices YoY in May’22

-35% – return from the 30-year US Treasury bond worst in over a century

<$1T - cryptocurrency crash took crypto market market cap from $3T to <$1T 2 - commodities were best performing asset class for 2nd consecutive year 90% - rise in natural gas prices, best performing commodity of ‘22 382 million barrels - US strategic petroleum reserve slashed to lowest since 1984 €750 billion - fiscal policy stimulus in Europe & UK to offset war 47% - rise in Chevron, best performing stock in Dow Jones -49% - collapse in Salesforce, worst performing stock in Dow Jones $3.6 trillion - market cap slump in FAAMG (Facebook, Apple, Amazon, Microsoft, Google) $33T - global equity market cap slump from November 2021 high -50% - decline in private equity stocks from November 2021 high 2009 - Hang Seng Index fell to its lowest level since 2009 33% - yield on China HY bonds rose to staggering 33% (spreads>3000bps)

-16% – Japanese yen was worst performing major currency

76% – best performing equity market in US$-terms was Turkey

* * * * *

Exchange-Traded Funds

You want the:

* * S&P 500? Buy VOO

* * Entire Stock Market? Buy VTI

* * Real Estate? Buy VNQ

* * Technology? Buy VGT

* * Dividend Appreciation? Buy VIG

* * Total World Stock? Buy VT

* * Growth? Buy VUG

* * High Dividend Yield? Buy VYM

* * * * *

Your reading Mandelbrot’s 10 Heresies of Finance Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.46) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $0.85) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $8.93) – Buy under $20, hold a long time for a 10x return

Graphite Bio (GRPH – $2.85) – Buy under $9, hold a long time

Inovio (INO – $1.60) – Buy under $7, hold a long time

Invitae (NVTA – $1.90) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.43) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.60) – Buy under $3, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $8.58) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $132.23) – Buy under $150 for new iPhones

Corning (GLW – $31.57) – Buy under $33, target price $60

Gilead Sciences (GILD – $85.28) – Buy under $70, target price $100

Meta (META – $117.12) – Buy under $250, target price $400

SoftBank (SFTBY – $21.40) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $38.46) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $8.11) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $26.82) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $5.00) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.73) – Buy under $13, target price $30+

Velo3D (VLD – $1.81) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Buy while fixed mortgage rates are low

Bag of Junk Silver – ($23.74) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $24.78) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $28.54) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.72) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $28.47) – Buy under $30, target price $50

Coeur Mining (CDE – $3.48) – Buy under $5, target price $20

First Majestic Mining (AG – $8.74) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.41) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.26) – Buy under $10, target price $25

Sprott Inc. (SII – $33.21) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $16,813.41) – Buy

Grayscale Bitcoin Trust (GBTC – $8.14) – Buy

Ethereum (ETH-USD – $1,216.81) – Buy

Grayscale Ethereum Trust (ETHE – $5.20) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.80) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $24.90) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.97) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $30.68) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.81) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.07 – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $29.40) – Buy under $36; $80+ target

EQT (EQT – $35.00) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.11) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $1.95) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.41) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.04) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Thank you Michael MERRY CHRISTMAS TO YOU AND FAMILY ((-:

Merry Xmas to all!

Lazy 3rd

Japan guaranteed the price of gold and silver will rise. Their recent action will pull down the value of the dollar. Also Japan is going to spend 326 billion on defense over the next 5 years. Happy holidays MM and everyone. Thanks for everyone’s input here and over the past year. Happy investing in 2023.

what are the chances that tgtx will get approved for their ms drug ?

Very high. Effective with low/no side effect issues.

Merry Christmas and Happy New Year!

Are people aware of the new technology of flash heating plastic trash etc.,into valuable graphene? Anyone know any traded companies that are leading this amazing advance?

https://www.youtube.com/watch?v=uhfCix7LFh0

REPORTED PROBLEMS WITH SANTA’S NEW TESLA SLEIGH

Eli Grober, 24 December 2022, New Yorker website

Facial recognition for sleigh ignition is unable to recognize Santa consistently through beard and hat.

Range is a little less than four hundred miles. Nearest village to the North Pole is about eight hundred miles away.

“Frunk” full of presents keeps catching fire.

Reindeer have begun to protest what they believe to be unlawful termination. Santa disagrees – insists that he doesn’t “need those weird little horses anymore.”

Rudolph is suing for I.P – believes red-nose technology was plagiarized.

Mrs. Claus has surprisingly widespread investments in fossil-fuel companies, and keeps trying to sabotage the Tesla sleigh.

Santa dangerously distracted by sleigh’s touch-screen gaming console.

Sleigh auto-parks while Santa is inside each house putting presents under the tree. When he exits via the chimney, he has no idea where the sleigh is.

Self-driving system keeps trying to take Santa’s sleigh on the highway.

Internal sleigh navigation won’t synch with the “naughty” or “nice” lists.

Santa inexplicably builds tunnel for sleigh, claiming “tunnels are faster than the air.”

Tunnel collapses. Santa blames “the libs.”

Elves assigned to sleigh repair report inhumane working conditions, vote to unionize. Santa declares, “I’ll just fucking do it myself,” and fires entire staff.

Santa unable to “just fucking do it” himself. Attempts to rehire recently fired elves.

Sleigh too tall, sensors unable to recognize elves or children. Sleigh is recalled owing to safety concerns.

Santa is forced to liquidate most North Pole assets to pay for updated sleigh model.

A frustrated Santa shouts, “Merry Christmas to only some of you!” as sleigh flies across the sky. Christmas stock plummets to all-time low.

Someone impersonates Santa’s sleigh on Twitter and convinces millions of people that Christmas has been cancelled.

Charging station at North Pole far too cold to function – sleigh unable to start. Santa’s mittens prevent use of touch screen, V.R. reins, and door handles.

Sleigh just exploded.

Very funny thank you

That is hilarious. Thanks for a Christmas stress relief chuckle. Especially amusing since Tesla is in a slide backwards. And EV purchases in Europe are as well. The problem is electricity is now so expensive in Europe because of all the fossil fuel issues that people are NOT buying. Not to mention Europe went “all in” on the green movement and spent billions on wind and solar farms and now it’s cold there (there is little wind blowing ) and the sun isn’t shining as great because it’s winter. Brilliant!! On another note 7000 illegal immigrants crossed the border in one three day period very recently. There are so many of them now in those holding facilities we don’t know what to do with them. The drug cartels are sending over enough to overrun the border patrols and then when they round up all of that first wave and start to process them , the cartels send over an even bigger army of men women and children. OMG

In staying with proven winners, Dan Rice is becoming CEO of New Power via SPAC (RONI) which uses natgas for power generation with full carbon capture. Would be interested in MM taking a look.

I think OXY has a carbon recapture program also

OXY is an investor in NET Power, wich RONI is acquiring. Terrific tecnology, but doesn’t generate revenues for years.

NET Power.

Merry Christmas everyone.

MM or Anyone out there do you expect TGTX to go down in price after they get approval tomorrow for their MS drug ?

It should pop. This will be a pretty fast ramp after the launch.

Are we to wait for FSLY to go below 7 before we buy it ?

I meant tgtx in above question not fsly.

You could buy part here and the rest after New Years, whether it’s higher or lower. My bet is higher after the bounce from tax-loss selling.

BTC down 1%, GBTC down 5% .. the market is screaming at you. Listen.

Are you saying GBTC does not own all the bitcoin they have reported to the SEC?

I am saying they do.

I’m saying that Coinbase has the exact business model as FTX and is suspect. I know you feel that Coinbase custodial is separate and safe from Coinbase. If Coinbase stumbles there is no way it doesn’t bleed into custodial.The market has priced in a huge discount for GBTC. Why? Are they stupid?

Take your BTC offline.

“If Coinbase stumbles there is no way it doesn’t bleed into custodial.”

Actually, given the separate legal status of Coinbase Custodial Services, Inc., the extensive licensing requirements for a custodian, and the fact that GBTC’s bitcoin is not an asset on Coinbase Custodial Services’ balance sheet – they are not a counterparty – I see no way any Coinbase problems bleed into custodial in a way that would affect GBTC.

Bought more GBTC = bitcoin at $8,650. I don’t see any reason to pay more than that for bitcoin today.

Heh heh .. we’ll see. You know that old adage, it it’s too good to be true … I predict that GBTC will go down.

I understand people that prefer to own paper assets over hard because of storage concerns ( gold and silver) but I can have millions on a small offline wallet. Why have a counter party risk?

BTW, I’ve noticed that GrayScale stopped advertising.

Ain’t that a bitch over at nvta that not one insider is willing to throw there own money out and buy shares at the current price of 1.70 in a company that you have been so positive about for so long,can you disagree with my thought MM,did you truly miss something, I understand with overall market being in the shit this year but com,on the crash on nvta! Is disappointing

Mm,can you share with us what your dollar cost average is on nvta,tx

$4.3501

Ok,tx

MM, EQT is down over 5 % since you recommended it Is this tax selling you think ? The same with TRTX ?

Do the short sellers follow around MM recommendations? It seems to happen often.

TGTX drug approved

They have halted trading is this to protect the shot sellers ?

They do not halt the trading when it goes down I notice

MM when will they open TGTX up for trading Do you have any idea ?

I did not sell my shares of TGTX i will wait for the buy out

Nat gas prices

very disappointing trading on TGTX

I agree Chaz 39. I thought we would see a 20-30% bump. 8% is quite disappointing IMO.

heck it got to 8.51 before halt was expecting between 11-12 but shorts play games however im hoping its the longs that were playing games today to accumulate more – iwill be patient for now

on the positive side i think downside is minimal

Agreed!

EQT saw a 30 percent drop in production during the recent extreme cold in the Appalachian Basin. Warren Buffet recently added to his stake in Oxi . He now holds 29 billion in that stock. China’s coal usage is up 49 percent. So while California is reducing its carbon footprint the rest of the world is taking their’s up!! The northeast is on the brink of an energy crisis. Boston is getting their natural gas from Russia because politicians are trying to kill off fossil fuels from places like Philadelphia. Got oil??

Arth has YTD 9-30-22 earnings out.

All SEC Filings :: Arch Therapeutics, Inc. (ARTH)

YTD Revenue $15,652. YTD cost of Revenue $51,489. I keep having to remind myself these numbers aren’t in 000’s.

Take a look at page F-3 which covers Accounting for Complex Financial Instruments. Still gets a going concern warning.

MM, what is the fair value of TGTX after BRIUMVI™ (ublituximab-xiiy) approval? Thanks.

MM said $25.00 or higher

thanks.

$25.00 or higher was the buy out price Mm suggested for trtx

Annual end of year pump. Great time to load up on SDOW, the Dow stocks are the next to go.

Have a look at ACHV. Results from their 1st Phase 3 trial for smoking cessation proved very safe and effective. They will have results for their second Phase 3 for smoking cessation in Q2 then off to the FDA. Also in Q2 they will have results from a Phase 2 trial in e-cig cessation.

Anyone care to share their picks of 2023?

I’ll take TSLA and BTC.

Have a look at ACHV. Results from their 1st Phase 3 trial for smoking cessation proved very safe and effective. They will have results for their second Phase 3 for smoking cessation in Q2 then off to the FDA. Also in Q2 they will have results from a Phase 2 trial in e-cig cessation.

gern, tgtx, tsla, rt.

GERN – Winner, winner! Chicken dinner!

Diamond Offshore – DO

Post script: I was able to order the Ledger, follow the instructions and transfer my crypto to the cold wallet as you suggested. Appreciate the advice, the info and the impetus to get it done! TKU!

I’m not as nervous about Coinbase as I was a few weeks ago but offline is best. Impossible to hack.

optt

Michael what do you think about SMMT corp ?

Read this….under DGC Group’s hood there is major corrosion…implications for GBTC not good.

https://open.substack.com/pub/dirtybubblemedia/p/digital-currency-grift?r=5bqkm&utm_medium=ios&utm_campaign=post

why is this bad for GBTC – as long as GBTC holds the coins they say to own, then the value of GBTC is safe and independent of any other venture, correct?

Exactly. GBTC’s coins are NOT an asset of any other company. There is no counterparty. It doesn’t matter what happens to Silbert’s other companies.

Then why the huge disconnect/discount? Risk manifests itself in the stock price. Someone out there is perceiving risk.

Someone out there is wrong.

DCG that is…..

MM, finally some good news for BLPH. It actually was over $3 premarket. Do you think they are going to do an offering after today’s large gains?

Bellerophon Therapeutics Announces License Agreement for the Commercialization of INOpulse® in Greater China with Baylor BioSciences

Bellerophon to receive a license payment of $6 million, as well as royalties on net sales in Greater China

WARREN, N.J., Jan. 05, 2023 (GLOBE NEWSWIRE) — Bellerophon Therapeutics, Inc. (Nasdaq: BLPH) (“Bellerophon” or the “Company”), a clinical-stage biotherapeutics company focused on developing treatments for cardiopulmonary diseases, today announced that it has entered into a license agreement for the development and commercialization of INOpulse® with Baylor BioSciences, a life sciences company dedicated to the development and commercialization of innovative medical products for Greater China.

Under the terms of the license agreement, Bellerophon will receive a license payment of $6 million, payable within 90 days subject to certain closing conditions set forth in the agreement. Additionally, Bellerophon is entitled to royalties of 5% on net sales resulting from all of the licensed INOpulse indications within Greater China. Baylor BioSciences will receive exclusive rights to develop and commercialize INOpulse within Greater China for diseases associated with pulmonary hypertension, including the lead indication of fibrotic interstitial lung disease (fILD), as well as PH-Sarcoidosis and PH-COPD.

“We are delighted to partner with Baylor BioSciences to potentially bring INOpulse to patients in Greater China,” said Peter Fernandes, Bellerophon’s Chief Executive Officer. “If approved, INOpulse has the potential to become the first therapy to treat a broad fILD population that includes patients at low-, intermediate- and high-risk of pulmonary hypertension. We believe that this agreement further validates the potential of INOpulse to address the significant unmet need for therapies that improve activities of daily living and quality of life in patients with fILD, as well as other underserved diseases, including PH-Sarcoidosis and PH-COPD. Importantly, this agreement enables us to gain access to one of the largest markets globally, while strengthening our balance sheet.”

Ted Wang is a member of Bellerophon’s Board of Directors, a co-founder of Baylor BioSciences and is a significant shareholder of Bellerophon and Baylor Biosciences. The transaction with Baylor BioSciences was approved by Bellerophon’s audit committee in accordance with Bellerophon’s related party transaction policy.

I hope so, they need to raise money.

So your saying that the $6 million license payment won’t prevent them from raising money now?

They burn about $5 million a quarter.

MM Comments on BLPH please.

Thanks!

It’s an OK deal. The stock is drastically undervalued, but this big a jump on this news is silly. This is an example of the computer bots reading the headlines, hitting an illiquid stock with buy orders, then the price jump attracts other computer bots and the day traders. Unless you think you can out=trade a supercomputer – I can’t – just ignore the jump and the inevitable drop back (especially if they announce an offering after the close) and wait for FDA approval.

MM, I was hoping this was going to be about MDNA55. Looks like the market doesn’t think much about this patent news.Medicenna Strengthens Intellectual Property Protection for MDNA11 and BiSKITs™ Programs with Issuance of U.S. PatentJANUARY 5, 2023 AT 9:14 AM EST

Download PDF

– Patent covers methods of treating cancer with an IL-2 Superkine and PD1/PDL1 or CTLA-4 checkpoint inhibitor, administered in combination or as a single agent BiSKIT™

TORONTO and HOUSTON, Jan. 05, 2023 (GLOBE NEWSWIRE) — Medicenna Therapeutics Corp. (“Medicenna” or “the Company”) (NASDAQ: MDNA TSX: MDNA), a clinical stage immunotherapy company, today announced that the U.S. Patent and Trademark Office (USPTO) has issued U.S. Patent No. 11,542,312 titled “IL-2 Superagonists in Combination with Anti-PD-1.” The patent provides intellectual property (IP) protection for methods of treating cancer with an IL-2 Superkine such as MDNA11 and a PD1 (for example, pembrolizumab), PDL1 or CTLA-4 checkpoint inhibitor in combination, as planned in the on-going ABILITY clinical trial, or as a single agent using our BiSKIT™ (Bifunctional SuperKine for ImmunoTherapy) platform. The patent’s term extends into at least 2039 without accounting for any potential extensions.

“MDNA11 has displayed promising anti-cancer activity during dose escalation in our ABILITY study and we expect further improvements at the optimal dose in the expansion cohort as well as the combination arm designed to evaluate the synergistic potential of pembrolizumab,” said Dr. Fahar Merchant, President and CEO of Medicenna. “Whereas checkpoint inhibitors have been shown to benefit less than a third of cancer patients while generating annual sales of over $30B, we believe that combinations with MDNA11 and our BiSKIT™ platform, as in MDNA223, may significantly improve outcomes and provide hope to cancer patients that do not respond to checkpoint inhibitors. As patents on checkpoint inhibitors expire from 2028 onwards, the added IP protection provided by this latest patent could allow us to maximize the value of our lead MDNA11 program, while leaving us better positioned to leverage preclinical BiSKIT™ data to pursue value accretive collaborations and partnerships.”

MDNA11 is a “beta-only” long-acting IL-2 super-agonist that is being evaluated in patients with advanced solid tumors in the Phase 1/2 ABILITY study. MDNA223 is a preclinical-stage BiSKIT consisting of an anti-PD1 antibody linked to an IL-2 super-agonist (MDNA109FEAA). Both MDNA11 and MDNA109FEAA are designed to selectively stimulate anti-cancer immune cells without activating cells associated with pro-tumor immune pathways or extreme toxicity. PD1/PDL1 and CTLA4 checkpoint inhibitors are designed to prevent the exhaustion of anti-cancer immune cells and are approved as treatments for a number of cancer indications.

This newly issued patent adds to Medicenna’s portfolio of issued and filed patents and applications providing protection for the Company’s innovative IL‐2 Superkines, including MDNA11, in the U.S., Europe, Japan, China, Canada, India, and Australia.

GRPH implodes:

https://seekingalpha.com/news/3922546-graphite-bio-sinks-45-on-halting-early-stage-trial-of-sickle-cell-candidate?mailingid=30167629&messageid=2900&serial=30167629.41&utm_campaign=rta-stock-news&utm_content=link-3&utm_medium=email&utm_source=seeking_alpha&utm_term=30167629.41

The new Radar Report for 1.5.23 is posted.