Dear New World Investor:

Date: Tuesday, March 7, 2023

Scene: Senate Banking Committee

Hearing: Humphrey-Hawkins Testimony

Presenter: Jerome Powell, Chairman, Federal Reserve

Chairman Powell: Due to the persistence of inflation, we may have to raise rates in larger steps again, and to higher levels than previously expected.

Senator Murphy (I-OR): Chairman Powell, why do you think inflation is so persistent?

Chairman Powell: The economy is stronger than we expected.

Senator Murphy (I-OR) So corporate earnings will be better than expected, and stocks will go up. What will you do if the economy weakens and inflation slows?

Chairman Powell: We’ll slow or stop the rate increases.

Senator Murphy (I-OR) So in an environment where corporate earnings are worse than expected, interest rates will go down and stocks will go up. Mr. Chairman, many pundits have said the strong stock market causes the Fed to be more hawkish. If inflation came down to 2%, would you care if the S&P 500 was at 3500 or 5500?

Chairman Powell: Nope.

Senator Murphy (I-OR) Do you still think the Fed’s 2% inflation target can be met without dealing a major blow to the US labor market?

Chairman Powell: Yes, although there will very likely be some softening in labor market conditions.

Senator Murphy (I-OR) Are you aware that the Fed’s interest rate increases have dramatically increased the budget deficit to the point that Federal interest expense is now larger than the defense budget?

Chairman Powell: Oh, yes. My friend Treasury Secretary Yellen mentions that almost every day.

And then I woke up to find the probability of a 50 basis point (1/2 percentage point) Fed funds hike on March 22 went from 31% before he spoke to 81%. The expected terminal rate went from 5.48% to 5.69%, with the brokerage firm gurus competing to scare you with 6% or even maybe 7% targets.

I just don’t see anyone saying that if the Fed has to raise quicker or higher, it will be because the economy and corporate earnings are strong. If the economy and earnings outlook weaken, the Fed won’t be raising quicker or higher. They’ll be pausing and then cutting.

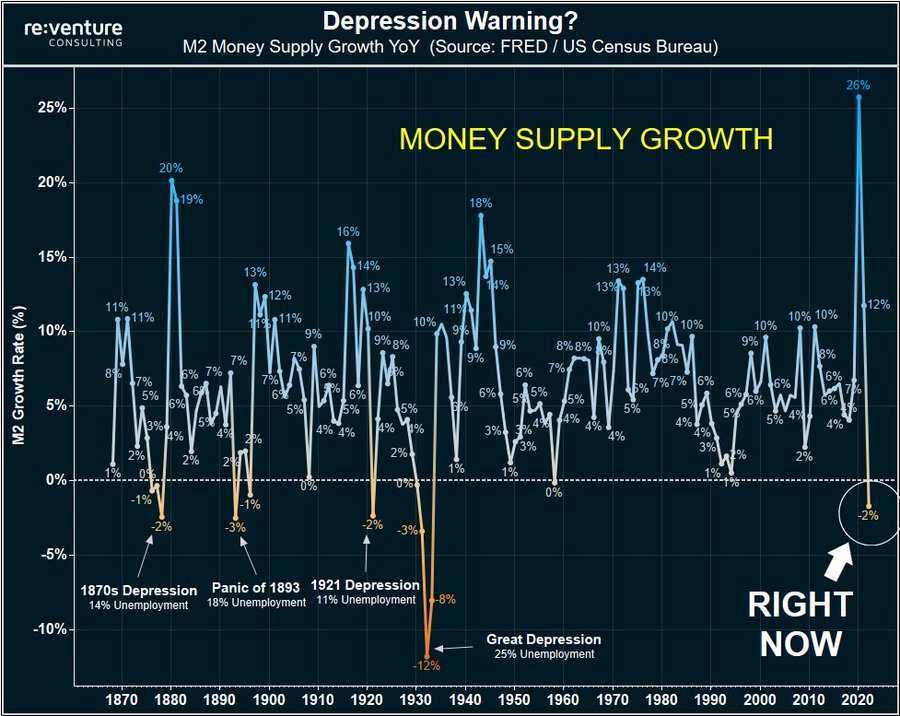

The Fed’s big impact actually is reducing the size of their balance sheet, or Quantitative Tightening, by not replacing expiring debt or even selling some bonds. The money supply, M2, is contracting for only the fourth time in the last 150 years. Each previous time a recession with double-digit unemployment rates followed. The last three times were the 1921 recession and disinflation after World War I and the Spanish flu pandemic; the Great Depression in 1930-32; and after World War II in 1946-48, followed by a recession and deflation in 1949. Powell knows this.

Click for larger graphic h/t @nickgerli1

Click for larger graphic h/t @nickgerli1

After Powell’s testimony the 10-year Treasury note yield barely moved. It’s where it was in mid-October when the funds rate was barely north of 3%. That causes the 10-year minus 2-year Treasury spread to be extremely negative, plunging to minus 106.7 basis points yesterday, a level not seen since September 22, 1981. That means the bond market is saying recession/disinflation is in our future. Powell knows this, too.

Market Outlook

The S&P 500 lost 1.6% since last Thursday after today’s 1.85% decline. The Index now is up only 2.1% year-to-date. The Nasdaq Composite lost 1.1% and still is up a decent 8.3% for the year. The small-cap Russell 2000 dropped 4.0% and is up just 3.7% in 2023. The American Association of Individual Investors sentiment survey is very bearish – an excellent contrarian indicator.

Click for larger graphic

Click for larger graphic

The fractal dimension consolidated a little more as this market tries to make up its mind between better than expected economic news and a scarier Fed.

Top 5

Changes this week: None

Near-Term – chronological order

EQT EQT – cold March & falling natgas supply

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model forecast for March quarter real GP growth increased to +2.6% due to increased spending on international travel. That’s far above the consensus estimate for 0.5% growth and will shock Wall Street.

Click for larger graphic

Click for larger graphic

Of course, shockingly strong growth can be good or bad, depending on how the Fed takes it. The good news is that the Department of Labor’s ridiculous seasonal adjustments to the initial unemployment claims data that caused JPMorgan to politely say that “some alternative seasonal adjustments of the initial claims data show some less favorable changes in filings from recent weeks than the official figures.” Goldman Sachs said that “seasonal adjustment issues have exerted an increasing amount of downward pressure on initial claims over the last few months.” adding that “the pressure will begin to reverse in a few weeks.”

We are about to see a big spike in unemployment claims, and the Fed has said they are mainly concerned about labor market strength in trying to get inflation down. A negative payrolls report is coming – not tomorrow, but soon.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, March 10

ACRDF – Acreage Holdings -Through 3/19 – South by Southwest (SXSW) Conference & Festival

ACRDF – Acreage Holdings – Through 3/12 – New England Cannabis Convention (NECANN)

February payrolls – 8:30am – +205,000 expected; January was +517,000

UUUU – Energy Fuels – 11:00am – Earnings conference call

AAPL – Apple – 12:00pm – Annual meeting

Sunday, March 12

Daylight Savings Time begins at 2:00am local time

Monday, March 13

CMPS – Compass Pathways – 10:00am – Oppenheimer Healthcare Conference

INO – Inovio – 10:40am -Oppenheimer Healthcare Conference

APTO – Aptose Therapeutics – 12:40pm – Oppenheimer Healthcare Conference

Tuesday, March 14

CMPS – Compass Pathways – 1on1s – Loop Capital Conference

Consumer Price Index – 8:30am – Headline year-over-year: +6.% expected; February was +6.4%. Month-over-month +0.2% expected: February was +0.5%.

Core YoY: +5.5% expected; February was +5.6%. Month-over-month +0.5% expected; February was +0.4%

MDNA – Medicenna – 2:40pm – Oppenheimer Healthcare Conference

Wednesday, March 15

GILD – Gilead Sciences – 10:15am – Barclays Global Healthcare Conference

PD – PagerDuty – 5:00pm – Earnings conference call

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Arch Therapeutics (ARTH – $4.10) said they are on track to add 15 independent commission-based sales representatives by the end of March. They’ll focus on high volume government facilities. Dan Yrigoyen, VP-Sales, said: “…we have experienced an increase in new and recurring sales orders in areas where Arch management directly provides dedicated selling and clinical support to our independent sales representatives. We believe at this stage of product rollout, that we can further advance our commercialization efforts by deploying additional qualified sales representatives who have a proven track record selling advanced wound care products in VA and other government facilities. For example, this approach recently resulted in a repeat order and subsequent decision to maintain and replenish AC5 inventory as it is used on an ongoing basis within the largest US-based government hospital and only Level 1 Trauma Center within the Department of Defense.” Good news!

The Centers for Medicare and Medicaid Services established a new Level II Healthcare Common Procedure Coding System code for AC5, effective April 1. The HCPCS code makes it easier for providers to charge CMS and other insurers for AC5 used in doctors’ offices, wound care clinics, hospital outpatient departments and ambulatory surgical centers. CEO Terry Norchi, said many clinicians have expressed interest in AC5 but have been hesitant to order in the absence of a dedicated HCPCS code. ARTH is a Hold for a buyout.

Primary Risk: AC5 fails to sell or the internal trial fails.

Clinical stage of lead product: External approved. Internal trial 2023

Probable time of first FDA approval: External done. Internal 2024

Probable time of next financing: March or June 2023 quarter

Bellerophon Therapeutics (BLPH – $6.53) placed a $5 million direct offering with a single life sciences-focused institutional investor to sell 718,474 shares of common stock at $2 a share and 1,781,526 prefunded warrants at $1.99 each. These deals happen when an institution wants to take a big position without running the stock up.

Although they did not identify the investor in the press release, it was Kevin Tang of Tang Capital Partners in San Diego. It’s a 20-year-old venture capital and private equity fund with about $700 million under management, generally considered a “whale.” Instead of dropping on the news, the stock shot up as others coat-tailed on Kevin. The stock is up 250% from last Thursday! Don’t chase it.

Buy BLPH under $5 for a $30 first target and $100 someday.

Primary Risk: The Phase 2b PH-ILD trial fails or the FDA turns down the INOpulse.

Clinical stage of lead product: Phase 2 transitioning to Phase 3 in the March quarter

Probable time of first FDA approval: 2024

Probable time of next financing: March 2023 quarter

Invitae (NVTA – $1.54) got their first commercial coverage of the Personalized Cancer Monitoring assay in all solid tumors by Blue Shield of California. The test is considered medically necessary for patients with stage I-IV cancer after surgical intervention for adjuvant or targeted therapy and/or monitoring for relapse or progression. It uses a novel set of personalized assays based on a patient’s tumor to detect circulating tumor DNA in blood, assisting with risk stratification, assessing response to treatment, and detecting cancer recurrence.

The company presented at the TD Cowen Healthcare Conference (TRANSCRIPT HERE). Management said their cash burn in 2023 had to start with a 2, and they have guided for $250 to $275 million. Their cash burn in 2024 has to start with a 1.

The new CEO said: “What provides long-term value for our shareholders is to get the company in a healthier space, give us the time and the runway to work on our business and to build a more profitable space for the company, get back to growing, get back to innovating and disrupting, which is what we do best. I think we have landed on a solution that optimizes all the things that we were trying to plan for.”

I agree. This guy is good. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: 2024 or not needed

Biotech MegaShift

Akebia Therapeutics (AKBA- $0.81) reported December quarter revenues down 7.4% from last year to $55.18 million, ahead of the $47.4 million estimate. The net loss of only four cents a share was much better than the 19¢ loss expected. So why did the stock get clobbered today?

Guidance. On the conference call (TRANSCRIPT HERE), they said they expect 2023 Auryxia revenues of $175 million to $180 million – no growth from 2022’s $177.07 million. They said that 2022 was helped by higher pricing, improved payer mix, and a 2022 year-end inventory build by a customer that exceeded 2021. In 2023 they expect an increase in realized net price per pill, partially offset by reduction in total units sold and inventories returning to normal levels. The CFO said: “We have set 2023 net product revenue guidance at $175-180 million as we remain cautious about a phosphate binder market recovery. The market continues to contract modestly due to COVID-19 and dialysis staffing issues. We will continue to be mindful of non-essential spend and work to reduce costs overall.”

They expect marketing authorization for vadadustat to be granted by the EC in May, which would be applicable to all 30 European Union member states and affiliated countries. Beyond the EU, they also anticipate a regulatory decision for vadadustat for ACCESS Consortium countries, the UK, Switzerland, and Australia later this year.

The company finished the quarter with $90.5 million in cash, enough to fund them for at least the next 12 months. AKBA is a Hold for the results of the FDA meeting on vadadustat.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Vadadustat NDA filed; CRL

Probable time of next FDA approval: Unknown

Probable time of next financing: Unknown

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $150.59) introduced a bright yellow iPhone 14 and 14 Plus so no one can miss that you have the latest and greatest.

Click for larger graphic

Click for larger graphic

Apple’s forthcoming virtual reality headset is expected to ignite the VR market, according to market research firm IDC. Their research director said: “In VR, we haven’t hit that hockey-stick moment yet, where this is just going to just take off like we saw with smartphones. We’re not yet at the place where people look at this and say, ‘Wow, I just want to put that on,’ but Apple just might help create that hockey-stick moment. Apple is perhaps the most trusted brand in the tech industry, and it’s in Apple’s DNA to make things so gosh darn easy to use.” Additionally, Apple’s “broad ecosystem of devices and applications and services” could provide a wide variety of entrance points for consumers, as they move back and forth seamlessly between between, say, Apple TV and applications from their Apple Watches or iPhones. “How would you like to watch Apple TV on your VR headset? There’s a certain flow there that could add up.”

Wedbush’s very respected analyst Dan Ives raised his Apple price target from $180 to $190, the third-highest on Wall Street. (Three analysts are at $195. See below for the highest target,) He cited signs that demand for iPhones in China has been growing, while supply was steady in January and February, in contrast to the supply-constrained December quarter that resulted from issues related to China’s zero-COVID policies. And early indications in March suggest conditions continue to improve.

He said said Apple is gaining market share in China and demand in the US and Europe is holding up well. He estimates that about 25% of current iPhone users have not upgraded their iPhones in more than four years, and he believes the new iPhone users added to Apple’s ecosystem over the past year will lead to a reacceleration of the company’s services business in the coming quarters.

Even Goldman Sachs finally recommended buying Apple for the first time in nearly six years, after being mostly on the sidelines as the iPhone maker’s stock more than quadrupled. The analyst who just took over coverage of the company moved it to a Buy with a Street-high $199 target price.

AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $33.95) gave a fireside chat at the Morgan Stanley Technology, Media & Telecom Conference (TRANSCRIPT HERE). Management said optical fiber “will be the largest area of growth opportunity for us over the next few years. We’ve talked about a multiyear time period of high single, maybe low double-digit growth. And I think that will be supported by both private and public investment. There’s a lot of public investment out there that’s beginning to come online. It will come online in ’23, ’24, ’25. And I think that will contribute to a lot of the growth. And in our discussions with customers, both on the fiber-to-the-home side, on the carrier side, as well as on the data center side, we’re convinced that they’re committed to continue to invest.”

Corning’s Hemlock solar business has seen a major resurgence just with the need for US production to meet some of the Federal legislation that’s passed. Management said: “We turned on solar capacity a little over a year ago. The need for US-based solar components has become critical. We were able to take advantage of that, turn on capacity. We’ve sold that out and it’s fully operational and fully sold out for a period of time. We have the ability to turn on more capacity and the IRA, for sure, affords us an opportunity to look at the solar supply chain. We’re excited about participating in a US-based solar supply chain.” Corning is planning to build a $1 billion solar business.

The company introduced a new connectivity solution, the EDGE Distribution System. It’s a pre-engineered data center solution that shortens installation time for server cabling by up to 70% and helps address shortages in skilled labor. The system simplifies the deployment of cabling within data centers, all the way to the server racks. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2023 .

Gilead Sciences (GILD – $75.95) did a fireside chat at the Cowen Healthcare Conference (TRANSCRIPT HERE). This was a very good, comprehensive review of the status and multiyear outlook of almost all of Gilead’s many drug programs. I am raising the buy limit on Gilead to $80 and the target price to $120. I really think it’s worth $160 – double today’s price. And you get a3.75% yield while you wait! GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $181.69) is up 57% this year, the 5th-best performer in the Nasdaq 100 Index. They plan to cut thousands of more jobs and may benefit from a US ban on TikTok. And they just hit two billion daily active users on Facebook. They have more than 140 billion Reels plays across Facebook and Instagram each day.

They just cut prices on the Quest 2 headset 14% to $429 and the high-end Quest Pro by 33% to $999 to spur adoption. Meta has a whopping 82% share of the VR headset market, according to IDC. The managing director at VRdirect said: “Meta is the obvious market leader in VR and very advanced in terms of building a compelling B2C and B2B ecosystem – the Meta-Microsoft partnership is an example. However, Meta is facing an uphill battle, when it comes to acceptance by enterprise customers. Apple already knows this market and leveraged their smartphone business in the B2B space. Meta will continue to be the market leader, but the competitive dynamics will grow.”

IDC’s research director said: “Once Apple’s headsets get to cycle two or three when we’re past the ‘warts-and-all stage,’ we’ll be able to go feature-by-feature and ask who’s doing it best. That’s where the battle’s really going to begin.”

But that’s likely years in the future, and meanwhile, investors will buy both META and AAPL to get exposure to this next great consumer product. You should, too. META is a Buy under $150 for a $400 target in 2024.

SoftBank (SFTBY – $20.43) will take ARM ltd. public in an $8 billion US initial public offering later this year in the most high-profile IPO in recent years. They are expected to file a preliminary prospectus in April, naming Goldman Sachs, JPMorgan, Barclays, and Mizuho as lead underwriters. Softbank is expecting a $50 billion valuation, nicely above the $40 billion Nvidia deal that the antitrust regulators nixed. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Other Tech

Fastly (FSLY – $14.18) did a fireside chat at the Morgan Stanley Technology, Media & Telecom Conference (TRANSCRIPT HERE). The new CEO said looking forward at what the Internet is going to deliver to the world, it’s going to be about the user experience of websites and applications over the Internet. That’s what’s going to matter. Fastly now is focused on building networking infrastructure in the edge cloud space. That is going to be one of the most exciting spaces for the next 10 years and how Fastly delivers that user outcome is what’s important.

He pointed out that the world just got a three-year tutorial through COVID about how the success of every organization – schools to governments to businesses across almost every vertical – is going to be dependent on the user digital experience that they provide. Every experience has to be fast, safe, and engaging. That’s Fastly’s total focus. By letting customers deploy their own bespoke workloads right at the edge, they can deliver a better user experience when it matters most.

Fastly will do $1 billion in revenues in 2025, up from $432.7 million last year. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Probable time of next financing: None needed

PagerDuty (PD – $28.77) reports January quarter results after the close next Wednesday, Analysts are looking for revenues up 25.9% to $98.84 million and a two-cent profit. April quarter guidance should be revenues up 22.8% to $104.82 million and three cents. PagerDuty usually guides low and then beats. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk:Digital operations management is a competitive area.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $4.08) will do their 34th Electron launch and second from the Virginia launch complex this Saturday, March 11, at 6:00pm EST. They’ll deploy two satellites for Capella Space’s Synthetic Aperture Radar imagery constellation. You can watch it starting at 5:40pm from the link on THIS PAGE. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Probable time of next financing: None needed

Velo3D (VLD – $2.65) will do a roadshow, the Proof is in the Printing Additive Manufacturing Tour, which will visit eight cities across the US – Phoenix on March 29, Denver on April 27, Houston on May 9, Jupiter on June 15, Schaumberg on July 20, Long Beach on August 17, Detroit on September 20, and Fremont on October 19. You can sign up HERE. They’ll also be in Europe, Japan, and South Korea. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,835.70) is about flat since last Thursday, thanks to a $16.90 upturn today. Precious metals were pressured Tuesday – the 2nd-biggest drop this year – by the hawkish Fed supporting a stronger dollar. The fractal dimension is deep in consolidation mode, building up energy for the inevitable run to new highs.

Miners & Related

Coeur Mining (CDE – $2.89) presented at the BMO Global Metals, Mining & Critical Minerals Conference (SLIDES HERE). Their message was straightforward:

Click for larger graphic

Click for larger graphic

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $20,536.00) and other cryptocurrencies were hit by the news that Silvergate Capital, a bank that has long been at the heart of the digital currency industry, is shutting down. Silvergate operated the Silvergate Exchange Network, so there may be a drop in liquidity as it ceases operations. But that will least affect bitcoin, which is deeply liquid everywhere. The more people who decide to give up chasing ishtcoins and focus back on bitcoin and ether, the better.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $11.80) jumped after oral arguments got underway in Grayscale’s suit against the SEC for not allowing GBTC to convert to an exchange-traded fund. The SEC’s opening argument that bitcoin’s unregulated nature leaves investors open to fraud seemed to fall on deaf ears.

The three judges in the District of Columbia Court of Appeals in Washington pressed the SEC on Grayscale’s argument that, because the regulator previously approved certain surveillance agreements to prevent fraud in bitcoin futures-based ETFs, the same setup should also be satisfactory for Grayscale’s spot fund, since both spot and futures funds rely on bitcoin’s price.

Judge Neomi Rao said: “It seems like it’s fine for an agency to say okay, we need some more information, but it seems there’s quite a bit of information here on how these markets work together, and the SEC has not offered any explanation… that the petitioners here are wrong.”

Grayscale is hoping to get a ruling before the July 6 deadline for the SEC to accept or reject its application.

A day before the oral arguments, the bankruptcy trustee for FTX’s Alameda Research filed a lawsuit against Grayscale Investments alleging “exorbitant management fees” and accusing Grayscale of “improperly preventing redemptions” from the Bitcoin and Ether trusts it manages. The chief restructuring officer for FTX said: “Our goal is to unlock value that we believe is currently being suppressed by Grayscale’s self-dealing and improper redemption ban.”

Obviously, when – not if – the SEC caves or loses, or the FTX trustee wins, GBTC will almost double. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $75.55

Oil fell about $2.50 since last Thursday, But oil demand in China after the COVID reopening is expected to be a record.

Click for larger graphic

Click for larger graphic

Oil consumption is heading for a record this year, according to the International Energy Agency. Supply, hurt by Russia’s invasion of Ukraine, a slowdown in US shale growth. and lackluster investment in production, won’t keep up. By the second half of the year, the market will face a shortage and as Bloomberg wrote, $100 oil is coming soon.

State-controlled Saudi Aramco just increased most official selling prices for Asia in April to $2.50 a barrel above the regional benchmark, 50 cents more than the level for March. It’s the second month in a row that Aramco has increased prices for Asia, it’s biggest market. The OPEC+ cartel is back in control of the world oil market as the shale revolution peters out, according to a number of industry executives who’ve warned of higher prices for crude in the year ahead.

Scott Sheffield, CEO of Pioneer Natural Resources, the biggest independent US shale oil company, said: “I think the people that are in charge now are three countries — and they’ll be in charge the next 25 years. Saudi first, UAE second, Kuwait third.”

Major US oil producers are warning that production from one of the fastest growing sources of supply appears likely to top out by the end of the decade. ConocoPhillips and Pioneer Natural Resources are among those saying the American shale-oil juggernaut soon will be a spent force as the best drilling targets are exhausted and financing new wells gets more difficult.

The July 2026 Crude Oil Futures (CLN26.NYM – $65.03) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.87) is a Buy under $36 for an $80+ target.

EQT (EQT – $31.34) rose a bit on cold weather forecasts and record gas flows to LNG plants for export, but the Energy Information Administration lowered its 2023 forecasts for US natural-gas prices by11.2% from the February forecast. But trying to trade the weather forecast is nuts. The front-month fell to a 28-month low below $2 per mmBtu in intraday trading on February 22 on warmer forecasts. Then it jumped 9% to settle at a five-week high over $3 on March 3 on colder forecasts. Then it plunged 15% on March 6 on a less-cold weather outlook, before rising 2% the next day on the cold weather forecasts and record gas flows to LNG plants for export.

Folks, we don’t own EQT for the weather forecast. We own it because it is a well-managed, low-cost, and the largest producer of natural gas, a fuel that will be replacing coal and providing cleaner energy and chemical feed stocks for decades to come. As a recent article on SeekingAlpha said: EQT Corporation: Weather Or Not. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

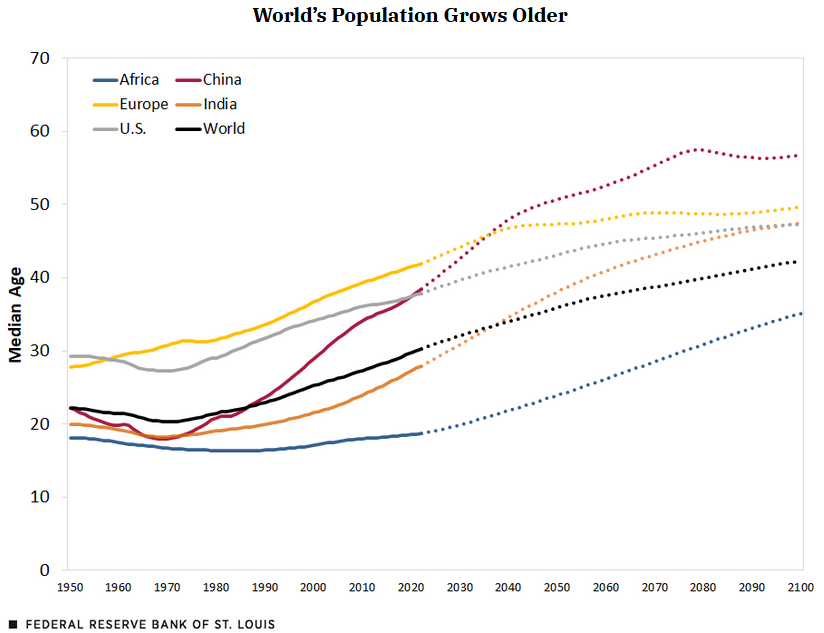

In 1973, half of the world’s inhabitants were under age 21. By the end of the 21st century, more than half will be 40 or older, according to projections.

Click for larger graphic

Click for larger graphic

* * * * *

The Hubble Space Telescope took this photo of the “Pillars of Creation” (a section of interstellar gas and dust in the Eagle Nebula, in the Serpens constellation about 7,000 light-years away from Earth) in 2014. The pillars are four to five light-years tall – a light-year is 5.88 trillion miles— yet NASA calls them “a fascinating but relatively small feature of the entire Eagle Nebula, which spans 70 by 55 light-years.”

Click for larger graphic h/t This Is True

* * * * *

Your glad Elon Musk bought Twitter Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

HERE

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Imagine that. Dan Yrigoyen VP of sales at ARTH has actually achieved got his size 12 shoe into the front door of the Veterans Administration giant medical system. Not only that but they now have recurring sales!! A feat that was labeled on this board that was impossible for a start up biotech company. The centers for Medicare and Medicaid have established a coding system for AC-5. Therefore, removing a giant hurdle to the purchase of AC-5. Very impressive, Dan.

All BS talk. Let’s see the actual sales numbers in press releases. As I said last year, AC5 variants are investigational, so almost no MD’s or institutions will take legal risks dealing with an investigational product and a company with lousy lying management. All the stupid codes for AC5 are complete crap in this context. I’ll change my opinion if all the AC5 products drop the “investigational” poison.

This horse has been beaten down so hard it’s time for the glue factory. MM will never back down on his picks.

Changed my mind and sold:

2016

BCRX

RLYP

SQNM

DRWI

TIL.V

2017

TWER

TWTR

2020

NYMX

2021

EWJ

2022

BIOC

CWBR

SD

You have CWBR as a hold. Are you telling me you sold it last year?

MM, SD was the best stock you have ever recommended to us profit wise since I’ve been here. I didn’t hear anybody say THANKYOU.

Unfortunately, his bad picks have dwarfed his good picks by a mile. Not saying that can’t change but the past few years have been less than stellar.

AC5 is approved, not investigational. AC5-G for endoscopic mucosal resection and AC5-V for vascular reconstruction are investigational, but who cares? AC5 is entering a huge market and the next big one is the internal surgery application.

Dearest Michael, what are your projections for stock price by the end of this year? In addition, when do you think the internal testing and approval process be completed?

Thank you and GOD Bless you!

George

The original AC5 is the super duper bandaid. After years of approval, why hasn’t it sold more than a handful? AC5-G and V are kinda like internal products. Why are they still investigational? The scientific people at the company should have gotten it approved by now, rather than stymied at the investigational stage. Why? Because they don’t have the money to get them approved–the money is squandered on high salaries for useless people like TN and the rest.

Suppose they get internal approval for AC5. They have been near total failures at sales for external uses. The same will probably be true for internal uses. Huge markets for both external and internal uses, but huge failure and incompetence of marketing will continue to be seen. No institutions will do business with an incompetent company like ARTH. A partner may emerge and offer a 2-3x multiple of the prevailing stock price. If TN repeats his past behavior, the partner will say F YOU to him, take it or leave it. The stock is now at 2 cents before the crazy 200 reverse split. Shareholders will be lucky to get 6 cents. Whoopee do after nearly 10 years of hopium in NWI.

MM, you said not to chase BLPH. Do you think it’s going to drop back to the offering price of 2?

Probably at least a big retracement.

No, but there’s a good chance we get it under the $5 buy limit.

MM – you said “Obviously, when – not if – the SEC caves or loses, or the FTX trustee wins, GBTC will almost double”. Question – if the FTX trustee is suing GBTC and wins, how would that positively effect the GBTC price? What am I misunderstanding?

In the words of Scott Adams, stay the hell away from GBTC. If you want BTC, buy it straight up with a private wallet.

Michael, are you still a believer in BTC and what price and when do you think it elevates to?

Yep, I dollar cost average a small amount every day. Once the FED pivots it should take out it’s old highs and more.

I agree.

MM–on VLD, please comment on the negative statements of Lazerator on YMB. He says that sales have mainly been from backlogs and are tenuous.

All their shipments (which is when they book revenue) are from backlog because they basically build to order. They finished 2022 with a $43 million backlog and guided 2023 for over $120 million in sales, so they need to sell about $20 million a quarter this year. They did $15 million in the December quarter. I expect them to hit their revenue goal unless there is a deep recession.

Incidentally, VLD has only $4 million at Silicon Valley Bank plus a credit line they had no plan to use. So no impact on the company.

Thanks.

Seems to me someone(s) is driving NVTA down to force it into a Reverse Split….

Swear I been thinking the same thought super dave,what a joke the way this has crashed,having so much potential,I guess that’s when we will see 10 dollars a share next,unless something magically happens to stop the fall,what a piece of shit it has been,have a nice day

The saddest part about the fall in nvta is that they can keep jerking it off until the next earnings report comes out and that’s not until the middle of may.they need to report some collaborations with other pharmaceutical companies or something..

Until then,with almost 19 percent of share short,no reason for them to close out there position ,I know we’re all in this together,also tx to everyone for bringing other picks to the table,if you are interested in oil and gas maybe look into cpg and ctra ,they both pay a dividend,have a great day

Janet is watching carefully at a “few” banks.

https://finance.yahoo.com/news/yellen-says-treasury-department-carefully-watching-crisis-at-a-few-banks-153243680.html

We’ve seen this movie before.

I bot a tiny bit of SKF this morning.

MM did Invitae have their corporate account at SVB and if so

Will they be covered?

Everyone is 100% covered.

To all on this message board – which of MM’s picks has the greatest potential to pop this year? If none of them then please share your best pick to pop – man do I need a winner, I’m so far down its painful! Thanks for the advise.

I like TSLA and BTC but you need patience. The only murphy pick I like is VLD because of its SpaceX connection.

I also think MRNA will be a big winner with their mRNA technology and possible cancer cure.

BUT … nothing is going to do much until J-POW is done messing with interest rates. MM points out that we are paying more than the defense budget to service the debt. That cannot stand for long and when it reverses .. watch out above.

VLD–besides SpaceX, how many other customers does VLD have? What do you think of Lazerator’s (YMB poster) assertions that sales are minimal or misleadingly reported?

https://velo3d.com/partners/

But this is a huge spec stock. I have a mere 1000 shares. Nothing to lose sleep about.

33

SVB- So, now we find out who is swimming naked as Jay Powell proceeds to dry up the system of ALL of its liquidity.

What is truly shocking is not only the speed of the collapse but that it came out of left field, unexpectedly. On a Saturday, just one day after the FDIC takeover, it is really hard to say what will happen next to the bank itself and to the hundreds of startups and growing companies with tens or hundreds of millions of dollars in deposit protected only up to $250,000.- (many perhaps all of the MM small co. picks probably with accounts there at risk, RKLB for sure). We are talking about thousands of customers and employees that may not receive their cash or payroll. This is a huge catastrophe. Under normal circumstances there should be a deal hastily arranged and blessed by the Biden administration with a large Money Center Bank taking over SVB perhaps with the help of Buffett and others in the mix announced tomorrow night and in any case before the market opens on Monday.

BUT, we do not live in normal circumstances. The Biden Administration has plunged the US and Europe with NATO, and it is totatlly absorbed by, in a losing proxy war in the Ukraine against Russia which is becoming a financial black hole after absorbing more than $100billion in 12 months. $10billion+/month are going to the Zelensky Government while the rail disaster in OH is being ignored and FL families damaged by Hurricane Ian are NOT receiving any insurance funds from FEMA. Chances that anybody in the West Wing has any plans beyond Yellen’s platitudes is doubtful.

Also, there is never just ONE cockroach; expect more bad news from Regional Banks. Many potential risks there; I am not shorting but watching FRC carefully. By the time we hit the 3rd or 4th disaster Powell will do a 180 and lower rates and firehose the economy with cash, again. Gotta hold a LOT of Gold when that happens.

Yeah, I see RKLB had 8% in SVB and this will most certainly hit many tech start ups. HOWEVER, the problem isn’t with the relative pittance we are spending in Ukraine or the other anti Biden rant you posted.

The problem is the servicing of our 31 trillion dollar debt that has been run up by BOTH the red tie guys and the blue tie guys. That number is larger than the defense budget.

I do agree there will be more issues with other regional banks. I bought a small amount of SKF Friday morning and sold some small tech I had. I also agree that J-Pow will HAVE to pivot sooner than later which will explode assets up once again. Boom-Bust-Boom-Bust.

The Fed has caused way more problems than they have solved and should be abolished.

We should also cut defense spending by 3/4 and start hitting that national debt immediately.

SKF sounds like a great idea provided one trades a portion depending on news flow. The latest is that Yellen declared NO bailout, a batshit crazy decision.

What needs to happen is, at a minimum, a repeal of the $250,000.- FDIC deposit guarantee, like Jim Bianco says “a made up number anyway”, and allow the FDIC/OTC/Treasury/FED to guarantee ALL deposits for any amount immediately and for a long enough period to stabilize the system. The alternative is more Banks’ failures very soon. (FRC??)

The whole FDIC only has a fraction of what would be needed in a complete bank failure so you can make up any number you want. 250k, 500k, a million .. whatever. If there was a major run, too bad so sad.

Physical gold and cold storage BTC would be the place to be in a failure. I’m betting they will come up with some kind of BS solution for SVB but the contagion word will spread in people’s minds.

I’m guessing that SKF will open down tomorrow but we’ll see. Small position, total gamble and will dump as needed.

Actually Yellen had said no bailout for the bank shareholders and officers, not no bailout. Employees are getting paid to continue working from home at the moment, since the bank is under “new management”. Those with funds deposited at the bank were never in danger of not being bailed out. That now includes those with deposits over the $250k limit. Those limits were in place to protect consumers and really small businesses so they consider the banks a safer place to store their cash (not in their homes or safes at work).

All deposits are being guaranteed, not limited to the $250k, so what are you talking about?

How many A-I stocks are in the path of SVB fallout? And now the Signature Bank in New York. And NWI stocks?

Janet Yellen will not bail out a bankrupt NWI or the losses of its investors. 😉

Thanks for the chuckle Opie

Why not? We are giving “free” money to everyone else. Just write a NSF check from the Treasury like everything else we seem to be doing. The DJIA was down today after the big fallout from SVB. 90.50 . TGTX $15.60 up 6.96 percent, BLPH $7.01 up 1.01 percent, Sprott up 6.85 percent VLD up 4.64 percent, UUUU up 1.27 percent, HYMC up 28.74 percent, SVM up 8.19 percent. Just say’n

NWI fall started long back ! Pioneers !!

MM is a buyout from BP still on the table for TGTX? The hit pieces on SA are starting to come in and the share price has dropped some in the past week. There is considerable more risk if they try to roll out Briumvi on their own so there is some concern. I think this has been one of your better picks in recent years. None of us want to see another DNDN scenario unfold where we sold too late. I was also wondering if you had any other recommendations on the AI platform besides Apple such as NVDA?. You once recommended NVDA years ago and it turned out to be big winner. I think a lot of us would have stayed invested in that pick and happier with our portfolios had you continued to recommend it. Thanks

The Radar Report for 3.16.23 is posted.