Dear New World Investor:

“Whenever the Fed hits the brakes, someone goes through the windshield.” It’s an old Wall Street saying born of painful observation, and it’s true. After 11 days of turmoil that brought down four banks and left a fifth teetering, the markets went from pricing a late-cycle inflationary expansion to a deflationary banking crisis requiring significant monetary stimulation in the course of five days.

Fed Chairman Powell had to thread a difficult needle. If he raised the Fed funds rate 50 basis points (0.5 percentage points) due to persistent inflation, he would have piled more stress on an already imploding situation. But if he didn’t raise rates or even followed Elon Musk’s terrible advice to cut by 50bps, the markets would think things are much worse than they thought and panicked.

2020 vs. 2023

Click for larger graphic

Click for larger graphic

So he raised by 25bps to a new range of 4.75% to 5%, the highest level since October 2007, and said that “some additional policy firming” – further increases – might be necessary, but the Fed was close to done. He pivoted language from “will” have ongoing hikes to “may” have ongoing hikes and did away with language for “ongoing rate increases” in interest rates. It’s as close to a pause as you are going to get because if he ruled out further rises, he would immediately be fighting the prospect of imminent cuts.

The markets were comfortable with that until former Fed Chair and current seemingly hapless Treasury Secretary Yellen said all depositors would not be protected if a bank failed. That dumb statement tanked the financial markets yesterday.

Click for larger graphic

Click for larger graphic

Right now, what has to happen in a bank failure is the shareholders and bondholders get wiped out, as they should be. All the depositors are protected, even over $250,000, as they must be. What needs to happen is that every director and member of the C-suite should have every dollar of salary, bonus, and insider sale profits for the last 12 months clawed back. That would provide all the incentives needed to ensure that the people who are supposed to worry about the bank’s solvency are doing their job.

As regional and hometown banks tighten their lending standards, particularly for commercial real estate (see my “Your Editor” sign-off), it will have the same effect as further interest rate increases. The Fed said the US banking system is “sound and resilient” but the financial turmoil is “likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation” to an uncertain extent.

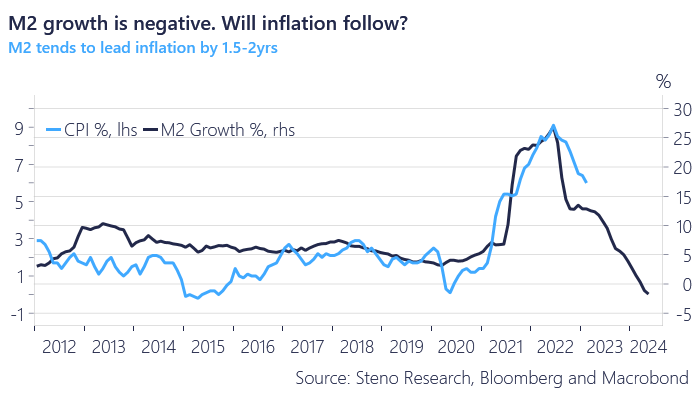

In addition, the Fed will continue its pace of reducing its balance sheet (Quantitative Tightening) so the money supply is plunging:

Click for larger graphic

Click for larger graphic

Peak inflation and peak Fed hike velocity are well behind us. They mattered a lot more when we were discussing 200bps, 300bps, or 400bps of hikes remaining. Now the driver of stock returns will be revenue and earnings growth (or drug progress) in a slow- to no-growth environment. And now the biggest fear for trillion-dollar funds is missing the next rally. Buckle up, cowboy.

Market Outlook

The S&P 500 lost 0.3% since last Thursday – thank you, Secretary Yellen. The Index is up just 2.8% year-to-date. The Nasdaq Composite gained 0.6% and was over 12,000 yesterday before Yellen. It is up 12.6% for the year. The small-cap Russell 2000 dropped the most, 2.9%, and now is down 2.3% in 2023.

The fractal dimension is very consolidated, as you might expect with all the cross-currents. When the next trend starts, it’s going to be a big one. I am expecting it to go north of 4400.

Top 5

Changes this week: Added BLPH to Near-Term

Near-Term – chronological order

EQT EQT – cold March coming

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

BLPH Phase 3 results mid-2023

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, March 24

Short Interest – After the close

Thursday, March 30

December quarter GDP – 8:30am – Third estimate

Friday, March 31

Personal Consumption Expenditures Index – 8:30am

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Algernon Pharmaceuticals (AGNPF – $0.31) is going to do a down-and-dirty rights offering of units of one share of stock and one warrant at 25¢ per unit for each share of stock you currently own, but only if you live in Canada. They’ll raise $2.4 million for 50% dilution. They’ve made a number of poor financial decisions and this one smacks of desperation. Sell AGNPF.

Primary Risk: Ifenprodil fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2024

Probable time of next financing: 2023

Aptose Biosciences (APTO – $0.57) reported a December quarter loss of $10.0 million or 11¢ per share, right on the consensus estimate. On this afternoon’s conference call (AUDIO HERE and TRANSCRIPT HERE), management said that this week they dosed the first patient in their combination trial of tuspetinib with venetoclax. During January’s JPMorgan Healthcare Conference, they discussed the tuspetinib program with several Big Pharma potential partners and found good interest.

CEO Bill Rice has pivoted the company twice, from APTO-253 to luxeptinib to tuspetinib. He can identify potentially powerful molecules, design tough trials to asses them quickly, and then expand into registrational trials that will give bulletproof safety and efficacy data for the FDA. Wall Street hates his slow, deliberate approach, but I want to see what he’s targeting: FDA approval of an effective drug for a very large market. That’s why I call him the best drug developer in biotech.

The company finished the year with $47.0 million in cash, enough to carry them into the March 2024 quarter.APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Bellerophon Therapeutics (BLPH – $7.55) is up sharply since March 6 as people coat-tail on the Kevin Tang investment. The top-line results of their Phase 3 trial in fibrotic Interstital Lung Disease are due in midyear. I expect total success and a filing for approval this year, with approval in 2024. I added it to near-term buys this week. Buy BLPH under $5 for a $30 first target and $100 someday.

Primary Risk: The Phase 2b PH-ILD trial fails or the FDA turns down the INOpulse.

Clinical stage of lead product: Phase 2 transitioning to Phase 3 in the March quarter

Probable time of first FDA approval: 2024

Probable time of next financing: September 2023 quarter

Graphite Bio (GRPH – $2.32) reported a December quarter loss of 44¢ per share, better than the estimate for a 51¢ loss. Unfortunately, they didn’t do a conference call. In the press release they said: “As announced last month, Graphite Bio has initiated a process to evaluate strategic alternatives that may result in changes to our business strategy. We are working expeditiously to complete this strategic review and look forward to providing an update in the future when appropriate.”

So we still don’t know what they are going to do. The company has unique, powerful technology, and they are continuing to research activities associated with their early-stage non-genotoxic conditioning program, with the goal of advancing toward one or more potential development candidates.

I don’t want to give up on them until after I can assess their new strategy. At the end of the year they had $283.6 million in cash to fund a new direction. GRPH is a Hold until the update call.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Pre-clinical

Probable time of first FDA approval:Unknown

Probable time of next financing:Unknown

Invitae (NVTA – $1.28) will integrate its genetic testing results with Aura, Epic Systems’ specialty diagnostics software suite that is widely used by many leading healthcare organizations. Invitae can streamline interactions with provider organizations in the Epic community, making test result information available in providers’ usual workflows so that it’s easier to use genetic insights to inform treatment decisions. One of Invitae’s real strengths is that they make it easier than competitors for doctors and patients to get value from the genetic tests.

In addition to their recent convertible bond deal with Deerfield, Invitae just partnered with them to advance genetics-based drug discovery and development in rare diseases. The partnership will leverage Invitae’s genetics and clinical data from millions of patients with Deerfield’s broad drug discovery and development expertise.

Deerfield’s head of genetics and genomics said: “Despite significant research efforts, there are thousands of rare diseases without a line of sight toward a viable therapeutic intervention. Invitae’s unique data and analytics capabilities position it to interrogate genetic effects on rare and many other diseases. With Deerfield’s extensive experience in rare diseases and drug discovery, we believe there is strong potential for this partnership to uncover valuable patient insights and create important therapies for a range of currently untreatable conditions.”

So the convertible financing actually was more meaningful than I thought. Deerfield is a great partner with heavyweight credentials on Wall Street. This will be a strong tailwind for higher stock prices. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

ScyNexis (SCYX – $1.81) rose 28.2% yesterday on a whopping 14.6 million shares after the CDC sounded alarms about the dangerous Candida auris fungus that has grown far more prevalent in the US since the start of the pandemic, particularly in hospitals. It was detected in more than half of all US states last year and infections more than tripled between 2019 and 2021.

Click for larger graphic

Click for larger graphic

In 2022, 2,377 cases were confirmed. Between 30% and 60% of people with Candida auris infections have died. The CDC said its resistance to current antifungal medications and its rapid spread make it an important threat to the healthcare system.

ScyNexis to the rescue! Ibrexafungerp kills Candida auris. We’ll see trial data in the first half of 2024, and I expect Emergency Use Authorization.

Guggenheim initiated coverage on ScyNexis with a Buy rating and an $8 target price. Buy SCYX under $2 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2023

Probable time of next financing: second half of 2023 or never

Biotech MegaShift

TG Therapeutics (TGTX – $14.91) got a curious report from the Institute for Clinical and Economic Review (ICER) questioning the price of Briumvi. ICER publishes cost-effectiveness reports on various drugs. They said to be cost-effective, TG should price it between $16,500 and $34.900. Really?

First, Briumvi is cheaper than all the competitors. According to ICER, every anti-CD20 antibody targeting multiple sclerosis is overpriced. Here’s the competition:

Click for larger graphic

Click for larger graphic

It’s obvious to us and to Big Pharma that this is going to be a blockbuster drug, Buy TGTX under $7 for a target price in a buyout of $25 or more now that the MS drug is approved.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Second half of 2023

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $158.93) restarts Friday Night Baseball, a weekly doubleheader, on April 7 for all Apple TV+ subscribers in 60 countries and regions with no local broadcast restrictions. Last season’s free games are no more – fans must subscribe (the US rate is $6.99 a month or $69 per year).

Apple has decided to spend $1 billion to produce movies for theaters. Silicon Valley rumors are potential films include Martin Scorsese’s Killers of the Flower Moon, Matthew Vaughn’s Argylle, and Ridley Scott’s Napoleon. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $78.76) said their subsidiary Kite’s Yescarta CAR T-cell therapy showed a statistically significant improvement in overall survival for initial treatment of relapsed/refractory large B-cell lymphoma. It is the first and only treatment in nearly 30 years to show statistically significant overall survival improvement in this class of patients. Yescarta led to a 2.5x increase in patients who were alive at two years and did not experience cancer progression or require the need for additional treatment. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $204.28) should benefit from the mediocre performance of TikTok CEO Shou Zi Chew in his Congressional testimony today. He focused on reasons to think TikTok is not sending data on its 150 million US users (half the population!) back to China. But that’s not the big problem.

The big problem is China’s ability to use TikTok to control the political narrative, sow racial discontent, and emphasize themes favorable to the Chinese government. It appeared from the questions that enough Congress-people got it. It looks like TikTok might be banned or sold to a US company.

Morgan Stanley raised META from Equal Weight to Overweight with a $250 target price. KeyBanc jumped on the bandwagon, raising from Sector Weight to Overweight.

META is a Buy under $150 for a $400 target in 2024.

SoftBank (SFTBY – $18.83) expects Colombian delivery app Rappi Inc. to go public as soon as the end of this year or early next if global markets stabilize.

Meanwhile, ARM ltd. is raising prices for its chip designs as the SoftBank-owned group aims to boost revenues ahead of its hotly anticipated initial public offering in New York later this year. Masayoshi Son is ready for the next leg up. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Other Tech

Rocket Lab USA (RKLB – $3.85) said their Rutherford rocket engines cope very well with a dip in the ocean. This engine was plucked from the water in a marine recovery mission and it performed flawlessly in a full duration hot fire. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Inflation MegaShift

Gold ($2000.50) closed above the $2K mark for the first time in years. Chinese gold demand surged again in February as their economy continues to rebound from their stupid government-imposed COVID policies. Gold withdrawals from the Shanghai Gold Exchange totaled 169 tons in February due to strong wholesale demand. Withdrawals were up by 30 tons from January and by a healthy 76 tons year-over-year. It was the strongest February for wholesale gold demand since 2014.

The fractal dimension is moving quickly towards the 55 level that signals a real trend is underway. A trend that starts from a new high is going to be huge.

Miners & Related

First Majestic (AG – $6.47) was hit after they temporarily suspended operations at the Jerritt Canyon gold mine, citing higher than expected costs. They said that ever since their acquisition of Jerritt Canyon in April 2021, they have tried to raise underground mining rates in order to sustainably feed the processing plant at a minimum of 3.000 tons per day in order to generate free cash flow.

But: “Despite these efforts, mining rates have remained below this threshold and cash costs per ounce have remained higher than anticipated primarily due to ongoing challenges such as contractor inefficiencies and high costs, inflationary cost pressures, lower than expected head grades and multiple extreme weather events affecting northern Nevada, which have compounded conditions and caused material headwinds for the operation.”

They will process about 45,000 metric tons of above-ground stockpiles through the plant during the suspension, and will continue exploration activities throughout 2023.

They increased their stock buyback program to up to five million shares or about 1.83% of the outstanding stock. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $28,413.09) took off as the bank problems multiplied, just as it should. It is headed for a quarterly gain bigger than any since the start of 2021, the year when it went on to hit an all-time high. The $300 billion increase in the Federal Reserve’s balance sheet last week — part of its efforts to support liquidity in the US banking sector — is very positive for risk assets and has aided both cryptocurrencies and gold.

Click for larger graphic

Click for larger graphic

But stupidity persists. Former Coinbase Chief Technology Officer Balaji Srinivasan bet bitcoin will hit $1 million by June 17 because of a rapid devaluation of the US dollar. He’s going to lose – or if he wins, his $1 million will buy him a dozen eggs.

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

The Grayscale Bitcoin Trust (GBTC- $16.10) conversion to an exchange-traded fund could happen soon, as the judges in Grayscale’s suit against the SEC seemed pretty sympathetic. That would close most of the ~37% discount overnight. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

International & Other Recommendations

It is important to hold some non-US assets, especially in China.

Acreage Holdings (ACRDF – $0.80) gain delayed releasing its December quarter results. This time they will tell us when they’ll report “in due course.” Yeah, right. How about “never?” Does “never” work for you?

They have final approval to be acquired by Canopy Growth, so why would they bother reporting? ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

Oil – $69.22

Crude oil slumped to $64.12 intraday on Monday, its lowest level in nearly two years amid worries over global demand and a rally in the dollar. But as we approach the end of the quarter, global oil inventories are finally starting to turn the corner. The Energy Information Administration’s oil storage report yesterday was the most supportive report for the year with total liquids declining by 10.4 million barrels.

Click for larger graphic h/t HFI Research

Demand for gasoline and jet fuel will be stronger than in 2022. Gasoline storage is currently at the lowest level for this time of the year in recent years.

Click for larger graphic h/t HFI Research

Click for larger graphic h/t HFI Research

The July 2026 Crude Oil Futures (CLN26.NYM – $62.71) are a Buy under $65 for a $200+ target. Only buy futures for all cash; do not use margin.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $26.60) is a Buy under $36 for an $80+ target.

EQT (EQT – $29.53) languished as natural gas fell to a one-month low today on warmer weather forecasts. This has been an unusually warm winter, even though a Federal report showed an expected storage withdrawal that was bigger than usual for this time of year because cold weather last week boosted demand for natgas for heating.

Plus, worries that the Freeport LNG export plant in Texas was canceling cargoes and could take longer than previously expected to return to full service weighed on futures prices even though the amount of gas flowing to all big US liquefied natural gas export plants was on track to hit a record high this month.

We’re in the “shoulder season” between natural gas demand for winter heating and demand for summer electricity production to power air conditioners. We own EQT because they are the largest and one of the lowest-cost producers of the least-polluting fuel until Gen IV nuclear takes over in 15 to 20 years. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

Absolutely the best guitar solo ever made in the history of rock music?

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

Your understanding “too small to not fail” Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.57) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $7.55) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $10.08) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.95) – Buy under $7, hold a long time

Invitae (NVTA – $1.28) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.54) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.81) – Buy under $3, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $14.91) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $158.93 ) – Buy under $150 for new iPhones

Corning (GLW – $32.66) – Buy under $33, target price $60

Gilead Sciences (GILD – $78.76) – Buy under $80, target price $120

Meta (META – $204.28) – Buy under $250, target price $400

SoftBank (SFTBY – $18.83) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $41.35) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $15.94) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $32.02) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $5.19) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.85) – Buy under $13, target price $30+

Velo3D (VLD – $2.17) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Hold

Bag of Junk Silver – ($23.26) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $27.45) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $31.78) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.85) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $29.40) – Buy under $30, target price $50

Coeur Mining (CDE – $3.27) – Buy under $5, target price $20

First Majestic Mining (AG – $6.47) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.33) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.63) – Buy under $10, target price $25

Sprott Inc. (SII – $36.20) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $28,413.09) – Buy

Grayscale Bitcoin Trust (GBTC – $16.10) – Buy

Ethereum (ETH-USD – $1,817.01) – Buy

Grayscale Ethereum Trust (ETHE – $8.31) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.98) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $26.04) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $14.23) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $30.31) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.80) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.05) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $62.71) – Buy under $65; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $26.60) – Buy under $36; $80+ target

EQT (EQT – $29.53) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.10) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Akebia Biotherapeutics (AKBA – $0.69) – Hold for FDA decision

Arch Therapeutics (ARTH – $4.25) – Hold for buyout

Graphite Bio (GRPH – $2.32) – Hold until they resolve the clinical hold

Sell

Algernon Pharmaceuticals (AGNPF – $0.31)

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

MM – On Scyx – can the Emergency Use Authorization be issued at any time? Like Now.

Good point, Roger! That is exactly the reason EUA’s exist.

Yes.

Michael, You are bullish on NVTA, and have been for a while. Why do others not see the value? What are they saying…

In case you forgot, I am an internist and will tell you the true story of genetic testing. In day to day medical practice, genetic testing is a very tiny aspect of care. Before NVTA, the main users of genetic testing, oncologists had their own genetic testing labs. In only a few cases does it really make a difference in treatment. Most cancer patients get the same chemo treatment, and only a few mutations have specific targeted treatments. I discussed this 1-2 years ago, before NVTA stock plunged to these levels. Bad financial management is an additional nail in the coffin. The stock is a lottery ticket with a high chance of complete failure to offset pie-in-the-sky Amazon projections.

Wish I had seen this earlier and sold when it reached as high as $60.

Well, that’s what makes markets. We’ll see.

No doubt you missed investing in REGN with your genetics “background”. You prescribing any of their drugs now? Where do you think they came from?

https://www.regeneron.com/about/perspectives/more-genomics-less-fear

Reply to JGMD

To JGMD

This future, ours, is a future of many, of all, of hundreds of billions; it is a future of opportunity: “Because the answer is in the genes.” Thus, the transformative effect of genomics in medicine is today unquestionable.

No, the answer is in the EXPRESSION of genes, a field called epigenetics. This takes into account nutritional, lifestyle, environmental factors which determine the phenotype. The genotype is the raw DNA, a starting point. But the clinically relevant factor is the phenotype. In practice, a small percentage of cases do better with targeted drugs based on genotype. These are handled by specialists, not by primary care MD’s like myself. Based on this, NVTA is a small niche company with high risk. I was intrigued by BIOC for liquid biopsy, but they did poorly even with their excellent technology in this niche field. NVTA and BIOC are both small niche players. BIOC is more interesting for their technology, but NVTA is merely a platform for cataloging of tests which are available elsewhere.

MM – You recently commented that VLD “was upgraded by Morgan Stanley to a Strong Buy with a 12-month target price of $27″. Can you provide a link to the corresponding source document?

Haven’t found it.

INO – now below $1 at a market cap of $250M. The CEO’s YE earnings call comment that discussions are underway regarding the next steps for their candidates with the greatest potential for impact didn’t seem to impress anyone that they have any kind of a clear go forward strategy.

Likely headed to the sub $100M valuation neighborhood where APTO, ARCH, BLPH, MDNA & SCYX all reside, which means there’s still a sizable haircut to come…

On March 20, I posted: “Have a look at ACHV. On the quarterly call last week, they said they have results of two major trials coming up in Q2. In the first half of Q2 (by mid-May) they will have results of their Phase 2 trial in e-cigarette nicotine vaping.” It closed that day at 4.38 and at 5.55 today.

On March 22, I bought AG at 5.88 and posted about it. Today it closed at 6.96. I hope some here followed my suggestions.

The value of New World Investor is found in the Mastermind’s comments. I thank Michael Murphy for having sufficiently thick skin to tolerate the criticism he sometimes receives here. Murphy’s back and forth with Michael in Asheville are worth their weight in gold.

Chris, thanks for the heads up ACHV,this one might make some money sooner than later.

I’ll take BTC thank you. ACHV is jumping for sure but I always like to pull up a 5 yr chart for perspective.

Well, Michael, on December 29, you wrote: “Anyone care to share their picks of 2023? I’ll take TSLA and BTC.” TSLA closed that day at 121 and is now up 67% to 196. BTC has gone up 56% from 16000 to 28480.

That same day (December 29) I replied sharing ACHV which closed that day at 2.55. Now it’s up 266% to 6.80.

I wouldn’t have bought ACHV 5 years ago, but December was a great time to buy.

Yeah that has turned out to be a great pick but its history is … well you know. I don’t really understand the company and negative PEs are a no no for me right now.

I wasn’t intending to compare picks, I was commenting on comments being worth their weight in gold (I’d prefer BTC).

SCYX is REALLY catching a bid. 38 million traded. I really hate to chase but …

SCYX up 80% pre-market

https://markets.businessinsider.com/news/stocks/gsk-scynexis-ink-exclusive-licence-agreement-for-brexafemme-1032203166

Nice jump but pull up a 5 yr chart for perspective.

Exactly. I’m still massively underwater as I’m sure many are……

SCYX – $90M upfront milestone is about $2.60/share. FY 2022 Q4 (exp. $ -0.44) / Full-year earnings (exp. ~$1.54) due out tomorrow morning before the bell. Not sure if this initial milestone shows up in 2022Q4 or 2023Q1. In any case up to $503M (~ $14/share on ~35M shares over 5-20 years [take your pick] in additional developmental and sales milestones. So SCYX should be able to have a positive EPS for some time to come. Pick your multiple, pick your target price.

Also, FY 2023 earnings estimate $ -0.80 to -1.00 / share (?) before any of the new milestone revenue. As they continue to scale, the earnings should be tracking to eventually go positive on their own.

$90 million in the June quarter financials.

The Radar Report for 3.30.23 is posted. New Buy!