Dear New World Investor:

Federal Reserve Governor Philip Jefferson, President Biden’s nominee to be Vice Chair of the Fed’s Board of Governors, and Philadelphia Fed President Patrick Harker suggested yesterday that the Fed could pause rate hikes at its next policy meeting on June 13-14.

But Wednesday’s Job Opening and Labor Turnover Survey (JOLTs report) showed 10.1 million job openings at the end of April, an increase from March’s 9.8 million and well above the consensus expectation for 9.4 million. So St. Louis Fed President Jim Bullard said he is looking for two more rate hikes, Dallas Fed President Lorie Logan said a pause is not in order right now, and Boston Fed President Susan Collins suggested the Fed may be at or near a pause, but reserved the option to make decisions meeting by meeting given the data at the time.

Meanwhile, President Biden and House Majority Leader Kevin McCarthy arrived at a debt limit deal (Surprise! Not.) that includes an end to student loan deferments in early September, which will reduce consumer spending by an average of $383 per month by those with loans. In other words, consumer spending is about to tank and Fed Chairman Powell knows it. I continue to believe they will announce a pause on June 14.

Market Outlook

The S&P 500 added 1.7% since last Thursday as the US avoided default. Whew! That was close – not. The Index is up 9.9% year-to-date. The Nasdaq Composite gained 3.2% as the AI rally rolled on. It is up 25.2% for the year. Even the small-cap Russell 2000 gained 0.8% and is back in the black, up 0.4% in 2023.

Latest news from the most-hated bull market ever: Hedge funds and other speculators have built up their bets that the S&P 500 will decline, marking their most-bearish positioning since 2007 when measured as a percent of open futures-market interest, according to data compiled by Bespoke Investment Group.

The fractal dimension continues to drop towards the 55 level, signaling a new uptrend is underway. One more good week could do it.

Top 5

Changes this week: None

Near-Term – chronological order

EQT EQT –natural gas price rebound

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

BLPH Phase 3 results mid-2023

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

Economy

The Atlanta Fed’s GDPNow model has pulled back to +2.0% for June quarter real GDP growth due to weakness in real personal consumption expenditures.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, June 2

GILD – Gilead Sciences – Through 6/6 – 30 presentations at ASCO

May Payrolls – 8:30am – +190,000 expected; was +253,000 in April

CMPS – Compass Pathways – 8:30am – Annual meeting

Saturday, June 3

NVTA – Invitae – 1:30pm – ASCO Presentation

Sunday, June 4

OPEC+ Meeting

Monday, June 5

CMPS – Compass Pathways – Unspec. – ASCO Presentation

AAPL – Apple – 1:00pm – Worldwide Developers Conference (WWDC) all week

NVTA – Invitae – 2:00pm – ASCO Presentation

Tuesday, June 6

QUIK – QuickLogic – 4:10pm – Stifel Cross Sector Insight Conference

FSLY – Fastly – 5:00pm – William Blair Growth Stock Conference

Wednesday, June 7

RKLB – Rocket Lab – Unspec – Stifel Cross Sector Insight Conference

GILD- Gilead Sciences – 11:00am – Jefferies Healthcare Conference

NVTA – Invitae – 1:40pm – William Blair Growth Stock Conference

Thursday, June 8

APTO – Aptose Therapeutics – Through 6/15 – European Hematology Association

FSLY – Fastly – 2:20pm – BofA Global Technology Conference

CMPS – Compass Pathways – 3:30pm – Jefferies Healthcare Conference

VLD – Velo3D – 4:00pm – Annual meeting

Friday, June 9

INO – Inovio – 8:00am – Jefferies Healthcare Conference

Short Interest – After the close

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Click for larger graphic

Click for larger graphic

Apple (AAPL – $180.99) starts the week-long Worldwide Developers Conference this Monday with a keynote address at 1:00pm EDT. The WWDC23 website now features the sentence “Code new worlds.” That almost certainly means they will showcase the long-awaited Apple Reality Pro augmented reality (AR) and virtual reality (VR) headset.

It will be priced at around $2.995 and include high-resolution displays, a dozen or more color pass-through cameras, one or maybe two powerful M2 processors, and an external battery pack to keep the headset light. It will have a new xrOS operating system, which may allow users to create AR apps using Siri without coding knowledge. I expect a December quarter launch in time to make this the prestige holiday gift. The stock hit a 52-week high today. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $30.87) presented at the Bernstein 39th Annual Strategic Decisions Conference (VIDEO HERE and TRANSCRIPT HERE). CEO Wendell Weeks did a great job of driving home four points:

* * The “More Corning” program to drive more Corning value into products like autos that aren’t growing allows them to steadily grow revenues

* * With the pandemic over, they are bringing down inventory levels, cutting costs, and raising prices

* * They are finding ways to use their technology in new areas like AI, solar, and biotech

* * They will continue to deliver increasing dividends and stock buybacks

Click for larger graphic

GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2024.

Gilead Sciences (GILD – $76.51) said the Committee for Medicinal Products for Human Use of the European Medicines Agency granted a positive opinion for the use of Veklury (remdesivir) in COVID-19 patients with severe renal impairment, including those on dialysis. Veklury will become the first and only authorized antiviral COVID-19 treatment that can be used across all stages of renal disease.

In Europe, approximately 75 million people suffer from chronic kidney disease (CKD). Patients with advanced CKD or end stage kidney disease represent a population that is highly vulnerable to COVID-19. They are at increased risk of morbidity and mortality from COVID-19, with mortality rates as high as 25%, and currently have limited treatment options that are safe and effective.GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $272.61) finished its latest round of layoffs last Friday, bringing the total to 21,000 since November. At yesterday’s annual meeting, Zuckerberg repeated that this is their “Year of Efficiency” with fewer layoffs but also less hiring in the near future. He also said that developing AI-efficient tools will improve productivity. Wall Street loves that.

He emphasized that they are still investing in the metaverse. Wall Street hates that, but they don’t understand the ways in which AI is inextricably linked with any company’s metaverse plans. They’ll figure it out in a couple of years. Meta is going to join the trillion-dollar market cap club thanks to the metaverse.

Today they said the Meta Quest 3 is coming this fall and cut prices for Meta Quest 2 as low as $299.99. The Quest 3 has higher resolution, stronger performance, breakthrough Meta Reality technology, and a slimmer, more comfortable form factor.

Nvidia announced its new supercomputer to enable the next generation of generative AI applications thanks to its bigger memory size (500x the current computer) and larger-scale model capabilities. Google, Meta, and Microsoft will be the first users when it ships around the end of the year.

The Silicon Valley rumor mill is saying Meta’s Instagram will introduce a Twitter rival this summer. The new app is reportedly being beta tested by celebrities and influencers, and has been secretly available to some creators for months. It is separate from Instagram but allows people to connect to their Instagram account.

The EU fined Meta $1.3 billion for privacy violations, the biggest fine ever levied by the group. That’s only 18 days of Meta’s pretax profits. LOL. The stock hit a 52-week high today. META is a Buy under $150 for a $400 target in 2024.

SoftBank (SFTBY – $20.98) and Nvidia announced a generative AI platform collaboration. Nvidia tried to buy ARM plc from Softbank but the bureaucrats blocked it. Now SoftBank has filed to take ARM public at a $40 billion valuation.

Most of ARM’s sales are in mobile phones, but part is for data centers, where they compete with Intel. At the Computex trade show in Taiwan, ARM CEO Rene Haas announced the Cortex-X4 as the fastest CPU it has made so far, with a focus on enabling artificial intelligence and machine learning-based apps. They are targeting on-device and small-scale AI applications like Amazon’s Alexa voice assistant and smart traffic light management.

If ARM runs up after the initial public offering, Softbank should soar. Each additional $10 billion of ARM valuation is worth about $3 a share on SoftBank’s price. As this article on SeekingAlpha said, SoftBank Group: Significantly De-Risked And Positioned Well For The Future. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $14.48) Chief Operating Officer Ajay Marathe, wrote about Bringing Operational Excellence to Enovix based on his 23 years at Advanced Micro Devices. ENVX is a Buy up to $13 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

PagerDuty (PD – $27.75) reported April first quarter results this afternoon. Revenues were up 20.9% from last year to $103.2 million, right on the $102.9 million estimate. Pro forma earnings of 20¢ a share more than doubled the 9¢ estimate as their profit margin expanded. Total paid customers were essentially flat at 15,089 compared to 15,040 a year ago. But customers with annual recurring revenue over $100,000 increased from 655 to 764. The dollar-based net retention rate of 116% compared to 126% last year.

On the conference call (ZOOM HERE and TRANSCRIPT HERE and SLIDES HERE), they guided for revenue of $103.5 million to $105.5 million, representing a growth rate of 15% to 17% year-over-year but below the $108.6 million estimate. They expect pro forma earning of 10¢ to 11¢ a share, above the 9¢ estimate.

For the full year, they guided for revenues of $425.0 million to $430.0 million, down from $446.0 million to $452.0 million. That’s a growth rate of 15% to 16%, but below the $448.3 million estimate. But they raised earnings guidance from 45¢ to 50¢ per share up to 60¢ to 65¢. That’s way ahead of the 44¢ estimate.

So why did the stock drop 15% in after-hours trading? Because the automated bots read “revenue guidance reduced” and shorted the stock for a one-day trade. Don’t play their game. PD guided revenues conservatively and obviously has expenses under control. This is a really well-run company. They had free cash flow of $20.8 million and ended the quarter with $495.1 million in cash.

PD is a Strong Buy on Friday’s dip and a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Rocket Lab USA (RKLB – $4.74) successfully completed the second of the two dedicated Electron launches to deploy the TROPICS constellation of tropical cyclone monitoring satellites for NASA. This was their fifth mission for 2023 and 37th Electron mission overall. It brings the total number of satellites launched to orbit by Rocket Lab to 163.

They have positioned themselves as the cost-effective, reliable supplier in the small satellite launch market. They just won a contract to launch the LEO 3 satellite for global satellite operator Telesat (TSAT) on an Electron mission scheduled for the September quarter. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $1.09) said the FDA denied its appeal of the Complete Response Letter for vadadustat, but guided them on how to resubmit the New Drug Application without any new clinical trials for chronic kidney disease patients dependent on dialysis.

On a conference call (AUDIO HERE), management said the FDA staffers indicated that the risk of vascular access thrombosis (VAT), a reason for the higher risk of thromboembolic events, is not large and can be managed as a labeling issue.

The FDA said the risk of drug-induced liver injury appears modest in intensity and is potentially manageable with appropriate monitoring that is routine among dialysis patients. They said data from Japan would be important to assess this risk further. Based on the safety data Akebia has received from its partner in Japan, Mitsubishi Tanabe Pharma, there have been no reports of drug-induced liver injury in the more than two years that vadadustat has been on the market in Japan.

The regulators suggested that the company request a Type A meeting with the Office of New Drugs. Management said they will do so as soon as possible and plans to resubmit the NDA before yearend. They expect a six-month review, so vadadustat should launch in mid-2024.

The good news was enough to make Piper Sandler upgrade the stock from Neutral to Overweight. They said: “Given this news, we are layering the US vadadustat opportunity back into our model with end-user revenue approaching $375 million by fiscal year 2028,” The stock also got a strong recommendation on Seeking Alpha: Buy This Undervalued Stock At Just 77% Of Revenue.

I moved Akebia to a Hold after the Complete Response Letter because I thought the drug would eventually be approved. That was the right call, so I am moving AKBA back to a Buy under $2 with a $20 target after vadadustat is approved.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Auryxia approved; Vadadustat NDA to be refiled

Probable time of next FDA approval: First half of 2024

Probable time of next financing: Unknown

Aptose Biosciences (APTO – $0.43) will provide a clinical update on Saturday, June 10, at 12:00pm EDT from the International Congress of the European Hematology Association in Frankfurt.

They signed a a Committed Equity Facility that gives them the right, at their option without obligation, to sell up to $25 million of stock over the next 24 months to an institutional investor, Keystone Capital Partners. APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Compass Pathways (CMPS – $7.59) will present results at ASCO on Monday from an open label Phase 2 trial of COMP360 for depression in cancer patients. About 15% of patients with cancer experience major depression, which is associated with lower treatment adherence and reduced quality of life. Yet, oncologists often feel inadequate to address mental health issues, and many treatments have limited success in treating depression.

In the longest clinical study of psilocybin ever conducted, more than half (16 of 28) of the patients demonstrated remission of depression at 18 months after a single 25-milligram dose of COMP360 psilocybin plus psychological support. The results were published in April in JAMA Oncology. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2023

Invitae (NVTA – $1.06) will make three presentations and show seven posters at the American Society of Clinical Oncology (ASCO) annual meeting. Saturday will showcase the benefits of germline genetic testing for lung cancer patients. A retrospective study of over 7,000 lung cancer patients who completed germline genetic testing showed that 14.9% of patients in this cohort had pathogenic germline variants, nearly all of which were clinically actionable.

A Monday presentation will show genetic testing use among patients for whom universal testing is currently recommended were as follows: male breast cancer (50%), ovarian cancer (38.6%), female breast cancer (26%), pancreatic cancer (5.6%), and colorectal cancer (5.6%). Additionally, results showed that compared to non-Hispanic whites, patients from other racial/ethnic groups received less testing without improvement over time, underscoring the need to improve access to genetic testing for underserved groups.

Invitae will be added to the Russell 3000 Index on June 26. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

TG Therapeutics (TGTX – $27.42), as expected, got European Commission approval of Briumvi to treat adult patients with relapsing forms of multiple sclerosis in all EU member states plus Iceland, Norway and Liechtenstein. Hold TGTX for a target price in a buyout of $25 or more now that the MS drug is approved.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Second half of 2023

Inflation MegaShift

Gold ($1,994.20) bounced off $1,930 back towards $2,000. The fractal dimension still says an uptrend is underway.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $26,887.37) is right in the middle of a $26,000 to $28,000 trading range. We still could see a quick drop to $25,000 and an equally quick recovery, but I continue to think the next move is well over $30,000.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $14.05) is the cheapest, easiest way to buy bitcoin. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $70.05

Oil prices dropped yesterday as weak Chinese manufacturing data increased fears over future demand from the world’s largest crude oil importer. My not-so-brave prediction: China will use more oil every year for the next 10 years.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

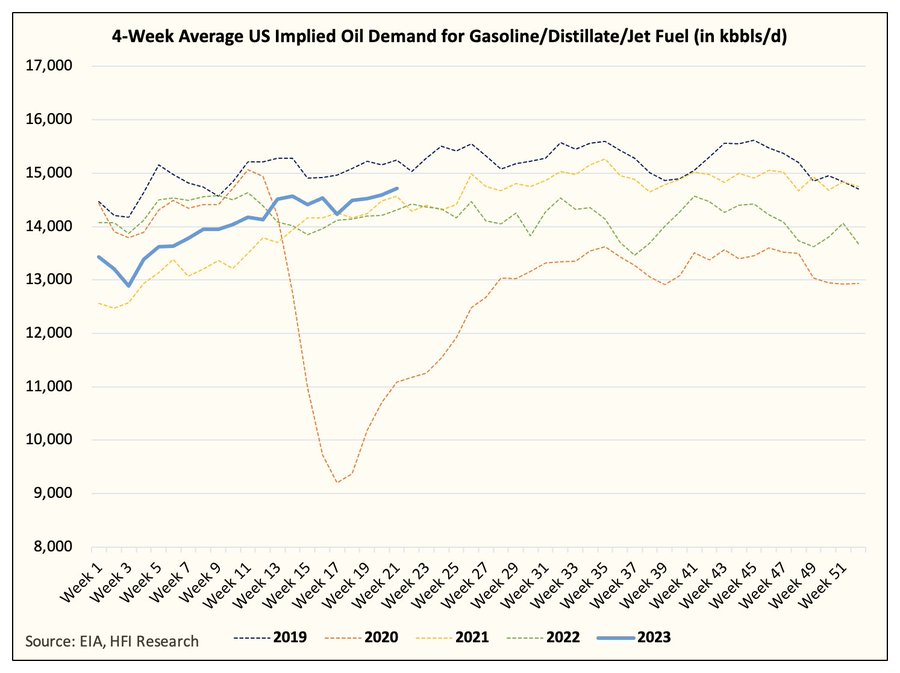

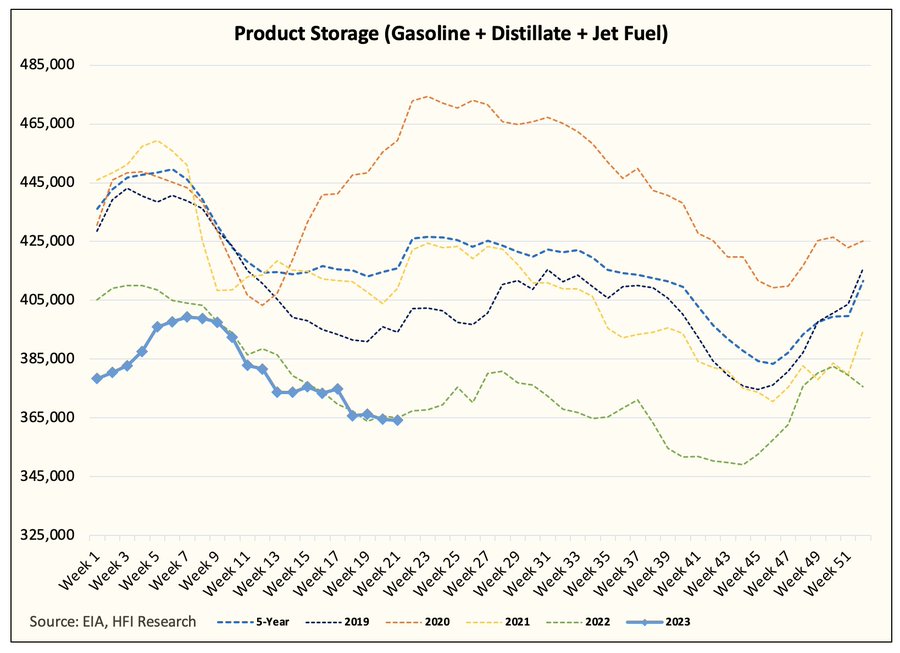

In March, the US sold more petroleum abroad than ever before, highlighting how exports are increasingly shaping the American oil-and-gas industry. Foreign buyers hoovered up about 11.27 million barrels a day.

US oil demand continues to trend in the right direction.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

With demand where it is, if US oil demand continues to trend higher, refinery throughput will need to materially increase. If not, then you will see product storage trend lower versus 2022’s increase.

Click for larger graphic h/t @HFI_Research

The July 2026 Crude Oil Futures (CLN26.NYM – $62.11) are a Buy under $65 for a $200+ target. Only buy futures for all cash; do not use margin.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $27.29) is a Buy under $36 for an $80+ target.

Energy Fuels (UUUU – $6.32) jumped as uranium rose 20% to $59 after Diablo Canyon ordered enough to fill one reactor. At the same time, Namibia is considering taking minority stakes in mining and petroleum production companies amid increasing concerns over local ownership of valuable resources, aka “How to kill your mining industry.” Namibia is Africa’s biggest producers of uranium. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

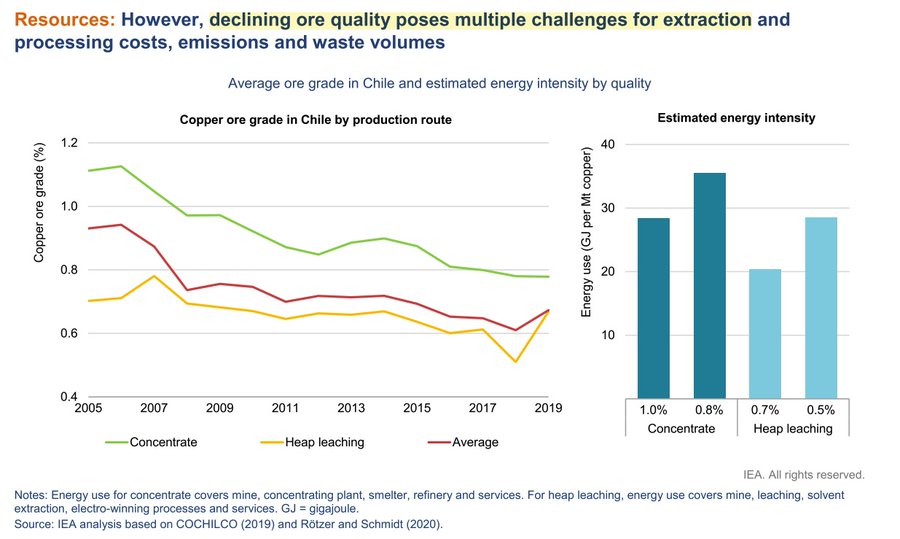

Freeport McMoRan (FCX – $35.47) weakened as copper prices hit a four-month low. But inventories are almost gone, even if China doesn’t grow (they will).

At the same time, there is a declining ore problem in Chile, a major producer. Copper ore grades have declined from ~0.90% to ~0.60%. Declining ore grades create higher inflationary cycles. Lower ore grades means more mining, extraction, fuel demand, energy output, water demand, and labor costs per pound.

Click for larger graphic

Click for larger graphic

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

Your following air-gen Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $180.99) – Buy under $150 for new iPhones

Corning (GLW – $30.87) – Buy under $33, target price $60

Gilead Sciences (GILD – $76.51) – Buy under $80, target price $120

Meta (META – $272.61) – Buy under $250, target price $400

SoftBank (SFTBY – $20.98) – Buy under $25, target price $50

Other Tech

Enovix (ENVX – $14.48) – Buy under $13; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $43.92) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $16.34) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $27.75) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $5.90) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.74) – Buy under $13, target price $30+

Velo3D (VLD – $1.89) – Buy under $6, target price $50

$20-for-$1

Akebia Biotherapeutics (AKBA – $1.09) – Buy under $2, target $20

Aptose Biosciences (APTO – $0.43) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $6.89) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $7.59) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.57) – Buy under $7, hold a long time

Invitae (NVTA – $1.06) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.61) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.62) – Buy under $2.50, target price $20, then $50

Inflation

A Short-Sale or REO House – ($447,000) – Hold

Bag of Junk Silver – ($23.96) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $27.68) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $31.52) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.87) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $27.78) – Buy under $30, target price $50

Coeur Mining (CDE – $3.12) – Buy under $5, target price $20

First Majestic Mining (AG – $6.02) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.28) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.49) – Buy under $10, target price $25

Sprott Inc. (SII – $34.43) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $26,887.37) – Buy

Grayscale Bitcoin Trust (GBTC – $14.05) – Buy

Ethereum (ETH-USD – $1,868.99) – Buy

Grayscale Ethereum Trust (ETHE – $8.34) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $62.11) – Buy under $65; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $27.29) – Buy under $36; $80+ target

EQT (EQT – $35.10) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.32) – Buy under $8; $30 target

Freeport McMoRan (FCX – $35.47) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $28.67) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $23.28) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.00) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $26.19) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.45) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $0.90) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $3.00) – Hold for buyout

Graphite Bio (GRPH – $2.92) – Hold until they update their strategy

TG Therapeutics (TGTX – $27.42) – Hold for buyout at $25+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

#2

MM (or anyone). Given a one-year horizon, from current levels, which of these three is the strongest buy: INO, NVTA, AKBA?

AKBA is by far the safest, although approval may take a little longer than 1 year. NVTA is irrelevant to most medical practitioners, as I have said. (Things like TGTX and APTO deal with uncommon diseases, but TGTX revenues are high per patient. APTO will have high revenues, but financials are horrible and may kill it before it gets approval.) NVTA has had poor uptake by doctors, and with low revenues per test, it will continue to be a bust, leading to bankruptcy.

Thank you for your reply. INO, in my estimation, has potential, but probably not within a 1-year time frame; however, trading in the 60 cents range it appears to be way oversold. I have read most, if not all, of your past comments on NVTA. Your take, given you are a practicing physician, offers a very different perspective than that of others.

My MD uses the tests like NVTA offers and uses them to prescribe preventive medicines for her patients which I take.

This the way doctors who want to keep their patients well instead just giving them drugs after they get sick.

These are generally holistic doctors. I love these doctors

Thank you for your observation about how NVTA’s test may be used.

You have an excellent MD. But she is in a minority. Most MD’s do little preventative medicine. They just prescribe drugs for HBP, diabetes, etc. For the most basic things like diet, few MD’s sit down and discuss this with their patients. Most nutritionists have been indoctrinated with politically correct diets such as moderate/high complex carb, low fat diets, which mainly serve the interests of grain manufacturers. This is an agenda to show that diets and nutrition aren’t effective and therefore drugs are needed for nearly every medical problem.

@JGMD

thanks for your assessment, I gave up on NWI Kidney drugs, I recall 2 that were delayed or never worked for one reason or another.

INO looks like another VICL although the mode of plasmid delivery is different the outcome in humans seems to be the same promising but that’s all.

I did 5x on NVTA wish i had sold it all but still did well but is dead $ going forward.

I like both TGTX and APTO.

I believe TGTX has more room to grow sales 3-5 years out and if they can do the $B+ can grow nicely.

Do you think APTO has $B+ sales potential if funded through FDA approval and is able to get sales traction.?

The other one from hear all be it years ago, that i have continued to fallow and re-entered in 2021. is GERN and my napkin # at $1B+ with Huge fallow on if underling mec/of/action is as disease modifying as first outcome seems to imply.

thanks

dyodd

APTO may have good drugs, but their financial situation is terrible. The trials are going at a snail’s pace. I have no clue whether they will get approval before they go BK. Follow Carol J on YMB who seems to be knowledgeable about these matters.

OK thanks for the reply, so in reference to APTO when you say “(Things like TGTX and APTO deal with uncommon diseases, but TGTX revenues are high per patient. APTO will have high revenues, but financials are horrible and may kill it before it gets approval.)” you believe that APTO will go BK and never get approval.

Carol J. from YMB clams “I am a clinical research specialist that has worked in the clinical research/drug development for 25 years.ect— ” self proclaimed BEAR with a short prospective and years on YMB warning other investors about the danger of APTO.

So my question “Do you think APTO has $B+ sales potential if funded through FDA approval and is able to get sales traction.?” will not be resolved on this thread.

I say yes to CG806 and i dont know to HM4323but thanks anyway.

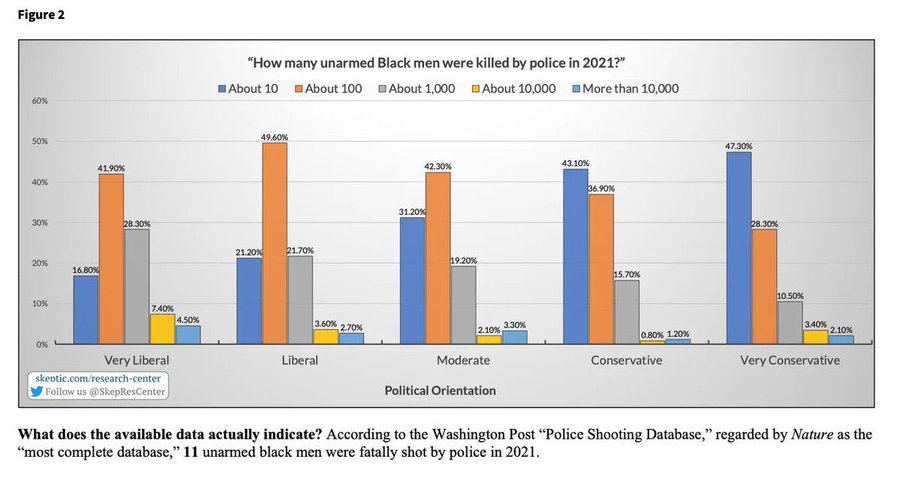

The USA is about 59% white and 12.5% black. In other words, there are nearly 5 times as many white people as black people. “How many unarmed black men were killed by police in 2021?” According to the WAPO database, which may be the best, but is admittedly incomplete, the number is 11. Were there anywhere near 55 unarmed white people killed by police in 2021?

According to that same database:

How many unarmed white men were killed by police in 2021? 7

How many unarmed black men were killed by police in 2015? 35

How many unarmed white men were killed by police in 2015? 30

How many unarmed black men were killed by police in 2016? 19

How many unarmed white men were killed by police in 2016? 27

How many unarmed black men were killed by police in 2017? 20

How many unarmed white men were killed by police in 2017? 24

How many unarmed black men were killed by police in 2018?

If it is not clear to you, these data show that police disproportionately kill unarmed black men compared to unarmed white men.

These data also indicate that police are getting better at not killing unarmed men, but the racial disparity persists.

How many unarmed black men were killed by police in 2022? 12

How many unarmed white men were killed by police in 2022? 16

How many unarmed black men were killed by police so far this year? 5

How many unarmed white men were killed by police so far this year? 6

When you include reporting on police killings of men where it is not known whether the victims were armed, undetermined or unarmed, the numbers increase substantially but still are disproportionately skewed towards black men.

Read the important disclaimer about the data, but also look at the numbers for yourself:

https://www.washingtonpost.com/graphics/investigations/police-shootings-database/

One other note, the database only includes people killed by police. It does not include all the unarmed people shot, but not killed by police, nor those who were otherwise improperly treated. Love your neighbor as yourself.

Perhaps the racial disparity exists because there are more black men whose behavior puts them in confrontational situations with the police. This has nothing to do with the 5:1 ratio of whites to blacks in the population at large. Consider, for example, that the ratio of NBA black players to white players is about 5:1 (a total reversal from that of the population at large.) In order to make sense of the numbers you quote, the key missing piece is the prevalence of the situation. In other words, how many unarmed white/black men were confronted by the police? Of those, what is the “killed” ratio for each group?

The problem is not that the police are racists although like all people some are it is that they are trained to look at people as their enemy and anyone who breaks the law is scum and does not deserve any respect. We need to return to police walking the beats and getting to know people as human beings like themselves.

Should your analysis be based on total population or the population of black men with a criminal record vs white men with a criminal record?

Wow, our fearless leaders agreed to extend our debt ceiling. What choice did they have? Say no and start a depression bigger than 1929!!

But longer term, the debt keeps increasing, and then the depression is worse. This deal was a drop in the bucket. No, Chris, debt/GDP comparisons are ridiculous. All US administrations are bad. When responsible individuals or companies have reasonably low debt, they are using it for productive investment which will easily wipe out debt, paid off by greater output. Govt rarely makes good investments, and govt debt is mostly used to pay off welfare special interests at the expense of people who are not politically connected. Govt almost never reduces debt. Rare “exceptions” are when the deficit is reduced, but then the debt keeps increasing.

The Democrats voted to raise the debt limit 3 times under trump with no drama It is a miracle Biden got the Republicans to agree to not destroy the economy and credit rating of the USA without chopping medicare or social security

Goodbye BLPH

BLPH was another ticker first brought to my attention years ago by Biopub.co Fortunately, Biopub dropped its coverage of BLPH when it became apparent that BLPH’s future was too speculative to be investable. Someone above asked about INO, NVTA, AKBA. While there is a chance that any of those might go up, ACHV (also brought to my attention by Biopub) is a lock to gain 300 to 400% in the next year or two. I anticipate a doubling when a Big Pharma partner is announced and that could happen at any time. Varenicline (generic Chantix) with all its baggage still had $300M in sales last year. Imagine what a new effective smoking cessation drug WITHOUT the adverse side effects of varenicline will do. AND it proved effective in a recent Phase 2 for vaping.

BLPH- Yep… another one bites the dust, after ARTH and many many others. I do not think there is a problem with MM’s research/stockpicking skills per se. But, imho, he is very much out of synch with the business/financial cycle and may not have taken into account the ease with which lots of kooky ideas and garbage companies/initiatives may have found funding after 2009 and zero interest rates policies of the Fed, culminating with the post-Covid orgy, particularly in Biotech and Medtech. Tide has turned and most of these were swimming naked. An era of malinvestment has occurred, we are now dealing with the wreckage.

Speaking of which, how about NVTA? It is presenting at the moment but the chart looks awful and the stock is having nary a bounce despite copious promotional efforts.

Also a very disappointing conference call with no questions asked. We know nitric oxide works well in the hospital and worked in the INOpulse in Phase 2, so this was a real shocker. The problem must be in the device’s delivery of nitric oxide, but then why did it work in Phase 2?

Any reason to hold this stock?

Yes. If you don’t want to make money, keep holding. Otherwise, put your money in ACHV.

Does their product require surgery?

No, it’s a 3x/day pill to help one quit smoking.

You were savvy to get back in Dec 22 when the stock was $2. Now at over $6, it needs a good correction. Many of the Chantix trials showed a little better efficacy but more side effects compared to ACHV’s drug. ACHV’s natural extract is interesting. My experience is that natural treatments are safer but less effective than drug treatments for many conditions. The real commercial risk for ACHV is competition from cheaper generic Chantix, varenicline.

Plenty of successful Phase 2s end up as failures in Phase 3s. There are several reasons for this. As one moves from a small number of trial participants to a large number, there will be an increased number of trial sites. The careful attention to detail of those conducting the trials is likely to become diluted and the trial participants themselves are often not as carefully selected either. In a Phase 2, the few patients involved can be monitored more carefully by the few professionals involved. In a Phase 3, the large number of patients are often not monitored as well for compliance with trial protocols. The small size of a Phase 2 also can sometimes have professionals who are more motivated to hope for success of the product, whereas with a large number of professionals in a Phase 3, those conducting the trials may not be as motivated to strictly follow trial protocols. Also, of course, statistics can be more misleading when sample sizes are small. As sample sizes grow, benefits that might appear significant in a small sample, can become less significant in a large sample.

ENVX- I bot this MM’s idea and I think he may have finally found a winner. BUT, it has a ton of shorts. Are they right or is he? I respect the amount of research the Bears usually perform, a real necessity when your upside is finite and your potential loss infinite. However, I do not like the fact that, now that the Uptick Rule is no longer there, they can gang up against any stock and destroy it given the right circumstances.

Generally speaking, even when shorting for the long term, the Bears maintain a solid short term/daily attitude regarding their portfolio, a necessity given the huge risks involved.

So, for example, after a very decent week, when ENVX got close to $14, today, in a moderately up Nasdaq day, the stock is getting crushed down $1.47 or more than 10% so far on no news that I can see. Imho, the Bears are in charge today, they saw the chart painting a quasi double-top and started offering pieces at the open rapidly running all the stops to below $13. It is vital for them to keep the stock where it is and avoid any new highs above $15 where many of them would be forced to cover and push the shares even higher. Let’s see where this one closes.

Perma bear Bill Fleckenstein also likes ENVX so take that for what it’s worth. I took a flyer on 500 shares but happy to dump it on a moments notice. IMO if there is a better battery solution, TSLA will create it.

WSJ has an article today covering the very competitive EV battery market including Quantumscape, Bollore and Solid Power. Nio’s 5 minute battery swap is an interesting alternative to charging stations.

https://www.wsj.com/articles/the-leaders-in-the-race-to-build-a-better-ev-battery-11610706600?mod=article_inline

Thanks. As in any crowded field, success depends on who the backers are. Early stage Quantumscape has Bill Gates, although ENVX is beginning to commercialize. Even if ENVX is the most promising technology in production, how will it compete against companies like Tesla that have evolving solutions? Remember the Alamo (ARTH) with its superior AC5 that is near bankruptcy due to marketing failure.

MM? Please address ENVX in the context of the WSJ article. Thanks.

Today? Date of the article is January 21, 2021.

PLTR- My choice to play the AI mania. Breaking out today above $15. Next target $20.

Concur.

Thanks. Bought it today at $15.00 and change.

Also bought 1669 SOFI at $6.58 several days ago. Up 17 percent to date. Just FYI Kathy Woods is buying NVTA.

MM Do you expect apple will fall to below $150.00 from the current price of $180.00 ?

APTO – looks like the reverse split went thru:

“As a result of the Reverse Stock Split, every 15 Common Shares issued and outstanding were automatically reclassified into one new Common Share. No fractional Common Shares will be issued as a result of the Reverse Stock Split and shareholders will not receive any compensation in lieu thereof.”

So it sounds like my 1,000 shares became 66 shares and 2/3rd of a share vanishes into the air.

Yep, I saw that language in their 5/23 news release so adjusted my share position at the end of May to be divisible by 15 with no fractional shares.

You have to love that crap. Is anyone doubling down on it now?

Read Carol J’s YMB posts on APTO, and weep. She has been correct so far.

Carol J’s bearishness has been right in the macro sense but most of what she posts is complete BS & she comes across as little more that a paid message board shill. The frequency of her posts only reinforces that. Just some of her fabricated BS is her rolling claim, made repeatedly for years now, that APTO would be out of business within a quarter along with her constant claims that APTO presentations & news releases contain lies and false data/results. Meanwhile most of her posts are intentional distortions of the status of APTO trials and other aspects of the company.

If you want a more informed view from someone that actually understands the science check out Tartiaboy’s comments on Investorhub.

We’ll likely have a better feel for whether APTO has a future or not around year-end when we see some of the preliminary data from the mono & combo trials.

Carol J says that debt obligations are horrendous. She has a running debate with Tartiaboy on YMB about the science. The science is still unknown until trials are actually done, but the snail pace trials have little to show for themselves. Today’s big plunge shortly after the reverse split is telling. I was once up 400% on this, but am now down 75%. My fault for following the buy and hold strategy of NWI.

I am wondering how the current lawsuits filed by the SEC against Binance and Coinbase will impact the determination of whether or not GBTC and/or ETHE will ever become ETFs or closed-end funds. For months, MM has advocated taking advantage of their 30%+ discount to NAV, repeatedly using the phrase “free money”…

PLTR- After reaching $17 in the early going yesterday got hit by massive selling, had a huge reversal day and closed a smidge under $15. It is trading slightly below it as it continues to work off its overbot condition. I think eventually st it should, at a minimum, retest $17; hard to say if that is the ultimate target for the year of if PLTR is destined to trade again well into the 20s. The huge volume in yesterday’s reversal certainly does not looks good.

Random observations: BA doing well, breakout at $220; half of ultimate position in GDX as it bounces together with the Bond market (Gold+Bonds seemingly joined at the hip lately). The all clear to back up the truck on Gold&Silver should be crossing again $2000/oz.to the upside. ENVX starting to paint a Bullish Wedge as it trades above $13.

The Radar Report for 6.8.23 is posted. Sell BLPH.