Dear New World Investor:

As I expected, the Fed did not raise interest rates Wednesday, after raising at each of its previous 10 meetings. They did, however, raise their interest rate forecasts for this year, signaling rates could rise to as high as 5.6%, implying at least one more rate hike, or roughly 37 basis points worth. Three officials see rates rising higher than that, closer to 6%, all “if inflation continues.”

Whether this is a pause before declines begin next year, as I believe, or just a skip before at least one more increase later this year remains to be seen. But why skip if nearly all the Fed participants really expect more hikes? There is no good answer to this question. The strength of these expectations is the crucial issue. If confidence were high, Fed officials would have hiked in June and not skipped as they did. Odds are that this is a bluff because inflation is going to continue to weaken in the second half of this year and into 2024. We are likely to see a 2-handle on year-over-year headline inflation shortly.

May Consumer Price Index headline inflation rose 0.1% over April and 4% over last year. That was a slowdown from April’s 0.4% month-over-month increase and 4.9% annual gain. Both measures were roughly in line with forecasts for a 0.1% month-over-month increase and a 4.1% annual increase.

Click for larger graphic

Click for larger graphic

May core inflation, which strips out the volatile costs of food and gas, climbed 0.4% month-over-month and 5.3% year-over-year. Core inflation remained sticky because the indexes for both rent and owners’ equivalent rent rose 0.5% each. The shelter index, which jumped 8% annually and 0.6% between April and May, was the largest factor in the monthly increase of core inflation, accounting for over 60% of the total increase. It lags reality by six to nine months and the Fed knows it.

JPow’s favorite inflation indicator – month-over-month core services ex-shelter – just had its lowest print since July 2022.

Click for larger graphic

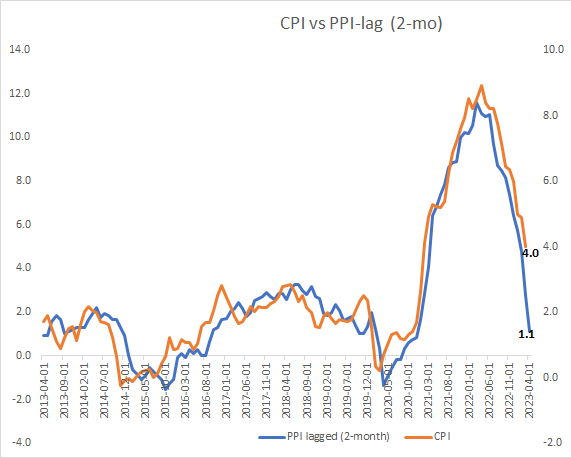

Wholesale pieces – the Producers Price Index – rose only 1.1% on a year-over-year basiss, well below last month’s +2.3%. The chart is breathtaking:

Click for larger graphic

As the CPI keeps easing, record short positioning in 10-Year Treasurys could cause a rally in prices. Compare traders’ positioning now relative to back in January. Just like five months ago, the market is coming off three consecutive lower-than-forecast CPI prints. Yet inflation expectations over the next couple of years are currently higher than they were at the beginning of 2023, despite tighter financial conditions, lower year-over-year inflation, and higher unemployment and jobless claims.

10-year Treasury yields fell about seven basis points to around 3.70% after the CPI report and have held there since the Fed decision.

Market Outlook

The S&P 500 added 3.0% since last Thursday and is up 15.3% year-to-date. If it felt like it took ages for the S&P to climb out of its bear market, that’s because it did. The Index was in bear market territory, or down 20% from a recent high, for 248 trading days. That meant the S&P suffered its longest bear market since the 484 trading days ending in May 15, 1948. Excluding this most recent bear market, the average bear market lasted 142 trading days.

Ed Yardeni predicted stocks will continue to rise through 2023 into next year, potentially taking the S&P 500 to 4,600 by yearend.

The Nasdaq Composite gained 4.1% as the AI opportunity drove Big Tech up. It is up 31.7% for the year. The small-cap Russell 2000 rose only 0.5% but at least is now up a solid 7.2% in 2023.

The fractal dimension shows this is a real trend underway with considerable headroom due to all the stored-up energy in the form of sideline cash and short sales. As that cash comes in, the energy is used up and the trend will end as the fractal dimension approaches 30.

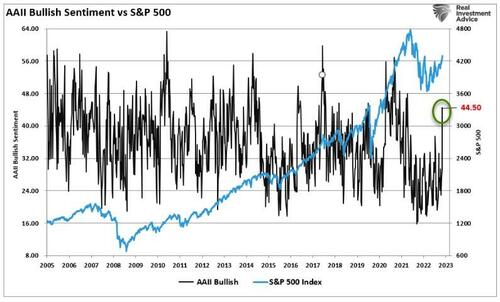

And just like always, retail bullish sentiment finally is surging as the Fear Of Missing Out (FOMO) kicks in long after they should have been buying.

Click for larger graphic

Institutions are doing the same thing, which means we are getting closer to an interim top. After most of the sideline cash is in, there’s no one left to buy. Not there yet, though.

Top 5

Changes this week: Added AKBA to Near-Term

Near-Term – chronological order

EQT EQT –natural gas price rebound

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

AKBA Akebia – Vadadustat NDA filing 2023; approval 2024

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

Economy

The Atlanta Fed’s GDPNow model June quarter real GDP forecast slipped to +1.8% this morning due to weaker estimates of both personal consumption expenditures growth and government spending growth.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, June 19

Markets Closed – Juneteenth

Tuesday, June 20

SFTBY – SoftBank – 9:00pm – Annual meeting

SCYX – ScyNexis – 12:30pm – Maxim Group Virtual Healthcare Conference fireside chat

Wednesday, June 21

RKLB – RocketLab – Unspec – Roth London Conference

GILD – Gilead Sciences – Through 6/24 – 6 oral and 28 posters at European Association for the Study of the Liver (EASL) Congress

ENVX – Enovix – 5:40am – International Advanced Automotive Battery Conference

Summer Solstice – 10:58am – The Earth’s axis has a tilt of around 23.4 degrees, relative to its orbit around the Sun. On June 21, the northern hemisphere is tilted at its closest point towards the sun, so the solstice marks the point when the Sun’s rays hit this part of the Earth most directly.

Thursday, June 22

FSLY – Fastly – 1:00pm – Investor Day

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $186.01) hit a new all-time high today after being bounced around by those who think the new Vision Pro is an overpriced Augmented Reality/Virtual Reality headset versus those who think it is the next great consumer product.

I am closer to the latter. There’s no doubt it is a new computing platform that will find a place in viewing movies and sports better than on a big flat screen, working from home (first) and in the office (later), video conferencing, recording events, virtual travel, education, and the two big drivers of most new technologies, video gaming and porn.

I expect the Vision Pro to be in short supply until at least 2026 – it’s not an easy or cheap product to build. If Apple can make five million in 2024, that’s a $17.5 billion hardware business, plus Apple’s cut of the third-party software.

AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $33.84) moved up after Morgan Stanley upgraded it from Equal Weight to Overweight and raised its target price from $35 to $38. They added that there is scope for positive earnings revisions over the coming year.

I am more bullish as sequential revenues begin to grow again in the current quarter and margins expand. Plus we get a 3.5% dividend while we wait, and they’ve raised it for 12 consecutive years. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2024 .

Gilead Sciences‘ (GILD – $79.00) CEO and CMO presented at the Goldman Sachs Global Healthcare Conference (TRANSCRIPT HERE). The CEO said by 2030 they want a third of their business coming from oncology. He added that they are “ keeping their eye on the ball on virology, building this world-leading oncology program, and also an early inflammation program. And now it’s really about execution. It’s about quarter-on-quarter execution which we’re focusing on last year and continuing into this year. And I think we’re just at the beginning really of a growth phase for Gilead.”

The CMO said: “I didn’t think we’d be talking about competing with Roche and AZ and Merck in oncology four years ago. I think that’s where we are. And I’m really looking forward. I think all this investment now, now we’re going to start to see the data. And I think that’s what I’m excited about. I’m the data junky, but I think, in particular, we have so many readouts coming up over the next couple of years. I’m really excited to be able to share that.”

GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $281.83) was the subject of a remarkably off-base piece in Barron’s: Apple, AI, Metaverse. Why Meta’s Identity Crisis Is Getting Worse Not Better. They wrote: “Meta’s identity crisis has plumbed new depths. If the company’s previous long-term strategy was to go all-in on the metaverse, its current plan seems to be a scattergun approach to ensuring it doesn’t miss out on whatever the next big thing actually is.”

The author cites the June 8 all-hands meeting when CEO Mark Zuckerberg unveiled a new app to compete with Twitter, announced a number of AI tools and initiatives to put AI everywhere on its platforms, and addressed the launch of Apple ’s new mixed reality headset. Apparently, Barron’s did not realize that: (1) social media is always changing, so a company changes or dies; and, (2) the new app, tools, and initiatives all work together and support each other. The new generative AI agents for Facebook Messenger and WhatsApp, plus the new Metamate productivity assistant, have a common technology base.

Meta has been at the forefront of generative AI research, and reorganized its AI efforts in February to get more of the technology into products. The stock hit a new 52-week high today. META is a Buy under $150 for a $400 target in 2024.

Small Tech

Fastly (FSLY – $17.70) presented at the BofA Global Technology Conference (TRANSCRIPT HERE). The CFO focused on their different approach compared to Akamai and other Content Delivery Networks. He said: “I think first and foremost, we look at the market less as a content delivery network, but more about enabling end user experiences. And the differentiation is if you’re just looking at delivering content not about the experience, not about the personalization, I think that is going to become more and more commoditized.

“But I do think the differentiation — and we saw early success in particular in industries where performance mattered. E-commerce, where time to load the web cart and personalization really had a direct impact on card conversion and the value of that card.

“I believe that customers across new industries are going to look at increasing their customer engagement. That means fast websites. It means immersive experience. That means personalized experiences. And that new buyer is really looking about buying that experience. Security, compute, delivery, that’s all part of what they’re buying. They’re buying an end user experience.”

Like PagerDuty, Fastly uses the “land and expand” sales model. They get a CDN contract with a group or division, and then they deliver faster than competitors with lower latency, with a modern platform that is extremely efficient in terms of caching data from the central cloud, purging it, and reducing costs for both the providers and their customers of that central cloud. Over time, that performance differentiation lets them take a bigger share of the traffic. Then they have a security portfolio to cross-sell. They have the leading product around firewalls. Later this year they will launch a Distributed Denial of Service (DDoS) product and a bot protection product.

And their biggest difference is Compute@Edge, a compute element that allows for personalization at the edge to create an immersive fast experience for users. All these are upsell opportunities to continue to expand and grow revenues within current customers.

They deliver content, security, and compute in one platform. The CDN competitors deliver those across three platforms. So Fastly can be competitive on price and still generate meaningful gross margins. But their main focus is on upselling and cross-selling the security piece, as well as the compute capabilities. They have a cost structure that allows them to compete but deliver performance differentiated results.

The forthcoming June 22 Investor Day will focus on the growth opportunity from all the non-CDN add-ons. Getting to operating breakeven, then to positive cash flow and starting to actually generate cash are their key objectives. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $22.91) did a fireside presentation at the William Blair Growth Stock Conference (WEBCAST HERE) and the Baird Global Consumer, Technology & Services Conference ( WEBCAST HERE). CEO Jennifer Tejada said as everything moved online and real-time, the mix of work in most companies has shifted from being planned and predictable to being unplanned, unpredictable, unstructured, and high-impact. A problem in online commerce or banking suddenly puts a company’s customer relationships and revenue at risk.

While most companies have changed their customer-facing processes to be real-time in the digital world, internally they still operate like traditional centralized, paper-based organizations. PagerDuty’s cloud-native platform enables customers to use automation, AI, and Machine Learning to detect incidents in their ecosystem and send them to the right teams to resolve an issue before it becomes a major business-impacting event. They have interfaces to over 700 popular business software packages and systems.

PagerDuty is essential infrastructure for their customers. Sales cycles are lengthening in the current macro environment, especially in the small and lower-midmarket business area. Upper-midmarket and enterprise are resilient, although tech layoffs are making it slower to get expansion seats on installed software. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $7.52) made an excellent presentation at the Stifel Cross Sector Insight Conference (AUDIO HERE and SLIDES HERE). They emphasized that while everything they do is based on their Floating-Point Gate Array (FPGA) technology, they have several revenue streams:

Click for larger graphic

They have won $16 million of new eFPGA contracts since mid-2021, most with significant expansion potential. eFPGA means licensing the intellectual property, not actually producing the chip. They have a $125 million pipeline of potential new contracts.

Click for larger graphic

Click for larger graphic

They are forecasting 36% annual revenue growth for the next three years and expect to hit $100 million quickly and $500 million in “a few years.” 2023 is their breakout year.

Click for larger graphic

Click for larger graphic

Click for larger graphic

QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets and wearables.

Primary Risk: New sensor hub competitor emerges.

Rocket Lab USA (RKLB – $5.68) gave an excellent presentation at the Stifel Cross Sector Insight Conference (AUDIO HERE). Highly recommended! After nine successful launches in 2022, they are targeting 15 in 2023 at $7.5 million each. The current Electron rocket can put 716 pounds of payload into low earth orbit, while the new Neutron rocket due at the end of 2024 can lift 15 tons. They emphasized that they have evolved the company from a lower-margin launch business to a broader space systems business serving a much larger potential market with excellent profit margins.

They don’t want to compete with Elon Musk’s SpaceX yet. SpaceX can lift hundreds of satellites at once, which works for some customers. But if you want a precise location with an exact declination, you need a small dedicated launch like Rocket Lab offers. They are picking up payloads from competitors that have had failed launches. Some competitors are trying to pivot from one-ton rockets that failed to thirty-ton medium heavy rockets. Good luck with that.

They can build an Electron in 18 days and could do one a week. The new hypersonic rocket for the DoD is basically an Electron that is much cheaper than the Northrop Grumman alternative. That means the US can run more tests and do R&D faster for the same budget. Rocket Lab sees “dozens and dozens” of launch opportunities at a similar profit margin.

They can launch up to 128 times a year from their company-owned New Zealand launch facility and are starting with a dozen launch slots in the NASA-owned Wallops Island, Virginia, facility. And they build satellites and sell parts and systems that are launched by other operators, Varda Space Industries, which does in-space manufacturing of pharmaceuticals, just launched the first of four Rocket Lab-built spacecraft using SpaceX’s rocket.

Rocket Lab just bought about $100 million of assets out of the Virgin Galactic bankruptcy for $16.1 million and took over a facility that’s just two blocks away. That eliminates lots of planned capital expenditures for Neutron, which is a $250 million program. They’ll turn EBITDA positive in the second half of 2024. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

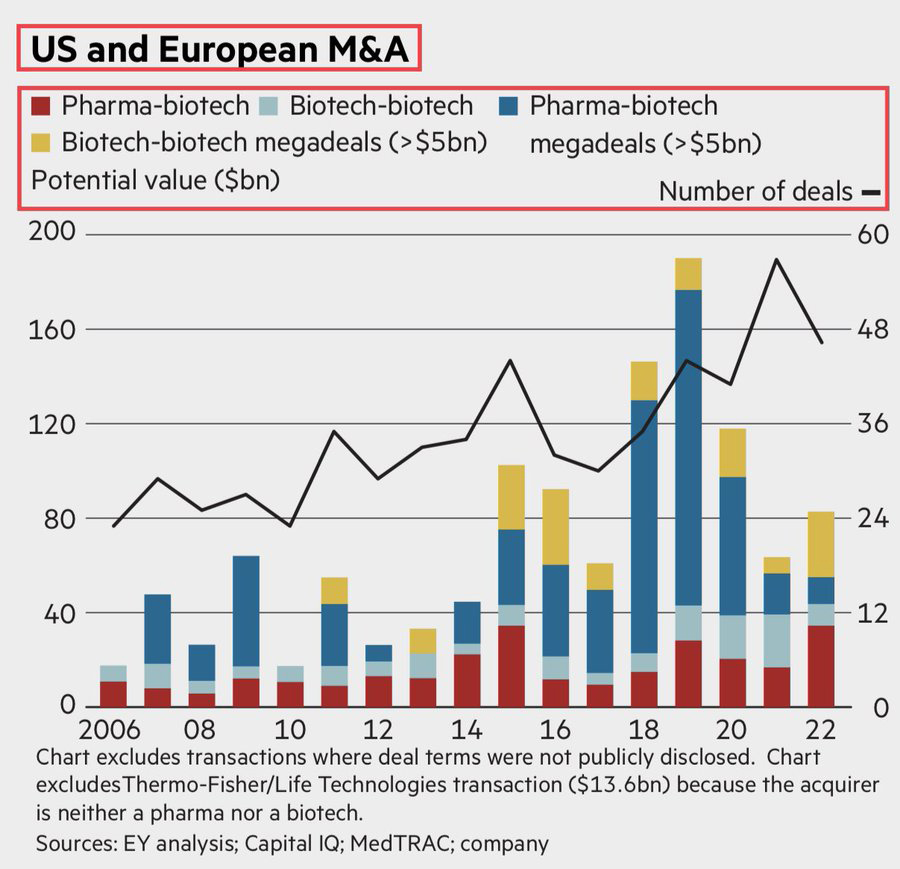

During 2022, over 50% of all mergers and acquisitions in the pharmaceuticals sector were made by pharma companies buying biotech ventures. M&A is important since many ventures face financial challenges and the weakening of the capital markets.

h/t @FT

h/t @FT

Cash-rich pharmas spent $85 billion on deals in the first five months of 2023. Many financial analysts expect Big Pharma to continue to focus on mid-to-large-size deals, especially with decreasing valuations of private and public biotech companies.

h/t @yaireinhorn

h/t @yaireinhorn

Akebia Therapeutics (AKBA- $1.14) presented at the Jefferies Healthcare Conference (WEBINAR HERE). The company finally is positioned to be a $20-for-$1 winner in a relatively short period of time.

As you know, they came public by acquiring Keryx Pharmaceuticals after that company got approval for Auryxia, a ferric citrate that is used to control the serum phosphorus levels in adult patients with diabetes-dependent Chronic Kidney Disease (CKD) on dialysis, and the treatment of iron deficiency anemia in adult patients with CKD not on dialysis. Auryxia did $177 million in revenue in 2022 and Akebia has guided for a flat year in 2023. Auryxia provides them an existing sales and patient support structure to launch their next CKD drug.

That drug is vadadustat, an oral hypoxia-inducible factor prolyl hydroxylase (HIF). It has been sold in Japan for two years through their partner, Mitsubishi Tanabe Pharma, and tens of thousands of patients have taken it. After two Phase 3 trials, Akebia applied for approval in the US. In March 2022, the FDA denied them with a Complete Response Letter and the stock collapsed.

Approval in non-dialysis patients wasn’t likely due to a random signal for Major Adverse Cardiac Events, but they expected easy approval for dialysis patients. The FDA cited both an elevated risk of vascular access thrombosis and drug-induced liver injury as reasons they did not approve. Both of these are easily controlled with proper labeling, and there has never been a case of drug-induced liver injury in Japan. So last October the company filed a formal dispute review request with the Agency.

Two weeks ago they got as close to a victory as the FDA gives. They were advised to refile the New Drug Application with a path to approval that does NOT require new clinical trials and will have a six-month review. They will refile by the end of this year, get approval in the first half of 2024, and launch in the second half.

Click for larger graphicClick for larger graphic

Click for larger graphicClick for larger graphic

While they were waiting for the dispute decision, they got EU and UK approval and signed a dialysis distribution partner, Medice. Medice will launch in Europe before the end of this year.

Click for larger graphic

Click for larger graphic

They’ve done a good job of cutting expenses and paying down debt. With the money coming in from Auryxia and the Medice launch, I don’t expect them to have to sell any stock.

Click for larger graphic

Click for larger graphic

After Vafseo (vadadustat) launches, they’ll still have label expansion opportunities and an interesting pipeline.

Click for larger graphic

Click for larger graphic

The underlying platform technology can produce many drugs, making the company a very probable acquisition candidate for Big Pharma:

Click for larger graphic

Click for larger graphic

And the stock has many catalysts coming this year:

Click for larger graphic

Click for larger graphic

Selling for less than $1.15 a share with a market cap under $215 million, Akebia has less-than-normal risk yet real $20-for-$1 potential rewards. I added it to the Near-Term Buys. Buy AKBA up to $2 for the vadadustat lunches in the EU, UK, and (after FDA approval in 2024) the US.

Primary Risk: Vadadustat not approved.

Clinical stage of lead product: Vadadustat NDA to be refiled

Probable time of next FDA approval: Mid-2024

Probable time of next financing: Unknown

Aptose Biosciences (APTO – $5.89) held their clinical trial update from the European Hematology Association (WEBCAST HERE). The focus was on tuspetinib, which looks like the long-awaited home run.

Click for larger graphic

They completed the “Phase 1” safety trial, which had a huge Phase 2 dose escalation component, and had their end of Phase 1 meeting with the FDA. They’ve selected 80 milligrams once a day to take into the Phase 2 trials, which will be registrational trials – they can get approval without doing a Phase 3. They’ve started the combination trial of tuspetinib with ventoclax with rapid enrollment. These patients only have weeks to a few months to live and everything else has failed, so it’s not surprising they’ll take a chance with TUS/VEN.

Tuspetinib is going to be a blockbuster – a $1 billion drug.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

They will report more data in October and December. The American Society of Hematology (ASH) meeting in December is especially important as that’s where a lot of partnerships and acquisitions happen.

Click for larger graphic

Click for larger graphic

They have paths to approval three ways: as a monotherapy, as a doublet with ventoclax, and as a triplet with ventoclax and a hypomethylating agent.

Click for larger graphic

Click for larger graphic

As you know, I recommended Aptose because I think CEO Dr. Bill Rice is a brilliant drug developer. He identified both luxeptinib and tuspetinib as in-licensing opportunities and has carefully developed each. Wall Street hates how slow he’s moved, but I call it relentlessly methodical and just what you want to bring a $20-for-$1 biotech to fruition.

Click for larger graphic

Click for larger graphic

APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Inovio‘s (INO – $0.51) CEO and CMO presented at the Jefferies Healthcare Conference (TRANSCRIPT HERE). Although they have not quite finished their Phase 3 trial design discussions with the FDA and EU for INO-3107 to treat recurrent respiratory papillomatosis, they already have engaged a Contract Research Organization and are qualifying sites globally. They want to reduce the time between finalizing the protocol with all the final FDA comments and getting the first patient into the trial. INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: Mid-2024

TG Therapeutics (TGTX – $26.48) presented at the Jefferies Healthcare Conference (WEBINAR HERE). CEO Michael Weiss said 50% of the MS market – 40,000 to 45,000 new patients a year – has transitioned to CD-20 therapies like their Briumvi. Of those, 30% choose monthly subcutaneous injections and 70% choose an IV drug like Briumvi. Most patients and infusion centers prefer Briumvi’s one-hour infusion every six months to market-leader Ocrevus’ four- to six-hour infusion.

The launch is going very well. They are way ahead of schedule on insurance coverage with a goal of 80% coverage by yearend. They expect to be on the market in Europe by the end of this year, either through a distribution deal or they’ll do it themselves. Hold TGTX for a target price in a buyout of $25 or more now that the MS drug is approved.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Second half of 2023

Inflation MegaShift

Gold ($1,970.70) rallied sharply today from an intraday low at $1,936. There seems to be a rock-solid bid at $1,940, so the shorts covered and we may be headed up for a while. The fractal dimension has spent a lot of energy defending this area, but there’s still enough left to hit a new high before this uptrend ends and the next (necessary) consolidation begins.

Miners & Related

Coeur Mining (CDE – $3.11) presented at the RBC Global Mining & Materials Conference (SLIDES HERE). Management said that in 2020 their revenues were 75% gold and 25% silver, and by 2025 they’ll be 65% gold and 36% silver.

Click for larger graphic

This was the standard “Why Coeur?” presentation.

Click for larger graphic

Click for larger graphic

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.17) renewed their At-The-Market facility for up to $150 million, although they never sold a share under the previous program and have no plans to use this one.

They got a notice from ICE Data Indices that they would be dropped from the NYSE Arca Gold Miners Index on June 20. They immediately objected and the decision was reversed the same day. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $25,385.01) has fallen out of the $26,000-$28,000 support range as SEC Chairman Gary Gensler pursues his vendetta against the altcoins and exchanges. The interesting dynamic is that if you want to be in crypto – and many investors do – the only safe havens are bitcoin and ethereum. I expect them to start going up as the Gensler Wrecking Ball drives crypto innovation out of the US.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

The Grayscale Bitcoin Trust (GBTC- $13.40) holds 0.00090465 bitcoin per share. That was worth $22.96 at today’s close, so the trust is selling for a 41.6% discount. You have an opportunity to buy bitcoin for $14,815.29. Take it. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $70.53

Oil prices are all over the place. Monday’s 4% sell-off reversed on Tuesday. But the

International Energy Agency published its latest oil market report with balances going to the end of 2024, and it’s getting very clear that those selling paper oil are going to be sorry.

Click for larger graphic h/t @HFI_Research

IEA is assuming a two million barrels a day deficit into yearend 2023. In 2024, it assumes flat balances in the first half of the year with hefty draws returning in the second half. These oil market deficits are unsustainable. A two million barrels a day deficit in the second half of 2023 equals a 366 million barrel draw that puts oil over $100 – easily.

The July 2026 Crude Oil Futures (CLN26.NYM – $63.14) are a Buy under $65 for a $200+ target. Only buy futures for all cash; do not use margin.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.42) is a Buy under $36 for an $80+ target.

EQT (EQT – $38.95) will benefit as hedge funds and other investors pile into natural gas exchange-traded funds, like the ProShares Ultra Bloomberg Natural Gas ETF (BOIL) and the United States Natural Gas Fund (UNG). The funds’ combined net assets are now $2.1 billion, twice the level of just six months ago. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $6.47) will jump as soon as the trend-followers that buy breakouts pounce on uranium. There’s an air-pocket above the magic breakout levels of roughly $65 in spot uranium and $20 in the Sprott Physical Uranium Trust (U-UN.TO or SRUUF).

The stock got a good writeup in SeekingAlpha: Energy Fuels: Empowering Decarbonization In The Digital Age. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

International & Other Recommendations

It is important to hold some non-US assets, especially in China.

Acreage Holdings‘ (ACRDF – $0.37) CEO will resign at the end of this month now that the turnaround is done and the Canopy USA business combination is imminent. The current COO will take over. No big deal.

Sen. Sherrod Brown (D-Ohio), the Senate Banking Committee chairman, said his panel will vote on moving a key piece of cannabis banking legislation to the floor “in the next two or three weeks.” The Secure and Fair Enforcement (SAFE) Banking Act would give legal cannabis businesses access to the US banking system. That will enable a wave of acquisitions and stock exchange listings. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

GPT4All

A free-to-use, locally running, privacy-aware chatbot.

No GPU or internet required.

* * * * *

Your understanding the fiscal impulse Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $186.01) – Buy under $150 for new iPhones

Corning (GLW – $33.84) – Buy under $33, target price $60

Gilead Sciences (GILD – $79.00) – Buy under $80, target price $120

Meta (META – $281.83) – Buy under $250, target price $400

SoftBank (SFTBY – $23.25) – Buy under $25, target price $50

Other Tech

Enovix (ENVX – $13.63) – Buy under $13; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $45.99) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $17.70) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.91) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $7.52) – Buy under $10, target price $40

Rocket Lab (RKLB – $5.68) – Buy under $13, target price $30+

Velo3D (VLD – $1.87) – Buy under $6, target price $50

$20-for-$1

Akebia Biotherapeutics (AKBA – $1.14) – Buy under $2, target $20

Aptose Biosciences (APTO – $5.89) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $8.05) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.51) – Buy under $7, hold a long time

Invitae (NVTA – $1.27) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.62) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.74) – Buy under $2.50, target price $20, then $50

Inflation

A Short-Sale or REO House – ($447,000) – Hold

Bag of Junk Silver – ($23.95) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $26.44) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $29.27) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.57) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $26.91) – Buy under $30, target price $50

Coeur Mining (CDE – $3.11) – Buy under $5, target price $20

First Majestic Mining (AG – $5.59) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.30) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.17) – Buy under $10, target price $25

Sprott Inc. (SII – $33.42) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $25,385.01) – Buy

Grayscale Bitcoin Trust (GBTC – $13.40) – Buy

Ethereum (ETH-USD – $1,666.23) – Buy

Grayscale Ethereum Trust (ETHE – $7.36) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $63.14) – Buy under $65; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $28.42) – Buy under $36; $80+ target

EQT (EQT – $38.95) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.47) – Buy under $8; $30 target

Freeport McMoRan (FCX – $40.08) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $31.51) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $24.16) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.28) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $29.81) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.37) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $0.91) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $3.25) – Hold for buyout

Graphite Bio (GRPH – $2.91) – Hold until they update their strategy

TG Therapeutics (TGTX – $26.48) – Hold for buyout at $25+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First

Hey mm is the oil etf still trading under the same symbol yahoo finance shows 28.42 last trade on June 8th is the symbol still oil,tx

Barclays has called/redeemed many of their ETN’s, my understanding is that OIL will not trade again until next March.

All my shares @ E*TRADE were liquidated on 6-14. They called it a reorganization. Does anyone have a good alternative presently ?

I want to be in oil, but I’m not facile in the futures market, nor comfortable with the minimum size. I agree with the MM premise that individual companies are likely to be too tightly regulated by the ESG wave.

Try using schwab very dependable

APTO – can you clarify the Phase 2 trials you refer to as being registrational trials.

The mono & doublet APTIVATE expansion trials that are currently dosing do not appear to be registrational trials. On the anticipated milestone slide that you pasted into the note there is a 2024 line item as follows:

In their April corporate presention that was a monotherapy registrational trial expected to start in 2023-Q4 rather than the combo therapy so it appears they have now prioritized the combo therapies over the mono therapy & pushed the registrational start date back once again.

Can you provide more color on these 2024 registrational trials that you mention as there is virtually no mention of them in the Aptose presentation slides or on their website.

The FED is done raising interest rates. So says other newsletter publications. I agree. The only reason Powell threw in the wrench at the end of the meeting was because he knew that if he just paused the stock market would explode to the upside and that in itself would create more inflation. Just IMO.

deleted.

TG Therapeutics: A Buy For Its Monster Multiple Sclerosis Agent | Seeking Alpha

Bullish case for TGTX

Add to Calendar:

Tuesday, June 20

SCYX – ScyNexis – 12:30pm – Maxim Group Virtual Healthcare Conference fireside chat

Akebia Announces Swissmedic Approval of Vafseo® (vadadustat)

Hi Michael – In my brokerage acct, my iPath Pure Beta Crude Oil Exchange-Traded Note shares were redeemed. It looks like the note was called by the company. Is that your understanding? Is there an oil ETF you would recommend to replace it?

Just FYI. Oregon DMV was hacked into some 2 weeks ago by some international hacker. (Probably Russia) which compromises over 3 million Oregon drivers personal information. Now Louisiana is also saying the same thing. So be on guard in your state for more of the same . If you have not heard already.

Why Russia? I would suspect China as Russia has its hands full. It’s most likely some dude in his mom’s basement as most DMV systems are run on old mainframes.

MM – TGTX is over $26 yet your recommendation is to hold for a buyout of $25 – can you update me please, is this still a buy as the Seeking Alpha article posted below believes? What is the time horizon for significant stock price appreciation?

Looks like a feeding frenzy to get a BTC spot ETF going from the big boys. Look out above for Bitcoin.

Any idea why XOM got so cheap yesterday? Not complaining as I bot some August $105 Calls on the weakness and they are up about 25% today. Just wondering what the reason was for the weakness yesterday.

Answering my question:

https://ibkrcampus.com/traders-insight/securities/commodities/seasonal-weakness-in-oil-companies-the-summer-slump/?=TWS

What is wrong with NVTA? Is it going bankrupt?

Don,mm did state on June 1st that nvta will be added to the Russell index 3000,hopefully it will see a little pop coming from that,besides that nothing good comes until earnings on Aug 9th and we all know that the previous earnings reports haven’t done shit to help the share price,for myself as long as cathie woods keeps buying,I will be holding,cause maybe somebody knows something,have a good day.

Sorry,nvta to be added on June 26th to the index

Pretty nasty hit piece on ENVX. https://www.pigfarmercapital.com/

What’s wrong with INO? Down everyday.

INO became irrelevant nearly 3 years ago.

More proof oil isn’t going away anytime soon. China has signed a 27 YEAR agreement with Qatar in which China will buy 4 million tons of LNG (liquefied natural gas) per year and take a partial stake in the expansion plans of a massive Qatari natural gas project. Also, SMCI is $226.46, AAPL is $187, and TSLA is $264.

The new Radar Report for 6.22.23 is posted.