Dear New World Investor:

The economy is a little stronger than most investors expected while inflation (or at least the headline year-over-year Consumer Price Index) is slowing faster, cutting the foundation of the stagflation bears. Today, first-time jobless claims unexpectedly dropped to 239,000 from 264,000 last week. They were expected to rise to 270,000.

The third estimate of real GDP growth rarely changes the second estimate very much. But today the Commerce Department’s third estimate of March quarter GDP rose to 2.0%, higher than the expected 1.4% estimate. GDP still decelerated from the September quarter’s 3.2% growth and the December quarter’s 2.6%. I still think we are headed to a short, shallow recession.

The Atlanta Fed’s GDPNow model is looking for a similar report for the June quarter. It’s due on July 27.

Click for larger graphic

Click for larger graphic

Market Outlook

Thanks to today’s rally, the S&P 500 added 0.3% since last Thursday with one more day left to post its best first half in years. The Index is up 14.5% year-to-date. These are the Index’s consecutive UP years (green) and consecutive DOWN years (black) from 1928 to now (2023 is first half).

Click for larger graphic h/t @donnelly_brent

Click for larger graphic h/t @donnelly_brent

In contrast, the Nasdaq Composite had a flat day today and lost 0.3% for the week. But it still is up 29.9% for the first half of the year. The small-cap Russell 2000 booked a 1.8% gain and is up 6.8% in 2023.

The fractal dimension eased back into an uptrend. I still expect it to last into June quarter earnings reports, but then we’ll probably take a breather.

Top 5

Changes this week: None

Near-Term – chronological order

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

SFTBY SoftBank – for ARM IPO this fall

AKBA Akebia – Vadadustat NDA filing 2023; approval 2024

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, June 30

Personal Consumption Expenditures Index – 8:30am – Expected: Headline +3.87% YoY, +0.13% QoQ. Core: +4.70% YoY, +0.38% QoQ

Monday, July 3

Market closes early – 1:00pm – Ahead of July 4 holiday

Tuesday, July 4

US Markets Closed

Happy 11th anniversary to the greatest fireworks show in history, when San Diego accidentally shot off 7,000 fireworks at once.

Friday, July 7

June payrolls – 8:30am – +200,000 expected; May was +339,000

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $189.59) hit a new all-time high today and is a skootch away from becoming the first company with a $3 trillion market capitalization. Well played, Tim Cook! We should get a market correction sometime this summer or early fall, and I’ll raise the buy limit to an appropriate level then. Wall Street will publish it’s usual “Apple component suppliers say iPhone orders are disappointing” stories in an attempt to separate you from your stock before the Vision Pro instruction in early 2024, but…

Gilead Sciences (GILD – $76.01) announced the Week 96 results from their pivotal Phase 3 trial of Hepcludex for the treatment of adults with chronic hepatitis delta infection. (Hepcludex is the only approved treatment for HDV in the EU but is not yet approved in the US – it will be.)

They saw additional improvements in combined response at Week 96 compared with Week 48, with no signs of treatment resistance. It was especially significant that patients who appeared to not respond or only partially respond to treatment at Week 24, went on to achieve a virologic response at 96 weeks with continued monotherapy. Hepcludex is an effective, well-tolerated treatment for HDV when used for a longer duration even in people who initially showed only a partial decline in HDV viral load.

The company also got a positive opinion from the Committee for Medicinal Products for Human Use of the European Medicines Agency for Trodelvy as monotherapy for the treatment of adult patients with unresectable or metastatic hormone receptor (HR)-positive, HER2-negative breast cancer who have received endocrine-based therapy, and at least two additional systemic therapies in the advanced setting. They’ll get final European Commission approval for the additional indication for Trodelvy in a few months. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $281.53) got a target price increase from UBS, who said the company isn’t getting enough credit for the consumer applications of its artificial-intelligence efforts. They think, as I do, that the company’s plans to release AI chatbots across Instagram, WhatsApp, and Facebook will increase the amount of time users spend on the platforms, boosting annual advertising revenue by $7.5 billion if they monetized just 5% of the search queries on Facebook.

They maintained their Buy rating and raised their target price from $300 to $335, based on a price-to-earnings multiple of 20x 2024 earnings. META is a Buy under $150 for a $400 target in 2024.

Small Tech

Enovix (ENVX – $17.92) has been rallying since the pigfarmer shortseller hit piece. This is a classic example of a short recommendation based on feelings and hype rather than factually supported statements. Right from the unnecessary dig at Marc Cohodes (“Enovix is worthless. Our farmer short seller research is better than the other farmer’s.”) to the lengthy, pointless bewailing of how much money the SPAC promoters made, to completely unsupported statements like “Enovix faces about a dozen companies with larger and more impressive intellectual property portfolios” and “…assumes that Enovix can successfully manufacture its own technology efficiently at scale, but there’s no evidence that it can,” this is a hit piece. And it must be a bit embarrassing to say production can’t scale a week before the CEO announces they are producing more batteries than expected.

Just to put the “farmer” dig in context, Cohodes owns an egg farm in Northern California and his Twitter handle is @AlderLaneEggs. But what pigfarmer may not know is that he actually lives in Montana. As for the rest of it – well, T.J. Rogers, who built Cypress Semiconductor, and investor/informal adviser Greg Reyes, who built Broadcom, both understand semiconductor production and packaging technology, which operates at tolerances 10x what Enovix needs. The company is full of experienced execs who know how to scale production – this is their last rodeo, not their first. As long as the new management team keeps hitting and exceeding goals, we should be buying the stock.

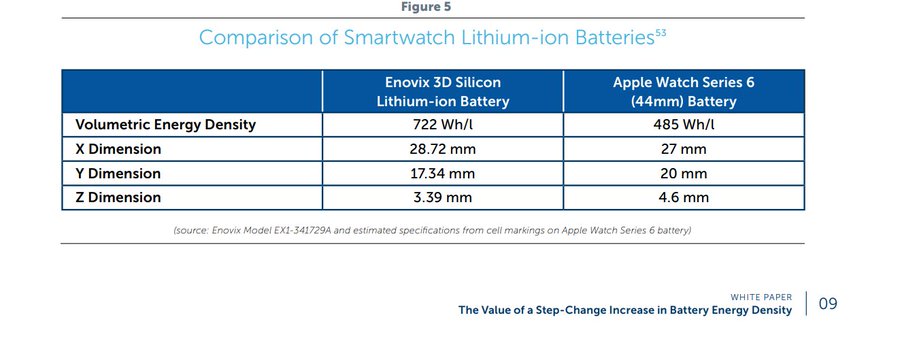

This week, Enovix announced a purchase order from the US Army to produce commercial cells for a soldier’s central power source, called the Conformal Wearable Battery (CWB). Soldiers carry more than 60 pounds of gear, including batteries, to power critical equipment. This agreement progresses this program to the next step towards full volume production. The CWB, created by Inventus Power, powers vital communications equipment and other devices. Enovix cells nearly double the energy density of the current CWB cells, which could result in substantial operational advantages including longer lasting and lighter battery packs. And since they can’t catch fire, they’re safer.

It’s interesting to compare the specs for the Apple Watch batteries to the ENVX wearable product specs. Energy density is 49% higher.

Click for larger graphic

Click for larger graphic

ENVX is a Buy up to $13 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

PagerDuty (PD – $22.02) said Forrester Research. named PagerDuty a leader in its The Forrester Wave: Process-Centric AI For IT Operations (AIOps), Q2 2023 report. PagerDuty AIOps receives and normalizes events from any source, and extracts signal from the noise to provide powerful context and noise reduction at scale. It is just one part of the PagerDuty Operations Cloud, an AI-powered platform to help enterprise companies operate.

PagerDuty received the highest score possible on many criteria. Forrester said: “PagerDuty goes beyond alerting to automate processes and workflows that accelerate resolutions… Normalizing event data and enriching it with remediation-specific data powers automation workflows throughout the PagerDuty platform. PagerDuty mobilizes teams during an incident by automatically adding chat-driven operations (ChatOps) channels, setting up conference bridges, and sending status updates…Reference customers praised PagerDuty’s event noise reduction with one calling its Event Intelligence ‘very powerful.’ PagerDuty is a good fit for enterprises with diverse technologies that will remain in place or must integrate into a common platform that can drive automation and eliminate low-value work.”

PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $9.20) has been on a long-overdue tear. Analysts are expecting revenues to grow 29.8% this year to $21 million, followed by 32.6% next year to $27.85 million. They’ll turn cash flow positive this year. QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets and wearables.

Primary Risk: New sensor hub competitor emerges.

Rocket Lab USA (RKLB – $5.98) did an excellent fireside chat at the Jefferies Space Summit (VIDEO HERE) and made a couple of interesting points. A lot of what they learned from launching the Electron small-payload rocket transfers really well to launching a mid-weight rocket like Neutron. They mentioned understanding reentry thermodynamics, composites lessons, avionics lessons, navigation, and control as some areas that make launching a rocket hard and transfer really well to Neutron.

Going from kerosene/liquid oxygen to methane/liquid oxygen propulsion is the big change. It’s not easy and Rocket Lab has studied all the previous successes and failures. Their engineering team is tasked with producing a motor that is both reliable and commercially viable. Look for the cryogenic fuel tank tests and the Archimedes motor hot fire tests by yearend.

They also said that industry-wide launch availability for small satellites is pretty constrained and it’s even worse for medium-size payloads. As they look forward for the next five years, demand is much greater than supply, so pricing should stay OK or even improve. Neutron is on track for a December 2024 quarter first launch.

A Neutron launch will cost $55 million versus SpaceX’s Falcon 9 launch at $67 million. There are some PowerPoint rockets out there forecasting a lower launch price, but Rocket Lab is not concerned about paper rockets.

Plus, Rocket Lab does not compete with their customers – they have no interest in launching their own satellites – and can sell Space Systems components to companies building satellites for launch by others. They also can build high-quality satellites with short lead times – another area where demand exceeds supply. They are targeting a 30% to 40% gross profit margin in Space Systems in 2024 and 2025.

Their next Electron launch, their 39th, will deploy seven satellites and the company will conduct a marine recovery of the first stage as a part of the mission. The launch window opens July 14. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $0.93) announced topline results from IMPACT, a post-approval Phase 4 trial investigating the impact of Auryxia used as the primary phosphate-lowering therapy on the utilization of erythropoiesis-stimulating agents (ESA) and intravenous (IV) iron, as well as on laboratory parameters indicative of phosphate and anemia management, compared to the standard of care (SOC) in adult patients with chronic kidney disease (CKD) on dialysis.

IMPACT, sponsored by U.S. Renal Care Kidney Research in collaboration with Akebia, was a randomized, open-label, active-controlled, multicenter study in adult patients with CKD receiving either in-center hemodialysis or home dialysis. The study enrolled 209 adult patients who were randomized 1:1 to Auryxia (starting dose of 6 tablets per day) or to remain on SOC, defined as a non-Auryxia phosphate-lowering agent, for up to 6 months. The two groups had generally similar baseline characteristics with the exception of atherosclerotic cardiovascular disease and congestive heart failure, which were more common in the SOC group.

The co-primary endpoints were the difference in mean change from baseline (month -3 to Day 1) to the efficacy evaluation period (months 4-6) in monthly ESA and IV iron doses between groups. Secondary endpoints were the difference in the proportion of patients with serum phosphate ≤5.5 milligrams per deciliter and hemoglobin (Hb) ≥10.0 grams per deciliter, during the efficacy evaluation period (months 4-6).

Treatment with Auryxia resulted in a statistically significant difference in mean monthly ESA use (-30.82 micrograms/month, P=0.02) and a non-significant difference in mean monthly IV iron use (-37.02 micrograms/month, P=0.17). There were similar proportions of patients in each group with Hb ≥10.0 grams per deciliter and serum phosphate ≤5.5 milligrams per deciliter.

Three patients stopped Auryxia due to gastrointestinal intolerance (n=2) or adverse events (n=1). Serious adverse events occurred in 39% of patients receiving Auryxia and 59% in those receiving SOC. Buy AKBA up to $2 for the vadadustat lunches in the EU, UK, and (after FDA approval in 2024) the US.

Primary Risk: Vadadustat not approved in the US.

Clinical stage of lead product: Vadadustat NDA to be refiled

Probable time of next FDA approval: Mid-2024

Probable time of next financing: Unknown

Aptose Biosciences (APTO – $4.48) posted this slide during their June 10 corporate update:

Click for larger graphic

Click for larger graphic

I’ve circled the key words in red. “Registrational” means a trial’s data will be used for an FDA application. Notice that the TUS (tuspetinib) monotherapy Phase 2 trial and the TUS/VEN (tuspetinib/venetoclax) Phase 2 trial are both registrational. To be sure we were on the same page, I contacted Aptose IR:

Dear Mr. Murphy,

Your read of the chart is correct.

Please let us know if you have any further questions.

Regards,

Aptose IR

APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Compass Pathways (CMPS – $8.01) did a fireside chat at the HC Wainwright Neuropsychiatry Conference (WEBINAR HERE) and another on Commercialization of Novel Agents in Neuropsychiatry (WEBINAR HERE). In more detail than usual, management discussed many facets of both COMP360 and the trial results to date.

The COMP005 Phase 3 trial, entirely in the US, will compare a single administration of 25 milligrams of COMP360 with placebo. There will be 255 patients with 1/3 getting the placebo and a primary outcome measured at six weeks. We get top-line data next summer.

The second COMP006 Phase 3 trial is an international study with 568 patients. They will be randomized in a 2:1:1 ratio to receive COMP360 25-milligrams, 10-milligrams or 1-milligram, and there will be two treatments. Again, the primary outcome will be measured at six weeks. We get top-line data in the summer of 2025.

Both trials will be followed by a Part B blinded follow-up for 26 weeks, after which patients will be eligible for ongoing open-label treatment with th 25-milligram dose.

Last Friday, the FDA published a new draft guidance on investigations into psychedelic drugs, detailing considerations for their clinical trials for the first time. Not surprisingly, their guidance closely follows their recommendations for the Compass Phase 3 trials. The draft recommendations are open for public comments for 30 days before the FDA issues its final guidance.

This quarter Compass raised another $27 million from their At-The-Market facility and they now have enough cash to get through at least the next 12 months. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2023

Graphite Bio (GRPH – $2.59) CFO Alethia Young is leaving, probably to go back to Wall Street, where she was a highly-paid biotech analyst. She joined Graphite Bio a year ago in part because she is a sickle cell gene carrier, and with the failure of that program she’s out of there. The company’s annual meeting is on July 19, and I’m expecting to hear what their future plans are then. GRPH is a Hold until the conference call.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Pre-clinical

Probable time of first FDA approval: Unknown

Probable time of next financing: Unknown

Inovio (INO – $0.47) settled a shareholder suit on the usual terms. Each of the seven plaintiffs gets $1,500. Their lawyers get $1,175,000. The D&O insurance will cover most of it. Thank goodness we have these brave strike suit lawyers to selflessly protect the poor shareholders. INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: Mid-2024

Medicenna (MDNA – $0.52) reported their March fiscal year results with no conference call. They lost $10.0 million for the year or 16¢ per share. They had $33.6 million in cash at the end of March, enough to carry them through the key milestones of the ABILITY study and into the September 2024 quarter.

In the coming September quarter they’ll do an MDNA11 clinical update with a conference call for all dose escalation patients, including high dose cohorts five and six. They also expect to start the Phase 2 ABILITY trial’s single agent dose expansion portion in the September quarter. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

Inflation MegaShift

Gold ($1,915.90) is fighting to stay over $1,900 as buyers showed up at that level today. The stronger economic news translated to a stronger dollar on the theory the Fed will have to lean hawkish – which, of course, they will. Reporters can always get a scary headline story by asking: “Chairman Powell, are you willing to take N more rate increases off the table?”

Powell’s answer to that question always will be “No” and – Boom! – a guaranteed byline with a clickbait headline.

What you won’t see them ask is: “Chairman Powell, are you willing to take N rate decreases off the table?” Because the answer to that question also is “no,” since Powell is data-dependent and won’t take anything off the table.

The fractal dimension is still in trend mode, but it sure looks like the uptrend turned into a downtrend without going through a consolidation. That would be really weird and if the rally resumes from here, I am just overthinking this. The next few weeks are important, though.

Miners & Related

Paramount Gold Nevada (PZG – $0.30) said it is wading through the bureaucratic morass of opening a gold mine in Oregon. Thy got approval for a two-year extension of their Conditional Use Permit from the Malheur County Planning Department. They’ve submitted all the responses and additional information requested by Oregon State permitting agencies that they require to determine if the company’s Consolidated Permit Application (CPA) is complete. These submissions address aspects of the CPA that the State deemed necessary to advance to the Notice to Proceed stage of the permitting process.

The Notice initiates the 225 days of draft permit writing by State Agencies and a final Environmental Evaluation (EE). Earlier this year, Stantec, a third-party environmental engineering firm, started work on the EE in advance of the Notice to help ensure the timing of the State process is aligned with the federal Environmental Impact Statement (EIS) process.

Meanwhile, the local BLM office has reviewed the Notice of Intent (NOI), which is now being sent to BLM headquarters for briefing. Once approved, the NOI will be filed in the federal registry initiating the National Environmental Policy Act (NEPA) process. As with the State EE, the federal EIS is being completed by a globally recognized engineering firm that has been involved in the project for several years. PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: 2023

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $30,508.56) rose over $30,500 and remains comfortably above the key psychological level of $30,000 it cleared last week after BlackRock filed for a spot bitcoin ETF, but remains below recent highs near $31,500.

Bernstein said if spot ETFs move forward, it could open the floodgates for investments by financial advisors who had previously found it too costly or inconvenient to put clients into bitcoin. Right now, money managers often have to manage crypto on separate platforms from clients’ other investments, or buy funds that have high costs and don’t track bitcoin’s price very well. ETFs, and the likely fee cuts that competition between issuers would bring, could solve both those issues.

Beyond that, according to Bernstein, the fact that fund companies are still moving forward with crypto and blockchain products shows that institutions are making a large bet that crypto is going to be sustained as an asset class. They wrote: “We believe institutional interest in crypto is across the entire traditional financial services space – banks, asset managers, investment banks, broker-dealers and custodians etc.”

HSBC Hong Kong, the biggest bank in Hong Kong, said they would “beat the USA to the punch” and is now permitting trades of bitcoin and ether ETFs listed on Hong Kong’s exchange. In an April letter sent by the Hong Kong Monetary Authority to the banks, the region’s banking regulator said that due diligence should not create “an undue burden” to accepting crypto exchanges as clients. Hang down your head, Gary Gensler.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $19.55) closed today at a 28.9% discount to its net asset value as we approach a decision in their lawsuit against the SEC. That’s not the 40%+ discounts we were seeing, but you’re still buying bitcoin at less than $22,000 a coin – cheaper than the $28,135 Michael Saylor paid in May and June for another $347 million worth.

With the lawsuit decision pending, the BlackRock spot exchange-traded fund filed (as well as funds from Invesco and WisdomTree), and the Fidelity spot fund about to file, GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $69.77

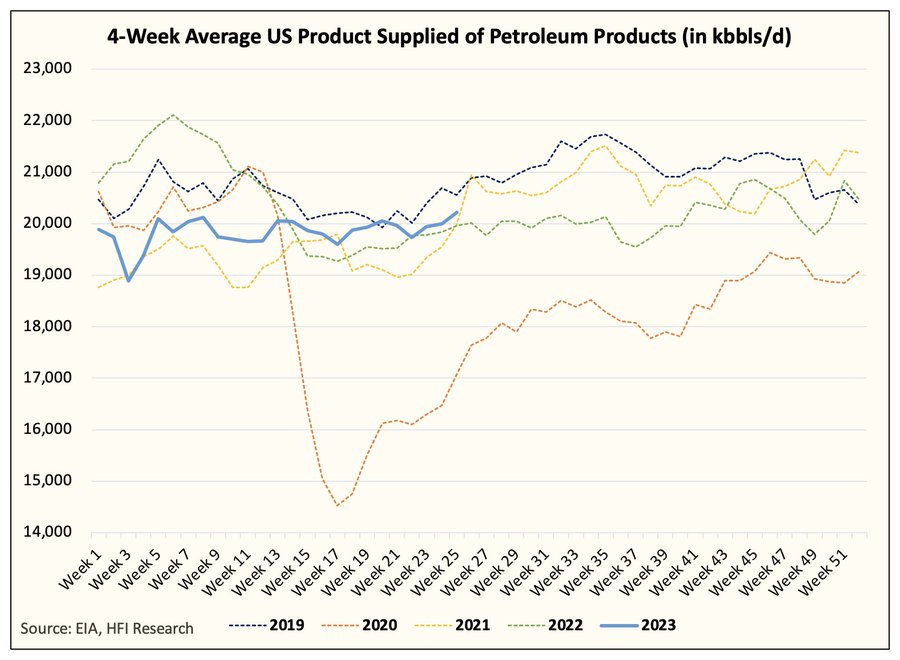

Oil continues to trade just under $70 even though US implied oil demand on a 4-week basis is now above ~20 million barrels a day.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

Saudi Aramco CEO Amin Nasser said market fundamentals remain “sound” for the second half of 2023 as demand from emerging markets led by China and India will offset recession risk in developed markets. He said: “The economies of developing countries – especially China and India – are driving healthy oil demand growth of more than 2 million barrels per day this year.”

The July 2026 Crude Oil Futures (CLN26.NYM – $62.89) are a Buy under $65 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $32.40) is a Buy under $35 for a $100+ target.

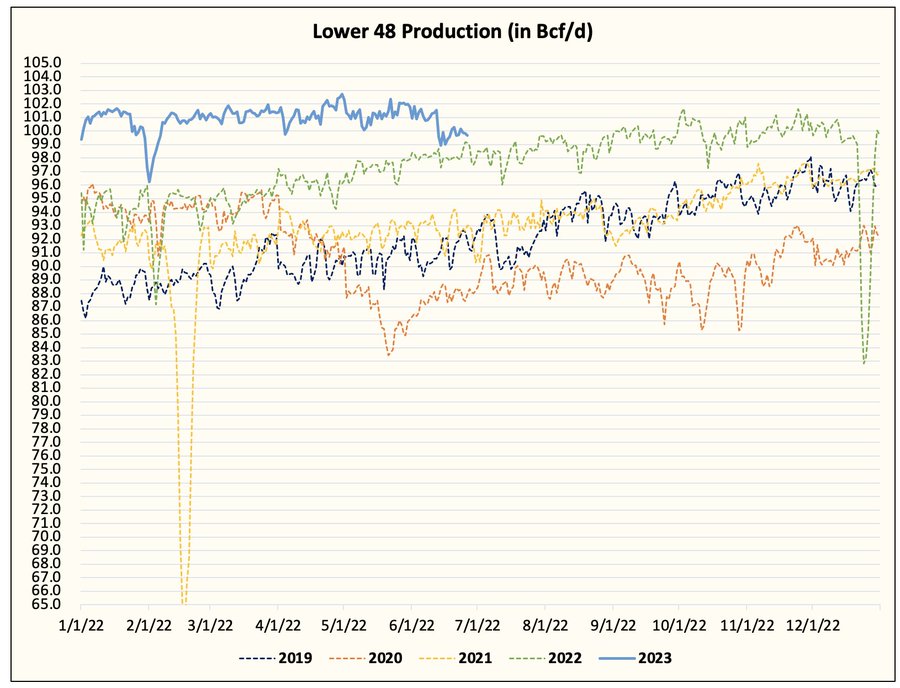

EQT (EQT – $41.04) has been inching up as natural gas production is peaking.

Click for larger graphic h/t @HFI_Research

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Freeport McMoRan (FCX – $39.35) was a Barron’s stock pick. They wrote: “Copper prices are getting ready to run—and Freeport-McMoRan stock is the way to play it…The Phoenix-based company already has the strongest balance sheet of any copper miner, a strong management team, and the ability to return capital to shareholders. And it will benefit from the long-term adoption of electric vehicles and other forms of alternative energy. Now, copper prices are starting to tick higher amid signs of economic resilience, and if they continue to, so will Freeport stock.

“There are long-term drivers for copper, as well. Electric vehicles, for instance, require at least three times more copper than internal-combustion vehicles. As consumers continue to adopt electric vehicles, that factor alone could help push global copper demand to just over 28 million metric tons by 2030, according to the International Energy Agency. Supply could have trouble catching up to that demand, with a potential shortfall of six million metric tons by that year, according to McKinsey.”

Billionaire Robert Friedland, the founder of Ivanhoe Mines, said: “We’re heading for a train wreck here. My fear is that when push finally comes to shove copper can go up 10 times.” He pointed to the very low physical inventories of copper I’ve talked about and said: “When metals are required, the prices go crazy and nobody’s willing to sell them. We’re heading into that sort of situation. Europe is in a panic about where their raw material is going to come from. The US is in a panic about where their raw material is going to come from. And so we’re going to see a lot of volatility and change in the way our supply chain is organized.”

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

Click for larger graphic h/t @charliebilello

Click for larger graphic h/t @charliebilello

* * * * *

Click for larger graphic From Stray Reflections by Jawad S. Mian

Click for larger graphic From Stray Reflections by Jawad S. Mian

* * * * *

Your experimenting with AI images Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $189.59) – Buy under $150 for new iPhones

Corning (GLW – $34.71) – Buy under $33, target price $60

Gilead Sciences (GILD – $76.01) – Buy under $80, target price $120

Meta (META – $281.53) – Buy under $250, target price $400

SoftBank (SFTBY – $23.14) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $17.92) – Buy under $13; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $45.11) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $15.83) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.02) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $9.20) – Buy under $10, target price $40

Rocket Lab (RKLB – $5.98) – Buy under $13, target price $30+

Velo3D (VLD – $2.07) – Buy under $6, target price $50

$20-for-$1

Akebia Biotherapeutics (AKBA – $0.93) – Buy under $2, target $20

Aptose Biosciences (APTO – $4.48) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $8.01) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.47) – Buy under $7, hold a long time

Invitae (NVTA – $1.13) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.52) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $3.02) – Buy under $2.50, target price $20, then $50

Inflation

A Short-Sale or REO House – ($447,000) – Hold

Bag of Junk Silver – ($22.77) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $25.43) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $27.51) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $17.90) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $25.50) – Buy under $30, target price $50

Coeur Mining (CDE – $2.86) – Buy under $5, target price $20

First Majestic Mining (AG – $5.45) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.30) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.00) – Buy under $10, target price $25

Sprott Inc. (SII – $31.92) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $30,508.56) – Buy

Grayscale Bitcoin Trust (GBTC – $19.55) – Buy

Ethereum (ETH-USD – $1,851.27) – Buy

Grayscale Ethereum Trust (ETHE – $9.92) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $62.89) – Buy under $65; $200+ target

United States 12 Month Oil Fund, LP (USL – $32.40) – Buy under $35; $100+ target

EQT (EQT – $41.04) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.11) – Buy under $8; $30 target

Freeport McMoRan (FCX – $39.35) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $29.20) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $22.88) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.62) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $26.83) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.19) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $0.83) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $2.65) – Hold for buyout

Graphite Bio (GRPH – $2.59) – Hold until they update their strategy

TG Therapeutics (TGTX – $24.11) – Hold for buyout at $25+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Good old Screwtape…C.S. is one of my favs

Happy 4th everyone

4th? I’m only 3rd….

MM–thanks for your attempts to evaluate ENVX. However, this ignores the basic science of battery function and long term reliability, which is still speculative. There is more to this than TJ’s expertise in semiconductor production. Often, engineering doesn’t anticipate disasters, such as the O-ring problem in the Challenger rocket, resulting in loss of lives. Nobody at the time thought about O-rings. This was a failure of conceptualization of possible problems. A common human problem is pursuing technical rabbit holes without awareness of other factors. I scorn the narrow-mindedness of 99% of practicing MD’s I have met in my long career, who are concerned only about drug bandaids and not basic root causes. Hence, the failure of Alzheimer drugs.

What is the truth about APTO? Is management really deserting, as claimed by Carol J? Emails and promotion from the company could be complete lies–the next day the lights could be out permanently. The continued plunging stock price tells the story.

And don’t expect AI to solve problems. AI is good at data crunching, which is merely an efficient tool to assemble combinations of existing knowledge. Most medical published literature contains only a small fraction of clinical experience and judgment. Many doctors are not politically connected to get their work published. They have knowledge gained from experience which AI doesn’t have access to. The same is true for hard science, even math. Hard science is not as firm as most people believe. For soft biological and medical science, they are in their infancy still. Smart people think outside of the box (the internet), but AI cannot.

I think you are vastly underestimating AI. ChatGPI represents a hockey stick type movement in the arena. I think you will be blown off your feet on the speed that AI disrupts jobs in law, medicine, and financial planning.

AI may well be more effective than robotic thinking by regulation mindful lawyers, doctors, financial planners. But it takes a human with judgment to be creative with relevant solutions. AI’s “creativity” just generates irrelevant junk data without perspective. Fast, but junk. Look at yesterday’s article from mercola.com about a lawyer who used AI for legal research. It came up with false case studies that got the lawyer into trouble. Junk for a junk lawyer who didn’t care about authentic, relevant research. Serves him right.

Carol J is trying to upset people with nonsense. Management is NOT “deserting to Canada.”

From the January 9, 2020 prospectus:

“We were incorporated under the Business Corporations Act (Ontario) on September 5, 1986 under the name RML Medical Laboratories Inc.”

“Our head, registered and records office is located at 251 Consumers Road, Suite 1105, Toronto, Ontario, Canada, M2J 4R3.”

https://www.sec.gov/Archives/edgar/data/882361/000119312520004710/d856471d424b2.htm#tx856471_5

MM, What are your thoughts on the price action with acrdf under 0.20 cents share?

Who blew hot air up INO’s skirt?

It’s only down 1000’s of percentage points. I think that was just a hot flash.

MM – thanks for reaching out to APTO to get clarification regarding the phase 2 registrational trial issue. I had also reached to IR last week to get clarification but never received a response back.

I still find their slide confusing but am happy to hear the currently dosing mono/doublet phase 2 trials count as registrational.

The new Radar Report for 7.6.23 is posted.