Dear New World Investor:

I was wrong. I thought that with inflation cooling, lagging components like rent set to fall for several months, manufacturing already in a recession, and labor markets cooling, the Fed would be smart enough to continue pausing interest rates and watching incoming data to see the full effect of their most aggressive rate hiking campaign since the 1980s – 10 increases totaling over five percentage points since March 2022.

Nope. They raised the Fed funds target range by 0.25% yesterday to 5.25%-5.5%, the highest level since March 2001. They repeated June’s language: “In determining the extent of additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Chairman Powell said the Fed staff is no longer forecasting a recession. But the Fed has already caused a manufacturing recession. The latest reading for the Institute for Supply Management Manufacturing Index fell to 46, the lowest level since 2009. This also marked the 8th consecutive quarter of declines. Over the last 70 years, this US economy has rarely avoided a recession when manufacturing output has declined by a similar magnitude.

Click for larger graphic

Click for larger graphic

Powell also said they don’t expect inflation to be back to 2% until 2025, which sounds right even after a shallow recession. For the stock market, the Fed saying “no recession” and “2025” just means higher for longer and a stronger dollar, creating a headwind for bonds, cyclical stocks, commodities, and precious metals. Of course, when the Fed has to say “Whoops, recession,” all that will reverse big time. Meanwhile, stocks of companies that can grow or get drug approvals will be sought after.

Market Outlook

The S&P 500 added just 0.1% since last Thursday, but that included a new 2023 high today. The Index is up 18.2% year-to-date. This was the first year in the history of the Bloomberg Data Series that Wall Street as a consensus expected the S&P to go down. They still are much more negative than Main Street:

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

The Nasdaq Composite was flat and still is up 34.2% for the year. The small-cap Russell 2000 dropped 0.6% and is up 11.0% in 2023.

The fractal dimension still shows an uptrend with enough remaining energy to push higher, but not enough to get to a new all-time high. The necessary consolidation to build up energy for the push to all-time highs could start anytime in the next three weeks.

According to @NDR_Research, almost 60% of stocks on the global index are now trading above their 200-day moving averages, which signals increasing confidence from the market that companies’ earnings will soon stabilize. That’s up from a low point this year of just below 20% as central banks hiked interest rates to reduce inflation and economic demand. NDR wrote: “Downside risk remains if the Fed stays aggressive, but upside risk is also present if inflation remains subdued.” Indeed.

Top 5

Changes this week: None

Near-Term – chronological order

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage this fall

SFTBY SoftBank – for ARM IPO this fall

AKBA Akebia – Vadadustat NDA filing 2023; approval 2024

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Economy

The first estimate of June quarter GDP growth was announced this morning at +2.4%, up from +2.0% in the March quarter. It was “surprisingly strong” for Wall Street, but not for us because the Atlanta Fed’s GDPNow model nailed it – again.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, July 28

Personal Consumption Expenditures Index – 8:30am

Wednesday, August 2

FSLY- Fastly – 4:30pm – Earnings conference call

Thursday, August 3

SAND – Sandstorm – After the close – Earnings release; call tomorrow

AAPL – Apple – 5:00pm – Earnings conference call

GILD – Gilead Science – 5:00pm – Earnings conference call

Friday, August 4

July payrolls – 8:30am -+184,000 expected; was +209,000 in June

SAND – Sandstorm – 11:30am – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

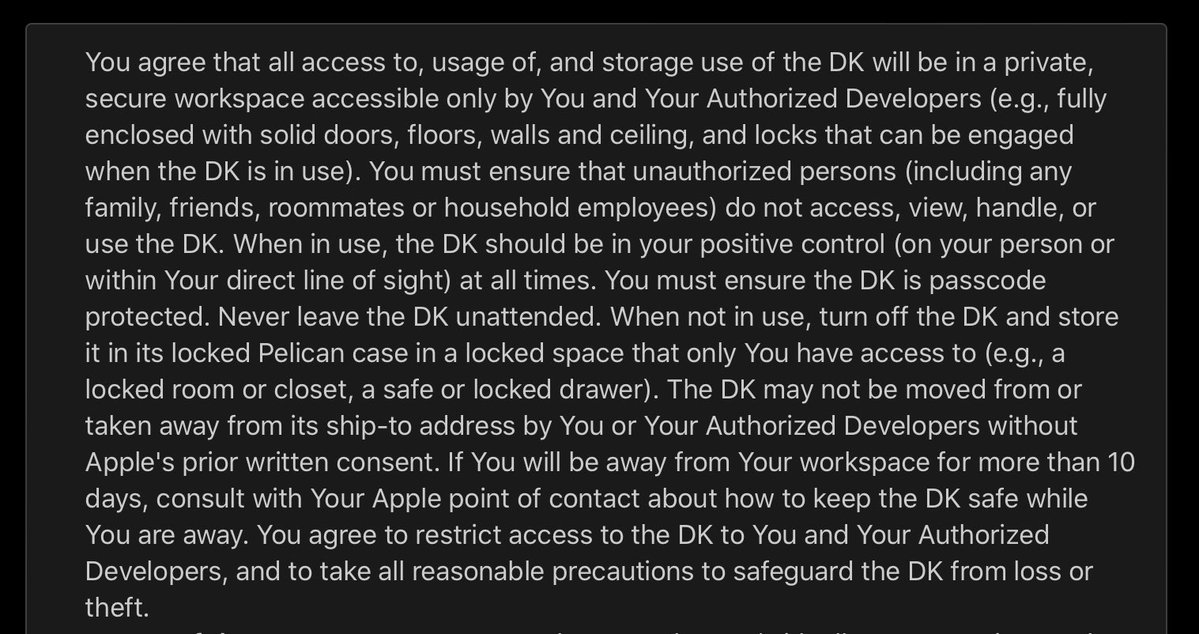

Apple (AAPL – $193.22) is taking applications for Vision Pro developer kits. The company will loan out headsets so that developers can get their apps up and running. The kit also includes help setting up the device, code-level support requests, and “check-ins” with Apple experts about designing and developing an app for visionOS.

Apple said: “Please note this is an Apple-owned development device. The kit will need to stay at its ship-to address in a private, secure workspace accessible only by you and your authorized developers. You’ll have regular check-ins with Apple and you’ll need to return the kit at Apple’s request.” And the user agreement is next-level:

Click for larger graphic

AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $33.81) reported June quarter revenues in line with expectations, down 7.4% from last year to $3.48 billion but up 3% from the March quarter. Pro forma earnings of 45¢ were a penny short of the 46¢ estimate.

For the September quarter, they guided for $3.5 billion in revenues, just under the $3.66 billion consensus estimate, with flat or slightly better earnings than the June period. Analysts were expecting 53¢. In spite of that, the stock closed up on the day.

That’s probably because on the conference call (SLIDES HERE and TRANSCRIPT HERE), management said: “We expect to continue improving profitability and cash flow despite our relatively muted sales environment. Furthermore, our ‘More Corning’ approach is opening additional revenue streams. Taken together, we anticipate strong operating leverage when our markets recover and our volume returns.”

Corning generated $310 million in free cash flow in the quarter. Their gross profit margin did improve a full percentage point from June’s, showing their price increases are sticking. It’s just a question of when volume recovers. They are innovating to drive additional growth:

Click for larger graphic

Click for larger graphic

The CFO said: “Looking ahead, we will continue improving profitability and cash generation in the second half despite our current sales outlook. Overall, we remain well positioned to capture upside, and as sales grow, we’ll drive strong operating leverage.”

Optical Communications had sales of $1.066 billion, down 5% sequentially as near-term demand for passive optical network products remained weak. Net income of $140 million was down 12% sequentially due to the lower volume, moderated by productivity improvements. Going forward, they said major innovation programs are underway in four significant secular trends: broadband, 5G, the cloud, and advanced AI. Corning’s connectivity solutions offer economic advantages for a broader range of customers than ever before, while long-term demand for optical networks is strongly supported by trends in computation and both private and public infrastructure investments.

Their second-largest product area, Display Technologies, had June quarter sales of $928 million, up 22% sequentially. Net income was a very strong $208 million, up 30% sequentially, primarily driven by higher volume. They said that since January, panel maker utilization has increased consistently, driving significant sequential glass volume increases in the quarter. The display industry recovery is underway.

They expect to finalize agreements for a double-digit price increase in third quarter. That will drive improving profitability, and they’ll return to pre-pandemic levels by the end of the September quarter. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2024 .

Meta Platforms (META – $311.71) reported an excellent June quarter and raised 2023 guidance. Revenues grew 11.0% from last year to $32.00 billion, beating the $31.06 billion consensus. Pro forma earnings per share hit $2.98, seven cents better than the $2.91 estimate.

Facebook daily active users were 2.06 billion on average, an increase of 5% year-over-year and just above the 2.03 billion estimate. Monthly active users grew 3% year-over-year to 3.03 billion. For the whole family of apps, the daily active people average grew 7% from last year to 3.07 billion and the monthly active people was 3.88 billion, an increase of 6% year-over-year.

Ad impressions delivered across the family of apps increased a remarkable 34% year-over-year while the average price per ad decreased by 16%.

On the conference call (SLIDES HERE and TRANSCRIPT 1 HERE and TRANSCRIPT 2 HERE), they raised September quarter revenue guidance to $32.0 billion to $34.5 billion, substantially above the $31.18 billion consensus estimate.

CEO Mark Zuckerberg said the Reels annual revenue run rate is up to $10 billion from $3 billion nine months ago. Threads daily active users are exceeding expectations, but they won’t monetize until at scale like everything else. Zuck said: “I’m quite optimistic about our trajectory here. We saw unprecedented growth out the gate and more importantly, we’re seeing more people coming back daily than I had expected. And now we’re focused on retention and improving the basics. And then after that, we’ll focus on growing the community to the scale that we think is going to be possible. Only after that we’re going to focus on monetization.”

CFO Susan Li said they will take their efficiency programs into 2024 and beyond. Costs will still grow in 2024 as they begin hiring again. They are helping free cash flow by deferring taxes to the December quarter and shifting capital spending to 2024. They bought back $793 million of stock in the quarter and finished the quarter with $53.4 billion in cash and $18.4 billion in long-term debt.

Meta and Microsoft introduced the next generation of their open source large language model, Llama 2. It is free for both research and commercial use – they had more than 10,000 requests for access to Llama 1. Meta said: “By making AI models available openly, they can benefit everyone. Giving businesses, startups, entrepreneurs, and researchers access to tools developed at a scale that would be challenging to build themselves, backed by computing power they might not otherwise access, will open up a world of opportunities for them to experiment, innovate in exciting ways, and ultimately benefit from economically and socially.”

Meta rolling out its verified tool to more countries this week. This is a potentially significant revenue stream. Converting 15% of current users would boost Meta’s current revenue base by around 5%. and be a larger EBIT boost, considering how high margin this business should be.

Yahoo Finance wrote: Meta CEO Mark Zuckerberg has led the ‘comeback story of the year.’ They quoted long-time tech analyst Dan Ives of Wedbush: “Meta is the comeback story of the year as Zuckerberg has gone from a villain on the Street to now a ticker tape parade in NYC.” META is a Buy under $150 for a $400 target in 2024.

SoftBank (SFTBY – $25.06) filed their annual report which “presents our corporate story, showing how our strategy and business model will deliver our core philosophy and vision, how we will build value, and how we will enable 300 years of sustained growth.” Great stuff. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $18.64) reported a September quarter loss of 19¢ a share, better than the 22¢ loss expected. On the excellent conference call (INVESTOR LETTER HERE and SLIDES HERE and TRANSCRIPT HERE), management said they produced 22,502 batteries in Fab-1, exceeding the forecast for 18,000. They delivered on their commitment to secure $70 million in non-dilutive financing for Fab-2 in Malaysia. They secured engagements with some key Chinese smartphone manufacturers, Vivo, Xiaomi, Lenovo being three of them. Xiaomi and Vivo are top five global OEMs and Lenovo’s Motorola brand is number three in the US.

CFO Ralph Schmitt said: “We shouldn’t lose sight of what was sort of announced in…Raj’s involvement in some of these mobile phone customers mostly out of China being much more aggressive and actually allowing us to talk about them as being customers and being involved. They’re the ones seeing the absolute need for this uplift because to the points that Raj has been making all day is, they need to enable features and they just can’t do it with the existing [battery] technology that exists out there. So they are pushing very hard and want to partner with us to make that a reality and mostly in mobile platforms today.”

Regarding Artificial Intelligence and the metaverse, CEO Raj Talluri said there are many, many revolutionary computing platforms that are enabled by high performance cameras, high performance memories, image processors, sensors, and displays that marry all this together, along with AI. But none of these new devices will really deliver on the promise to the end consumer until they have a much better battery.

President Ajay Marathe is in Asia, checking the performance and timetable for the equipment headed for Fab-2. He showed this video:

The total size of the US Army order for pre-production cells to be put into early prototypes of their vest is nearly $600,000 for this year, predominantly in the December quarter. But they said this is just a first step in what they hope will be a very significant business in the multiple tens of millions of dollars in the years to come. They are working on making these in Fab1, so they are pivoting production from IoT and wearables to bigger batteries for the Army contract and “a laptop manufacturer.” The laptop contract has not been announced, but I’m pretty sure it is Dell. When that news comes out, the stock will jump.

I am raising the ENVX Buy limit to $20, still for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

By the way, Chairman T. J. Rogers wrote a scathing reply to the ENVX shorts. It’s a fun read.

PagerDuty (PD – $24.68) said market research firm Forrester Research named them a leader in Process-Centric AI For IT Operations (AIOps). PagerDuty AIOps takes in and normalizes events from any source, and then extracts signal from the noise to provide powerful context and noise reduction at scale. Forrester gave PagerDuty its highest possible score in adoption criterion and “goes beyond alerting to automate processes and workflows that accelerate resolutions.”

PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Rocket Lab USA (RKLB – $6.73) scheduled its next Electron launch for Capella Space during a launch window that opens tomorrow. It will be their third launch for Capella. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $1.52) did a fireside chat at the H. C. Wainwright Kidney Conference – wait for the delayed start. Management said vadadustat will “disrupt” the $1 to $2 billion market to treat anemia due to chronic kidney disease (CKD) in adult patients on dialysis.

They will resubmit by September 30. The FDA accepts that within 30 days. They expect a six-month review, giving them a PDUFA date before March 31. They’ll launch right away, but they don’t expect a major uptake until they get their Transitional Drug Add-on Payment Adjustment (TDAPA) status approval, which takes another six months. They’ll get TDAPA around October and the big launch will be in the December 2024 quarter.

About 15% of dialysis patients are treated at home, where an oral drug like vadadustat is preferred. In the dialysis centers, patients on high doses of erythropoiesis-stimulating agents (ESAs) are an obvious first target. Doctors worry about the health risks of giving high doses of ESAs, while centers will be able to replace expensive ESAs that are only reimbursed by the standard bundle payment with separately-reimbursed vadadustat.

They expect to launch in Europe by the end of this year. They have a cash runway over 12 months long. Buy AKBA up to $2 for the vadadustat lunches in the EU, UK, and (after FDA approval in 2024) the US.

Primary Risk: Vadadustat not approved in the US.

Clinical stage of lead product: Vadadustat NDA to be refiled

Probable time of next FDA approval: March 2024

Probable time of next financing: April 2024

Compass Pathways (CMPS – $8.77) had the first clinical study results of psilocybin treatment for anorexia nervosa published in Nature Medicine. As you know, anorexia is a deadly illness with no proven treatments to reverse core symptoms and no medications approved by the FDA. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2023

Medicenna (MDNA – $0.44) presented at the Brain Cancer Research Roundtable organized by the National Brain Tumor Society. He talked about MDNA55 for recurrent glioblastoma, which more than doubled the median survival in end-stage rGBM patients in its Phase 2 trial. So far, they’ve been completely unsuccessful in partnering the compound with someone who’ll fund a Phase 3 registrational trial. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

ScyNexis (SCYX – $2.81) posted an all-new corporate presentation. The key slides included a history of antifungal development:

Click for larger graphic

Click for larger graphic

Their technology is poised to become the next standard of care in antifungals:

Click for larger graphic

So Glaxo SmithKline licensed ibrexafungerp, including Brexafemme for yeast infections and the hospital applications currently completing clinical trials. It’s a very lucrative deal for ScyNexis:

Click for larger graphic

They have a next -generation fungerp in development that is not included in the GSK deal:

Click for larger graphic

Click for larger graphic

With preclinical work in progress to file an IND (Investigational New Drug) and get into human trials.

Click for larger graphic

Click for larger graphic

I am raisng the SCYX Buy Limit to $3 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2023/2024

Probable time of next financing: Never

Inflation MegaShift

Gold ($1,944.00) continues to fluctuate around $1,950. The fractal dimension reversed course this week before getting down to 30. A consolidation most likely has begun, either in the form of a sharp, transient drop (unlikely) or an extended period trading between $1,900 and $1,950 or so (most likely). Nothing to do but wait it out, unless you can see some good options premium to take in.

A Short-Sale or REO House

The median sales price for new houses sold in the US declined 0.5% month-over-month and 4.0% year-over-year in June to $415,400.

Click for larger graphic

Click for larger graphic

I first recommended buying a Real Estate Owned (by the lender) or short-sale (about to go into foreclosure) house in the August 18, 2010 Radar Report at $170,700. There should be another opportunity in 2024. You’ll be able to refinance at lower rates later, and if the rental is cash flow positive with a 7% mortgage, you’re good anyway. The banks will be giving away real wealth. If you can find a deal that is a cash flow positive rental, take it! Core holding.

Primary Risk: Housing will weaken if and when interest rates rise substantially or in an economic downturn.

Miners & Related

Sandstorm Gold (SAND – $5.25) posted a second installment of CEO Nolan Watson answering shareholders’ most asked questions, unscripted.

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $29,157.48) is pinned under $30,000 for now.

Click for larger graphic

Click for larger graphic

A research report from crypto trading firm NYDIG says bitcoin spot-based exchange-traded funds could bring $30 billion in new demand for the world’s largest digital asset, but the only way spot ETFs will happen is if the Grayscale Bitcoin Trust wins its lawsuit against the SEC.

The Bitcoin Fear & Greed Index is neutral, so it doesn’t seem likely that a major selloff is in the cards.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $18.39) is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $79.80

Oil rose for the fifth week in a row to a three-month high as the Russia-Ukraine war intensified and it became obvious that the Saudi voluntary cuts will last into yearend.

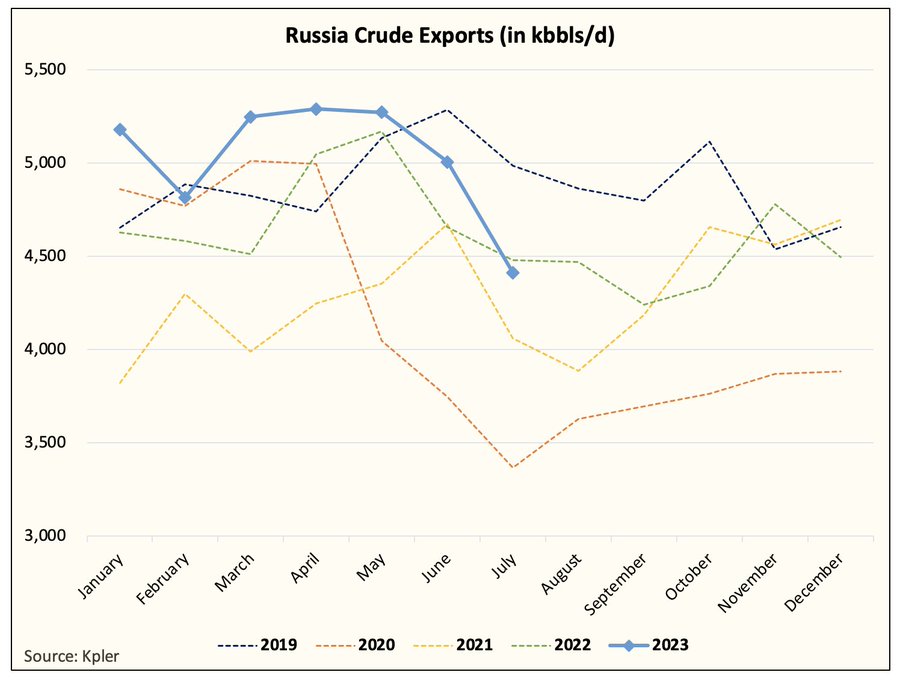

We’re moving from demand fears and negative sentiment keeping oil prices stagnant to Goldman Sachs expecting “all time high” oil demand to spur large deficits, boosting prices in the near-term. After China and India’s imports of crude oil from Russia hit an all-time high in June, Russian crude exports are falling:

Click for larger graphic h/t @HFI_Research

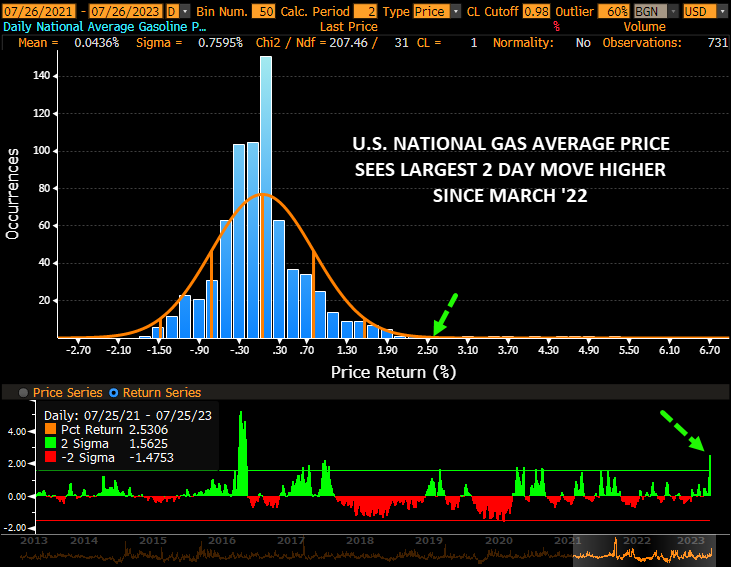

As you’ve probably noticed, gasoline prices are on the move up, with the largest two-day jump in the national average price since March 2022.

Click for larger graphic

Click for larger graphic

The July 2026 Crude Oil Futures (CLN26.NYM – $67.05) are a Buy under $65 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $36.37) is a Buy under $35 for a $100+ target.

EQT (EQT – $41.42) reported June quarter revenues down 59.7% to $1.02 billion, just above the $993 million estimate. Their average realized price fell to $2.11 million cubic feet equivalent (Mcfe) from $3.21/Mcfe in the year-ago quarter. The pro forma loss of 17¢ per share was much better than the 27¢ loss expected. While June quarter production and capital spending were at the midpoint of their guidance, their operating expenses were near the low end of guidance.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management maintained full-year guidance of 1.9 trillion to 2.0 trillion cubic feet equivalent total sales volume and $1.7 billion to $1.9 billion in total capital spending, including $1.4 billion to $1.535 billion planned for reserve development.

During the quarter, they retired another $800 million of debt, bringing them to a total of $1.9 billion retired. They are drilling 68% faster than the average of their peers and set a new world record of 18,200 feet drilled in one 48-hour period. They completed one four-mile-long lateral in the quarter, one of the longest in the history of US shale.

They’ve hedged about 30% of 2024 production at a weighted average floor of $3.64 per million BTU. They now expect the Tug Hill/Xcl Midstream acquisition to close by the end of September.

Click for larger graphic

As HFI Research wrote,Natural Gas Is Sitting In The Comfort Zone. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $5.87) will go up with uranium prices.

UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

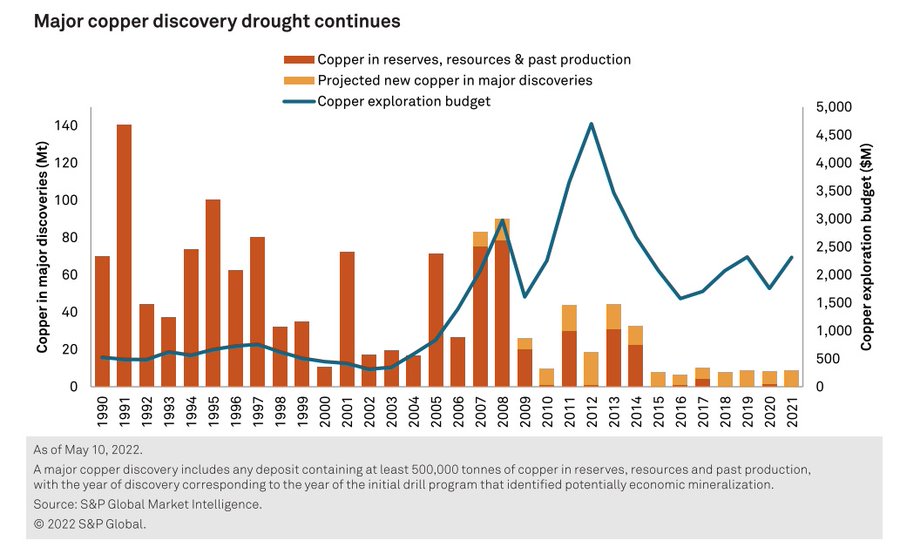

Freeport McMoRan (FCX – $43.29) has a lot of copper when the world is in the middle of a Copper Discovery Drought. The demand headwinds are obvious (China slowdown, etc.). What’s not so obvious is that we haven’t found a Major New Copper Discovery since 2014. The longer the drought, the more significant the supply imbalance

Click for larger graphic h/t Brandon Beylo

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

RIP Sinead O’Connor

* * * * *

And goodbye to Tony Bennett

* * * * *

Your supporting 9th-grader Joshua recover from brain cancer Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $193.22) – Buy under $150 for new iPhones

Corning (GLW – $33.81) – Buy under $33, target price $60

Gilead Sciences (GILD – $76.51) – Buy under $80, target price $120

Meta (META – $311.71) – Buy under $250, target price $400

SoftBank (SFTBY – $25.06) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $18.64) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $46.21) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $16.94) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $24.68) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $8.18) – Buy under $10, target price $40

Rocket Lab (RKLB – $6.73) – Buy under $13, target price $30+

Velo3D (VLD – $1.98) – Buy under $6, target price $50

$20-for-$1

Akebia Biotherapeutics (AKBA – $1.52) – Buy under $2, target $20

Aptose Biosciences (APTO – $3.95) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $8.77) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.50) – Buy under $7, hold a long time

Invitae (NVTA – $1.32) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.44) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.81) – Buy under $3, target price $20, then $50

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($24.30) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $25.87) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $28.88) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.41) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $26.60) – Buy under $30, target price $50

Coeur Mining (CDE – $2.92) – Buy under $5, target price $20

First Majestic Mining (AG – $6.28) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.33) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.25) – Buy under $10, target price $25

Sprott Inc. (SII – $32.05) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $29,157.48) – Buy

Grayscale Bitcoin Trust (GBTC – $18.39) – Buy

Ethereum (ETH-USD – $1,861.27) – Buy

Grayscale Ethereum Trust (ETHE – $10.66) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $67.05) – Buy under $65; $200+ target

United States 12 Month Oil Fund, LP (USL – $36.37) – Buy under $35; $100+ target

EQT (EQT – $41.42) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.87) – Buy under $8; $30 target

Freeport McMoRan (FCX – $43.29) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $31.63) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $24.00) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $13.07) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $29.51) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.24) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $0.95) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $2.10) – Hold for buyout

Graphite Bio (GRPH – $2.49) – Hold until they update their strategy

TG Therapeutics (TGTX – $19.82) – Hold for buyout at $30+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First

2

FCX is moving higher. Thanks for the update on SCYX. I bought some more @ $2.00 and change. SMCI is HOT. My $5,900 stake is now over $29,000. Nailed it. Oil keeps coming back from the dead.

MM – thanks for the newest report. Your excitement for Bitcoin seems to be cooling and almost dependent on whether or not a spot ETF is approved – what is the timing for a decision on the Greyscale lawsuit and do you still believe bitcoin hits $100,000 and when?

The Grayscale decision could come any day. I still think bitcoin hits $100,000. It should happen before the next halving in the first half of 2024 but may slide to the 2028 halving.

MM–please address the negative article on QUIK linked by Roger in Seattle on the last board.

Strange article – it basically says their past does not justify the current n the current price is based on expected future results. As he mentioned, the company is growing 30% a year and will have positive non-GAAP operating income in the CURRENT quarter, And his comment “especially if those operating expenses are not going to be tamed in the long-run” is weird since they have been REDUCING opex quarter-by-quarter.

He wrote: “Since they are the leading provider of open reconfigurable computing solutions on fully open-source software and hardware, I thought that this would come with some sort of profit margin. I guess I was wrong.”

No, you were right. They have about a 90% profit margin on their IP licenses.

Also: “if a company’s share price doubled but shares outstanding also doubled that means your holdings essentially went nowhere.”

No, your stock doubled.

Good, thanks.

MDNA – MM you have the following projection for MDNA’s first FDA approval:

Probable time of first FDA approval: 2024

What product are you expecting to be approved in 2024?

As you mentioned, MDNA has been unable to find a Phase 3 partner for MDNA55 ever since they completed their Phase 2 trial in late 2020. So that program appears dead in the water. Meanwhile, the MDNA11 ABILITY Phase 1/2 trial hasn’t yet started Phase 2. So what’s getting approved next year?

With limited cash & an inability to advance their molecules into Phase 3 trials, what are the realistic prospects for MDNA, hope for a buyout?

Yeah, 2024 was for MFNA55. I think they can get MDNA11 to the finish line, but someone else probably will own them.

Hi Guys, I am a lifetime member here. Recently I am receiving news letter from “Boomberg”. What is this service? I did not subscribe to this service. And they are asking for paid subscription. Is it different from what we have here or different? Really confused here. Thanks for all your inputs.

It is another venture that mm is doing that and biotech moonshots and yes he is selling subscriptions most of the the picks from the biotech moonshot newsletter he is selling is mostly comprised of the biotech picks from the new world investor newsletter from what he states,as for myself I will not be buying any other newsletter he is pushing until nvta gets back to at least 36.01 that was when he suggested for everyone to buy buy buy after Cathy woods sold and the stock went from 50.42 to 36.01,that was when he stated it was time to lock in a full position .

And that was March 4th 2021 when mm suggested to take a full position in nvta if we didn’t already do so.

Cathy and CLM Pro are both well worth fallowing. I sold 75% of my in at $12 NVTA on them. wish i had sold it all then the last went as end of year tax loss 2022 and haven’t looked back. but its all on me MM has great Picks and on the Bio side has numerous 10 bags but the ideas are MM and the buys are mine, so i don’t jest count on MM. I used to use BioInvest.com but Jim is no longer at the helm and its not the same with the kid. so im mostly using Cathy, CLM and to a lesser extent Biopub as a balance for MM

are there other resores you use for Bio that have been working? streakey as bio is.

thanks

Is Biopub still into AUPH, CWBR, DMAC and VTGN?

actually its my second round with BioPub after letting it go for a year and im begining to think I was right to have let it go in the first place.

it appers to be a dead site in a lot of arreas or i jest cant figure out how to use it. most of the stuff i fallow has been dropped there and I cant find a susinct path of discution everything jumps around topic to topic. you had any lock using biopub?

I acquired positions in all four I mentioned (plus a position in NVDA pushed to extremes by member Dr. Helen Ong, early enough to now be up 1000%) but only AUPH (which I took some profit in at 30 and replaced those shares in Dec under 5) shows a profit. Otherwise I was disappointed I could not get answers to my questions and dropped out when he raised his price. (Wish I’d dropped ARTH when he did though.)

TG Therapeutics: Addressing The SC Ocrevus Concern (NASDAQ:TGTX) | Seeking Alpha

An update from an analyst with a strong buy.

The 5 big Socks which you are discussing on substack seems like a remake of “the other end of the barbell” strategy, which I thought you were supposed to do in NWI for years….maybe a decade.

Seems like you should reveal the big 5 and discuss fully here as well at no additional charge.

I understand your need for new marketing and revenue, but feels like you should honor your past promises here as well ?

Those stocks are way too risky for the conservative end of the barbell. Apple, Meta, and SFTBY provide plenty of exposure to AI and the metaverse.

APTO??? Bought it at $6 45 days ago and only down 50%!!

MM- Any Thoughts?

YES, MM, you should also respond on our repeated questioning about the article on QUIK posted by Roger in Seattle on the last board. QUIK has plunged, as warned in that article. You have long noted that you like to read alternative points of view to your uber bullishness on your picks.

Today’s winners . FCX up $1.02 , TGTX up .99 , SOFI up 19 percent, VLD up 10.63 percent. Analysts at S&P Global estimate that copper production will be nearly 10 million metric tons short of annual demand by 2035. “You don’t need to take big risks to make five to 10 times your money in the space” Dan Ferris

TGTX–near 50% plunge to $11 this AM after revenue and “earnings” misses. We had opportunities to sell at $30-35. The only times I had good results from NWI was when I took profits after big runups. I ignored my lessons learned because of hopium about pie in the sky projections that Briumvi would be the holy grail of MS treatments. Complete nonsense. Briumvi is merely the best current drug for MS, but it doesn’t address root causes of MS. Nearly all NWI stocks must be traded. Sell on optimism, buy on pessimism. If there are any NWI subscribers who sold TGTX above 30, a reasonable strategy is buying here around 10.

NWI is a minefield of disasters with only a small chance of success.

MM, with an open, unbiased mind, please respond to our questions about QUIK, APTO.

TGTX ran too far too fast. It was overvalued at the top and even yesterday. I do believe they have the best MS treatment on the market. But it’s just a matter of time until NervGen’s drug hits the market and people start trying it for MS. NervGen (NGENF) is scheduled to begin a 16 week trial in Spinal Cord Injury (SCI) within the next few weeks. Any improvement in chronic SCI patients should rocket the stock. I believe the next indication they will try their drug in is CVA or stroke. This is unfortunate for MS patients as NervGen’s drug may be the best treatment for MS as well. However, a Phase 2 trial in stroke patients can be a lot cheaper than a Phase 2 in MS. Also, not nearly as much competition in stroke as in MS. To read about what their drug can do for MS, read here: https://www.nature.com/articles/s41467-018-06505-6

Good info about NGENF. The main problem with trials for stroke is that recovery is highly variable. “Mini stroke” is a relatively new name for “transient ischemic attack” or TIA. As TIA implies, recovery is very quick–minutes to hours. Some major strokes show recovery in days, others take months. It is near impossible to have matching stroke groups for the same baseline stroke severity just after the stroke. It would take a large number of patients to have enough randomization to draw meaningful conclusions. A small phase 2 won’t cut it.

There’s little or no spontaneous recovery from SCI, so a small SCI trial should be more meaningful than for stroke. I wonder how MM is doing in his stroke recovery from a few years ago.

I do like NGENF’s approach to brain conditions better than TGTX’s. NGENF has a plausible product which targets brain repair, whereas TGTX’s Briumvi is merely a blunt instrument that manipulates lymphocytes, which has consequences for the immune system elsewhere. Eventually, cancers and infections will occur from the immunodeficiency from Briumvi.

Imagine an initial Phase 2 trial in stroke with matched groups on the 42 point NIH Stroke Scale 7 days after CVA. One group gets std of care treatment plus a daily saline injection and the other gets std of care plus a daily NVG-291 injection. If you see significantly better or faster improvement in the NVG-291 group after X weeks, then that would warrant a larger trial if p value is less than .05%, would it not?

Agree, except that I believe it is difficult to obtain MATCHED groups for stroke. Perhaps you can find matched groups for the NIH Stroke Scale at 7 days, but you cannot predict how individual stroke patients will spontaneously improve after a longer time in weeks, months, years. Group A may have patients that are doing better after 6 months than group B, if A and B get no treatment. Say B gets NVG-291 and A gets none. Suppose after 6 months, B does about as well as A. To me, this could represent an excellent effect of NVG-291, since without NVG-291 B would have done worse. But the trial will be pronounced a failure because A and B couldn’t be fairly matched.

In real world practice of uncontrolled trials, we use plausible evidence to try safe strategies on individual patients. Yesterday, I was excited to spend 2 hours with a new patient. She has a history of several chronic (perhaps autoimmune) diseases–ulcerative colitis, Graves’ hyperthyroidism, fibromyalgia, chronic fatigue, migraine headaches. I had read about great clinicians’ experiences with treating these diseases by correcting leaky gut. These clinicians don’t use drugs for symptom relief in these patients. The drugs have limited benefit and have lots of side effects. All the noted experts in many specialties follow drug treatments only. They refuse to recognize the importance of nutrition in treating the leaky gut which is the root cause of these conditions. However, my patient had observed for herself the benefit of following a gluten/dairy free diet. Her wrongheaded specialists insisted that there is no evidence showing that nutrition matters. The truth is that there is good evidence showing that nutrition does matter, but these drug pushing specialists whose clinical trials are funded by Big Pharma have a vested biased interest in closing their minds to the real benefits of non drug treatments. My own experience confirms what these great holistic clinicians know, and it was gratifying to hear from my patient about her success. I told her to ignore her specialists and do what we both know helps her.

They over promised and under delivered and took a haircut. Lesson learned . They still made good money and had good forecast. It was a market knee jerk reaction. Unless you get everything exactly right now there will be a short term sell off because expectations are insane. I agree , I bought some more today at bargain basement prices. IMO. I am surprised MM didn’t have a flash alert !!

100% sequential revenue growth is a good quarter. They needed to tell Cantor Fitzgerald their $24 million to $32 million estimate for the June quarter was ridiculous.

The European distribution deal is excellent. Strong Buy.

100% growth from very low initial sales is nothing to get excited about. We want to see CONSISTENT SUSTAINED sequential growth at maybe 20% or more. 20% to the 4th power (1 year) is 100%, or 2x. At 2 years, that’s 4x. At 3 years, that’s 8x.

At 25% quarterly growth, that’s 2x in 3 quarters, 4x in 6 Q, 8x in 9 Q.

At 41.4% Q growth, that’s 2x in 2 Q, 4x in 4Q. It will take something like this to justify higher stock prices after a year.

MM, Please comment on TGTX. Very disappointing once again.

The Bullish Analyst on TGTX posted an update on results:

TG Therapeutics: The Hype Is Gone (NASDAQ:TGTX) | Seeking Alpha

“Results fell short of my above-consensus expectations”

I expect $25+ million in the current quarter, 56%+ sequential growth..

MM, Is tgtx now a Buy?

Yes.

Today’s Radar Report may be late. My youngest daughter broke both bones in her lower arm when the horse she was riding stepped in a gopher hole and went down, fortunately not on her (big horse) . Amazingly, the horse is OK. Rose is in the ER and we’re waiting to hear if an operation is needed.

That had to be quite a scare. Fortunate that she didn’t end up under the horse. Hope you get good news regarding the arm.

Radius broken in two places, ulna in one. The surgery is next Tuesday. Could have been way worse. I’m teaching her to drive, so that goes on hold for a while.

Childhood accidents are a parents’ worst nightmare! You all dodged a bullet on this one. She’s young, her bones will mend. And, these kind of events are character-building life lessons for her.

I hope your daughter is feeling better.

The Radar Report for 8.3.23 is posted. Made TGTX a Top Buy Near-Term under $12.