Dear New World Investor:

This morning’s Personal Consumption Expenditures Index (PCE) announcement showed October prices grew 3% year-over-year, down from 3.4% in September and in line with expectations. The core PCE, which excludes volatile food and energy prices and is the Fed’s favorite measure of inflation, grew 3.5%, down from 3.7% inSeptember and also in line with expectations. Month-over-month, the core PCE rose 0.2% in October, down from 0.3% in September.

While both the core Consumer Price Index (CPI) and core PCE clearly are in a downtrend, they are a long way from the Fed’s 2% target.

Click for larger graphic

Click for larger graphic

What this means is the Fed is on hold – no further increases needed when inflation rates are steadily declining,

BUT

no interest rates cut either, until at least the core PCE gets closer to 2%.

“Higher for longer” will be replaced by “high for longer” and those expecting rate cuts early next year will freak out and try to get you to panic-sell your stocks. Don’t listen to them. I still think we’ll have a mild 2- to 3-quarter recession before this is all over, but basically Chairman Powell is going to both bring inflation down and pull off his pretty soft landing.

On another topic, we’ve now seen nine straight months of downward revisions to private (non-government) nonfarm payrolls and more than 50% of the supposed job creation from the birth/death model of small companies has disappeared, all in the middle of the biggest bankruptcy cycle since 2010. At some point I expect the revisions to show a negative payrolls number, although they’re unlikely to show that in the initial report during a Presidential election year.

Click for larger graphic h/t @DiMartinoBooth

My sense is that both retail and institutional investors are getting more bullish, although BofA says asset allocators are bearish on stocks and bullish on bonds.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

But American Association of Individual Investors (AAII) Bulls are up to 48.8%, the highest since last summer when they were 51. Bears are now teenagers at 19.6%, the lowest since June 2021. Folks have finally gotten in the pool.

Click for larger graphic

Click for larger graphic

Market Outlook

The S&P 500 added 0.2% since last Wednesday, closing November with an 8.9% gain. The S&P 500’s rally of the past few weeks has been impressive, with the percentage of stocks trading above their 50-day moving average swinging from 10% to 72%. The Index is up 19.0% year-to-date.

The Nasdaq Composite lost 0.3% but still booked a 10.7% gain in November. It is up a whopping 35.9% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 3.7% as the biotech bear market ended with a 14.0% gain in November. It is down 9.0% year-to-date.

The small-cap Russell 2000 moved up 0.8% since last Wednesday and 8.8% in November. It is up 2.7% in 2023. Since 1979, the four-month stretch between November and February has been the strongest of the year, favoring small-cap over large-cap returns:

Click for larger graphic h/t @chigrl

Click for larger graphic h/t @chigrl

Investors are sitting a record $5.7 trillion cash in money-market funds. That’s a potential tailwind for stocks and bonds if the inflation outlook continues to improve.

Click for larger graphic

The fractal dimension fell below 55, signifying the consolidation is over and a new uptrend is underway that can last for months.

Top 5

Changes this week: None

Near-Term – chronological order

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage this fall

SFTBY SoftBank – for ARM IPO valuation

AKBA Akebia – Vadadustat approval March 27, 2024; TDAPA approval October

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The second estimate of September quarter real GDP growth was raised from +4.9% to +5.2%. Remember that the Atlanta Fed’s GDPNow model had estimated +5.4% after forecasting a very strong quarter for months when Wall Street was looking for +4.5% and the Blue Chip economists were at +3.5%.

Click for larger graphic

Click for larger graphic

Much of the revision – 1.4 percentage points – was due to increased inventories, which will reduce December quarter real GDP. This morning’s GDPNow estimate for the current quarter dipped to +1.8%, still above the Blue Chip economists.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Tuesday, December 5

RKLB – Rocket Lab – Unspec. – Morgan Stanley Space Summit

Thursday, December 7

Pearl Harbor Day

Friday, December 8

November payrolls – 8:30am

Saturday, December 9

APTO – Aptose Biosciences – 6:15pm – American Society of Hematology (ASH) annual meeting

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Corning (GLW – $28.50) VP of Investor Relations Ann Nicholson presented at the UBS Global Technology Conference (AUDIO & SLIDES HERE and TRANSCRIPT HERE). It was the standard presentation.

Click for larger graphic

Click for larger graphic

Corning is dirt-cheap and well-run, but three of their major markets – large-screen TVs, smartphones, and autos – are consumer products that Wall Street fears will be hurt in a deep recession. If I’m right about a shallow recession, GLW should hit my 2024 target. As Ann said: “We’ve been executing plans to improve profitability and cash flow during this current period of lower volume. So while we’re not certain when our markets will return, we’re confident that they will. And when they do as a result of our execution, we expect improving leverage on that volume.”

“So looking ahead, we have the capacity and the capability to deliver $3 billion plus in additional sales with minimal additional cash investment. This revenue will have strong incrementals as it returns. And it represents a significant opportunity.”

And we get a 3.97% dividend while we wait! GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2024 .

Gilead Sciences (GILD – $76.60) CFO presented at both the Evercore ISI HealthCONx Conference (AUDIO HERE and TRANSCRIPT HERE) and the Piper Sandler Healthcare Conference (AUDIO HERE and TRANSCRIPT HERE). His message at each was the same: “…the readouts that I would really highlight and there’s a number of them, but first and foremost, Trodelvy, which is, for those of you that don’t know Gilead as well as our Trop-2 directed antibody drug conjugate that we acquired by acquiring Immunomedics. The product is approved in three different solid tumors already, two forms of breast cancers and bladder cancer.

“We have a very extensive late stage clinical development program underway in multiple tumor types, including earlier lines of breast cancer, earlier lines of bladder cancer and lung cancer. Next year, there will be a lot of data, but two things that I would highlight, in particular, our EVOKE-01 study of Trodelvy in second-line non-small cell lung cancer. This is a Phase 3 study that we’ll read out in the first half of next year…The other data set next year that is important is the second line bladder cancer data set that’s coming, again, Phase 3 data set. So it’s an exciting time for Trodelvy.

“Maybe I’ll transition then there are two other — again, there’s at least five or six Phase 3 data readouts next year. One other one that is incredibly important is lenacapavir, which is our novel, it’s already approved, it’s an HIV capsid inhibitor that’s dosed subcutaneously every six months. We started our prevention, HIV prevention, studies a couple of years ago, at least the first of the two Phase 3 studies, if not both of them, will read out by the end of next year. HIV prevention is an extraordinary opportunity for Gilead and for people that are at risk of getting an HIV, this could be a really transformative development. So that data will come next year.

“And then, finally, one of the two studies that we had started with our oral broad acting nuc that can be used in COVID and other emerging viruses, we’ll have a data readout next year in the ordinary risk or regular risk patients. So that’s just the tip of the iceberg. There’s a lot of Phase 2 data coming next year as well “

Gilead cut 7% of the staff at their Kite Pharma unit as they introduced a “refreshed business strategy” (= cut costs). GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $327.15) is far ahead of its competitors in Artificial Intelligence due to their now 10-year-old Fundamental AI Research team. They have made impressive strides in the past 10 years in object detection with Segment Anything, which recognizes objects in images. They built a model that could translate across 100 languages without relying on English, which most recently expanded text-to-speech and speech-to-text technology to more than 1,000 languages. I didn’t even know there were 1,000 languages.

Earlier this year they released Llama, an open, pre-trained large language model, followed by Llama 2, which is free for research and commercial use.

Click for larger graphic

META is a Buy under $150 for a $400 target in 2024.

Small Tech

Fastly (FSLY – $16.60) CEO Todd Nightingale and CFO Ron Kisling presented at the UBS Global Technology Conference (AUDIO HERE and TRANSCRIPT HERE). Management said: “We’ve built — organically built a bot mitigation solution, leveraging the data that we have at the edge built into that edge, and it’s super exciting. It’s in beta right now. We have a ton of customers running the beta, it will be limited availability, start closing deals before the end of the year and GA [general availability] in Q1. And that will really complete I think the security portfolio today that we really need, which is super exciting.”

The company was named a Leader in The Forrester Wave: Edge Development Platforms, Q4 2023 report, which evaluates software and development platforms that enable developers to build applications that tap into distributed managed infrastructure. Fastly’s Compute@Edge received the highest rating possible in 22 criteria, including vision, innovation, roadmap, pricing flexibility and transparency, runtime execution environment, and security features criteria.

The stock was hit today after Chief Revenue Officer Brett Shirk resigned effective December 1 to pursue another opportunity. His resignation was not due to any disagreement with the company on any matter related to its operations, policies or practices. I’m sorry to see him go, but the truth is Chief Revenue Officers are like Chief Financial Officers – they’re easily replaced, often by someone better. Take advantage of this drop. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $21.80) reported good October third quarter results after the close today. Revenues grew 15.4% from last year to $108.7 million, just above the $107.34 million consensus estimate. Pro forma earnings of 20¢ per share were almost 50% higher than the 14¢ estimate, and even above the highest Wall Street estimate for 18¢.

On the conference call (ZOOM HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Jennifer Tejada said annual recurring revenue grew 13% year-over-year to $438.9 million. Customers with annual recurring revenue over $100,000 grew 10% to 778 as of October 31, compared to 710 in the year ago period. Their dollar-based net retention rate was 110%.

Total free and paid customers grew about 18% to more than 27,000. New customers – “lands and expands” – included Banco Santander, Carhartt, Carparts.com, Cloudflare, Docaposte, Equinix, Salesforce, Snowflake, and The Vanguard Group – some very sophisticated companies. PagerDuty has delivered AI-based tools for years:

Click for larger graphic

Click for larger graphic

They guided for December quarter revenues of $109.5 million to $111.5 million, in line with the $110.29 million estimate, and 8% to 10% above last year. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $10.99) was selected by an unnamed “leading global semiconductor company” for an eFPGA IP license targeting the United Microelectronics foundry’s 22 nanometer platform. QUIK was chosen for its ability to deliver a customized eFPGA IP version within one quarter of contract signing, and the short time for creating subsequent eFPGA IPs. The company will deliver the eFPGA IP in the March quarter, booking the revenue with a very high gross profit margin. QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets and wearables.

Primary Risk: New sensor hub competitor emerges.

Rocket Lab USA (RKLB – $4.38) has completed payload integration for their 42nd Electron launch. The last step before launch day is a wet dress rehearsal to confirm all systems are ready for lift-off. They are targeting no earlier than December 13 for the launch of this dedicated mission for QPS Inc.

They have more than 20 spacecraft in development on their spacecraft production line. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $0.97) sold a Sapphire printer that is calibrated to produce parts in M300 tool steel, an ultra-low carbon alloy with high-strength and hardness properties derived from intermetallic compounds rather than carbon content. The buyer, Atomic Industries, is a creator of artificial intelligence-powered manufacturing solutions for aerospace, automotive, and energy customers. Atomic Industries is the first company to qualify M300 tool steel for injection molding tooling with the Sapphire printer.

The company exchanged the $70 million of senior secured convertible notes they sold on August 10 for $12.5 million in cash, 10 million shares of stock, and $57.5 million of new of senior secured convertible notes. This was expensive but necessary to cure the technical default to maintain minimum levels of quarterly revenue through the quarter ended June 30, 2026. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $1.06) presented at the Piper Sandler Healthcare Conference (AUDIO HERE). Management said they are very confident that vadadustat will be approved. Competitor products require a patient to be on dialysis for four months before starting the drug. Akebia hopes to avoid that on the label because their trials included 1,000 patients that started dialysis after being on the drug, with no significant safety signal. Buy AKBA up to $2 for the vadadustat launches in the EU, UK, and (after FDA approval in March 2024) the US.

Primary Risk: Vadadustat not approved in the US.

Clinical stage of lead product: Vadadustat PDUFA date 3/27/24

Probable time of next FDA approval: March 27, 2024; TDAPA October

Probable time of next financing: Late 2024 or never

Aptose Biosciences (APTO – $2.43) will present the latest data on the tuspetinib/venetoclax dose escalation trial at the American Society of Hematology (ASH) annual meeting on Saturday, December 9. I think they have treated over 45 patients with continued outstanding results. APTO is a Buy under $2.50 for a $300 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Compass Pathways (CMPS – $5.98) did a fireside chat at the Evercore ISI HealthCONx Conference (AUDIO HERE). There wasn’t much they could say about the Phase 3 trials. They still expect the Phase 2 PTSD safety data by the end of this year, with efficacy data early in 2024. In mid-2024 we get the top-line data from the first Phase 3 trial in treatment-resistant depression. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

ScyNexis (SCYX – $1.68) has a new 5.35% holder of 2,237,048 shares: Kingdon Capital Management. Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2023/2024

Probable time of next financing: Never

TG Therapeutics (TGTX – $12.81) also did a fireside chat at the Evercore ISI HealthCONx Conference (AUDIO HERE). It was a deep-in-the-weeds conversation about the multiple sclerosis market, when distributors build inventory (Spoiler Alert: December), and what’s coming. CEO Michael Weiss didn’t give any hints about how the quarter is going, but I still expect more than $35 million in Briumvi sales versus $25.1 million in the September period. Buy TGTX under $12 for a target price in a buyout of $30 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,059.00) finally is breaking out, closing the month above $2,000 for the first time ever. The all-time high is $2,074.88 reached in August 2020. We are just $16 away. The fractal dimension is rapidly headed for the 55 level that will confirm a new trend. It looks like we could be near all-tine highs just as a new uptrend is starting. At the least, we’re likely to see a substantial rally in coming months. At the most – fireworks!

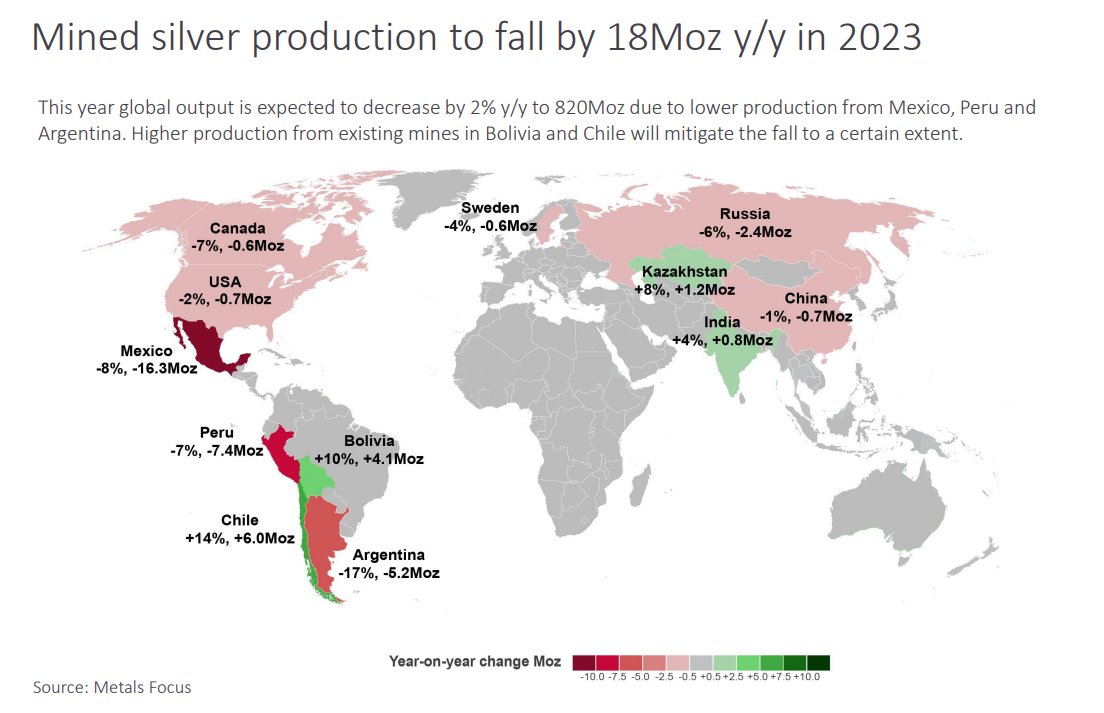

Silver stocks are declining, in part because annual production is falling. That hurts this quarter’s earnings, but lower production means much higher silver prices in the future, which means much higher prices for miners.

Click for larger graphic h/t @chigrl

Click for larger graphic h/t @chigrl

Click for larger graphic h/t @chigrl

The longer term silver chart shows massive bullish potential:

Click for larger graphic h/t @JamieSaettele

Click for larger graphic h/t @JamieSaettele

Ways To Invest:

A Bag of Junk Silver ($25.67) is a Buy for a hold until 2024-2025.

Global X Silver Miners Exchange-Traded Fund (SIL – $27.69) is a Buy up to $30 for a first target of $50 when silver gets back over $40. The silver miners should outperform both the large and junior gold miners in the next upleg for precious metals that will run until 2024-2025.

Sprott Physical Gold and Silver Trust (CEF – $19.31) is a Buy under $18 for a target price of $30.

First Majestic (AG – $5.97) is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Coeur Mining (CDE – $3.06) presented at both the Bank of America Leveraged Finance Conference (SLIDES HERE) and the Scotiabank Mining Conference in Toronto (SAME SLIDES HERE).

Coeur produces both gold and silver.

Click for larger graphic

They are especially interested in silver.

Click for larger graphic

So they’ve invested heavily to expand the Rochester silver mine. That investment starts paying off in 2024.

Click for larger graphic

I think Wall Street will have a much different view of Coeur by the end of next year.

Click for larger graphic

Click for larger graphic

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk of all of these: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $37,647.47) is holding up well as we wait for the SEC to approve spot exchange-traded funds. Anticipation of a fund has helped to spur inflows into digital-asset investment products for a ninth consecutive week, the longest run since the crypto bull market in late 2021. Those products, such as trusts and exchange-traded products, saw inflows of $346 million last week, with Canada and Germany contributing to 87% of the total, according to CoinShares. Only $30 million came from the US, a sign of continued low participation from Americans.

Click for larger graphic

Click for larger graphic

The people who hold a large majority of the world’s wealth still have zero bitcoins, yet over 93% of all bitcoins that will ever exist have already been mined. Trillions of dollars will be scrambling for a few coins. Get there first.

Click for larger graphic h/t Bullion By Post

Click for larger graphic h/t Bullion By Post

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $30.26) is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $75.63

Oil slipped today after OPEC+ agreed to additional output curbs of one million barrels a day (bpd), Saudi Arabia extended its voluntary one million bpd cut to the end of March, and Brazil agreed to join OPEC+ on January 1. Brazil is the world’s sixth largest oil producer and resides in one of the few remaining growth basins in the world. That’s all very bullish for oil prices, so why did they come down?

Because traders think there will be substantial cheating and because OPEC+ set the next meeting for June 1, implying no further efforts to shore up oil prices. The additional cuts announced so far, all lasting till the end of March: Oman: 42,000 bpd, Kazakhstan 82,000 bpd, Russia 500,000 bpd, Kuwait 135,000 bpd, Algeria 51,000 bpd.

Except for Saudi Arabia and Russia, most of OPEC+ can’t even produce enough to hit their current quotas, so I’m not sure this changes much. The Saudis clearly want oil between $80 and $100, and the only non-OPEC+ country with significant spare capacity is Iran. So I expect they’ll get what they want in 2024.

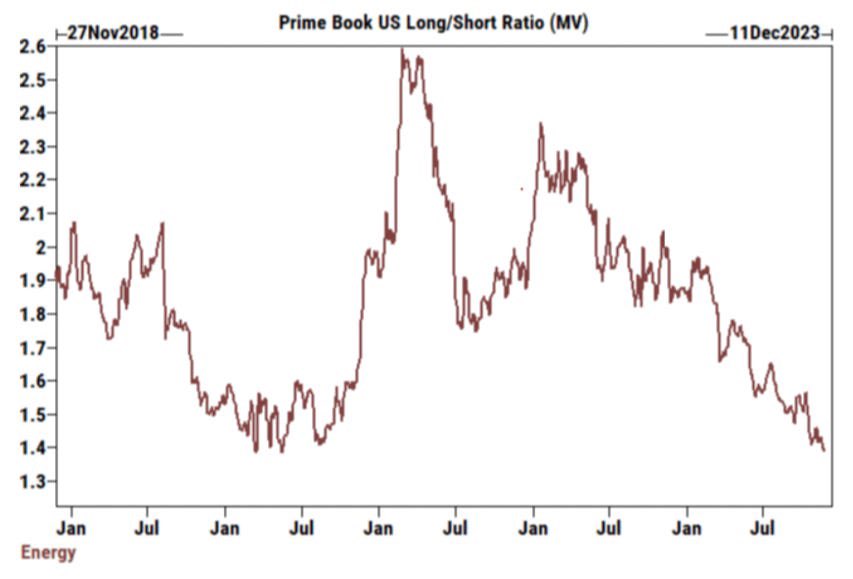

Click for larger graphic h/t @UrbanKaoboy

Meanwhile, hedge fund positioning in energy stocks is near year-to-date lows – a contrarian buy signal.

Click for larger graphic h/t @jessefelder

Click for larger graphic h/t @jessefelder

This week showed the first crude draw in six weeks and I expect a very large draw next week, so this should be a good time to start or add to a futures or OIL position.

The July 2026 Crude Oil Futures (CLN26.NYM – $68.58) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $36.69) is a Buy under $40 for a $100+ target.

Freeport McMoRan (FCX – $37.30) is one of the largest copper miners in the world. Over the course of human history, we’ve produced 700 million tons of copper. To reach Net Zero by 2050, we’d need to produce 1.4 billion tons of copper over the next 27 years. Doubling all of human history production in less than three decades? That’s not going to happen without much higher prices.

Click for larger graphic h/t @marketplunger1

Click for larger graphic h/t @marketplunger1

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

International & Other Recommendations

It is important to hold some non-US assets, especially in China.

Mongolia Growth Group (MNGGF – $1.05) published their September quarter Letter to Shareholders. Kuppy sold all their Mongolian assets, netting $10,279,408. KEDM, their investment newsletter subscription business, brought in $727,496 of revenue but the subscriber count has flatlined.

The public securities portfolio produced a $7,511,239 unrealized gain and a $449,077 realized gain. The portfolio is concentrated in investments in oil futures and futures options, energy services companies, uranium equities, The St. Joe Company (JOE), and a small position in the Monero cryptocurrency.

In order to avoid being taxed as a personal holding company, they have to purchase over 25% of an operating business in the very near future. Unfortunately, they have not been able to identify any attractive opportunities and have started to lose confidence that they will be able identify an opportunity that is sufficiently attractive. If they can’t find a suitable acquisition in the near future, they likely will choose to liquidate the company, so as not to burden shareholders with the costs of a public company. MNGGF is a buy under $1.30 for a long-term hold.

Primary Risk: Harris Kupperman makes bad investments.

* * * * *

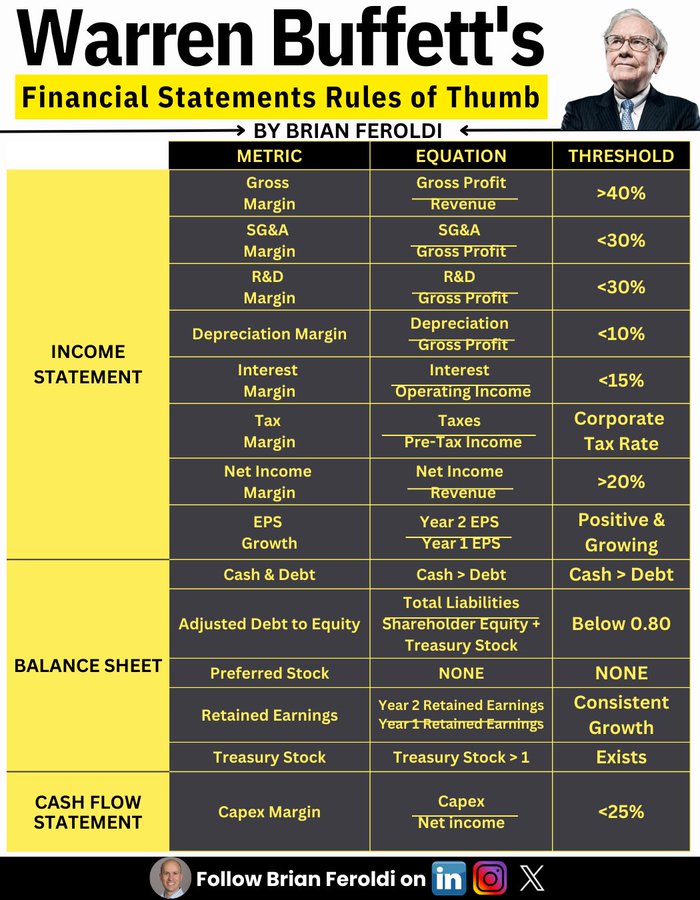

Click for larger graphic h/t @BrianFeroldi

Click for larger graphic h/t @BrianFeroldi

* * * * *

Give friends and family the gift of happiness and success. This is a GREAT book!

https://www.amazon.com/Reframe-Your-Brain-Interface-Happiness/dp/B0CGC8LSS1

Click for larger graphic

Click for larger graphic

* * * * *

Your drinking bone broth Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 11/30/23. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $189.95) – Buy under $150 for new iPhones

Corning (GLW – $28.50) – Buy under $33, target price $60

Gilead Sciences (GILD – $76.60) – Buy under $80, target price $120

Meta (META – $327.15) – Buy under $150, target price $400

SoftBank (SFTBY – $20.23) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $11.07) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $49.72) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $16.60) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $21.80) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $10.99) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.38) – Buy under $13, target price $30+

Velo3D (VLD – $0.97) – Buy under $6, target price $50

$20-for-$1 Biotech

Akebia Biotherapeutics (AKBA – $1.06) – Buy under $2, target $20

Aptose Biosciences (APTO – $2.43) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $5.98) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.39) – Buy under $7, hold a long time

Invitae (NVTA – $0.50) – Buy under $10, first target $50, then $100+

Medicenna (MDNAF – $0.36) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.68) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $12.81) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($25.67) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $25.65) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $30.20) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $19.31) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $27.69) – Buy under $30, target price $50

Coeur Mining (CDE – $3.05) – Buy under $5, target price $20

First Majestic Mining (AG – $5.97) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.39) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.00) – Buy under $10, target price $25

Sprott Inc. (SII – $32.55) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $37,647.47) – Buy

Grayscale Bitcoin Trust (GBTC – $30.26) – Buy

Ethereum (ETH-USD – $2,088.16) – Buy

Grayscale Ethereum Trust (ETHE – $16.41) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $68.58) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $36.69) – Buy under $40; $100+ target

EQT (EQT – $39.97) – Buy under $35; $70 first target

Energy Fuels (UUUU – $7.96) – Buy under $8; $30 target

Freeport McMoRan (FCX – $37.30) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $31.26) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $21.38) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.12) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $28.06) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.21) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.05) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $6.00) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Elon is F-ing awesome

He’s F-ing something, all right.

He can afford to be awesome. As he says, he has the freedom of not having to be liked.

that was a quote from, Elon, meant to reply to eversong

We all can have that freedom even without Elon’s money!! One of the good things about getting older is you figure out that you can’t please everyone. And the net result of that is, some people are not going to like you and you them. Just make peace with it.

I think you missed the point, Elon meant that from a perspective of financial freedom, not personal freedom.

Oh, yes of course then. Good point. I saw the interview where he told advertisers to go F—— themselves. That was very telling. And he thinks , as I do , that China will take over Taiwan either peacefully or by force.

whats the point in having fu $ if you never use it. the fu that is.

MM–on VLD, it is clear that the finances are desperate, with the sacrificial new deal. This is because the lenders have little confidence in the company’s sales prospects. It is your responsibility to assess their sales strategies and explain in your experience with other companies what “go-to-market” means and how it applies to VLD. With sales on a big downtrend, the stock could plunge to a small fraction of $1. Doubling down there could provide a mega multi bagger performance for us if marketing is successful, or a BUST. Your listing VLD last in chronological order suggests this scenario.

Anyone else with marketing experience with insights on this situation?

AGAIN on SCYX, you promised a detailed updated analysis, but it belongs in THIS newsletter since it has been a major near-wipeout for NWI subscribers.

Thanks.

What do you make of the law suite against SCYX ? Is this going to cost the company a lot of money?

Thanks for bringing this to my attention. I am not knowledgeable in these matters. This is MM’s expertise. He should answer your question, and also publish his promised SCYX analysis in NWI as I advised.

No. This is another BS class action suit to enrich bottom-feeders with an LLB. ScyNexis’ Directors & Officers insurance pays the inevitable out-of-court settlement.

VLD financials are not desperate. They have $71.5 million in cash and are up to a $100 million revenue run rate. The key to VLD is their revenue growth rate. Between the return of manufacturing to the US and defense/space spending, I am expecting better than consensus revenues in 2024. After selling about $101 million this year, the consensus expects $112 million in 2025. I expect ~$120 million.

There isn’t anything to say about SCYX. After GSK fixes the manufacturing issue, their royalties will start to flow. Meanwhile, we have the results of 4 completed trials coming, each one probably with a milestone payment. The company has loads of cash and the stock sells for half of cash per share.

VLD financials are not desperate. They have $71.5 million in cash and are up to a $100 million revenue run rate. The key to VLD is their revenue growth rate. Between the return of manufacturing to the US and defense/space spending, I am expecting better than consensus revenues in 2024. After selling about $101 million this year, the consensus expects $112 million in 2025. I expect ~$120 million.

There isn’t anything to say about SCYX. After GSK fixes the manufacturing issue, their royalties will start to flow. Meanwhile, we have the results of 4 completed trials coming, each one probably with a milestone payment. The company has loads of cash and the stock sells for half of cash per share.

It will be my pick for the Money Show’s Top Picks for 2024.

Thanks for responding.

VLD–by the company’s own 8K, the loan problems will affect customers’ confidence in VLD’s ability to service their needs, so they withdrew Q4 and even 2024 guidance. They are only hopeful of getting new customers in 2024 through their “go-to-market” strategy. What is that, and do you believe them on that?

If revenues continue to drop in 2024, that is a much sooner prospect of dilution.

SCYX–how long does it usually take to correct manufacturing problems? It seems like GSK is very slow on this one.

“Go to market” is just corporate speak for delivering a company’s unique value proposition – usually a superior product with competitive pricing – to customers.

They have the single best additive manufacturing solution, and I think revenues will grow ~20% in 2024.

Also wouldn’t be surprised if they hit their December quarter guidance anyway.

MM – which one will be your top pick for 2024, SCYX or VLD?

SCYX

SCYX would be the choice, provided they (GSK?) resolve the Brexa manufacturing problem. Do you have any indications of when?

I want to clear up some confusion. My two Substack newsletters on Friday basically repurpose content from the Thursday New World Investor. Every stock in Biotech Moonshots is a reprint from here. Boomberg mostly duplicates here. AAPL and META are my favorite metaverse stocks. Boomberg also has INTC, NVDA, PLTR, SNAP, and TWLO.

I recently sold PLTR. On advisory advice. Also still holding INTC. Lots of data saying very positive things for INTC . And wall street is not all over it , yet.

Bad advice. PLTR is in the sweet spot of AI and defense spending. I added more.

ARTH is $18 from .60 in early November. Anyone jump on? Was hoping it would drop back down to $1.00,

So I have owned ARTH way too long. However i am really pleased with it’s performance of late. My value went from close to zero to over $4000.

Maybe MM will give us his opinion on it’s recent move and should we hold on or sell?

May as well hold for the uplisting to Nasdaq and eventual acquisition.

Yes, recently. Currently at $8700. And change. Also bought SCYX and QUIK yesterday.

I forgot the ratio of the most recent ARTH reverse split–200? Then today’s $18 is only 9 cents. My average cost ages ago was 59 cents. I sold it all at 4 cents a few years ago.

Velo3D today announced its Sapphire printers are the first to achieve the Department of Defense’s Green-level STIG (Security Technical Implementation Guide) Compliance. The certification allows Sapphire printers to be connected to the DoD’s Secret Internet Protocol Router Network (SIPRNet) and gives customers the confidence their metal 3D printers are hardened against potential cyberattacks.

Will this bring in new customers?

MRK’s MS drug failed st3 fda MS trial. good news for TGTX

Yes, good news for TGTX. I don’t know whether the MRK drug was an oral BTK inhibitor which showed liver toxicity. The main risk for TGTX was BTK competition for Briumvi. Now that risk is receding, so it seems full steam ahead for TGTX. I added at $7.25 on Oct 31, but today’s $14-15 may be too soon, being pushed by the fill-the-gap technicians who say the stock should be $20 already.

Today’s Yahoo MB has more details from posters like “Anal Retort” who follow the research. I believe MRK’s drug is a BTK inhibitor which failed its trial. There is a link to an article claiming that BTK inhibitors are good for B cell malignancies like CLL, but probably not for autoimmune diseases like MS. Briumvi is the clear leader for relapsing MS, and may be used for earlier stages as well. Someone posted that if Briumvi gets 35% of the MS market, the market cap of TGTX would be $53 billion, or about $400/share. The sentiment in the stock is wildly bullish now, so hopefully new investors can get in or add on a pullback to the low teens or lower.

second week of November i had some squamous snipped off my ear i asked if there was a little epi in the anesthetic and got the not on extremity talk.older guy early 70 i wood guess, he told me he snips several a day and ass the blood ran down my chest i asked if he had ever heard of ARTH. he had not so i gave him the shmeel probably fell on deaf ears. The guys job is biopsying skin for big Boston hospital chain and his go to for bleeding is stop it and hit it with silver-nitrate.

fwiw

As long as this MD and hospital are making good money following routine procedures, they are not interested in better products like ARTH’s AC5. It will take an open minded MD to show the hospital that patients are much happier with AC5. If the hospital and MD don’t wise up, they deserve to lose business and good will.

MM–on VLD, please critique this extremely bearish post from last PM.

6 hours ago (by ja)

“Been watching VLD crash now for the past 9 months.. great call option play on Ms Wood’s disrupter playbook.. Pretty sure it’s not going out of business.. They do need to start executing the $300 mil shelf as they will soon be out of $$.. So as a savvy investor it appears waiting till .30-.50 cent range a great play . this company market cap will fall below sales shortly.. Dilution will kill it further hence the 30 cent target.. Then I expect Elon Musk to ride in and buy it for nothing.. a pure gold mine for his companies.. First thing Musk does is fire the lame MGMT and start literally “printing bucks” at past shareholder expense.. Pathetic MGMT.”

You said their finances are not desperate, but the share price plunge is acting like 30-50 cents is a possible target. Normally, tax loss selling in a viable company is a buying opportunity, but there will be fear awaiting the next Q4 earnings or revenue news in several months.

New World Investor for 12.7.23 is posted. Added SCYX to Near-Term Top 5.