Dear New World Investor:

The headline Consumer Price Index (CPI) for November increased 2.7% year-over-year (YoY), the second consecutive increase in annual inflation – a trend not seen since April, and 0.3% month-over-month (MoM). Both were a slight uptick from October’s 2.6% YoY and 0.2% MoM. It was the largest monthly gain since April.

But shelter costs, the largest component of the CPI that accounted for 40% of November’s overall monthly CPI increase, rose just 0.3% from October. This was lower than October’s 0.4% increase. On an annual basis, shelter costs rose 4.7% in November, down from October’s YoY gain of 4.9% and the smallest 12-month increase since early 2022.

The core CPI increased 3.3% YoY for the fourth consecutive month and 0.3% MoM. Core services prices increased 0.3% for the second straight month, after a couple of 0.4% monthly increases – pretty good news. Core services inflation over the past 12 months eased to 4.6%, the least since February 2022.

The Good News: All were in line with consensus estimates.

The Bad News: Inflation is sticky.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

This morning’s Producer Price Index, which includes health care services prices, airline fares, and portfolio management fees that feed into the the Fed’s favorite inflation indicator, the core Personal Consumption Expenditures Index, rose more sharply than expected in November to 3%. The PPI is a volatile index, but that was its second consecutive increase and the largest since February 2023. It was a significant uptick from October’s upwardly revised 2.6% and the consensus forecasts of 2.6%, It also was the fifth consecutive increase in producer prices, reaching its highest level since June 2024.

But the more important (to the Fed) core PPI rose by 3.4% annually, no higher than an upwardly revised 3.4% in October and only a bit above expectations of 3.2% On a monthly basis, the core PPI increased by 0.2%, a slight decline from October’s 0.3%, and right on expectations.

The inflation reports didn’t stop traders from taking the CME FedWatch Tool to 97.5% now expecting another quarter-point cut at next week’s Fed meeting. That’s up from 65% a month ago and 78% a week ago.

They’re most likely right, because Chairman Powell doesn’t like to totally shock expectations. But I expect this cut to be followed by a tsunami of FedSpeak about how they aren’t in any hurry to cut further as long as inflation is above 2% and the labor market and economy are OK. That would cap stocks for a while.

Markets are now pricing in a 3.73% year-end Federal funds rate for the end of 2025. Assuming the quarter-point cut next week, that implies a slightly higher likelihood of three quarter-point rate cuts than two cuts in 2025.

Yardeni Research is forecasting that the S&P could reach 7,000 by the end of 2025, based on a big driver people have been missing – very strong productivity growth. In the latest “I’ll see you and raise you” Wall Street game, Oppenheimer published a 2025 S&P 500 target of 7,100. They wrote that their bullish outlook is “based on a number of factors including current stateside monetary policy, the resilience in economic growth, business activity, the consumer, and job creation evidenced in recent years and the current year.” Winner, winner, chicken dinner – so far.

Click for larger graphic h/t Yahoo Finance

If President Trump really does cut the corporate tax rate from 21% to 15% for companies that make their products domestically, Oppenheimer could be low.

Market Outlook

The S&P 500 lost 0.4% since last Thursday as everyone waits for the Fed to do the expected. The S&P rose 24% in 2023, and so far in 2024 it is up 26.9%. If those gains hold, this will mark just the fourth time since the Great Depression nearly 100 years ago that the S&P 500 rallied more than 20% in back-to-back years. It has only done that three times before: in 1935/36, 1954/55, and 1995/96.

After the two boom years in 1935/36, stocks immediately crashed about 40% in 1937. That boom turned into a bust almost immediately. Following the market boom in 1954/55, stocks were flat in 1956 and then dropped 15% in 1957. That boom turned into a bust after about a year.

But after the1995/96 boom, the Internet happened. Stocks kept going up through 1999, only to crash about 50% from 2000 to 2002. So it took three years of huge gains before that big boom turned into a big bust. We have a driver similar to the Internet today – Artificial Intelligence. It’s going to remake almost every industry and company over the next decade. And, like 1997-1999. the sarcastic articles are starting to flow: Stocks are expensive, and nobody cares.

Stock buyback announcements are roaring to a $1.248 trillion record high.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

The Nasdaq Composite gained 1.0% and closed above 20,000 for the first time ever. It is up 32.6% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 3.2% and is clinging to an up year at +5.5% year-to-date. The small-cap Russell 2000 dropped 1.5% and is up 16.5% in 2024.

The fractal dimension edged back into consolidation mode, where we like to see it. More up-and-down movement will accumulate enough energy for a decent uptrend early in 2025.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Announce resolution of the manufacturing problem, lifting of clinical hold, restart of MARIO trial, maybe GSK files for hospital use approval

EQT EQT –natural gas price rebound

AKBA Akebia Therapeutics – Vafseo launch in January

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Tuesday, December 17

QUIK – QuickLogic – 1on1s – 13th Annual NYC Summit

Wednesday, December 18

Fed Meeting Statement – 2:00pm press release; 2:30pm press conference

Thursday, December 19

September quarter GDP – 8:30am – Third estimate

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $247.96) hit another all-time high Thursday for its 23rd record of the year. With iOS 18.2 including Chat-GPT now introduced and more Apple Intelligence features rolling out all year long, iPhone 16 sales will accelerate. Expectations for iPhone sales are low – there’s really no expectation for AI adding much of anything to Apple over the next year. I think that’s really wrong. AAPL is a HOLD – I expect to move back to Buy under $175 for new iPhones.

Gilead Sciences (GILD – $92.38) made several presentations at the big American Society of Hematology (ASH) annual meeting. Kite’s is the only CAR T-cell therapy to show a durable response and long-term survival after five years in patients with relapsed/refractory non-Hodgkin lymphomas. Over half of the trial patients were alive at the time of analysis, with no need for subsequent therapy. There were only rare instances of any late disease progression, which means Yescarta has curative potential for this deadly disease.

Kite also presented new data showing the curative potential of Yescarta in relapsed/refractory large B-cell lymphoma. In second-line treatment it showed a 71% Overall Survival Rate with a stable long-term quality of life for patients.

Finally, Tecartus showed a 91% Overall Response Rate, including a 73% Complete Response Rate, in Bruton tyrosine kinase inhibitor-naïve relapsed/refractory mantle cell lymphoma patients. GILD is a Long-Term Buy under $80 for a first target of $120 as they build their oncology franchise.

Meta Platforms (META – $630.79) hit another all-time high Wednesday. They are building their biggest-ever data center in Louisiana. The utility, Entergy, has already submitted plans to build three natural gas plants that can serve the data center campus with 2.2 gigawatts of capacity. META is a Hold – Buy or add at minus 2 standard deviations.

Palantir (PLTR – $73.20) hit another all-time high on Monday. PLTR probably will be added to the Nasdaq 100 on Friday in the annual rebalancing. That will require all the Naz 100 index funds to buy the stock. Palantir is the largest Nasdaq company by market value that isn’t in the index. Others include MicroStrategy, Equinix, CME Group, Interactive Brokers, and Coinbase Global.

On Wednesday, the company announced its first Warp Speed cohort, comprised of companies committed to reindustrializing America’s manufacturing and production capabilities through advanced AI and technology. The inaugural members include Anduril Industries, L3Harris, Panasonic Energy of North America, and Shield AI.

Warp Speed is a manufacturing operating system that provides speed, flexibility, and security for the modern manufacturer. The inaugural cohort is already using the software to gain an advantage in dynamic production scheduling, engineering change management, automated visual inspection for quality, and more.

Shyam Sankar, CTO of Palantir, said: “At the dawn of WW2, we didn’t have a Defense Industrial Base, we had an American Industrial Base. This is also what our future must look like—America must reindustrialize and mobilize at warp speed to win. We are proud to support Anduril, Shield AI, L3Harris, and Panasonic Energy with best-in-class software to manufacture the critical products that underwrite our freedom and prosperity.”

The company expanded its contract with the US Special Operations Command, securing a $36.8 million deal to act as the lead software integrator for its Mission Command System. This was the first deployment for Palantir’s Mission Manager platform to special-operations units. It’s really more about the opportunity to be the lead software integrator for the military’s Socom units, which is potentially very lucrative, and not about an immediate increase in the top-line performance

They signed an interesting partnership with Booz Allen Hamilton, which is a competitor in some government and defense services. The two companies said the partnership will focus on “driving transformational information infrastructure modernization and secure interoperability and rapidly accelerating integrated warfighting operations with coalition partners through data-centric systems that improve collaboration and combined mission planning with U.S. allies and partners.”

Palantir stock is expensive, no doubt, but not because everyone loves it. Analysts think 10 stocks in the S&P 500, including Palantir, Tesla, Garmin, Netflix, and Super Micro Computer will sink 10% or more in the next 12 months. They think Palantir will drop the most and only trade for $39.57 a share 12 months from now, a 45.9% drop, even though earnings will be up 52% in 2024 and 23% in 2025. It’s hard for an analyst or brokerage firm to admit they’ve been that wrong, so the way these usually resolve is the firm blames and maybe fires the analyst and gives someone else coverage to put a Buy rating on the stock.

Case in point: Baird analysts William Power and Yanni Samoilis initiated coverage of Palantir with a Neutral rating and a $70 target price. Baird’s salesforce can’t write a ticket from that recommendation.

CEO Alex Karp made two interesting presentations:

PLTR is a Buy under $22 for a $100+ target.

PayPal Holdings (PYPL – $89.40) hit a 52-week high Monday after it was upgraded by BofA from Neutral to Buy with a $103 target price, up from $86. They said PayPal is demonstrating increased turnaround progress just over a year after the C-level management change, which warrants a higher valuation multiple. BofA wrote: “We see potential ’25 acceleration in underlying TP [transaction profit] growth, recent holiday season e-comm spending data points have been encouraging, and we don’t think potential modest improvement in branded TPV [total payment volume] growth is priced in.” They think PayPal’s coming Investor Day on February 25 could be a positive catalyst and forecast strong free cash flow generation and share buybacks to continue. I’d add that on February 4 they’ll report December quarter earnings and give 2025 guidance, both of which should be above expectations. PYPL is a Buy under $68 for a double in three years.

Snap (SNAP – $11.38) CEO Evan Spiegel spoke at the 2024 WeProtect Global Alliance Summit.

SNAP is a Buy under $11 for a $17+ target.

SoftBank (SFTBY – $30.57) bought back 2,717,300 shares in November as CEO Masayoshi Son continues to be a buyer at 50% of book value. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Fastly (FSLY – $10.60) is one of the Best AI Stocks to Invest in Under $10, according to Insider Monkey. They wrote: “The company’s innovative AI accelerator is poised to revolutionize the AI landscape. By significantly reducing latency and costs associated with AI applications, this cutting-edge technology positions Fastly as a leader in AI innovation.”

FSLY is a Buy up to $10 for a 3- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $20.26) released the results of a survey of 1,000 IT and business executives who were director level and above, from the US, UK, Australia, and Japan. Service disruptions remain a critical concern, with 88% of the respondents saying they believe another major incident as large as the July global IT outage will occur in the next 12 months. Needless to add, they need PagerDuty software to protect them and respond quickly. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Rocket Lab USA (RKLB – $22.58) stock fell after a series of SEC filings that showed company insiders had recently sold stock. Chief Operating Officer Frank Klein sold 35,968 shares, Chief Financial Officer Adam Spice sold 62,511 shares, General Counsel Arjun Kampani sold 28,562 shares, Board Directors Merline Saintil and Alexander Slusky each sold 50,000 shares.

BFD. I don’t understand why Wall Street always is shocked, shocked that people who got part of their compensation in stock options for years would sell a little after their efforts are completely successful. They all still have large amounts of stock and plenty of skin in the game.

President Trump picked Jared Isaacman, the CEO of Shift4 Payments, to be head of NASA. Isaacman is a space enthusiast, and his appointment to the role is being seen as a sign that the Trump Administration will promote the space industry.

Rocket Lab’s next launch for Synspective, the Japanese Earth observation company, will be #6 out of a total of 16 missions Synspective booked on Electron. The launch window opens December 18. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Editas Medicine (EDIT – $1.89) presented a poster at ASH (accompanying presentation HERE) on the updated safety and efficacy data in 28 patients living with severe sickle cell disease (SCD) treated with reni-cel in the Phase 1/2/3 RUBY clinical trial. (You won’t see “Phase 1/2/3” very often.) Patients were at a median of 9.5 months after reni-cel infusion, with 11 patients having over one year of follow-up.

Since their reni-cel treatment, 27 of the 28 patients were free of vaso-occlusive events. Patients were observed to have early normalization of total hemoglobin and mean corpuscular concentration, well above the anti-sickling threshold. In addition, sustained clinically meaningful improvements were observed in patient-reported outcomes for pain, physical function, and social roles and activities.

There are great results and I expect them to license reni-cell early in 2025, probably in a deal that includes their second-generation in vivo sickle cell drug. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2026

Probable time of next financing: 2026 or never

Inflation MegaShift

Gold ($2,705.40) prices hit two-week highs on Tuesday on the collapse of Syria’s ruling Assad dynasty, anticipation of a Fed interest rate cut next week, and renewed buying by the People’s Bank of China (PBoC) following a six-month pause. In 2023, China was the world’s largest official sector buyer of gold, but the PBOC paused its 18-month buying streak in May. After two quarters of no gold purchases, the PBoC just resumed buying. They added 160,000 troy ounces – about 5½ tons – in November, bringing their reserves to 72.96 million ounces.

Gold prices fell 3.7% month-over-month in November, the biggest monthly decline of 2024, probably due to the stronger dollar since President Trump’s election. The PBoC may be capitalizing on lower prices to bolster its gold reserves, now up to 5.9% of its foreign exchange holdings from 3.5% in 2022.

TD Securities wrote: “The most important factor is news that People’s Bank of China reported that it again resumed its gold purchases … the market is getting hopeful that we could see other central banks follow suit and we could see a resumption of record territory buying.”

Between October 2020 and May 2024, eighteen physical gold exchange-traded funds collectively sold 1,200 tonnes, rivaling the massive outflows of 2012–2015. But since mid-May, these same ETFs have bought 150 tonnes — a decisive shift that mirrors broader changes in sentiment.

Silver tells a parallel story. From 2021 through early 2024, Western investors liquidated physical silver holdings, reducing exchange-traded fund reserves by 13,000 tonnes — two-thirds of the silver amassed during the buying phase of 2019–2021. Since May, these ETFs have added 2,500 tonnes of silver, echoing the shift in gold markets.

Since late October, gold has traded inside a triangle/wedge-like formation in a consolidation phase. Another close above the 50-day moving average at $2,684.17 (green line) and the negative trend line and things could get squeezy again.

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

The fractal dimension clearly shows the consolidation I’ve been tracking is firmly underway.

Miners & Related

Gold prices are in a substantial bull market, yet investor interest in gold miners remain eerily absent. Miners stocks today are as cheap as they were in 1999–2000, a period marked by deep skepticism and relentless selling from European central banks. Despite a 15% rise in gold prices over the last three months, the Van Eck Gold Miners ETF (GDX) – the most widely held gold equity ETF – has seen its outstanding shares shrink by 5% as investors sold. Since gold’s breakout in March, GDX shares have contracted by nearly 20%, even as gold prices climbed over 30%.

Click for larger graphic h/t @Go_Rozen

Dakota Gold (DC – $2.28) released more drilling results from the Richmond Hill prospect, including 1.00 gram per tonne (g/t) over 38.2 meters, 3.30 g/t over 11.8 meters, 2.22 g/t over 50.0 meters, and 2.54 g/t over 11.4 meters. These excellent results will be in an updated resource report in the March quarter. DC is a Buy under $2.50 for a $6 target as gold goes higher.

Primary Risk: Robert Quartermain doesn’t find enough gold. Secondary risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $6.20) began mailing the meeting materials for the special meeting of shareholders on January 14 to approve the Gatos Silver acquisition. Vote yes. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.69) entered into an Automatic Share Purchase Plan with its designated buy-back broker that allows them to buy stock at times when they would ordinarily not be permitted to make purchases, whether due to regulatory restriction or customary self-imposed blackout periods. I never heard of these ASPPs before, but I expect they limit the daily volume to something like 10% of the total. It provides a nice floor under the stock.

In addition, they renewed their $625 million revolving credit facility at a lower interest rate. Sandstorm is paying off debt – this is a “just in case” for a bluebird they don’t expect. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

President Trump named venture capitalist David Sacks as the incoming administration’s “AI and Crypto Czar.” He is very pro-crypto and will be hospitable to crypto innovation. Stephen McBride of Risk Hedge Ventures did an instructive, two-hour “Ask Me Anything” on crypto. He pointed out that the first phase of crypto was about the cryptocurrencies, primarily bitcoin and ethereum. Bitcoin is “digital gold” – a store of value that can easily be moved around the world, electronically or physically on a flash drive. It is essentially a global decentralized currency run by a network of computers around the world.

Ethereum is like the App Store. It is a platform where developers can go and build an app, product, service, or business. Stablecoins exist on top of ethereum. Ethereum has lagged bitcoin because of the lack of usage on the ethereum blockchain deliberately caused by SEC Chairman Gary Gensler’s regulatory clarity issues.

Ethereum and solana are “base-layer” blockchains – the foundations upon which crypto apps are built.

Ethereum is ultra-safe and decentralized. BlackRock CEO Larry Fink said he wants to tokenize every stock and exchange-traded fund. His new “stock exchange” will be built on Ethereum. Solana is faster and cheaper than ethereum. It will be used by applications that don’t need Pentagon-level security.

I expect bitcoin, ethereum, and solana to at least triple over the next few years. Solana ETFs should be approved next summer or fall, and I’ll probably recommend it soon if it backs off from the recent rally. We can buy solana on Coinbase before the ETFs are approved.

The first phase of crypto led to 7,900% gains on bitcoin. The big winners were bitcoin copycats like Litecoin.

The second phase of crypto yielded 2,800% gains on bitcoin. This phase was led by Initial Coin Offerings (ICOs) like Ripple, Neo, and Cardano.

The third phase led to 660% gains in bitcoin, but the big returns were in Decentralized Finance or DeFi projects like Uniswap and Synthetix.

We’re now in bitcoin’s fourth big upcycle. McBride thinks the fourth phase we are entering will be led by a whole universe of innovative crypto businesses that don’t have any ETFs and won’t for a while. You have to buy these cryptos through an exchange like Coinbase (COIN), a company and stock that is on my Monitor list. His main reason is that the Biden Administration has stifled crypto for four years. Regulators leaned on banks to shut down the accounts of crypto entrepreneurs. They made it illegal to launch quality tokens. They stopped Wall Street from backing innovative crypto projects.

But, finally, the war on crypto is over. Bitcoin is up 30% since election day, while dozens of smaller cryptos are up much more. Hivemapper (HONEY), a crypto project aiming to disrupt Google Maps, has surged 47%. Render Network (RNDR), which is like “Uber” for GPU computer chips, has shot up 51% over the past two weeks. In the fourth phase, the big money will be made by buying great crypto businesses emerging from regulatory purgatory.

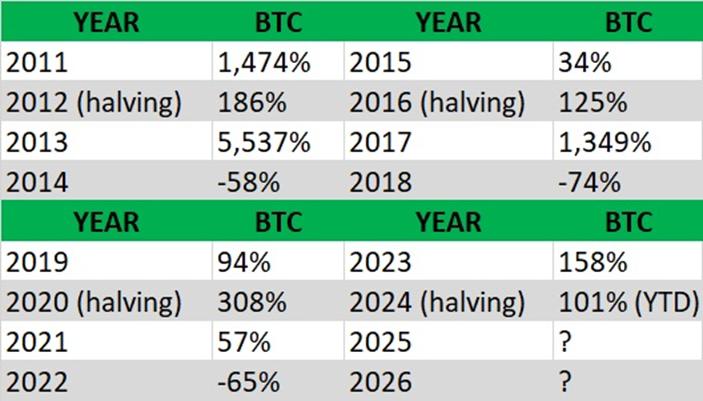

All of this is against the background of the four-year crypto cycle, driven by the every-four-years halvings of miners’ rewards. In their short history, bitcoin prices have had a “3 up, 1 down” pattern where every fourth year crypto prices plunge. The last time that happened was in 2022. It then recovers slowly and erratically in the first year (2023), and much faster in the second – halving -year (2024) and third (2025) year.

Click for larger graphic h/t RiskHedge

As the first, second, and third cycles showed, every bitcoin upcycle has created an even bigger upcycle for a specific group of tiny cryptos. I am not going to be recommending many or even any of them for two reasons. First, I think we can make a lot of money in less risky, more established tokens and companies like bitcoin, ethereum, solana, and Coinbase. Second, McBride has 10 people doing this full time – it takes an effort of that size to get an edge in tiny cryptos. I would be doing you a disservice if I tried to analyze them. If you really want to invest in that area. McBride is your guy.

Bitcoin (BTC-USD on Yahoo – $99,728.06) hit an all-time high of $103,900.47 on December 4. Benzinga ran a poll asking “Which level is Bitcoin more likely to reach next: $105,000 or $85,000?” The results were:

* * $105,000: 63%

* * $ 85,000: 37%

As a contrarian, it’s comforting that 37% still think they’ll get a chance to buy at $85,000. Bitcoin last traded below $85,000 on November 11. The last three times bitcoin broke out to fresh highs, it doubled in an average of 40 days. That would put bitcoin at $140,000 by the end of December. And, of course, Microstrategy just keeps buying. They added 21,550 bitcoin last week, funded by a share sale. The company now holds 423,650 bitcoin, worth around $41.5 billion.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

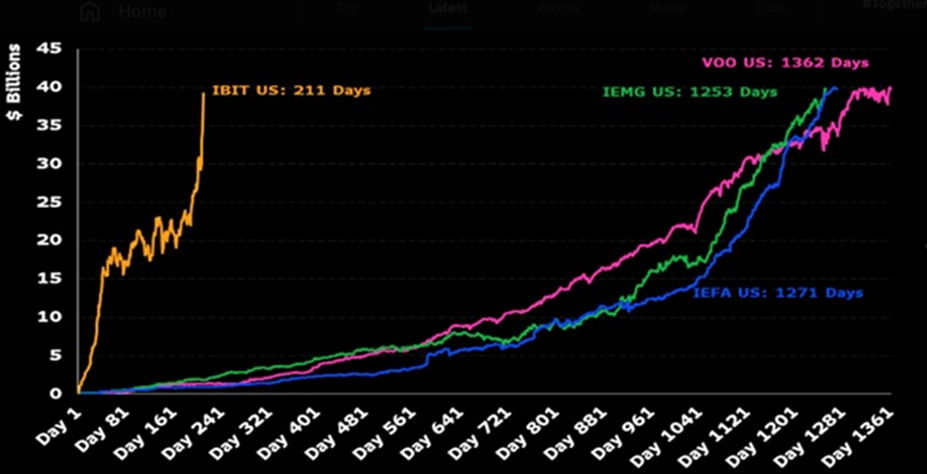

iShares Bitcoin Trust (IBIT- $56.92) has collected $53 billion in assets since it launched a little over 200 days ago. That is an all-time speed record. The iShares Core MSCI Emerging Markets ETF (IEMG) took 1,253 days; the iShares Core MSCI EAFE ETF (IEFA) took 1,271 days; and the Vanguard 500 Index Fund (VOO) took 1,362 days.

Click for larger graphic

IBIT is already in the top 1% of ETFs by assets. It remains the cheapest and easiest way to buy bitcoin. And as Barron’s wrote: “The race to become the go-to Bitcoin exchange-traded fund appears to have a runaway winner. And when it comes to ETFs, investing in the biggest, most heavily traded fund is usually the best option.” IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $3,893.08) is benefiting from purchases by the eight new ethereum exchange-traded funds. Although the impact hasn’t been nearly as large as what happened with bitcoin, Fidelity and BlackRock alone have bought over $500 million of ethereum in the last two days.

BlackRock’s iShares Ethereum Trust ETF (ETHA), which I recommended, has had total inflows of $2.93 billion, making it the largest issuer of ethereum ETFs. Fidelity’s Ethereum Fund (FETH) is second, with $1.35 billion in inflows. Last Tuesday saw the eighth consecutive day of inflows and the largest single-day activity, with ETHA bringing in $372.4 million and FETH bringing in $103.7 million.

Although we haven’t seen bitcoin-like fireworks, I expect ethereum to increase steadily for years as thousands of projects are built on it. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

iShares Ethereum Trust (ETHA- $29.47) is the only ethereum ETF listed on the Nasdaq exchange. BlackRock is seeking regulatory approval to launch spot trading options for ETHA, with an SEC decision expected from the Trump Administration by April. That will sharply increase the demand for ETHA and therefore ethereum. ETHA is a Buy.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

The excellent commodity and natural resource analysts at Goehring & Rozencwajg wrote Copper and Uranium: The Coming Divergence. They wrote: “In the short term, we remain bullish on both copper and uranium. However, we believe a crucial fundamental divergence is emerging that will make one metal a far superior investment over the coming decade. ..Our research suggests that the universally bullish copper demand forecasts are poised to unravel, potentially leading to bearish copper price implications…Molten salt SMRs [Small Modular nuclear Reactors] are poised to revolutionize energy production, addressing the fears of past accidents and the CO2 crisis that looms over our planet. Data centers – prodigious energy consumers – are already adopting this technology to meet their immense demands – the uranium section of this letter lists all recent announcements. Regulatory hurdles remain formidable, but the momentum is undeniable.”

Oil – $70.07

Oil has been trading in a tight range between $67 and $70 for three weeks as the paper oil bears battle the real oil bulls. Another crude draw this week of 1.425 million barrels only pushed it barely over $70.

More from Goehring & Rozencwajg’s Copper and Uranium: The Coming Divergence: “The great drama of American shale production may now be nearing its final act. For years, we have anticipated that the relentless growth in shale output would crest by late 2024 or early 2025, catching many off-guard. In hindsight, even this expectation might have erred on the side of caution. Quietly and without much fanfare, both shale oil and shale gas appear to have passed their zenith several months ago. Recent data from the Energy Information Agency (EIA) reveal that shale crude oil production reached its high-water mark in November 2023, only to slide 2%— roughly 200,000 barrels per day—since then. Likewise, shale dry gas production peaked that same month and has since slipped by 1%, or 1 billion cubic feet per day. The trajectory from here, according to our models, looks steeper still…Indeed, total shale oil and gas production likely peaked late last year. Both are already down 1%, and our models predict year-over-year production declines will turn sharply negative within six months.”

It is easy to say “Drill, Baby, Drill,” but it’s not so easy to defeat geology. Short of a new technological advance of the size of fracking, domestic oil and gas production is entering a long period of decline, accompanied by ever-rising prices. Everyone needs exposure to this trend.

The July 2026 Crude Oil Futures (CLN26.NYM – $65.00) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $37.29) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $9.51) got a small target price increase from JPMorgan from C$15 to C$16. They got the direction right but they are way off on the magnitude. Oil assets in Canada and natural gas assets in Europe will be the sweet spot in 2025.

JPMorgan expects natural gas producers to benefit from “three powerful secular demand trends:” the build-out of significant liquefied natural gas export capacity, rising power demand from electrification, and coal-to-gas switching. They updated their exploration and production models through 2030, which supports their forecast of long-term gas prices above $3.50 per million British thermal units (MMBtu). They believe prices will need to reset to a higher level to incentivize incremental supply growth from the Haynesville and other higher-cost gas basins.

Thy raised their VET target even though they wrongly believe the oil market will shift from balanced conditions in 2024 to surplus in 2025 on supply additions, and therefore shifted to a “more defensive stance.” Another victim of the Energy Information Administration’s overstated supply forecasts. VET is a buy under $11 for a target price of $24 or more.

Primary Risk: Oil prices fall.

Energy Fuels (UUUU – $6.16) will benefit as small modular reactors replace coal- and natural-gas fired generation. SMRs are up to six times more energy efficient than hydrocarbon-based power generation, capable of providing the surplus energy needed to drive an increasingly power-intensive global economy. The adoption of SMRs over the next 20 years will create a paradigm shift in uranium demand, introducing step-change increases that are not in most analysts’ models today. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

EQT (EQT – $45.86) is the best-positioned natural gas company, but the stock still is strongly affected by the price of gas. Yet more on natural gas from Goehring & Rozencwajg’s Copper and Uranium: The Coming Divergence: “The 2023–2024 winter, among the warmest on record, left a legacy of near-record storage levels. At the outset of the injection season, inventories stood at a staggering 700 billion cubic feet (Bcf) – or 40% – above the ten-year average. Yet, tight fundamentals have nearly erased this surplus in a remarkable turn. Over the third quarter alone, inventories were drawn down by almost 400 Bcf. By quarter’s end, storage levels stood less than 5% above the norm, a quiet but profound shift that few have fully grasped. This brings us to the present moment, where the market stands at a crossroads. If the coming winter delivers typical cold – after two years of unseasonable warmth – U.S. natural gas prices could well align with international benchmarks which currently hover near $14/MMBtu. The implications are vast, mainly as U.S. natural gas production, once seemingly boundless, now hints of rolling over. ..The result? A market that is shifting, after fifteen years of structural surplus, toward a long-running structural deficit. The abundance of shale gas has defined the natural gas story for the past decade and a half. That era, we believe, is drawing to a close, and the implications for prices—and the broader energy landscape—are profound.“

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Freeport McMoRan (FCX – $42.08) moves mostly on the price of copper. The latest data from the World Bureau of Metal Statistics shows that global copper demand remains strong, still outpacing supply. Through the first eight months of 2024, copper demand grew by nearly 4%, evenly split between developed and developing economies. Among OECD countries, copper consumption rose a healthy 3.2%, while non-OECD countries saw consumption grow by 8.3%. But in spite of the strong growth copper inventories on the major metals exchanges have shot up.

Click for larger graphic h/t @Go_Rozen

Click for larger graphic h/t @Go_Rozen

This probably is a reaction to the copper short squeeze that rattled the COMEX futures exchange in April and May. Traders are stockpiling inventories as a precaution against being caught in another financial squeeze. Fairly soon, the ongoing deficit will overwhelm the bears. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

Francis Weller on Grief

* * * * *

Your understanding tariffs Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 12/12/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $48.61) – Buy under $33, target price $60

Gilead Sciences (GILD – $92.38) – Buy under $80, target price $120

Palantir (PLTR – $73.20) – Buy under $22, target price $100+

PayPal (PYPL – $89.40) – Buy under $68, target price $136

Snap (SNAP – $11.38) – Buy under $11, target price $17+

SoftBank (SFTBY – $30.57) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $9.10) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $64.81) – Buy under $60; 3- to 5-year hold

Fastly (FSLY – $10.60) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $20.26) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $7.73) – Buy under $10, target price $40

Rocket Lab (RKLB – $22.58) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $2.95) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.82) – Buy under $2, target $20

Compass Pathways (CMPS – $4.41) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $1.89) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $3.76) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.23) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.11) – Buy under $3, target price $20, then $50

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($31.23) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $30.05) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $37.38) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $24.77) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $37.61) – Buy under $30, target price $50

Coeur Mining (CDE – $6.89) – Buy under $5, target price $20

Dakota Gold (DC – $2.28) – Buy under $2.50, target price $6

First Majestic Mining (AG – $6.20) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.35) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.69) – Buy under $10, target price $25

Sprott Inc. (SII – $44.71) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $99,728.06) – Buy

iShares Bitcoin Trust (IBIT – $56.92) – Buy

Ethereum (ETH-USD – $3,893.08) – Buy

iShares Ethereum Trust (ETHA- $29.47) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $65.00) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $37.29) – Buy under $40; $100+ target

Vermilion Energy (VET – $9.51) – Buy under $11; $24 target

Energy Fuels (UUUU – $6.16) – Buy under $8; $30 target

EQT (EQT – $45.86) – Buy under $35; $70 first target

Freeport McMoRan (FCX – $42.08) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $247.96) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $630.79) – Expect to move back to Buy

TG Therapeutics (TGTX – $30.69) – Hold for buyout at $40+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

2 (buckle my shoe)

TO: M. Murphy

Do you know anything about XRP Crypto? It has been under attack by the Govt trying to claim it is a stock. After about 8 years, the Gov’t lost the case. I bought the Crypto at a 63 cents. It is now in the $2.30 to $2.40 range. Many people are claiming it could go way up from this range to unbelievable numbers. It apparently has the market on being able to be used by all banks for rapid transfer of money internationally at low costs. I don’t know if you have access to any Crypto experts or not.

TO: M. Murphy

https://ripple.com/insights/10-things-need-know-xrp/

Info on XRP.

MM – still waiting for your Alt Coin recommendations, lets get to it before the crypto summer turns to winter again!

From above:

“As the first, second, and third cycles showed, every bitcoin upcycle has created an even bigger upcycle for a specific group of tiny cryptos. I am not going to be recommending many or even any of them for two reasons. First, I think we can make a lot of money in less risky, more established tokens and companies like bitcoin, ethereum, solana, and Coinbase. Second, McBride has 10 people doing this full time – it takes an effort of that size to get an edge in tiny cryptos. I would be doing you a disservice if I tried to analyze them. If you really want to invest in that area. McBride is your guy.”

I recommended Ripple (XMR) on March 15, 2018 at $209.10 and we sold it on April 8, 2021, at $270.00. It has a real use case and you should be good.

MM, INO is down over 30% from offering. I didn’t see anything about INO in this weeks report. Thoughts? Are we headed to another R/S?

INO announced today the pricing of the stock offering that they announced yesterday. $10M common shares & 10M accompanying warrants priced at $3 per common share for gross proceeds of $30M before fees. So adding 10M shares immediately to the 26M shares outstanding prior to the offering to get them an additional quarter’s worth of cash.

https://ir.inovio.com/news-releases/news-releases-details/2024/INOVIO-Announces-Pricing-of-30-Million-Public-Offering/default.aspx

“They will bank about $27.6 million, which will carry them past FDA approval of INO-3107 in early 2026.”

No, it won’t get them into 2026.

INO ended Q3 with ~$85M in cash/investments and provided guidance for a $24M Q4 cash burn. Add back ~$27M from the Dec. capital raise for a net increase of ~$3M in Q4 so they’ll end 2024 with ~$88M in cash/investments.

Assuming a 2025 quarterly cash burn of ~$25M, which is less than INO’s quarterly average for 2024, their quarter-end cash/investment balances will be the following without any additional funding:

In INO’s Q3 press release they stated they had a cash runway into 2025-Q3. The ~$27M raise got them an additional quarter’s worth of cash, and as the numbers above indicate, they now have a cash runway into about mid-Q4. So they will need additional capital to get into 2026.

Everyone can make their own assumptions as to how much of a cash cushion INO would want in 2026-Q1 when they get FDA approval and the timing and number of capital raises(s) to get there.

My guess is there will be two. I’m guessing they’ll do another one in Q2 about the time their cash/investment balance drops to $50M. I think they will do a second in Q4 to create a cash cushion going into FDA approval. They did two raises in 2024, two quarters apart, so that also continues that pattern.

I think they’ll want a minimum of a $50M cash balance in 2026-Q1. Given that, they will need to raise an additional $60M in 2025. That’s a whole lot of additional near-term dilution!

I expect warrant exercises.

MM – I see now you wont be making any Alt coin recos. Regarding your projection that the BIG # cryptos will at least triple – since you were spot on with BTC getting to $100k, I’ll ask what’s your timeframe for them to triple from here, does it take the next halving in 2028 to get there?

End of 2026/early 2027.

I have L3 Harris on board. It been a great pick for return on investment. I am currently up 130 percent @$29k. Other news you can use. PARNF (Parnell) is getting bought out for others who are still holding. You can take the cash or take shares of the new company. Mexico’s interest rate is getting cut to 10 percent. (And you thought the US was bad!!) UK , Bank of England is at 4.75 percent. And finally Canadian inflation data for November is out on Tuesday.

Like Murphy, I believe Small Module Reactors will replace coal and natural-gas fired generation. Murphy writes: “The adoption of SMRs over the next 20 years will create a paradigm shift in uranium demand,” which I also believe. Twenty years is a pretty big span of time compared to the amount of time I have remaining on the earth. In fact, maybe bigger than the time I have on this side of the grass. It would be helpful to know if we could get a better bead on the timeline for the first SMR to go online and how long after that we will see 10, 100 or 1000 operating. Any educated guesses?

UH OH, what’s wrong with your health? Will you live to see the final NGENF patient enrolled in the trial? There are lots of SCI and other neuro patients that could benefit, but this company is made of intellectual masturbators who can’t get anything done.

Don’t be alarmed. It’s just that I’m a man in my sixties and I’m not so optimistic that I’ll be the anomaly who makes it into my eighties. Had to laugh at the NervGen poke. As you know SCI presents in a wide spectrum of severity and NervGen wanted to get a homogenous sample patients to test. In retrospect, maybe the award winning design of this trial should have been open to a slightly wider number of patients. Once they announce the final patient is enrolled, though, results will be about 16 weeks away. I am beginning to think MDNAF could be the bigger winner for 2025.

Male average life expectancy is almost 80. If you’ve made it to the 60’s, it is well over 80. That’s an average of people like me who spend over $6K yearly (wholesale prices) on supplements, nonsmoker, nondrinker, slender, and early deaths from murders, accidents, drug abuse.

What supplements do you use for extended life?

My laundry list is too long, is customized for myself, and may not be applicable to you. But think of living longer by making as few mistakes as possible, and avoid most drugs whenever a much safer, effective natural substance works. I have an unfortunate 40 year old patient who has been a letter carrier with the Post Office. He is obese with severe HBP, metabolic syndrome, heart disease, His job of walking miles every day would have been great for weight loss, but his body has so much inflammation from obesity that he has been disabled for over a year. He lost his job and health insurance. 99% of MD’s would have loaded him with dangerous NSAID drugs for pain, which cause fatal stomach hemorrhage, kidney disease, etc. But I gave him MSM, a natural anti-inflammatory and detoxifier. I take 2 grams AM and 1 gram PM for my mild arthritis in the fingers. For him, it took 7 grams total every day, spread out in 3 doses to avoid diarrhea. Now he is walking better and will return to work very soon. The underlying problem is his inability to lose weight, despite following my low carb diet. Most obese people are sidetracked by stupid social activities of eating out, partying, etc. They prefer to take the dangerous drugs for diabetes, pain and the new weight loss drugs pushed by Big Pharma, ALL AT THE EXPENSE OF THE REST OF THE HARD WORKING POPULATION, following the stealing immorality which is the first commandment of the socialized system. You want to know how to get better health care while saving money? Get rid of insurance coverage for “lifestyle” drugs for cholesterol, diabetes, etc. Say to the patient–“If you choose to remain stupid, pay for your own dangerous drugs. OR, listen to the rare doctor who will teach you how to eat. That will save you lots of money, you will lose weight because you HAVE TO if you want to survive.”

But my patient is not a stupid party animal. I reviewed basic biochemistry on L-carnitine. It enhances fat burning in the mitochondria, the energy factory of the cell. I read the account of Dr. Robert Atkins decades ago in helping his patients lose weight with L-carnitine. This is a natural method of increasing fat burning, unlike the artificial method of using drugs like Ozempic to suppress appetite, which causes lots of side effects, and is exorbitantly expensive. The public is being fleeced for the benefit of the lazy. I just started him and a few people on L-carnitine.

There are many studies on the benefits of L-carnitine to corroborate Dr. Atkins’ experience. But the Big Pharma cartel censors nutritional research and pushes dangerous, expensive drugs. Most of the public has their finances drained by the BP drug cartel, so they have little money left to do the right thing–PERSONAL RESPONSIBILITY for healthy lifestyle plus judicious use of natural supplements.

DonB, you will have to recognize the evils of the socialist system, get out of VA care, and seek doctors with real knowledge.

anyone remember when or why WE NWI stopped fallowing XMR ?

Scyx,1.08 new 52 week low,way to go

Fucking biotechs

Guess I should include vldx with that also

Don’t forget INO. $2.03 new 52 week low.

Crushing blows Douglas,unbelievable how many of MM biotech pick have crippled some of us here

Ronald S, forget all bios except AKBA. TGTX will probably double or triple from here, but AKBA at $1.85 is a MUCH better opportunity. The key to AKBA is TDAPA which amounts to a 3 fold subsidy for 2 years. On Stocktwits, follow hsainu who yesterday translated the morass of regulatory gibberish into much better payment for Vafseo in years 3,4,5 post TDAPA than I thought. I would be lukewarm about AKBA if it weren’t involved with TDAPA. TDAPA is the way for stock investors to get the big welfare benefits that the socialist special interests get. Why don’t all honest people shun the stealing mentality of socialism? The only reason is socialists know how to scheme to get benefits for themselves at the expense of most people. HERE IS OUR CHANCE. Dialysis centers are incentivized to get most of the dialysis anemia market to switch to Vafseo and drop ESA’s. Today’s $1.85 has a good shot at $30 in 2-3 years for dialysis anemia. Nondialysis anemia in chronic kidney disease has a good shot at approval in 2027. Look at $100. Pipeline drugs look good for acute kidney injury and acute respiratory distress syndrome by 2035. $200 or more? I’ve had feuds with hsainu and his sidekick buythehornz127, mainly because I don’t accept that V is clearly superior to ESA’s. It may not become standard of care, but it is an attractive oral option that will be pushed hard by dialysis organizations, all due to TDAPA. All the big players are beneficiaries of TDAPA. It’s time to be a beneficiary as a shareholder of AKBA.

AKBA will become MM’s best idea. Maybe he can put together a portfolio of other stocks that get special treatment from TDAPA. Without TDAPA, they all suck.

MM are you aligned and agree with JGMDs projection of AKBA at $30 in 2 years?

Certainly directionally right and certainly possible.

Hey just checking JGmD are you still holding the scyx shares that you recently stated

Tx

Yes, still holding SCYX. Some ymb poster named Lemuel thinks GSK is behind the delay in getting Brexa back on the market. He thinks they are doing the MARIO trial with their supplies of Brexa. The plan is to rebrand Brexa as a general antifungal, not just VVC for women.

MM, what do you think of this theory?

Ok,tx hope that theory works and they issue some kind of press release sooner than later to stop this slide,have a nice day

The biggest thing I hate about SCYX is the underhanded role of GSK if Lemuel is correct. If true, the whole story of FDA approval of the new manufacturer is a HOAX. Come on, how long does approval take?

Additionally, we have a fucked up society full of abbreviations to disguise what entities really mean. GSK, FDA, ICE, etc.

JGMD – are there other analysts or websites corroberating the $30 AKBA price?

I don’t know. Stocktwits is the major source for info. Any time I ask on ymb, I am referred over to ST. Hsainu thinks $30 is in the bag for 2025. If it takes another 1-2 years, I’ll still be happy. The non dialysis subset of patients was considered favorable for approval by the FDA. That’s good for $60. If complete population of non dialysis, then $100 or more in 2028 or so. The excellent 9090 drug for acute respiratory distress and acute kidney injury is another drug based on the hypoxia inducible factor principle of Vafseo, looks favorable for 2030-35. Ultimate target, $200?

If you find other communities than ST, let us know.

Chris, does biopub discuss AKBA?

Used to, not anymore. But I think I’ll bring it up on that discussion forum. Look at MDNAF.

Keytruda may be the world’s best selling drug but it works better with help from MDNAF.

Perhaps biopub mirrors my hate/love feeling about AKBA. I started with KERX. When it merged with AKBA, my average entry to AKBA became $4. I was never enthusiastic about Auryxia, so I had only a small position. Auryxia is a simple iron compound, no great innovation. I was slow to wake up to Vafseo, AKBA’s exciting, innovative product. But I got my average cost basis down to $1.75. This would not have been possible if I had followed the NWI methodology of repetitive buying of wild speculations on the way down. But AKBA looks for real. Use my enthusiastic posts on AKBA as counterpoint to the good discussants on biopub. Whatever mistakes CEO Butler made in the past, I think he has done great work on getting Vafseo ready for a great launch 1/1/25, and especially in getting TDAPA benefit, the real key to a great launch.

A big human error is not being willing to change one’s mind. I’ll have to give MDNAF another look.

SCYX Francis Weller on grief really

Please tell me this is not to prepare us for another disappointment such as the Nvta fiasco please tell us to bail, Hail Mary or whatever . It sure doesn’t look promising, without any input from you. I will definitely bail at $1. Your newsletter is only worth what a good portion of us pay which is nothing.

Quantum computing. D-Wave interview by Yahoo. QBTS Has had a big run the last month.

https://finance.yahoo.com/video/quantum-computing-ai-positioning-2025-183122363.html?guccounter=1&guce_referrer=aHR0cHM6Ly9maW5hbmNlLnlhaG9vLmNvbS9uZXdzL2Qtd2F2ZS1jZW8tZHItYWxhbi0xMjAwMDA1NDguaHRtbA&guce_referrer_sig=AQAAAKpAjTVuWKIrNgrju8Xhfac3BL3uSeN3NmqaA8DiaruyH8VTHwRfsXlhsfCIaSg4mgkoLu9QN3dknWYarnl3PJzuKWuBBfykaNTLNx6PAyDZZ-k5P-0Vt3sOuC_843228kiVtxHdqeZHvjP2RcHPjup60XDeDGV9htGp97E4oO_t

SCYX

PPPFFFFFFFFFSSSSSSSTTTTTT!!!!

As suspected

SCYX

Anyone waiting 5 years to cross $2 again?

Hopefully Chris this is tax loss selling with scyx and once the new year is here maybe we can start to see some kind of upward momentum,here’s hoping

Hey, Everyone. Have a look at CGTX. I saw a blurb on Biopub about them having a very successful trial of their drug in Lewy Body Dementia. I have been friends all my life with a brother and sister whose mom died of lung cancer and whose father died from Lewy Body Dementia (LBD or DLB). About a million people in the USA have LBD, often misdiagnosed as Alzheimers or Parkinsons. Horrible way to go. I was interested enough to watch the video of the one hour presentation they did yesterday morning and bought some shares at $0.75 after the morning rush into the stock died down. Today in the pre-market it’s trading up from its close yesterday at $0.58, but still under .75. This could be one of my best investments ever. After the Lewy Body conference next month in Europe they will have their End of Phase 2 meeting with JGMD’s favorite government agency, the FDA, and we’ll get an idea of when their drug may be approved. Results in their 6 month, 130 person study were extremely good vs, placebo.

Chris–the main positive is that you have recommended a stock near the low point of the past year, instead of after huge runs. I watched the brief intro, the 14 min discussion by the qEEG expert and the 1st 20 min of yesterday’s video. The basic error is assuming that amyloid beta plaques or the oligomer derivatives are the CAUSE of Lewy Body or other types of dementia like Alzheimers. The amyloid hypothesis generated many drug candidates which failed or even made the disease worse. WHY? Because amyloid is not the CAUSE of AD, but the RESULT of it. What are the many possible causes? Please read Dr. Dale Bredesen’s now 10-15 year old book, THE END OF ALZHEIMERS. Amyloid is like a scab that contains the neuroinflammation, so if you destroy the scab, the fiery inflammation of AD spreads more. Bredesen talks about toxins, oxidative stress, mitochondrial dysfunction, nutritional and hormonal deficiency, diverse occult infections. Unless these are sought and treated, the situation is hopeless. Dr. James Galvin is an intellectual lightweight, merely diagnosing LB dementia on the basis of symptom clusters. It is good that he admits that this methodology is vague, which leads me to question how any trials using symptoms can be meaningful. The psychiatric profession is a big mess, with drugs designed to treat symptoms which help some but worsen others. One positive is that Galvin claims that CT1812 helps many symptoms without worsening others, which is the case in most of psychiatry. Another sad element of the hour video is that the 2 company interviewers misuse the word, “symptomology” when the correct word used by most doctors is “symptomatology.”

CT1812 has shown slowing of deterioration of clinical findings over 6 months. I like the supportive qEEG data. It may have some commercial success similar to the cholinesterase inhibitors like Aricept, Exelon patch, which slow the declines only. Since you bought at a cheap price, you may make good money, but I don’t know if this company will have profound impact on your dear friends. They would be better served by going to Bredesen’s network of practitioners using his methods of diagnosis and treatment. Start by having your friends read his book. His network is Apollo Health. I get their emails regularly.

Financially, for the 10X gain of CGTX, I think of that gain in AKBA as a better bet in 1-3 years, with potential of 100X in 10 years as I described in all my recent posts. Thanks for CGTX–I may take a small position, but I have a big position in AKBA. CGTX is tackling the most significant health problem, whereas AKBA is merely doing one thing well, treating anemia of CKD. It is not CURING CKD, only managing it better.

I believe you are correct about the amyloid being a result and not a cause of Alzheimers. I also think the more rapid progression of DLB than AD may be why CT1812 didn’t meet endpoints for its 6 month AD trial but showed great results for DLB. Will be an interesting story to follow.

Chris, if you could only buy one MDNAF or CGTX, which one would you buy for near term gains?

MDNAF. I took a decent stake a year ago because it was stupid cheap ahead of 2024. I’ve been adding lately because I think 2025 could be explosive for MDNAF. Then again, last year I thought 2024 would be a great year for NGENF and ACHV, forgetting the 1st Commandment of biotech: “Everything takes longer than you expect.”

MM, I posted this a few months back. I feel that they are a BO candidate in the near future.

MM, have you ever considered recommending Altimmune – ALT? Altimmune is a clinical-stage biopharmaceutical company focused on developing innovative next-generation peptide-based therapeutics. The Company is developing pemvidutide, a GLP-1/glucagon dual receptor agonist for the treatment of obesity and metabolic dysfunction-associated steatohepatitis (MASH). For more information, please visit http://www.altimmune.com.

Read my long post from yesterday to DonB. The GLP drugs for obesity work, but are expensive and fraught with side effects. But anything that reduces obesity like diet, exercise, cheap L-carnitine supplements all reduce MASH. These “lifestyle” drugs are a great way to bankrupt the medical system, on a par with big defense spending. I’m in favor of drugs only when there is no natural therapy that works. NOT for obesity related problems.

MM or anyone, this is another one I posted about a few months ago. It might be worth looking at.

ESPR – https://www.esperion.com/

They have 2 products that help people lower cholesterol who can’t tolerate statins.

New World Investor for 12.19.24 is posted. No issue next week. January 2 is the 2024 performance review and first thoughts on 2025.

Bought AKBA on today’s little dip. I expect them to announce a contract with Fresenius, the other big dialysis company (they already have DaVita), then announce the Vafseo launch on Thursday, and then present at the big JPMorgan conference on Jan. 16.