Dear New World Investor:

Today’s Personal Consumption Expenditures Index (PCE) was both high and completely expected. The headline year-over-year number hit a three-year high in April at +3.8% – right on expectations. It was a clear acceleration from March’s +3.5%. Month-over-month, it was up 0.4%.

The core PCE, the Fed’s favorite inflation indicator that excludes food and energy prices, was up 3.3%, also right on expectations and up a tenth from March’s 3.2%. It was a 2 ½-year high. Month-over-month, it was up 0.2%.

Kevin Warsh, the new Federal Reserve Chairman, is sworn in and there is a growing perception that the Fed may consider raising interest rates, even though Warsh was brought in by President Trump to cut rates.

In the past, the S&P 500 has experienced a drawdown in the first three months following every change in Fed chairs dating back to at least 1930. The average three-month decline has been 12%. However, the individual drawdowns have varied significantly, from as much as -33% after Alan Greenspan took the helm in August 1987 to as little as -2% after Ben Bernanke was confirmed in February 2006.

Of course, every decline was followed by a rally to new highs.

Market Outlook

The S&P 500 added 0.8% over the last two weeks to new intraday and closing highs today. The Index is up 10.5% year-to-date. The Nasdaq Composite gained 1.1%, also to new intraday and closing highs today, as the AI trade returned. It is up 15.8% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 0.8% and is up a respectable 11.5% year-to-date. The small-cap Russell 2000 soared 2.6% and leads the 2026 performance derby, up 18.3% in 2026.

Top 5

Changes this week: None

Near-Term – chronological order

INO Inovio – bounce back from equity offering + FDA allows 6-month review of INO-3107

AKBA Akebia Therapeutics – Vafseo launch

BTC-USD Bitcoin – rebound from sell-off

ETH-USD Ethereum – rebound from sell-off

EQT EQT – natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model forecast for June quarter real GDP increased to +3.8%, about double the consensus estimate. The economy is A-OK.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Tuesday, June 2

FSLY – Fastly – 5:40pm – William Blair Growth Stock Conference

Wednesday, June 3

CMPS – Compass Pathways – 12:45pm – Jefferies Global Healthcare Conference

ON – Onsemi – 4:20pm – BofA Securities Global Technology Conference

PYPL – PayPal – 6:00pm – Evercore Global TMT Conference

Thursday, June 4

NVDA – Nvidia – 11:40am – BofA Securities Global Technology Conference

ABCL – AbCellera – 11:40am – Jefferies Global Healthcare Conference

EDIT – Editas – 4:20pm – Jefferies Global Healthcare Conference

Friday, June 5

May payrolls – 8:30am

Monday, June 8

AAPL- Apple – Through 6/12 – Worldwide Developers Conference (WWDC)

Tuesday, June 9

Short Interest – After the close

GILD – Gilead Sciences – 1:20pm – Goldman Sachs Global Healthcare Conference

Wednesday, June 10

Consumer Price Index – 8:30am

FCX – Freeport McMoRan – 10:00am – Annual meeting

Thursday, June 11

DC – Dakota Gold – Unspec. – RBC Capital Markets Global Mining and Materials Conference

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $312.51) is holding their Worldwide Developers Conference the week of June 8. There is always positive news from WWDC.

Bank of America raised its target price from $330 to $380 and reiterated their Buy rating, citing a potential boost from agentic artificial intelligence. They wrote: “In an agentic world, value accrues to the platform that controls user intent, personal context, app access, permissions, identity, authentication, payments, and trust. Smartphone is the scaled consumer device where these factors already converge. If AI assistants become the new front door to search, apps, commerce, scheduling, payments, and workflow completion, we think Apple should have meaningful leverage over model providers, app developers, merchants, advertisers, and payment networks.”

They think Apple’s advantage in agentic AI comes from its semiconductors and iOS, as Apple’s silicon can dictate what happens on a device (which is important for latency, reliability, privacy, and costs), and iOS will determine how the AI is used by the user. They said if the coming Siri redesign is integrated into the iPhone to become an agent that is capable of understanding intent, retrieving context, bringing up apps, and completing workflows, an agentic version of Siri could boost fiscal 2030 revenue between $15-$30 billion, or as much as $40-$65 billion if users really became acclimated to it.

I agree, but from a different viewpoint. If the Siri upgrade isn’t an effective agent, which is the most likely outcome, we’ll probably exit the stock for now. AAPL is a Buy under $205.

Gilead Sciences (GILD – $136.22) presented at the RBC Capital Markets Global Healthcare Conference (WEBCAST HERE and TRANSCRIPT HERE). Chief Medical Officer Dietmar Berger said that the Committee for Medicinal Products for Human Use of the European Medicines Agency recommended the marketing authorization of Trodelvy as a monotherapy for the treatment of adult patients with unresectable locally advanced or metastatic triple-negative breast cancer (TNBC). The European Commission will approve the additional Trodelvy indication soon. Gilead has also submitted an application to the FDA for approval of Trodelvy in this indication, which will be approved later this year.

Metastatic TNBC is an aggressive form of breast cancer that is associated with low survival rates. For many patients with metastatic TNBC, first-line therapy like Trodelvy may be their only line of treatment, necessitating an urgency to act using the most effective treatment options first to maximize patient outcomes.

The company just got accelerated approval from the FDA for Hepcludex for the treatment of chronic hepatitis delta virus (HDV) infection, making it the first and only approved treatment for HDV in the United States. Chronic HDV is the most severe form of viral hepatitis and is associated with a markedly higher risk of rapid disease progression, liver failure, and mortality compared with chronic hepatitis B virus (HBV) alone. In the United States, studies in general populations have estimated that HDV affects between 2% and 4% of individuals who have chronic hepatitis B virus (HBV), or 40,000-80,000 people. GILD is a Long-Term Buy under $115 for a first target of $150.

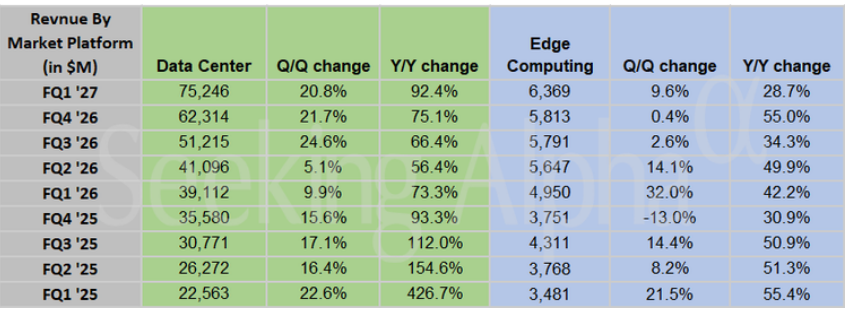

Nvidia (NVDA – $214.25) reported March quarter results.

Revenues up 85.2% from last year to $81.62 billion? √

$320 billion company growing 85% a year? √

Record revenues beat the $79.18 billion consensus estimate? √

Record Data Center revenues up 92.3% to $75.2 billion? √

Data Center revenues beat the $73.47 billion consensus estimate? √

Record free cash flow of $49 billion? √

Pro forma earnings per share up 140% from last year to $1.87? √

Pro forma earnings beat the $1.77 consensus estimate? √

June quarter revenue forecast up 90.6%-98.5% to $89.1-$92.8 billion? √

June quarter revenue forecast clobbered the $87.3 billion consensus estimate? √

Company announced additional $80 billion stock buyback? √

Dividend increased from 1¢ to 25¢? √

and, of course:

Stock down $3.96 the next day? √

Stock still lower than before they reported the double beat, guided above consensus, and sharply increased the stock buyback program? √

Stock has the largest short position in the S&P 500 ($62.5 billion)? √

The two sure winners in the AI revolution are Nvidia in hardware and Palantir in software…and neither Wall Street nor the big institutions can stand the valuations they have to pay to get on board. I sympathize, but only a little, because there are ways (start small and dollar-cost average, sell puts, buy stock and insurance puts, buy LEAPS) to get in over time at lower risk. As CEO Jensen Huang said: “The buildout of AI factories — the largest infrastructure expansion in human history — is accelerating at extraordinary speed. Agentic AI has arrived, doing productive work, generating real value, and scaling rapidly across companies and industries. Nvidia is uniquely positioned at the center of this transformation as the only platform that runs in every cloud, powers every frontier and open source model, and scales everywhere AI is produced — from hyperscale data centers to the edge.

“We are growing share in inference. Vera Rubin is going to be even more successful than Grace Blackwell. We’re gaining share tremendously fast in inference.”

Click for larger graphic h/t Seeking Alpha

On the conference call (CALL HERE and TRANSCRIPT HERE), Jensen said the new Vera CPU (not a GPU, but a direct competitor to Intel, AMD, and ARM) “opens a brand-new $200 billion TAM [Total Available Market] for Nvidia. We have visibility to nearly $20 billion in total CPU revenue this year [it just started shipping in mid-May], setting us up to become the world’s leading CPU supplier. All of the thinking happens on GPUs, all of the orchestration essentially runs on CPUs. ”

My main worry about the long-term outlook for Nvidia is China. Our government blocking GPU exports to China just ensures that country will develop competitive products. If and when they develop a comprehensive AI operating system like Nvidia’s CUDA, they will be a real threat selling against Nvidia outside the US. Jensen said: “The demand in China is quite large. Huawei is very, very strong. They had a record year, they’ll likely, very likely, have an extraordinary year coming up, and their local ecosystem of chip companies are doing quite well, because we’ve evacuated that market. We’ve really largely conceded that market to them.”

He had no choice. And, to be fair to the US government bureaucrats, Chinese companies are not buying even the Nvidia GPUs that are legal to export. It would upset Chairman Xi Jinping. Instead, they have placed large orders for Huawei’s latest AI processor, Ascend 950PR. Demand for that chip soared after DeepSeek unveiled its V4 AI models that run on Huawei’s chips.

I first called on Jensen in 2001 and immediately recommended the stock. It does not surprise me that Nvidia has evolved from a chipmaker to the primary architect of the AI industry, strategically investing across the AI value chain. They have made investments in AI infrastructure to expand compute real estate, the supply chain to break bottlenecks, and industry-specific AI companies to foster AI consumer markets. These investments widened and deepened their moat, extending their growth runway well into the 2030s. With a fortress balance sheet, robust cash flows, and forward earnings multiples at a historical discount, only an 18% premium to the S&P 500, I am raising the buy limit to $225.

During the quarter, Nvidia returned a record $20 billion to shareholders through stock buybacks and a tiny dividend. They had $38.5 billion remaining on that buyback authorization, and just added an additional $80.0 billion. NVDA is a Buy for a $225 first target.

Jensen agrees with me that AI will create more new jobs than the old jobs it obsoletes, just like every other historical advance in technology. Why are people confused about this every time? Because it’s easy to see the repetitive work that AI can replace, but it’s hard to see the new companies that can be created thanks to the new technology. Cf., Amazon, Netflix, Spotify…

Palantir (PLTR – $143.34) and Dell partnered to create an AI-based operating system that includes data sovereignty, zero-trust security, and legal compliance for highly regulated industries and governments. That’s a HUGE market. PLTR is a Buy under $160 for a $200 first target.

PayPal Holdings (PYPL – $44.46) presented at the Bernstein Strategic Decisions Conference (WEBCAST HERE and SLIDES HERE and TRANSCRIPT HERE). The new CEO, Enrique Lores, said: “The scale that the company has, the technology assets that we have, some of the skills and capabilities in terms of risk management are very unique.”

Click for larger graphic

Click for larger graphic

He described their roadmap to simplify their structure, optimize their operations and portfolio, and accelerate their AI adoption to achieve at least $1.5 billion in savings in the next two to three years.

Click for larger graphic

Click for larger graphic

“Simplifying the structure” means reducing layers across the company, optimizing role ratios (reducing management levels), and refining location strategies. “Optimizing their operations and portfolio” means improving productivity and performance across business units while increasing efficiency in marketing, outside services, and vendor spend.

“Accelerating AI adoption” is the big one. PayPal can be one of the biggest winners of AI adoption. Enrique plans to drive AI-enabled process redesign and execute AI and automation use cases. There are obvious applications in risk management, operations, fraud, and workforce planning.

He reiterated that free cash flow of around $6.0 billion in 2026 will all be used for stock buybacks. And no wonder! Based on the company’s current market capitalization of around $39.0 billion, this is over a 15% free cash flow yield. And their balance sheet is bulletproof, with $4.0 billion in cash at the end of March, just over 10% of the current market capitalization. PYPL is a Buy under $50 for a triple in three years.

SoftBank (SFTBY – $24.22) jumped after reports surfaced about OpenAI preparing to file for an IPO soon. SoftBank is a major shareholder in OpenAI, holding more than a 10% stake, making it one of the largest direct beneficiaries of any valuation re-rating tied to the IPO. SFTBY will make a bundle if OpenAI goes public, or lose a bundle if OpenAI goes bankrupt. GuruFocus published clickbait articles on both possibilities on the same day:

Click for larger graphic

Click for larger graphic

Sentiment was further boosted by expectations that SB Energy, a SoftBank-backed infrastructure business, is also preparing to submit a confidential IPO filing in the US, adding another potential listing pipeline. SoftBank has hired JPMorgan Chase, Goldman Sachs, Morgan Stanley, Citi, and Mizuho for the IPO. The energy and infrastructure developer could seek a valuation of over $50 billion in the IPO, which could come as early as September.

On top of that, rumors are that SoftBank is going to IPO Roze, its planned autonomous robotics spinout. Roze is a new AI and robotics company designed to automate data center construction. Supposedly, they are planning a $100 billion IPO led by Goldman Sachs, JPMorgan Chase, Mizuho, and Morgan Stanley.

Both of these will drive the hard asset value and stock price even higher. Hold SFTBY for a first target of $50 and then higher as the discount to hard book value disappears.

Small Tech

PagerDuty (PD – $7.44) reported April quarter results after the close today. Revenues were up 1.0% from last year to $120.97 million, ahead of the $119.37 million consensus estimate. Pro forma earnings per share of 32¢ beat the 25¢ estimate. This was the last quarter under the guidance of former CEO Jennifer Tejada. On the conference call (WEBCAST REPLAY WILL BE HERE and SLIDES HERE) John DiLullo, the new CEO, guided the June quarter to revenues of $122.0-$124.0 million, a skotch above the $122.61 million consensus estimate. But pro forma earnings guidance for 29¢-31¢ was below the 32¢ consensus.

For the full year, he guided revenues to $488.5-$495.5 million, a skotch below thw $493.44 milllion consensus. But he raised full year earnings guidance from a range of $1.23-$1.28 to $1.267-$1.32. The Street was at $1.26, so they marked the stock up after hours.

John sees PagerDuty as head and shoulders above the competition:

Click for larger graphic

He announced a new $100 million stock buyback program. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

ARK Venture Fund (ARKVX – $49.85) must have participated in the recent OpenAI funding round, because it now has 13.76% of its net asset value in SpaceX and another 2.96% in Anthropic.

Click for larger graphic

Click for larger graphic

The private market value of Anthropic has been rising quickly, and these two AI companies will be among the hottest IPOs of 2026. SpaceX – perhaps the hottest – has targeted a June 12 IPO.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

The SpaceX prospectus claims the largest total addressable market (TAM) ever listed in a public-company offering: $28.5 trillion, which the filing describes as the “largest actionable” market opportunity “in human history.” Only $370 billion of that comes from launch and other space-enabled services. Another $1.6 trillion comes from Starlink-based connectivity. The remaining $26.5 trillion, nearly 90% of the opportunity, is artificial intelligence.

SpaceX is targeting a raise of about $75 billion at a valuation of roughly $1.75 trillion. According to The Information, BlackRock is weighing a $5-$10 billion investment in the SpaceX IPO. I suspect this headline is misinformation designed to excite retail interest – BlackRock likes to buy early and cheap, rather than be the supplier of exit money at a $1.75 trillion valuation. ARKVX is a Buy for the SpaceX IPO.

Primary Risk: Cathie sells the stock before the IPO.

Biotech MegaShift

There were so many earnings reports in last week’s huge issue that for biotech I decided to write up only AbCellera and ScyNexis. In this issue I’ve covered the March quarter earnings calls from Akebia Therapeutics, Compass Pathways, Editas Medicines, Inovio Pharmaceuticals, and TG Therapeutics.

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like

Akebia Therapeutics (AKBA- $1.05) reported March quarter Vafseo revenues of $15.8 million. The total number of prescribers increased by 28% to around 1,025, and the total number of patients increased 60% to nearly 7,500. You may remember in their year-end results call, CEO John Butler said Vafseo end user demand, which excludes inventory changes, was flat at $12 million in the September quarter and $11 million in the December quarter as they transitioned to the in-center dosing regimen. John said they “absolutely expect and are seeing growth from that level” with “steady growth month-over-month, quarter-over-quarter as we start to penetrate deeper in terms of breadth and depth.”

Well, that happened. Total revenues, including declining Auryxia sales, were down 6.7% from last year to $53.5 million, but that beat the $51.67 million consensus estimate. The GAAP loss of $9.1 million or 3¢ a share was in line. On the conference call (CALL HERE and TRANSCRIPT HERE), John said: “In Quarter 1, approximately 2/3 of all Vafseo patients were being treated 3 times weekly. First refill adherence rates through the end of March were approximately 86% for patients treated under an observed dosing protocol. Alliance organizations are systematically electing to move to an observed dosing protocol, We believe that shift is improving adherence and could lead to greater utilization over time. We believe DaVita will implement an observed dosing protocol in the second half of the year.”

Akebia had $162.6 million in cash at the end of the quarter, enough to fund them for at least two years. Buy AKBA up to $4 for the Vafseo launches in the EU, UK, and US. I think GSK and/or Amgen will make a bid for the company.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: 2026

Probable time of next financing: Never

Compass Pathways (CMPS – $11.92) reported a March quarter GAAP loss of 30¢ a share, much better than the 45¢ loss estimate. On the conference call (CALL HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Kabir Nath said: “COMP360 has demonstrated what no approved drug for TRD (treatment-resistant depression) offers, clinically meaningful efficacy with both rapid onset and extended durability. We will be launch ready by the end of this year. Part B data from the COMP006 Phase 3 trial, which we continue to expect in early Q3, will be the final data set to complete the rolling submission.”

Chief Commercial Officer Lori Englebert said: “One benefit of being selected for the Commissioner’s National Priority Voucher includes the potential for an ultra-accelerated review timeline of 1 to 2 months after final NDA submission. Almost 90% of the U.S. population lives in a state that intends to reschedule COMP360 within 30 days after FDA approval and DEA rescheduling.”

Compass could become one of my best recommendations ever. The White House Executive Order on psychedelic treatments directs the Drug Enforcement Administration (DEA) to initiate and complete a review of any psychedelic treatment that has successfully completed Phase 3 trials so that rescheduling may proceed as quickly as possible. The one- to two-month FDA review time is an unexpected gift, and it looks like approval and a very fast launch are virtually certain. The TRD market is huge, and label expansions to PTSD and then all depression are likely over the next few years.

Click for larger graphic

The company finished the quarter with $50.5 million in debt and $466 million in cash, enough to carry them into 2028, past the COMP360 approval and launch. CMPS is a Strong Buy under $10 for a very long-term hold to $200. I hope everyone owns a position.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2027

Probable time of next financing: Never

Editas Medicine (EDIT – $3.43) had a GAAP loss of 26¢ in the March quarter, in line with estimates. There was no conference call (APRIL CORPORATE PRESENTATION HERE), but CEO Gilmore O’Neill wrote: “We continued to advance EDIT-401, a potentially transformative in vivo gene editing medicine designed to treat hyperlipidemia, toward the clinic. We are highly encouraged by our recent preclinical safety and efficacy data, including emerging data from our GLP toxicology study, as well as data demonstrating EDIT-401’s ability to reduce multiple independent risk factors for atherosclerotic cardiovascular disease, including LDL-C, Lp(a), and ApoB, in non-human primates. Based on these data, we believe EDIT-401 has a potential best-in-class profile as a one-time treatment for hyperlipidemia, and we remain on track to initiate a first-in-human study with early human proof-of-concept data by year-end.”

I’m coming around to the view that ApoB is by far the critical factor, not LDL, so it was good to see that EDIT-401 reduces ApoB. (By the way, the next time your doctor wants an LDL test, ask them to add ApoB.) Editas finished the quarter with $123.6 million in cash and did a huge 55,555,556 stock and $3.50 warrant sale this week that should net about $115 million now and another $180 million when the warrants are exercised. I’ve changed the “Probable time of next financing” to Never. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved. Owned: Going into the clinic in 2026.

Probable time of next FDA approval: 2028

Probable time of next financing: Never

Inovio (INO – $1.30) reported a March quarter GAAP loss of $19.7 million or 28¢ per share, solidly better than the 35¢ loss estimate. On the conference call (CALL HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Jacqueline Shea said: “We remain focused on achieving our top priority, advancing our lead candidate, INO-3107, through the regulatory process and toward its October 30 target PDUFA date. The FDA recently completed their standard mid-cycle review with no new significant issues being raised and scheduled the late-cycle review for the third quarter.”

That sounds to me like they were not yet able to get the FDA to reschedule the 10-month PUFA date (October 30) to six months, which explains why they did the April stock sale. They are still trying to reschedule.

Click for larger graphic

Jackie added: “We are continuing to advance our commercial readiness plans in anticipation of a potential U.S. approval in 2026, and we’re planning to manage commercialization ourselves with the support of a contract sales organization.”

That’s practical for recurrent respiratory papillomatosis because most patients are treated in specialty clinics.

After the quarterly report, Inovio said that ApolloBio, their partner in China, announced positive results from a Phase 3 trial of VGX-3100, a therapeutic DNA vaccine for cervical dysplasia, and their intention to file for approval. Inovio is entitled to receive up to $20 million in milestone payments plus tiered royalties on net sales. Jackie said: “We believe these positive topline results for VGX-3100 reflect both the potential of our DNA medicine platform in HPV-related diseases and the power of partnerships to advance innovative DNA immunotherapies.”

The company finished the quarter with $37.7 million in cash and raised another $16.0 million in April for the INO-3107 launch. INO is a Buy under $5 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2026

Probable time of next financing:After FDA approval in 2026

Medicenna (MDNAF – $0.32) did a down-and-dirty public offering of 8,880,000 units of one share of stock plus ½ of a three-year, 65¢ warrant for 50¢. They netted about $4.1 million. Buy MDNAF under $3 for a first target of $20.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 2

Probable time of first FDA approval: 2028

Probable time of next financing: 2025

ScyNexis (SCYX – $0.74) announced a 1-for-8 reverse split effective this Monday, June 1. The symbol remains SCYX, but the CUSIP number changes to 811292 309. So far this week the stock has been flat, but the real damage usually happens when the stock drops after the reverse split. I’m leaving it on Hold until we see if we can pick it off lower. Hold SCYX through the coming reverse split.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2028

Probable time of next financing: Never

TG Therapeutics (TGTX – $38.82) reported strong revenue growth, up 69.6% from last year to $204.92 million, beating the $201.21 average estimate. They saw a record number of new patient starts and better-than-expected persistence. Briumvi US sales hit $194.8 million, above their $185-$190 million guidance, plus they sold $6.5 million to Neuraxpharm, their ex-US partner. But they whiffed on the bottom line, reporting GAAP earnings per share of 12¢, less than half of the 27¢ estimate. They had a one-time $9.2 million charge related to the refinancing of their Blue Owl credit facility, of which approximately half was noncash.

On the conference call (CALL HERE and TRANSCRIPT HERE), CEO Michael Weiss gave June quarter guidance for $220 million of Briumvi US revenue. He raised the full-year target from $825-$850 million to $885-$900 million. He also raised total full-year revenue guidance to $925 million, well above the $900.34 million consensus.

We got positive top-line data on the Phase 3 consolidated Briumvi dosing schedule trial that met its primary endpoint, demonstrating bioequivalent drug exposure between the currently approved initiation dosing (150 milligrams on Day 1 and 450 milligrams on Day 15) and a new single infusion of 650 milligrams on Day 1 only. I expect a supplemental Biologics Licensing Application to be filed in the September quarter, with approval early next year, followed by an immediate launch. Briumvi will be the first and only IV anti-CD20 for which therapy can be initiated with a single infusion.

The Phase 3 subcutaneous administration trial is fully enrolled, with top-line data due around year-end or early next year, putting them on track for a potential 2028 launch. A positive result will probably add around $10 a share to the stock price.

After buying back $100 million of stock in the quarter (Mike said: “Until we see some significant price reassessment, we’ll continue to be buying shares”), they finished with $573 million in cash. Buy TGTX under $30 for a target price in a buyout of $40 or more.

Primary Risk: Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($4,530.80) hit a two-month low yesterday. It has been trending lower since the start of the war with Iran, because the effective closure of the Strait of Hormuz has caused a surge in oil prices, which has stirred inflation woes and sparked expectations of rate hikes. But gold is a safe haven because it is the best hedge against dollar debasement, and dollar debasement is no longer merely a thesis. It is now an official budget projection. Don’t say you weren’t warned!

According to Goldman Sachs, central bank demand for gold has proven stronger than previously estimated and likely will pick up again, helping prices to recover by year-end. Purchases are expected to increase to an average of 60 tons per month over 2026, raising the 12-month moving average of purchases to ~50 tons in March, up from 29 tons under the bank’s previous methodology. Among central banks, the People’s Bank of China bought the most gold in more than a year in April, lifting holdings by 260,000 ounces. It was the 18th straight month of additions, matching a streak that began in late 2022. Goldman reiterated its $5,400/ounce gold price target for year-end 2026.

Silver held up better than gold, hitting only a one-month low at $72.00 today. It will rise with gold, but higher prices are forcing industrial segments of the market to find ways to use less of the metal or substitute it with cheaper alternatives. Also, solar PV production has flatlined in China, along with a potential decline in solar installations this year.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Miners & Related

Coeur Mining (CDE – $18.59) presented at both the Canaccord Global Metals & Mining Conference (SLIDES HERE) and the Raymond James London Silver Conference (SLIDES HERE). As usual, they blocked us from the presentations in violation of SEC Rule FD. Also as usual, it doesn’t matter because they didn’t say much that was new.

At Canaccord, they did present summaries of the new technical reports for the New Afton and Rainy River mines that they added with the New Gold acquisition:

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

CDE is a Hold as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Dakota Gold (DC – $5.62) reported additional assay results received from its 2026 Drill Campaign at Richmond Hill. The 2026 Campaign includes 15,481 meters of drilling in 109 holes and consists of a combination of infill, expansion, and geotechnical drilling. Gold and silver assay data from more than 350 drill holes completed during the 2025 and ongoing 2026 Drill Campaigns at Richmond Hill will be incorporated into a Pre-Feasibility Study being published in the second half of 2026. The last projection was for a life of mine All-In Sustaining Cost (AISC) of $1,047 per gold ounce for the measured and indicated mine plan.

Over 85% of the total planned drilling for this year’s Richmond Hill Campaign has been completed to date with 13,718 meters in 92 drill holes. They have completed the infill and expansion drilling of the 2026 Drill Campaign on budget and ahead of schedule. Drilling productivity and assay turnaround times remain on track, and the Campaign is expected to be completed in the third quarter of 2026. That is an important milestone on the critical path to delivering the Pre-Feasibility Study by year-end.

The company closed a $75 million financing in the March quarter and received more than $10 million from warrant exercises, which eliminated all outstanding warrants. They had $107 million in cash at the end of March, enough to carry them through permit issuance for Richmond Hill. DC is a Hold for a $6 target as gold goes higher.

Primary Risk: Robert Quartermain doesn’t find enough gold. Secondary risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $1.39) updated the 2022 Feasibility Study for Grassy Mountain to reflect current metal price assumptions, capital and operating cost estimates, and a revised mine plan. The economic analysis is based on assumed metal prices of $3,600 per ounce of gold and $48 per ounce of silver.

Proven and Probable gold mineral reserves are 405,000 ounces, while Measured and Indicated gold mineral resources (inclusive of reserves) are 1.36 million ounces. Total recoverable ounces of gold have increased 7% from 361,800 ounces to 385,800 ounces. The revised production schedule extends the mine life from 7.8 years to 9.3 years. The Study outlines significantly improved project economics, including an after-tax Net Present Value (NPV) at a 5% discount rate of $374.7 million, an Internal Rate of Return (IRR) of 38.9%, and a payback period of 2.2 years. That is relative NPV and IRR increases of 228% and 72%, respectively, compared to the 2022 study.

The Study includes sensitivity analysis to higher commodity prices. Assuming metal prices of $4,618 per ounce of gold and $74 per ounce of silver, the after-tax NPV increases to $608.6 million, with an IRR of 55.4%, and a payback period of 1.4 years. State permitting is in the final stages, with approval expected in the second half of 2026.

They expect average annual gold production of 41,400 ounces, with average annual silver production of 51,500 ounces. The initial capital expenditure to build the mine is $189.8 million. All-In Sustaining Costs (AISC) net of silver by-product credits at $48 per ounce are $1,442 per ounce of gold. PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: 2026

Royal Gold (RGLD – $222.68) restructured their ownership in Artmin Madençilik, the joint venture company that owns 100% of the Hod Maden project. The restructuring includes a 50% reduction in Royal Gold’s direct equity ownership in Artmin (from 30% to 15%), the grant to Royal Gold of a new effective 2.5% net smelter return royalty interest, and certain rights pertaining to a new royalty interest being granted to SSR Mining, Inc. over the project. Royal Gold expects to receive attributable production of approximately 9,000 gold-equivalent ounces per year during the first full five years of production from the project.

As part of this restructuring, SSR and Lidya Madençilik, the additional partner in the ownership of Artmin, have agreed that SSR will sell all its interests in Artmin to Lidya. Additionally, SSR resigned as operator, and Lidya assumed operatorship of Hod Maden upon entering into the agreements related to this restructuring. In return, SSR will be granted a new effective 4.0% royalty interest on the project. The full economic burden of both the SSR royalty and the new Royal Gold royalty will be assumed by Lidya and will not reduce Royal Gold’s economic exposure to its remaining equity interest in Artmin.

Royal Gold CEO Bill Heissenbuttel said: “We believe the project will benefit from Lidya, an established and experienced local company, increasing its ownership and taking operating control of the joint venture. Lidya is the mining arm of a Turkish conglomerate with the financial and technical resources to effectively develop and operate the project, and we believe a local partner with these credentials is well-positioned to advance this high-quality project.”

SSR gave Royal Gold an option to acquire half of the SSR royalty (an equivalent 2.0% NSR royalty interest) for $160 million, exercisable from closing through the period that ends 12 months after the achievement of commercial production at the project.

Royal Gold will fund the next $70 million of project costs (including during the interim period until closing), to be followed by the funding of $397 million of project costs by Lidya. Further funding would then be split pro rata between Royal Gold and Lidya according to their 15%/85% ownership in Artmin. Closing for the transactions is expected in the second half of 2026. RGLD is a Buy under $180.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly.

Bitcoin (BTC-USD on Yahoo – $73,141.34), like gold, has been very weak. I think this is due to increasing interest rates making alternatives look more attractive, although interest rates are increasing due to inflationary pressures that normally would cause bitcoin to go up, not down. I still think dollar debasement outweighs interest rates, so my $150,000 next target for bitcoin is unchanged.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $41.56) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Ethereum Trust (ETHA- $15.19) remains the cheapest and easiest way to buy ethereum. ETHA is a Buy for the coming explosion in token-funded start-ups.

Primary Risk: Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $88.76

Oil slipped from over $108 to under $90 in 10 days on hopes that the Iran war will end. But Sultan Al Jaber, the CEO of ADNOC, the UAE’s oil company, said that it will take at least four months to get back to 80% of pre-conflict flows. To make up the supply shortfall, countries are relying on commercial and strategic inventories.

US crude stockpiles reported by the Energy Information Administration fell by 3.327 million barrels in the week ended May 22. We’re seeing the bottoms of some storage tanks. Britain has watered down sanctions to allow imports of diesel and jet fuel refined abroad from Russian crude. Saudi Arabia’s crude oil exports and production dropped to record lows in March. It’s happening.

The September 2027 Crude Oil Futures (CLU7.NYM – $72.06) are a Buy under $75 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $52.11) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $11.38) is a Strong Buy, with significant upside supported by a fundamental transformation and attractive valuation. Their five-year plan targets C$1.7 billion cumulative free cash flow, 8%-10% annual production per share growth, and substantial net debt reduction. Their portfolio shift toward long-life European gas assets and improved capital efficiency supports robust free cash flow and shareholder returns. Yet, despite substantial hedging ( about 50% of 2026 production), VET trades for only 6x free cash flow (a greater than16% free cash flow yield). VET is a buy under $11 for a target price of $24 or more.

Primary Risk: Oil and natural gas prices fall.

EQT (EQT – $55.35) was added to its sector Top Picks by Mizuho. EQT is a buy under $70 for a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

* * * * *

Mark Cuban on AI

Click for larger graphic h/t The AI Corner

* * * * *

RIP the GOAT, Sonny Rollins

* * * * *

Your considering Two Centuries of Innovations and Stock Market Bubbles Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 5/28/26. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $312.51) – Buy under $205

Gilead Sciences (GILD – $136.22) – Buy under $115, first target price $150

Meta (META – $635.29) – Buy under $705 for a long-term hold

Nvidia (NVDA – $214.25) – Buy under $225 for a long-term hold

Onsemi (ON – $123.77) – Buy under $60, first target price $130

Palantir (PLTR – $143.34) – Buy under $160 for $200 first target price

PayPal (PYPL – $44.46) – Buy under $50, target price $150

Snap (SNAP – $5.91) – Buy under $11, target price $17+

Small Tech

Enovix (ENVX – $7.65) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $83.68) – Buy under $75; 3- to 5-year hold

Fastly (FSLY – $16.94) – Buy under $10 for a 3- to 5-year hold to $50+

PagerDuty (PD – $7.44) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $21.56) – Buy under $10, target price $40

ARK Venture Fund (ARKVX – $49.85) – Buy for SpaceX IPO

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $5.73) – Buy under $6, target $30+

Akebia Therapeutics (AKBA – $1.05) – Buy under $4, target $20

Compass Pathways (CMPS – $11.92) – Buy under $10, hold a long time for a 20x return

Editas Medicines (EDIT – $3.43) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $1.30) – Buy under $5, hold a long time

Medicenna (MDNAF – $0.32) – Buy under $3, first target $20, then maybe $40

TG Therapeutics (TGTX – $38.82) – Buy under $30 for buyout at $40+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($75.97) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $71.80) – Buy under $50, target price $75

Sprott Junior Gold Miners ETF (SGDJ – $86.50) – Buy under $60, target price $100

Sprott Physical Gold and Silver Trust (CEF – $47.29) – Buy under $35, target price $60

Global X Silver Miners ETF (SIL – $90.98) – Buy under $60, target price $100

Coeur Mining (CDE – $18.59) – Buy under $10, target price $20

Paramount Gold Nevada (PZG – $1.39) – Buy under $1, first target price $10

Royal Gold (RGLD – $222.68) – Buy under $180

Cryptocurrencies

Bitcoin (BTC-USD – $73,141.34) – Buy

iShares Bitcoin Trust (IBIT – $41.56) – Buy

Ethereum (ETH-USD – $2,017.23)– Buy

iShares Ethereum Trust (ETHA- $15.19) – Buy

Commodities

Crude Oil Futures – September 2027 (CLU7.NYM – $72.06) – Buy under $75; $200+ target

United States 12 Month Oil Fund, LP (USL – $52.11) – Buy under $40; $100+ target

Vermilion Energy (VET – $11.38) – Buy under $11; $24+ target

Energy Fuels (UUUU – $18.44) – Buy under $18; $30 target

EQT (EQT – $55.35) – Buy under $70; hold for much higher prices ($100+)

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

SoftBank (SFTBY – $24.22) – Hold

ScyNexis (SCYX – $0.74) – Hold through reverse split

Dakota Gold (DC – $5.62) – Hold for higher gold prices

First Majestic Mining (AG – $20.58) – Hold for higher silver prices

Freeport McMoRan (FCX – $65.87) – Hold for higher copper prices

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2026

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

MM–you persist in recommending to buy AKBA up to $4, despite basic financial analysis by amateurs like Brent and to a lesser extent, myself. Your $4 is way outdated, due to much slower uptake of V than we all thought and the looming expiration of TDAPA. I will be lucky to break even on my average cost of $1.75 for V alone. For uninvested subscribers, the current $1 is a good speculative buy, but advice to buy up to $4 is a great way to mislead and alienate subscribers. I will be happy to get out in several years at $4, but only IF the pipeline drugs get approved and sell well. I would like to buy some NWI cheap techs and bios, but I have NO confidence in your buy and target prices. You don’t do numerical financial analysis any more.

MM has given up and just cuts and pastes week to week. no insightful deep dive analysis or new opportunity research outside of less than casino odds type biotech startups. He stays married to losing investments with the promise that 5 years from now, maybe. It’s sad and feels like a ruse because I paid years ago for a lifetime subscription to a relevant and reputable financial newsletter offering sound and solid leads on emerging growth stocks – today its far from that. I don’t know how this newsletter can miss the biggest wealth creation opportunity in a lifetime – sure you recommend PLTR and NVDA but that’s like shooting fish in a barrel – everyone recommends those, those are the no brainers. Doing my own research, I have 3X my investments in MU, STX, AMD, NBIS, IREN, CIFR, HUT, OPEN. This amazing time of technology advancement is a generational opportunity that this newsletter is missing – my suggestion is you do your own research. Here’s another lead as I have given several over the last year listed above – research the ETF’s SPRX (an excellent mix of high growth industry stocks) and DRAM (because menory has at least another year of high growth before the Chinese enter the market)

“…married to losing investments” and selling too soon on winning ones. I’m sorry I sold MU when he said — it’s up over 4x since — but glad I only sold half my RKLB (and supplemented that with addition of RKLX) and held onto all my GLW (because of a family connection; I owned it before he recommended it, and now supplemented my holding with the new 2x ETF GLWG). I plan to sell (all or part of) the 2x ETFs to take profits and continue holding the shares a long time.

Ive read Corning is a possible hot stock due to the Optical demand for the datacenters – do you think it still has room to run? What other stocks or 2X leverage plays are you excited about?

As I said Corning is a family matter for me. My aunt and uncle donated their Wedgwood, cameo and pate-sur-pate collections to the museum, established the annual Rakow Commission, and endowed their library with the ability to acquire everything written on glass worldwide (for which the library was named after them), so I plan to hold those shares a long time and only trade in and out with GLWG. I am not the best analyst for datacenters’ optical demand, but after several years of trading in the 40s I’m eversoglad to see them catch fire and hope it continues. (4 insiders just sold substantial shares but each holds way more than he sold.)

I have nowhere near their wealth (he was a surgeon and they were unable to have children) so I could not afford shares of either AAPL or AMD and used AAPU (+83%) and AMDL (+328%) to establish small positions in each. I also use IONX and QBTX to supplement my positions in IONQ and QBTS in the hope to hold my shares in those quantum stocks for several years, and do the same with NVDX and PTIR for NVDA and PLTR, and I am watching AVGG in the hope of getting a good entry into AVGO. My biggest such positions are RKLB (+3340% from a buy at 4.14) and RKLX (+328%). The percentages are more impressive than the amounts involved but they have enabled me to make substantial gains over the last 14 months.

MUU is Micron 2X is up over 200% the past 30 days. It can go up 10% or down 10% the next day. CIFU is 2X CIFR. IREX is 2X IREN.

Chris, do you still have a huge position in NGEN? Are you buying more around $2? How long do you think it will take to enroll for phase 3, report results and get FDA approval for SCI/chronic tetraplegia? I am confused by what is meant by a registrational phase 3. If it is successful, is approval soon after that?

Opie, thanks for your input on NGEN.

Chris are you ok? We are all getting older.I’m very concerned. far more important than wether your undecided on NGEN. Please let us know.

Gentlemen, I am well. Just been way too busy at my day job. I don’t recall whether I said it here, but I told a lot of people when NGEN was much higher that I was taking some profits due to the facts that 1) I thought Accelerated Approval would not be forthcoming until perhaps after Phase 3 was in progress; 2) NGEN would need more money to finance their Phase 3 and it would probably come from a dilutive raise; 3) with few catalysts in the near future, share price would do the inevitable ‘no news swoon’; and whether the drop would come from a big dilutive event like this or from a general market crash, I was pretty sure I would have the opportunity to buy back at lower prices. I had no idea the opportunity to buy back my shares would be at such a discount and come so quickly. But last week I started buying back some of the shares I had sold and I will continue to do so this week.

A “registrational Phase 3” means that the upcoming trial is the last thing they need to do to get approval. I do believe Accelerated Approval is still on the table and could come before the trial is completed if results progress similarly to Phase 2’s results. If so, the company could start selling the drug to people not in the trial while the trial carries on to completion.

Now that everyone in the SCI community knows the drug works, I expect rapid enrollment. For those Phase 2 participants, they didn’t know if the drug would work and they had to move for months to Chicago to take part despite their disabilities. That was a big ask. For the Phase 3, participants already know the drug works and with as many as 60 sites opening, nearly everyone can find a site near their homes. If your city is big enough to have a team in the NFL (32), MLB (30) or NBA (30), you will have a site near you. I expect at least 5 sites each in Florida, California and Texas alone. I won’t even guess at the Boston to DC corridor, plus Buffalo, Pittsburgh, Indiana, New Orleans, Atlanta, Denver, Portland, Seattle, Nashville, Memphis, St Louis, Kansas City, Detroit, etc.

The first of 20 patients in Chicago was enrolled in September 2023 and the last in February 2025 (16 months). I anticipate that NervGen can fully enroll the 150 people in this trial in less than a year with so many sites. I expect data to be released at the end of 2027, but AA could come as early as H1 2027. I anticipate approval will come in 2028 at the absolute latest. I will gladly wait 18 to 30 months to 5x my money from here (at a minimum) and much higher down the road.

Glad to hear your well.

Thanks for the detailed and informative reply Chris. Glad to hear you’re well and hope work responsibilities settle down a bit so you can post a little more often. Your ideas and info have helped more than you know.

Thanks, Chris. Sounds plausible. Get approval for SCI. Then do developmental trials for other neurologic conditions, which will require money. The stock may go above $10 on approval in 2028, then resume the rollercoaster as cash flow is consumed in trials for other conditions. Who will be skillful to take profits and get back in after future dilutive cash raises? Let’s hope they do this better than AKBA. This cash raise could have been done AFTER they reported good recent data at maybe $4 instead of $2.50. I will probably remain a timid FOMO investor and hold long term through the ups and downs.

Brent makes sense that there is no rush to buy now, in the news vacuum for another year. Dollar cost averaging over the next few months is reasonable.

Got a little more NGEN at $2.04 today. It closed at $1.94. Will patiently add over medium term at even lower prices.

MICHAEL—-WHEN ARE YOU PLANNING ON COMPLETELY DISCONTINUING THIS NEWSLETTER THAT I FIND VERY REPETITIVE AND BORING?

So don’t read it. Why urge him to stop?

I still enjoy receiving it

Me to.

I enjoy it very much, too!

T double o.

The real value of NWI is the original ideas from subscribers. My sub runs out in 2028. I would be happy to pay a much smaller fee to convert this to a subscriber forum after 2028. My likely best bonanza will be CAPR, contributed by Chris. ACHV, also from Chris will also be good. Congrats and thanks to Steve for his AI/data center ideas.

MM has excellent general market commentary, still. He can retire by converting NWI to what I just mentioned in the 1st paragraph. Until CAPR has the BIG payoff, my current biggest winner is TSM, recommended 30 years ago by MM when he was on fire. I am holding for a potential further double in several years of AI boom.

But MM can recapture his fire by doing what he used to do–numerical valuation analysis, keeping buy and target prices current with ongoing events. Then he would have increases in subscriber numbers instead of the rapid drop from subscribers who realize he is not doing the job he used to do. The weekly comments used to require several boards instead of the current sparse numbers only every 2 weeks. Analogy to AKBA–Butler is trying to build a pipeline of drug approvals that will be attractive to a Big Pharma. If MM gets his mojo back, he could rebuild an attractive newsletter that would be more valuable to a 50 year old financial advisor than the current prospect of having little value to anyone when MM retires. Mark Skousen just retired from Forecasts and Strategies, handing it over to Jim Woods, another eminent analyst who saw the value of Skousen’s work.