Dear New World Investor:

The average New World Investor recommendation finished 2024 up 20.2%, or 16.7% including the two S&P put recommendations that expired worthless. The biotech and small cap stocks made it underperform the S&P 500 and Nasdaq Composite.

Click for larger graphic

Click for larger graphic

Business Insider, 12/28/23: “Legendary investor Jim Rogers sees an epic market bubble and looming economic disaster. He hopes to short the ‘Magnificent 7’ stocks when the time is right.”

Porter Stansberry, 12/22/23: “The Naughty List – 10 Stocks Headed Straight to Hell”

Click for larger graphic

Click for larger graphic

Although some gurus were trying to scare people at the end of 2023, 2024 ended with the major stock market averages near their all-time highs. As of December 31, the S&P 500 index was up 23.3%, the Fed Funds rate was 100 basis points lower from the start of the year, and the 10-year Treasury yield was 50 basis points higher. In 2024, 41% of stocks outperformed the Index, better than the 26% in 2023. But because of the AI-driven Mag 7, the market felt as narrow as it did in 2023, even though it wasn’t.

Price/Earnings multiples expanded even further in 2024. I remain bullish, although earnings growth will have to carry the day in 2025. I think the Fed won’t cut rates any further unless the labor market falls apart, which probably would mean we go into a recession.

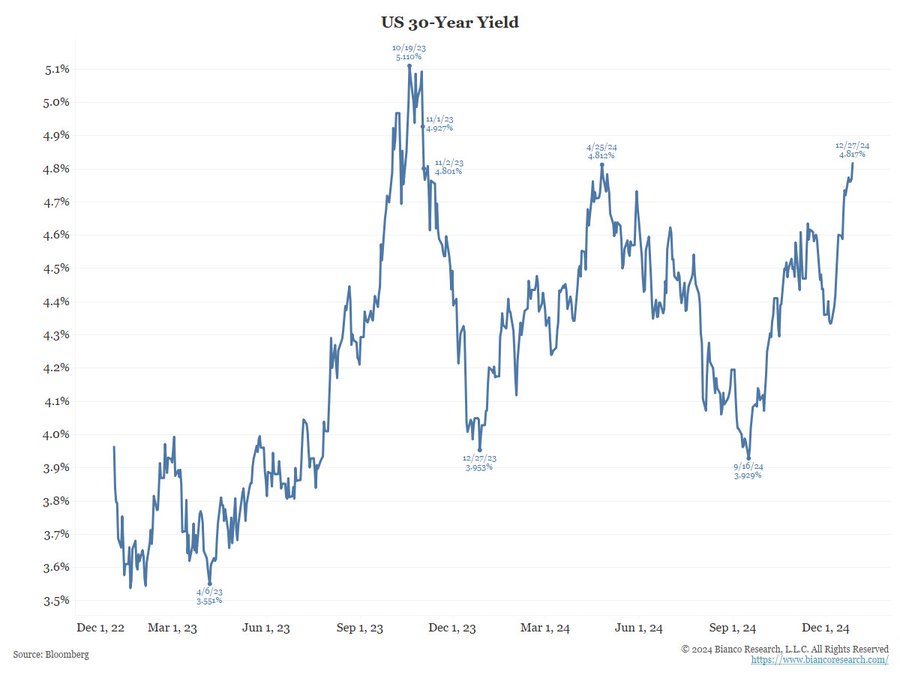

The bond market does not see a recession. The 10-year yield is just eight basis points away from a new 2024 high. The 30-year yield made a new 2024 closing high on December 27 at 4.811%, the highest yield since November 2023. It closed near that at 4.798% today.

Click for larger graphic h/t @biancoresearch

Click for larger graphic h/t @biancoresearch

The momentum rally since the election clearly is animal spirits returning in expectation of an extension of President Trump’s tax cuts and deregulation. That means they are at least partly – and probably mostly – discounted. Following the 2016 election, the market rallied 10% from election day until the late January inauguration, and then consolidated for several months. Most likely. that’s a good model for 2025. That rally did resume and 2017 finished up 22%.

I think the next 11 years are going to “rhyme” with the Reagan years, but the economy and the market will change even more. When Reagan entered the Oval Office in 1981, the S&P 500 was at 131.65, up about 28% from four years earlier when Jimmy Carter took the oath of office. When Reagan left the White House in 1989, the S&P had risen 118%.

The American economy also performed better during the Reagan years. Real median family income grew by $4,000 (about 18%) during the eight Reagan years after experiencing a loss of almost $1,500 in the previous eight pre-Reagan years. Interest rates, inflation, and unemployment fell more under Reagan than they did immediately before or after his presidency. The productivity rate was higher in the Reagan years than in the pre- or post-Reagan years.

Reagan’s 1981 tax cuts, combined with a scrupulous attention to federal monetary policy, deregulation, and free trade, created America’s greatest sustained wave of prosperity ever. The American economy increased by a third during his tenure, producing a $15 trillion bump in American wealth. Consumer and investor confidence soared. Cutting federal income taxes, reducing U.S. government spending, scaling down the government workforce, maintaining low interest rates, and keeping a watchful inflation hedge on the monetary supply was Ronald Reagan’s formula for a successful economic turnaround.

Previously, high taxes, excessive spending, and over-regulation had thrown a wrench in the works of our free markets. In essence, the government was trying to run the economy, but was ruining it instead.

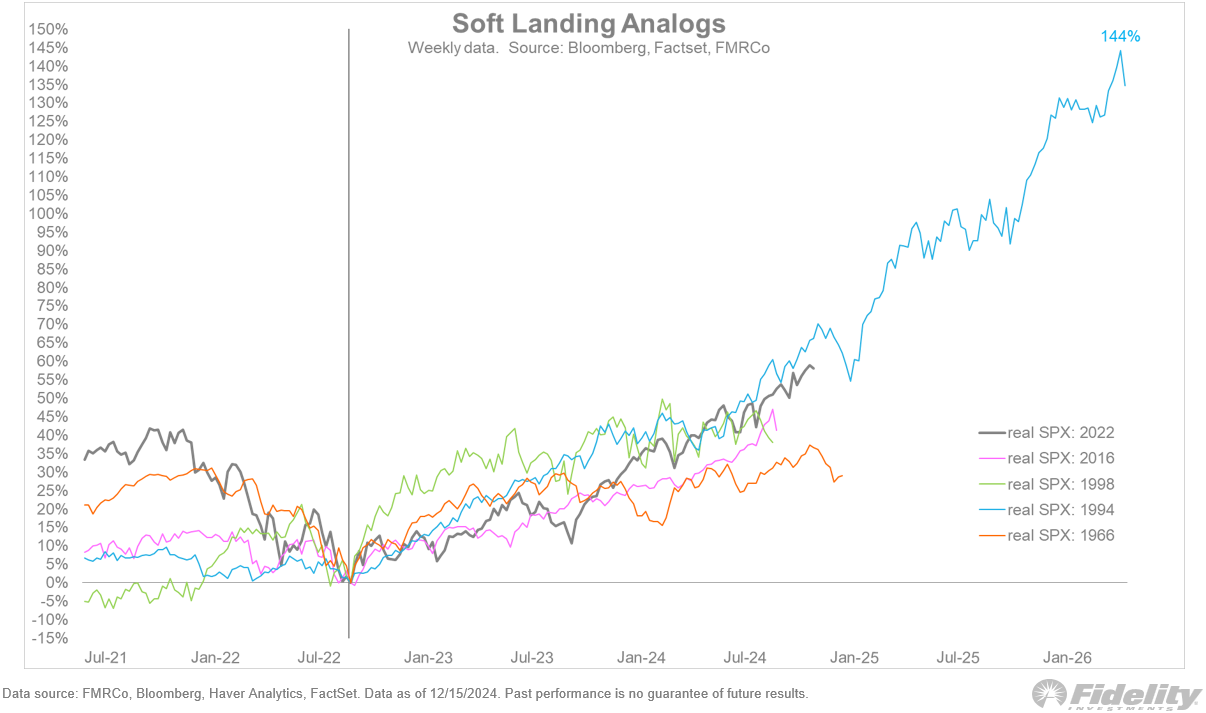

I agree with Jurrien Timmer, the Director of Global Macro at Fidelity Investments, who wrote: “The current era is of course reminiscent of the 1990’s. It’s interesting that this bull market has now outpaced all other soft landings except for the 1994-1998 rally. That boom, the result of the Maestro Alan Greenspan perfectly landing the plane in 1995 at a time when the Internet revolution was about to transform the market, seems as fitting an analog to today’s market as ever, although the 1998-2000 period might be an equally compelling contender given where valuations are.”

Click for larger graphic h/t @TimmerFidelity

Click for larger graphic h/t @TimmerFidelity

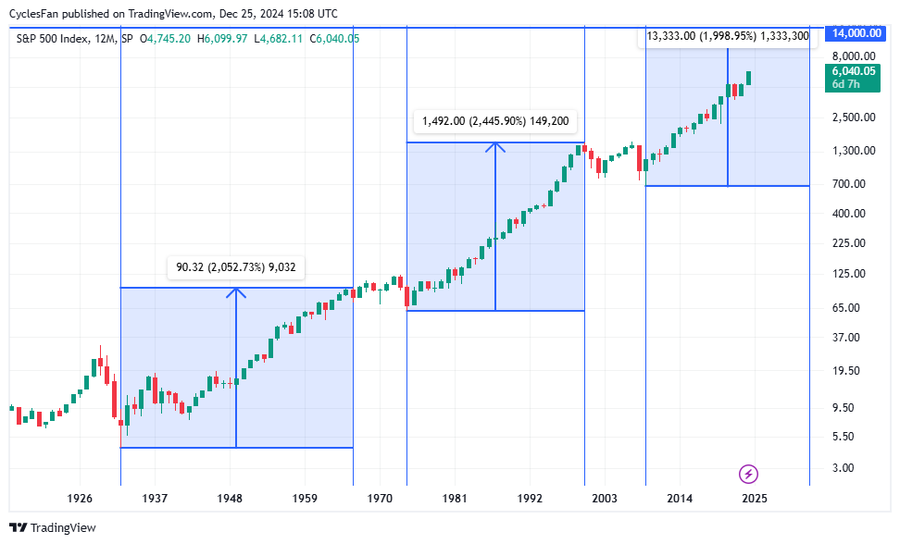

Timmer pointed out that the S&P 500 is in the third secular bull market since 1932. The previous secular bulls were 1932-1966 (34 years), which gained 2053%, and 1974-2000 (26 years), which gained 2446%. The current secular bull started in 2009 and I expect it to top in 2036 (27 years). The minimum price target is 14000, up 2000% from the 2009 low, with ~15750 more likely.

A reasonable roadmap to the 2036 top:

* * A post-inauguration pullback in February 2025

* * A ~7000 bull market top in early 2026

* * A 25% decline to ~5250 into late 2026. similar to the 2022 bear. The second year of a Presidential term often is weak

* * A 100% rally to ~10000 in 2029, driven in large part by Generative AI percolating through the economy

* * A 30% decline to ~7000 in 2030. Again, the second year of the next Presidential term.

* * A 125% rally to ~15750 in 2036, driven by robotics and cheap nuclear energy

Click for larger graphic h/t @CyclesFan

Click for larger graphic h/t @CyclesFan

Market Outlook

The S&P 500 lost 0.3% since December 19, but closed 2024 with the most highs ever recorded in a calendar year and booked two consecutive years of more than 20% gains, an achievement not seen since 1997-1998. The Index was up 23.3% in 2024. The Nasdaq Composite lost 0.5% since the 19th and was up 28.6% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 1.9% as the whole biotech sector caught a bid in advance of the JPMorgan conference opening January 15. It was up a measly 0.9% for the 12 months. The small-cap Russell 2000 edged up 0.5% on small cap bargain hunting. The Russell was up an even 10.0% in 2024.

The weak back-and-forth Santa Claus rally this year had one big benefit- the fractal dimension is fully consolidated! We don’t know when the next trend will start, but there now is enough energy to power one. The odds are it will be up and my guesstimate is that it starts soon.

Click for larger graphic

Click for larger graphic

Top 5

Changes this week: Moved AKBA to first position in Near-Term

Near-Term – chronological order

AKBA Akebia Therapeutics – Vafseo launch in January

SCYX – ScyNexis – Announce resolution of the manufacturing problem, lifting of clinical hold, restart of MARIO trial, maybe GSK files for hospital use approval

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model estimate of December quarter real GDP growth slipped from 3.1% to 2.6% due to a big drop in their estimate of private domestic investment growth.

Click for larger graphic

Click for larger graphic

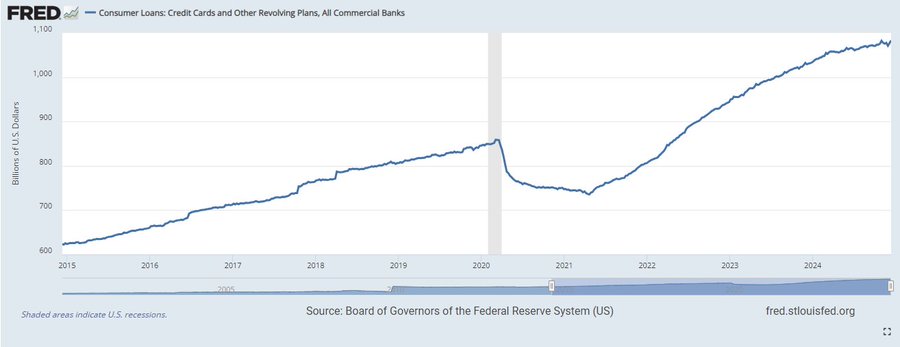

We are in the nosebleed seats on consumer credit card debt. Spending during the holiday shopping period (November 1 to December 24) rose 3.8% over 2023, according to a Mastercard SpendingPulse report. That was above the consensus forecast for a rise of 3.2% and topped the 3.1% increase during the same period last year.

Click for larger graphic h/t @chigrl

Click for larger graphic h/t @chigrl

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Thursday, January 9

Markets Closed – President Carter Tribute

Friday, January 10

December payrolls – 8:30am

Short Interest – After the close

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

The Digital Dominators had a great 2024 as AI fever spread to Corning and SoftBank, while driving my timely recommendation of Palantir. I expect Snap to be the star in 2025.

Click for larger graphic

Click for larger graphic

Apple (AAPL – $243.85) had another great year, although the Vision Pro did not sell as much as I expected. I think sales will accelerate in 2025 as more and more content is created. At the same time, a steady introduction of new Apple Intelligence features should drive a multi-year upgrade cycle for the iPhone 16 and subsequent phones. AAPL is a HOLD – I expect to move back to Buy under $175 for new iPhones.

Corning (GLW – $46.71) finally got some love for their optical fiber connections in AI data centers, but the real driver for the stock will be adding $3 billion in sales over the next three years with little added expense. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

Gilead Sciences (GILD – $91.88) also is finally getting some love, in this case mostly for their oncology programs. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $599.24) had an outstanding year as their early commitment to AI started paying huge dividends. Their Year In Review: 2024 Highlights focused on their open-source Llama AI model, which they used to build Meta AI, their AI assistant that is the most advanced one available for free. It is the world’s most used AI assistant, with nearly 600 million monthly active users.

They also are focused on Augmented Reality (AR) and showed Orion,their first true AR glasses prototype. Meta wants to build the next computing platform that puts people at the center so they can be more present, connected, and empowered in the world. They also released Meta Quest 3S, their most affordable mixed reality headset yet. They announced new styles and smart features for Ray-Ban Meta glasses, like helping you remember where you parked and answering questions based on what you’re looking at.

The company announced today that its latest Llama 3.3.70B model outperforms Google’s Gemini 1.5 Pro, OpenAI’s GPT-4o, and Amazon’s AlexaTM 20B. META is a Hold – Buy or add whenever it hits its lower Bollinger Band, now under $580.

Palantir (PLTR – $75.19) was the biggest 2024 winner in this group, even though we’ve only been in it for eight months. Their software is just right for the current state of the AI market. I think it could eventually become the enterprise resource planning (ERP) standard, displacing SAP and Oracle.

Stan Druckenmiller interviewed Palantir CEO Alex Karp about his new book, The Technological Republic. This is worth listening to!

PLTR is a Buy under $22 for a $100+ target.

PayPal Holdings (PYPL – $86.18) was a timely recommendation and under the new management team should increase steadily to hit my targets. PYPL is a Buy under $68 for a double in three years.

Snap (SNAP – $11.24) was the lagger in this group and probably will be the winner of the 2025 performance derby. All they have to do is follow Meta’s lead in monetizing their user base with AI-assisted targeted advertising. SNAP is an immediate Buy under $11 for a $17+ target.

SoftBank (SFTBY – $28.86) still sells at a 50% discount to net asset value because Wall Street hates it. But CEO Masayoshi Son keeps driving net asset value up at a steady clip, most recently with the ARM Holdings plc IPO, so the stock goes up. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Click for larger graphic

Click for larger graphic

First Trust NASDAQ Cybersecurity Exchange-Traded Fund (CIBR – $63.75) continued its steady march upward. If you think hacking is just going to get worse and worse – looking at you, North Korea – buying some CIBR is an easy decision. CIBR is a Buy up to $60 for a 3- to 5-year hold as the need for cybersecurity gets stronger and stronger at every level of society.

Primary Risk: A technology emerges to stop hackers.

Enovix (ENVX – $12.11) hit a major milestone: They shipped second-generation EX-2M samples to customers manufactured in its Malaysian Fab 2 plant. As expected, the samples have an energy density improvement of approximately 10% over the EX-1M products scheduled for mass production in Malaysia this year. EX-2M will launch in 2026.

Enovix also announced that it received its first mobile phone customer purchase order for custom samples from a customer with an NDA. The product is expected to ramp into mass production in late 2025. CEO Raj Talluri said they are on schedule for significant revenue growth in 2026. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $9.21) had a really bad year as competitor Edgio slashed prices to the big content companies like Netflix. Edgio drove itself into bankruptcy and in December Akamai – not a price cutter – acquired the assets with any value. 2025 will be much better. FSLY is a Buy up to $10 for a 3- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $18.00) has a valuable relationship with Amazon Web Services that should help move the stock higher in 2025. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $11.98) was down in 2024 even though CEO Brian Faith obviously has turned the company around. They just won a a $6.575 million contract extension for the continued development and demonstration of Strategic Radiation Hardened (SRH) high reliability Field Programmable Gate Array (FPGA) technology. QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $24.96) had a great 2024 as Wall Street finally realized what we saw early: This is the #2 space company to SpaceX. Just before Christmas they did their 16th launch for 2024 and sixth launch to date for Synspective, the Japanese Earth-observation company. 2025 will see even more Electron launches and, most important, the introduction of Neutron, their medium-lift rocket. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Click for larger graphic

Click for larger graphic

As you can see from the two right-hand columns, the biotech bear market has been devastating for my picks in this industry. But beyond that, as I wrote on the Comments board, two things I have learned about my foray into biotech stocks:

1. I am not nearly as good as I thought I was at predicting FDA approval.

2. It requires a venture mindset to buy and hold these stocks, so they are not appropriate for this newsletter.

The venture funds that invest in biotech know there will be several rounds of financing before a drug gets approved and a company can become self-funding. They also know that as hard as they try to back winners, six or seven out of every ten will go broke, one or two will be a modest win, and one will be a home run. When a biotech bear markets hit, as we’ve been in since February 2021, they have the reserves to keep funding the companies that are advancing.

So I am planning to follow the stocks I’ve recommended, but not make any new recommendations. We should see some substantial bounces in 2025, like ScyNexis’ 45% over the last three days (I should have bought SCYX instead of AKBA!) but I’m not planning to recommend sale of any biotech until it is in home run status.

AbCellera Biologics (ABCL- $3.03) was a 2024 recommendation that has wilted in the biotech bear. It has the technology, cash, and partners to be a huge success. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $1.90) has not announced either a Fresenius contract or the Vafseo launch. I expect both announcements before their January 16 presentation at the JPMorgan conference. Buy AKBA up to $2 for the Vafseo launches in the EU, UK, and US.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: NM

Probable time of next financing: Never

Compass Pathways (CMPS – $4.15) was hit by the FDA turndown of Lycos Therapeutics’ MDMA drug. Sure, a different drug treating a different disease with inferior clinical trial design got turned down. Only Wall Street traders could care. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2027

Probable time of next financing: Late 2025

Editas Medicine (EDIT – $1.31) was my last development-stage biotech recommendation in New World Investor and it’s already down because they pivoted to a superior technology. Wall Street thinks the value of having basic patents on gene therapy is $0. I expect we’ll see more licensing deals this year. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2026

Probable time of next financing: 2026 or never

Inovio (INO – $1.82) will file a Biologics Licensing Application this year and get approval early in 2026. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Early 2026

Probable time of next financing:After FDA approval in 2026

Medicenna (MDNAF – $1.12) had a great 2024 because management told Nasdaq to stuff their reverse split and retreated to the Canadian exchange. I still think they have a far better Interleukin-2 drug for a multi-billion dollar market. Buy MDNAF under $3 for a first target of $20.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

ScyNexis (SCYX – $1.45) should have a great 2025 as they get the clinical hold lifted, restart and complete the MARIO trial, and get milestones and royalties as GSK files for approval and launches ibrexafungerp for hospital use. Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2025

Probable time of next financing: Never

TG Therapeutics (TGTX – $31.06) was up 76.2% in 2024 as they did a great job of launching Briumvi. In 2025 they will either continue to take market share or get acquired, or both. Hold TGTX for a target price in a buyout of $40 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Click for larger graphic

Gold was up 29.5% in 2024, its largest yearly gain since 2010, while silver was only up 21.9%. The odd thing about 2024 was that the miners didn’t outperform the metals, as they usually do in an up market. I added Dakota Gold at the end of October to take advantage of this anomaly.

Gold ($2,667.80) in 2025 will look a lot like 2024 – sticky inflation means a slowdown in Fed interest rate reductions and a stronger dollar. So either gold goes up because inflation, or it goes down because interest rates and the dollar. Longer term, gold is an inflation hedge and even for President Trump, Elon Musk, and Vivek Ramaswamy it will be hard to bring inflation down.

In 2025, I expect silver to outperform gold and the miners to outperform the metals. The triangle consolidation in gold is obvious and the fractal dimension is racing towards full consolidation.

Click for larger graphic

Click for larger graphic

Miners & Related

First Majestic (AG – $5.95) said Gatos Silver, which they are about to acquire, has amended its agreements with Dowa Metals & Mining regarding the Los Gatos Joint Venture. The Amended Agreements expand Gatos’ management rights to allow for the financial statements of the LGJV to be fully consolidated.

This does not affect my advice to vote yes on the acquisition at the January 14 shareholders meeting. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Click for larger graphic

Click for larger graphic

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. Bitcoin more than doubled again in 2024, and we’re now up 1,033.9%. It dramatically outperformed ethereum – I expect that to reverse in 2025 as the Trump Administration allows the creation of new businesses on the ethereum blockchain.

The main investment moves I recommended were to swap the high-fee Grayscale funds for the low-fee BlackRock funds. As I expected, we were able to bank the ridiculous discounts the Grayscale funds went to as soon as the exchange-traded funds were approved.

Bitcoin (BTC-USD on Yahoo – $97,047.45) is headed for $150,000 or more in 2025.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

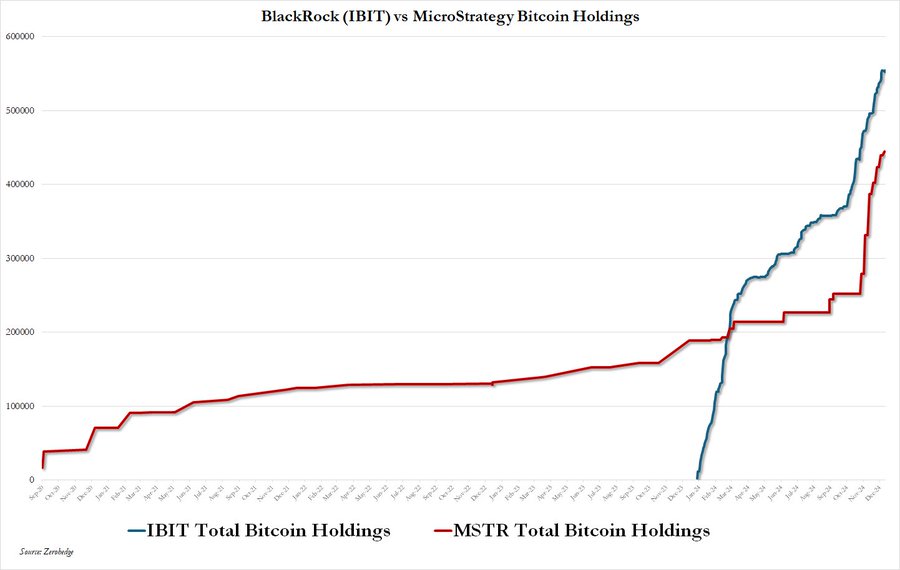

iShares Bitcoin Trust (IBIT- $55.37) now owns more bitcoin than Microstrategy. Combined, they own almost one million coins.

Click for larger graphic h/t @zerohedge

Click for larger graphic h/t @zerohedge

It remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $3,445.86) should go over $6,000 in 2025. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

iShares Ethereum Trust (ETHA- $26.20) remains the cheapest and easiest way to buy ethereum. ETHA is a Buy.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

International and Other

Click for larger graphic

Click for larger graphic

Although my China, marijuana, and Kuppy recommendations were up a bit in 2024, they were very badly timed initial recommendations and I pulled the plug on China in April and the other two in June. Acreage Holdings (ACRDF) was especially painful because I know people in the business who were pretty sure marijuana prices had bottomed. They just kept going down, and now rural real estate is chock full of properties with meaningful acreage and hundreds of thousands of dollars of infrastructure for sale for 10¢ on the dollar.

Commodities

Oil – $73.23

Click for larger graphic

Click for larger graphic

To my surprise, oil went nowhere in 2024. The combination of misleading US shale production figures from the Energy Information Administration, bizarrely overstated 2025 production forecasts from the International Energy Agency, and legitimate worries about the Chinese economy encouraged the bears to take extreme short positions.

Oil gained for the last two days on less negativity about the Chinese economy. I wouldn’t call it a bullish outlook yet – just a little less bearish. Bullish is coming.

The December 27 inventory data showed crude oil down another 4.2 million barrels. That was the fifth straight week of crude stock drawdowns. And another month, another US demand revision higher. US oil demand rose by 379,000 barrels a day or 1.8% year-over-year to 21.010 million barrels a day in October. That was a new record high for the month of October and was above the Energy Information Administration’s forecast of 20.535 million barrels a day.

Click for larger graphic h/t @staunovo

To some, this is an “oil glut.” To me, it is a market with record high demand, inventories at record lows, sputtering US shale, disappointing non-OPEC supply growth, and ~4 million barrels a day of OPEC spare capacity tightly held by those with a “will and intent.” The oil bears are Sleepwalking Into A Freight Train. Consider the excellent Eric Nuttall on OPEC, oil demand, and Canada’s role:

The July 2026 Crude Oil Futures (CLN26.NYM – $67.15) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $38.62) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $9.82) was recommended because they have a very sharp, disciplined management. They are developing natural gas projects in Europe. Russian gas flows to Europe via Ukraine stopped after a key transit deal expired New Year’s Eve. Gazprom ended gas supplies for deliveries Wednesday morning. Zelensky repeatedly said that he wouldn’t allow Russian gas, which benefits the Kremlin’s war machine, to transit through Ukraine after the five-year transit deal ended on December 31. Europe needs Vermilion’s gas.

The company announced the acquisition of privately-held Westbrick Energy for C$1.075 billion. CEO Dion Hatcher said: “The strategic acquisition of Westbrick represents a significant step forward in Vermilion’s North American high-grading initiative to increase operational scale and enhance full-cycle margins in the liquids-rich Deep Basin. The Deep Basin is an area Vermilion has been operating in for nearly three decades and is currently the largest producing asset in the Company. The Acquisition adds 50,000 boe/d of stable production and approximately 1.1 million (770,000 net) acres of land from which Vermilion has identified over 700 drilling locations, providing a robust inventory to keep production flat for over 15 years while generating significant free cash flow to enhance the Company’s long-term return of capital framework.”

They are paying less than 4x net operating income and less than 12x the value of the reserves. Over the past five years they have paid off over $1 billion in debt, which created the balance sheet capacity to execute this acquisition that gives them a 15% increase in excess free cash flow per share in 2025. They now expect 2025 funds from operations of $1.2 billion (~$7.80 per share) and free cash flow of approximately $450 million (~$2.90 per share). The stock is selling for 3.4x free cash flow – a New Year’s gift! VET is a buy under $11 for a target price of $24 or more.

Primary Risk: Oil prices fall.

Energy Fuels (UUUU – $5.68) is an easy way to invest in both uranium and rare earth elements at a cheap price. Both are crucial for the future of the US. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

EQT (EQT – $47.37) moved up as the Polar Vortex again threatens the Midwest all the way down to Texas. At the same time, US natural gas demand from LNG plants hit a record on Tuesday, the last day of the year, climbing to 15.2 billion cubic feet in a sign of a strong year ahead from the startup of two new gas-processing plants.

Demand for LNG is forecast to rise to 17.8 billion cubic feet a day (Bcf/d) in 2025 with the commissioning of Venture Global LNG’s 20 million tons per year Plaquemines plant in Louisiana and Cheniere Energy’s Corpus Christi Stage 3 expansion in Texas.

Lower 48 gas production reached ~104.5 Bcf/d again last week but continues to hover around ~104 Bcf/d. Due to winter weather, that should be the peak in production until April 2025. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Freeport McMoRan (FCX – $37.88) slipped in 2024 due to worries over Chinese demand for copper. The world’s demand for copper is only going to grow, whether stuff is made in China, Vietnam, India, or the US. $5 copper is coming. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

RIP Olivia Hussey

* * * * *

Click for larger graphic h/t @TheRabbitHole84

Click for larger graphic h/t @TheRabbitHole84

* * * * *

* * * * *

Your getting free stock on SoFi Invest Editor, (referral code)

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 1/2/25. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $46.71 – Buy under $33, target price $60

Gilead Sciences (GILD – $91.88) – Buy under $80, target price $120

Palantir (PLTR – $75.19) – Buy under $22, target price $100+

PayPal (PYPL – $86.18) – Buy under $68, target price $136

Snap (SNAP – $11.24) – Buy under $11, target price $17+

SoftBank (SFTBY – $28.86) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $12.11) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $63.75) – Buy under $60; 3- to 5-year hold

Fastly (FSLY – $9.21) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $18.00) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $11.98) – Buy under $10, target price $40

Rocket Lab (RKLB – $24.96) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.03) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.90) – Buy under $2, target $20

Compass Pathways (CMPS – $4.15) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $1.31) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $1.82) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.12) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.45) – Buy under $3, target price $20, then $50

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($29.98) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $28.86) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $34.99) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $24.24) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $33.12) – Buy under $30, target price $50

Coeur Mining (CDE – $6.20) – Buy under $5, target price $20

Dakota Gold (DC – $2.31) – Buy under $2.50, target price $6

First Majestic Mining (AG – $5.95) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.35) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.71) – Buy under $10, target price $25

Sprott Inc. (SII – $43.48) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $97,047.45) – Buy

iShares Bitcoin Trust (IBIT – $55.37) – Buy

Ethereum (ETH-USD – $3,445.86)– Buy

iShares Ethereum Trust (ETHA- $26.20) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $67.15) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $38.62) – Buy under $40; $100+ target

Vermilion Energy (VET – $9.82) – Buy under $11; $24 target

Energy Fuels (UUUU – $5.68) – Buy under $8; $30 target

EQT (EQT – $47.35) – Buy under $35; $70 first target

Freeport McMoRan (FCX – $37.88) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $243.85) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $599.24) – Expect to move back to Buy

TG Therapeutics (TGTX – $31.06) – Hold for buyout at $40+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2025

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First

Happy New Year!

MM, your sector tables appear to have some discrepancies.

Crypto: the ETHE prices for 2023 & 2024 are the same. 2024 s/b your sale price of $26.42

Your average values in 4 of the 7 tables appears to be incorrect as they don’t match the average Excel gives me.

Right on both counts. The divisor was wrong by 1 on the averages for biotech, hyperinflation, cryptos (off by 2), and oil. The correct averages are: biotech -42.1%, hyperinflation 11.7%. cryptos 289.0&, and oil 12.0%.

Are we surprised that akba hasn’t said a peep about any shipments starting,why would they wait until the conference on the 16th to say something as there stock drops after zacks put a sell rating,really,any opinion

Ignore Zacks. They are merely AI bots and do no fundamental company analysis. Follow Stocktwits. Gaboriar posted news that Fresenius has software that will make ESA less risky to get hemoglobin overshoot. This is a small negative for Vafseo. F won’t be announced as the 3rd major dialysis contractor pushing V. They are dedicated to ESA for now. Still, AKBA is one of the few bios worth investing in.

JGMD posted late yesterday on the previous board:

Chris, you must be happy about today’s NGENF PR that the last of 20 patients has been enrolled in the chronic SCI trial. Now we wait 16 weeks to complete the trial on this new patient with either NVG 291 or placebo. A few more weeks to analyze and report data, before June 30. Rumor is that one patient is walking with aid of parallel bars. The stock is still risky. If this is the only patient out of 10 who responded to a mild degree, the stock plunges in June. Protocols for 291 will have to be tweaked, with more dilution for all the trials that will be needed. But if 3/10 responded, and the 10 placebos are offered 291 in the open label extension, more responses will be seen. Maybe Jerry Silver will tweak the protocol for the placebos to increase the batting average of significant responses.

Here is my response:

Happy indeed. A year ago I believed full enrollment would be announced in 2024 and as late as last summer I thought we’d have Phase 2 results in 2024. Then I figured some people may have been putting off participation until after the holidays. My earliest purchase of shares was in May of 2020 at 90 cents and my last was in November at about $1.50 because enrollment (although slowing) was nearly complete. The final data on 20 (or possibly more) patients will be collected at the end of April or beginning of May. Rather than a few more weeks to analyze and report data, I anticipate data release in May because data collection has been ongoing and the data analysis team has probably completed full data analysis for the first 19 participants. They will only have to plug in data for the last enrollee(s).

As far as news leaking out, in late December of 2023, on Episode #194 of the Blink of an Eye podcast, 42 minutes into the conversation with the director of the trial provided this nugget:

Hostess: “Another one of our families who has been involved, they don’t know if they have the placebo or the real peptide or not, but they’ve just been thrilled by the hour that they’ve had everyday at the Shirley Ryan by the assessments, what they’ve learned about their son’s body AND they believe there has already been improvement and it was only days then and now weeks (LAUGHTER)

The Trial Director: We don’t know who has the placebo and who has the peptide but obviously there’s speculation when we see individuals making gains. Is it the placebo effect? Is it the drug?

Later in 2024, a man who participated in the trial blogged that he had doubled his walking speed (although he hopes he was in the placebo group because he was not impressed by doubling his walking speed in 16 weeks)

Finally, the family of a boy who became paralyzed in the summer of 2023 revealed that their boy had been accepted as Patient #2 in the trial. After a year of going silent, a couple weeks ago they returned to the blog frustrated because enrollment had been so slow. They went public with how their son did as a participant. He had done so well in the trial, they were trying unsuccessfully to get more NVG-291 from the company so their boy could keep improving which NervGen could not legally provide. However, they had recently discovered a way they might be able to get the drug by petitioning the FDA and so they let everyone know about the FDA loophole they were hoping might allow them to continue treatment.

Jerry Silver did not design the trial. CMO Dan Mikol was responsible for the trial which won awards for its design. Changes to the 20 patient sub-acute trial should lead to quicker enrollment beginning very soon.

With results in May, I think this is the best investment one can make now. NWI had some excellent results in 2024, but I think accumulation of NGENF from January to April will outperform even PLTR’s 254% gain since NWI recommended it after the May pullback. Also of note, NVGNF’s drug has also had superior results in animal studies of MS and stroke and success in this human SCI trial will lead to human trials in those indications.

I also believe that MDNA’s price, which is going into hibernation for a few months, will take off in the summer, making its 280% gain in 2024 look like a warmup lap. And then in August CAPR will triple from its current price.

CAPR has a fantastic drug. The share price will go sharply higher, there is nothing holding it back. Strong buy!

Hi John, could you also advise what you see as the catalysts that will drive the CAPR stock price up and timing? Thx

Hey John, pls share your insights and why such strong belief in CAPR, thank you

They have plenty of cash on hand. They were just granted a BLA for their drug Deramiocel, which we will be an easy approval, and will target a much wider audience. FDA seems to be pushing for an early and easy approval.Last presentation from their CEO was rock solid with full steam ahead, No supply chain issues. A very safe drug for the children who are diagnosed with MS, Their drug has shown an added benefit for cardiomyopathy , which was not expected. They will file approval with EU agencies and they have a partner in place. Their drug is better than Sarepta in treating this disease. 500 patients at launch that is 500 million right off the bat.It has come down from 23 but they will have plenty of demand and within 18 to 24 months it will be over $100.00 dollars a share and even higher.

Thx John

Your welcome.

Thanks Chris. The 3 responders in the NGENF trial could be just 1 or 3 different cases. Still promising. As always, the ultimate price target depends on how much dilution is needed to fund all the trials for various conditions. Dilution is Brent’s pet peeve, with good reason. In May or June 2025, 3/10 responses could get a spike to $5-10, then settle down to $3 as the reality of dilution and long term trials is confronted.

Hey Chris, could you share your thoughts why you expect major moves on MDNA and CAPR? Thx

Lots of cancer drugs show early success and then fail the longer patients are followed. MDNA has shown more durable responses and as data becomes more mature, I think by this summer the data will reveal the differentiated nature of MDNA’s drugs, especially how much more effective the #1 selling drug (Merck’s Keytruda) is when paired with Medicenna’s MDNA 11, in studies which began in 2022. I expect new data to continue to show significantly better results from the combination than from Keytruda alone. New data will drive up MDNA’s mkt cap (currently $82M) as more people realize how special MDNA’s medicine is. Merck (mkt cap $255Billion) will probably want to buy Medicenna outright at a price at more than 10x higher than than its current market cap.

CAPR filed its BLA for its drug, deramiocel, before the end of the year,THe DFA has 60 days to accept or reject the application. Expect a pop in early March if CAPR does not need to refile. All indications are that the FDA wil then approve CAPR’s license to sell its drug around September. I anticipate shares will go to $45 that day and then double from there in 2026.

MDNA or MDNAF? .15 for one and 1.06 for the other. Why?

MDNA was the Nasdaq symbol. It left the Nasdaq over a year ago & now trades as MDNAF.

Happy New Year MM! Thanks for the year recap.

MM – With regard to VET, would you please provide the source of the 2025 free cash flow estimate ($450 million or $2.90/share) cited above? I did not notice that number being explicitly provided in VET’s 12/23/24 summary of the Westbrick acquisition. Thanks.

https://www.vermilionenergy.com/invest-with-us/press-releases/press-release-detail/?id=122844

“Based on a mid-Q1 2025 close and forward commodity prices, including the impact from the current hedge position which covers approximately 25% of 2025 production, Vermilion forecasts pro forma 2025 FFO of $1.2 billion (~$7.80 per share)(3) and FCF of approximately $450 million (~$2.90 per share).”

Jensen Huang’s Quantum Computing Reality Check: Impact on Quantum StocksLast updated 1 hour ago

During an investor meeting, NVIDIA CEO Jensen Huang expressed skepticism about the near-term realization of practical quantum computing, estimating that useful quantum computers are 15 to 30 years away. This statement led to a significant drop in the stock prices of several quantum computing companies like IonQ, Rigetti Computing, and Quantum Computing Inc. in after-hours trading. Huang’s cautious timeline contrasted with previous optimism, sparking discussions on the viability and market speculation around quantum technology. While some investors and analysts remain hopeful about the future of quantum computing, others see the current market enthusiasm as speculative and possibly overhyped.

This story is a summary of posts on X and may evolve over time. Grok can make mistakes, verify its outputs.

New World Investor for 1.9.25 is posted. New Big Tech AI recommendation!