Dear New World Investor:

Buy The Next Big AI Stock

My position on Artificial Intelligence (AI) is that what we have and are likely to have for the foreseeable future actually is Imitative Intelligence, if only because no one understands how human intelligence really works. Using lots of very fast parallel-processing semiconductors, a.k.a. graphics processing units or GPUs, can make it seem like a computer is thinking, but really what it is doing is wowing us by retrieving and comparing data at speeds we’ve never seen before.

We saw this when IBM’s Deep Blue computer beat world chess champion Garry Kasparov in 1997. Was IBM’s software “smarter” or “more creative” than Kasparov? Not at all. It simply played thousands of potential future moves and counter-moves at lightning speed and then picked the one that had the highest probability of success. Then, after Kasparov made his next move, Deep Blue did it again. Today, chess programs running on mobile phones can defeat even the strongest human players.

Like the chess programs, OpenAI’s latest large language model, OpenAI o3, breaks down complex tasks into smaller steps. If one approach doesn’t work, it tries something else. o3 often spends 15 minutes on a single problem, keeping track of everything it tries along the way. All of this “thinking” uses a lot of processing power, roughly 50x more than ChatGPT. On a competitive programming exam, o3 scored among the world’s top 175 coders. It already solves math problems that professional mathematicians haven’t been able to. It’s really fast, so you think it’s smart.

A lot of venture capital is now being spent – wasted, I suspect – on Generalized AI. gAI actually will think like a human, and it may happen sometime. Just not soon.

But.

Having said that, I also believe that Imitative Intelligence is going to dramatically remake many industries and human endeavors, and create more wealth than the Internet and mobile revolutions did. So what’s the best investment to take advantage of this in 2025?

I expect the AI investment opportunities to follow the usual cycle. The first opportunities are in hardware, then system software, and then applications software. Right now, the major opportunities are in hardware: AI systems, semiconductors, networking, and other components. Most of the system software companies like OpenAI are private or a small part of a much larger company like Google, Microsoft, or Meta. I think Google is in trouble and Microsoft is fairly valued, so I recommended Meta. The only applications software company I’ve recommended is Palantir because it’s the only real one I’ve found. Most of the pretenders are just coat-tailing on AI to get their stock prices up.

Focusing on hardware, in the future the AI personal computer upgrade cycle should drive both Intel and Advanced Micro Devices (AMD).Today, while all the money is going into the big data centers, hardware is dominated by Nvidia. I first called on CEO Jensen Huang in 1999, and I recommended Nvidia in Boomberg. I plan to recommend it here at lower prices, but there’s an opportunity today to buy the next big AI stock at an attractive price

The key is in the phrase “keeping track of everything along the way.” There’s a huge amount of “everything,” so o3 needs a huge amount of memory. Today’s AI servers use 8x more memory than CPU-based computers. The memory in Nvidia’s latest AI racks costs more than the GPUs. The need for memory is going to rocket higher over the next two or three years.

But not just any memory. The DRAM (dynamic random-access memory) in your laptop just isn’t fast enough. Nvidia uses high-bandwidth memory (HBM) semiconductors from Micron and SC Hynix, and integrates a stack of memory chips together with their logic chips. HBM memory sales of $4 billion in 2024 are forecasted to increase 20x to $80 billion in 2026.

According to Mordor Intelligence, the top five HBM companies are Micron Technology, Samsung Electronics, SK Hynix, Intel, and Fujitsu:

Click for larger graphic h/t Mordor Intelligence

Buy Micron

I’ve followed Micron (MU) since its IPO and recommended it from time to time. They have a very productive R&D team and, most important, they know how to make semiconductors.

Unfortunately, that means they have to spend huge amounts of money to keep up with rapidly advancing semiconductor manufacturing technology to produce chips that sell for only a few dollars each during volatile computer sales cycles. That, in turn, has made for a very volatile stock – Micron has always been a trading sardine, not an eating sardine. That might be changing now as AI takes over computing at every level, but I’ll have to see it to believe it. As long as we remember that this is not a “buy and forget” stock, we’ll be OK.

As you can see from the Mordor chart above, Micron is a global leader in memory and is all-in on HBM. They are building a new $7 billion plant in Singapore just to do HBM advanced packaging. Yet the stock took a hit after they reported November first quarter results:

Click for larger graphic h/t Stockcharts.com

Click for larger graphic h/t Stockcharts.com

November quarter revenues rose 84% from last year to a record $8.71 billion, essentially right on the $8.70 billion estimate. Data center revenue grew 400% year-over-year and 40% sequentially, surpassing 50% of total revenue for the first time ever. But NAND (Not-AND) flash memory revenues dropped 5% from last year due to customer inventory reductions at PC and smartphone manufacturers that will continue through the current quarter. They had a 39.5% gross profit margin. Pro forma earnings of $1.79 a share also hit the $1.77 estimate.

The problem was that their February quarter guidance of $7.90 billion, ±$200 million, was over $1 billion below the $8.97 billion consensus estimate. They said their gross margin will drop a percentage point to 38.5%. Earnings guidance of $1.43 ±10¢ a share was a full 50¢ below the $1.93 estimate.

Management said they expect growth in consumer-oriented DRAM personal computer and NAND markets in the May and August quarters. (NAND flash is a non-volatile storage technology that does not require power to retain data. It is used in devices to which large files are frequently uploaded and replaced. MP3 players, digital cameras, and USB flash drives use NAND technology.)

On the conference call ( SLIDES HERE and PREPARED REMARKS HERE), CEO Sanjay Mehrotra said: “In 2028, we expect the HBM total addressable market (TAM) to grow four times from the $16 billion level in 2024 and to exceed $100 billion by 2030. Our TAM forecast for HBM in 2030 would be bigger than the size of the entire DRAM industry, including HBM, in calendar 2024. This HBM growth will be transformational for Micron, and we are excited about our industry leadership in this important product category.”

Nvidia accounted for 13% of November quarter revenues. That’s a good thing as long as Nvidia’s unit sales keep growing, as they will in 2025 and maybe 2026. Micron’s HBM3E 8H is designed into NVIDIA’s Blackwell B200 and GB200 platforms. The company already began high-volume shipments to their second large HBM customer and will start high-volume shipments to their third large customer in the current calendar quarter.

They said they continue to receive positive feedback from their leading customers for their HBM3E 12H best-in-class power consumption, which is 20% lower than the competition’s HBM3E 8H, even as the Micron product delivers 50% higher memory capacity and industry-leading performance.

For the August 2025 year, analysts are looking for revenues up 39.4% to $35.0 billion with earnings of $8.90 per share versus $1.30 last year. At Wednesday’s close, we can buy MU for only 11.2x this year’s earnings, a Price/Earnings/Growth (PEG) multiple of 0.36%, and less than 3.2x sales per share. That’s cheap. Buy MU under $102 for a first target of $140.

* * * * *

The CME FedWatch tool now has 93.1% agreeing with me and expecting no Fed funds rate cut at the January 29 meeting. That’s good because it’s already in the market and we’re still near the all-time highs. But that falls to 57.7% at the March 19 meeting, with 39.7% expecting a 25 basis point cut and 2.6% expecting 50bps.

The bond vigilantes seem determined to run the 10-year Treasury note yield to 5.0% and the 30-year bond to 6.0% based on relatively strong services sector activity and labor figures. I still expect the economy to slow because consumers are tapped out, but I’ve been singing that tune for a year and wrong so far.

If I’m right and the pace of economic growth slows during the first half of 2025, even without a recession bond yields are way too high. The 10-year bond yield seems likely to surprise most by declining significantly this year.

Market Outlook

The S&P 500 added 0.8% since last Thursday. About 85% of the time, the S&P trend for the year is in the same direction as the first five trading days of the new year, which were up, but only 0.6%. The Nasdaq Composite gained 1.0%. The SPDR S&P Biotech Exchange-Traded Fund (XBI) climbed 0.9% in advance of next week’s big JPMorgan Healthcare Conference. The small-cap Russell 2000 squeaked up 0.3% .

The fractal dimension continues to consolidate and now is fully consolidated with enough energy to start the next trend anytime.

Top 5

Changes this week: None

Near-Term – chronological order

AKBA Akebia Therapeutics – Vafseo launch in January

SCYX – ScyNexis – Announce resolution of the manufacturing problem, lifting of clinical hold, restart of MARIO trial, maybe GSK files for hospital use approval

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model estimate for December quarter GDP growth has settled at +2.7%, above the Blue Chip economists’ 2.1% average.

Click for larger graphic

Click for larger graphic

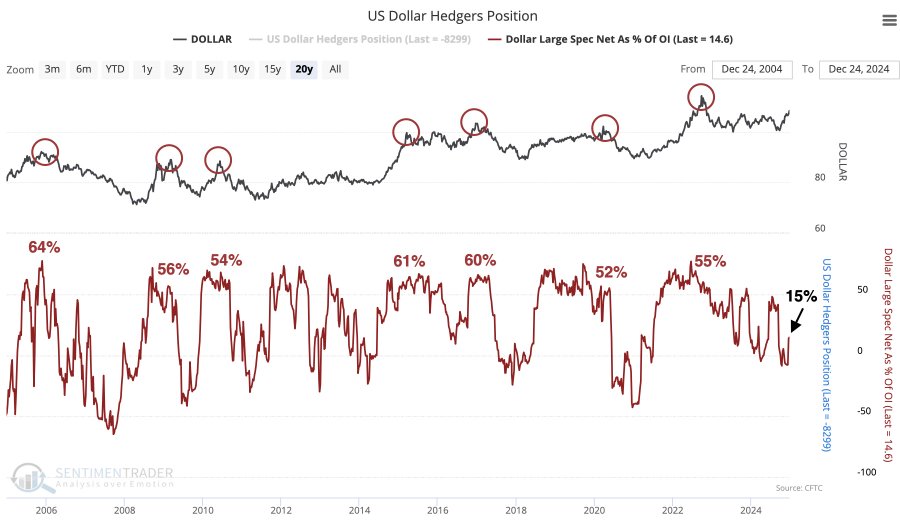

Dollar Death Watch

The dollar is going up against other currencies (currency futures) while it goes down in purchasing power (inflation). Every peak in the dollar over the past 20 years was accompanied by speculators holding at least 50% of futures net long. They are only 15% net long now. A higher dollar is a headwind for stocks, gold, and cryptocurrencies.

Click for larger graphic h/t @jasongoepfert

Click for larger graphic h/t @jasongoepfert

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, January 10

December payrolls – 8:30am – +160,000 expected; November was +227,000

Short Interest – After the close

Monday, January 13

GILD – Gilead Sciences – 2:15pm – JPMorgan Healthcare Conference

Tuesday, January 14

AG – First Majestic – 2:00pm – Special shareholders meeting to approve the Gatos Silver acquisition

Wednesday, January 15

Consumer Price Index – 8:30am

EDIT – Editas – 2:15pm – JPMorgan Healthcare Conference

QUIK – QuickLogic – 3:45pm – Needham Growth Conference

ABCL – AbCellera – 7:30pm – JPMorgan Healthcare Conference

Thursday, January 16

AKBA – Akebia Therapeutics – 10:30am – JPMorgan Healthcare Conference

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $242.70) introduced a number of new Fitness+ programs, including a three-week progressive strength training program, a conditioning program for pickleball, a new yoga program, and a breath meditation program for managing stress. It’s $9.99 a month or $79.99 a year. It’s included in the Premiere Plan that includes many other Apple services and can be shared with up to five family members. Buyers of most Apple products get three months free. This is how Apple is steadily growing its multibillion dollar Services business.

The stock was downgraded from Neutral to Sell at MoffettNathanson. AAPL is a HOLD – I expect to move back to Buy under $175 for new iPhones.

Meta Platforms (META – $610.72) is replacing it’s “Fact Checkers” with Community Notes, obviously copied from X (formerly Twitter). “On one hand, it’s frustrating to see Silicon Valley CEOs locate their testicles only after it’s easy to do so. (Although many are still quiet!) TFW you find the courage to fight for the truth at the exact moment it becomes risk free to do so. On the other, it’s incredible to see how hard the vibe is truly shifting. This is feeling more durable now.”

– h/t @eoghan

META is a Hold – Buy or add whenever it hits its lower Bollinger Band, now under $580.

Click for larger graphic

Click for larger graphic

Palantir (PLTR – $68.23) was hit after Morgan Stanley predicted a 25% decline in the stock. Maybe, maybe not. I’d raise the buy limit if that happens. If Palantir is a mystery to you, check out this 2009 interview with CEO Alex Karp.

PLTR is a Buy under $22 for a $100+ target.

Snap (SNAP – $12.04) did a study on how Augmented Reality (AR) affects the attention of consumers looking at advertisements. They already knew that consumers pay 2x attention to video ads. With AR in the mix, Snapchat drives 5x more active attention compared to industry peers. All types of Lenses drove high active attention and lifts in both short-term brand choice and long-term brand loyalty, but shareable AR experiences supercharged impact.

New independent research from The Netherlands and Australia validates how Snapchat was designed from the beginning – as an alternative to social media to connect with friends and family. The University of Amsterdam conducted research into adolescent use of large social media platforms and concluded that Snapchat is the only platform that positively impacts well-being. Findings from the study included:

“We found a consistent negative impact on time spent on TikTok, Instagram, and YouTube across all three mental health dimensions. Conversely, spending time on Snapchat positively affected friendship closeness and well-being but had no significant impact on self-esteem.”

“The positive and null effects associated with Snapchat and WhatsApp indicate that we should avoid a blanket condemnation of all social media platforms.”

Three Australian mental health organizations recently jointly submitted research results as part of the Australian Parliament’s investigation into social media and Australian society. The findings, which are drawn from The Future Proofing Study, Australia’s largest longitudinal study into youth mental health, uncovered that:

“[In contrast to other platforms], a higher number of hours on Snapchat was not found to be significantly associated with any of the mental health symptoms examined.”

“The study found no evidence to indicate that using social media to facilitate social connections was associated with poorer mental health. Rather, it found that more frequently using social media to communicate with people teens knew in real life was associated with lower symptoms of depression and anxiety. This may explain why a higher number of hours using Snapchat was not associated with any of the mental health symptoms examined, because Snapchat is a messaging app that adolescents primarily use to communicate with their friends.”

SNAP is a Buy under $11 for a $17+ target.

Small Tech

Enovix (ENVX – $12.33) said it received a sizable pre-paid purchase order from a Silicon Valley-based global technology leader in AI and immersive technologies for a cutting-edge battery solution tailored for next-generation head-worn Mixed Reality (MR) wearables. These batteries will support the revolution of smart glasses, augmented reality devices, and other pioneering products in the MR space. Enovix is scheduled to deliver initial shipments by mid-2025.

I assumed this was the same customer to whom they previously shipped samples, but CEO Raj Talluri said: “I’m incredibly excited for Enovix to be selected by another leading OEM in this emerging space.”

ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

QuickLogic (QUIK – $9.24) is going to sell SensiML. CEO Brian Faith said he acquired SensiML for the leverage opportunities between its unique AI/ML software and QUIK’s focus on sensor processing. But with the success and profitability of their eFPGA Hard IP and ruggedized FPGA products, he wants to focus all of their resources on the growth of their core business model and the Storefront opportunities it leverages.

Brian said his decision was influenced by recent events, including eFPGA Hard IP design wins with strategic customers, expansion of large government ruggedized FPGA and eFPGA Hard IP contracts, performance improvements of their eFPGA Hard IP products, recent change in the eFPGA market competitor landscape (Intel spinning out Altera and AMD’s president and ex-CEO of Xilinx retiring), and an increase in inbound interest from customers of former eFPGA market competitors.

Brian has done a great job of remaking QuickLogic and QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $27.36) was selected by Kratos to deliver hypersonic test launches for DoD with its HASTE Rocket. HASTE is a suborbital variant of Rocket Lab’s Electron launch vehicle. The total potential value of this MACH-TB 2.0 contract award is $1.45 billion over five years. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

On Statnews, Allison DeAngelis and Adam Feuerstein wrote: “Next week brings the return of the J.P. Morgan Healthcare Conference, and with it another fabled opportunity for companies in the industry to court possible mergers, acquisitions, and licensing deals. This year, there will be even greater pressure to make a good match, as the pharmaceutical industry, which drives more than $1 trillion in economic activity and thousands of jobs, faces one of the largest patent cliffs in recent history.

“Between now and 2033, the patents on dozens of brand-name medications will expire, allowing generic drugmakers to begin selling cheaper versions. Drug companies stand to lose more than $400 billion in revenue as patents expire for Keytruda, Eliquis, Jardiance, Opdivo, and other blockbuster therapies. (By comparison, the last major patent cliff that hit the industry, in 2011, jeopardized around $250 billion in drug revenue.)

“One of the few tried-and-tested methods for navigating a patent cliff is to acquire startups and new drugs — and lots of them. As a result, many experts anticipate pharma ramping up M&A activity in 2025, starting at the J.P. Morgan conference.”

Four of our recommendations are presenting at the conference: Gilead, AbCellera, Akebia, and Editas.

AbCellera Biologics (ABCL- $3.03) is a Buy up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $1.79) is a Buy up to $2 for the Vafseo launches in the EU, UK, and US.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: NM

Probable time of next financing: Never

Editas Medicine (EDIT – $1.34) is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2026

Probable time of next financing: 2026 or ne

Inflation MegaShift

Gold ($2,691.60) has held up well as the dollar strengthens. That probably means some substantial central bank buying is underway. The fractal dimension is racing towards full consolidation as speculators sell and short because of the dollar and the Fed, while central banks buy.

Click for larger graphic

Click for larger graphic

Miners & Related

First Majestic (AG – $5.88) had December quarter production of 5.7 million silver equivalent ounces, up 4% from the September quarter, consisting of 39,506 gold ounces and 2.4 million silver ounces. Silver production was up 20% from the September quarter, led by a 39% increase at the La Encantada mine as it returned to historical production rates following the recovery of water inventory levels.

Total production for the full year was 21.7 million silver equivalent ounces, consisting of 8.4 million silver ounces and 156,542 gold ounces. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.69) said in the December quarter they sold approximately 17,700 attributable gold equivalent ounces and realized preliminary revenue of $47.4 million. They had cash operating margins of approximately $2,397 per attributable gold equivalent ounce.

They reiterated their long-term production forecast of approximately 125,000 attributable gold equivalent ounces within the next five years, based solely on streams and royalties already bought and paid for.

In 2024, they deleveraged their balance sheet by paying down debt used to make several royalty and streaming acquisitions in 2022. As of December 31, the outstanding balance on their revolving credit facility was approximately $355 million, with an undrawn and available balance of $270 million. During the year they also bought back 2.0 million shares for approximately $10.8 million. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $92,114.84) blipped over $100,000 for the nth time, clutched its pearls for the nth time, and retreated. This is classic consolidation action and it will keep happening until it doesn’t, trapping large amounts of money on the sidelines as it takes off.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $53.34) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Ethereum Trust (ETHA- $24.84) remains the cheapest and easiest way to buy etherum. ETHA is a Buy.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $74.16

Oil moved up as US oil production fell to ~13 million barrels a day. That is ~500,000 to ~550,000 barrels a day lower than consensus estimate for exiting 2024. Last year will show the weakest year-over-year US oil production growth since the US shale revolution started, excepting the 2020 COVID-19 production shut-in. There was no adverse weather event in December, this is the new normal. Speculators are all-in on lower oil prices and still think they are facing only short-term supply risks. It’s going to be great fun watching the elephants run for the exit.

The July 2026 Crude Oil Futures (CLN26.NYM – $67.27) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $38.71) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $10.19) is a Buy under $11 for a target price of $24 or more.

Primary Risk: Oil prices fall.

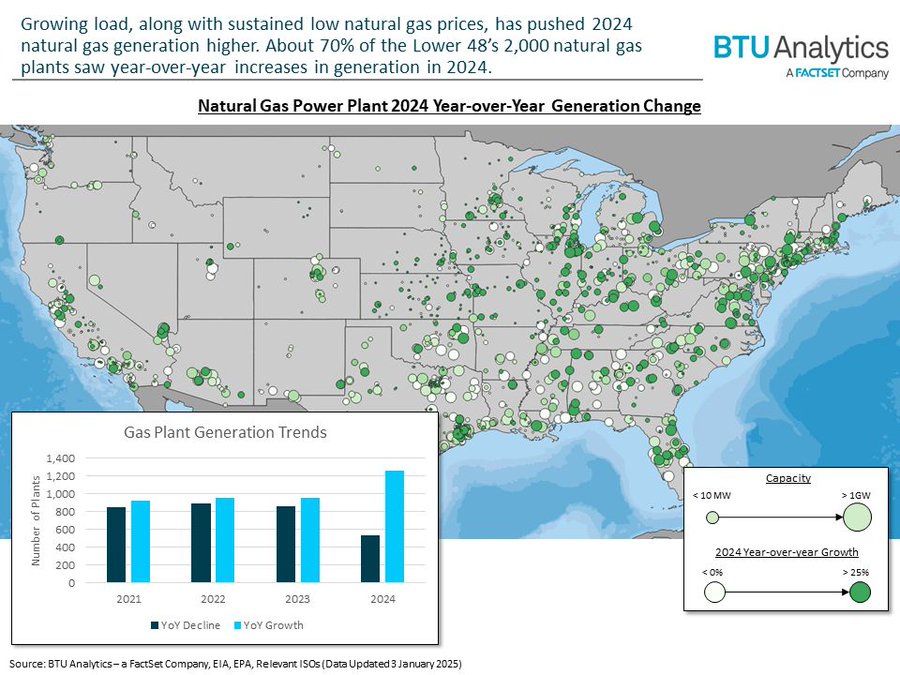

EQT (EQT – $49.00) closed the sale of its remaining non-operated natural gas assets in Northeast Pennsylvania to Equinor USA Onshore Properties and its affiliates. EQT received approximately $1.25 billion in cash, which was used to repay outstanding borrowings under their revolving credit facility.

In 2025, grid operators are thinking about how they will be meeting the expected rise in demand from data centers and load growth. According to BTU Analytics latest Energy Market Insight, the answer is natural gas. They looked at generation interconnection queues in the US to see just how much natural gas generation is lining up to join the grid and the challenges these generators could face in sourcing the country’s predominant fuel.

Click for larger graphic h/t @FactSet

Click for larger graphic h/t @FactSet

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Freeport McMoRan (FCX – $39.74) will move up as the copper chart is looking great again.

Click for larger graphic h/t @AndreasSteno

Click for larger graphic h/t @AndreasSteno

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

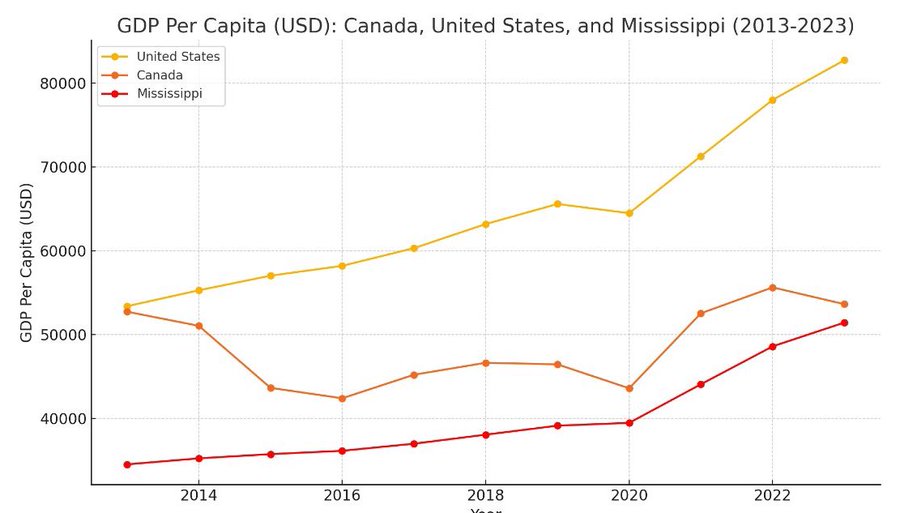

Is it really worth it to have Canada as the 51st US state? During the last decade, Canada has gone from being as prosperous as the US to being almost as poor as the poorest US state, Mississippi.

Click for larger graphic h/t @MichaelAArouet and @BuBarrelBull

Click for larger graphic h/t @MichaelAArouet and @BuBarrelBull

* * * * *

Your appalled by the UK rape gang scandal Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 1/8/25, except bitcoin, ethereun, and crude oil futures priced 1/9/25. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $47.73 – Buy under $33, target price $60

Gilead Sciences (GILD – $89.14) – Buy under $80, target price $120

Micron Technology (MU – $99.41) – Buy under $102, first target price $140

Palantir (PLTR – $68.23) – Buy under $22, target price $100+

PayPal (PYPL – $87.94) – Buy under $68, target price $136

Snap (SNAP – $12.04) – Buy under $11, target price $17+

SoftBank (SFTBY – $29.38) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $12.33) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $64.16) – Buy under $60; 3- to 5-year hold

Fastly (FSLY – $9.42) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $17.71) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $9.24) – Buy under $10, target price $40

Rocket Lab (RKLB – $27.36) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.03) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.79) – Buy under $2, target $20

Compass Pathways (CMPS – $4.14) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $1.34) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $2.09) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.02) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.23) – Buy under $3, target price $20, then $50

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($30.73) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $29.08) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $35.48) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $24.75) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $33.22) – Buy under $30, target price $50

Coeur Mining (CDE – $6.44) – Buy under $5, target price $20

Dakota Gold (DC – $2.30) – Buy under $2.50, target price $6

First Majestic Mining (AG – $5.88) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.36) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.69) – Buy under $10, target price $25

Sprott Inc. (SII – $42.05) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $92,114.84) – Buy

iShares Bitcoin Trust (IBIT – $53.34) – Buy

Ethereum (ETH-USD – $3,233.13)– Buy

iShares Ethereum Trust (ETHA- $24.84) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $67.27 ) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $38.71) – Buy under $40; $100+ target

Vermilion Energy (VET – $10.19) – Buy under $11; $24 target

Energy Fuels (UUUU – $5.40) – Buy under $8; $30 target

EQT (EQT – $49.00) – Buy under $35; $70 first target

Freeport McMoRan (FCX – $39.74) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $242.70) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $610.72) – Expect to move back to Buy

TG Therapeutics (TGTX – $28.77) – Hold for buyout at $40+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2025

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First on a boring snowy day

Yeah, it stinks when the market is closed during the week!!

One good thing. you didn’t lose any money today.The market was flat.

META: What kind of Free Speech is Prevented By Fact Checking??

Lies. Gross exaggerations. Psychotic statements.

It depends on who is doing the fact checking, are they unbiased or do they have an agenda.

I agree with your take on Micron . I bought it several years ago (when it was out of favor with brokerages) , held it a few years and sold it tripling my money. Which was great at the time but now the price has tripled again!! Also the information on energy is on the money IMO. The demand for electricity will double starting in 2025. AI and data storage will suck up huge amounts of electricity. Warren Buffett seems to think so because he has added to his position in OXY recently while selling off other positions. He now has some $325 billion in cash.

So John, what in your opinion is the best stockmor stocks to buy to profit on the energy demand coming?

Add to calendar – TODAY

TGTX @ JPMorgan 7:30pm EST

that was a good one with bonus of preliminary Q4#

%24 revenue growth Q over Q and %160 from Q4 2023

5 year 0.02 relapse rate is about as close to a cure as can be. wate till eu # start really coming in.

In the Jan. 2 Radar Report, Murphy wrote, AKBA “has not announced either a Fresenius contract or the Vafseo launch. I expect both announcements before their January 16 presentation at the JPMorgan conference.” Today Akebia announced the Fresenius contract. it also announced its plans to begin a Phase 3 trial for the use of vadadustat in treating anemia in late-stage CKD patients who are not on dialysis expected to begin in midyear. Akebia received feedback from the U.S. Food and Drug Administration (FDA) on its protocol submission for a label expansion study and is incorporating feedback as appropriate.

Said John P. Butler, Chief Executive Officer of Akebia, “During 2025 our commercial organization will remain focused on executing the U.S. launch of Vafseo, while our development team pursues label expansion of Vafseo into the non-dialysis population, which represents a potential multiple billion-dollar market opportunity in the U.S.

https://finance.yahoo.com/news/akebia-therapeutics-announces-multiple-positive-130000009.html?fr=yhssrp_catchall

Yes I saw the press relesse but very muted response on the stock price. MM – why such a disconnect in stock price from the supposed billion dollare promise of this drug?

Many people like us have been long suffering KERX shareholders. When KERX merged with AKBA, holders had a high cost basis in AKBA. We are pissed. But I slowly awoke to the huge potential of Vafseo, AKBA’s new drug. There were a few lucky investors who went all-in at 25 cents at the time of the CRL. The minor risk is the following. In Japan, the 5 HIF drugs including V have had mediocre sales after 4 years. V had only $12-24 million annual sales. The population of Japan is 125 million, 38% of US. The dialysis population is 350 million in Japan, 550 million in US. Why is the per capita dialysis incidence so high in Japan? Average life expectancy in Japan is 87 for a woman, 81 for a man, excellent and much better than US at 81, 77, respectively. The answer is that the longer you live, the more likely you get kidney disease. CKD is caused by toxins and microvascular disease. As we age, we accumulate more toxic junk in the body. The main risk for AKBA is if US experience follows that in Japan.

For me, THE key to AKBA bullishness is TDAPA. TDAPA is a govt mandated huge subsidy program that will make V profitable with only modest uptake of the drug. Dialysis organizations get paid to pressure nephrologists to prescribe V and switch patients from ESA’s to V. A recent survey of nephrologists found that almost 100% say they want to try V in 2025. Why TDAPA in CKD? It is a political ploy for the benefit of Black Americans whose incidence of diabetes and HBP is much higher. Diabetes and HBP are big root causes of CKD. This is our chance to profit from preferential treatment, instead of suffering the stealing of high taxes for the benefit of others and sacrifice of ourselves.

Correction–dialysis pop is 350 thousand in Japan, 500 thousand in US.

To some extent, word was leaked out yesterday? Look at the chart, higher than normal volume and some bounce higher in price, but nothing way out of ordinary yesterday. Last six months stock has appreciated, expectations already built in?? Not many people paying attention to this stock, or not willing to invest in biotech, or willing to wait for financial benefits to materialize??

Expectations for only small sales built in, based on experience in Japan and other countries. But only the US has TDAPA, which is a game changer. Also, now Vafseo is the only HIF drug available in US, so it’s either V or established ESA’s. Yahoo Finance average target is $5.50, based on minimal 2025 sales estimates. Follow buythehornz127 and hsainu on Stocktwits, who have done the most research. Hornz is a big time lawyer, hsainu is a doctor.

AKBA, SCYX What are you missing that is clearly reflected in the stock price of each of these biotechs? It seems nobody wants either

It’s not what I am missing, it is what I am seeing that others don’t see yet. AKBA -rapid uptake of Vafseo due to TDAPA. SCYX – fungicidal for hospital use (FURI, CARES, and especially MARIO trial)..

MM so why doesnt anyone else see it? Ive lost lotsa money on biotechs that held high promise but never delivered, sime recommended by thus newsletter. So tell me/us plesse, what level of conviction do you have on the success of both companies and their stock prices THIS yesr not 5-10 years from now? Thank you

I don’t think enough people are looking to see it. Biotech is a hated sector right now. My best guess for AKBA by the end of this year is $5, but I hope you intend to hold it longer. I certainly do.

SCYX is harder because much depends on what GSK does. but I’d say $3 easy and $5 maybe on 12/31/25.

NGENF (overwight Long)

From the Associated Press:

Elon Musk says a third patient got a Neuralink brain implant. The work is part of a booming field

January 13, 2025

Elon Musk said a third person has received an implant from his brain-computer interface company Neuralink, one of many groups working to connect the nervous system to machines.

“We’ve got … three humans with Neuralinks and all are working well,” he said during a wide-ranging interview at a Las Vegas event streamed on his social media platform X.

Since the first brain implant about a year ago, Musk said the company has upgraded the devices with more electrodes, higher bandwidth and longer battery life. Musk also said Neuralink hopes to implant the experimental devices in 20 to 30 more people this year.

Musk didn’t provide any details about the latest patient, but there are updates on the previous ones.

The second recipient — who has a spinal cord injury and got the implant last summer — was playing video games with the help of the device and learning how to use computer-aided design software to create 3-D objects. The first patient, also paralyzed after a spinal cord injury, described how it helped him play video games and chess.

But while such developments at Neuralink often attract notice, many other companies and research groups are working on similar projects. Two studies last year in the New England Journal of Medicine described how brain-computer interfaces, or BCIs, helped people with ALS communicate better.

https://apnews.com/article/elon-musk-neuralink-brain-computer-interface-9dbc92206389f27fd032825cf1597ee5

From your humble contributor

While being able to play chess is a neat trick for an SCI patient, it is a far cry from actually improving mobility or manual dexterity. NervGen’s market cap is $248M. Neuralink had a valuation of $5Billion in 2023

https://www.reuters.com/technology/musks-neuralink-valued-about-5-bln-despite-long-road-market-2023-06-05/

$5Billion is 23x higher than $248M. Just sayin’

New World Investor for 1.16.25 ib posted. It’s Time To Invest In Human-Like Robots