Dear New World Investor:

It’s Time To Invest In Human-Like Robots

Artificial Intelligence will have many impacts on our economy and society. Large Language Models already are answering customer questions, helping coders debug programs, and designing biotech drugs. AI also will affect the physical world, from full self-driving cars to humanoid robots. Both need to quickly adapt to their environment and respond appropriately to new information. That’s why Tesla and Nvidia are making large investments in robot development, as well as the many robot-focused private companies like Boston Dynamics.

Tesla’s Optimus robot already is working in their offices and factories. Factories, of course, will use humanoid robots first while they are still expensive. They’ve used automation, often in the form of robots designed for specific jobs like auto door assembly, since the 1960s. Management is used to thinking about robots as useful parts of the production process. But those robots are not easily adaptable to other jobs and aren’t aware of their surroundings.

With the advances in AI, machine vision, and batteries, humanoid robots are happening right now. Elon Musk’s price point of around $25,000 per Optimus robot times initial US demand for maybe one million robots makes this a $25 billion market. Eventually, most families will want a humanoid robot for help around the house – laundry, meal prep, fixing appliances, babysitter, executive assistant. I think demand will grow to at least 10 million robots a year over time, a $250 billion market. Let’s get our share.

Musk has said that the majority of Tesla’s long-term value will come from Optimus. I’d love to recommend Tesla but automobile manufacturing is a terrible, low-margin business and still the core of Tesla. Instead, we’re going to buy one of Tesla’s key suppliers of the sensor technology that enables self-driving cars to see. It also supplies more than 300 power and analog semiconductors to Tesla.

Buy Onsemi

Onsemi’s (ON) best businesses are sensors and power semiconductors. Power semiconductors historically have been built on two technologies: metal-oxide-semiconductor field-effect transistors (MOSFETs) and insulated-gate bipolar transistors (IGBTs).

MOSFETs are typically built on silicon and used in lower-voltage applications ranging from 10 to 500 volts. Think low-voltage consumer products, adapters, and power supplies. A variant, super-junction MOSFETs, are used in 500- to 900-volt systems.

IGBTs also are built on silicon and are used in high-voltage applications like EVs and solar panels. They are typically used for 1200 to 6600 volt applications. When I set the Class 1/E electric car record at the Bonneville Salt Flats in 1999, the Godzilla controller that sat between my car full of batteries and kept the four electric motors from melting was built by the great Otmar Ebenhoech using IGBTs, which he called “insanely great bits.” But silicon-based MOSFETs and IGBTs aren’t optimal for very high-power applications like electric vehicles and 5G wireless networks.

So demand is shifting to materials that can handle higher power. Gallium nitride-based field-effect transistors (GaNFETs) have a 5x to 50x performance improvement over silicon MOSFETs. GaN is 10x faster than silicon and produces less heat, even at higher power levels.

Silicon carbide (SiC) has the same 5x to 50x performance improvement and can handle a much higher voltage level than even GaN. Onsemi is a leader in both GaN and SiC. They have a 24% market share in SiC power chips. They just acquired the Silicon Carbide Junction Field-Effect Transistor (SiC JFET) technology business, including the United Silicon Carbide subsidiary, from Qorvo for $115 million in cash. They said the addition of SiC JFET technology will complement their extensive EliteSiC power portfolio and enable the company to address the need for high energy efficiency and power density in the AC-DC stage in power supply units for AI data centers. In electric vehicle applications, SiC JFETs help improve efficiency and safety by replacing multiple components with a solid-state switch based on SiC JFET in battery disconnect units. In the industrial end-market, SiC JFETs enable certain energy storage topologies and solid-state circuit breakers.

About half of Onsemi’s revenues come from auto manufacturers, where they sell various internal sensors and chips to manage the flow of power during charging, control how the power from the battery turns the axles, enable advanced driver-assist systems for full self-driving, provide in-vehicle networking, and so on.

Virtually every auto manufacturer and many component manufacturers are customers, including Aptiv, BorgWarner, Bosch, BYD (the world’s largest producer of EVs by volume), Denso, Hyundai Kia, Li Auto, Nio, Tesla, Veoneer, and Volkswagen. Tesla and other car companies developing autonomous vehicles also use Onsemi’s imaging sensors, acquired in 2014 with their $400 million purchase of Aptina. ON has a 45% share of the automobile industry image sensor market.

The autonomous software, sensors, and power management needed to operate an EV are similar to the software, sensors, and power management needed to operate a humanoid robot that has to navigate the real world. I expect Onsemi to leverage their EV position to be a major supplier of image sensors and power management chips to the humanoid robot industry. They could probably sell $500 worth of components per robot.

They’ll report December fourth quarter earnings early in February. Due to global weakness in autos and manufacturing, analysts are expecting revenues to be down 12.9% to $1.71 billion and earnings to fall from $1.25 a share last year to 98¢. That would bring them in at $7.12 billion in revenues for the year, down 13.7%, with earnings of $4.00 per share versus $5.16 last year. Sounds bad, right?

Revenues and earnings probably will be down, but ON usually beats the estimate and is about to enter a multiyear growth phase driven by EVs, robots, AI data centers, and new products. Onsemi can grow at 10% to 12% a year for the foreseeable future. Yet the stock is selling for only 13.7x earnings, 3.25x sales per share, and 2.75x book value. It’s the cheapest it’s been in two years.

Click for larger graphic

I want you to Buy ON under $60 for a first target of $100. If the market re-rates it as an AI and robotics play, it can hit $150+.

* * * * *

The headline December consumer price index (CPI) rose 2.9% year-over-year (YOY), right on consensus expectations and a tad quicker than November’s 2.7%. The month-over-month (MOM) increase was 0.4%, a tenth above both the consensus and November’s 0.3%.

The YOY core CPI ex-food and energy was up 3.2%, a tenth below the consensus and November’s 3.3%. The MOM core was up 0.4%, a tenth above the consensus and November’s 0.3%.

The stock market liked it, but my take is: “Move along, move along, nothing to see here.”

The real problem is not the debt, it’s the rate at which the debt is increasing. The December first quarter of fiscal year 2025 produced a deficit of $710.9 million. That’s $200 billion more than the December quarter of fiscal 2024, or a 39% increase YOY. It is a $2.8 trillion annual deficit rate.

In the quarter, the Federal government had total revenues – taxes, fees, and tariffs – of $454 billion. They paid $140 billion in interest on the national debt – 31% of all government revenue was consumed by interest payments on the debt. Getting this under control – reining in Congress and reducing the bureaucracy – will pressure economic growth. It could be offset by increased capital spending if people are more confident that our economy will stabilize. We shall see.

Market Outlook

The S&P 500 added 0.3% since last Wednesday. The Index is up 0.9% year-to-date. The Nasdaq Composite lost 0.7% as the big AI stocks lagged before upcoming earnings reports, but it is up 1.4% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 4.8% as the painful biotech bear market continued, even though the big JPMorgan Healthcare Conference was this week. It is down 2.4% year-to-date. The small-cap Russell 2000 gained 1.2% and is up 1.6% in 2025.

The fractal dimension included last Friday’s wipeout to end the week and this week’s sharp recovery to say: “Hey, I know more consolidation when I see it.”

Top 5

Changes this week: None

Near-Term – chronological order

AKBA Akebia Therapeutics – Vafseo launch

SCYX – ScyNexis – Announce resolution of the manufacturing problem, lifting of clinical hold, restart of MARIO trial, maybe GSK files for hospital use approval

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

UUUU Energy Focus – Domestic uranium supplier

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $150,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model raised its estimate this morning of December quarter real GDP growth from +2.7% to +3.0% due to strength in both personal consumption expenditures growth and government expenditures growth.

Click for larger graphic

Click for larger graphic

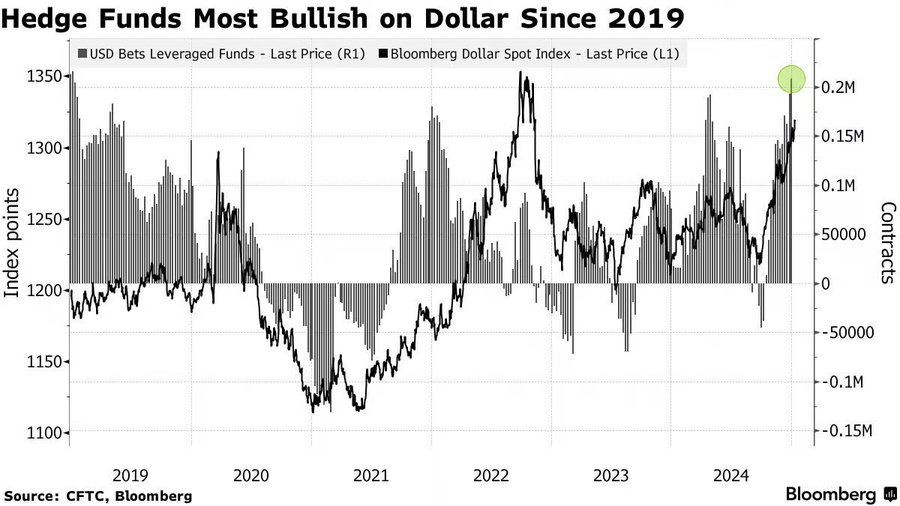

Dollar Death Watch

Bullish dollar positioning is at its highest since January 2019. Crowded trades almost never work out.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, January 20

Markets Closed – MLK Day

President Trump’s Inauguration – 12:00pm

Thursday, January 23

FCX – Freeport McMoRan – 10:00am – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Gilead Sciences (GILD – $92.33) presented at the big JPMorgan Healthcare Conference, the granddaddy of these meetings (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE).

CEO Dan O’Day said: “…after several years of high investments, which was really necessary to diversify the portfolio and strengthen our approach to HIV, we’re really now in a period of time of consistent execution – at a point in time where that investment is turning into commercial benefits, and we’re set to see those investments set to grow into the future. So in the year ahead, in summary, you’re going to see a growing portfolio, growing revenues, and a significantly improved operational efficiency as a result of where we are in our financial discipline.”

They expect lenacapavir to extend their HIV leadership beyond the 2030s. Because it is long-acting it should become the drug of choice for those already infected. In addition, it is very effective for HIV prevention, where it will launch this summer.

Click for larger graphic

Click for larger graphic

They plan nine product launches based on this molecule by the end of 2033.

Click for larger graphic

Click for larger graphic

Dan said Gilead has a very deep pipeline of over 100 future drugs. They are deliberately diversified across therapeutic areas, mechanisms of action, and phase of development from preclinical to Phase 3. They expect three best-in-class near-term launches to drive their growth (R/R MM is relapsed/refractory multiple myeloma). The have more than 10 potential first-in-class drugs in Phase 2 and Phase 3 trials.

Click for larger graphic

Click for larger graphic

As the R&D investment that depressed earnings turns into commercial products, operating margins will expand.

Click for larger graphic

Click for larger graphic

Gilead has grown their dividend from $2.72 a share in 2020 to $3.80 in 2024 and bought back another $1.2 billion in stock last year. They expect to return at least half of free cash flow to shareholders. It’s a great stock for the conservative part of your portfolio. You get a 3.3% yield while you wait for higher stock prices. I am raising the buy limit to $90. GILD is a Long-Term Buy under $90 for a first target of $120.

Meta Platforms (META – $611.84) is going to fire 5% of their lowest performers, according to Bloomberg. META is a Hold – Buy or add whenever it hits its lower Bollinger Band, now under $581.

Palantir (PLTR – $70.78) partnered with EllisDon, a global construction services and technology company, to deploy AI. The UK Ministry of Defense disclosed the existence of Nordic Warden, backed by Palantir. It is the AI system that identifies ships and calculates the risk posed by each vessel entering areas of interest. PLTR is a Buy under $22 for a $100+ target.

SoftBank (SFTBY – $29.45) bought back another 908,200 shares in December, from December 2 to the 23rd. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $11.32) successfully completed Site Acceptance Testing (SAT) for its high volume manufacturing line at Fab2 in Malaysia. SAT validates the readiness of the manufacturing equipment through comprehensive testing. It follows the Factory Acceptance Testing (FAT) milestone completed earlier in 2024, marking the final stage before commercial-scale production begins. Together, FAT and SAT ensure that Fab2 is fully equipped to produce high-performance silicon batteries at volume. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

PagerDuty (PD – $18.61) presented at the Needham Growth Conference. CFO Harold Wilson gave the basic introductory presentation. He said they now have 15,000 paying customers, including 825 spending more than $100,000 a year, and another 15,000 in the free period that often leads to them becoming paying customers. Customers include half of the Fortune 500 and 87 of the Fortune 100.

Click for larger graphic

Click for larger graphic

In total they have about one million users today. The total market is 80 million potential users, so they are still early.

Click for larger graphic

Click for larger graphic

This is their typical journey with one customer:

Click for larger graphic

Click for larger graphic

PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $9.09) presented at the Needham Growth Conference (AUDIO HERE and SLIDES HERE). CEO Brian Faith said customers asked them to provide field-programmable gate array technology to include in new ASICs (application-specific integrated circuits), which launched their new business model:

Click for larger graphic

Click for larger graphic

In 2025. they expect positive cash flow in the March quarter and full-year profitability.

Click for larger graphic

Click for larger graphic

QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Rocket Lab USA (RKLB – $24.60) made a surprise presentation at the Needham Growth Conference (AUDIO HERE) and it is highly recommended if you have any interest in this area at all. CFO Adam Spice shortened the usual “Disclaimer and Forward-Looking Statements” boilerplate to: “It’s a rocket company” – to general merriment.

Rocket Lab has launched over 200 satellites on 58 Electron launches from the US and New Zealand. It is the second-most frequently launched US rocket and they have 40 spacecraft the backlog (a few of those are the forthcoming Neutron, a direct competitor to SpaceX’s Falcon 9). There are over 1700 satellites in orbit with Rocket Lab technology and they now have over 2000 employees across the globe. Over 70% of revenues are generated from non-launch activities. About 50% of revenues are from commercial customers, although 80% of their commercial customers are selling to the government, 30% from non-defense government, and 20% from defense.

There are thousands of satellites in orbit with three to five year lifespans, creating a large ongoing market for replacement launches. Rocket Lab’s two New Zealand launch pads can do up to 128 missions a year thanks to the low level of air and sea traffic. That is dramatically better than any US launch pad, including theirs in Virginia.

Electron can put about 660 pounds into orbit. Neutron can lift 28,660 pounds. It uses technology from Electron like carbon fiber fuel tanks instead of stainless steel to save rocket weight, which means more payload weight.

Click for larger graphic

Click for larger graphic

Rocket Lab is bringing it to launch for under $350 million, a fraction of the billions most spend.

Click for larger graphic

Click for larger graphic

After 2025’s test launch, they expect three commercial launches in 2026 and five in 2027. SpaceX is booking 70% gross margins on Falcon 9 launches.

The Space Systems satellite backlog is up to $720 million:

Click for larger graphic

Click for larger graphic

Once Neutron is on the launch pad, R&D will fall sharply and create an inflection point for earnings. Until then, they can report increasing revenues and improving gross margins, including in the coming December quarter report.

Click for larger graphic

Click for larger graphic

RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Click for larger graphic h/t @Biotech2k1

Click for larger graphic h/t @Biotech2k1

AbCellera Biologics (ABCL- $2.88) canceled their presentation at the JPMorgan conference, which is a shame. They could have talked up their just expanded collaboration with AbbVie to include the discovery of T-cell engagers (TCE) in oncology.

CD3 T-cell engagers have the potential to be a cornerstone of cancer treatment. They guide the immune system to find and eliminate cancer cells by binding tumor targets and the CD3 protein on cancer-killing T cells at the same time. The development of T-cell engagers has been limited due to challenges with efficacy and safety. AbCellera developed a T-cell engager platform that includes novel CD3-binding antibodies to expand the therapeutic window and co-stimulatory building blocks to enhance efficacy for difficult-to-treat cancers. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $1.93) announced that they signed a Vafseo supply contract with Fresenius Kidney Care and now have nearly 100% coverage of dialysis providers. Vafseo started shipping on January 9.

They also got guidance from the FDA on their Phase 3 label expansion trial for late-stage chronic kidney disease patients not yet on dialysis. They’ll begin the trial in 1,500 patients in mid-2025. This is about a $3 billion market and dialysis is about a $1 billion market. Can you say “blockbuster?”

CEO John Butler presented at the JPMorgan conference (AUDIO & SLIDES HERE). As we know, the current standard of care for patients on dialysis – erythropoietin-stimulating agents (ESAs) – has remained unchanged for 30 years. Nearly 25% of dialysis patients with anemia due to chronic kidney disease (CKD) fall below target hemoglobin levels. Patients who don’t respond well to ESAs (about 20% of the patients on dialysis) have higher rates of hospitalization and higher one year mortality.

The risk of a major adverse cardiac event (MACE) increases as the dose of an ESA increases. And, of course, ESAs are a sub-optimal approach for home dialysis patients because they need to be injected subcutaneously or intravenously. In Akebia market research, more than two out of three nephrologists identified an unmet need for the treatment of anemia due to the CKD. They’re looking for treatment with good efficacy, oral administration, and efficacy for ESA treatment-resistant patients. They’re looking for Vafseo.

Click for larger graphic

Click for larger graphic

John said they have enough cash for at least two years, and I think Vafseo profits will mean they never have to sell equity again. Buy AKBA up to $2 for the Vafseo launches in the EU, UK, and US.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

set Probable time of next approval: NM

Probable time of next financing: Never

Compass Pathways (CMPS – $3.43) did an earlier than expected $150 million offering of stock and warrants. The warrants exercise at $5.796 and will bring in another $353 million. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2027

Probable time of next financing: Late 2025

Editas Medicine (EDIT – $1.22) presented at the JPMorgan conference (AUDIO HERE and SLIDES HERE). CEO Gilmore O’Neill said there are a number of challenges to gene therapy and gene editing including recent slow launches into low total addressable markets, high cost of goods with low profit margins, highly complex patient journeys, and launches into competitive indications with very high standards of care. Editas has the solution:

Click for larger graphic

Click for larger graphic

Editas uses gene upregulation instead of gene knockdown or correction. The reni-cel program proved upregulation works.

Click for larger graphic

Click for larger graphic

Editas has a cash runway into the June 2027 quarter. In addition, there are over 100 clinical-stage programs in development that will require an IP license from EDIT for use of CRISPR Cas9 and Cas12a. Also, Editas’ oncology partners – Bristol Myers Squibb, Immatics, and Shoreline Biosciences – will report clinical milestones in the next 12-18 months.

Their 2025 milestones are:

Click for larger graphic

Longer-term, they plan to:

Click for larger graphic

Editas is an investment based on two forecasts. First, I believe in vivo upregulation is a good way to do gene editing. Second, I believe their foundational patents will allow them to fund the company without dilution. If you don’t think both of those beliefs are accurate, don’t buy this stock. Otherwise, EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2026

Probable time of next financing: 2026 or never

Inovio (INO – $1.88) said their 2025 milestones include resolving the Cellectra manufacturing issue by the end of February, starting and completing a 100-patient confirmatory trial of INO-3107 at 20 centers, and submitting the Biologics Licensing Application by midyear. They also will present and publish recently announced durability and immunology data, as well as the full efficacy and tolerability data from their completed Phase 1/2 clinical trial, in a peer-reviewed scientific journal.

Their all-new Corporate Presentation shows their longer-term plan:

Click for larger graphic

Click for larger graphic

INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Early 2026

Probable time of next financing:After FDA approval in 2026

Medicenna (MDNAF – $0.99) also posted a new Corporate Presentation.

Click for larger graphic

Click for larger graphic

MDNA-11 plus Merck’s Keytruda looks like an easy winner in both the clinic and the market.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

Medicenna has several milestones and events coming this year to drive the stock higher. And there’s always the possible bluebird of a partner for MDNA-55.

Click for larger graphic

Click for larger graphic

Buy MDNAF under $3 for a first target of $20.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

TG Therapeutics (TGTX – $29.89) presented at JPMorgan (AUDIO HERE and SLIDES HERE). CEO Mike Weiss was in fine form, basically teasing the analysts and portfolio managers for missing the anti-CD20 drugs story. There are three approved drugs – Ocrevus, Kesimpta, and Briumvi – with no additional ones expected. Those three already have half of the multiple sclerosis market with $8 billion in sales, growing to $12 billion over the next five years.

Click for larger graphic

Click for larger graphic

Briumvi, which has patent protection to 2042, has several advantages. It takes only a one hour infusion twice a year following the starting dose, and Mike thinks they can get that down to 30 minutes. It is the only anti-CD20 therapy that showed less than 0.1 annualized relapse rate in two Phase 3 trials. The latest five-year long-term data shows an ARR of 0.020 – that means a patient might have one recurring MS attack every 50 years.

Importantly, the Briumvi label does not include a risk of breast cancer – 80% of MS patients are women. Finally, TG decided to price Briumvi below the other two anti-CD20 drugs. The insurers love them. Mike revealed fourth quarter revenues of $103.6 million, bringing them in at $310 million for the year – $60 million above the consensus estimate at the beginning of 2024.

Click for larger graphic

Click for larger graphic

TG expects to start a pivotal trial of every-other-month subcutaneous Briumvi in mid-2025. It would be done at home by the patient – no doctor visit required.

For 2025, Mike guided for US revenues of $525 million, plus international revenues of $15 million, with $300 million of operating expenses. They ended 2024 with $310 million in cash and will not need to raise equity. Hold TGTX for a target price in a buyout of $40 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,746.00) is up more than 100% since 2009, while junior gold mining stocks are down 56%. Since December 2009, the SPDR Gold Trust ETF (GLD) that tracks the price of the metal is up more than 100%. The VanEck Vectors Gold Miner ETF (GDX) is down 22% and the VanEck Junior Gold Miners ETF (GDXJ) is down 56%. Much of this underperformance has happened during the recent rally. I think gold miners are about to catch up in 2025, with the juniors outperforming the majors and silver outperforming gold.

And that’s in a context of gold continuing to rise. I agree with Michael Howell, the liquidity king, who says the global debt spiral will drive up gold, bitcoin, and yields (driving down bonds).

He thinks China will devalue the yuan against gold, pushing up the price of gold by about 30%. The fractal dimension continues to move towards full consolidation.

Miners & Related

Coeur Mining (CDE – $6.40) presented at the TD Securities Global Mining Conference. Although we are not blessed by a replay, possibly in violation of SEC Regulation FD, they did post the SLIDES HERE. They focused on the impact of the SilverCrest acquisition:

Click for larger graphic

Compared to their peer silver miners – First Majestic, Hecla, Silvercorp, Endeavour Silver, and MAG Silver, Coeur now has the most silver production, the largest market capitalization for institutional ownership, the highest EBITDA (earnings before interest, taxes, depreciation and amortization) thanks to lower costs and higher profit margins, and the highest free cash flow. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $5.70) shareholders approved the Gatos Silver acquisition with 98.44% voting yes. Gatos shareholders also approved with 71.3% voting yes. The deal closed today. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.75) is my favorite way to benefit from rising gold prices without concentrated mining risk. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $99,890.36) bounced back from the prior week’s drop to a two-month low and is knock, knock, knocking on the $100,000 door again. Is this the bust-through moment? Don’t know, don’t care. It’s going to happen, possibly very early in the Trump Administration, and I still think we hit $150,000 or more this year.

After last Friday’s drop caused by the strong payrolls report, Piotr Matys, a senior FX analyst at InTouch Capital Markets if he still has a job, said a head and shoulders chart pattern may have now formed for bitcoin, which indicates a trend reversal from bullish to bearish territory. Since $91,600 was viewed as a major support level, the token’s breach below that point now points to a “strong technical bearish signal for bitcoin.”

Matys said bitcoin’s next low may come around the $88,000 mark if bearish sentiment wins out, with a quick pullback from there to around $74,000 also possible.

Ignoring Piotr, Microstrategy bought bitcoin for the 10th consecutive week, this time picking up 2,530 coins at an average price of approximately $95,972 for a total of $243 million. The company now owns about $41 billion worth of bitcoin, 2% of all the coins that will ever exist.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $56.71) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Ethereum Trust (ETHA- $25.39) remains the cheapest and easiest way to buy etherum. ETHA is a Buy.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $78.64

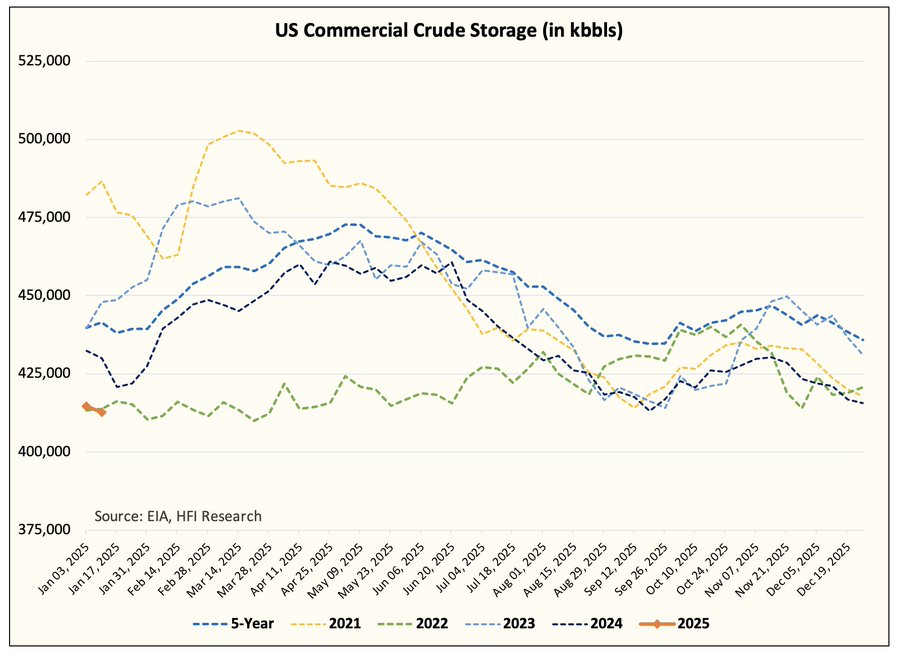

Oil closed over $80 on Wednesday at a five-month high due to (1) fresh sanctions on Russian tankers, leading to (2) continued panic in the physical market from Chinese oil traders replacing sanctioned barrels from Russia and Iran with alternatives, and (3) continued inventory draws in the US with commercial crude storage sitting near multi-year lows, due to (4) weak US oil production. Did I miss anything? Oh, yeah, OPEC+ is holding firm.

Because of the visibility of the Russian tankers, it will take time before they go offline, conduct ship-to-ship transfers, and offload the crude. Meanwhile, last week saw a 1.962 million barrel crude oil storage drawdown, the 8th straight week. US commercial crude storage is starting the year near the multi-year lows.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

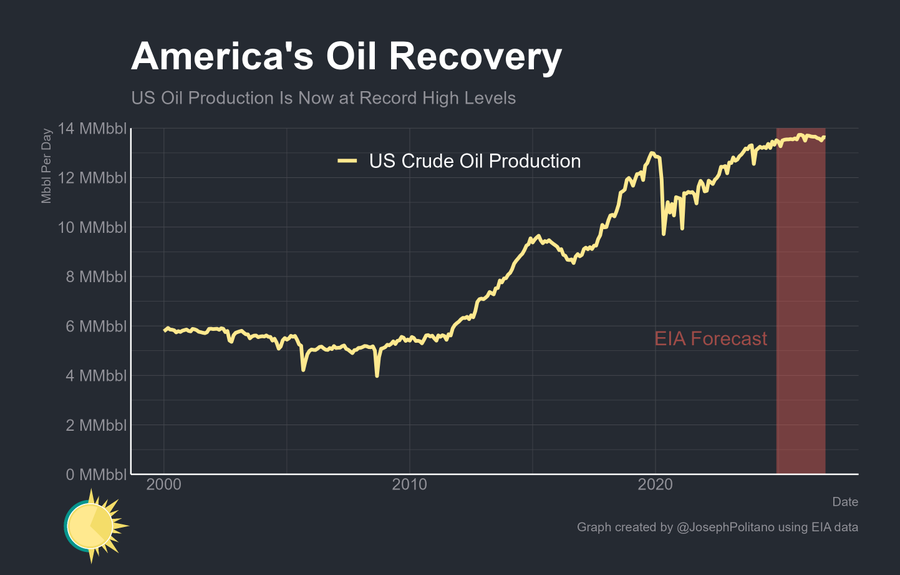

The new Energy Information Administration (EIA) update of its short-term projections through 2026 was true to its bias, still projecting a massive surplus for 2025. The EIA projects US crude oil production will inch to new record highs through 2025, before declining ever so slightly in 2026. I project that 2025 production will be below 2024, and 2026 will be below 2025.

Click for larger graphic h/t @JosephPolitano

Click for larger graphic h/t @JosephPolitano

The drop in US oil production that has already occurred will on its own eliminate one million barrels a day of surplus for January. Meanwhile, colder than normal weather will boost heating-related demand by 0.5 to 0.75 million barrels a day. In total, the data relative to the consensus estimate is lower by 1.5 to 1.75 million barrels a day. As a result, there is almost no plausible scenario right now that the IEA will be correct about a surplus in March quarter balances. The fact that it is still projecting that much of a surplus just illustrates how delusional they are.

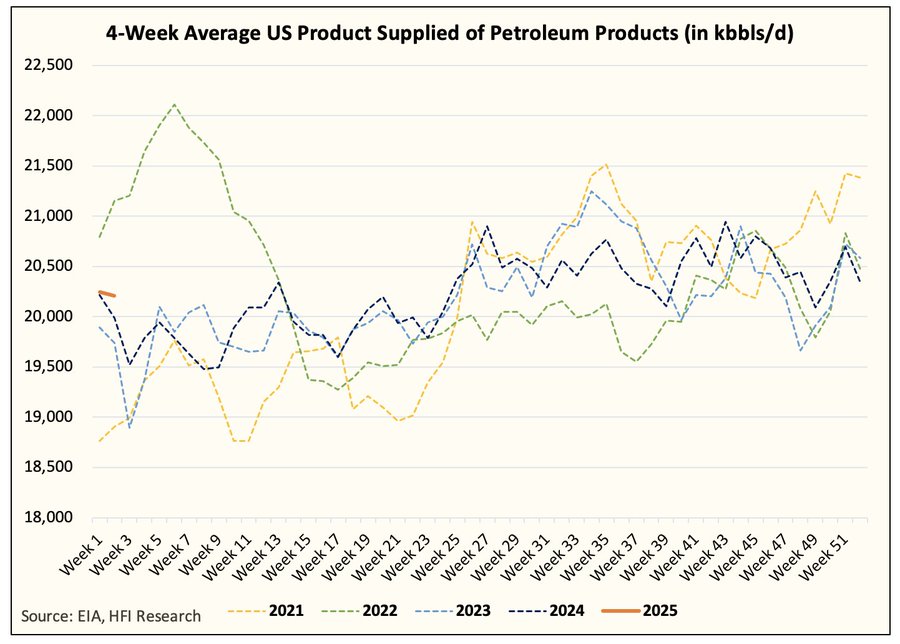

At the same time, US oil demand is starting 2025 off better than 2023 and 2024. Colder than normal weather in January should keep oil demand elevated.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

Persistent bearishness in the paper oil market due to the surplus expected in 2025 will meet reality soon. With US oil production disappointing to the downside, oil market balances will be closer to neutral for the March quarter versus the +1.4 million barrels a day expected by the market. US oil inventories will fail to build in the March quarter, the market will change its tone rapidly, and oil prices will re-rate to a range from the high $70s to the low $80s.

One caution as a reminder for those that don’t remember the 2018 Trump tweeting oil debacle. We all are one tweet away from a $2-$3 transient drop in crude prices. Keep a little dry powder to take advantage of it.

The July 2026 Crude Oil Futures (CLN26.NYM – $68.57) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $39.98) is a Buy under $40 for a $100+ target.

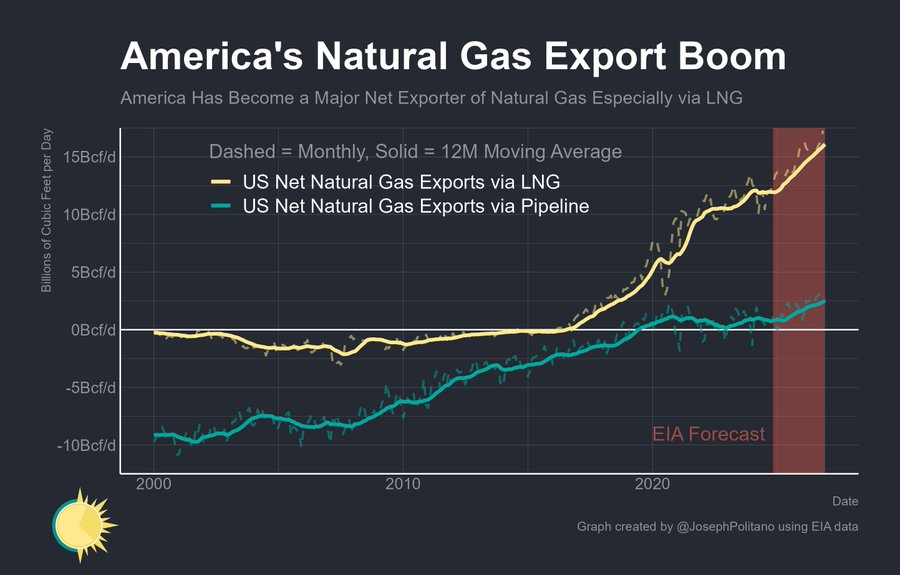

EQT (EQT – $53.46) will benefit from a surge in LNG exports. The rate at which European inventories have been depleted this winter is significantly higher than the same period last year, with an average daily withdrawal of approximately 350,000,000 cubic meters per day, compared to 220,000,000 cubic meters per day last year. EU storage is 64% full, a 15% decrease compared to last year. European gas inventories are likely to conclude the winter season only 34% full. To meet the European Union’s 90% storage fill target before the start of the next winter season in October, Europe will need to import around 30% more LNG on an annualized basis.

The EIA also projects that US net natural gas production will increase 1.3% in 2025 and 2.7% in 2026. Exports will rise to record highs in 2025 and 2026 as additional liquefied natural gas (LNG) export terminals come online. I agree, and EQT will benefit.

Click for larger graphic h/t @JosephPolitano

The natural gas market tends to move to extremes. The most recent weather updates show higher cold intensity in the 6 to 10 day range. This has pushed higher storage withdrawal estimates, which is what’s causing natural gas prices to rally. I think it’s time to temper near-term expectations a bit. Although the latest weather model update shows severe cold on the horizon, the duration is short, and the impact to storage, while large, is still not enough to severely push storage to a material deficit. We may step aside on EQT in the $50s and reenter in the fall. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Freeport McMoRan (FCX – $39.88) reports December quarter earnings next Thursday morning. The consensus expects revenues barely up from last year to $5.95 billion with earnings down from 27¢ last year to 22¢. Guidance for the March quarter should be $6.45 billion and 39¢.

Freeport may issue full-year guidance. Analysts expect 2025 revenue growth of 4.45% to $26.94 billion with earnings up from $1.40 to $1.94. I expect $5 a pound copper in 2025. which would generate over $30 billion in sales and around $2.75 a share. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

RIP Sam Moore

* * * * *

Your reading the FTC on investment newsletter promotion Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 1/16/25. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $48.86 – Buy under $33, target price $60

Gilead Sciences (GILD – $92.33) – Buy under $90, first target price $120

Micron Technology (MU – $103.77) – Buy under $102, first target price $140

Onsemi (ON – $54.13) – Buy under $60, first target price $100

Palantir (PLTR – $70.78) – Buy under $22, target price $100+

PayPal (PYPL – $90.16) – Buy under $68, target price $136

Snap (SNAP – $11.35) – Buy under $11, target price $17+

SoftBank (SFTBY – $29.45) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $11.32) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $64.93) – Buy under $60; 3- to 5-year hold

Fastly (FSLY – $9.60) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $18.61) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $9.09) – Buy under $10, target price $40

Rocket Lab (RKLB – $24.60) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $2.88) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.93) – Buy under $2, target $20

Compass Pathways (CMPS – $3.43) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $1.22) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $1.88) – Buy under $14, hold a long time

Medicenna (MDNAF – $0.99) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.16) – Buy under $3, target price $20, then $50

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($31.81) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $29.65) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $36.13) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $25.20) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $33.33) – Buy under $30, target price $50

Coeur Mining (CDE – $6.40) – Buy under $5, target price $20

Dakota Gold (DC – $2.29) – Buy under $2.50, target price $6

First Majestic Mining (AG – $5.70) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.36) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.75) – Buy under $10, target price $25

Sprott Inc. (SII – $42.13) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $99,890.36) – Buy

iShares Bitcoin Trust (IBIT – $56.71) – Buy

Ethereum (ETH-USD – $3,347.39)– Buy

iShares Ethereum Trust (ETHA- $25.39) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $68.57 ) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $39.98) – Buy under $40; $100+ target

Vermilion Energy (VET – $10.15) – Buy under $11; $24 target

Energy Fuels (UUUU – $5.01) – Buy under $8; $30 target

EQT (EQT – $53.46) – Buy under $35; $70 first target

Freeport McMoRan (FCX – $39.88) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $230.03) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $611.84) – Expect to move back to Buy

TG Therapeutics (TGTX – $29.89) – Hold for buyout at $40+

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2025

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First

AKBA moved nice off their low of $1.75 earlier this week. Good volume on Friday. Now we watch the weekly script numbers. I’m in.

MM….please add silver fractals on a regular weekly basis. Silver informs on many fronts. In addition it seems we are nearing a major inflection point and its lag vs gold could be dramatically repriced.

Thanks,

The debt to GDP ratio is 120 percent or more by now. Anyone with a 3rd grade education (except politicians) can figure out that the US government is in debt to the tune of 120

percent of the entire gross domestic product of the United States. We are now finally at a point where politicians can no longer kick the can down the road. The added burden of the interest on the debt will increase exponentially with every passing of 100 days. We are now that ordinary Joe who has 100,000 racked up on his credit cards at 28 percent interest who can only make the minimum payment. His debt and our debt is unsustainable. Washington state just came out with their budget forecast. They have billions and billions of dollars of shortfall. Yet there is NO mention of spending cuts. Just added taxes to implement. DUH!! Today is just a preview of coming attractions! Excellent RR , MM.

when did we stop fallowing Monero XMR i still hold it @ app $30 its over $200 not much compared to BTC move in the same time as I recall it was app10k

Among the Executive Orders signed by President Trump yesterday was a revocation of dozens of Biden’s Executive Order s including Executive Order 14087 of October 14, 2022 (Lowering Prescription Drug Costs for Americans).

https://thehill.com/policy/healthcare/5098715-trump-executive-order-biden-prescription-drug-costs/

I can’t understand how the revocation is good for Americans and would appreciate any comments on how the revocation of that Order helps our country. Anyone? Bueller?

If you read the article the findings of this study were published in 2023, the title is very deceiving. The order Biden signed in 2022 was basically a study looking at options to help lower cost, not actually lowering cost. I would assume there is nothing more to do with the study since the findings were published in 2023 and probably the Government still had taxpayer funds allocated to this. Thankfully we now have accountability and transparency with DOGE that are acting on behalf of all the US taxpayers.

Last one out shut the lights. i am done. SCYX same stock response every week as we watch it sink. AKBA, and we won’t talk about all the 99% losers.

Haven’t heard from you lately JGMD, all good are you ok

I’ve been spending more time on Stocktwits following AKBA. Follow buythehornz127, hsainu, Acemaker12, as well as me, viber7. AKBA zoomed up to $2.37 two days ago after the upgrade in price target to $10 by an analyst, recovered from $2.30 to $2.39 yesterday, and so far today, recovered from $2.27 to $2.37 now. I hope you got a position at recent lower prices. It’s funny how MM is relatively conservative with his PT of $5 this year, when he is usually wildly bullish on most NWI stocks which have been disasters. MM is also conservative on TGTX getting a buyout over $40, whereas many Yahoo Finance posters expect $75 to even $200. I am not looking to buy more TGTX at current prices, but I will add even more AKBA if sales growth is delayed. I believe AKBA is the best opportunity with minimal risk.

Glad you are good and yes I am in akba, I am wondering why MM hasn’t raised the buy in price higher on akba with there outlook,maybe tonight,so much potential

I am fully invested also. Looking forward to the weekly script numbers.

New World Investor for 1.23.25 is posted.