Dear New World Investor:

The headline October Consumer Price Index showed prices fell 0.04% over September – deflation! – and rose 3.2% over last year. Both were slower than September’s 0.4% monthly and 3.7% annual increase, and below the consensus expectation for 0.1% and 3.3%.

The core CPI rose 0.23% monthly and 4.0% yearly, the smallest annual increase in two years. Both were below September’s CPI and consensus expectations. The shelter index, which lags reality by six to nine months, rose 6.7% on an annual basis, the slowest in a year. It was the largest factor in the monthly increase in core inflation, increasing 0.3% month-over-month, but still slower than September’s 0.6% monthly jump.

And we know we can trust the numbers. The government says Health Insurance fell 34% from last year to account for only 0.525% of people’s budgets. Hmm…

Stocks soared as Treasury bonds climbed. The Fed is done raising rates but will hold them at these high levels for a year or two to let inflation cool. I think oil prices are headed much higher, but declines in the lagging shelter component will easily offset that. As Chairman Powell said: “Slowing down is giving us, I think, a better sense of how much more we need to do, if we need to do more.”

As M2 sinks, so will inflation The chart below shows CPI is headed a lot lower:

Click for larger graphic h/t @menlobear

Click for larger graphic h/t @menlobear

Oxford Economics economist Michael Pearce summed it up well: “There are signs that services inflation will prove sticky, reflecting tight labor market conditions, with the prospect of a return to the 2% target still some way off. Overall the October CPI report gives Fed officials more confidence that inflation is on a firm downward trajectory, which should stay their hand on any additional rate hikes. However, the disinflation process still has some way to go, and the path to weaker services inflation depends on a continued cooling in labor market conditions, so it will still be a long time before the Fed is able to think about lowering interest rates.”

Others are belatedly turning bullish. The latest BofA institutional survey showed fund managers are now overweight equities for the first time since April 2022, and 65% see bond yields falling in 2024, the highest percentage ever.

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

Market Outlook

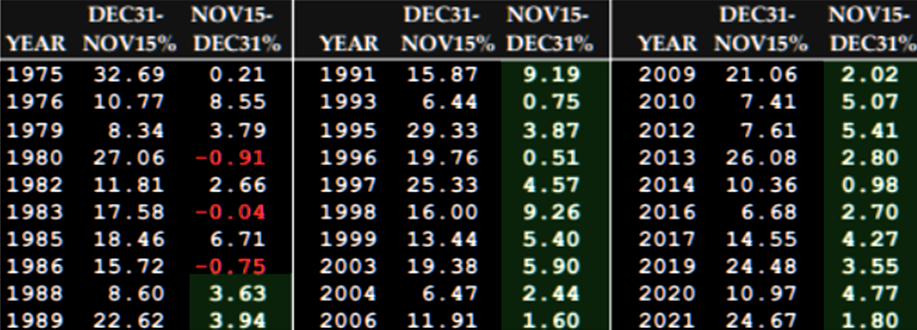

The S&P 500 added 3.7% since last Thursday as seasonality kicked in. The Index is up 17.4% year-to-date. The last 22 years that the Index was up over 5% by this time of the year, the remainder of the year was positive EVERY year. For the past 30 years the set-up was 27 positive years versus 3 negative.

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

And seasonal factors are strong, although we may be front-running them.

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

The Nasdaq Composite gained 4.4% and exited correction territory. It is up 34.8% for the year. The small-cap Russell 2000 jumped 5.1% with its best day in more than a year on Tuesday. It now is just barely up 0.7% in 2023. Last week, the Russell had its worst week versus the S&P 500 since March 2021.

The fractal dimension is dipping towards an uptrend signal, but we’ve seen these turn into headfakes before. Only a drop through the 55 level can signal a real new trend.

Top 5

Changes this week: None

Near-Term – chronological order

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

SFTBY SoftBank – for ARM IPO valuation

AKBA Akebia – Vadadustat approval March 27, 2024; TDAPA approval October

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model estimate for December quarter real GDP growth increased slightly to +2.2 due to upward revisions in personal consumption expenditures growth and gross private domestic investment growth. That’s more than double the Blue Chip consensus.

Click for larger graphic

Click for larger graphic

I still think the December quarter is the last hurrah, but my belief that the first two or three quarters of 2024 will show real GDP declines in a mild recession is dramatically different from the consensus estimate:

Click for larger graphic

Click for larger graphic

If I’m right, stocks may sell off on recession fears or may go up on hopes the Fed will cut interest rates sooner rather than later (they won’t). We’ll take advantage of the move either way.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, November 17

SAND- SandStorm – 11:30am – Earnings conference call

MDNA – Medicenna – 9:30pm – Society for Neuro-Oncology annual meeting

Thursday, November 23

HAPPY THANKSGIVING!

AG – First Majestic – Through 11/25 – Deutsche Goldmesse, Frankfurt

Friday, November 24

Market Closes Early – 1:00pm

Short Interest – After the early close

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $189.71) extended free access to Emergency SOS via satellite for another year for existing iPhone 14 and 15 users. They said: “Emergency SOS via satellite has helped save lives around the world. From a man who was rescued after his car plummeted over a 400-foot cliff in Los Angeles, to lost hikers found in the Apennine Mountains in Italy, we continue to hear stories of our customers being able to connect with emergency responders when they otherwise wouldn’t have been able to.”

Apple is building on this satellite infrastructure, with Roadside Assistance via satellite to connect users to AAA if they have car trouble while outside of cellular and Wi-Fi coverage. Crash Detection can detect a severe car crash and automatically dial emergency services if a user is unconscious or unable to reach their iPhone – how cool is that? Users can open the Find My app and share their location via satellite to reassure friends and family of their whereabouts while traveling off the grid. Check In allows users to automatically notify friends and family when they have made it to their destination safely. Users can set up their Medical ID in the Health app to help first responders access critical medical information from the Lock Screen without needing a passcode.

All of a sudden, an iPhone 15 looks like an awfully good holiday present to keep your kids and grandkids safe. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $74.52) presented at the Jefferies London Healthcare Conference (VIDEO HERE). The CFO said the last three years were about investment as they raised R&D spending to be more in line with industry norms. 2024 is the first big payoff year with many clinical results, including Phase 3s. They expect a “significant” acceleration in revenue growth over the coming years as the clinical catalysts play out.

Biktarvy is now a $12 billion a year drug and growing, used in 62% of naive HIV patients. Prevention is growing much faster and they will get Phase 3 results in 2024 on lenacapavir, their once-every-six-months injection. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $334.19) rolled out a new feature that will allow users to link their Facebook and Instagram accounts to Amazon, so that they can buy products directly from promotions on the social media apps. Customers will be able to shop Amazon’s Facebook and Instagram ads and check out with Amazon without leaving the social media apps. Customers in the US will see real-time pricing, Prime eligibility, delivery estimates, and product details on the Amazon product ads in Facebook and Instagram.

This feature will improve targeted ads and could be a massive revenue opportunity for both companies. Citi wrote: “For Meta, we believe the partnership can deliver closed loop attribution of ads as Social increasingly becomes a larger product discovery channel. This partnership can deliver incremental sales and we reiterate Buy ratings on top picks META & AMZN.”

META is a Buy under $150 for a $400 target in 2024.

The SoftBank (SFTBY – $20.05) September quarter transcript finally is up HERE. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $11.37) filed a prospectus related to the proposed resale of 5.92 million shares by selling shareholders, not by the company. This is not an immediate offering, but some of these shares probably will be sold from time to time. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $16.25) presented at the RBC Capital Markets 2023 Technology, Internet, Media and Telecommunications Conference (AUDIO HERE and TRANSCRIPT HERE) and the D.A. Davidson Technology Summit (AUDIO HERE).

CEO Todd Nightingale said: “Traditionally, Fastly has delivered technology for content delivery, content delivery networks. But in the past few years, that offering has been expanded and really the market moving forward is about Edge Cloud services. And what that means is that for people who are delivering web experiences, whether that’s applications or Web sites or streaming services, they leverage our technology at the edge to make that user experience great. That’s our differentiation. We focus on delivering the best end user experience. We partner with our customers to deliver that experience on their behalf, and we like to say that we make the Internet a better place for all experiences are fast, safe, and engaging. That’s what Fastly does. We do that largely in the area of content delivery, of security, of edge compute and edge observability…the leaders in that space tend to be ourselves, Akamai and CloudFlare. Akamai comes from a traditional CDN space. We come from a next gen performance CDN space and CloudFlare comes from a security space.”

CFO Ron Kisling said: “At the Investor Day, we shared that we expected to be cash flow breakeven in 2024…we grew from enterprise basis early on, particularly in streaming and publishing, that tends to have a concentration of traffic usually in the evenings. As we expand our presence in other verticals that have different time sequences, such as tech or travel where most of that traffic’s in the middle of the day, we’re using underutilized traffic, underutilized hardware, and margins on that business are dramatically higher. And so by balancing out the verticals, we can see a significant contribution to margins as well.”

FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

QuickLogic (QUIK – $10.30) reported September quarter revenues up 91.4% – not a misprint – from last year to $6.7 million with record pro forma earnings of 13¢ per share compared to a seven-cent loss last year. The two publishing analysts were expecting $6.5 million and 13¢. New product revenue was approximately $6.1 million, an increase of $3.9 million, or 173%, sequentially from the June quarter.

On the conference call (TRANSCRIPT HERE or if you hit the Premium paywall, go to

https://www.removepaywall.com), CEO Brian Faith said a significant contribution from the $15 million second phase of the large government contract for Strategic Radiation Hardened FPGA Technology contributed to the increase in third quarter revenue. The total awarded so far to $22 million. The contract has the potential to extend through 2026 with a total potential value of $72 million.

Their sales funnel grew to a record $162 million and accelerated conversions from funnel opportunities contributed to new bookings during the third quarter. For the December quarter, they guided for record revenues of $7.4 million ±10% with pro forma earnings of 10¢ to 14¢ a share. They reaffirmed 2023 guidance for full year revenue growth of 30% and full year non-GAAP profitability of 8¢ to 12¢.

Brian said: “We believe this customer could represent tens of millions of dollars of potential device revenues starting in a couple of years. …Furthermore, we announced the availability of our eFPGA IP on the Global Foundries 12LP process technology and we now have multiple new opportunities for this IP, totaling several million dollars …Customers are increasingly seeing QuickLogic as the lowest risk path to a solution that meets their technical requirements, development schedule and target costs. The not-so-subtle point here is by lowering risk and shortening time to market, we save our customers’ money and that provides us with a meaningful competitive advantage.

“The primary drivers for our growth over the last 3 years have been development contracts. Looking forward, we believe these will lead to production devices and new opportunities even beyond our sales funnel of $162 million…While we will provide our full year outlook for 2024 during our year-end conference call, I believe we are well positioned to grow total revenue by over 30% and report very solid non-GAAP earnings per share with each quarter contributing to the profitability in 2024. Following the investments we are making during the second half of 2023 to support anticipated growth in 2024, we expect to generate positive cash flow for the full year 2024.”

They finished the quarter with $18.6 million in cash. QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets and wearables.

Primary Risk: New sensor hub competitor emerges.

Rocket Lab USA (RKLB – $4.22) presented on “The Launch Shortage” panel at the Deutsche Bank Space Summit (AUDIO HERE). Panelists were the CEO of Firefly Aerospace and the CFOs of Isar Aerospace, Relativity Space, and Rocket Lab. It was an interesting survey of the launch business and made it obvious how far ahead RKLB really is.

The company is developing two spacecraft to enable NASA’s ESCAPADE mission to Mars orbit to study the planet’s magnetosphere. Named Blue & Gold, the twin spacecraft will spend 11 months in interplanetary space before entering a highly elliptical orbit around Mars. They will spend six months gradually descending into the same nominal science orbit, passing within 100 miles (160 km) of the Martian surface at closest approach

On board: a Floating Potential Probe, Planar Ion Probe, and Electrostatic Analyzer, integrated by Rocket Lab. The golden sphere-on-a-stick is the Floating Potential Probe. It measures how electrically charged the spacecraft gets (positively or negatively).

Click for larger graphic

Click for larger graphic

The flat golden square is the Planar Ion Probe, which can measure both solar extreme ultraviolet irradiance and low energy ion density at low altitudes under 300 miles (500 km).

Click for larger graphic

Click for larger graphic

Launch is scheduled in 2024. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $1.06) sold a Sapphire XC printer to Valiant Products, a contract manufacturer serving major industries from medical to outer space. Valiant plans to upgrade its new printer to a Sapphire XC 1MZ, which is capable of producing parts up to one-meter-tall. They purchased the printer after a mutual aerospace customer sought to leverage Velo3D’s additive manufacturing technology in its supply chain to produce components for its rocket engines.

The stock was down 24.8% today after they filed an 8-K saying that approximately $200,000 of revenues previously reported in the Earnings 8-K should have been deferred. As a result, they will not satisfy the minimum revenue covenant for the quarter ended September 30 in the their senior secured convertible notes due 2026. If the holders don’t waive the covenant (Hint: They will), it would result in an event of default under the notes and allow the holders to declare the notes due and payable in cash. So Velo3D will have to present the debt as current on the consolidated balance sheet, which will require the boilerplate disclosure that the company has substantial doubt about its ability to continue as a going concern.

Of course, VLD has been negotiating a proposed amendment to the notes with the holders, which I am sure will be successful. Take advantage of today’s dip and Buy VLD up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Compass Pathways (CMPS – $5.66) initiated the UK component of their global Phase 3 trial of COMP-360 psilocybin treatment for treatment-resistant depression after the Medicines and Healthcare Regulatory Agency approved the trial.

UK sites will include the newly-opened Centre for Mental Health Research and Innovation in London, developed by Compass in partnership with South London and Maudsley NHS Foundation Trust and the Institute of Psychiatry, Psychology & Neuroscience at King’s College, London . CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Medicenna (MDNAF – $0.36) reported a September quarter loss of $3.7 million or five cents a share.

Tomorrow, at the Society for Neuro-Oncology annual meeting, they will report four-year follow-up survival data from the Phase 2b bizaxofusp (MDNA55) trial in patients with recurrent glioblastoma, a uniformly fatal form of brain cancer. This may finally get them a Phase 3 partner. Bizaxofusp has been granted Fast Track status by the FDA and Orphan Drug status by both the the FDA and EMA.

Before the end of 2023, they will start the combination portion of the ABILITY-1 study evaluating MDNA11 with Keytruda. We’ll see data from both the monotherapy and combination arms during the first half of 2024. It has Best in Class potential:

Click for larger graphic

Click for larger graphic

They have a deep pipeline:

Click for larger graphic

Click for larger graphic

They finished the quarter with $25.7 million in cash, and their cash runway now extends through multiple data readouts in mid-2024 and into the first quarter of 2025. With about 70 million shares outstanding, the stock finished today with a $25.2 million market capitalization – less than cash! Buy MDNAF under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

ScyNexis (SCYX – $1.58) reported a September quarter loss of $1.8 million or four cents per share, also with no conference call.

In an SEC filing, they said it was Glaxo SmithKline that discovered the potential contamination problem: “Following a recent review by GSK of the manufacturing process and equipment at the vendor that manufactures the ibrexafungerp drug substance, the Company became aware that a non-antibacterial beta-lactam drug substance was manufactured using equipment common to the manufacturing process for ibrexafungerp.

“Current FDA draft guidance recommends segregating the manufacture of non-antibacterial beta-lactam compounds from other compounds since beta-lactam compounds have the potential to act as sensitizing agents that may trigger hypersensitivity or an allergic reaction in some people. In the absence of the recommended segregation, there is a risk of cross contamination.

“It is not known whether any ibrexafungerp has been contaminated with a beta-lactam compound and the Company has not received reports of any adverse events due to the possible beta-lactam cross contamination. Nonetheless, out of an abundance of caution and in line with GSK’s recommendation, the Company has recalled BREXAFEMME® (ibrexafungerp tablets) from the market and placed a temporary hold on clinical studies of ibrexafungerp, including the Phase 3 MARIO study, until a mitigation strategy is determined.”

In the earning release they said: “While options for resolution of these issues are being evaluated we continue making progress towards data analysis for recently completed clinical studies (FURI, CARES, SCYNERGIA and VANQUISH).”

They finished the quarter with $105.2 million in cash, giving them a cash runway of more than two years. With about 28 million shares outstanding, the stock finished today with a $44 million market capitalization – less than half their cash with a $500 million deal in place with GSK! That’s nuts. Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2023/2024

Probable time of next financing: Never

Inflation MegaShift

Gold ($1,984.00) started the week at $1,939.90, near its low, and finished at $1,984.00, near its high, after spending most of the week within spitting distance of the $1,950 tractor beam. It has to break away from that to mount a real rally. The fractal dimension continues to show the obvious almost year-long consolidation.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $35,920.01) went to an 18-month high just under $38,000 this morning as the “Here comes spot ETFs” rally continued, but fell sharply in the afternoon. But the SEC delayed a decision on a filing from Hashdex to convert its existing Bitcoin futures ETF into a spot fund to 2024, a move they have already done for all the other ETF hopefuls, and bitcoin fell sharply today.

I noticed that BlackRock said the USDT and USDC stablecoins pose risks to bitcoin. I’m no fan of Larry Fink or BlackRock, but they’re absolutely right. Circle’s USDC and Tether’s USDT are both dangerous products without proper Know Your Customer and Anti-Money Laundering (KYC/AML) in place, as shown by the number of Hamas and cartel accounts. Tether is a total fraud propping up bitcoin, and I worry that the SEC will shut it down before they approve a spot exchange-traded fund, causing a rapid drop in bitcoin’s price.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $28.99) remains a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $1,960.41)slipped back under $2,000. The SEC also delayed action on Grayscale’s attempt to launch a new Ether futures ETF as BlackRock filed today for a spot ethereum exchange-traded fund. The dam will burst in early 2024. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

Commodities

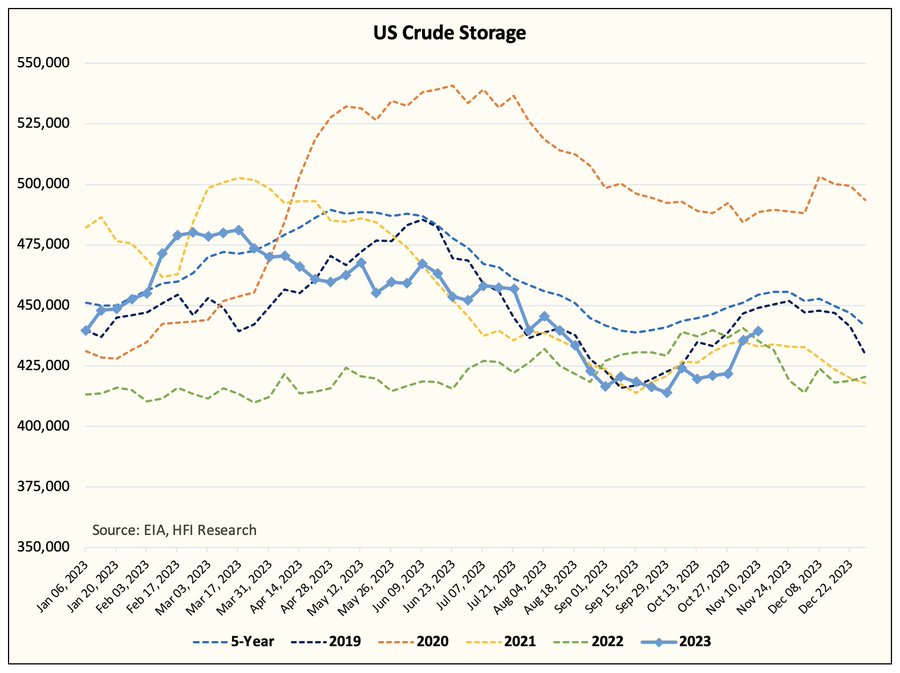

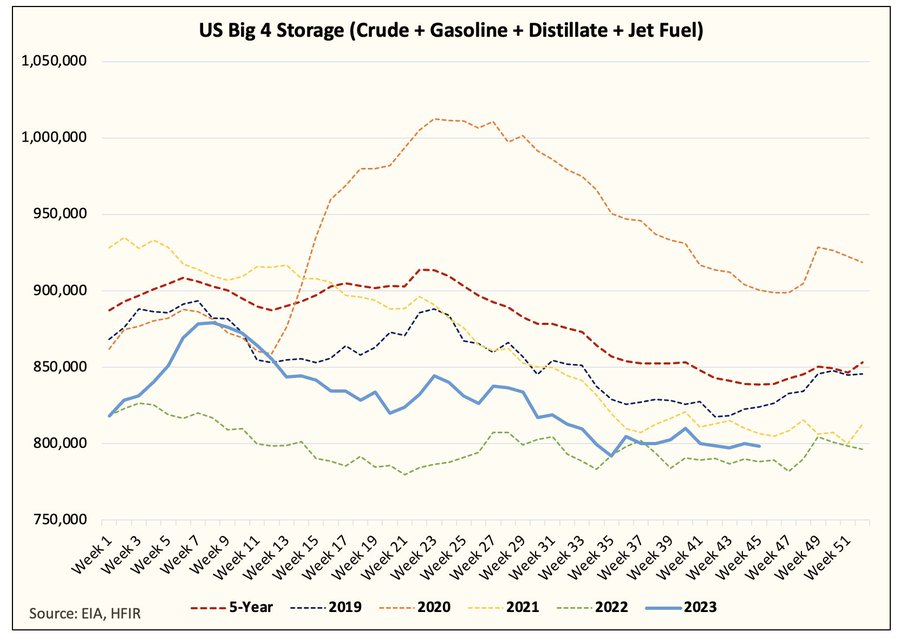

Oil – $72.93

Oil plunged back to its July low as computer trading algorithms amplified the supply-driven drop in response to a 17.5 million barrel build in crude inventories over the last two weeks – not the usual one-week report.

Click for larger graphic h/t @HFI_Research

But the Energy Information Administration’s Supply & Disposition report shows 502,000 barrels a day of Natural Gasoline (derived from Natural Gas Liquids) went into crude oil. Part of the crude build is due to relabeling natural gasoline tanks in the field from gas blend stock to crude oil. The big four – crude+gasoline+distillates+jet fuel – actually are flat (at a low level) over the last two weeks.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

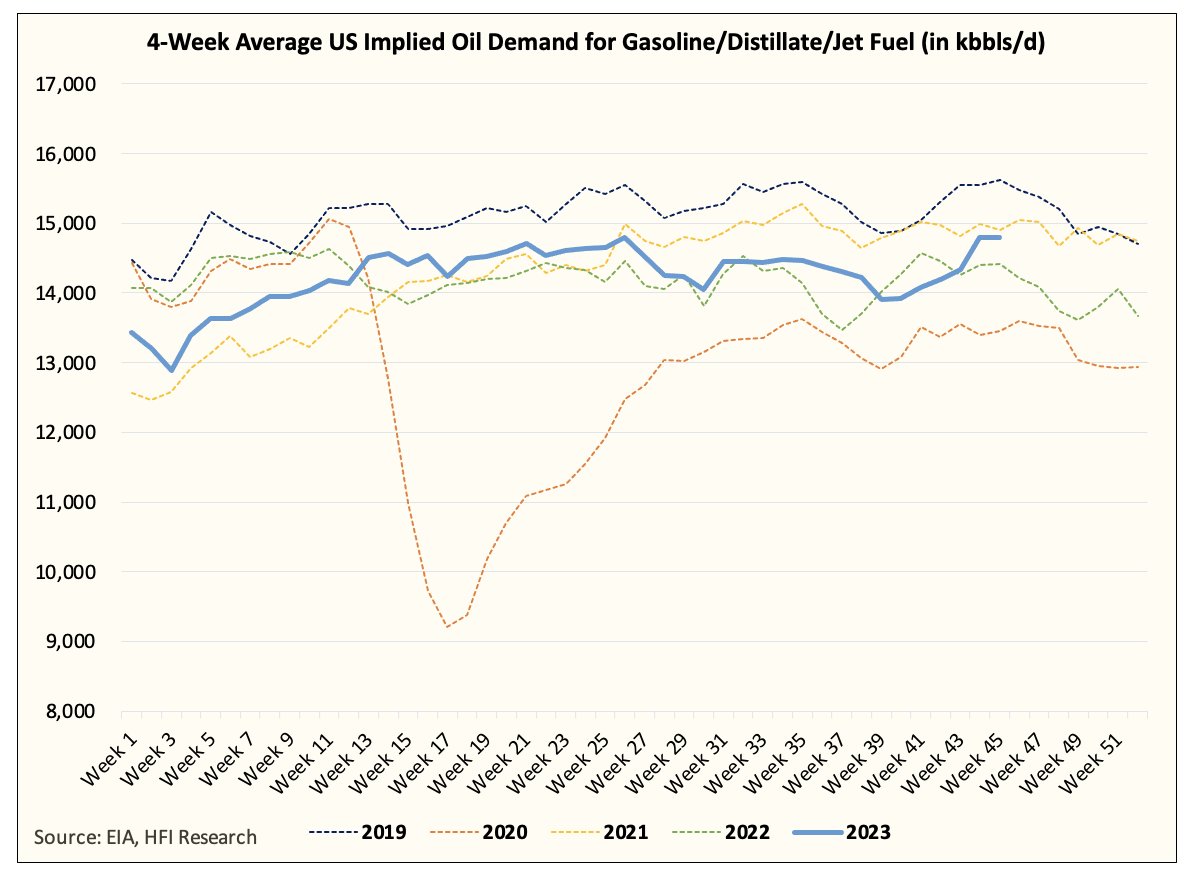

While demand stays high.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

It looks like EIA has overstated US crude storage by eight to nine million barrels. This will reverse over the coming weeks, driving up oil prices. Net longs are close to five year lows, US total oil inventories are at levels we ran in the early 2000s, US rig counts are back at Covid levels, oil demand is outpacing supply, and the financial consensus is that oil should trade lower. Really? Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $68.27) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $35.60) is a Buy under $40 for a $100+ target.

EQT (EQT – $40.05) slipped a bit today after the EIA reported an increase in gas storage last week that was higher than expectations. With very cold weather forecast for the first half of December, I’m not worried. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $8.28) sold the remaining unpaid balance of $20 million owed under the secured convertible note issued to the company by enCore Energy as partial consideration for enCore’s purchase of the Alta Mesa In-Situ Recovery Project. enCore previously paid $40 million toward the $60 million principal note balance and $1.8 million of interest.

The buyer, MMCAP International Inc SPC, paid $22.4 million, so UUUU has now received payment in full. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $35.54) is moving up as copper prices are rising again. Futures contracts have gained 5.4% to $3.71 per pound from a multi-month low of about $3.52 on October 23. I think copper will hit $5 soon due to dangerously low inventories, and FCX will soar. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

International & Other Recommendations

Acreage Holdings (ACRDF – $0.24) reported September quarter revenues down 2.8% from the June quarter to $56.5 million with a loss of $7.9 million. They had their 11th consecutive quarter of positive adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation & Amortization) at $6.6 million.

CEO Dennis Curran said: “The playbook we have created from our experiences launching adult-use sales in Connecticut and New Jersey will benefit us greatly as our other core markets begin to adopt adult-use regulations. With the adult-use market finally beginning to open in New York, and the recent vote for adult-use legalization in Ohio, we are readying our operations for increased output and innovation to continue differentiating our offering in anticipation of the long-term growth potential these markets offer.”

They finished the quarter with $15.1 million in cash plus $9.7 million in restricted cash that can be used for capital expenditures. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

* * * * *

Wildest Motorcycle Chase Ever

* * * * *

Your reading the plot to kill the Censorship Industrial Complex Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 11/16/23. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $189.71) – Buy under $150 for new iPhones

Corning (GLW – $28.38) – Buy under $33, target price $60

Gilead Sciences (GILD – $74.52) – Buy under $80, target price $120

Meta (META – $334.19) – Buy under $150, target price $400

SoftBank (SFTBY – $20.05) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $11.37) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $47.41) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $16.25) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $21.17) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $10.60) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.22) – Buy under $13, target price $30+

Velo3D (VLD – $1.06) – Buy under $6, target price $50

$20-for-$1 Biotech

Akebia Biotherapeutics (AKBA – $0.99) – Buy under $2, target $20

Aptose Biosciences (APTO – $2.77) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $5.66) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.41) – Buy under $7, hold a long time

Invitae (NVTA – $0.54) – Buy under $10, first target $50, then $100+

Medicenna (MDNAF – $0.36) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.58) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $11.26) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($23.84) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $23.59) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $27.71) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.58) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $25.28) – Buy under $30, target price $50

Coeur Mining (CDE – $2.48) – Buy under $5, target price $20

First Majestic Mining (AG – $5.27) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.35) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.65) – Buy under $10, target price $25

Sprott Inc. (SII – $30.10) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $35,920.01) – Buy

Grayscale Bitcoin Trust (GBTC – $28.99) – Buy

Ethereum (ETH-USD – $1,960.41) – Buy

Grayscale Ethereum Trust (ETHE – $16.10) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $68.27) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $35.60) – Buy under $40; $100+ target

EQT (EQT – $40.05) – Buy under $35; $70 first target

Energy Fuels (UUUU – $8.28) – Buy under $8; $30 target

Freeport McMoRan (FCX – $35.54) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $30.27) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $21.58) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.02) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $27.55) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.24) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.01) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.60) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First!

MM–you have not addressed my post from nearly a week ago–

JGMD

November 10, 2023 12:33 pm

MM–statement from VLD–

“Additionally, we have also implemented new go-to-market and service strategies to rebuild our bookings and backlog pipeline which came in below our plan for the third quarter. With the early success of these programs, we expect to resume bookings growth in the fourth quarter for fiscal year 2024 deliveries.”

What the heck are “go-to-market and service strategies”?–sounds like promotional BS to me. Now that backlogs are gone for the 4th quarter, it looks bad. Never mind bookings GROWTH. Q4 could have much lower sales. There have been consistent 3 quarters of sales declines.

Last edited 6 days ago by JGMD

You merely addressed the minor accounting issue in tonight’s RR. More important is whether VLD is on an extended decline in sales–3 quarters and counting. The company forecasted lousy Q4 sales now that backlogs are gone. I searched “go-to-market” and it looks like horsecrap marketing lingo. There are sales people I respect who know the technical details and applications of the products, and then there are marketing people who lack technical understanding. Marketing people merely know the attention grabbing BS buzzwords and cheer leading behaviors. My friend in the food product development business told me about all this. The food scientists worked nicely with the sales people, but had conflicts with the marketing people.

Please address how all this applies to VLD. You got some subscribers in at $10 who are now down 90%. I recently got in at $1.54 which you said was a gift. Now even I am down over 30% in a short time, so please address this in a timely fashion. Thanks.

MM – please explain your conflicting position on bitcoin – you still call it an aggressive buy and predicting its going to at least $100k (in one post you told me possibly as soon as in 2023) now more recently you’re creating fear it could drop rapidly citing tether as the catalyst. If your premise for the drop is that criminals are using tether to purchase bitcoin (correct me if I misunderstand) and tether may fall or be banned under new regulation, I find that a weak premise for the destruction of the bitcoin price. Criminal activity in bitcoin has always been overblown as reports I read say it is a small percentage of transactions and once ETF’s are approved, the inflow of retail and institutional investors will by far overshadow any criminal activity. Please reply to this post and provide a more clear explanation with adequate support of when and where you expect bitcoin pricing to go.

something going on with ARTH I been out for long time.

no information on the ARCH web site, maybe a buyer taking a large position ???

Not sure what is going on, however, they said how well they have been sell their product usage. So I purchased a lot at .60 cents this week and today it closed at $2.70 dollars. That’s 350 percent above my purchase price. So guess they will share at some point their earnings soon. I’m considering purchasing some more….

Would like to hear what Mr. Murphy has to say and wondering if he will put it on Buy List again ?????

Is this the first time you bought ARTH shares? If so, congrats on your gains, and also waiting and waiting and waiting for 99% declines from many years ago when MM recommended purchase and when he said it was his largest personal holding. If not, the typical purchaser of ARTH is still down way over 90%.

Do not buy any stock that has gone up 350% in a week. If you think that ARTH will eventually be profitable with earnings, sell now, and wait to re-enter at half the current price or less. MM has talked about Fibonacci retracement, so if 30-40% of the current price holds, buy at that price.

Thank for the CONGRATS, JGMD! Hopefully, we will hear from Mr. Murphy on what’s going on. THANKS AGAIN!!

ARTH, at $7.05 today. Was as high as $9.00 and change. Just sayin. Happy turkey day , everyone.

https://ir.medicenna.com/news-releases/news-release-details/medicenna-announces-compelling-survival-benefit-phase-2b-study

Chris, very interesting. I’m not familiar with the length of time it takes for these types of trials, but I imagine P3 could last a long time. Have you seen NWBO? Seems to be considerably more advanced and very successful so far. I think both companies address the same issue. I tend to look at the amount of time a company is anticipated to get to the finish line, given my age.

Unfortunately, MDNA started looking for a MDNA55 Phase 3 partner over 3 years ago after completing their Phase 2 trial and has has no success thus far. So MDNA55 has been in a holding pattern going nowhere, which is concerning.

MDNA is using their little remaining cash to get MDNA11 further along it’s Phase 1/2 trials but will face the same issue of needing a Phase 3 partner to proceed further.

The second SpaceX was a failure, with 2 self-destruct explosions after 10 min of flight, which was supposed to last 90 min. The first SpaceX in April exploded after 4 min, so Musk will consider the second as a success since it lasted longer. He will say it was a deliberate experiment to test variables in the process.

WARNING–these tech experimenters, esp in biotech, don’t know their ass from their elbow. AI is an early stage experiment, and at this point is not to be trusted in running society. Humans despite flaws, at least have honesty about their abilities and limitations. Humility is better than hubris. Central socialist planning is based on the flawed idea that masterminds know what they are talking about in “efficiently” (let’s all vomit) controlling what’s best for others. The masterminds are fools.

MM : Any insights as to what is going on with ARTH would be most helpful.

Don’t know. I bought it a week ago at .60 cents. Reason why I bought it was they were claiming GREAT EARNINGS! However, so far to my knowledge, haven’t seen their earnings yet!!

What were sales/revenues reported? (As an aside, TGTX had a one time big cash infusion from their EU partner in Q3. Earnings were fantastic. Although sales grew 50% from Q2, sales will need to keep growing consistently to get to cash flow positive.) So what is the overall financial position of ARTH? Since they have to wait another quarter to see if sales are consistently growing, the stock is vulnerable to a big pullback in the interim.

New World Investor for 11.22.23 is posted.