Dear New World Investor:

The September quarter was the best earnings quarter in a year for the S&P 500, thanks to strong consumer spending as Americans continued to dine out, take trips, and buy online. That drove profits at some of the biggest companies.

Click for larger graphic

Click for larger graphic

According to FactSet, in addition to the 3.7% increase in earnings, the first such increase since the 2000 third quarter, revenues are on track to grow 2.3% from a year ago.

Can this keep up? No. The Atlanta Fed’s GDPNow model increased its estimate of December quarter real GDP to 2.1% due to strength in personal consumption expenditures growth and gross private domestic investment growth. So we’re OK through the end of this year.

Click for larger graphic

Click for larger graphic

But I still think a mild two- or three-quarter recession is likely next year. Consumers are tapped out.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

A mild recession probably means a long pause from the Fed – I don’t think they are eager to cut rates – and lower earnings and stock prices for the same companies that benefited in the September quarter. Tech companies that can grow should be OK.

Market Outlook

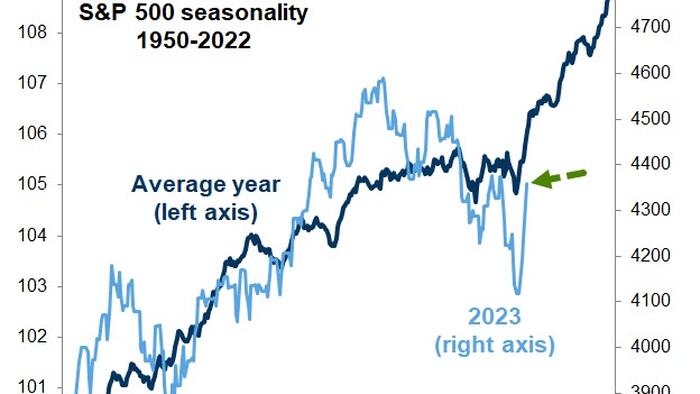

The S&P 500 added 0.7% since last Thursday after an eight-day winning streak that ended today, its longest since 2021. The Index is up 13.2% year-to-date. Seasonally, November is the strongest month of the year and December is close behind, so we should end the year on a high note.

Click for larger graphic h/t @zerohedge

Click for larger graphic h/t @zerohedge

The Nasdaq Composite gained 1.7% after a streak of nine consecutive up days – its best run since January – also ended today. It is up 29.2% for the year. The small-cap Russell 2000 dropped 1.6% and is down 4.2% in 2023. Small-cap bear markets are painful, but the Russell could easily be up by yearend.

The investment professionals continue to get it wrong. According to Goldman Sachs: “In the US, Commodity Trading Advisers (CTAs) are short about $52 billion of equities after selling ~$17 billion last week. Per our model, they are now buyers of global equities in every scenario over the next week.”

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

In the bond market, hedge funds extended their short positions on Treasury bonds to a record just before smaller-than-expected US bond sales and weaker jobs data spurred a rally. According to the Commodity Futures Trading Commission, as of October 31, leveraged funds ramped up net short Treasury futures positions to the most in data going back to 2006. Ouch.

Click for larger graphic

Click for larger graphic

Yields on 10-year Treasuries have fallen 39 basis points since their 5.02% peak on October 23, as traders of the $26 trillion bond market swung back to pricing in the end of rate hikes. The combination of more benign US refunding needs, weaker-than-expected jobs data, and signs of the Federal Reserve turning less hawkish probably spurred widespread covering of short positions, with more to come.

The pros need to put up strong numbers to finish the year because 2023 has been awful for them so far – and that means redemptions and no holiday bonus. If a move down starts, they already are positioned for it. If a move up starts, it will be explosive as all the elephants try to get through the door at once.

The fractal dimension is showing continued consolidation of the recent drop, with no real indication of what comes next. I think positive seasonality combined with very bearish sentiment will cause a breakout, probably to new all-time highs.

Top 5

Changes this week: None

Near-Term – chronological order

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage this fall

SFTBY SoftBank – for ARM IPO valuation

AKBA Akebia – Vadadustat approval March 27, 2024; TDAPA approval October

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, November 10

GILD – Gilead Sciences – Through 11/14 – 80 presentations at the American Association for the Study of Liver Diseases (AASLD) “The Liver Meeting”

Saturday, November 11

Veterans Day

Tuesday, November 14

QUIK – QuickLogic – 5:30am – Space Tech Expo Europe

Consumer Price Index – 8:30am

QUIK – QuickLogic – 5:30pm – Earnings conference call

Wednesday, November 15

GILD – Gilead Sciences – 4:00pm – Jefferies London Healthcare Conference

FSLY – Fastly – 11:20am – RBC Technology, Internet, Media and Telecommunications Conference

Thursday, November 16

QUIK – QuickLogic – Unspec. – Craig-Hallum Alpha Select Conference

FSLY – Fastly – 11:45am – D.A. Davidson Technology Summit

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $182.41) introduced updated Final Cut Pro video editing software for Mac and iPad. I’ve used several video editing systems, including editing an entire movie on a rented Avid in my living room, and Final Cut Pro is one of the best.

The company opened their latest Apple retail store in Wenzhou, China, with 100 employees selling iPhone 15 and all the rest of the product line. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

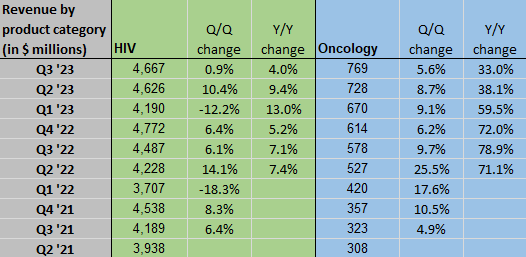

Gilead Sciences (GILD – $74.98) reported September quarter revenues up 0.1% from last year to $7.05 billion, just above the $6.79 billion estimate. While HIV revenues only grew 4% (although Biktarvy was up 12%), Oncology soared 33%:

Click for larger graphic

Click for larger graphic

They earned $2.29 pro forma per share, far ahead of the $1.91 consensus estimate.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said they have numerous data updates coming:

Click for larger graphic

Click for larger graphic

They raised their 2023 revenue guidance again, this time from a range of 6.5% to 8% growth from 2022 to a range of 7% to 8%. Earnings guidance is up to $4.55 to $4.75.

Click for larger graphic

Click for larger graphic

CEO Dan O’Day said: “This was also another very good quarter for clinical execution as we continued to advance our 60 clinical programs across virology, oncology, and inflammation. One of the highlights for the quarter was the European Commission approval of Trodelvy for pretreated hormone receptor positive/HER2-metastatic breast cancer, allowing us to extend Trodelvy’s reach to many more patients globally…Our clinical pipeline now includes 27 programs in Phase 2 and 19 in Phase 3. We are looking forward to a busy period of updates from many of these studies in 2024.”

GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $320.55) worked with their partners at the Tech Coalition to establish Lantern. It enables technology companies to share a variety of signals about accounts and behaviors that violate their child safety policies. Lantern participants can use this information to conduct investigations on their own platforms and take action.

Meta provided the Tech Coalition with the technical infrastructure that sits behind the program and manages and oversee the technology. Meta reports more child sexual abuse material to the National Center for Missing & Exploited Children than any other service today. META is a Buy under $150 for a $400 target in 2024.

SoftBank (SFTBY – $19.75) reported September first half results early this morning. Revenues were up 1.4% from last year to $21.3 billion, including $11 billion in the September quarter. They lost $6.2 billion after writing down their $1.5 billion WeWork investment, which filed for bankruptcy. Their $47 billion gain on ARM did not go through the income statement but was recorded as a capital surplus. This is the key to understanding SoftBank – they continue to build (untaxed) value, even if it only shows up on the balance sheet. Wall Street will moan over the WeWork loss and ignore the ARM gain. Don’t get sucked in!

There was a (CFO VIDEO HERE and SLIDES HERE ), but no conference call or transcript I could find. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $10.71) reported a pro forma loss of 19¢ per share, better than the 23¢ consensus estimate.

On the conference call (SHAREHOLDER LETTER HERE and very worthwhile SLIDES HERE and TRANSCRIPT HERE), management said they expect December fourth quarter revenue of $3 million to $4 million due to a partial quarter from Routejade and continued shipments of silicon batteries to the US Army. The stock jumped.

Factory Acceptance Testing of Gen2 manufacturing equipment began on schedule in August and is complete for one zone of the full production line. They continue to expect to complete acceptance testing for all four zones by January.

President and CEO Dr. Raj Talluri said: “We are in a large and fast-growing industry (McKinsey is now projecting the entire lithium-ion battery chain will grow over 30% annually to $400 billion by 2030) that remains starved for product performance improvement to unlock economic value for the World’s most important industries. Based on customer feedback, the ecosystem is looking for silicon replacement of graphite as the lever to unleash increased battery performance and we believe our progress this year, backed by customer feedback, has positioned Enovix as the leading contender in silicon batteries.

“Products such as smartphones with large displays face the greatest challenge in keeping up with user demands for battery capacity. On top of this, emerging artificial intelligence applications drain even more power. Contrast that with meager improvements from conventional battery architectures, and the opportunity for Enovix to make a meaningful impact has never been greater.

“We remain on track to move to high volume production in Malaysia in 2024 and deliver an industry-leading battery that enables our customers to launch compelling new products.”

EV batteries would be icing on the cake.

Click for larger graphic

Click for larger graphic

Polaris Battery Labs, an established testing lab based in Beaverton, Oregon, was engaged recently by a Tier-1 wearable company to assess advanced performing cell options for their next generation product. The Enovix cells met the customer’s performance specifications, including cycle life and storage testing, and showed the highest energy density among the cells evaluated.

Polaris said: “The Enovix cells perform better than the other silicon products we’ve assessed in our lab. We are impressed by the performance of the cell and the commercial availability of their products for a variety of OEM applications.”

There was a good Seeking Alpha article: Enovix Q3 Earnings: Accelerating Towards Modern Battery Dominance. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

PagerDuty (PD – $20.70) is acquiring Jeli, an enterprise-grade, all-in-one incident management solution. In addition to PagerDuty’s incident response and management tools, Jeli adds deep, actionable analysis to help customers turn every incident into an opportunity to learn how to reduce the impact of future incidents and shift their organizations from a reactive stance towards a more proactive, methodical approach, allowing them to operate more efficiently. Jeli surfaces patterns from incidents, prioritizing opportunities for improvement in escalations, resource allocation and project planning. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

QuickLogic (QUIK – $9.49) reports next Tuesday after the close. The consensus of two publishing analysts is expecting $6.5 million in sales and 13¢ earnings per share, compared to a seven-cent loss last year. Guidance should be for $7.65 million and 10¢. That would bring them in at $21.2 million and eight cents for 2023. Analysts expect 2024 to hit $28.6 million and 35¢.

Earlier that day, they’ll present at the Space Tech Expo Europe 2023 in Germany. QUIK is a Buy up to $10 for my $40 target as their sensor hub is widely adopted in smartphones, tablets and wearables.

Primary Risk: New sensor hub competitor emerges.

In spite of the launch shutdown, Rocket Lab USA (RKLB – $4.28) reported September quarter revenues up 7.3% from last year to $67.66 million,right on the $66.56 million estimate. They lost eight cents a share, a penny better than the consensus estimate for a nine-cent loss.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said: “…the findings of the Rocket Lab investigation team overwhelmingly indicate that an electrical arc occurred within the power supply system that provides high voltage to the Rutherford engine’s motor controllers, shorting the battery packs which provide power to the launch vehicle’s upper stage. With growing confidence in our determination of the anomaly’s probable root cause and corrective measures in place, we expect to formally close our investigation in the coming weeks. Electron’s return to flight is scheduled during a launch window that opens from November 28, 2023, and extends into December.” That is a a dedicated mission for Japan-based Earth-imaging firm iQPS.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

They had continued strong growth in HASTE bookings for hypersonic test launches from Rocket Lab Launch Complex 2 in Virginia. They announced a new win: A HASTE mission for the Defense Innovation Unit (DIU) to deploy a scramjet-powered suborbital payload by Australian company Hypersonix. The hypersonic vehicle is capable of flying non-ballistic flight patterns at speeds of up to Mach 7. This is the seventh launch contract Rocket Lab has won with prime hypersonic defense customers in the past six months.

For the December quarter, they guided for revenue between $65 million and $69 million, with Space Systems revenue between $48.5 million to $52.5 million, and Launch Services revenue of approximately $16.5 million. They expect an adjusted EBITDA (Earnings Before Interest, Taxes, Depreciation & Amortization) loss of $23 million to $27 million.

For the March quarter, they expect a big jump in revenues to between $95 million and $105 million. Space Systems revenue will be between $65 million to $68 million as they deliver the first spacecraft n their largest program, the $143 million Globalstar contract. Launch Services revenue will be between $30 million and $37 million as they go back to a full schedule. Their launch manifest is fully allocated for 2024 and into early 2025.

Click for larger graphic

Click for larger graphic

RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $1.32) reported September quarter revenues up 25.9% from last year to $24.1 million, below the $27.1 million estimate. They lost 10¢ a share, also under the eight-cent loss consensus estimate.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said they have laid off 20% of the workforce and: “…we now believe our industry leading growth has come at the expense of cash flow, profitability and our commitment to the highest level of customer service.

“As a result, in October 2023, we made the strategic decision to realign our operations to pivot from emphasizing top line growth to optimizing free cash flow, maximizing customer success, reducing expenditures, and improving our operational efficiency. We firmly believe that this strategy will ensure the company will have the liquidity it needs to achieve its profitability goal in 2024.

“Specifically, we expect this realignment to lower our overall cost structure by approximately 40%, by the first quarter of 2024, including reductions in operating and facilities expenses.

“Additionally, we have also implemented new go-to-market and service strategies to rebuild our bookings and backlog pipeline which came in below our plan for the third quarter. With the early success of these programs, we expect to resume bookings growth in the fourth quarter for fiscal year 2024 deliveries. However, given the delays in certain fourth quarter orders, as well as the impact of our realignment, we now see our fiscal year 2023 revenue to be in the range of $91 million to $103 million.”

Click for larger graphic

Click for larger graphic

That guidance is well below the $108.62 million consensus. For the December quarter, which they expect: “to be a transition period as it focuses on the execution of its realignment strategy. As a result of the impact of our realignment and delays in certain fourth quarter bookings, the company now expects…revenue in the range of $15 million to $27 million.” Some range!!! That is short of the $29.69 million consensus.

Click for larger graphic

Click for larger graphic

Their rapid growth in 2022 – revenue tripled year-over-year – impacted customer support. They are reallocating resources to expand customer support, increasing new product training programs, and partnering engineering and support to quickly resolve field issues. These initiatives should pay off in higher orders in 2024.

Free cash flow increased 30% from the June quarter and they ended September with $71.6 million in cash. VLD is a Buy up to $6 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Last Friday, the equal-weighted SPDR S&P Biotech Exchange-Traded Fund (XBI) added 5%, marking its biggest intraday gain in almost a year. The market-cap weighted Nasdaq Biotechnology Exchange-Traded Fund (IBB) was up 3%, its best weekly performance since October 2022. These are just green shoots, but they are early signs that the biotech bear market is over.

Akebia Therapeutics (AKBA- $0.91) reported September quarter revenues down 13.7% from last year to $42.05 million, below the $48.18 million estimate. The decrease was primarily due to a decrease in license, collaboration, and other revenue. They lost eight cents a share, better than the consensus estimate for a nine-cent loss.

On the conference call (TRANSCRIPT HERE), management said: “With [vadadustat] approval, we have the potential to target an approximately $1 billion market based on estimates that approximately 88% of the nearly 550,000 patients on dialysis would be treated with an erythropoiesis-stimulating agent, or ESA, for anemia. These are the injectables that are the standard-of-care.

“It’s important to highlight that we are already well prepared for a potential launch and have identified important tailwinds we believe will contribute to our success. First, we have our commercial product supply ready to go, awaiting final label post potential approval.

“Second, we also have an experienced commercial sales organization actively calling on dialysis centers. We believe there is approximately a 96% overlap between Auryxia prescribers and potential vadadustat prescribers. Importantly, we’ll also benefit from our partnership with CSL Vifor ,which enables potential access to 60% of the treatment centers through its collaboration with Fresenius Medical Care and other small and medium-sized providers.”

After about $170 million in Auryxia sales in 2023, they expect Auryxia revenue to grow in 2024 as they exit unfavorable payer contracts, incrementally expand their commercial and medical footprint, and gain broader access to providers from their interest in learning about vadadustat.

The company finished the quarter with $48.2 million in cash, enough to fund them into late 2024. Buy AKBA up to $2 for the vadadustat launches in the EU, UK, and (after FDA approval in March 2024) the US.

Primary Risk: Vadadustat not approved in the US.

Clinical stage of lead product: Vadadustat PDUFA date 3/27/24

Probable time of next FDA approval: March 27, 2024; TDAPA October

Probable time of next financing: Late 2024 or never

Aptose Biosciences (APTO – $3.24) reported a September quarter loss of $1.76 a share, better than the consensus estimate for a $2.05 loss. In the quarter, they spent $8.3 million on R&D and $3.4 million on General & Administrative.

On the conference call (AUDIO HERE and TRANSCRIPT HERE), management said they put in place a committed equity facility and ATM facility to fund the company and give them “time to collect critical data with Tuspetinib that may drive improved financing terms and potential collaborations.” They are looking at all alternatives for raising money, including debt.

They will have an oral presentation at the American Society of Hematology (ASH) Annual Meeting and Exposition on December 9: Tuspetinib Myeloid Kinase Inhibitor Safety and Efficacy As Monotherapy and Combined with Venetoclax in Phase 1/2 Trial of Patients with Relapsed or Refractory (R/R) Acute Myeloid Leukemia (AML).

The company finished the quarter with $17.7 million in cash, which can only carry them through the March quarter. APTO is a Buy under $2.50 for a $300 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Soon

Arch Therapeutics (ARTH – $0.80) has not filed their September fourth quarter 10Q yet, but they said that during the quarter, they experienced a significant increase in AC5 orders, posting record monthly order volumes during both August and September. Taken together, orders from August and September represented more than half of total fiscal year volume, and September orders more than doubled August orders. They also observed favorable coverage and reimbursement decisions from multiple payers in different regions of the country with a commensurate increase in paid claims. At last!

They filed to sell up to $4,887,500 of stock plus warrant units and up to $4,250,000 of pre-funded units. We’ll see how they do. ARTH is a Hold for a buyout.

Primary Risk: AC5 fails to sell or the internal trial fails.

Clinical stage of lead product: External approved. Internal trial 2024

Probable time of first FDA approval: External done. Internal 2025

Probable time of next financing: December 2023 quarter

Compass Pathways (CMPS – $5.40) finally got a transcript (HERE) of the earnings conference call I covered last week. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Inovio (INO – $0.36) also reported a September quarter loss of nine cents a share, better than the consensus estimate for a 13¢ loss.

On the conference call (AUDIO HERE and CORPORATE PRESENTATION HERE and TRANSCRIPT HERE), management said they have requested an FDA meeting before yearend to discuss the requirements for their upcoming BLA (Biologics Licensing Application) for INO-3107 for Recurrent Respiratory Papillomatosis. This will be the first DNA medicine ever approved, and Inovio is accelerating their commercialization strategy in preparation for an earlier launch.

They’ve gone from proof of concept to a BLA filing in a lightning-fast three years.

Click for larger graphic

Click for larger graphic

They will begin the required confirmatory trial before the BLA submission. They will request a rolling review of the BLA filings with a priority review of six months instead on the usual ten months. I think its a shoo-in for approval.

Click for larger graphic

Click for larger graphic

Inovio is not a one-trick pony. DNA medicine is a platform technology like acquirers love.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

INO is a Buy under $7 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: 2025

Invitae (NVTA – $0.42) dropped 38% today after they reported September quarter revenues down 9.2% from last year to $121.24 million, in-line with the estimate. Their pro forma loss was only 10¢ a share, clobbering the 32¢ loss estimate. The pro forma gross profit margin hit 52.4% showing continued improvement for nine consecutive quarters.

Click for larger graphic

Click for larger graphic

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said by the end of the quarter they had served 4.4 million patients, with 64% available for data sharing.

Management pointed to their obvious continued operational excellence and improvements in billing workflow and collections. They said they are “working on solving balance sheet and capital needs,” which is what tanked the stock today. The dramatic reductions in cash burn have ended:

Click for larger graphic

Click for larger graphic

Management said: “We are creating plans that will, over the next 12 months, further reduce operating cash burn and improve the company’s liquidity. This is a top priority and we are actively engaging with our stakeholders in seeking constructive feedback and solutions.

“Our board of directors has formed a special committee to focus on addressing our capital structure needs. With our board, we are exploring a number of options, which could include raising capital, addressing our debt, selling certain assets, and continuing operational improvement and cost reduction efforts.”

They reaffirmed 2023 guidance for revenues of $480 million to $500 million and a non-GAAP gross margin in the range of 48-50%.

The company finished the quarter with $264.7 million in cash, enough to carry them through 2024. But they either have to cut cash burn further or raise money around mid-2024. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Mid-2024.

They presented promising single-agent response and durability of MDNA11 in the Phase 1/2 ABILITY trial during dose escalation at the 38th annual meeting of the Society for Immunotherapy of Cancer. The drug showed deep ongoing partial responses with 100% reduction of target lesions in one pancreatic patient and a 70% reduction of target lesion in one melanoma cancer patient. It also showed durable stable disease in three melanoma patients for at least five months to as long as 18 months with concomitant shrinkage of tumor size following failure with check-point inhibitor therapies. It was well-tolerated with no dose-limiting toxicities or vascular leak syndrome reported in any of the dose escalation cohorts.

They also presented, for the first time, preclinical data on MDNA113, a targeted metalloprotease activated SuperKine (T-MASK). While its good to know R&D has produced another viable candidate, I’m not much interested in preclinical or even Phase 1 safety data. The rubber meets the road in Phase 2 dose escalation studies, preferably with a placebo or standard of care control. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

TG Therapeutics (TGTX – $10.14) did a fireside chat at the Guggenheim Inflammation, Neurology & Immunology Conference. They are expecting $33 million to $37 million in Briumvi sales in the December quarter, quite a jump from September’s $25.1 million. There are about 80,000 multiple sclerosis patients starting a new therapy every year, some new and some switching from a different therapy. About half of them choose a CD-20 therapy like Briumvi.

TGTX will have about a 20% market share next year, or 8,000 patients. That means in 2025 they have those 8,000 minus some low loss factor plus the new 8,000. In 2026, they start with over 15,000 patients and add another 8,000, and so on. CEO Michael Weiss specifically called out the BofA analyst for publishing a model that only shows the new 8,000 patients each year and ignores this accumulation effect, saying: “Anyone who has read his research is completely misguided in how they are thinking about that part of the opportunity.” Ouch!

Buy TGTX under $12 for a target price in a buyout of $30 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($1,963.30) went over $2,000 and fell back for the fourth time, towards the $1,950 tractor beam.

Click for larger graphic h/t Kuppy

Click for larger graphic h/t Kuppy

Ever since President Biden weaponized the US Dollar and stole Russia’s reserves, other countries are wondering why they should hold Biden Bucks, or Yellen Treasuries. They’re buying as much gold as the liquidity window will allow. It’s said that there’s no such thing as a triple top – what about a quadruple top?

It’s frustrating, and gold may need a few weeks of rest, as the Commitments of Trader report shows that the fast money mob got a bit too giddy, but I also think that gold makes its move before too long. The fractal dimension continues to consolidate, building energy to power the next move to and through $2,000.

Miners & Related

Coeur Mining (CDE – $2.19) reported September quarter revenues up only 6.3% from last year to $194.6 million. There was only one, thoroughly out-of-date, estimate for $257.5 million. They lost five cents a share pro forma, worse than the consensus one-cent loss estimate from four analysts.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management pointed to their strong 10% quarter-over-quarter revenue growth from the June period’s $177.2 million, as well as good cost performance.

They said the Rochester mine expansion is complete with significant production increases now underway. During the month of October, Rochester recovered 537,000 ounces of silver and 8,050 ounces of gold, which is more than double their year-to-date monthly average silver production and more than triple their year-to-date monthly average gold production. It will transition the company to positive free cash flow during 2024.

The low end of their total 2024 production guidance remains unchanged at 304,000 ounces, but they trimmed the high end to 342,500 ounces. Silver full-year production guidance of 10 million to 12 million ounces remains unchanged.

They ended the quarter with $60 million in cash and $220 million of available credit. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $0.33) filed a shelf offering for $25 million of securities. This is not an offering. PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: 2023

Sandstorm Gold (SAND – $4.64) reported September quarter revenues up 5.9% from last year to $41.3 million, right on the $41.4 million estimate. The broke even. under the two-cent consensus estimate.

On the conference call (INVESTOR PRESENTATION HERE and SLIDES HERE and TRANSCRIPT HERE), management repeated that attributable gold equivalent ounces for 2023 are forecasted to be between 90,000 and 100,000 ounces, and they still expect to reach approximately 125,000 attributable gold equivalent ounces within the next five years. They are targeting over $200 million in annual cash flow.

Click for larger graphic

They are paying down bank debt and expect to be under $350 million by the end of 2024. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

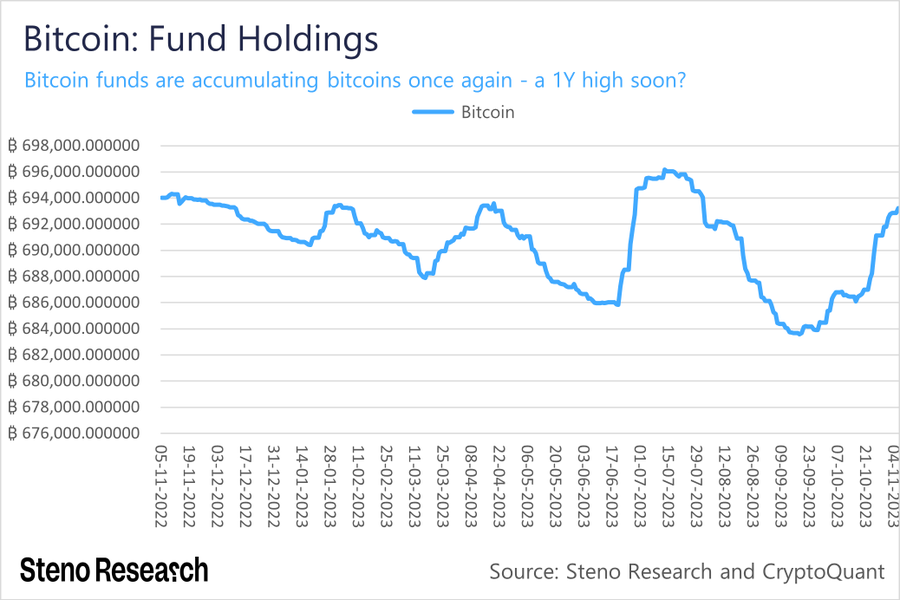

Bitcoin (BTC-USD on Yahoo – $36,720.55) went over $36,000 as the recent rally continued. Until the SEC finally caves on a spot bitcoin exchange-traded fund or moves to shut down Tether, the rally can continue.

Click for larger graphic

Click for larger graphic

The bitcoin holding of funds, including trusts, exchange-traded funds, and exchange-traded products, is increasing. They may be front-running the approval of bitcoin spot exchange-traded funds in the US, or simply increasing their portfolio allocation.

Click for larger graphic h/t @MadsEberhardt

Click for larger graphic h/t @MadsEberhardt

BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $29.09) got quite an article on Seeking Alpha: Bitcoin Is Booming Again: Last Chance To Snag GBTC At A 13% Discount Before The 2024 Halving. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $75.58

$75 oil? Really? Let’s see. Rig counts were coming down even with oil at $80. The Middle East is unstable. US shale oil is peaking. The Russia sanctions eventually are going to bite. Demand is fine, the world will always revert to growth. Demand growth has actually consistently been revised up during the year, and mobility data shows an acceleration in demand and demand growth. EV adoption is slowing. OPEC+ is backstopping the market as Saudi Arabia and Russia – the two biggest OPEC+ producers – are maintaining their production cuts through at least the end of the year.

Saudi Arabia said it will maintain its one million bpd (barrels per day) production cuts through the end of 2023. And Russia is cutting 300,000 bpd through the end of 2023. Those cuts amount to roughly 1% of daily global demand. I expect the Saudis to announce a 2024 first quarter extension in early December.

After the cuts, Saudia Arabia produces around 9 million bpd and Russia produces 9.5 million bpd. Of that, Saudi Arabia exports around 5.6 million bpd and Russia exports 3.4 million bpd. Both countries are likely to maintain cuts into 2024 in some form to keep pressure under the oil price.

And refilling the SPR is going to keep a floor under oil prices for years to come.

Did I miss anything? Oh, yeah, A Record Number of Supertankers Is Headed to Collect US Oil. Forty-eight vessels are bound for the US in the coming three months – the most in at least six years. Shipments from the Gulf Coast — the main exporting region — are expected to rise next month to 4.1 million bpd as the OPEC+ curbs are prompting tankers to leave the Middle East.

Oil demand is now at all-time highs, and it’s only going up from here. World oil consumption is set to reach a record average of 102.1 million bpd in 2023. That’s driven by a 2.3 million bpd demand increase in developing countries. Next year, OPEC expects oil consumption to increase by 2.2 million bpd based on an improving Chinese economy. That will take oil demand to a record of around 104.3 million bpd in 2024.

Even if OPEC’s forecast is overly optimistic, Paris-based intergovernmental organization the International Energy Agency expects oil demand to rise by almost one million bpd. Either way, demand is growing.

OPEC sees oil demand reaching 110 million bpd by 2028 and 116 million bpd by 2045, based on strong demand from developing countries. What’s more, that estimate includes growing demand for renewable energy. Further, OPEC estimates energy companies will have to invest $14 trillion between now and 2045 to meet demand targets. With the anti-fossil fuel people targeting major banks, where will the drillers get the money?

OPEC expects the combination of strong demand and supply cuts will lead to a major supply shortfall of more than three million bpd in the fourth quarter. This alone is enough to push oil prices higher.

It’s no wonder that the Department of Energy just upped its 2024 oil-price forecast from $86 per barrel of Brent crude (the international standard) at the end of August to its current estimate of $95 per barrel on average. JPMorgan Chase expects oil to go even higher. The bank sees a global supply-and-demand imbalance of 1.1 million bpd in 2025, growing to a 7.1 million bpd deficit in 2030. As a result, it expects Brent crude to trade around $150 per barrel by 2026.

Meanwhile, net long speculative positioning in oil (crude+products, options delta+futures) is fast approaching the lowest level since this data began in 2011. The managed money category in the Commitment of Traders report, representing hedge funds, sold about 400 million barrels in the last six weeks. Part of it can be explained by OPEC+ exports going back up since August. But this is largely because they overshot to the downside in August, and they seasonally go back up in September and October. It is not a sign of OPEC+ cheating. When these worthies unwind, the rally will be fast and furious. Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $67.15) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $36.41) is a Buy under $40 for a $100+ target.

Energy Fuels (UUUU – $7.89) reported September quarter revenues grew 275.1% from last year to $10.99 million, essentially right on the $11.02 million estimate. They earned seven cents a share; Wall Street expected a four-cent loss.

There was no conference call, but they have an excellent UPDATED PRESENTATION. They are booking new uranium sales contracts:

Click for larger graphic

Switzerland joins the growing list of nations (France, Belgium, Finland, Romania) planning to extend the operation of their nuclear reactors to continue consuming uranium for 60 to 80 years or longer in order to achieve 24/7 carbon-free energy security and NetZero goals. Uranium demand keeps climbing!

Energy Fuels finished the quarter with $125.16 million in cash, no debt, and $27.66 million in inventory made up of 586,000 pounds of uranium, 906,000 pounds of finished vanadium pentoxide, and 11 million tons of finished high-purity, partially separated mixed REE (Rare Earth Elements) carbonate. They hold an additional 409,000 lbs. of uranium as raw materials and work-in-progress inventory, along with an estimated one to three million pounds of solubilized vanadium pentoxide in tailings solutions that could be recovered in the future.

The stock got a balanced write-up on Seeking Alpha: Trailblazing The Energy Transition With Uranium. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $33.24) owns the largest copper mine in America and the fourth and fifth largest in the world.

Click for larger graphic h/t @WinfieldSmart

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

* * * * *

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

* * * * *

Your reading Doomberg on fission chips Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 11/9/23. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $182.41) – Buy under $150 for new iPhones

Corning (GLW – $27.07) – Buy under $33, target price $60

Gilead Sciences (GILD – $74.98) – Buy under $80, target price $120

Meta (META – $320.55) – Buy under $150, target price $400

SoftBank (SFTBY – $19.75) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $10.71) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $45.70) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $16.39) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $20.70) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $9.49) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.28) – Buy under $13, target price $30+

Velo3D (VLD – $1.32) – Buy under $6, target price $50

$20-for-$1 Biotech

Akebia Biotherapeutics (AKBA – $0.91) – Buy under $2, target $20

Aptose Biosciences (APTO – $3.24) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $5.40) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.37) – Buy under $7, hold a long time

Invitae (NVTA – $0.42) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.39) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.69) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $10.14) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($22.67) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $22.94) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $26.78) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.23) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $23.72) – Buy under $30, target price $50

Coeur Mining (CDE – $2.19) – Buy under $5, target price $20

First Majestic Mining (AG – $4.65) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.33) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.64) – Buy under $10, target price $25

Sprott Inc. (SII – $29.54) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $36,720.55) – Buy

Grayscale Bitcoin Trust (GBTC – $29.09) – Buy

Ethereum (ETH-USD – $2,129.03) – Buy

Grayscale Ethereum Trust (ETHE – $16.32) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $67.15) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $36.41) – Buy under $40; $100+ target

EQT (EQT – $39.41) – Buy under $35; $70 first target

Energy Fuels (UUUU – $7.89) – Buy under $8; $30 target

Freeport McMoRan (FCX – $33.24) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $2*.44) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $21.75) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.09) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $26.82) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.30) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.00) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $0.80) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First!

Repost of my thoughts on TGTX–

JGMD

Reply to Michael Murphy

November 7, 2023 9:24 am

Thanks. I listened to the Nov 1 conference call reporting better than expected sales. At the end, an analyst asked about oral BTK inhibitors. Mike Weiss said that TGTX is perhaps developing a BTK inhibitor, which is considered appropriate for MS at certain stages, a different patient class than for anti CD such as Briumvi or Ocrevus. To me, this is arbitrary. Neither anti CD nor anti BTK drugs address root causes, and are merely great bandaids. Regardless of that, Weiss seemed evasive and uncomfortable, and this analyst suggested that anti BTK drugs are the main risk for Briumvi. They speculated that perhaps one day, oral anti BTK drugs may take away use of anti CD drugs like Briumvi. Earlier in the Q&A, Weiss and Waldman, the marketing chief said that some patients on therapies other than anti CD are switching to Briumvi, a positive. Many TGTX bulls say that Briumvi is THE best drug for MS, but we should research anti BTK and perhaps other classes of drugs which are competition. What do you know at this point?

If all this is true, Weiss may be seeking an exit strategy by selling the company before anti BTK or other drug classes claim preferred status.

More tomorrow. Hint–I’m still bullish, but BTK is a risk factor.

TGTX- So the question is, are there any clinical trials ongoing for BTK inhibitors use for MS? How long before the FDA extends the labels?

Months? Years?

See the above. That’s all I know. I asked MM to research this.

More thoughts after listening a few times to the webcasts of Nov 1 and 6. Another company will report phase 3 on their oral BTK drug by the end of this year. Suppose the results are good. Mike Weiss is honest to say that we don’t know whether BTK drugs will reduce sales for CD20 drugs like Briumvi, Ocrevus, Kesimpta. But I strongly disagree with his assertion that oral drugs taken 1-2x daily are inferior in compliance to a 6 month intravenous (IV) infusion. The industry is pushing that narrative, but come on, every investor should ask the question. For any drug, is it so difficult to remember to take your drug orally every day? Especially for an ultimately fatal condition like MS, you better not miss any dose. (As an aside, I remember many years ago for osteoporosis, oral bisphosphonates like Fosamax/Actonel were recommended. You took the pill first thing in the AM, 45 minutes before eating, to prevent esophageal irritation. Somewhat inconvenient, but not too much to ask. Later, 6 month IV infusions of a similar drug were offered to get around this problem. Today, I see plenty of patients who take the oral drugs, and don’t hear about takers for the 6 month IV version.) So, unless the oral drug causes nausea or other major side effects, I believe that it will be preferred by most MS patients vs the 6 month IV.

The oral BTK drug is being targeted for a different class of MS–primary/ progressive. CD20 drugs like Briumvi/Ocrevus/Kesimpta are targeted for relapsing MS. CD20 can still be used for primary/progressive. If the phase 3 for the BTK is good, then I foresee big competition for Briumvi. TGTX has a BTK in very early stages of development, but there is a significant risk that the other company’s BTK will be a threat to Briumvi. BTW, companies can price oral drugs comparable to IV drugs. Most of the cost of any drug is related to all the R&D, dealing with a politically corrupt FDA, rather than the cost of manufacture. But if the price of an oral BTK is significantly less than IV drugs like Briumvi, that is a significant risk to TGTX shareholders. Still, Ocrevus is a big revenue generator for Roche, and the same will be true of Briumvi for TGTX. This is true in the medium term, but with BTK it is unknown whether it will be a threat to TGTX in the long term. At the current stock price of $10, if BTK turns out to be insignificant, then ultimate targets of $30 to $100 are reasonable. But if BTK becomes significant, then a target of only $20 is possible.

Be careful, build a position in TGTX way below $10.

The absence of snark renders commenting impossible so I must forbear until the snarks returns in the Spring

Do you live in Capistrano?

Someone mentioned NGENF a few weeks ago. Looking for any info

NervGen continues dosing SCI patients and expect to have all 20 in the chronic cohort (1/2 getting placebo) enrolled around the end of the year with data in the 16 week trial to be released mid-2024. Success will send the stock soaring. Failure will kill it. I would buy some now to catch the big upside of 1000% in 9 months, knowing there is a possibility you could lose over 90% of your investment if the drug shows no effect in any of the 10 humans getting the drug. I also consider it likely that word of success could leak out prior to mid-2024. See their quarterly report published yesterday: https://nervgen.com/nervgen-pharma-reports-q3-2023-financial-results-and-operational-updates/

How about ACXP? When do you estimate we get the full analysis of extended time observation on the P2B patients for Cdiff recurrence? If ibeza shows no recurrence and Vanco shows recurrence, I can see a small cash infusion by Big Pharma or other entity, which will boost the stock somewhat. But the big payoff will require P3, which won’t get off the ground with the history of very slow enrollment in P2A and B. Maybe the cash of $9 million is enough for an interim readout on P3, but it could be much longer until recurrence rates are compared for ibeza and Vanco. To me, the stock risks floundering to $1 or less.

What do you think? Thanks.

Thanks for your analysis of TGTX above. I think you are correct. As to ACXP, we should have full data from the recent 2b trial around the end of 2023 (within 2 months). I anticipate a nine figure deal will follow in early 2024, perhaps prior to the end of Phase 2 meeting with the FDA.

Perhaps enrollment in P2A and B were slow due to covid, but covid is mostly insignificant now. But perhaps enrollment was slow because the company didn’t have money for marketing to get patients for the trials. I still regard this as the biggest risk factor for the stock, a huge wild card.

Imagine that, they are selling AC-5!!! Who would have thunk that? I still remember those comments, it’s a turd, no one will buy a start-up’s stuff, etc. .Can you hear me now? Call me a wacko , but I am buying some more tomorrow. RIP Don G. Yes, he was a hell of a guy. My sympathy for all his friends and family.

What are the sales numbers? Be careful. Compared to ARTH, TGTX is a blue chip like Berkshire Hathaway.

Agreed. Would absolutely stay away from ARTH which is now, apparently, once again diluting into oblivion by hitting the ATM. Mind boggling.

TGTX, probably a buy here for when Biotechs recover; it has been almost a 2 and a half year bear market which should be nearly over.

Look at the 5 year charts of XBI and IBB. You will see that the 2.5 year (so far) bear market was preceded by a 2.5 year bull market. Despite where these indices were 2.5 years ago, they are virtually unchanged compared to 5 years ago. 5 years ago the cost of capital was still near zero. That is no longer the case and will be a significant headwind for biotechs going forward. At least 80% of biotechs are pure junk and you have to be a very good stock picker and trader to make money in this arena. Still, the possibilities for windfall gains are out there. I would strongly advise anyone interested in the field to subscribe to Biopub.co which has seen more than its share of 10-baggers in the few years of its existence. Perhaps even more valuable, Biopub gives up on companies when cracks appear in their foundations.

Does biopub follow TGTX, ACXP?

ACXP yes. Followed TGTX years ago when it went from $5 to $50 and then came back to it after FDA delays made it cheap again.

There is far too many losers in this portfolio and too much ink is wasted every week repeating the same old, same old. It is doubtful these companies will survive and if they ever turn a profit (which I doubt) it will be long after we are gone. I would like to see you become credible once again and offer your subscribers real hope. Clean up the junk. Just a thought. Reply Michael.

Totally agree. Why spend a single minute cutting and pasting graphics for companies like INO and NVTA when it’s obvious that both companies are going to zero.

Unfortunately MM can’t simply cut his dogs as that would severely damage his newsletter returns.

Been a very busy couple of weeks for me and just this morning got around to catching up on last week’s Radar Report and comments and this week’s. Couldn’t help smiling at the comments near the top of last week’s by Michael, John Miller and Michael Murphy about Florida. Except for 2 years out of state to learn I hate living in snowy and icy areas, I lived in Dade County for over 60 years. My last day living there was Saturday, November 4. I shed my home and its attached rapacious insurance expense and bought a far better home 5 hours north in the least flood and hurricane prone area in the state.

The intersection of Covid and the Work From Home era brought scads of people from up north to Miami and instability in Haiti, Venezuela, Cuba, Nicaragua continues to bring more from the south (as well as from other parts of the world). Wealthy northerners saw 2020 Miami prices and not only bought a Miami home, but also bought “investment properties” in Miami. However, new residents from the south are limited in what they can earn because more than ever they are failing to learn English as they can get by speaking only Spanish. In a vicious cycle, having to work extra hours to afford the high cost of rent in Miami, these immigrants have less free time to learn English.

As Michael pointed out, if your last name is Trump, Gates, Bezos, Icahn or Brady and your house gets inundated, you will still have plenty of money and your life won’t be ruined. And when a hurricane threatens you can just fly to another state for a week or a month until power gets restored. It won’t matter that airfares are ten times normal because you can have your private jet depart from Opa-Locka, Kendall-Tamiami or Ocean Reef. Even if you have your own generator, you probably don’t want to be among the only people in the city to have electricity. I have talked to so many new residents who respond with “What’s that?” when I ask “Are you prepared for hurricane season?” that I fear there will be masses of unprepared, hungry and desperate people when the next major hurricane arrives.

I have attended unforgettable lectures by climate professors who have shown maps of this peninsula both when it was much fatter and much smaller over the eons. Manatee fossils have been found far from the coast or rivers. They say when the tipping point comes, sea level can rise very rapidly. I have been saying for years that if that happens in my lifetime, my new home will be the new waterfront property and the millions in south Florida who have acclimated to the warm weather will drive up prices here. The beaches, diving and fishing are just depressing to anyone who enjoyed south Florida’s watersports decades ago. Traffic problems will only get worse as taller buildings are popping up even in Coral Gables and the far western and southern reaches of the county and the drinking water from the Everglades is under siege from salt water intrusion. It may look like paradise to people from cold overcrowded cities up north, but in northern Florida you can get similar weather without all the problems of southern Florida.

Thank you for posting about Don Galamage. His absence, as oldster’s and a few others make this board less interesting.

As to ACXP, their quarterly report will be Nov. 14. They have received congratulatory calls from more than one big pharma representative and due to the connections of several Board members will receive attractive offers from several. Their cash situation is not strong, but I don’t think that matters when you have several interested buyers competing with each other for a valuable asset. Their C DIff drug will be worth well over $500M when approved. If ACXP does a deal next year for half that price, that’s 5x from here. The wild card is their MRSA drug.

And thanks to Murphy pointing out 2 or 3 weeks ago that ENVX news which was widely seen as negative was actually a positive, I finally bought my first tranche at $8.59 and also bought 2026 $8 Calls. I sell short-term OTM Calls against my shares and if it appears they may be called away, adjust them to higher strikes at later expirations.

Finally, I love the discussion about socialism, which is found in different degrees in every country in the world. Socialism is an evil if present in the extreme and in absence. The trick is to find the Goldilocks range and try to maintain it.

p.s. the new Speaker of the House is going to crush the Republican party with his ideas on abortion, homosexuality, Social Security and the only part of the U.S. government that makes a profit (the IRS).

Agree that the Republicans are shooting themselves in the foot with their abortion stance. In the 1960’s, Ayn Rand correctly pointed out that Dems want economic control, Repubs want moral control. Both are bad. The ideal is libertarianism, responsible freedom of choice. As for socialism, it is an unstable situation as more and more people see the special interests getting in on the “benefits/freebies” and get politically/emotionally charged to get the “goodies” for themselves. Yes, there is a Goldilocks happy medium, but it is about 10%, not the 40-60% today in the US. In the 1980’s the Asian Tiger countries had rapid growth rates due to their low 10% taxation. Religious traditions figured out a long time ago that 10% tithe is fair. But in the 1970’s, the UK marginal rates skyrocketed to over 90%. The US is in danger of the same, due to political envy as they push 40% to 90+ %.

Aside from hurricanes, high humidity year round in Florida makes the higher prevalence of water damaged homes with ensuing mold a real health hazard. Toxic mold illness is a major cause of chronic fatigue, but mainstream medicine doesn’t recognize it and only recognizes mold allergy, a much less significant illness. Mainstream MD’s merely prescribe drugs for physical and emotional symptoms of chronic fatigue, which don’t help much, while patients continue to suffer. In order to get well, they go outside the socialized medical system and pay lots of money to get well.

Good comments on the Great State of Florida. I did not understand some of the negative commentary on last thread so it is refreshing to hear some hard truths from a long time resident.

Undoubtedly, some of the negativity stems from a large dose of butt hurt that flares up, particularly at tax time for those here living in Blue States having to pay very high rates of State Income Taxes. Hence, the usual memes on hurricanes, rising sea levels, insurance costs etc.

It is a question of choices; hurricanes can be seen and predicted weeks/days in advance with technology now capable of high precision regarding the storm strength and direction. One plans and gets out of the way, making sure of leaving hurricane shutters on windows and doors. Insurance is a problem for sure and sooner or later the State will have to do better than it has in the recent past in offering decent state sponsored policies to residents. Very different from California, where Earthquakes can hit at anytime/anywhere with no warning. Again, I’d rather be exposed to the natural disaster that can be seen and predicted. Admittedly, CA appears to have done a better job on the insurance issue with the CEA, perhaps FL could learn a thing or two from the progressives on that front.

Rising sea levels are simply non-existent. I know, that makes me some kind of Neanderthal, but I have been everywhere up and down the Coast and I visually cannot detect anything, the Atlantic and the Gulf of Mexico continue to be, boringly, at more less the same place for the last 20 years. Seasonal floodings in South Beach and other coastal areas have been there forever and would appear to be unrelated to climate change. Having said that, Florida could eventually re-submerge and go back to where it came from in, say, 100million years or so.

Should the Cumbre Vieja volcano in the Canaries drop in the ocean there could be a 25meter Tsunami hitting FL according to models. It would take 9 hours, enough time to take some action though I am not sure what it would be worse if the wave hitting or 5-10million people panicking all at the same time. I think THAT is the Tsunami risk not some random earthquake in the Atlantic.

Sub-tropical weather and high humidity causing molding and plenty of allergies are probably the worst part about living in FL as noted by JGMD.

Other than that, my recent trips to CA have showed me a pretty subdued, quasi depressed state with old infrastructure full of potholes and ZERO new construction of any kind. Nothing changes in CA anymore a bit like Europe. Contrast that to the boom in Miami with huge infrastructure projects in the middle of the city and a very large number of new buildings just in the last 5-10 years.

Ok .. so you can’t visually detect rising sea levels. That isn’t research, it’s anecdotal.

Real research using things like .. you know .. science disagree.

https://climatecenter.fsu.edu/topics/sea-level-rise

The biggest indicator of problems in Florida is the fact that more than a dozen property insurers have left the state and many more simply won’t write a policy. Ask any Floridian about their property insurance increases.

Actuarial tables don’t lie.

So we will see how fast this happens. It’s totally out of anyone’s control at this point but it is certainly a fact.

Ok, now lets see all the links from nutty climate deniers who also want to label me as a socialist commie 🙂

Well, your very scientific linked document indicates a rise in the Miami area of a whoppy 15cm in the last 31 years, no wonder that, anecdotally, I cannot see anything.

Perhaps there will be an acceleration but at this lethargic pace we are talking about a 22nd Century event and I am not planning to be around.

The Insurance Companies’ situation has my attention and Chris provides a thorough review of some of the issues. There has been a near doubling of premiums for wind damage in the last year and that is totally unacceptable. I know some Committees and State authorities are at work on these issues and, as I already mentioned, they will have to come up with a scheme similar to the CEA that hopefully works.

What is also NOT working is FEMA, a Federal Agency, very involved in the aftermath of Hurricane Ian as most of the damage was from flooding. They are paying extremely slowly and in some cases only after lawsuits have been filed. A disgrace considering the hundreds of billions the US Government has squandered at the same time for the Ukraine and elsewhere around the world.

You are correct that earthquakes are a non-issue in Florida, but hurricanes are still unpredictable. Everyone expected Ian to hit around Tampa Bay last year and it caught Naples and Ft. Myers by surprise. Warming oceans (whatever the cause) have led to rapid intensification increasing so that a relatively storm like Ian went from a relatively mild 115 mph on 9/27 to 160 mph the next day.

To make matters worse, insurance companies routinely slashed amounts paid to insureds which were far below the amounts recommended by the adjusters who were contracted by the insurance companies to evaluate damage.

And adding insult to the insult to injury, this year the legislature gave the green light to insurers to rape their customers further by stripping legal fee awards away from insureds who successfully sue their insurers. Who can afford to fight an insurance company’s refusal to pay what they should pay if their lawyer cannot recover fees from the insurance company? Insurers now have a license to steal. Which is another reason I sold my overvalued home in Miami and paid cash for a much better home in a much lower risk area and will not be required to carry worthless windstorm insurance as I now have no mortgage.

and one more thing, the last time a major hurricane appeared to be heading to Miami, there were huge traffic jams and no hotel rooms available for anyone trying to drive out of the area. And don’t forget, airports close down hours before hurricanes may be arriving.

Agreed. Not only airports close but Airlines fly out all the planes they have on the tarmac so even a couple of days before the storm hits there are very few flights left.

Yours are all good points, hurricanes are extremely dangerous. I just wanted to emphasize that with the NOAA website and plenty of other weather services online, one can get a pretty good idea of the risks of staying put and, if necessary, get out of Dodge before the freeways get too crowded.

All insurance businesses stink for the customer, but the thieving management does well. Medical insurance is an ongoing fraud. Regulations don’t work, as insurance execs know how to maximize premiums and minimize payouts through exclusions in coverage, delays, etc. The business model of insurance companies is similar to socialism. The beneficiaries scheme to use other people’s premium money. All the same crap, whether the govt or private entities do it.

Could you explain the MRSA drug (wild card)

Hi Chris any advice on northern Florida areas/ cities that you would recommend?

MM–statement from VLD–

“Additionally, we have also implemented new go-to-market and service strategies to rebuild our bookings and backlog pipeline which came in below our plan for the third quarter. With the early success of these programs, we expect to resume bookings growth in the fourth quarter for fiscal year 2024 deliveries.”

What the heck are “go-to-market and service strategies”?–sounds like promotional BS to me. Now that backlogs are gone for the 4th quarter, it looks bad. Never mind bookings GROWTH. Q4 could have much lower sales. There have been consistent 3 quarters of sales declines.

VLD continues to remain on MM’s Near-term list but should be taken off as the reasoning no longer applies and hasn’t for a while now.

VLD Velo3D – Rapid revenue growth; low market cap

MM could possibly point to YoY revenue growth through Q3, rather than this year’s QoQ declining revenue, but with Q4 guidance we are almost guaranteed a double digit drop in both yearly & quarterly comparisons.

With minimal backlog (~$2M), they went out of their way on the call to avoid mentioning a specific number, VLD is likely in for several rough quarters until they can establish a backlog cushion again. The rapid revenue growth story is history for now.

VLD did well on Fri, 2 days after releasing their terrible Q4 sales estimates of $15-27 million, below the $29 million consensus. Perhaps all this bad news is already discounted in the stock price, although tax selling could cause declines from here.

MM–please answer my question about “go-to-market and service strategies.”

VLD just filed a notification of late filing for their 10-Q with the following reason given:

Subsequent to the Earnings 8-K referred to below, in connection with the preparation of its Quarterly Report on Form 10-Q for the quarter ended September 30, 2023 (the “Quarterly Report”), Velo3D, Inc. (the “Registrant”) determined that approximately $200,000 of revenues previously reported in the Earnings 8-K should have been deferred. As a result, the Registrant expects that it will not satisfy the minimum revenue covenant for the quarter ended September 30, 2023 in the Registrant’s senior secured convertible notes due 2026 (the “Notes”) when the Registrant finalizes its condensed consolidated financial statements as of and for the periods ended September 30, 2023 in connection with the filing of the Quarterly Report, which, if not waived, would result in an event of default under the Notes and allow the holders of the Notes to declare the Notes due and payable in cash in an amount equal to the Event of Default Acceleration Amount (as defined in the Notes). Since discovering the issue, the Registrant has been negotiating a proposed amendment to the Notes with the holders thereof, although the Registrant does not expect that a waiver or an amendment will be obtained prior to the extension period provided for within Rule 12b-25. As such, the Registrant will present the debt as current on the consolidated balance sheet and will include disclosure that the Company has substantial doubt about its ability to continue as a going concern. The Company expects to continue discussions with the holders of the Notes subsequent to filing the Form 10-Q; however, the Registrant may not be able to obtain a waiver or an amendment on favorable terms or at all. If a waiver or amendment is not agreed to by the holders of the Notes, the Registrant does not have sufficient capital to satisfy the outstanding principal and interest due.

As a result of those negotiations and other related matters that have required the attention of senior management and other key personnel, the Registrant could not, without unreasonable effort or expense, complete the Quarterly Report within the prescribed time period. The Registrant plans to file the Quarterly Report within the extension period, in compliance with Rule 12b-25.

JOHN FLEMING,

Northwest corner of Florida: Pensacola (the redneck Riviera) has about 200,000 people in the county. The Naval Air Station there is the home of the Blue Angels.

Just east of there is Eglin Air Force Base and the city of Niceville where I have a few friends. Some love it, others not.

Next is Panama City (pop. 20,000) with a beautiful white sand beach that fills up with spring breakers.

Further east is the capitol, Tallahasse, also in the Central time zone and home of FSU.

Further east is Lake CIty near the junction of I-10 and I-75 and so an important industrial hub.

Continuing east another hour, you’ll get to Jacksonville, the biggest city in north Florida. The St. Johns River runs north from near Orlando to the ocean through J-Ville, which has 2 big industries: Finance/Insurance and the Baptist Church. The Church buys up liquor licenses and doesn’t use them so the city has few fun spots, but Jville beach is really nice (Tim Tebow IS Jacksonville).

About an hour south is St. Augustine, a great place to visit. A NJ friend of mine who went to college at Flagler College there recently moved there after practicing law several decades in south Florida.

About another hour south is Daytona/Ormond Beach. A dentist buddy moved there a few years ago when he realized Miami was not a place for a non-spanish speaking dentist.

Going west from there far from the coasts is Ocala, the horse capital of the USA

Less than an hour north of Ocala is Gainesville, from whence came Tom Petty and the Heartbreakers and Don Felder in blue Alachua County, and home to UF which USNews called the #1 public U in the USA.

An hour south of Ocala and still far from the coasts is Orlando which is too crowded for me since it boomed after Disney opened there 50-some years ago, but that’s more central Florida and in the lower lying regions like the coasts

Thank you for the information. I appreciate it.

ACXP–moderately disappointing update this AM. Enrollment in Phase 2b was stopped Oct 2. Monitoring for CDI recurrence will be for 94 days after that, I guess. It is well known that Vanco recurrence rate is 20-40%, but I don’t know how long it usually takes to see the recurrence. Will 94 days allow enough time to observe comparative recurrence rates between Ibeza and Vanco, especially in only 16 Ibeza/14 Vanco patients? Ibeza has a theoretical advantage for lower recurrence rates because of superior microbiome and bile acid parameters.

The stock looks very vulnerable while we wait another 50 days for the extended monitoring, and maybe another 10 days to report the results. Even then, recurrences might not be seen in the 94 day period. Optimistically, suppose we see 3 recurrences in the 14 Vanco patients (20%) and 0 recurrences in the 16 Ibeza patients. Will that impress a big Pharma to buy ACXP or at least partner for the phase 3 trial? We might see only 1 recurrence for Vanco and 0 for Ibeza, since the 100% short term cure for Vanco was much better than the usual 81% cure. That will be considered a statistically insignificant difference between Ibeza and Vanco, phase 3 could be cancelled, and ACXP will plunge to pennies from $3 now. Or, the rights to develop Ibeza might be worth $1 to a big Pharma to fund a phase 3 on their own.

Chris?

VLD – Notification of Late Filing (SEC Form 12b-25) issued today: