Dear New World Investor:

Bloomberg said the tailwind from surging immigration would boost March quarter GDP.

Click for larger graphic

Click for larger graphic

Oops. Real GDP only grew at 1.6%, short of all estimates including the Atlanta Fed’s GDPNow +2.7%. Could it be that housing massive illegal immigration from South America, Asia, and the Middle East in luxury hotels isn’t really good for the economy?

Click for larger graphic

Click for larger graphic

To be fair, the growth details were better than the headlines, although the inflation data was slightly hotter than I expected. The headline number was mainly driven by weakness in volatile components, especially net exports. Private domestic final purchases, the “core GDP” of consumption and fixed investment, grew a strong 3.1%.

Click for larger graphic h/t @ernietedeschi

Click for larger graphic h/t @ernietedeschi

Consumption was above expectations, business investment was below expectations, and overall private sector activity remains pretty strong. Part two of the Fed’s dual mandate – full employment – is on track.

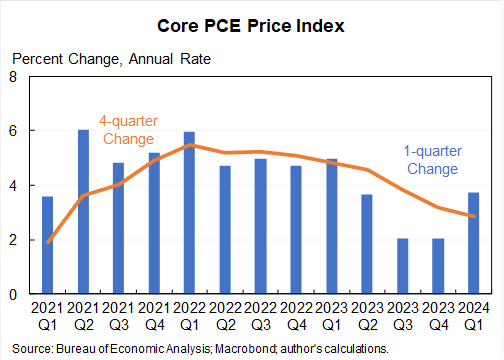

But part one, lower inflation, was not. We get the final March Personal Consumption Expenditures Index number Friday morning and it is not likely to be much different from the one released today in the GDP report. Core PCE rose at an annual rate of 3.7% during the March quarter, faster than the 2.9% reported for last year’s March quarter and the 2.0% in the December quarter, and above the consensus estimate for 3.4%.

Click for larger graphic h/t @jasonfurman

Click for larger graphic h/t @jasonfurman

Bottom line: The real side of the economy remains healthy but the nominal side is too hot. Overall that is not a bad place to be, but also not a place where the Fed will need to cut rates anytime soon. Inflation remains sticky and paused – maybe reversed – its clear trend lower. The Fed will stay on hold at next Wednesday’s meeting.

The futures market is still pricing a first rate cut in September, but the probability is down to 58%. I’m not quite ready to give up on my forecast of a mild recession starting this year, but it won’t take much more to convince me that this is the first time in 56 years the leading indicators fell below -5% without being in a recession.

Click for larger graphic h/t @DiMartinoBooth

Click for larger graphic h/t @DiMartinoBooth

Stocks should get a bid tomorrow because the buyback blackout ends Friday. Goldman Sachs wrote: “On the authorization front, 2024 YTD authorizations stand at $317.4B vs $377.0B 2023 YTD authorizations. We expect to see authorizations this year finish higher, estimating 2024 authorizations to finish $1.15T (up ~16%).”

Click for larger graphic h/t @zerohedge

Click for larger graphic h/t @zerohedge

Market Outlook

Even after today’s intraday drop below 5,000, the S&P 500 added 0.7% since last Thursday. The Index is up 5.8% year-to-date. The Nasdaq Composite eked out a 0.1% gain and is up just 4.0% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 1.5%. It is down 7.9% year-to-date as the biotech winter continues. The small-cap Russell 2000 gained 2.0% but still is down 2.3% in 2024.

The fractal dimension stopped the consolidation for the moment, but this probably is not a renewed uptrend. The fractals still are so low that they need many weeks of consolidation to build up the energy for another upleg. Don’t be panicked out by drops like last week – markets can consolidate by periodic price reversals, sometimes sharp, or the passage of time. Or, most likely in this case, both.

Top 5

Changes this week: Added ABCL to Long-Term

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements at June WWDC and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, April 26

Personal Consumption Expenditures Index – 8:30am

Sunday, April 28

SCYX – ScyNexis – 7:30am – Oral presentation on SCY-247 at the European Congress of Clinical Microbiology and Infectious Diseases (ECCMID)

Monday, April 29

SCYX – ScyNexis – 6:00am – 2 Poster presentations on SCY-247 at ECCMID

Tuesday, April 30

GLW – Corning – 8:30am – Earnings conference call

PYPL – PayPal – 8:30am – Earnings conference call

Wednesday, May 1

Fed Meeting – 2:00pm press release; 2:30pm press conference

CDE – Coeur – After the close – Earnings release; call tomorrow

FSLY – Fastly – 4:30pm – Earnings conference call

ENVX – Enovix – 5:00pm – Earnings conference call

Thursday, May 2

CDE – Coeur – 11:00am – Earnings conference call

GLW – Corning – 12:00pm – Annual meeting

SAND – Sandstorm – After the close – Earnings release; call tomorrow

AAPL – Apple – 5:00pm – Earnings conference call

Friday, May 3

April payrolls – 8:30am

SAND – Sandstorm – 11:30am – Earnings conference call

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $169.89) reports next Thursday after the close. Wall Street expects revenue to all 4.5% from last year to $90.6 billion with $1.51 earnings per share.

Morgan Stanley wrote: “We expect a March Q beat and a well-telegraphed June Q guide down, but with the stock at $165 we’d argue this is largely priced in.” They maintained their Overweight rating but trimmed their target price from $220 to $210.

According to data from Consumer Intelligence Research Partners, Apple’s shares of smartphone activations fell to 33% in the most recent quarter in the US, down from 40% in the 12 months ended March 2023. Google’s Android accounts for roughly two-thirds of all U.S. activations. They wrote: “In some respects, the current one-third share represents a return to a much earlier time. Six years ago, Apple iPhone captured a similar share of activations. Then, operating systems beyond iOS and Android, including Blackberry and even some Windows phones controlled a portion of the smartphone market. Apple’s share increased steadily until the first year of the COVID-19 pandemic and has now returned to the historic level of about one-third iPhone, two-thirds Android.”

Apple TV+ is about to sign a deal with FIFA for a new World Cup-like soccer tournament to be played in the US between June 15 and July 13, 2025. The new tournament was initially supposed to be held in China in 2021, but was scrapped because of the pandemic. The traditional World Cup will take place in 2026 in the US, Mexico, and Canada, from June 11 to July 19.

Beginning in May, Made for Business, a special Today at Apple series, will offer small business owners and entrepreneurs free opportunities to learn how Apple products and services can support their growth and success. Led by small business owners, the sessions will highlight how these organizations have used Apple products such as iPhone, iPad, and Mac, along with resources such as Apple Business Connect, Apple Business Essentials, and Tap to Pay on iPhone, to reach customers in new ways and build their businesses.

According to a survey by Ming-Chi Kuo, the highly-respected Apple analyst, Apple is expected to ship only 400,000 to 450,000 2024 Vision Pro units during 2024-25. That is nearly half the market consensus expecting 700,000 to 800,000 units shipped during the two-year time frame.

He wrote: “Apple is reviewing and adjusting its head-mounted display product roadmap, so there may be no new Vision Pro model in 2025…Apple now expects Vision Pro shipments to decline year over year in 2025.”

The survey points to several issues regarding mixed reality headsets such as the Vision Pro, including the dearth of applications, the $3,499 price, and headset comfort. All three of those factors will steadily get better as time goes by, and I still expect Vision Pro to be a success. AAPL is a Buy under $175 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $31.35) report March quarter results Tuesday morning. The consensus of analysts expects revenues to fall 7.4% from last year to $3.12 billion with earnings down 14.6% to 35¢ a share. June quarter guidance is expected to be for revenues down 4.3% from last year to $3.33 billion but earnings only down a penny to 44¢.

Corning’s excellent cost control gives them substantial earnings leverage as revenues pick up. Management says they can do $3 billion more in revenues from their current factory capacity without increasing general and administration expenses.GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

Gilead Sciences (GILD – $65.27) reported March quarter results after the close today. Revenues rose 5.4% from last year to $6.69 billion, beating the $6.34 billion estimate. Biktarvy sales increased 10% year-over-year to $2.9 billion. Oncology sales increased 18% year-over-year to $789 million.

Click for larger graphic h/t @seekingalpha

Click for larger graphic h/t @seekingalpha

They closed the CymaBay acquisition, which resulting in a one-time $3.9 billion Acquired In-Process R&D Charge that knocks $3.14 off their diluted earnings per share. They reported a pro forma loss of $1.32 per share, better than the $1.49 loss estimate. (Excluding this charge, pro forma diluted earnings would have been $1.82 per share, above expectations.) For the full-year, Gilead now expects reported pro forma earnings per share of $3.45 to $3.85, a slightly-more than $3.14 reduction from their previous guidance for $6.85 to $7.25.

On the conference call (PREPARED REMARKS HERE and SLIDES HERE and TRANSCRIPT HERE), management said they have filed for regulatory approval of CymaBay’s seladelpar as a treatment for primary biliary cholangitis with both FDA and EMA. They expect an FDA decision in August and the EMA to follow early in 2025. CymaBay should be breakeven in 2025 and accretive from 2026 on. They have an inflammation pipeline:

Click for larger graphic

Click for larger graphic

They are hitting their 2024 milestones:

Click for larger graphic

Click for larger graphic

In the quarter, they generated $2.2 billion in operating cash flow, paid $990 million of dividends, and bought back $400 million of stock. They ended the quarter with $4.7 billion in cash. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $441.38) reported a double beat for the March quarter. Revenue rose 27.3% (!!!) from last year to $36.46 billion, just above the $36.22 billion estimate. Earnings per share hit $4.71, well above the $4.32 estimate. Until recently, the consensus was at $34.00 billion and $4.06.

Family daily active people (DAP) was 3.24 billion on average, an increase of 7% year-over-year. Ad impressions increased by 20% year-over-year. Average price per ad increased by 6% year-over-year.

On the conference call (PREPARED REMARKS HERE and SLIDES HERE and TRANSCRIPT HERE), Zuckerberg, the king of under-promising, forecast June quarter revenue of $36.5 billion to $39.0 billion. The midpoint of $37.75 billion is up 24.1% from last year but below the consensus for $38.3 billion, so the weak hands did what Wall Street wanted them to. The stock was down as much as 16.0% today before closing down $52.12 or 10.56%.

Meta expects full-year expenses of $94 billion to $99 billion due to “higher infrastructure and legal costs.” Full-year capital spending is forecast at $35 billion to $40 billion, up from the previous forecast of $30 billion to $37 billion “as we continue to accelerate our infrastructure investments to support our artificial intelligence roadmap.” RD spending continues at a high level:

Click for larger graphic

Click for larger graphic

Wall Street pretends to worry about Meta’s expense levels, but one slide shows that’s nonsense:

Click for larger graphic

Click for larger graphic

Meta has started rolling out its free AI assistant across WhatsApp, Instagram, Facebook, and Messenger. Zuckerberg says it’s the most intelligent AI assistant you can freely use – it can answer questions and create images and animations. Llama 3 models will soon be available on AWS, Databricks, Google Cloud, Hugging Face, Kaggle, IBM WatsonX, Microsoft Azure, Nvidia NIM, and Snowflake, and with support from hardware platforms offered by AMD, AWS, Dell, Intel, Nvidia, and Qualcomm. Watch out, OpenAI!

On the conference call, Zuck said: “Overall, I view the results our teams have achieved here as another key milestone in showing that we have the talent, data and ability to scale infrastructure to build the world’s leading AI models and services. And this leads me to believe that we should invest significantly more over the coming years to build even more advanced models and the largest scale AI services in the world…Realistically, even with shifting many of our existing resources to focus on AI, it will still grow our investment envelope meaningfully before we make much revenue from some of these new products.”

That might be bad news if a company was just throwing a Hail Mary pass to catch up in AI. But who really has the compute power to effectively use AI?

Click for larger graphic h/t @learnbiotech

Click for larger graphic h/t @learnbiotech

If the TikTok ban becomes law, in about a year Meta, Google, and Snap stand to gain the most. Although data from Sensor Tower shows a 4% year-over-year decline for time spent on TikTok per daily average user, probably due to the success of Meta’s Reels and YouTube’s Shorts, it still surpasses its rivals. Even with that decline, the average TikTok user still spent about 80 minutes per day on the video shorts platform. Meanwhile, the average daily user on Meta’s Facebook and Instagram spent 60 minutes and 45 minutes, respectively. A survey by TD Cowen found that if TikTok was banned, 28% of TikTok users would shift their time to Reels, while 22% would shift to YouTube Shorts – already my 16-year-old’s favorite.

During the quarter Meta bought back a whopping $14.64 billion of stock and paid $1.27 billion in dividends. META is a Buy under $345 for a $400 target in 2024.

PayPal Holdings (PYPL – $64.10) reports next Tuesday morning at the same time as Corning. Analysts want to see revenues up 6.7% from last year to $7.51 billion with earnings up 4.3% to $1.22 a share. It’s always difficult with a turnaround to pick the exact quarter that success will be obvious to Wall Street, but it’s easy to forecast what will happen when it does: A big jump in the stock price. PYPL is a Buy under $68 for a double in three years.

Small Tech

Enovix (ENVX – $5.84) reports March quarter results after the close next Wednesday. Analysts expect $3.87 million in sales and a 29¢ loss per share. June quarter guidance is expected to be $4.08 million and a 22¢ loss.

What will be important is an update on completing Fab2 in Malaysia and progress on their sales pipeline. CEO Ajay Marathe has scheduled an Ask Me Anything for May 6, so I suspect he has solid news to report. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Fastly (FSLY – $12.40) also reports after the close on Wednesday. Wall Street expects revenues up 13.2% from 2023 to $133.11 million with a six-cent per share loss, less than last year’s nine-cent loss. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

PagerDuty (PD – $20.20) announced their 2024 “ PagerDuty On Tour” event series starting May 22 in New York City, then San Francisco, London, Tokyo, and Sydney. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Rocket Lab USA (RKLB – $3.65) successfully deployed two satellites to two completely different orbits on Wednesday with one Electron mission – its 47th. The capability to deploy two satellites more than 310 miles apart on the same launch is enabled by Electron’s Kick Stage, a small stage with engine relight capability to enable last-mile delivery.

After deploying the first satellite, Electron’s Kick Stage completed multiple in-space burns of its Curie engine to raise its apogee and circularize its orbit before deploying the second one. The Kick Stage then completed a fourth and final engine light to perform a deorbit maneuver that returned the stage closer to Earth to speed up its eventual deorbit, helping to reduce long term orbital debris.

This was Rocket Lab’s fifth launch of 2024, continuing Electron’s streak as the United States’ second-most frequently launched rocket annually. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $0.23) fired their Chief Marketing Officer. The acting CFO is leaving next week to be replaced by a new CFO, Hull Xu. He has been CFO of Cepton and holds an MBA from UC-Berkeley, an MS in Electrical Engineering from Stanford, and a BS in Electrical Engineering from the UC-Davis. VLD is a Buy up to $1 for my $10 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $3.63) is my latest addition to the long-term Top Buys. @Biotech2k1 wrote: “They blend a lot of the old school with some of the new school to make the first logical step in using technology to improve the antibody discovery process. They use mice and other older approaches by injecting proteins. The mice make antibodies toward those proteins. Then they sequence those antibodies and use that data for their machine learning. They use the algorithms to help them model the antigen/antibody binding. They can even use it to predict best antibodies for a specific target. This makes them somewhat TechBio, but not completely. That is one of the reasons I chose to go with ABSI [Absci Corp.]. It’s more risk, but it’s more transformative.”

I certainly agree with that “more risk” comment. AbCellera is much further along in partnering, has more cash, and is severely undervalued. Over the next 10 years they will steadily transform into a biotech royalty company with large free cash flow and a high dividend payout. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Invitae (NVTAQ – $0.01) will be sold to Labcorp (LH) for $239 million plus “other non-cash consideration.” Invitae has not filed an 8-K yet. Labcorp reported earnings today and filed an 8-K but not yet a 10-Q that might have more details. The Labcorp press release said: “Upon completion, Labcorp expects this transaction would generate approximately $275-$300 million in annual revenue…” so they got an amazing deal if this wiped out all the debt. A hearing for court approval is set for May 6.

I expect the current shareholders get nothing, but we won’t know for sure until the 10-Q. Hold NVTAQ.

Primary Risk: Current shareholders don’t own any of the restructured company.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: NM

Medicenna (MDNAF – $1.40) will present two abstracts, including an oral podium presentation, at the annual meeting of the American Society of Clinical Oncology (ASCO). The oral podium presentation on June 3 will include new clinical data from the ongoing Phase 1/2 ABILITY-1 Study evaluating MDNA11 as both a monotherapy and in combination with Keytruda in patients with advanced or metastatic solid tumors. Buy MDNAF under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2024

Probable time of next financing: March 2024

ScyNexis (SCYX – $1.47) presents SCY-247 data at the European Congress of Clinical Microbiology and Infectious Diseases (ECCMID) this Sunday and Monday. It looks like another antifungal winner. As soon as GSK announces a qualified supplier for ibrexafungerp, which I expect to happen by the end of June, SCYX will soar.

In the 10-K filed today, ScyNexis said: “In response to the hold on clinical studies of ibrexafungerp by the FDA due to possible beta-lactam cross contamination, we have entered into certain new manufacturing agreements with third-party contract manufacturers to begin producing new batches of ibrexafungerp which we believe will allow us to lift the clinical hold and restart our impacted clinical studies, the Phase 3 MARIO study and a Phase 1 lactation study.”

That sound you hear is the fat lady singing. The wait is over, folks. Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2024

Probable time of next financing: Never

TG Therapeutics (TGTX – $13.91) said the VA awarded it a national contract listing Briumvi as a preferred therapy for multiple sclerosis. Buy TGTX under $12 for a target price in a buyout of $30 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,344.60) backed off a bit from the $2,400 level but seems solidly bid over $2,300. The lack of Fed cuts normally is a strong negative, but global markets are sniffing out persistent inflation with an unsustainable Federal deficit and escalating debt. The fractal dimension paused the trend, but I doubt this is a real reversal to consolidation already. Next week’s Fed meeting could put it back on track.

Miners & Related

Coeur Mining (CDE – $4.82) reports after the close next Wednesday, with a conference call Thursday morning. Wall Street expects robust 19.5% growth in revenues to $223.8 million with the loss cut from last year’s 11¢ to four cents a share. CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.49) reports after the close next Thursday, with a conference call Friday morning. It should be a great quarter. The consensus expects sales to fall 17.5% from 2023 to $41.27 million. That should be easy to beat. They also expect earnings per share to fall from lat year’s nine cents to just two cents a share. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $64,973.50) has steadied after the halving. Barring a quick dump to clean out the weak hands, I expect a steady run to $100,000 over the next six to twelve months.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $36.86) is the easiest Buy for the 2028 and 2032 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $83.77

Today’s Energy Information Administration report of a massive crude draw of 6.4 million barrels was a full 50% more than I expected. Also, US shale production is rapidly shifting away from oil to natural gas liquids. The oil weighting in US shale oil producers is dropping at an alarming rate as Permian players become gassier and gassier. Diamondback Energy, one of of the best producers in the Permian, is a great example of this with oil weighting dropping from 74% in 2017 to 59% in 2023.

In 2008, the S&P 500 was almost 16% Energy. By 2020, it was down to 2%. Today, it’s still just 3%. This uptrend is just getting started

Click for larger graphic h/t @allstarchart

Click for larger graphic h/t @allstarchart

How important is a strategic oil reserve? China is building theirs while the Biden Administration drew ours down to try to reduce gasoline prices.

Click for larger graphic h/t @AndreasSteno

Click for larger graphic h/t @AndreasSteno

The July 2026 Crude Oil Futures (CLN26.NYM – $70.66) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $40.75) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $12.03) will report March quarter results at their annual meeting next Wednesday afternoon. The two analysts with revenue estimates are at $464.05 million and $482.71 million. The average of $473.38 million is up 17.4% from last year. The earnings per share average of three analysts is 84¢, ranging from 72¢ to 91¢. Last year Vermilion reported $1.72. VET is a buy under $11 for a target price of $24 or more.

Primary Risk:Oil prices fall.

EQT (EQT – $40.41) reported revenue down just 9.0% from last year to $1.72 billion, a touch above the $1.59 billion estimate. They controlled costs and reported 82¢ earnings per share, much better than the 65¢ estimate. As I said last week, EQT is a very well-managed company and should be able to do a little better than expectations. Their total sales volume of 534 billion cubic feet equivalent was towards the high end of their guidance, adjusted for curtailments. They showed continued operational efficiency gains and strong well performance.

Click for larger graphic

Click for larger graphic

On the conference call (SLIDES HERE and TRANSCRIPT HERE), CEO Toby Rice said: “Last month, we announced our agreement to acquire Equitrans Midstream, a transaction that will transform EQT into America’s first vertically integrated large-scale natural gas business. As we described in our conference call last month, this deal catapults EQT to the absolute low end of the North American natural gas cost curve, providing free cash flow durability in the low parts of the commodity cycle, while simultaneously unlocking unmatched price upside by mitigating defensive hedging needs, thus providing investors with peer-leading risk-adjusted exposure to natural gas prices.

“This combination is anticipated to drive our long-term, free cash flow breakeven price to approximately $2 per million Btu, which is 75¢ below the peer average and $1.50 below the marginal cost of supply in the Haynesville. This gap between EQT and both average and marginal natural gas producers is a sustainable advantage, which is rare to find among any commodity business and ensures EQT is best positioned to create through-cycle value for shareholders, while other producers are forced to either chase commodity prices with the drill bit in a similar fashion to what has led to historical industry value destruction or defensively hedge a significant amount of production, thus limiting the ability to capture value in the upcycle.”

They have built a free cash flow machine with less sensitivity to natural gas prices:

Click for larger graphic

Click for larger graphic

They’ve done this by relentlessly driving down their costs and capturing transmission revenues:

Click for larger graphic

Click for larger graphic

Their 2024 guidance shows good cash flow even at low gas prices with dramatic upside to the higher prices coming.

Click for larger graphic

Click for larger graphic

In a follow-up conversation on CNBC, Toby said: “…this AI revolution is only going to take place with affordable, reliable clean energy.”

AI power demand is estimated to reach 75 gigawatts, the equivalent of meeting enough power to power an additional 15 New York Cities, he said. “This is a massive opportunity here.”

Click for larger graphic

Click for larger graphic

Those 75 gigawatts of new power demand would amount to an incremental 13 billion cubic feet a day of natural gas. In addition, he said that the market in the future will call for significantly greater amounts of natural gas through demand from liquefied natural gas growth – an incremental 15 billion cubic feet a day, or a 15% increase in natural gas demand. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $5.36) is acquiring Australian miner Base Resources (ASX: BSE) in an A$375 million cash and stock deal. The key asset is Base Resources’ Toliara project in Madagascar, a world-class, advanced-stage, low-cost, and large-scale heavy mineral sands project. In addition to its stand-alone ilmenite, rutile (titanium), and zircon (zirconium) production capability, Toliara also contains large quantities of monazite, which is a rich source of the “magnet” rare earth elements used in electric vehicles and a variety of clean energy and advanced technologies.

The monazite can be recovered as a byproduct of ilmenite and zircon production at low incremental cost of production that will be globally competitive and position Energy Fuels to be a first-tier rare earth element oxide producer. It will also provide material quantities of low-cost uranium.

The CEO said: “The transaction will not only secure a world-class project for Energy Fuels at a highly attractive acquisition price compared to the fundamental value of the Project but will also secure a mine development and operations team with a successful track-record of designing, constructing, and profitably operating a world-class heavy mineral sands operation in Africa.”

The company said they are currently engaged in high-level discussions with numerous US government agencies and other offices who provide financial support for critical mineral projects within the US and internationally, which may include grants, low-interest debt, non- or limited-recourse debt, loan guarantees, and other support vehicles. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $49.40) reported a good March quarter. With revenues up 17.3% from last year to $6.32 billion, clobbering the latest consensus estimate for $5.7 billion, which was up from $5.33 billion. The also beat on the bottom line with pro forma earnings of 32¢, well ahead of the 28¢ estimate (recently revised up from 25¢).

Click for larger graphic

Click for larger graphic

They produced 1.085 billion pounds of copper, 549,000 ounces of gold, and 18 million pounds of molybdenum in the quarter:

Click for larger graphic h/t @seekingalpha

Click for larger graphic h/t @seekingalpha

And they sold all the production plus 23 million pounds of copper, 19,000 ounces of gold, and two million pounds of molybdenum from inventory.

Click for larger graphic

Click for larger graphic

Their average realized price was $3.94 per pound for copper, $2,145 per ounce for gold, and $20.38 per pound for molybdenum. Their average unit net cash cost of copper was $1.51 per pound in the quarter and is expected to average $1.57 per pound for the full year.

On the conference call (SLIDES HERE and TRANSCRIPT HERE) they guided sales in the June quarter slightly lower at 1.0 billion pounds of copper, 500,000 ounces of gold, and 21 million pounds of molybdenum.

Click for larger graphic

Click for larger graphic

For the full year they guided for 4.15 billion pounds of copper, 2.0 million ounces of gold, and 84 million pounds of molybdenum. I expect substantially higher prices for copper and gold, so it will be a strong year. Over the last 2 years, Freeport has beaten earnings estimates 75% of the time and beaten revenue estimates 88% of the time.

Click for larger graphicClick for larger graphic

Click for larger graphicClick for larger graphic

Copper prices have increased sharply since the end of the first quarter. The copper shortage is here. On the conference call, management said: “Copper producers, including us at Freeport, have been citing physical market tightness for some time. And in the last several weeks, the copper price has risen to reflect the reality of the market situation. Based on historical periods of above trend growth in demand, we may be in the early stages of a repricing for long-term copper prices…We’re not predicting where prices will go from here, and recognize there will be volatility. But clearly, the fundamentals point to an extended period of deficits and significantly higher copper prices over the long term. That’s very positive for a company like ours with large-scale, long-life producing assets and organic development opportunities.”

Click for larger graphic

Click for larger graphic

Freeport has lots of leverage to copper prices:

Click for larger graphic

Click for larger graphic

China is stockpiling everything from copper to oil to nickel to iron ore. That’s what you do AHEAD of a currency devaluation, even though it makes no economic sense. China is preparing something major.

Click for larger graphic h/t @AndreasSteno

Click for larger graphic h/t @AndreasSteno

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

International & Other Recommendations

As I said above, China may be about to devalue even though it makes no economic sense, so we have to step aside on all the China-related recommendations for now. Sell EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $32.53), KraneShares Bosera MSCI China A Share Fund (KBA – $21.61), Morgan Stanley China A-Share Closed-End Fund (CAF – $12.07), and KraneShares CSI China Internet Exchange-Traded Fund (KWEB – $28.01).

* * * * *

RIP Calvin Keyes

* * * * *

Click for larger graphic

* * * * *

Your wondering if I’ll watch Channel 1 Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 4/25/24. Check out the complete Portfolio page HERE.

Portfolio Protection

June 21 SPY $505 put (SPY240621P00505000 – $8.46)

June 21 SPY $410 put (SPY240621P00410000 – $0.44)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $169.89) – Buy under $175 for new iPhones

Corning (GLW – $31.35) – Buy under $33, target price $60

Gilead Sciences (GILD – $65.27) – Buy under $80, target price $120

Meta (META – $441.38) – Buy under $345, target price $400

PayPal (PYPL – $64.10) – Buy under $68, target price $136

SoftBank (SFTBY – $24.55) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $5.84) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $54.18) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $12.40) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $20.20) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $13.13) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.65) – Buy under $13, target price $30+

Velo3D (VLD – $0.23) – Buy under $1, target price $10

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.63) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.33) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.16) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $7.86) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $10.12) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.40) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.47) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $13.91) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($27.39) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $27.02) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $32.81) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $21.66) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $31.76) – Buy under $30, target price $50

Coeur Mining (CDE – $4.82) – Buy under $5, target price $20

First Majestic Mining (AG – $6.94) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.44) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.49) – Buy under $10, target price $25

Sprott Inc. (SII – $40.11) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $64,973.50) – Buy

iShares Bitcoin Trust (IBIT – $36.86) – Buy

Ethereum (ETH-USD – $3,156.19) – Buy

Grayscale Ethereum Trust (ETHE – $22.55) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $70.66) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $40.75) – Buy under $40; $100+ target

Vermilion Energy (VET – $12.03) – Buy under $11; $24 target

EQT (EQT – $40.41) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.36) – Buy under $8; $30 target

Freeport McMoRan (FCX – $49.40) – Buy under $44; $65 target within two years

Other Recommendations

Acreage Holdings (ACRDF – $0.38) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.05) – Buy under $1.30; long-term hold

Hold

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.18) – Hold for buyout

Invitae (NVTAQ – $0.01) – Hold for April 17 auction

Sell

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $32.53)

KraneShares Bosera MSCI China A Share Fund (KBA – $21.61)

Morgan Stanley China A-Shares Fund (CAF – $12.07)

KraneShares CSI China Internet ETF (KWEB – $28.01)

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

The government is finally having an in your face moment with all its spending. The reality now is it is becoming difficult to find buyers of our debt even as our treasury is trying to flood the the market with mega issues of our paper instruments!!!

Naw. The FED will just print into oblivion. Got BTC?

Yes, got that too, and ETH. MM and others are saying it’s going over $100k.

It’s starting to look like Powell has decided to be the adult in the room to force lower deficits. Interesting times.

MM–VLD. Please answer the financial questions asked by taos_red and me on the last board. You just gave superficial info in this RR already known to any investor. We expect you as a financial analyst to analyze the current financial situation. It is highly uncertain that VLD will have enough sales coming in the long term, but short term, they are obviously in financial trouble, with a likely 50 fold reverse split favored at the meeting June 10. You have taught us that reverse splits are a negative, and I agree. 50 fold is a biggie. Utilizing whatever financial info that is currently available, what is your estimate of the chances of bankruptcy? If buyout, the likely price considering the high likelihood of big dilution after the capital raise after the huge reverse split? If VLD really has military orders in the works, they will likely be significantly delayed due to the usual inefficiency of govt funding.

Your repetition of “buy up to $1, target $10” is out of touch with current financial reality. Early this year, you had a nice acknowledgment of what needs to change in NWI. I was encouraged by that, and I hope you will address the facts of reality for VLD (as well as other risky stocks in NWI). If the crucial current financial info is incomplete, we’ll know more after the Q1 report in May. I trust that you will have a full detailed analysis soon after that, answering our questions.

Thank you.

The market has spoken on VLD. It’s another NVTA. Stick with the winners like GOOG, AMZN, TSLA, AMD, NVDA, some BTC and some gold. I guess META would be in that group but I absolutely DESPISE Facebook and refuse to invest. AI is the theme for the next 10+ years and will produce many trillion dollar companies.

For smaller caps, AXON is doing very well as they are the clear leader in police/defense body cams with a very deep and wide moat. DXCM is another winner even though they missed yesterday. Their over the counter glucose meter will be hitting the shelves this summer and is a fantastic way to monitor your metabolic health. I’ve been playing around with it via https://www.levelshealth.com and it’s fantastic tool see what various foods do to your glucose levels. It really encourages a healthy diet.

Speaking of which, I’d be willing to bet my house that this widespread use of Qzempic for weight loss is going to turn into a disaster.

MM is constantly going for home runs when singles are all you need to win the game.

MDNA is currently halted. Maybe we’re finally getting the news we want to hear!!

Not for distribution to United States news wire services or for dissemination in the United States

TORONTO and HOUSTON, April 26, 2024 (GLOBE NEWSWIRE) — Medicenna Therapeutics Corp. (“Medicenna” or the “Company”) (TSX: MDNA) (MDNAF: OTCQB), a clinical-stage immunotherapy company focused on the development of engineered cytokines, today announced a CA$20 million investment by RA Capital Management, a multi-stage investment manager based in Boston, MA, by way of a non-brokered private placement (the “Offering”). Medicenna intends to use the net proceeds from the Offering for further development of its MDNA11 program, advancement of its preclinical programs and general corporate purposes.

Pursuant to the terms of a subscription agreement entered into as of the date hereof between the Company and RA Capital Healthcare Fund, L.P. (“RAHF”), a fund affiliated with RA Capital Management, RAHF will subscribe for 5,141,388 common shares in the capital of the Company (the “Shares”) at a price of CA$1.95 per share and, in lieu of common shares, pre-funded warrants to purchase 5,141,388 common shares (the “Pre-Funded Warrants”) at a purchase price of $1.94 per pre-funded warrant for total net proceeds to the Company of approximately CA$20 million.

The Offering is expected to close on or about April 30, 2024 and is subject to the approval of the TSX.

“We are excited to announce the financial backing by RA Capital Management as a result of promising single-agent clinical activity of MDNA11, our differentiated IL-2 superkine,” said Dr. Fahar Merchant, President and CEO of Medicenna. “With this funding, we have strengthened our balance sheet at a time of strong momentum, demonstrated enthusiasm for our platform by attracting a prestigious investor and extended our cash runway well into 2026 enabling us to exploit the deep clinical potential of MDNA11 and our pipeline of early-stage superkines.”

The Shares and Pre-Funded Warrants have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or any U.S. state securities laws and may not be offered or sold within the “United States” or to “U.S. Persons” (as such terms are defined in Regulation S under the U.S. Securities Act) unless registered under the U.S. Securities Act and applicable state securities laws or pursuant to an applicable exemption from such registration is available.

This news release shall not constitute an offer to sell or a solicitation of an offer to buy these securities, nor shall there be any sale of these securities in any state or other jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such state or other jurisdiction.

Sounds like issuance of more shares (via warrants) which aren’t available to the U.S.? Sounds like a “watering down” of stock value?

So apparently the market likes it as it’s up 20%.

That’s why I’m still poor !!!

MDNA closed up 30% at $1.82 on Friday after they did a C$20 million private placement of 10,282,776 shares and prefunded warrants at an impressive $1.95 per share, a 39% premium to Thursday’s closing price. Why, you ask, would smart healthcare investors like RA Capital Management do an above-market deal?

It is because (1) they knew they couldn’t buy $20 million of stock in the public market without running it to the moon; (2), they knew their cash would make Medicenna stronger and move the stock they now own up; and (3), they knew the announcement of the financing would trigger the computer bots, day traders, and MOMO crowd to pile on.

MM – so where does MDNAF go from here and how soon?

Steadily up as they continue to announce responses from the clinical trials.

MM, see below. Isn’t that $1.95 canadian, so it’s not that much of a premium as you listed above?

Pursuant to the terms of a subscription agreement entered into as of April 26, 2024 between the Company and RA Capital Healthcare Fund, L.P. (“RAHF”), a fund affiliated with RA Capital Management, RAHF subscribed for 5,141,388 common shares in the capital of the Company (the “Shares”) at a price of CA$1.95 per share and, in lieu of common shares, pre-funded warrants to purchase 5,141,388 common shares (the “Pre-Funded Warrants”) at a purchase price of CA$1.94 per pre-funded warrant, for total net proceeds to the Company of approximately CA$20 million.

MM – Thanks for the insight an SCYX, Im in and believe this may be a best pick for 2024. Please provide opinion on MDNAF, is this also a possible best pick for 2024, how does the news today impact its ability to take off?

How much of a hit did you take selling all your china holdings?

At least the China stocks are down only 50%. A “gift” compared to the near 100% wipeouts in a growing long list of NWI spec stocks.

This is the opportunity of a lifetime for China to attack Taiwan. I used to have TSMC for decades. But sold it all off awhile back when China publicly said they would get Taiwan back either thru diplomacy or FORCE. Unlike the US, China doesn’t make idle threats . They took over Hong Kong and met NO resistance. That was a major mistake and now they have full confidence that the same can happen with Taiwan. I think this whole mess with Iran, Russia, Syria , and all the other puppet’s of China have been leading up to an attack on Taiwan. Also MDNAF was up 30 percent today. $1.82.

John Miller is correct. China’s aggressive foreign policy is the reason for their stockpiling of industrial materials. They know that their lack of a deep sea navy will result in being unable to break a naval blockade for such materials in the future. They are stockpiling for military rather than industrial purposes, as China is already overbuilt and their inescapable demographic decline also militates against the stockpiles being for domestic consumption. As the world fails to react to China’s aggressive creation of islands in the territorial waters of Indonesia, the Phillipines and Vietnam as well as its military bases in other nations to its south and west, China is simply waiting for the opportunity to solve its terminal demographics the same way Russia is attempting in Ukraine.

I don’t think demographics is the major issue. Taiwan has a tiny population compared to China. But China wants to own and control Taiwan’s industries.

Wrong question.

MM or anyone-

any ideas on why SAND is doing so poorly while spot Gold is doing well? Wheaton Precious Metals WPM, another royalty company, is also doing well. Any ideas on other gold investments, not minors ?

People are worried about SAND announcing an earnings disappointment next Thursday.

Thanks for the reply.

I am asking why SAND is doing so poorly over the long-term, not recently. You recommended on about 3/7/13 at 8.85. Now it is around 5.56.

Compared to charts of Spot gold, CEF, WPM, PHYS, all have done markedly better over the same time period, as well as recently. After the upcoming earnings announcement, what is the rationale for why SAND will be better going forward than any of the above?

First, they took on a lot of debt to buy as lot of future royalty streams. They’re paying that off rapidly, but the streams hven’t kicked in yet. They will.

Second, they have a big position Wall Street hates – Hod Madden, where it isn’t clear how fast the developer will move forward. That uncertainty should go away soom.

MM or anyone-

how do I search the website for all previous comments on a particular stock? How do I see, for example, every time and in what issue MM referred to SAND.

What is moving Synexis today?

could be because they presented some preclinical data yesterday and today,in spain

Flash in the pan. I am looking for a decline in SCYX as conference euphoria dies down. Only when the FDA approves the new manufacturer will the stock have a sustained advance. We have until June 30, MM’s estimate of approval.

Preview of coming attractions in my opinion. Also VLD was up 19 percent today. Another miracle in the making?

MM or anyone, why SCYX up 20% with double avg daily volume?

maybe because it has in the bottom of the toilet for so long,could just be day trading

at least there was some life with it today unlike nvtaq

Just short term conference boost. Still not high volume.

Due to positive reception in Barcelona of SCY-247. Also a new manufacturer has been selected and the clinical hold on sales and study completions is about to be lifted. AND, the stock price as MMsays is STUPID CHEAP.

SCYX

Michael M a question about competition. A small biotech today published positive results for their MAT 2203 which demonstrated efficacy agaist a mucormycosis infection as an oral form of amphoteracinB. I do not see much competition here. Company symbol is MTNB. What si your opinion here?

Oral amphoteracin B, an old generic drug is poorly absorbed from the GI tract. Mucormycosis is treated with IV anti-fungals. Ampho B is also used intranasally to treat chronic sinusitis. Mucor can cause sinus infections. Ampho is a stronger version of nystatin–both are polyene structures. Nystatin is a very safe anti-fungal, very cheap. Before everyone gets too excited about Brexa or SCY 247, remember that nystatin is a cheap old drug with minimal side effects. For recurrent VVC, the first line approach is to use oral nystatin for a period of time in higher doses if needed because it is very safe, unlike the azole drugs which have liver toxicity. The expensive Brexa will be a big hyped bust for recurrent VVC. SCYX did a lousy job of selling it, and had to give it away to GSK in return for milestone/royalty payments. SCY 247 may be a game changer for serious systemic fungal infections, but it is a long ways off.

If you want to learn many useful treatments ignored by mainstream medicine, read parkcompounding.com, a custom compounding pharmacy used by real doctors who are leaders in the field of mold/fungal illness.

counting strictly on SCY-247, otherwise it’s a bust. I agree with you on this. However, SCY-247 may not be further away than 2026 if it is fast tracked. I believe it will be a game changer

I just read about MAT 2203. It utilizes interesting LNC (lipid nanocrystal) technology to increase GI and cellular absorption of amphotericin B. LNC seems like a type of liposomal technology I am familiar with, used by Quicksilver Scientific for vitamin C and glutathione oral delivery. Quicksilver’s tiny sized liposomes achieve about 4x better oral delivery compared to common forms of these items, and almost as good plasma levels as expensive and almost unavailable intravenous forms. MAT 2203 is way ahead of SCY 247 with some good phase 2 studies on a variety of fungal infections, although phase 3 is slow in coming for the usual reasons. Both MAT 2203 and SCY 247 are wild cards as far as I am concerned–which will pan out and when? Both companies are highly speculative situations. SCYX may have better financial status than MTNB, I don’t know. I already have too much money in SCYX with current average cost of $4.70, and initial cost of $22 from MM’s imprudent buy price many years ago. The major play in SCYX is the bump that will happen when the FDA approves the new manufacturer of Brexa. As for getting rich on SCY 247, that is highly speculative.

Enovix (ENVX) up 32% this morning. This is one of the few NWI stocks I have some money in. Been buying LEAPs while it was cheap. Now I’ll sell some near term OTM Calls after this jump.

Original Recommendation: April 20, 2023 @ $12.64

Signing a deal with an unnamed smartphone OEM is interesting though. If it’s Apple or Samsung this price might double.

Original Recommendation: April 20, 2023 @ $12.64

Anyone who has been reading NWI as long as we have knows not to buy a recommendation when first made. I watched and waited for the price to drop to 8.60 before I made my first buy. At that price it seemed like a reasonable speculation because the company was executing well enough and management’s past success was impressive enough and the competition was moving slowly enough.

I doubt the top 5 smartphone OEM is Apple or Samsung. Great if it is, but I expect ENVX to announce at least one more top 5 OEM customer this year.

Well, my only NWI holdings are CWBR and VLD. Both down over 90%. Probably shouldn’t have touched either but VLD had a connection with SpaceX and CWBR seems like a good spec. I might take a small position in ENVX but still think that any EV battery ( the big bucks) development will be done by Tesla. I think RIVN might be a decent spec as I’m seeing more and more on the road. The Cybertruck appears to be a loser and Illinois just gave Rivian a nearly 1 billion dollar incentive to build a plant. Also, I’m seeing more and more Amazon Rivian vans on the road ( there’s one dropping off a package as I type).

DIdn’t know that about Rivian. That’s a nice incentive. ENOVIX is not a play on EVs. Their battery will be for much smaller applications like phones. If they become #1 in that this will be a great investment. I think it’s a worthwhile spec.

I like your LEAP strategy.

New World Investor for 5.2.24 is posted.