Dear New World Investor:

CRISPR is an acronym for Clustered Regularly Interspaced Short Palindromic Repeats. They are DNA sequences found in the genomes of bacteria. These sequences are derived from DNA fragments of killed agents that had previously infected the bacteria. They are used to detect and destroy DNA from similar agents during subsequent infections, providing acquired immunity.

Cas9, an acronym for CRISPR-associated protein 9, is an enzyme that uses CRISPR sequences as a guide to recognize and open up specific strands of DNA that are complementary to the CRISPR sequence. CRISPR sequences and Cas9 enzymes together (CRISPR-Cas9) can be used to edit (correct) genetic mutations that cause diseases in humans, animals, and plants. This technology can develop targeted new drugs to treat genetic diseases. It won the Nobel Prize in Chemistry in 2020 for Emmanuelle Charpentier and Jennifer Doudna.

Because CRISPR-Cas9 was a new way to edit DNA, there was a rush to patent it. Doudna and her UC Berkeley collaborators applied for a patent, but so did a group at the Broad Institute, affiliated with MIT and Harvard. Feng Zhang at the Broad Institute had shown that CRISPR-Cas9 could edit genes in cultured human cells a few months after Doudna and Charpentier published their method. Broad got the patent and Berkeley filed suit. They lost the first patent infringement case in the US Patent and Trade Office. Berkeley appealed to the Patent Trial and Appeal Board, which decided in favor of the Broad Institute in 2017. Berkeley appealed again, but in September 2018 the US Court of Appeals also decided in favor of the Broad Institute’s patent.

Early in the court fight, Doudna and Feng Zhang cofounded Editas Medicine (EDIT). Although she quit in June 2014, the suite of patents stayed with Editas in the form of exclusive licenses executed in December 2014 from the Broad Institute, MIT, and Harvard. Collectively, they hold about ten times as many genetic editing patents as Berkeley. And Editas has added new patents to its intellectual property (IP) portfolio every year. As the exclusive holder of the foundational patents for CRISPR genetic editing technology, Editas will collect royalties – LARGE royalties – from every gene editing drug approved. They’ll pay about half of those royalties to the patent owners.

Already, Juno Therapeutics (now owned by Bristol Meyers Squibb) signed a license deal worth up to $737 million to fight cancer and autoimmune diseases. Juno has opted into 13 different programs across 11 gene targets to date. Two programs are currently in IND-enabling studies and four are in late-stage discovery. Yesterday, they announced a two-year extension to their strategic research collaboration.

Allergan paid Editas $90 million for eye diseases, a small market. On November 16, Vertex Pharmaceuticals [VRTX – partnered with CRISPR Therapeutics AG (CRSP)] got UK approval for a CRISPR-Cas9 treatment for sickle cell disease. On December 8, they got FDA approval, followed by the European Medicines Agency’s Committee for Medicinal Products for Human Use on December 15.

It’s the first CRISPR-based therapy regulatory approval ever and shot CRSP up 84% to a $4 billion market cap. Editas only has a $462 million market cap (just above its $427.1 million in cash), but VRTX had to get a license from Editas before they could sell the drug. They signed a non-exclusive licensing agreement with Vertex a few days after they got approval in December covering only ex vivo therapies targeting the gene for sickle cell disease. (Ex vivo means cells are taken out of the patient, edited, and then injected back into the patient.)

Editas’ 8-K says Vertex will pay $50 million upfront, plus an additional $50 million contingent payment, plus annual sales-related licensing fees between $10 million and $40 million through 2034. Editas said this deal extends their cash runway through 2026. In total, the company probably will get around $500 million in licensing fees at a 100% gross profit margin for licensing just one gene to one company for only ex vivo therapy for just two diseases. If Vertex wants to sell a drug based on another gene, or this drug for another disease, or develop an in vivo therapy, it will have to pay more. All the many other companies bringing CRISPR-based therapies to market are faced with the same requirement as Vertex.

My first gene editing recommendation, Graphite Bio, crashed and burned when their Phase 1 safety trial failed. No doubt there will be other clinical failures, but there also will be many successes. No matter who wins, Editas gets paid.

Editas has a three-pronged strategic plan:

1. Strengthen and focus their R&D to build an in vivo – in the body – editing pipeline

2. Increase their business development activities to monetize their IP

3. Drive their internal sickle cell program, EDIT-301, through the clinic to FDA approval

Click for larger graphic

Click for larger graphic

The near-term important one for the stock is the EDIT-301 data updates midyear and yearend. Editas Medicine doesn’t need EDIT-301 to be successful, because they will get billions of dollars in intellectual property licensing fees and royalties from their patents over the next decade. But EDIT-301 clinical progress would be a major bluebird:

Click for larger graphic

Click for larger graphic

“VOE” is a Vaso-Occlusive Episode that always requires an immediate trip to the ER.

Click for larger graphic

Click for larger graphic

Editas lost 23¢ a share in the December quarter, much less than the consensus estimate for a loss of 52¢ and 2022’s fourth quarter loss of 88¢. Collaboration and other R&D revenues hit $60 million versus $6.5 million in the 2022 quarter due to payments received from Vertex.

At the same time, R&D expenses increased 34% year-over-year to $69.6 million because that is where they book sublicense payments to the Broad Institute. In 2023 they did a strategic reorganization to trim ongoing costs. There were some R&D savings, and general and administrative expenses were down 20% from last year’s period to $14.5 million.

The March quarter is expected to show revenues up 18.3% from last year to $11.63 million with a 65¢ loss per share. They haven’t set a conference call date yet.

Editas lost $153 million last year and will lose about that much for at least the next three years. DO NOT BUY THIS STOCK IF YOU DON’T WANT TO HOLD IT FOR MORE THAN FIVE YEARS. I expect it to increase steadily as more and more deals are signed, but the really big royalty flows will be after 2030.

Click for larger graphic

Click for larger graphic

Editas has plenty of cash to fund their drug development programs, additional CRISPR-Cas9 research, and patents. Subtracting its cash from its market value means Wall Street values EDIT-301 and its IP at just $34.9 million. That’s ridiculously undervalued.

The stock closed today at a $462 million market cap. CRISPR Therapeutics closed today at $4.675 billion, 10 times higher. Jennifer Doudna also cofounded Intellia Therapeutics (NTLA), another gene editing biotech, which closed today at $2.244 billion. Both will be paying royalties to EDIT for any gene editing therapy they bring to market. I want you to Buy EDIT under $6 for a double in 12 months and a long-term hold to much higher prices.

Click for larger graphic

Click for larger graphic

Primary Risk:Other companies’ gene therapies don’t get approval.

Clinical stage of their lead product: Phase 1/2

Probable time of their next approval: 2029

Probable time of next financing: 2026

The Fed

Yesterday, the Fed held rates steady, to no one’s surprise, and said: “In recent months, there has been a lack of further progress towards the committee’s 2% inflation objective,” also to no one’s surprise. But Chairman Powell added: “It is unlikely the next policy move will be a hike,” and that apparently was a surprise to some – but not you, I hope. I’ve said: “High – but not higher – for longer” so many times we’re all tired of it, but it is right on. The next shocker for the many bears is that US companies can report good earnings even in this interest rate environment.

Even as the Fed raised the Fed funds rate 11 times, the economy kept growing, companies kept hiring, and unemployment stayed under 4% for 26 straight months — the longest streak since the 1960s.

Wednesday’s JOLTS report showed US jobs openings slid in March to 8.5 million vacancies, down from 8.8 million in February, and the fewest since February 2021 – more than three years. But even though job openings are down sharply from the March 2022 peak of 12.2 million, they remain at a high level. Before 2021, they’d never exceeded 8 million — a level they have now beaten for 37 straight months.

The number of Americans quitting their jobs fell to the lowest level since January 2021 — a sign of diminishing confidence in their ability to find something better. Hires declined 281,000 to 5.5 million, but layoffs also fell. It was a mixed report.

Click for larger graphic

Click for larger graphic

In contrast, the revised Business Employment Dynamics jobs data from the Bureau of Labor Statistics is squarely in recessionary territory:

Click for larger graphic h/t @DiMartinoBooth

And construction job openings imploded from 456,000 to 274,000. The 182,000 monthly drop is the biggest ever.

Click for larger graphic h/t @MichaelKantro

Click for larger graphic h/t @MichaelKantro

Beginning June 1, the Fed will slow the pace of Treasurys rolling off its balance sheet on a monthly basis to $25 billion from $60 billion. That is a back-handed acknowledgment that Treasury Secretary Yellen’s massive bond sales are disrupting the money markets.

Market Outlook

Thanks to today’s rally, the S&P 500 added 0.3% since last Thursday and should add more tomorrow after Apple’s beat. The Index is up 6.2% year-to-date. The Index could reach an important interim top around 5900 in late November. There are two historical precedents for bull market tops in election years. In November 1968, the incumbent Democrat Vice President Hubert Humphrey lost to Republican Richard Nixon. The S&P 500 declined 35% in the next 18 months. In November 1980 , the incumbent Democrat President Jimmy Carter lost to Republican Ronald Reagan. The Index declined 28% in the next 21 months.

The Nasdaq Composite gained 1.5% as Big Tech reported good earnings. It is only up 5.5% for the year, though. The SPDR S&P Biotech Exchange-Traded Fund (XBI) won the week, climbing 7.4%. It is still down 1.1% year-to-date.

The small-cap Russell 2000 booked a respectable 1.8% but also is down in 2024, down 0.5%. Of all 13 bull markets since WWII, this is the worst 18-month performance for the small-caps.

Click for larger graphic h/t @SethCL

The fractal dimension is waffling a bit, but still in an ongoing consolidation. As I’ve said, unless there is a big, sudden drop, this will go on a while.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements at June WWDC and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model initial estimate for June quarter growth was a very strong 3.9%, but they trimmed that to 3.3% this morning. The Blue Chips are near 3% too. Right now, it looks like another strong quarter, but I expect the forecast to weaken steadily over the next three months.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, May 3

April payrolls – 8:30am – +243,000 expected: March was +303,000

SAND – Sandstorm – 11:30am – Earnings conference call

Monday, May 6

RKLB – Rocket Lab – 5:00pm – Earnings conference call

ENVX – Enovix – 5:00pm – CEO AMA

Tuesday, May 7

AAPL – Apple – 10:00am – Product introductions event, probably updated iPads

ABCL – AbCellera – 5:00pm – Earnings conference call

Wednesday, May 8

AG – First Majestic – Unspec. – Earnings release; no call

GILD – Gilead Sciences – 1:00pm – Annual meeting t

Thursday, May 9

QUIK – QuickLogic – 1:00pm – Annual meeting

Short Interest – After the close

EDIT – Editas – 12:00pm – Poster presentation at American Society of Gene and Cell Therapy (ASGCT) annual meeting

Friday, May 10

EDIT – Editas – 12:00pm – Second poster presentation at ASGCT

EDIT – Editas – 3:45pm – Oral presentation at ASGCT

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $173.03) March quarter results beat on the top and bottom lines by a little bit, despite fears around iPhone sales in China. Revenue from Greater China fell 8.1% year-over-year to $16.37 billion, above the $15.87 billion that analysts expected. Total revenues fell 4.3% from last year to $90.80 billion, beating the $90.33 billion estimate. iPhone revenue fell while Services hit another all-time record.

Click for larger graphic h/t Seeking Alpha

Click for larger graphic h/t Seeking Alpha

GAAP earnings of $1.53 a share, a March quarter record, beat by three cents. They raised the quarterly dividend 4% to 25¢ and added a whopping $110 billion to the stock buyback program.

On the conference call (AUDIO HERE and TRANSCRIPT HERE), CEO Tim Cook said the company expects to grow revenues “low single digits” in the June quarter. Wall Street expects 1.33% revenue growth to $82.89 billion. Analysts had expected Mac sales to decline in the March quarter, but instead they grew to $7.5 billion, compared with estimates of $6.86 billion. Cook said: “They were really driven by the strength of the new MacBook Air that’s powered by the M3 chip. About half of our MacBook Air buyers during the quarter were new to the Mac.”

Regarding AI, he said: “We continue to feel very bullish about our opportunity in generative AI and we’re making significant investments. We’re looking forward to sharing some very exciting things with our customers at events later this year.”

The company has stealthily built a dream team of AI experts, according to the Financial Times, hiring 36 engineers from Google, 10 from Amazon, and eight each from Microsoft and Netflix. They’ve also hired people from Meta, Uber, Intel, and ByteDance. I expect to see major announcements at the Worldwide Developers Conference the week of June 10 and an iPhone 16 in September able to run a Large Language Model (LLM). AAPL is a Buy under $175 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $33.57) reported March quarter revenue down 3.3% from last year to $3.26 billion, just above the $3.12 billion estimate. The gross profit margin was up 1.6 percentage points from last year to 36.8%, showing excellent cost control even on lower volume. Since the December 2022 quarter, gross margin is up 3.3 percentage points even though revenue has declined almost $400 million. Pro forma earnings of 38¢ a share beat the 35¢ estimate.

On the conference call (INFOGRPHIC HERE and SLIDES HERE and TRANSCRIPT HERE), management said the March quarter will be the lowest of the year.

Click for larger graphic

They guided the June quarter to $3.4 billion and 42¢ to 46¢, essentially right on the $3.34 billion and 44¢ consensus. Management is doing a very good job of managing expenses and expectations through this soft period.

Longer term, they can add $3 billion in revenues without needing any more factories or people.

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

Meta Platforms (META – $441.68) opened their Meta Quest mixed reality operating system to third-party hardware makers. They said they are working with leading technology companies to create a new ecosystem of mixed reality devices, making it easier for developers to build mixed reality apps that reach a wide audience. This is an attempt to create an industry standard against Apple, with Meta in charge (like Microsoft with Windows).

At the same time, they introduced new Ray Ban Meta smart glasses styles that add video calling to WhatsApp and Messenger to share a user’s view on a video call. And they introduced Meta AI with Vision, so users can ask their glasses about what they’re seeing and get helpful information completely hands-free.

Meta said: “Our second-generation smart glasses, in partnership with EssilorLuxottica, have been flying off the shelves — they’re selling out faster than we can make them.” Aside from that being the very definition of “selling out,” I do think Meta will dominate the low end of augmented reality (AR) while Apple’s Vision Pro creates a whole new high end of spatial computing. META is a Buy under $345 for a $400 target in 2024.

PayPal Holdings (PYPL – $66.98) reported March quarter revenues up 9.4% from last year to $7.700 billion, just above the $7.520 consensus estimate. Payment transactions increased 11% to 6.5 billion and total payment volume increased 14% to $403.9 billion. Pro forma earnings of $1.40 per share beat the consensus of $1.22, although they are changing their pro forma calculation to include stock-based compensation, which would reduce the $1.40 to $1.08.

Two key metrics improved. Active accounts fell 1% from last year, as expected, to 427 million. But that was up two million from the December quarter. Trailing 12-month payment transactions per active account – the biggie – increased 13% to 60.0 million. That pushed the stock up 84¢ today.

Click for larger graphic

Click for larger graphic

On the conference call (SLIDES HERE and TRANSCRIPT HERE), they guided the June quarter to revenue growth of 6.5% to $7.76 billion, just under the $7.79 billion consensus, with low double-digit pro forma earning growth from last year’s 87¢ (based on the new pro forma methodology). For the year, they guided for mid- to high-single-digit earnings growth compared to $3.83 (based on the new non-GAAP methodology) in 2023, with about $5 billion in free cash flow. The turnaround is on track:

Click for larger graphic

Click for larger graphic

PYPL is a Buy under $68 for a double in three years.

Small Tech

Enovix (ENVX – $9.47) reported March quarter revenue of $5.30 million, clobbering the $4.05 million estimate. The pro forma loss of 31¢ was two cents worse than the -29¢ consensus.

On the conference call (INVESTOR LETTER HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Raj Talluri said: “We are thrilled to announce we have advanced our engagement further with one of our top customers by reaching a formal development agreement, underscoring the value and competitive advantage our silicon batteries can provide to the next generation of smartphones…Smartphone battery requirements are incredibly rigorous and set the standard for consumer electronics more broadly. Our goal is to provide our customers with a leading-edge battery that will enable demanding AI applications without compromising battery life.”

Enovix has begun manufacturing its battery cells based on smartphone customer specifications and is on track to deliver first samples in the June quarter. High volume production will take place at the Fab2 facility in Malaysia.

Click for larger graphic

Click for larger graphic

Raj said they are taking “decisive actions to reduce cash burn,” targeting a reduction of more than one-third of their fixed costs, more than $35 million a year, by the end of 2024.

Click for larger graphic

Click for larger graphic

They guided the June quarter to revenues of $3 million to $4 million and a loss of 22¢ to 28¢ per share, worse than the consensus at $4.07 million and a 23¢ loss. But the stock shot up 45% today on the smartphone contract news. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

In contrast, Fastly (FSLY – $8.79) was down 32% today after reporting March quarter revenues of $133.52 million, up 13.6% from last year but just below the $133.87 million consensus estimate. The gross profit margin improved to 58.8% in the quarter, up 3.2 percentage points year-over-year. The pro forma loss of five cents a share was better than the six-cent loss expected.

But on the conference call ( SLIDES HERE and TRANSCRIPT HERE), they guided the June quarter to revenues of $130.0 million to $134.0 million with a loss of 6¢ to 10¢. That was below Wall Street’s expectation for $140.3 million and a two-cent loss.

Even worse, they guided 2024 full-year revenues to $555.0 million to $565.0 million, way below the $584.62 million expected. They expect a full-year loss of 6¢ to 12¢, also worse than the 4¢ expected. That was enough to clobber the stock.

If management is sandbagging, they certainly made a tactical error. The important metrics for the quarter weren’t bad. The last 12-month net retention rate increased to 114% in the quarter from 113% in the December quarter, reversing quarterly declines in this metric since the end of 2022. Total customer count was up 47 from the December quarter to 3,290, although enterprise customers were down one to 577.

But they said they saw a reduction of revenue from a small number of their largest customers,and revenue from their top 10 customers dropped from 40% to 38%. Many of the top 10 accounts run a multi-vendor strategy, and they lost some share of the traffic. In some accounts they saw an addition of Content Delivery Network vendors, a reversal of the vendor consolidation they saw last year.

BofA downgraded the stock from Buy to Underperform and cut their target price from $18 to $8. They wrote: “Decelerating growth in Fastly’s largest customers, share loss in delivery, and limited visibility in 2H cause us to question a rebound in 2024. While we continue to like Fastly’s positioning in the edge compute market, we see it as a 2025 opportunity instead of a near-term growth driver.”

I think that’s too negative. Edge compute is very much a 2024 story, and Fastly management is laser-focused on getting new customers and getting back share of old customers’ traffic. But I am going to reduce the buy limit to $14 and increase the low end of the expected holding period from two to three years. But the ultimate target price dies not change – edge computing is going to be huge in the AI era, and Fastly is one of the very top suppliers. FSLY is a Buy up to $14 for a 3- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Rocket Lab USA (RKLB – $3.95) is preparing two back-to-back Electron launches to deploy NASA’s PREFIRE (Polar Radiant Energy in the Far-InfraRed Experiment) mission. The two dedicated missions will each deploy one satellite to a 525km circular orbit from Rocket Lab Launch Complex 1 in New Zealand. The first mission is scheduled to launch no earlier than May 22. The second launch will take place within three weeks of the successful deployment of the first. These missions will be Rocket Lab’s 48thand 49th Electron launches overall and its sixth and seventh launches of 2024.

The company said this new documentary premiering at DC/DOX24 on June 15 is: “Quite possibly the most detailed behind the scenes look at our work and team yet.”

The breathless promo is: “Less than one hundred miles above our heads is where some of the most valuable real estate in the universe lives: Low Earth Orbit. This is an extraterrestrial land grab, a galactic Wild West where the cowboys are visionaries, tinkerers, and capitalists dead set on owning the future. From spaceports at the edge of the earth to local communities that are being transformed and upended by these technologies, Wild Wild Space thrusts the audience into this critical and unknown world.

“Wild Wild Space focuses on the intense rivalry between two visionaries and founders of contesting rocket companies, Chris Kemp and Peter Beck [CEO of Rocket Lab]. Their mission transcends mere competition; it’s a strategic bid to outdo each other, disrupt Elon Musk’s cosmic dominance, and claim significant shares in the burgeoning space industry. Amidst The stakes rise as they race against time to deploy commercial satellites for prestigious clients, including Planet Labs, led by visionary Will Marshall, encapsulating their shared goal — to redefine space, one satellite launch at a time.”

There was a pretty good writeup on Seeking Alpha: Rocket Lab: Winning Contracts And Neutron Coming, Prepare For Takeoff. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Compass Pathways (CMPS – $8.25) set up another research collaboration, this one with Mindful Health Solutions, to develop a scalable, cost-effective delivery model for COMP360 psilocybin treatment. Mindful Health Solutions offers comprehensive mental health care services for patients living with treatment-resistant depression and other mental health conditions. They focus on early adoption of advanced, interventional treatment options, as part of a long-term, holistic care model that includes medication management and psychotherapy. They operate over 20 outpatient clinics located across California, Washington, Texas, and Georgia.

These research collaborations are really smart. Compass CEO Kabir Nath said: “It is crucial that we understand how different mental health service providers are positioned to deliver COMP360 psilocybin treatment to patients.” They will hit the ground running after FDA approval. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2026

Probable time of next financing: Late 2025

Medicenna (MDNAF – $1.75) closed their C$20 million investment from RA Capital Management. My “Probable time of next financing” goes from March 2024 to 2026. Buy MDNAF under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2026

Probable time of next financing: 2026

ScyNexis (SCYX – $1.78) presented preclinical efficacy data on SCY-247, its second generation fungerp candidate, at the European Society of Clinical Microbiology and Infectious Diseases (ESCMID) Global 2024 congress. CEO David Angulo said: “We continue to be excited about the potential of our second generation fungerp SCY-247 to address the critical need for new antifungal treatments, particularly for invasive fungal infections where current options are limited and resistance is increasing. The positive data presented at ESCMID Global further strengthen our confidence in SCY-247’s ability to combat these difficult-to-treat infections, and we look forward to its continued advancement as we aim to enter clinical stage by year-end.” Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2024

Probable time of next financing: Never

TG Therapeutics (TGTX – $16.42) reported strong March quarter Briumvi sales of $50.5 million, up 25% from the December quarter. In addition, they booked a $12.5 million milestone payment for Briumvi’s launch in Germany, the first EU country. Total revenue of $63.47 million clobbered the consensus expectation for $54.61 million. They lost seven cents a share, more than the four-cent loss estimate.

On the conference call (AUDIO HERE), CEO Michael Weiss said: “We believe this strong momentum will continue to build throughout 2024 and are pleased to update our yearly guidance to $270 to $290 million in Briumvi US net revenue in 2024.” That was a big increase from the previous guidance for $220 million to $260 million, and the stock jumped over 20% from Tuesday’s close through today. They also guided for $65 million in Briumvi sales in the June quarter, which probably is low.

Their 2024 development pipeline anticipated milestones are:

* * Commence clinical development of subcutaneous BRIUMVI

* * Commence a clinical trial evaluating BRIUMVI in an additional autoimmune disease outside of multiple sclerosis (MS)

* * Commence a clinical trial evaluating azer-cel in autoimmune disease

* * Present data from the ENHANCE Phase 3b CD20 switch trial at multiple conferences throughout the year

The company finished the quarter with $209.8 million in cash, enough to take them to cash flow positive. Buy TGTX under $12 for a target price in a buyout of $30 or more.

Primary Risk:Briumvi, the MS drug, fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: NM

Probable time of next financing: Never

Inflation MegaShift

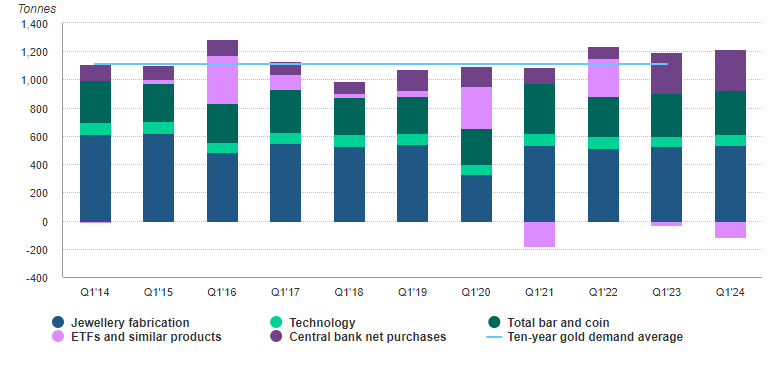

Gold ($2,313.40) liked what Chairman Powell said, but still can’t break over $2,400. The World Gold Council said in spite of record high prices, March quarter gold demand, including sizable over-the-counter buying by investors, increased 3% year-on-year to 1,238 tonnes, the strongest first quarter since 2016. Global jewelry consumption was 2% lower than last year at 479 tonnes, but technology demand for gold recovered 10% year-over-year as the AI boom boosted demand in the electronics sector.

Quarterly gold demand by sector and 10-year quarterly average, tonnes

Click for larger graphic h/t @GOLDCOUNCIL

Click for larger graphic h/t @GOLDCOUNCIL

Mine production increased 4% y/y to 893 tonnes. The fractal dimension is consolidating the big run from $2,000 to $2,400.

Miners & Related

Coeur Mining (CDE – $4.79) reported March quarter revenues up 13.8% from last year to $213.06 million, nicely ahead of the $203.19 million estimate. The pro forma loss of five cents a share was a penny worse than the four-cent loss estimate. They had strong year-over-year production increases in line with their 2024 guidance. Solid performances at Palmarejo and Wharf led to total production of 80,744 ounces of gold and 2.6 million ounces of silver compared to 69,039 ounces of gold and 2.5 million ounces of silver in the first quarter of 2023. Production levels are expected to increase over the balance of 2024, driven primarily by the ramp-up at Rochester.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), CEO Mitch Krebs said the strong quarter compared to planned puts them in a great position for a successful 2024.

Click for larger graphic

Click for larger graphic

Mitch said: “We’re on track to flip to positive free cash flow in the second half of the year, which will be earmarked for debt repayment. That deleveraging process can be further accelerated assuming current silver and gold prices continue, leading to a rapid and dramatic improvement in our overall financial condition and outlook…The convergence of all of these catalysts, higher commodity prices, a completed Rochester, a stable suite of US-centric mines in North America and a world class Canadian exploration project sets us apart from our peers and leaves us very well positioned.”

The CFO said: “Beginning in the third quarter, the company expects to begin aggressively paying down the revolver and our prepaid gold sales agreements as we drive towards achieving our long term leverage targets of total debt to EBITDA of 1x and net debt to EBITDA of 0…No ATM is currently in place or is being contemplated and the company’s remaining hedges roll off at the end of the second quarter, commensurate with the Rochester ramp up to full nameplate capacity.”

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Sandstorm Gold (SAND – $5.54) reported after the close today, but the conference call will be on Friday. Revenue dipped 2.7% from last year to $42.80 million, beating the $41.41 million estimate. They lost a penny a share; the Street expected them to make a penny a share.

The company said they signed a definitive asset purchase agreement to sell a collection of non-core, non-precious metals royalties for cash proceeds of $21 million plus the retention of the next $10 million in proceeds from the Copper Mountain Royalty. Since the September 2023 quarter, Sandstorm will have sold over $50 million of non-core royalty and equity investments, including approximately $40 million in cash consideration. Sandstorm will receive the cash purchase price in the second quarter of 2024.

The transaction is not expected to materially impact Sandstorm’s near or long-term production guidance. They maintained their 2024 production guidance of between 75,000 and 90,000 gold equivalent ounces, expected to increase to approximately 125,000 ounces within the next five years.

They also renewed their stock buyback program for up to 20 million shares, or about 7% of the issued and outstanding stock. SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $59,271.81) has been surprisingly weak since the April 19 halving – surprising mostly because the sellers must know they are going to have to reverse course and chase shortly. April was its worst month in nearly a year and a half as “sell the news” hit the coin. In the past, these post-halving dips have lasted about three months before bitcoin makes new all-time highs in the subsequent 12 months. Take advantage of this dip. March’s pre-halving record was $73,803.

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $33.80) is the easiest and cheapest way to Buy bitcoin for the 2028 and 2032 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $79.06

Oil slid back under $80 as demand from the summer driving season hasn’t hit yet – but soon. The July 2026 Crude Oil Futures (CLN26.NYM – $68.63) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $38.99) is a Buy under $40 for a $100+ target.

EQT (EQT – $39.48) would be a major beneficiary if the answer is “Yes” to the question: Is A Multi-Year Natural Gas Bull Market In The Making?

Click for larger graphic h/t @HFI_Research

Asia is pulling in record amounts of LNG from non-Asia sources for this time of year. Qatar, the US, and Russia are the primary sources.

Click for larger graphic h/t @ira_joseph

Click for larger graphic h/t @ira_joseph

Microsoft signed a deal with Brookfield Asset Management to invest $10 billion to develop 10.5 gigawatts of renewable energy capacity between 2026 and 2030 for use in its data centers. That is 3x the existing 3.5 gigawatts consumed by data centers in Northern Virginia, the world’s largest data center market. (h/t @fitz_keith) Guess what will provide baseload power? EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $5.60) will be a major beneficiary of a problem identified by the highly respected natural resource investors Goehring & Rozencwajg: Uranium Mine Supply Faces Challenges. They wrote: “The world’s two largest producers are now both short of uranium. On September 3rd, Cameco, the world’s second-largest uranium producer, announced expected production shortfalls at McArthur River and Cigar Lake, totaling 3 mm pounds. Given that before their recent announcements, Cameco and Kazatomprom were likely fully contracted for the next four years, we believe both companies have committed to selling more uranium than they can produce. If correct, both companies may have to buy material on the spot market, driving higher prices…

“Uranium has now slipped into a structural deficit and is about to get even tighter. Demand continues to grow, while production is beginning to disappoint. Although we believe new production will eventually end the bull market, we expect very little new mine supply for the next several years. In previous letters, we predicted the uranium bull market would soon become chaotic– that period is now upon us.”

Tuesday evening, the Senate passed a bipartisan bill banning Russian imports of uranium, which will only make things worse for US utilities. President Biden plans to sign it. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $48.78) will be a major beneficiary of the copper shortage for years. It would require a Herculean effort to bring enough supply online in time to prevent copper from hitting $7.50 a pound.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

Other Recommendations

Acreage Holdings (ACRDF – $0.37) reported December – not March – fourth quarter revenue of $52.8 million with a gross profit margin of 32%. Their net loss was $35.7 million.

For the full 2023 year, they had $223.4 million in revenue compared to $237.1 million in 2022. They’ve now launched their Superflux craft cannabis brand in New Jersey, Ohio, Massachusetts, and Illinois. The CEO said: “Throughout 2023, we completed various strategic initiatives that have positioned us strongly ahead of our acquisition by Canopy USA…We firmly believe we have built one of the strongest Northeastern footprints, and our robust presence in states such as New York, New Jersey, and Connecticut will continue to grow our topline as we deepen our presence in these developing markets in anticipation of our entry into Canopy USA.”

The stock moved up a bit after the Drug Enforcement Administration indicated they will move to reclassify marijuana as a less dangerous drug, probably Schedule 1. The proposal still must be reviewed by the White House Office of Management and Budget. It would recognize the medical uses of cannabis and acknowledge it has less potential for abuse than some of the nation’s most dangerous drugs. However, it would not legalize marijuana outright for recreational use. ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

Mongolia Growth Group (MNGGF – $1.01) finally published their fourth quarter report. CEO Harris Kupperman said: “I have on many occasions noted that there are tax and regulatory reasons why we cannot be a publicly traded business where the primary assets are marketable securities. Therefore, we MUST purchase over 25% of an operating business in the very near future. Unfortunately, we have not been able to identify any attractive opportunities and have started to lose confidence that we will be able to identify a sufficiently attractive opportunity. If we cannot find a suitable acquisition in the near future, we will likely choose to liquidate this Company, so as not to burden shareholders with the costs of a public company. In the meantime, we hope that future gains from our existing marketable securities portfolio can utilize our tax assets, maximizing the after-tax return to shareholders.”

Because Kuppy is one of the largest shareholders, I expect we’ll do fine in a liquidation. I’m moving MNGGF to a Hold for whatever comes next. MNGGF is a Hold.

Primary Risk: Harris Kupperman makes bad investments.

* * * * *

* * * * *

RIP Paul “Pooch” Tavares

* * * * *

Your reading Tesla’s Master Plan, Part Deux Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 5/2/24. Check out the complete Portfolio page HERE.

Portfolio Protection

June 21 SPY $505 put (SPY240621P00505000 – $8.87)

June 21 SPY $410 put (SPY240621P00410000 – $0.32)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $173.03) – Buy under $175 for new iPhones

Corning (GLW – $33.57) – Buy under $33, target price $60

Gilead Sciences (GILD – $65.33) – Buy under $80, target price $120

Meta (META – $441.68) – Buy under $345, target price $400

PayPal (PYPL – $66.98) – Buy under $68, target price $136

SoftBank (SFTBY – $25.20) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $9.47) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $54.41) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $8.79) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $20.44) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $13.43) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.95) – Buy under $13, target price $30+

Velo3D (VLD – $0.23) – Buy under $1, target price $10

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.85) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.30) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.19) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $8.25) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $12.01) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.75) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.78) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $16.42) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($26.93) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $26.33) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $32.39) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $21.28) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $30.97) – Buy under $30, target price $50

Coeur Mining (CDE – $4.79) – Buy under $5, target price $20

First Majestic Mining (AG – $6.72) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.41) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.54) – Buy under $10, target price $25

Sprott Inc. (SII – $40.45) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $59,271.81) – Buy

iShares Bitcoin Trust (IBIT – $33.80) – Buy

Ethereum (ETH-USD – $2,993.90) – Buy

Grayscale Ethereum Trust (ETHE – $21.65) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $68.63) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $38.99) – Buy under $40; $100+ target

Vermilion Energy (VET – $11.76) – Buy under $11; $24 target

EQT (EQT – $39.48) – Buy under $35; $70 first target

Energy Fuels (UUUU – $5.60) – Buy under $8; $30 target

Freeport McMoRan (FCX – $48.78) – Buy under $44; $65 target within two years

Other Recommendations

Acreage Holdings (ACRDF – $0.37) – Buy under $2 for the Canopy Growth merger

Hold

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.01) – Hold for buyout

Invitae (NVTAQ – $0.00) – Hold for final auction results

Mongolia Growth Group (MNGGF – $1.01) – Hold for probable liquidation

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Michael: Long term client here, love your through analysis! NOTE PLEASE: Maybe you need a better proof reader… Meta is trading at >$441; this radar report suggests buy under $345( ?) ; for a target price of $400. ( It’s at $441!).Did I miss something here ?

No. I was pounding the table on META under $100. They’ve done well, but Instead of chasing I think we’ll get another chance under $400.

Where is the FSLY update?

Between the ENVX & RKLB updates

TO M. Murphy

You may want to reclassify the 20 to 1 items. It appears half or more aren’t 20-1. Maybe just BIOTECH? Just a thought.

Or, perhaps, $20 to $1, given half of them are down over 90%

A good thought. There is a huge difference between stupid cheap stovks like ABCL, EDIT, and SCYX on the one hand, and ARTH or NVTA on the other.

MM – thanks for the reco on EDIT – how much conviction do you have on your projection it will double in 12 months?

Stay away. DNA fragments can cause autoimmune disease. If EDIT just collected royalties and was not exposed to risks of CRISPR development for diseases, that would be a low risk business model. But Graphite Bio failed. Even MM said you must hold EDIT for 5 years for payoff.

EDT is primarily a royalty play.

DNA manipulation is DANGEROUS. Foolish bioengineers don’t know what they’re doing. All drugs are risky. Abnormal, unnatural substances are created that the body was not designed to handle. It is no surprise to me when many drugs are withdrawn years after approval, as problems are seen after millions of patient-years use which weren’t revealed after a few thousand patients in phase 3 trials. As to the artificial drug hormone, medroxyprogesterone being called a progestin, it has many different properties than the real thing, natural progesterone. Medroxy-p causes blood clots, not the real thing. Millions of menopausal women dropped natural bioidentical HRT because they were given medroxy-p instead of natural p which is safe when prescribed by a real doctor who knows what he is doing. Medroxy-p increased the incidence of heart attacks, but natural p doesn’t. Big Pharma is relying on the stupidity of doctors who forgot their biochemistry that they learned in college. Big Pharma is thereby able to indoctrinate many doctors by providing political pressure to alter their minds. I could show a 3 year old child who has learned that you can’t put a square peg into a round hole that medroxy-p has a different structural formula than the real p. Most doctors are more ignorant than that 3 year old.

Biotech investing is about making money for a few years until the problems are seen. Forget about noble intentions of helping mankind.

As a relevant aside, I get 3D printing emails about various applications of that. In Iran, they are printing bioengineered bone fragments to treat osteoporosis. These bioengineers and medical people are doing risky things. Xeno-materials cause autoimmune disease and cancer.

Your best bet for a reasonably safe stock to double in 1-2 years is TGTX. The vast majority of bios fail, but TGTX is lucky to have Briumvi which will become a blockbuster drug fairly soon. NEVER NEVER set fixed time horizons. Most successful companies take a lot longer than anyone thinks. It is all completely unpredictable. Nearly all NWI stocks are down severely after waiting MANY years, and the few that are winners like TGTX also take much longer than expected to achieve good results.

Forget the crazy marketing come on about putting $2k into one stock, sell when it is $20k, then buy another stock with $2K or more, rinse and repeat. I’d bet that absolutely NOBODY in the history of all MM’s newsletters has ever been successful with this strategy. Trying to follow it to even a moderate degree is a guaranteed ticket to poverty and being banished to the jungle to compete with lions and poisonous snakes.

Steve, if you seek guarantees, you will get 5% in a bank CD which rolls over at maturity to whatever the prevailing interest rate is. But adjusting for taxes and “official” inflation, that’s about a 0% return. To beat inflation, you have to accept higher risks. The odds of a 100% return in 1 year on general stocks is extremely low. The odds are even lower for small NWI stocks because the buy and target prices are way too optimistic. Take VLD. The buy price was $10. I thought I was lucky by initially buying at $1.50 in Oct 2023 when MM said it was a gift. A few months later, it reached 19 cents. I kept averaging down to 44 cents. It is now 22 cents as there is reasonable concern about bankruptcy and guaranteed prospects of lots of dilution after a huge reverse split soon to raise money for survival. I may break even if there is a desperate buyout at 44 cents. But any NWI subscribers who may have bought at $10 will suffer over 95% losses in that scenario.

It’s not just NWI. Subscriber Chris who is very prudent suggested ACXP, NGENF as top choices. ACXP is down 60% from when he first mentioned it, largely due to a lying lawyer CEO who talks big but has failed to deliver after several years. NGENF is a great speculation about a peptide that may change the lives of people with incurable neurological conditions. Both the rewards and risks are very high.

A major part of the risk of these small stocks is the bad behavior of execs who collect huge inappropriate salaries at the expense of shareholders who love to gamble. These huge salaries foster laziness from management who fail to market their products properly. (This is different from salesmen who work mainly on commission. The high commissions incentivize them to increase sales.) Big example–TN of ARTH. I am worried about AKBA for the same reason. Their recently approved Vafseo should become a blockbuster, but the continued rapid plunge in the stock after approval reflects distrust of management. They did a poor job selling Auryxia, and we are worried about the same for Vafseo.

Despite the hype that SCYX is a cheap stock, the fact is that Brexafemme is a mediocre drug only slightly better than generic fluconazole. SCYX couldn’t sell this expensive drug, and gave most of the revenue away to GSK in return for mere milestone and royalty income. The new prospect SCY 247 may be better, but approval is many years away. I see competition from MTNB whose drug candidate MAT 2203 is further along, having completed phase 2. The major play in SCYX is the bump in the stock when the manufacturing approval occurs soon. From $1.70 currently, we may get $2.50 after approval, which is where the stock was before the drug recall. After that, it is totally speculative. My problem is that I have too much money already invested in SCYX, again due to MM’s overly optimistic buy price many years ago at $22. I averaged down, most recently 6 months ago at $1.70, but my average cost is still high at $4.70. Even if I bought lots more now, I could only get my average down to $3.00 at best. I am a victim of gambler’s ruin. Many NWI subscribers are in even worse shape.

The EDIT chart is terrible. It could easily get chopped in half to $3 or worse. MM will say it is a gift next year at $4. If you want to gamble, wait for a smooth cup and handle formation on the chart. The chart resembles VLD 6 months ago when MM said VLD was a gift at $1.50.

Feb 11th 2021 he was recommending buying tgtx up to 50.00 as it was then around 46.00 then,most likely 97 percent of his picks have turned to garage so if you bought back in 21 your only down 65 percent on tgtx compared to say dndn or now nvtaq down percent

TGTX is one of the few NWI investments that I played properly. I bought some at $5, then doubled up on Oct 31, 2023 at $7.25. I am looking to add more around $12. It may still exhibit the problems of cancer that Ocrevus has, hopefully less.

In the very early days of DNDN, I played it well. I took good profits twice, selling out completely. I avoided the eventual total loss. I admire the TGTX trading strategy of YMB poster Very. He is bullish long term, but has been very successful doing trading, even though he has made a few minor mistakes. TGTX most likely has a great longterm future, so a combination of holding a core position and trading the rest makes sense. Very advises that strategy.

A lot. They’ll have a strong flow of royalties from Vertex and sign more deals. It would be cheap at twice the price.

Even if that’s true, the EDIT chart is horrible. Big sawtooth plunges, small % recoveries. No Fibonacci bounces, just dead cat bounces. The slope of the declines may be slowing down slightly lately, but wait for smooth and long basing, then a recovery in a cup formation. Your major error in setting your buy and target prices is estimating market potential without any allowance for failures. Things nearly always take much longer than you forecast, resulting in inexorable losses necessitating capital raises with dilution.

Wonder what became of MM’ and spouse’s green funeral/burial start up business for which he solicited venture from certain subscribers, including moi….

Investors deserve updates. Looks like you haven’t gotten any.

Decided not to take outside investors.

Tarlton is an investor in your venture. He deserves an update without having to ask questions. More generally, NWI subscribers deserve answers to questions. If VLD won’t supply relevant financial info until Q! earnings, at least you can say that you will give an in-depth analysis as soon as you have more data points.

He is not an investor. VLD reports next Wednesday and it will be the first “normal” quarter for orders and expenses sunder the new CEO. I will be updating then.

I hope you are right about VLD, and look forward to your analysis, thanks.

Stiill working on it. Got outbid at the last minute on the property we wanted. Now pursuing another property adjacent to the Cascade-Siskiyou Monument.

Hey MM, and fellow subscribers…long time no see…I was scrolling through SPY options today for fun and noticed these big transactions…I’m retired and never really traded options much before, but just wondering why someone might do this…it’s obviously some sort of hedging options strategy but I honestly can’t figure out why they did it this way unless they are just writing all these options and hoping market stays high…any input would be appreciated… Here’s what I saw… All for 6/14/2024 expiration: 175,000 450 PUTS (@.37/38), 350,000 405 PUTS (@.15/.16), 175,000 360 PUTS (@.07/.08)…. that’s a lot of PUTS in anybody’s portfolio… so why do you think these positions and this date…and which are likely buys and sells… I should be able to see this, but I just don’t see it yet… again any thoughts, speculations would be appreciated, just a puzzle I’m trying to figure out… thanks…

There is a Fash Alert to buy Palantir (PLTR) under $22.

How about and update with nvtaq

Maybe you can look at what came out on nvtaq after the close,and see what you make out of it

The court approved the purchase of Invitae’s assets by Laabcorp for $239 million, Labcorp assumed some liabilities but none of the debt. The lenders will split the $239 million. The common stock is worthless.

Really horrible that this happened my question for you if you don’t mind answering it,how did you get this so wrong with all your experience ..nvtaq buying it up to 10 the Thursday before the Monday after declared bankruptcy as alot of have have to deal with this and start over

And also are we assuming this Will stop trading altogether nvtaq

You’re about a year late recommending this. It was trading around 8+ then and hit a 52 week high of $27+ in March. Not much room for it to run.

What’s your target in 3 to 5 years?

Repost of an excerpt from my scathing analysis of AI on the Flash Alert Palantir page. This concerns another risk for SCYX, a competitor named MTNB.

On SCYX, someone mentioned MTNB, whose drug product MAT 2203 is an innovative reformulation of amphotericin B, the long standing standard of care for serious fungal infections. MAT 2203 uses proprietary liposomal technology to let oral bioavailability approach the efficacy of intravenous delivery, while possibly offering much less risk of kidney toxicity. SCY 247 has yet been unproven, and is only starting early trials. No doubt 247 can be further improved by using liposomal technology, just as Dr. Chris Shade has done at Quicksilver Scientific by custom designing different types of liposomes to suit different nutrients for much better bioavailability and thus better efficacy. But then SCYX would have to pay MTNB licensing fees for this.

SCYX–I am also doubtful about the potential of approved Brexafemme. The sales for VVC have been mediocre. Recurrent is more effectively and more cheaply treated by variable time courses of oral nystatin, one of the first now generic drugs for candidiasis, having been in use for most of our lifetimes. It is very safe. Stupid standard of care for VVC uses fluconazole at a dose of one pill repeated at 3 day intervals twice as needed. Brexa use is similar short bursts of 1 day. But the reservoir of yeast that causes recurrent VVC is the GI tract. It is far better to use a continuous course of nystatin, with the optimum time and dose schedule to be individualized. I don’t respect the medical competence of the medical crew of SCYX, which has engineered underwhelming results for Brexa in VVC. Who knows what they will do with SCY 247? We’ll see what has been accomplished in the FURI, CARES and other already completed trials for Brexa in serious candida infections.

On PLTR, I would say instead of buying 100 shares for $2,200, buy a couple Jan 2026 13.0 Calls at $11.00 or less. When PLTR hits $30, the Calls will be worth at least $1,700 each ($3,400) but the shares will only be worth $3,000.

Even if PLTR only goes back to its previous high of $27, the shares will be worth $2700 and the 2 Calls will be worth at least $2800.

And at $40, the difference will be $4000 vs $5400 (enough to buy 135 shares at $40 each)(or sell one and use the proceeds to execute the other and and still have $100 left over to donate to your favorite charity).

Hi Chris, Heard anything on NGENF. No volume at all today, like 2000 shares traded. Bought some more yesterday at 1.50. I know we won’t here much until September.

New World Investor for 5.9.24 is posted.