Dear New World Investor:

Wall Street wants you to focus on how many times the Fed will cut rates this year even though economic data is coming in stronger than they expected. Almost every brokerage firm expects a quarter-point cut at the June 12 Fed meeting, followed by two or three cuts through the end of the year. After all, Fed Chairman Powell has telegraphed rate cuts are coming since his pivot late last year.

I have a two-part different view. First, Powell really is “data-dependent.” so he will wait until he sees at least early signs of weakness before cutting rates. Because:

(A) this is an election year when Presidents of either party benefit from initial data releases showing a strong economy (that are quietly revised lower, later),

(B) government economists mostly use trendline models to estimate those data releases, so they miss inflection points when things change, and

(C) there’s a lot of anecdotal evidence that economic activity is weakening,

I still expect the Fed to yet again cause a recession, this time mild and brief.

Second, what the Fed does is not nearly as important as what our companies do. From Apple opening the kimono on their AI features at June’s Worldwide Developer’s Conference, to Enovix shipping batteries from their Fab2 in Malaysia, to ScyNexis announcing the FDA has lifted the clinical hold on ibrexafungerp, to Acreage Holdings completing their merger with Canopy Growth US, company news and execution will drive stock prices much more than whether the Fed cuts three times, two times, one time, or not at all. As usual, Wall Street wants you to focus on the shells while they hide the pea.

Next Wednesday’s Consumer Price Index report will be a key indication of whether the pickup in inflation at the start of 2024 was a function of early-year noise or if inflation’s journey back to the Fed’s 2% target has been drawn out materially. Wells Fargo economists think the headline CPI likely rose by 0.4% for the second straight month, which would push the year-over-year rate up to a six-month high of 3.5%. They think the core rate, excluding food and energy, rose 0.3% — a bit softer than January and February, but similar to the December quarter average. That would be a sign that underlying progress remains stubbornly slow.

Looking beyond March, inflation probably will move lower this year as the shelter components start to reflect 2023’s softness in rents. Further moderation in shelter costs will help drive the year-over-year rate of core CPI down from 3.8% at present to 3.3% by yearend. But headline progress will be more of a grind ahead because a rebound in commodity costs have turned food and energy from tailwinds to headwinds.

Click for larger graphic

BofA’s Sell Side (Wall Street brokerage firms) indicator ticked up 22 basis points to 55.0% in March, the highest level since May 2022, but nowhere near euphoria.

Click for larger graphic h/t Savita Subramanian – BofA

Click for larger graphic h/t Savita Subramanian – BofA

As Jurrien Timmer of Fidelity (@TimmerFidelity) said: “With the S&P 500 equal-weighted index (SPW) gaining another 1% last week, this broad measure of the market has now gained 8% year-to-date and 36% since the bull market started in late 2022. That remains shy of the 51% gain for the cap-weighted index (SPX), but it’s a respectable performance considering how narrow the market was until last October, when the market peered into an abyss of “higher-for-ever rates.”

“But it survived that retest, and since that October 27th low the SPW is up 27.8% and the SPX is up 28.4%. Neck and neck. After a tediously narrow start in 2023, the tape has turned green and broad, with 86% of stocks in the S&P 500 in long-term uptrends (i.e., above their 200-day moving average). If that’s not a bullish broadening, I don’t know what is. The market has survived not only diminished expectations of rate cuts, but also a fraying within the Mag 7. It’s heartening to see, and it shows the power of earnings to take over in the heavy lifting department.”

The S&P 500 bottomed 17 months ago on October 13, 2022. Now that we are 17 months into a bull market cycle, it’s worth asking how much life there is left. Cyclical bull markets can be as modest as 48% (1966-1968) or as grand as 200% or more (1982-1987, 1994-1998). Over the past 100 years, the median bull market has produced a gain of 90% spanning around 30 months. By that measure there should be some life left for this cycle.

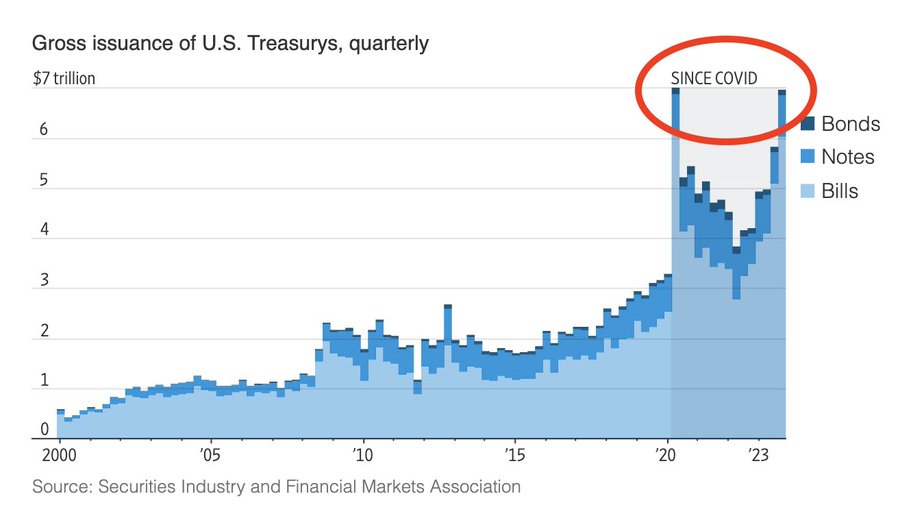

There is one disgusting statistic that worries me. Issuance of US Treasuries are now at pandemic levels: We saw nearly $7 trillion in gross issuance of US Treasures in just 3 months during 2023. For the entire year of 2023, a whopping $23 trillion were issued. US government spending as a percentage of GDP is at World War 2 levels. Of course we have a “strong” economy when US federal debt is rising by $1 trillion every 90 days right now.

There’s plenty of blame to go around. The Biden Administration proposed a giant budget deficit. Congress approved it. Treasury Secretary Yellen is selling bonds to fund it. The Fed is making sure banks have enough liquidity to buy the bonds. Any of these worthies could put a stop to this disaster, but they aren’t because they gain while you lose.

Click for larger graphic h/t @KobeissiLetter

Portfolio Protection

If you still are worried about a short-term market decline and bought either the April 30 SPY $505 put (SPY240430P00505000) or the April 30 SPY $410 put (SPY240430P00410000), it is time to roll them out to reduce the loss from declining time to expiration. The $505 put closed today at $3.91 and can be sold and replaced by the June 21 SPY $505 put (SPY240621P00505000) at $8.33. The $410 put closed today at 16¢ and can be replaced by the June 21 SPY $410 put (SPY240621P00410000) at 82¢.

Remember that these are insurance puts and, like any insurance premium, they are more likely to cost you money than pay off. If you can hold through a transient market dip or don’t want to mess with options, don’t do it.

Market Outlook

The S&P 500 lost 2.0% since last Thursday as the market priced in “high – but not higher – for longer.” The Index is up 7.9% year-to-date. The Nasdaq Composite also lost 2.0% and is up 6.9% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) was clobbered for 5.7% as long Treasury yields climbed. It is barely up 0.2% year-to-date. The small-cap Russell 2000 dropped 3.3% and is up only 1.3% in 2024.

The fractal dimension finally reversed, marking the end of the uptrend. It has a long way to go to consolidate such a huge move, which means either a sharp drop or – more likely – months of churning, possibly all the way to the election.

Top 5

Changes this week: Added AAPL to Short-Term

Near-Term – chronological order

SCYX ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements at June WWDC and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model forecast for March quarter real GDP growth ticked down from +2.8% to +2.5% due to weaker exports.

Click for larger graphic

Click for larger graphic

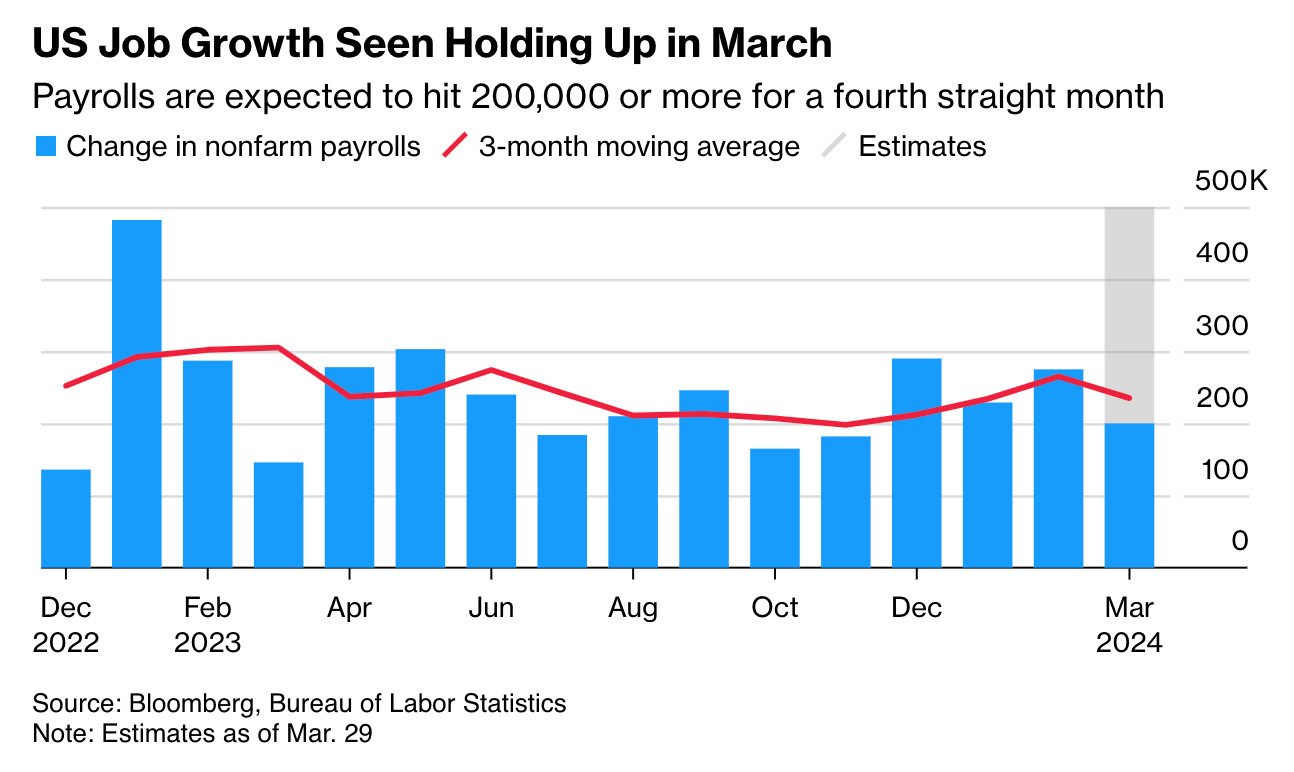

Tomorrow’s March payrolls report is expected to be at least +200,000 for a fourth straight month, according to a Bloomberg survey of economists. Average hourly earnings are projected to climb 4.1% from the same month last year, the smallest annual advance since mid-2021.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, April 5

March payrolls – 8:30am – +200,000 expected; February was +275,000 – let’s see if it is revised down

Monday, April 8

Solar Eclipse!

ABCL – AbCellera – 12:00pm – American Association for Cancer Research (AACR) Annual Meeting

Tuesday, April 9

MDNA – Medicenna – Unspec. – AACR

AG – First Majestic – Through 4/11 – Gold Forum Europe

CMPS – Compass Pathways – 8:00am – Needham Healthcare Conference

Short Interest – After the close

Wednesday, April 10

Consumer Price Index – 8:30am

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $168.82) Vision Pro users can now enable up to five people to watch movies and TV shows, play games, collaborate, and hang out together. The feature requires VisionOS 1.1 and is enabled through the FaceTime app.

UBS said February iPhone sales were down 4% year-over-year, from 18.1 million to 17.4 million. They said “weak carrier upgrade rates” combined with the success of Samsung’s S24 series prompted a 9% drop in the US. China’s local smartphone brands, including Huawei, Xiaomi, Vivo, and Oppo, continued to gain market share, prompting a 16% year-over-year drop in iPhone sales. Huawei sales nearly doubled YoY. Sales in India were also down 13% year over year, but sales in Europe jumped 24% YoY.

UBS expects Apple to sell 51 million iPhones during the March quarter, down from 56 million last year. They maintained their Neutral rating and target price of $190. All this already is in the stock. That’s why I raised the AAPL buy limit to $175 for AI announcements at the Worldwide Developers Conference, new iPhone rollouts, and augmented/virtual reality products. I added the stock to the Short-Term Top Buys. It’s below the new buy limit – you know what to do.

Meta Platforms (META – $510.92) marked the 10th anniversary of their metaverse and AI work at Reality Labs. They’ve been far ahead of others in recognizing the importance of AI and the metaverse, and – most important – spending R&D money to do something about it. Ten years ago, Zuckerberg said: “Virtual reality was once the dream of science fiction. But the Internet was also once a dream, and so were computers and smartphones. The future is coming, and we have a chance to build it together.”

I like prescient CEOs. META is a Buy under $345 for a $400 target in 2024.

Small Tech

Fastly (FSLY – $12.59) introduced Fastly Bot Management to help organizations combat automated “bot” attacks at the edge and significantly reduce the risk of fraud, Distributed Denial of Service (DDoS) attacks, account takeovers, and other online abuse. This is an important cybersecurity milestone for the company, building on its proven bot mitigation expertise. They let the good traffic in and keep the bad traffic out, FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Rocket Lab USA (RKLB – $3.90) said their next launch will be from New Zealand during a 14-day launch window that opens on April 24th. Electron will carry two satellites for two separate customers: NEONSAT-1, an Earth observation satellite for the Satellite Technology Research Center at the Korea Advanced Institute of Science and Technology, and NASA’s Advanced Composite Solar Sail System. Rocket Lab will perform multiple in-space engine burns to deploy the two payloads to separate orbits several hundred kilometers apart. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

The XBI has corrected -12% over the past month but the tape has been weaker for a broad list of biotechs. The percentage of biotech stocks within 5% of a 52-week high has collapsed from 25% to 7%. The percentage above their 50-day moving average has been cut in half from 80% to under 40%. It’s typical of a new bull market to get 50% to 70% retracements before upleg resumes.

Click for larger graphic h/t @EdenRahim

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Compass Pathways (CMPS – $9.80) Board Chair and co-founder George Goldsmith and co-founder Ekaterina Malievskaia have resigned from the Board of Directors. I usually don’t comment on Board changes, but this is both notable and not in any way a negative. In eight years, they got the company to this level where the professional team they have installed can finish the job. George said: “It is time to turn my attention to the next phase of making this vision a reality for patients, providers, and health systems independent of any particular treatment modality.”

That sounds to me like they’ll be working on how to deliver therapies, not any competitor to Compass. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

ScyNexis (SCYX – $1.68) reported 2023 results and said SCY-247 will start a Phase 1 trial in the second half on 2024. Top line data from the CARES study has been received and is positive and consistent with previously disclosed results from interim analyses. Data analysis for the FURI study is ongoing.

The clinical study reports for FURI, CARES and NATURE in refractory invasive fungal infections are on target for delivery to GSK in the first half of 2024, which would trigger a $10 million development milestone payment to ScyNexis. They will get up to $30 million for the achievement of two interim milestones associated with their resumption and continued performance of the MARIO Study after the clinical hold is lifted, and another $7.35 million for the successful completion of the MARIO Study.

As I wrote on the Comments board, in their 10-K filing they said: “In response to the hold on clinical studies of ibrexafungerp by the FDA due to possible beta-lactam cross contamination, we have entered into certain new manufacturing agreements with third-party contract manufacturers to begin producing new batches of ibrexafungerp which we believe will allow us to lift the clinical hold and restart our impacted clinical studies, the Phase 3 MARIO study and a Phase 1 lactation study.”

The stock immediately jumped. They ended 2023 with $98.0 million in cash, which gives them a cash runway of “more than two years.” Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2024

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,310.90) set six straight record highs to close over $2,300 today for the first time ever. Silver just hit its highest level since March 2022. Is the long-awaited silver squeeze on the fraudsters happening? Costco is now selling silver bars in Canada with strict limits and no refunds.

Click for larger graphic h/t @KatusaResearch

Click for larger graphic h/t @KatusaResearch

Normally, gold goes up when the outlook for interest rates is lower, and gold goes down when the outlook shifts to higher. For the past few weeks, Treasury yields have trended higher and Wall Street gurus have trimmed their outlook for Fed rate cuts, yet gold has surged to an all-time high.

That tells you two things: (1) demand for gold is really strong; and, (2), something else may be going on. “Something else” may be the early recognition that $1 trillion in new debt every 90 days may keep the economy humming, but could be devastating for the dollar. We shall see. If you feel the need for actual gold or silver in your pocket, my friend Kieth Fitz-Gerald recommended Asset Strategies.

The fractal dimension said: “I am gold; hear me roar.” A new trend has started with a lot of energy to power it.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

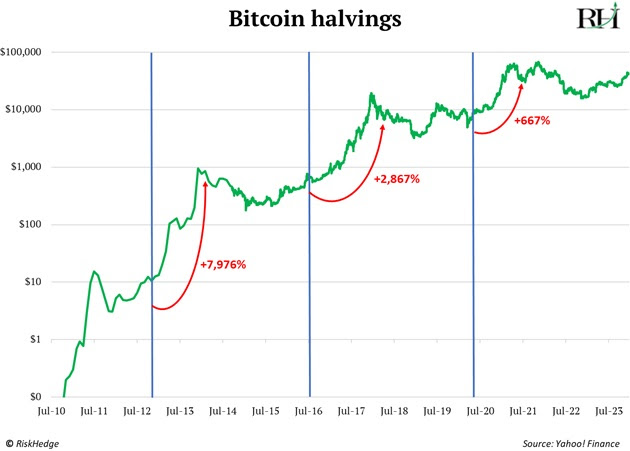

Bitcoin (BTC-USD on Yahoo – $67,506.73) halving is less than three weeks away. When bitcoin started in 2009, miners earned 50 BTC every 10 minutes (or “per block”). That’s the sole way new bitcoin is created.

Bitcoin’s creator programmed it to cut these rewards in half every four years. Hence the name “halving.” In 2012, rewards dropped to 25 BTC. Four years later, they were slashed to 12.5 BTC. The third halving happened in May 2020, with issuance being cut to 6.25 BTC.

This matters because each halving ignited a huge run-up in bitcoin’s price:

Click for larger graphic h/t @DisruptionHedge

Click for larger graphic h/t @DisruptionHedge

Bitcoin is volatile, no doubt, but you can use that to your advantage by adding a little on each big dip – like now.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

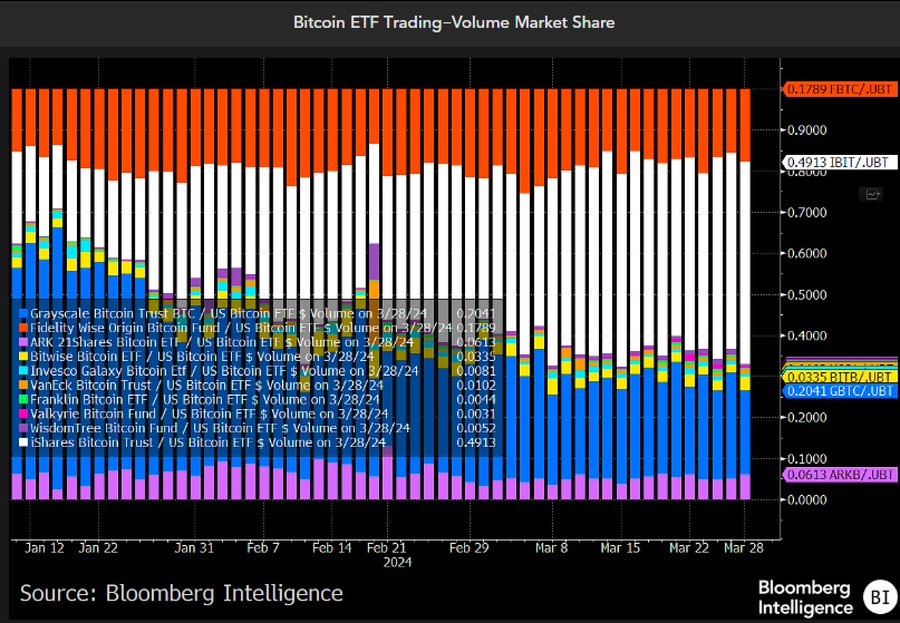

iShares Bitcoin Trust (IBIT- $39.08) has taken over the volume market share from the Grayscale Bitcoin Trust (GBTC). While all of the exchange-traded funds won in terms of being profitable, IBIT won the volume race and is officially the GLD of bitcoin. It’s basically a wrap.

Click for larger graphic h/t @JSeyff

Click for larger graphic h/t @JSeyff

IBIT is a Buy for the 2024 and 2028 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Ethereum Trust (ETHE- $24.16) would benefit from an SEC approval of spot ethereum exchange-traded funds, We moved one step closer to that when financial services giant Fidelity Investments filed a registration statement with the SEC yesterday. Fidelity said its Ethereum Fund would trade on the CBOE BZX Exchange. After BlackRock files, it should be a done deal. ETHE is a Buy under net asset value.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $86.53

Brent crude oil surged over $90 a barrel today for the first time since October as Israel put their embassies around the world on maximum alert for a retaliatory Libyan strike. This came on top of OPEC+ extending its output cuts, continued healthy demand, and Ukraine once again striking oil infrastructure targets deep inside Russia. Ukrainian drones hit the primary refining unit of Russia’s third-largest refinery southeast of Moscow, more than 700 miles from the front line. The refinery has a capacity to process 340,000 barrels per day (bpd) of crude. Its primary refining unit, with a capacity to process about 155,000 bpd, was hit in Tuesday’s attack and caught fire.

According to Reuters estimates, 900,000 bpd or 14% of Russia’s total refining capacity has been taken offline due to Ukrainian drone strikes.

Global oil inventories have only increased by four million barrels year-to-date. By this time last year they increased by 95 million barrels. That is a year-over-year change of one milllion barrels a day because the OPEC+/Saudi cuts are working. With the summer driving season just ahead and oil over $85, the Saudis may begin to bring back curtailed volumes in the secomd half of the year. But then the market narrative will gradually switch to falling spare capacity again, keepimg prices increasing.

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

Demand is strong.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

Although one source of demand is gone. The Biden Administration has canceled plans to refill the Strategic Petroleum Reserve due to high prices.

The July 2026 Crude Oil Futures (CLN26.NYM – $70.65) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $41.36) is a Buy under $40 for a $100+ target.

Freeport McMoRan (FCX – $49.18) is responding well to the run up in copper prices. There is much more to come. Do I hear $7.50?

Click for larger graphic h/t StockCharts.com

Click for larger graphic h/t StockCharts.com

FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

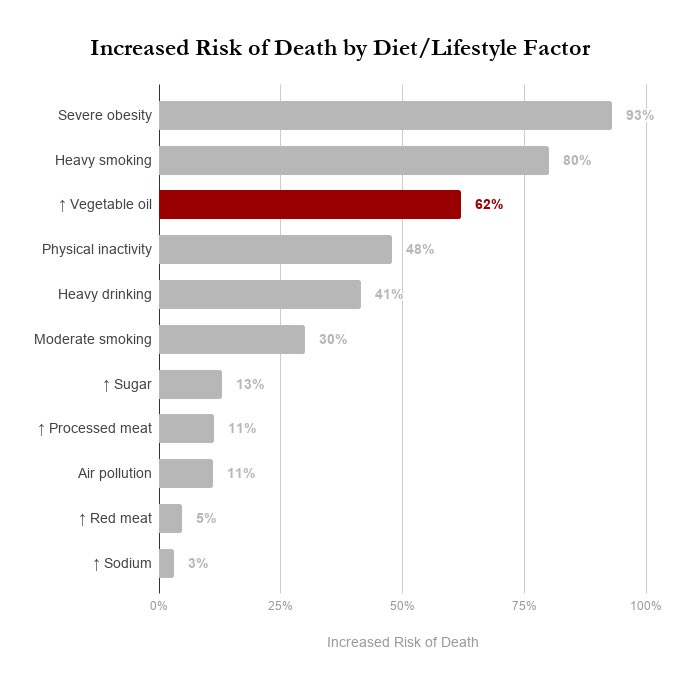

Seed Oils are enemy #1, then comes Sugars and Refined Carbs

Click for larger graphic h/t @bava23

Click for larger graphic h/t @bava23

* * * * *

Former Obama National Security Advisor turned BlackRock CEO, Tom Dillon, on the New World Order.

Click for larger graphic h/t @WillHild

Click for larger graphic h/t @WillHild

* * * * *

Your reading about The Coming of Neo-Medievalism and the Great Decentralization Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 4/4/24. Check out the complete Portfolio page HERE.

Portfolio Protection

April 30 SPY $505 put (SPY240430P00505000 – $3.91) swap for the June 21 SPY $505 put (SPY240621P00505000 – $8.33)

April 30 SPY $410 put (SPY240430P00410000 – $0.16) swap for the June 21 SPY $410 put (SPY240621P00410000 – $0.82)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $168.82) – Buy under $175 for new iPhones

Corning (GLW – $32.37) – Buy under $33, target price $60

Gilead Sciences (GILD – $69.55) – Buy under $80, target price $120

Meta (META – $510.92) – Buy under $345, target price $400

PayPal (PYPL – $64.54) – Buy under $68, target price $136

SoftBank (SFTBY – $28.22) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $7.73) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $55.03) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $12.59) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.10 – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $14.82) – Buy under $10, target price $40

Rocket Lab (RKLB – $3.90) – Buy under $13, target price $30+

Velo3D (VLD – $0.50) – Buy under $6, target price $50

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $4.40) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.51) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.43) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $9.80) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $11.95) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.32) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.68) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $14.46) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($27.25) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $25.98) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $31.95) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $21.28) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $30.08) – Buy under $30, target price $50

Coeur Mining (CDE – $4.34) – Buy under $5, target price $20

First Majestic Mining (AG – $7.50) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.44) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.36) – Buy under $10, target price $25

Sprott Inc. (SII – $38.70) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $67,506.73) – Buy

iShares Bitcoin Trust (IBIT – $39.08) – Buy

Ethereum (ETH-USD – $3,313.29 – Buy

Grayscale Ethereum Trust (ETHE – $24.16 – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $70.65) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $41.36) – Buy under $40; $100+ target

Vermilion Energy (VET – $12.59) – Buy under $11; $24 target

EQT (EQT – $36.76) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.63) – Buy under $8; $30 target

Freeport McMoRan (FCX – $49.18) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $31.37) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $21.70) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.25) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $26.52) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.55) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.04) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.70) – Hold for buyout

Invitae (NVTAQ – $0.004) – Hold for April 17 auction

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First

2

Repost of mine recently. MM, please evaluate.

Thanks. How can the US account for 50% of WW sales? The major economies are US, Canada, Australia/NZ, Europe, China, India, Japan, Asian Tigers, Russia. By population, the US is less than 10% of WW. What % of WW GDP is the US? I would say 20%. Any idea of the annual selling price of Vafseo without TDAPA? TDAPA bonus is only for 2 years, so for 8/10 or 18/20 of those years, ignore TDAPA to be conservative. Will the dominance of Amgen medically/politically/financially shut out much of the oral market for Vafseo and Daprodustat? How much cheaper will Vafseo be compared to Amgen’s IV ESA’s? It will take some time for Vafseo to increase sales to be a threat to Amgen. When do you think Amgen would buy AKBA?

How can the US account for 50% of WW sales? Two reasons:

1) The US GDP of $26.9T is 26% of the world GDP of $105T

https://www.visualcapitalist.com/visualizing-the-105-trillion-world-economy-in-one-chart/

2) The US allows drug companies to charge much higher prices than other countries do for the exact same drug (often more than double).

https://www.statista.com/chart/27932/us-prescription-drug-prices-in-international-comparison/

Oh, and the US’s 336M people account for less than 5% of the world’s 8 billion.

Thanks for your research. My estimates for 1 and 3 were pretty good. But 2 illustrates the political corruption from Big Pharma in the US. You can save big money by paying cash using GoodRx for many drugs, esp for generics. Insurance is a ripoff because many branded drugs are in high tiers with high copays and high deductibles for those high tiers. Sometimes a generic drug is in tier 2 for certain insurance plans, which is not subject to the deductible, whereas in other plans it is in tier 3 which is subject to a high deductible. Another option is Canadian pharmacies like PlanetDrugsDirect and Northwest Pharmacy which are middlemen for certified international pharmacies. You pay cash which is much lower than US retail prices, and also lower than using US insurance.

Mark Cuban’s costplusdrugs.com has the lowest prices I’ve found.

Thanks. Many common drugs aren’t listed. Just try various sources.

Most drugs get 50% of global revenues from the US. It’s a combination of higher prices than ROW nationalized healthcare systems, higher # of ptescriptions per capita, and a wealthier country,

Once the TDAPA period is over at the beginning of 2027, Vafseo will be pretty well entrenched in dialysis clincs and for home diaysis , where oral vs. IV is a big deal. Akebia will cut the price then to keep market share, and Vafseo is a better drug.

I think Amgen buys them before or soon after the launch.

Repost of another AKBA post of mine from today. MM, please address.

AKBA–ominous article of July 2023 about GSK deciding to withdraw marketing of Daprodustat outside Japan and US, due to poor sales. D was approved Feb 2023. Maybe the TDAPA process sabotaged them. AKBA is doing things right, and V is slightly better than D, but this is worrisome. What does everyone think?

Despite a positive opinion from local drug reviewers, GSK has decided not to bring its FDA-approved oral anemia drug daprodustat to Europe—or any additional countries for that matter.

Daprodustat, marketed as Jesduvroq in the U.S., earned backing from the drug evaluation committee at the European Medicines Agency a month ago. The recommended indication was for treating anemia associated with chronic kidney disease (CKD) in patients on chronic dialysis. From there, an official approval from the European Commission was largely considered a done deal.

But in reporting its second-quarter financial results (PDF) on Wednesday, GSK said it has decided not to commercialize daprodustat in Europe. The company said it will withdraw the application in Europe and won’t seek approvals in other territories. Besides the U.S., daprodustat is also available in Japan under the brand name Duvroq. It’s distributed there by Kyowa Kirin.

In making this decision, GSK cited the “significant reduction” in the size of the drug’s potential market opportunity, the fact that the EMA didn’t include non-dialysis patients

This looks like a power play to me – “You didn’t give us non-dialysis approval, so we’re taking our ball and bat and going home.” TDAPAA makes all the difference for Vafseo.

But GSK still loses by taking away Dapro sales outside US and Japan. Dapro was the first oral agent approved. Why would GSK cut off their nose to spite their face? Unless Dapro sales weren’t so great in the rest of the world. Vafseo is slightly better than Dapro, but why haven’t the Dapro sales for dialysis been good? Maybe I am wrong–what have been worldwide sales of Dapro?

Michael regarding PZG buyout price, does its expected sale price go up by .70 cents per share with each 100 increase in the price of gold, does the time line, November 2025, for Grassy laid out by PZG seem reasoanble? Thanks

The timeline is reasonable. The way I look at it is as the price of gold goes up, it increases the probability of a deal more than it increases the price of a deal. Seabridge (SA) might make the first offer – CEO Rudi Fronk is Chairman of PZG’s Board.

Michael, is it a reasonable possibility that PZG may not be bought out for much more than its all-time high?

I don’t think they’d sell it that cheap after all this work. They could sell one mine and keep the other, but even that’s not likely.

Thank you.

APTO – Notice of Delisting or Failure to Satisfy a Continued Listing Rule or Standard; Transfer of Listing

On April 2, 2024, Aptose Biosciences Inc. (the “Company”) received a letter (the “Notification Letter”) from The Nasdaq Stock Market (“Nasdaq”) stating that the Company was not in compliance with Nasdaq Listing Rule 5550(b)(1) (the “Rule”) because the stockholders’ equity of the Company as of December 31, 2023, as reported in the Company’s Annual Report on Form 10-K filed with the SEC on March 26, 2024, was below the minimum requirement of $2,500,000. Notwithstanding the Notification Letter, the Company believes that following the closing of its financings on January 30, 2024 and January 31, 2024, respectively (the “Financings”), as disclosed in the Company’s recently filed Annual Report on Form 10-K that as of the dates of the closing of the Financings that the Company’s stockholders’ equity exceeded $2,500,000.

As of the date of this Current Report on Form 8-K, the Company does not have a market value of listed securities of $35 million, or net income from continued operations of $500,000 in the most recently completed fiscal year or in two of the last three most recently completed fiscal years, the alternative quantitative standards for continued listing on the Nasdaq Capital Market.

The Notification Letter received has no immediate effect on the Company’s continued listing on the Nasdaq Capital Market, subject to the Company’s compliance with the other continued listing requirements.

Pursuant to Nasdaq’s Listing Rules, the Company has 45 calendar days (until May 17, 2024), to submit a plan to evidence compliance with the Rule (a “Compliance Plan”). The Company intends to submit a Compliance Plan within the required time, although there can be no assurance that the Compliance Plan will be accepted by Nasdaq. If the Compliance Plan is accepted by Nasdaq, the Company will be granted an extension of up to 180 calendar days from April 2, 2024 to evidence compliance with the Rule.

In the event the Compliance Plan is not accepted by Nasdaq, or in the event the Compliance Plan is accepted but the Company fails to evidence compliance within the extension period, the Company will have the right to a hearing before Nasdaq’s Hearing Panel. The hearing request would stay any suspension or delisting action pending the conclusion of the hearing process and the expiration of any additional extension period granted by the panel following the hearing.

The Company intends to submit the Compliance Plan on or before May 17, 2024, monitor its stockholders’ equity and, if appropriate, consider further available options to evidence compliance with the Stockholders’ Equity Requirement.

Thanks. APTO will do more reverse splitting and subsequent big dilution to avoid delisting and fund the trials. As your earlier post indicates, 4x dilution is expected, so a reasonable buy price in early 2027 will be 1/4 of today’s $1.60, or 40 cents.

No reverse split here, as the stock trades over $1 a share. The problem was Shareholder’s Equity under $2.5 million, and they’ve already fixed it.

But as Brent said, huge dilution will be necessary to raise enough money for APTO to survive until possible approval in 2027 or later. 4x dilution will get the stock down to 40 cents without reverse split.

VLD – a poster on the YMB indicated that this Sunday’s Barron’s includes a rumor of GE Aerospace acquiring VLD. I don’t have a Barron’s subscription so can’t verify but it certainly makes a lot of sense. GE Aerospace has far more resources than any of Velo’s 3D competitors so is best able to maximize Velo’s technology and Velo’s market niche in defense & aerospace is perfect for GE Aerospace.

I don’t see any reference to GE buying VLD in the paper version of Barron’s delivered this morning. Neither GE nor VLD are in the index of companies mentioned on page 4. I wouldn’t think VLD would be large enough (market cap $120MM) to rate a mention. For GE it wouldn’t move the needle – I don’t really think of Barron’s as a “rumor” periodical.

So the poster may ultimately be right…some day…

For GE Aerospace, it probably WOULD move the needle.

https://3dprintingindustry.com/news/ge-aerospace-to-scale-the-production-3d-printed-jet-engines-with-650-million-investment-228977/

“GE Aerospace is not the only company working to scale the production of aerospace components with additive manufacturing…Elsewhere, Aerospace and defense contractor Lockheed Martin, metal 3D printer manufacturer Velo3D and aerospace part inspection company Vibrant collaborated with the US Department of Defense’s (DoD) LIFT Institute.

Through this collaboration, the partners assessed the validity of 3D printing hypersonic ramjet engines.

Velo3D Announces Proposed Public Offering

https://ir.velo3d.com/news-events/press-releases/detail/144/velo3d-announces-proposed-public-offering

Not a surprise given Velo indicated in their 10-K that “the Company expects that it will need to engage in additional financings to fund its operations and satisfy its obligations in the near-term. The Company is in discussions with multiple financing sources to attempt to secure additional financing.”

Brent, MM, others–Is this announcement a negative, or actually a positive for buying time until more orders come in to get to profitability in a reasonable time?

A necessary evil that buys them additional time. Like a number of the biowrecks Velo is now in dilution hell.

They issued 70 million additional shares in 2023 and have now added 34 million more this year. Unfortunately, because their share price is so low each stock sale only seems to buy them about a quarters worth of time. How far is $12 million going to get them when they’ve forecast sales of only $6M to $11M for Q1? They’ll have substantial cash burn with sales that low.

Additionally, most of these stock sales come with an associated warrant. Velo had 50 million in warrants outstanding at the end of 2023 and have added another 56 million more in 2024 between the note amendment announced last week & this stock sale. The vast majority of which have trigger prices under $1. While not immediately dilutive, they will provide headwinds to stock appreciation & will likely be in the money & become dilutive if Velo is acquired.

I don’t see any short-term positive catalysts. Without an acquisition Velo will almost certainly need to do a reverse split in the next few months for listing purposes and will, in all likelihood, follow that up with another capital raise & warrant issue given their poor Q1. I also expect a lowering of 2024 guidance on their Q1 call as I can’t see them hitting the bottom of their 2024 revenue guidance given such low Q1 revenue numbers.

Despite the prospect of a pop on a buyout, this doesn’t look at all compelling to me at the moment given the risk of additional dilution. I’ll reevaluate after their Q1 call, reverse split, and next capital raise. I hate dilution. It’s so erosive to an investment.

I bought 598 @$1.67 of SCYX and 650 @$2.77 of ADPT today. ADPT is a AI centric company which focuses on biotechnology companies and shortens the pathway to FDA approvals. And it’s extremely out of favor since the shift out of growth stocks over the last few years. It’s down 70? Percent over the last couple of years. Highly speculative but a grand slam if it gets back up to its high. Also has good revenue.

Hi John thx for the ADPT tip, what’s your price goal and timeline for SCYX, I’m debating a buy?

I am sticking with MM’s $20 target. But I am not good with timeframes? Especially with everything going on in the market in the short term. The inflation boogeyman came out again today and the algorithms beat up everyone’s pizza pie. So Powell will now have some sleepless nights thinking about his next moves with interest rates. MM is forecasting a mild recession. He may get his wish after a day like today. On a brighter note. ACRDF is up some 95 percent since I ventured into the weeds some days ago. Also hot of the press is news that Samsung is getting 6.6 Billion from the US government to build giant fab manufacturing in the US. And it’s NOT even an American company!! If Intel gets a mother load like that I can only imagine what will happen to INTC stock!

MM,

The results seemed pretty good, but the stock is down 13% currently. Any thoughts?

Medicenna Presents Updated Preclinical Data on MDNA113, a First-in-Class, Targeted and Masked Bi-functional anti-PD1-IL2 Superkine, at the 2024 Annual Meeting of the American Association for Cancer Research (AACR)

12:01 PM ET 4/9/24 | GlobeNewswire

Medicenna Presents Updated Preclinical Data on MDNA113, a First-in-Class, Targeted and Masked Bi-functional anti-PD1-IL2 Superkine, at the 2024 Annual Meeting of the American Association for Cancer Research (AACR)

MDNA113 is targeted to the tumor site where it is activated to simultaneously deliver two immunotherapies, an IL-2 superkine and anti-PD1 antibody, to the same cancer fighting immune cells in the tumor micro-environment (TME) to maximize efficacy and minimize systemic toxicity

MDNA113 is our most advanced pre-clinical candidate that targets IL-13R2, a tumor associated antigen, which is overexpressed by immunologically “cold” tumors with high unmet needs in pancreatic, prostate, ovarian, breast and brain cancer affecting over two million patients every year

TORONTO and HOUSTON, April 09, 2024 (GLOBE NEWSWIRE) — Medicenna Therapeutics Corp. (“Medicenna” or the “Company”) (TSX: MDNA), a clinical-stage immunotherapy company focused on the development of Superkines, today announced new preclinical data on MDNA113, the Company’s novel T-MASK (Targeted Metallo/protease Activated SuperKine) candidate, an IL-13R 2 (Interleukin-13 receptor alpha2) specific superkine featuring unique masking and tumor targeting characteristics, were presented at the 2024 Annual Meeting of the American Association for Cancer Research (AACR) held in San Diego, CA, on April 9(th) , 2024.

“We are pleased to show preclinical data demonstrating the ability of Medicenna’s first T-MASK candidate, MDNA113 to enhance tumor accumulation and tolerability of our potent bi-functional immune modulator, anti-PD1-IL-2(SK) ,” said Fahar Merchant, Ph.D., President and Chief Executive Officer of Medicenna. “MDNA113 has novel features, including the tunable blockade of the IL-2R agonism to reduce peripheral immune stimulation for enhanced tolerability, and tumor targeting to IL-13R 2 which is linked to aggressive cancers that annually affect over 2 million patients world-wide. The cleavage and release of the IL-13 tumor-targeting/masking domain by matrix metalloproteases restores IL-2R signaling within the tumor microenvironment, thereby benefiting from the simultaneous and synergistic activity of IL-2R agonism and immune checkpoint blockade at the tumor site.”

The Company selected MDNA113, a novel, first-in-class tumor-targeted and tumor-activated bi-functional anti-PD1-IL-2 superkine with high selectivity and affinity for IL-13R2, a tumor associated antigen expressed in many aggressive solid tumors. The IL-13 Superkine (MDNA213) is a highly specific tumor-targeting/masking domain which is fused via a protease sensitive linker to a bi-functional immunotherapy domain (MDNA223) containing an IL-2 Superkine fused to an anti-PD1 antibody.

Key findings presented at the conference include:

— When not activated, MDNA113 shows reduced IL-2R agonism with no change to

PD-1/PDL-1 blockade activity.

— Cleavage and activation of MDNA113 by cancer specific enzymes

(metalloproteases) releases the T-MASK domain (MDNA213), restoring

activity of the IL-2 Superkine at the tumor site.

— MDNA113 shows attenuated systemic lymphocyte expansion compared to

non-masked version (MDNA223), consistent with design of MDNA113.

— MDNA113 is better tolerated than non-masked counterpart (MDNA223),

supporting higher and more efficacious dosing schedule.

— MDNA113 selectively binds IL-13R 2 positive tumor cells in vitro, and

durably accumulates (>7 days) in IL-13R 2 positive tumors in mice.

— Cleavable MDNA113 shows similar efficacy as non-masked MDNA223 in mouse

tumor models by either localized (intra-tumoral) or systemic

(intra-peritoneal) delivery, consistent with proteolytic activation

within TME.

— Single neoadjuvant treatment with MDNA113 in a highly invasive orthotopic

4T1.2 breast cancer model significantly increases survival by preventing

metastasis.

— In summary, the T-MASK platform exemplified by MDNA113, facilitates tumor

targeting and minimizes systemic toxicity while maximizing therapeutic

activity at the tumor site.

The poster, “Characterization of MDNA113, a Tumor-Targeting Anti-PD1-IL-2(SK) Immunocytokine with Conditional Activation to Increase Tolerability and Maximize Efficacy” can be found on the AACR website for conference registrants. It will be also available on the Scientific Presentations page of Medicenna’s website following the conclusion of the 2024 Annual Meeting of AACR.

About the T-MASK Platform

Medicenna’s novel T-MASK (Targeted Metallo/protease Activated SuperKine) platform involves fusion of a dual tumor-targeting/masking domain to an immune modulator (such as a Superkine or a BiSKIT) via a matrix metalloprotease (MMP) sensitive linker to (i) reduce and fine-tune the potency of the immune modulator, (ii) increase its systemic tolerability (iii) prolong its retention in the TME and (iv) to maximize and restore full potency at the intended target site. The T-MASK platform offers opportunity to target and fine-tune immune cell stimulation in the TME to improve the therapeutic index of Medicenna’s Superkine and BiSKIT platforms.

About MDNA113

MDNA113 is a novel, first-in-class tumor-targeted and tumor-activated bi-functional anti-PD1-IL-2 Superkine with high affinity for IL-13R2 without binding to the functional IL-13R 1. IL-13R2 is overexpressed in a wide range of solid tumors, including cold tumors. IL-13R2 is a tumor-associated antigen with minimal to no expression in normal tissues but is highly expressed by a wide range of tumors including “cold” tumors. IL-13R2 expressing tumors also have abundant MMPs in the TME that may efficiently activate MDNA113. IL-13R2 expression is associated with poor clinical outcome in multiple tumor types with an annual world-wide incidence of over 2 million in different tumor types including prostate cancer, pancreatic cancer, ovarian cancer, liver cancer, breast cancer and brain cancer, and among others.

Velo3D The securities were sold to new and existing institutional investors at an offering price of $0.35 per share

https://finance.yahoo.com/news/velo3d-announces-pricing-12-million-123900535.html?

Valuation for AKBA, 2 methods.

Summary–If peak V sales are $375 million or $600 million, use a 4X price/sales multiple for a market cap of $1.5 or $2.4 Billion. That’s a target price of $7.5 or $12, assuming no dilution. In 3-5 years. Brent would cut the target several fold due to dilution only. At 2X dilution, that’s $3.75 or $6. Hold, or accumulate shares as cheaply as possible, well under the present price of $1.50.

Comments, please.

I haven’t made any comments regarding AKBA & dilution.

AKBA only increased outstanding shares by 10 million in 2023. In early 2024 they sold an additional 13.26 million shares for $19.2 million, which used up their Jeffries ATM. These were each roughly 5% dilution events so no biggie. AKBA has guided that they now have enough cash to fund them for the next 24 months so I’m not expecting any new short-term dilution events.

Now Velo, that’s another story…

Brent, I am acknowledging your major criticism of most speculative stocks–dilution, dilution, dilution. For AKBA, you are correct that so far, dilution has been minor. However, a few posters on YMB note that worldwide sales of Dapro and Vafseo have declined in the past 2-3 years. As a result, GSK is scaling back its marketing of Dapro to the US and Japan only. This is my major worry about AKBA and its drug, Vafseo. Why have sales for Dapro and Vafseo declined? If V is slow at the launch and next 2 years, profitability will be delayed much more than anticipated. The stock could plunge for 2 reasons–big losses, need for dilutions.

Ignoring possible future dilution, are my assumptions about valuation reasonable to you?

New World Investor for 4.11.24 is Posted