Dear New World Investor:

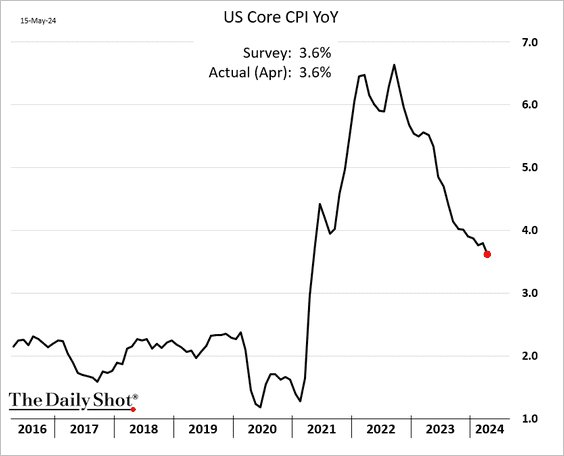

The headline Consumer Price Index increased 3.4% year-over-year in April, a tick slower than March’s 3.5% and right on the consensus estimate. The month-over-month change was 0.3%. Year-over-year core inflation, leaving out food and energy, was +3.6% in April, down from +3.8% in March. Monthly core inflation was +0.3%, also a bit lower than March’s +0.4%.

Click for larger graphic

Click for larger graphic

As usual, the lagging shelter component, 44% of the index, accounted for much of the increase. Inflation is below 2% if the Bureau of Labor Statistics used current rents.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

The easy declines from unwinding the supply chain mess are behind us, and shelter costs will fall steadily for the next 12 months. But the Fed wants to see at least three months of much lower inflation, reasonably headed for 2.0%, before they cut rates. Wall Street is still pricing in a 53% chance of a cut in September, but I think they’re dreaming. I doubt there will be any cuts before the December meeting, after the election, and probably none this year. But – bonds, stocks, gold, and bitcoin all rallied. I’ll take it.

BofA’s fund manager survey is the most bullish it’s been since November 2021, but still has room to move higher:

Click for larger graphic

Market Outlook

The venerable Dow Jones Industrial Average broke 40,000 for the first time ever today but couldn’t hold it. The S&P 500 added 1.6% since last Thursday, closing above 5,300 for an all-time high on Wednesday and setting an all-time intraday high at 5,325.49 today. The Index is up 11.1% year-to-date. The Nasdaq Composite gained 2.2% to a new record close of 16,742.39 — its first record since April 11. It is up 11.2% for the year.

Over the last 50 years, the Nasdaq is 35-15 in the month of May for a median gain of 1.44%. As of May 11, the Nasdaq was up 4.36% since May 1, which history suggest bodes well for additional upside in the remainder of May. In those 13 years of the last 50 in which May was up at least 2% as of May 11, the remainder of the month was 13-0 for a respectable average gain of 2.82%.

Click for larger graphic h/t @WayneWhaley1136

Click for larger graphic h/t @WayneWhaley1136

The SPDR S&P Biotech Exchange-Traded Fund (XBI) won the week, climbing 4.1%. It is only up 3.7% year-to-date, though. The small-cap Russell 2000 notched a 1.1% gain and is up 3.4% in 2024.

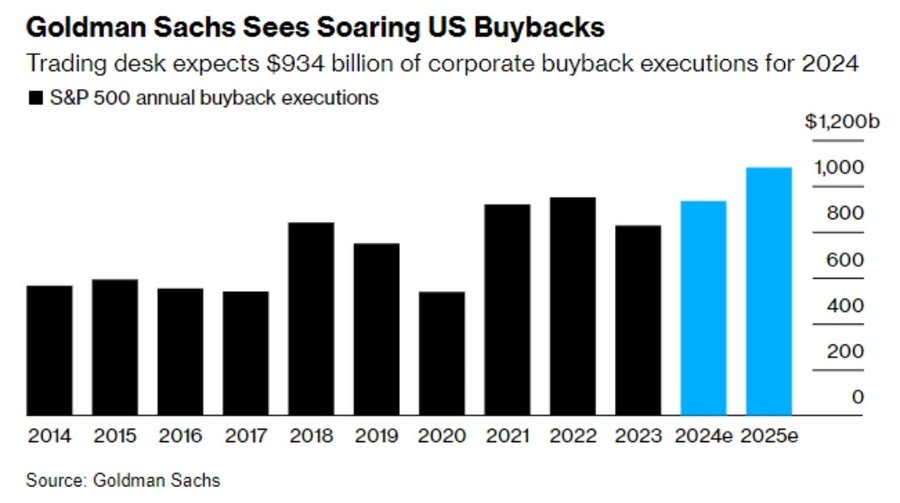

The buyback bid is back and it is big. Companies might be front-loading the approximate $5.5 billion scheduled daily buying. This bid is present until June 14. Goldman Sachs thinks strong corporate cash flow will fund 2025 US stock buybacks at an all-time high $1.1 Trillion.

Click for larger graphic h/t @WinfieldSmart

According to BofA: “Companies are stepping up repurchases of their own shares, which is giving a resurgent stock market an extra boost. S&P 500 companies that have reported first-quarter results as of Monday have disclosed buying back $181.2 billion of their shares, up 16% year-over-year…The pace of purchases has been brisker than usual for nine straight weeks…”

The fractal dimension is back in trend mode but out of energy for another big run. It really needs to consolidate, either by a drop to lower prices or just churning around current levels for a couple of months.

Sell in May and go away? This graphic shows the results of strategies where you sell US equities at the end of April and buy back at the end of August, either keeping the proceeds in zero interest cash or the US Treasury index. For the rest of the year you stay fully invested in equities. It worked for a while.

Click for larger graphic h/t The Market Ear

Click for larger graphic h/t The Market Ear

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements at June WWDC and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model March quarter real GDP estimate updated this morning was +3.6%.

Click for larger graphic

We appear to be in or in danger of what VanEck has described as “fiscal dominance.” Fiscal dominance is an economic condition that arises when debts and deficits are so high that monetary policy loses traction. This is because as debt service costs rise beyond a certain level, fiscal deficits obviously rise, but their main policy implication is that they create the need for more monetary financing. The main driver of money creation becomes fiscal policy (“fiscal dominance”), and traditional tools like higher policy rates only feed inflation and inflation expectations (by increasing debt servicing costs), rather than starve them.

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Monday, May 20

INO – Inovio – 12:30pm – H.C. Wainwright BioConnect Investor Conference

AKBA – Akebia – 3:00pm – H.C. Wainwright BioConnect Investor Conference

Tuesday, May 21

GLW – Corning – 8:50am – JPMorgan Global Technology, Media, and Communications Conference

INO – Inovio – 9:00am – Annual meeting

ENVX – Enovix – 4:35pm – JPMorgan Global Technology, Media, and Communications Conference

Wednesday, May 22

PYPL – PayPal – 11:00am – Annual meeting

Thursday, May 23

ENVX – Enovix – Unspec. – B. Riley Institutional Investor Conference

AG – First Majestic – 1:00pm – Annual meeting

Friday, May 24

Short Interest – After the close

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $189.84) and OpenAI are partnering to put ChatGPT features in iOS 18, Apple’s next iPhone operating system, to create an AI foundation for the iPhone 16 coming in September. That’s according to Dan Ives at Wedbush, who maintained his Outperform rating and $250 target price. He wrote: “While Apple has been in discussions with Google AI for a partnership for Gemini, the golden goose for Cook and Cupertino was to have exclusive OpenAI and ChatGPT-powered AI features in iOS 18 and ultimately embedded in the upcoming iPhone 16 launch this September.”

Ives expects the OpenAI partnership to be formally unveiled at Apple’s Worldwide Developers Conference starting June 10. He expects it to consist of an OpenAI Chatbot with exclusive features that build upon on-device Apple large language models. He thinks a collaboration with OpenAI opens up several avenues and revenue opportunities for Services. For example, an advanced Siri technology with OpenAI that can do complex tasks will eventually be a separate monthly subscription service, along with other AI features.

I actually see a deal as a sign of weakness – Apple should have the in-house technology to put AI into iPhones, but the must have missed the boat. There’s also a question of what the economics will be – OpenAI, and Microsoft behind the scenes, probably want a cut of the Service revenues from Apple’s 2.2 billion installed base. We shall see.

Meanwhile, for you golfers, the Apple Watch is the perfect golfing companion. They say: “The high-frequency motion API released in watchOS 10, which takes advantage of the latest accelerometer and gyroscope in Apple Watch to detect rapid changes in velocity and acceleration, has equipped developers such as Golfshot with tools to create innovative new experiences that help users improve their golf swing and performance.

“For swing practice, Golfshot’s new Swing ID On-Range experience, launching today, utilizes this API to detect the precise moment the club strikes the ball. Apple Watch sensors also offer a comprehensive analysis of a golfer’s swing from the beginning to the end of the motion, and users of any skill level can track key swing metrics with precision, including tempo, rhythm, backswing, transition, and wrist path, to improve their gameplay.”

AAPL is a Buy under $175 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $67.86) presented at both the BofA Health Care Conference (AUDIO HERE and TRANSCRIPT HERE) and the RBC Global Healthcare Conference (AUDIO HERE and TRANSCRIPT HERE). At the BofA conference, the CFO said Kite can return CAR-T treated cells for reinfusion into the patient in 14-17 days, while competitors take 30-45 days. The patients are often in an explosive stage of their cancer and simply can’t wait that long.

On the HIV market, he said that Biktarvy, now a $12 billion a year drug, is the recognized gold standard. It’s a combination of three active agents, all of which work against the virus in different ways. There is no resistance developing to Biktarvy, unlike many other therapies. You don’t have to genotype patients before you start on Biktarvy. After five years, 98% of patients that are treated on Biktarvy still have viral load reduction to the targeted level. In the March quarter it picked up another three percentage points of market share and now is used in 49% of HIV patients in the US. The market overall is growing 2% to 3% a year, and Biktarvy is patent protected to 2033. Gilead has nine more HIV drugs in the clinic.

The Chief Commercial Officer presented at the RBC conference. She said some 2025 negative changes in Medicare Part D drug reimbursement for HIV therapies will be offset by market and market share growth, so they expect a flat 2025 from this one-time reset, followed by resumed growth in 2026.

Trodelvy has the leading share in second-line metastatic triple-negative breast cancer, but only about 1/3 of the patients are getting Trodelvy. There’s still 2/3 of patients that are not – they’re getting chemotherapies, even though Gilead has clearly shown better overall survival data over chemo. So they think they have a lot of room to grow just in triple-negative breast cancer. Plus they will move up to first-line status. Bladder and lung cancer other growth paths for Trodelvy. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $473.23) is shutting down Workplace, its enterprise communication tool, effective August 31, 2025. They said they are discontinuing Workplace to focus on building AI and metaverse technologies that will fundamentally reshape the way we work. META is a Buy under $345 for a $400 target in 2024.

SoftBank (SFTBY – $27.01) reported March fourth quarter revenues up 3.5% from last year to $11.23 billion and returned to profitability with $2.11 billion in net income versus a $202.56 million net loss last year. The recovery was driven by a big swing at the Vision Fund due to the ARM initial public offering.

The full fiscal year loss improved from $6.23 billion in 2023 to $1.46 billion. On the conference call (VIDEO HERE and 126 SLIDES HERE and TRANSCRIPT HERE), CFO Yoshimitsu Goto said the Vision Fund now holds positions in 500 companies, of which 50 have gone public. He said : “I have a different view on the risk, because our risk is not changing. Changing is the biggest risk hedge that the company can do.”

Bloomberg reported that CEO Masayoshi Son has been selling down stakes of publicly traded Vision Fund companies to fund a further push into AI, semiconductors, and related hardware. The Vision Fund has sold stakes in DoorDash, Coupang, and Grab Holdings.

Deutsche Bank upgraded their rating to Buy based on Masa’s accelerating ambitions in artificial intelligence. They said the company is reportedly looking to invest over $900 million in hardware to build a large language model with one trillion parameters, with the construction of the third phase happening in the second-half of this year. For comparison purposes, OpenAI’s GPT-4 has roughly 1.7 billion parameters. SoftBank will monetize its investment by leasing computational power, applications, and solutions. They wrote: “We see the company as well positioned in AI, given its investment and access to so much media and consumer content. We see investors valuing such business, and especially AI, highly, and expect SoftBank’s position in the market to get attention.”

For a negative and I think too short-term take on the quarter, see this Seeking Alpha article: SoftBank Group Q4 Earnings Review: High Risk For Low Reward.

If the market won’t pay up, Masa will just keep buying back stock. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $9.19) has begun customer sampling of its breakthrough EX-1M battery. The initial samples were built and tested at the Fremont facility for Internet-of-Things and smartphone customers. They will build a larger number of EX-1M samples from the Agility Line at Fab2 in Malaysia later in the current quarter. They plan to consolidate manufacturing of all silicon batteries in Malaysia by July. That puts them on a path to reduce fixed costs by over $35 million annually, significantly reducing capital needs and accelerating the path to profitability.

South Korea pledged $7 billion to help wean its EV battery supply chain away from China and align with US trade rules. The aid, which involves cheaper state loans and tax incentives, is also for supporting the development of alternatives to replace graphite. Enovix acquired South Korea-based Routejade last year. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

QuickLogic (QUIK – $12.10) reported revenues up a whopping 45.5% from last year to $6.01 million, just under the $6.2 million consensus estimate. It was driven by a nearly 60% increase in new product revenue. Pro forma earnings of 11¢ per share more than doubled the 5¢ estimate and marked their third straight quarter of pro forma profitability.

On the conference call (AUDIO HERE and PREPARED REMARKS HERE and TRANSCRIPT HERE), CEO Brian Faith said: “With continued strong bookings, a record $179 million funnel and some very significant eFPGA contract proposals pending, we remain confident that we’ll deliver greater than 30% year over year revenue growth in 2024.”

They are projecting June quarter revenue will be up significantly year over year, but a sequential decrease from Q1 to the low point for this year. They continue to be cash flow positive and solidly profitable for the full year. June quarter revenue should be up 55% from last year to $4.5 million, with pro forma earning from breakeven to three cents a share.

They have a major system-on-a-chip (SOC) contract shipping now where their eFPGA technology is used for AI acceleration, which is a necessary function in most AI applications. This will be a rapidly growing application that is better served by eFPGA technology than a processor running the acceleration algorithms in software. eFPGA IP can be reprogrammed to adapt to changes in acceleration algorithms and performs acceleration more quickly using much less power than a processor-based solution.

QUIK is a Buy up to $10 for my $40 target as their earnings repeatedly surprise Wall Street.

Primary Risk: Customers’ product introductions and associated royalties are unpredictable.

Velo3D (VLD – $0.22) reported the March quarter I wanted to see, even though it was down from last year.. Revenues were down 63.3% from last year to $9.8 million. They had a pro forma loss of eight cents a share compared to last year’s nine-cent profit. But on the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), management pointed to $17 million of order bookings in the quarter, with 50% from existing customers, an indication that they are (1) satisfied with their current machines and level of support; and, (2) not worried about the company’s survival. Velo3D ended the quarter with $22 million in backlog, which will give them 30% sequential revenue growth to ~$12.7 million in the June quarter. They added three new defense sector customers this quarter.

Click for larger graphic

They are executing well on their cost reduction goals. Excluding one-time charges, quarterly operating expenses were down 30% year-over-year and down 15% from the December quarter. Management said they are on track for their quarterly cost reduction goals for the rest of this year.

Click for larger graphic

Click for larger graphic

Best of all, operating cash flow improved 35% year-over-year. They said they are “well positioned to achieve cash flow breakeven in the second half of FY 2024.” They will do that in two ways. The first is to improve the gross profit margin on every machine shipped:

Click for larger graphic

Click for larger graphic

The second is to cut OpEx so more of the gross margin hits the bottom line.

Click for larger graphic

Click for larger graphic

My spreadsheet now looks like this:

Click for larger graphic

Click for larger graphic

I am assuming 40% sequential revenue growth in the June quarter, followed by 50% growth in the September period and 60% in the fourth quarter. That’s really aggressive, but it only gets me to $77 million for the year and their guidance is for $80 to $95 million. As I’ve been saying, revenue growth is the key to everything else, so my bottom-line numbers probably are lower than their targets.

I took their gross margin guidance for the year to calculate gross profit. Selling expenses are, to a large part, dependent on revenue because the salespeople are on commission. They’ll squeeze General & Administrative expenses a bit more.

Cutting R&D to $3 million a quarter will help short-term cash flow and not endanger them for a couple of years, but in the long run they need to get the gross margin up to 40% – price increases can help there – to fund 15% Selling, General & Administrative expenses and 10% R&D, leaving 15% for net pretax profits. That’s been the successful technology model for decades.

I have 2024 operating expenses totaling $56.9 million, above the company’s guidance for $49 million to $50 million. I will be interested to see what gets cut further in the June quarter.

I have the pro forma loss per share improving by a penny a quarter. Note that the number of shares increases about 15 million a quarter due to stock-based compensation. The company expects to be cash flow positive in the second half of 2024, but I don’t see that yet. I’ll update the spreadsheet after the June quarter results.

Please note that all spreadsheets are not forecasts, they are a means to understand how a company works and what the levers are for improved results.

They continue to win orders due to superior technology. In the graphic below, the turbo fan part on the left was a demonstration part built on the Sapphire XC to show the dramatic reduction in construction time compared to investment casting. The hear exchanger is the middle is a part produced by an existing customer. The ramjet on the right was for a competitive bidding situation where they creamed the competition. Velo3D is engaged with the Department of Defense, which wants to see US-based additive manufacturing widely deployed.

Click for larger graphic

Click for larger graphic

Velo3D has an enormous lead in 3D printing technology, which is crucial for defense and aerospace applications, and will have widespread use in virtually all manufacturing. VLD is a Buy up to $1 for my $10 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Aptose Biosciences (APTO – $1.19) reported a March quarter loss of $9.6 million or 73¢ per share. That was better than the consensus for an 81¢ loss and much better than last year’s $13.7 million loss. On the very detailed conference call (AUDIO and SLIDES HERE and SLIDES HERE and TRANSCRIPT HERE), they laid out their plans for the tuspetinib/venetoclax/hypomethylating agent (TUS/VEN/HMA) triplet drug development, which provides an important opportunity for us to examine the investment case for development-stage biotech companies.

First, I believe the TUS/VEN/HMA triplet therapy will be the best first-line therapy for Acute Myeloid Leukemia (AML) patients, replacing VEN/HMA and saving or extending lives. I think the FDA wants to see the drug approved and Aptose will get approval. If I didn’t think the clinical evidence supported that, I would say sell the stock. If I’m wrong and the triplet fails a clinical trial, we will sell the stock – undoubtedly at a big loss. That’s what happens when drugs don’t work. So I agree with this slide:

Click for larger graphic

Click for larger graphic

And I agree with the investment thesis on the left, below. The problem – for all development-stage biotechs – is in the milestones on the right.

Click for larger graphic

Click for larger graphic

Aptose has $9.3 in cash, which basically is out of money, starting a Phase 1 trial this summer, and planning a Phase 2/3 trial start in December 2025. That won’t require a lot of patients, maybe 200 or so, and will enroll quickly. But at best that means applying for FDA approval around mid-2026 with a six-month PDUFA date in early 2027.

A venture capitalist looking at this would realize they need to participate in three or four rounds of funding to get to cash flow positive, at which point they’ll own part of a company worth $1 billion or more. Each round would be at a higher valuation, giving them an unrealized gain.

But in the public markets, Aptose closed today with only a $20 million market capitalization. They probably need $40 million a year to stay alive and run the trials. The public market usually does not pay up for Phase 1 results, although they will for strong Phase 2 results. So Aptose is going to have to sell a lot of stock to get to the goal line.

That means either you don’t want to own APTO at all OR you are willing to participate in every financing for the next four years to keep your position from being diluted into insignificance. I think it’s worth the risk, but your mileage might vary. APTO is a Buy under $2.50 for a $300 target in a buyout.

Primary Risk: The TUS/VEN/HMA triplet fails in clinical trials.

Clinical stage of lead product: Phase 1

Probable time of first FDA approval: 2027

Probable time of next financing: Mid-2024

Editas Medicine (EDIT – $5.89) did a fireside chat at the RBC Capital Markets Global Healthcare Conference (AUDIO HERE and TRANSCRIPT HERE). CEO Gilmore O’Neill said: “I have been very lucky in my career. I’ve had six drugs that I’ve directly had my hands on that were approved. I have never seen efficacy like we see here. And I’m not just talking about our product, I’m talking about gene edited – CRISPR gene edited products, which we got, where you have essentially a response rate of 100%, biological response with 100% and almost 100% clinically, it’s something we’ve never seen, you’ve never seen it before. I’ve never seen it before. Our ancestors have never seen it before. So I think sometimes it’s easy to forget. And we should just pause and reflect just how phenomenally powerful this technology is.”

JPMorgan upgraded the stock from Underweight to Equal Weight and kept their $7 target price. They said: “Editas has a systemic, modular approach that may allow for differentiation over competitors.”

As the next catalyst for the stock, they highlighted mid-year data updates expected from the RUBY and EdiTHAL clinical trials for gene-edited reni-cel in severe sickle cell disease and transfusion-dependent beta-thalassemia. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered; Approved; Owned: Preclinical.

Probable time of next FDA approval: 2025

Probable time of next financing: 2026 or never

Inovio (INO – $12.79) reported a March quarter loss of $30.5 million or $1.31 per share, worse than the $1.00 loss estimate. They reduced total operating expenses 29% from last year, dropping from $44.1 million to $31.5 million. General & Administrative expenses fell from $13.9 million to $10.6 million. They are running a tight ship.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Jacqueline Shea said the FDA has agreed to starting a single confirmatory trial of INO-3107 before they file the Biologics Licensing Application (BLA) for recurrent respiratory papillomatosis (RRP). They will file the BLA before the end of the year. They do not have to complete the trial before they file.

Click for larger graphic

The 100-patient trial will be randomized and placebo controlled, with a treatment option for the placebo arm at the end of the trial. European regulators said that they will require a randomized, placebo controlled study, so this trial also sets them up for EMA approval. I expect accelerated FDA approval by mid-2025. RRP is mostly treated in academic centers, so they can sell the drug with a small sales force. RRP has three main age peaks. Pediatric RRP tends to peak at around age seven, and then there’s a peak in adults in the 30s and then a further peak in the early 60s. INO-3107 will be approved for adults only.

Click for larger graphic

Click for larger graphic

Inovio has an extensive pipeline. Following feedback from the FDA, they expect to submit plans for a Phase 2/3 study with INO-4201 as an Ebola vaccine booster in this quarter. In the second half of this year we’ll get the first clinical data from the DARPA-funded Phase 1 trial of their next-generation anti-SARS-CoV-2 dMAb drug.

Click for larger graphic

Click for larger graphic

The company has a slew of brokerage presentations lined up, starting with last Tuesday’s presentation at the Citizen’s JMP Healthcare Conference (AUDIO HERE and TRANSCRIPT HERE) followed by Wednesday’s at the RBC Capital Markets Healthcare Conference (AUDIO HERE). On May 20 they will be at the H.C. Wainwright BioConnect Investor Conference.

The next drug is INO-3112 for throat cancer. This is another anti-HPV drug like INO-3107. The FDA has agreed to a Phase 3 trial in combination with Loqtorzi, a drug for nasopharyngeal cancer that has spread or returned. It is used in combination with chemotherapy and can cause serious immune system problems and other side effects. INO-3112 would be able to replace chemo.

They had $105.6 million in cash at the end of March and raised another $33.2 million in April, which will carry them into the September 2025 quarter – past FDA approval of INO-3107. During the quarter, they paid the last $16.9 million on their convertible notes and have no remaining debt. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2025

Probable time of next financing: After FDA approval in 2025

Inflation MegaShift

Gold ($2,381.70) is edging higher despite high real rates, slowly declining inflation, and a strong dollar. That suggests the central bank diversification bid is strong. I think they fear the “fiscal dominance” danger I discussed above, especially since some of them have gone through it. Kuppy calls the Biden Administration’s fiscal policies “Project Zimbabwe.” Recent IMF data shows decoupling is real, and Cold War analogies suggest it could go further. The ongoing global rate cut cycle will add even more fuel.

Click for larger graphic h/t @FedGuy12

Click for larger graphic h/t @FedGuy12

There’s even more central bank gold buying that is under-reported, according to Goldman Sachs.

Click for larger graphic h/t @Mayhem4Markets

Click for larger graphic h/t @Mayhem4Markets

After the CPI report, gold and silver rose even though the Fed will stay higher for longer. Silver hit its highest price in 11 years. Citi said as long as Wednesday’s early low holds, the “path of least resistance” for silver will remain to the upside over $30 an ounce. They said gold and silver’s recent gains “partly reflect a weaker dollar and increased odds of a rate cut by the Fed, although the bulk of its gains have been driven by inflation hedging demand and central bank purchases in the case of gold.”

The fractal dimension is back in trend mode, with enough energy to get over $2,500.

Miners & Related

Sprott Inc. (SII – $44.85) reported March quarter revenues up 8.1% from last year to $37.09 million, missing the $40.16 million estimate. GAAP earnings of 45¢ per share were on target. Assets under management (AUM) grew 2% from December to $29.4 billion at the end of March and a further $1.8 billion to an all-time high $31.2 billion on May 6.

On the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), CEO Whitney George said March was their first quarter of net redemptions in four years, but that trend has reversed in April and May.

The exchange-listed physical trusts are growing again:

Click for larger graphic

Click for larger graphic

Buy SII under $40 for a $70 target price.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $65,441.40) has recovered from the post-halving dip. I think it is headed over $100,000, but these moves never happen in a straight line.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $37.15) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $79.34

Oil has been flattish as the physical market gets ready for the summer driving season and speculators back off. Last week Friday’s CFTC positioning report saw a dramatic drop in net-long positioning in oil futures. It looks like the mild correction from $85 a barrel down to $78 may be all the bears get.

Click for larger graphic h/t @HFI_Research

The July 2026 Crude Oil Futures (CLN26.NYM – $69.24) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $39.27) is a Buy under $40 for a $100+ target.

EQT (EQT – $40.51) has done OK so far, but natural gas producer discipline will be tested soon with the recent increase in prices to the $2.50 area. Production remains low for now.

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $6.22) got a good article on Seeking Alpha: Energy Fuels Is Positioned For Major Growth In The Coming Years. The author points out that Energy Fuels is benefiting from a bipartisan bill that bans Russian uranium imports. This legislation will provide support for a higher price floor in the uranium market. I think a 60% price increase is likely. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $52.04) presented at the BofA Securities Global Metals, Mining and Steel Conference (AUDIO HERE and TRANSCRIPT HERE). Chairman & outgoing CEO Richard Adkerson commented on copper prices: “And what we at Freeport do is we look at a scenario of future prices and think how much money could we make by investing? And then we say, what if we have this asset in our portfolio, how do we manage the portfolio if prices weaken? So it’s not like there’s some magic price and there’s this big dam of projects that’s going to break forward when that price gets hit, because a lot of the barriers to building new projects are far beyond just price. You have the government you’ve got to work with, you’ve got workforce issues, you’ve got community issues, whether you can get support from the local communities for your project…I think it’s going to go higher. I think just the fundamentals will drive it higher.”

Copper futures in New York surged as much as 5.5%, driven by a short squeeze that saw the most-liquid contract trade at a huge premium to other market benchmarks. Comex copper for July delivery jumped to an intraday high of $5.026 a pound on Tuesday, within a whisker of the record high of $5.0395 set in March 2022. Copper is up 30% this year. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

Bill Ackman: Everything You Need to Know About Finance and Investing in Under an Hour

* * * * *

Your reading Kuppy on inflection investing Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 5/16/24. Check out the complete Portfolio page HERE.

Portfolio Protection

June 21 SPY $505 put (SPY240621P00505000 – $1.43)

June 21 SPY $410 put (SPY240621P00410000 – $0.12)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $189.84) – Buy under $175 for new iPhones

Corning (GLW – $35.22) – Buy under $33, target price $60

Gilead Sciences (GILD – $67.86) – Buy under $80, target price $120

Meta (META – $473.23) – Buy under $345, target price $400

Palantir (PLTR – $21.65) – Buy under $22, target price $100+

PayPal (PYPL – $64.10) – Buy under $68, target price $136

SoftBank (SFTBY – $27.01) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $9.19) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $56.00) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $8.89) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $20.97) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $12.10) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.24) – Buy under $13, target price $30+

Velo3D (VLD – $0.22) – Buy under $1, target price $10

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.78) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.14) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.19) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $7.99) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $5.89) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $12.79) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.74) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.41) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $17.42) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($29.91) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $28.13) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $34.62) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $22.46) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $33.59) – Buy under $30, target price $50

Coeur Mining (CDE – $5.27) – Buy under $5, target price $20

First Majestic Mining (AG – $7.43) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.63) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.69) – Buy under $10, target price $25

Sprott Inc. (SII – $44.85) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $65,441.40) – Buy

iShares Bitcoin Trust (IBIT – $37.15) – Buy

Ethereum (ETH-USD – $2,946.17) – Buy

Grayscale Ethereum Trust (ETHE – $21.80) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $69.24) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $39.27) – Buy under $40; $100+ target

Vermilion Energy (VET – $12.06) – Buy under $11; $24 target

EQT (EQT – $40.51) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.22) – Buy under $8; $30 target

Freeport McMoRan (FCX – $52.04) – Buy under $44; $65 target within two years

Other Recommendations

Acreage Holdings (ACRDF – $0.47) – Buy under $2 for the Canopy Growth merger

Hold

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.04) – Hold for buyout

Mongolia Growth Group (MNGGF – $1.08) – Hold for probable liquidation

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1st

Test.

Why haven’t you included PLTR in the portfolio?

Fixed, thanks.

Intel scored $20 Billion with the free money folks in our government. The costs of their giant new fabrication plant in Ohio is some $28 Billion so they are getting the government to pay for almost 75 percent of that facility. Amazing. When in the history of tech companies has that happened? Yet, no one seems to be paying attention!!

A mere pittance compared to the years of excellent jobs that will come to Ohio. We are trying to move more jobs to the US? Right?

Gird your loins, there will be billions more spent in the US for tech. Make America great again.

Michael was that a pump for Trump coming from you??

Are you kidding? This Ohio investment is from Biden’s Chips and Science act. You know, something that actually brings high paying jobs to the US.

MM Wall street sees something with Akeba that you are missing.

Time to dig a little deeper.

Let’s not wait for MM. I couldn’t find any info. AKBA seems to be waiting for 2025. Is the plunge in the stock due to any negatives that WS knows?

It’s just the delayed launch of Vafseo from June to January. The two-year TDAPA window starts in December, so it makes sense for them to pre-launch for several months, build demand, and get all their ducks in order for a big launch. But Wall Street figures they can buy it in December and get the benefits of the launch.

what happened to that Amazon of the Pharma Industry ? was at one time , told to hold , it may hit $ 200 . Not seeing that name .

Sold to Labcorp, $0 for shareholders

MM & everyone: please reply with the one (or two) stocks that has the highest potential to double in 2024 – no longshot 3 or 4X just a 2X. I must recover my NVTA losses so really do appreciate the knowledge of Mm and this board.

As someone who also needs to recover NVTA losses, I would suggest that you give consideration to BioCryst Pharmaceuticals (BCRX), which has ~35% annual revenue growth (based largely on sales of Orledeyo for HAE) and is approaching cash-flow breakeven.

BCRX an oldie and a goodie from the H1N1 days.

TGTX is the safest stock with the highest potential to go 2-4X or much more. It could take 1, 3 or 5 years. It is wrong to plan your life on timetables. Even the Commies have 5 year plans, although they always fail.

My bets on ACXP. I think CEO partners up this year. The stock is at 2.25 ,been lower. “Should” double when he partners. Told myself at one point I would buy 1000 shares every time it goes under 2.00. Realized I can’t afford to. Also have A lot of NGENF. Last 4 buys at 1.50 GTC were filled but took a while. If clinical trials match preclinical will double or more.

I am negative on ACXP. CEO Luci has a history of lying. He is merely a lawyer who licensed the promising antibiotic. This antibiotic has been known for years to be superior to Vanco. Why has Luci been so slow in getting a partner to step up? Why has it taken so long to get enrollment for phases 1, 2? He also did no scientific work, unlike the CEO’s of VLD, APTO, etc. If you have no position already in ACXP, $2 is a reasonable entry point only as a speculation. There are plenty of NWI stocks with better safety.

NGENF is a wonderful speculation with high risk and reward. It certainly is near the bottom of my list for stocks most likely to double soon. For someone with a total loss on NVTA, NGENF could well be NVTA 2.0. It could easily lose 50% when trial results are reported in early 2025. If there are some benefits, the stock could double, but would decline to current levels in later 2025, just as it has done this past year. As further trials are done for other neurological conditions, and if successful, the stock could be a home run many years from now, maybe in 2030-35.

Learned a few very good things about ACXP last week, but I still give the nod to NGENF over ACXP. If ACXP announces a partner for P3, it will double, but I still think NGENF will jump earlier than ACXP. Although NGENF announced that they no longer expect Phase 2 results in Q3, I think you will see a nice jump when they announce complete enrollment in the 20 person trial for chronic SCI, as that will indicate that the trial will wrap up in 16 weeks. I think bad results would cause a bigger haircut than the 50% JGMD posits. But I anticipate positive results will drive shares into double digits as millions of dollars in new investment capital flows into the company and unlike JGMD, I still expect those results in 2024, not 2025.

Chris could you elaborate on the very good things you learned about ACXP. Information is very hard to come by.Read everything I could. Also what do you think the odds of a good outcome on NGENF are 50/50? The upside seems huge.

Good questions.

I got all this information from participating in the BioPub webcast with Bob Luci of ACXP last Friday:

1) The upcoming Phase 3s will allow enrollment up to 48 hours post diagnosis instead of 24.

2) ACXP has hired the person who was responsible for Summit’s excellent enrollment record in eastern Europe in Summit’s failed ridinilazole trial for C diff.

3) The FDA and EMA have agreed that the Phase 3 data will be presented based on a mITT approach,

4) The one patient who was not cured by ibezapolstat stopped taking his medicine (under the mITT approach, his data would not be included and ibezapolstat would still have a 100% cure rate).

If you find this information helpful, you should consider subscribing to BioPub, as the honchos at NervGen will be BioPub’s guest for an extended interview on May 31 to answer your questions.

No question that ibeza is an excellent drug, but my main reservation about this company is Luci’s slowness in getting phase 3 funding from a partner. Every potential partner knows about the drug, but why is it taking so long for any of them to make financial commitments? It won’t be too expensive–Luci estimated several months ago it would be $17M. “A nip and a tuck”–flowery and BS language from Luci.

Appreciate the ACXP update Chris. BioPub is too expensive for my budget so I am grateful for your willingness to share your ACXP & NGENF insights.

I’ve been wondering about the cause of the one failure. Fantastic news that it wasn’t related to ibezapolstat. The ability to claim a 100% cure rate so far for patients that completed the protocol is wonderful news for the company and should help in their negotiations.

Thank you Chris…He should have press released this information. The stock would be trading 1.00 higher right now. Still think he partners.If he has to do phase 3 on his own he will dilute all shares including his own. He would have to get four times for the company to break even. On NGENF please let us know what you think along the way. Would like to buy more. At 50% chance of good outcome I think it’s way better than true odds.

NGENF–I love Jerry Silver’s optimism that the peptide will work in people. A ymb poster named Herb is a T-9 paraplegic. He says that every SCI patient is unique. I infer that matching peptide and placebo baseline characteristics will be just about impossible. My expectation is that some peptide patients will get some benefits corroborated by objective MEP data, and placebos will get no response. But outside academics will criticize the reports based on inadequate matching of patients. This will be an invalid criticism, and it could mitigate any stock jump based on good results.

Morning Steve,I’m also one trying to figure out how to recoup some of our losses from the shit that nvta left us with,to me scyx looks like there is a chance for a double this year,since they have a catalysts coming,hope this helps

In Oct 2023, I bought more SCYX at $1.70. Until quite recently, I had a negative opinion on it. But that was my error due to not studying the protocol of FURI, CARES for Brexa in serious fungal infections. A few days ago, I went back and found that in FURI 180 days of Brexa were used, and possibly more than 180 days if Brexa was combined with other approved antifungals. CARES was for serious candida auris, using Brexa for 90 days. To me, these are much better protocols using Brexa than for VVC.

I projected that after FDA approval of the new manufacturer of Brexa and start of the MARIO trial, the PPS would rise to $2.50. It has already reached $2.60. Whether it will soon double from here to $5 after FURI and CARES are known is uncertain. If you get lucky and put in a stink bid at $2, a quick double will be more certain. As for me, I probably will hold my medium size position for another few years until we see how good SCY 247 is. Or you might sell half at $4-5, and hold the rest for much higher prices, but that is speculative.

Time will tell,have a nice day,and also after reading the report they state the cash on hand is enough for 2 years so scyx shouldn’t have to tap the atm.

Thanks to all respondents, MM how about you?

SCYX

MM do you believe SCYX still doubles from current runup price?

Sounds like winner is SCYX. I thought you said you bought some a while back. I have a medium position. Best of luck to you and all of us. It has run lately. Last 1000 shares I bought at 1.40. Shocked when it filled. Had to transfer funds to stay out of margin.

MM–thanks for your VLD analysis. Good summary of its growth prospects. But you didn’t analyze the critical cash situation. Most investors are worried about their desperate need for cash to pay employees and other expenses. Your outlook for positive proforma earnings is more conservative than the company’s. Your estimate is 2026. Meanwhile, where and how are they going to get cash to survive? Dilution is inevitable. Please read the YMB post by UWHuskies from 2 days ago.

“Before anyone gets too excited about VLD stock one should read through the 10-Q and consider just how much additional capital VLD is going to need just to get to year-end given the guidance that they’ve provided.

Assuming Q2 guidance (revenue 30% higher than Q1; 0% GM & 10% lower Op Ex) VLD will have an Op Loss/cash burn of $16M. From the 10-K, as of May 9 they had only $5.7M in cash so they will need at least $5M more just to get through Q2.

On July 1st they have a $10.5M note payment due.

Assuming continued P&L improvement in Q3, they will incur an Op Loss/cash burn of $12.5M on top of the note payment.

On October 1st they have another $10.5M note payment due.

Assuming their P&L guidance in Q4, they will incur an Op Loss/cash burn of $5M on top of the note payment.

Finally, at year-end they will need cash on hand to pay the January 1st 2025 $10.5M note payment plus have at least a $5M cash cushion to start the year.

In total that’s $59M in additional capital that VLD will need in 2024 assuming they hit all their guidance metrics. The only metric they hit in the past 2 quarters was Q1 revenue so the above is likely optimistic. In order to raise $59M they would need to issue 235 million more shares at $.25 per share. That almost doubles the amount of shares outstanding. If any of that capital raise comes with a matching warrant as their recent raises all have then that’s even more dilution. Regardless you are looking at a lot of future dilutive downward pressure on the stock.”

If this is correct, dilution needed to survive before proforma EPS is about 100% or even 150%. So the stock price this year will likely be one third to one half of the present, or 7 to 11 cents. My own estimates of cash flow are more optimistic than UWH because I believe that new efficiencies will get shipments and revenue much earlier than the market is assuming. And the company guidance is $80-95M, in agreement with mine. So I believe dilution will be somewhat less than 100%, still a lot. It won’t be higher so bad if the military/aerospace contracts come very soon at very high levels. What is the chance of that?

In any case, your buy up to $1 is out of touch with current reality. Many years from now, business may justify $10, but with dilution, cut that to $3-5. Please assess the accuracy of UWHuskies’ post, and comment. After considering the cash situation and dilution, what is your target for end of 2024, 2025?

Thanks.

His numbers are in the ballpark. As I wrote above regarding Aptos: “That means either you don’t want to own APTO at all OR you are willing to participate in every financing for the next four years to keep your position from being diluted into insignificance. I think it’s worth the risk, but your mileage might vary.”

I recommend buying VLD while it is under $1, including participating in any financings, as they hit cash flow positive.

Please, MM address that post of UWHuskies and my observations. No more wishful cheerleading. Be realistic. Answer the question–How is VLD going to avoid 100-150% dilution from here? I have already bought many times over the past 8 months from $1.50 down to 24 cents, getting an average cost of 44 cents. I have too much money in VLD already. There are probably many subscribers whose average cost is much higher, near your entry PPS of $10. Do the math. You can average down many times, but you have more total money in the hole. When things don’t work out as expected, there is more money lost. Why do you think most subscribers are asking desperately for stocks to save them? NWI has more wipeouts as time goes by, and few significant gains to compensate. Please pay attention. In the light of coming big dilution, current company projections and 10-Q facts, what are your realistic targets, not wishful thinking, for 1 and 2 years from now?

Let’s see how other subscribers feel.

Never average down. That rule eliminates most of MM’s picks.

Good point. Buffett said to buy more of a high quality stock when it is down 20%. 2 different universes, MM and B.

With VLD now at $.20, the massive dilution outlined above understates by 20% the actual dilution that would now be incurred at the current stock price and future capital raises will likely continue to drive the stock price lower inflating the upcoming dilution even more.

I agree with Michael that riding the stock through the upcoming capital raises and averaging down to maintain your position is a horrible strategy. Why not wait until Velo is cash flow positive and avoid your investment being erroded by all of the upcoming dilution? There are thousands of stocks that would be a better investment then Velo over the next 6 to 9 months.

Since cash reserves will decline until earnings are positive, that factor alone will cause the PPS to decline. In that case, it is more prudent to get the dilution over with now when the PPS is 20 cents rather than 10 cents or so. On the other hand, if the sales trajectory actually increases over the next few quarters, that will give confidence that the company is truly on the mend, and the PPS will rise even if the cash reserves are declining.

Another way to look at it would be the P/S ratio. P refers to the market cap. Current forward 2024 P/S is about 0.8, assuming $64M market cap and company estimates of 2024 total revenue of $80M. That’s considered cheap. But assume as much as 3 fold dilution, and we get corrected P/S of 2.4, which isn’t bad. Assuming continued growth in sales, that’s reasonable. So perhaps we are near the bottom in stock price, and the plunge in the stock already mostly discounts the large dilution ahead.

It is certainly safer to buy when VLD is cash flow positive. Pre-dilution, PPS would be at least $1 at that time. Post-3 fold dilution, over 33 cents. Assuming good sales trajectory continues, what is the realistic potential? $3 pre-dilution or $1 post-dilution? Whatever the potential is, suppose we hold what we have and suffer at 7 cents post-dilution for this year, but then catch the full rebound to $1 post-dilution. More short term risk, but better long term return from 20 cents to $1 compared to safer return from 33 cents to $1.

Brent, others, MM, what do you all think of my reasoning?

I doubt the share price has mostly discounted the upcoming 2024 capital raises.

While it’s easy to project an estimate of the raise, or raises, needed based on guidance & SEC reports who really knows the approach they’ll take. They have a $70M ATM set up so do they rely on that & sell those shares as needed? They’re note payments will be big hits on specific dates so do they handle those differently? Who knows.

What makes you so sure Velo will bounce to $1 once they get to cash flow positive? Velo currently has 296 million shares outstanding and will likely double that this year to roughly 600 million. In addition, there are now 105 million warrants outstanding and most of those have an exercise price of $.57, $.46 or $.35 so will be exercised as the price rebounds. And more warrants could be issued with any new capital raise. So it appears that at a minimum, Velo would need to be valued at $700 million to hit your $1 target, which is more than 10 times it’s current valuation of 59 million. What are the chances the market values Velo at $700 million on annual sales below 100 million?

Right. I assumed 3 fold dilution, and revised the cash flow positive target to $1 divided by 3, or 33 cents. I wasn’t aware that they have a $70M ATM set up. To come up with $59M to pay expenses and debts that UWHuskies figured, or whatever amount this year, they could sell shares as needed. This is still equivalent to huge dilution that would plunge the PPS, no?

VLD is only attractive today based on its low forward P/S assuming they get $80M in revenue for 2024.

Correction to my earlier statement regarding the ATM, it’s actually $75 million not $70 million. It was announced in a 1/31/24 press release. Increasing the limit to $75 million was one of the conditions of the 12/27/23 note amendment.

Velo3D announces Amendment 1 to it’s 2/6/23 “at-the-market” (ATM) sales agreement with Needham & Company, increasing the aggregate dollar amount of common stock shares sold from $40M to $75M.

The benefit of using the ATM to shareholders is that there would not be any associated warrants issued for whatever shares are sold.

But yes, the share count Velo needs to sell is roughly the same no matter what method they choose assuming everything else, like timeframe, is the same.

Steve just a thought. Been watching AKBA for a while. If it goes to 1.00 I will open a position. Good chance of a double. I like AKBA at 1.00 better than SCYX at 2.75. Just a thought. Don’t know if it will see a 1.00 but close right know.

On SCYX, we’ll get FURI and CARES trial results by around June 30. If those are promising, SCYX will get a big pop even from $2.75. AKBA won’t move until 3 months later, and not much until early 2025. The first sales in Q1, Q2 are what will start the move from $1 to $2 at most. I still think SCYX is still 1st choice. Both companies’ managements suck, and AKBA even worse. If your money is tight, then deploy some of the early profits from SCYX into AKBA in late summer.

I like that. I am sure you guys are better traders than me.

Not me. I’ve been wrong on timing. Things may not work out according to logic.

MM–30 min ago, I couldn’t post several comments. Two were simple, one was long. Everything was said in good taste, but I got a red message saying something like “some of the field is invalid.” An example of AI or algorithms causing sabotage.

I seriously doubt that MM has implemented AI. It’s probably a simple javascript error.

Either way, AI or javascript, tech can be an intrusion which causes at least temporary chaos. The most common example is computer systems that are down at airports, and cause much stress for passengers. Decades ago when humans ran airport flight schedules, were there as many flight disruptions as there are today?

Humans couldn’t handle the volume of airplane schedules today. Obviously.

Most flight disruptions are due to greedy airline companies that underpay and cut staff to keep their bottom line happy. Also, when planes aren’t filled to the brim, they will cancel them. Just happened to me last week.

Flying used to be a nice experience, now they treat you like cattle and or shit.

You never find out the real reasons for cancellations. Bad IT is a very common cause of company disruptions. A few weeks ago, a small private medical lab I deal with was shut down for an afternoon. I called them the next day–they said IT was to blame. Worse, there was a nationwide shutdown of doctor insurance payments. Change Health is the middleman for processing of payments. Change was hacked. It took 2 months to correct the situation. Meanwhile, many offices had to drastically cut employee hours because no money was coming in.

Chris–big jump in ACXP starting at 1 PM today on 4X average volume. No PR news. Many months ago I saw several intraday spikes to $8 when I was off work that day. Even you missed them. Of course, the spikes were like July 4 fireworks that fizzled.

JGMD, ACXP went to 8.00 one day, infact I think it was 8.80 on one day I think October 12. Ended the day at 4 plus The next day or two it went to 5 or 6. I don’t know why. It was acting like a meme stock.I hate meme stocks, no fundamentals. You probably missed Chris’s comment but he said he bought a lot under 2.00 and took some off at 8.00. If he took a quarter off at 8.00 he got his cost out. I remember thinking what an excellent trader.I was on a cruise ship and could’t trade. I love reading both you and Chris’s post. I know we disagree on ACXP. But know we have 100% cure rate. The world does’t know this. I’ve read the comment boards. It would have showed up if anybody knew. I don’t know why it’s going up.I think everyone thinks he will partner up. I will probably lose my ass on this. I did on NVTA. Probably because of greed. Why did NVTA fail. I think they tried to grow to fast, buying company after company. Creating too much debt. And then interest rates doubled. I don’t mean to rant. I just need someone to talk to.

I’m in the same boat as you Rick with nvta way much invested in it and with MM totally missing it,continuing to pump it like that was it,oh well the sun does come out we have to move on and hope we don’t fall for something like that again,better days ahead.have a nice day

MM is not doing a complete analysis of financials. Latest case in point, VLD. He is completely silent on the critical cash situation and prospect for big dilution. He evades questions about this. As a stock plunges, he should be doing financial analysis and not just merely re-tell good stories about company hopes. Louis Navallier gets out quickly when financials deteriorate. Investors can wait 30 days for the wash rule to expire, and then re-enter when the outlook looks better. Subscriber Brent does the best financial analysis. I don’t know if he is a diligent amateur or a professional investor.

Nice of you to say JGMD. I’m not a professional but like many here like yourself I treat investing almost like a job in a way. If I want/expect to have success than I need to put in significant time and effort into knowing what I own or may own and that goes far beyond MM’s picks and updates.

Here are three things that I do for staying on top of my stocks that others may find useful:

It’d love to hear any tips or tricks that others find useful for staying on top of their investments as well. I’m always happy to learn from others.

Thanks Brent.

MM–please take that as a hint that as a CFA, you should do this kind of due diligence and report on your companies that are having problems. This is an important part of what subscribers pay you to do.

MM and board – with the focus on emerging viruses, Covid 19, RSV, now bird flu, I was alerted to a small company called NanoViricides (NNVC) who are part of this huge emerging sector of nanotechnolgies and they may have a remedy for bird flu. Anyone else wathcing this sector or have a stock play in it?

I don’t care what virus comes along or is created by corrupt gain of function research. To control inflammation caused by any infection, permanently keep vitamin D 25 hydroxy blood levels 60-80 ng/ml. Take the vitamin D at the end of a fatty meal to enhance absorption. Average D requirements are 5000 IU daily, but do blood tests to adjust dose. On empty stomach, take NAC (N acetyl cysteine) 600 mg plus Ester C vitamin C 1000 mg together 1x/day for maintenance, and 4x/day at the first sign of illness. Another strategy is nucleotide complex from Invite Health. Jerry Hickey, the pharmacist/nutritionist at Invite, takes 3 capsules 2x/day for a few days when he gets sick. He claims great and rapid efficacy. The rationale is that nucleotides provide energy for the immune system. DNA is a chain of nucleotides. The DNA makes proteins for the immune system. Buy now in the quiet period. In cold/flu season he has sales on nucleotides, but they are often out of stock due to high demand then. I think for Memorial Day he is having a sale.

At best, Pharma solutions reduce viral growth. But without the above nutritional strategy, the prognosis will be worse. People who are obese and have vitamin D levels below 20 have had much higher covid death rates. People who are slender and high D levels as above have rarely had more than mild symptoms. BP censored this info, because they wanted mass vaccination with mandates.

Steve, I was in NNVC for years and finally got out. The chief scientist/owner also owns the lab and seems content with profiting from “testing” rather than actually moving the science forward. Dr Seymore once told me how aggravated he was with how Diwan was dragging his feet on purpose. Now, watch it soar.

RDGL is an interesting play if you’re looking for something

Thanks Larry, what’s the driver or catalyst on RDGL?

Vivos Inc. has developed an Yttrium-90-based injectable Precision Radionuclide Therapy brachytherapy device to treat tumors in animals (IsoPet®) and humans (RadioGel™). Using the company’s proprietary hydrogel technology, Brachytherapy uses highly localized radiation to destroy cancerous tumors by placing a radioactive isotope directly inside the treatment area. The injection delivers therapeutic radiation from within the tumor without the entrance skin dose and associated side effects of treatment that characterize external-beam radiation therapy. This feature allows the safe delivery of higher doses needed for treating non-resectable and radiation-resistant cancers.

RadioGel™ is a hydrogel liquid containing tiny yttrium-90 phosphate microparticles that may be administered directly into a tumor. The hydrogel is a yttrium-90 carrier at room temperature that gels within the tumor interstitial spaces after injection to keep the radiation sources safely in place. The short-range beta radiation from yttrium-90 localizes the dose within the treatment area so that normal organs and tissues are not adversely affected.

RadioGel™ also has a short half-life – delivering more than 90% of its therapeutic radiation within 10 days. This compares favorably to other available treatment options requiring up to six weeks or more to deliver a full course of radiation therapy. Therapy can be safely administered as an outpatient procedure, and the patient may return home without subsequent concern for radiation dose to family members.

The biggest opportunity could come any day as the company is waiting for FDA approval to start human trials. Already have major hospital lined up.

Thanks do you what the timetable is?

The plan is to submit to FDA for human trials by end of Q2. I just confirmed today that they are on schedule to accomplish that. After that, it’s up to FDA to respond. My understanding is they’ve worked with the FDA on submission requirements. They already have a hospital ready to perform the trials (Mayo, I believe). Unfortunately, I don’t know what I don’t know. They post updates on X (Twitter) and are very responsive to questions submitted from their website. RDGL is their symbol.

Currently .147

Larry, I was just checking this out. Looks interesting. What price range are you looking for this to get to if they get FDA approval?

Douglas, I’m kind of new to this one myself, but am very intrigued. I saw yesterday where an early investor thinks it’s a potential 10x from current price. I consider than hopeful enthusiasm, but hope it to be possible. I’ve emailed the company several times and they are very responsive. They just confirmed that they’re on track to submit to FDA by end of Q2. The exact same process/procedure is currently utilized in animals with success. Of course if approved , the human market would be significantly greater. I expect to add to my existing position soon. I see the risks of being turned down by FDA as minimal and the risk of not working as minimal as well, since it’s been used on animals for some time with success.

New World Investor for 5.23.24 is posted. Palantir is the next Nvidia.