Dear New World Investor:

We’ll get the next Personal Consumption Expenditures Index on May 31 and the next Consumer Price Index at 8:30am on June 12. That same day, at 2:00pm, the Fed issues their next meeting results. Albert Edwards, the Société Générale strategist, wrote: “I believe the Fed is sowing the seeds of yet another policy disaster. Having let the inflation cat out of the ‘transitory’ bag, it now seems determined to regain its credibility by driving CPI inflation all the way back down to its 2% target. This has led to a huge divergence between goods and services inflation. This policy error is the mirror image of the mistake the Fed made after the 2008 Global Financial Crisis, the very mistake it was castigated for by former Fed Chair, Paul Volker, back in 2018.

“Super core inflation is rising mainly due to vehicle insurance at 22.6%. The excuse of rising maintenance and parts have long since passed. This and other rampant services inflation is impervious to higher rates. The Fed are nuts to target something they can’t really control, creating unprecedented goods deflation.”

Click for larger graphic h/t @albertedwards99

Click for larger graphic h/t @albertedwards99

In their usual trend-following way, Wall Street is getting more excited as stocks go higher.

Click for larger graphic h/t Bloomberg

Click for larger graphic h/t Bloomberg

The Street’s biggest bear, Morgan Stanley’s Mike Wilson, flipped and raised his yearend S&P 500 price target by 20% from 4500 to 5400, a daring 132 points above today’s close.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

I still expect high-level churning through the election, followed by a sharp move depending on who wins.

Market Outlook

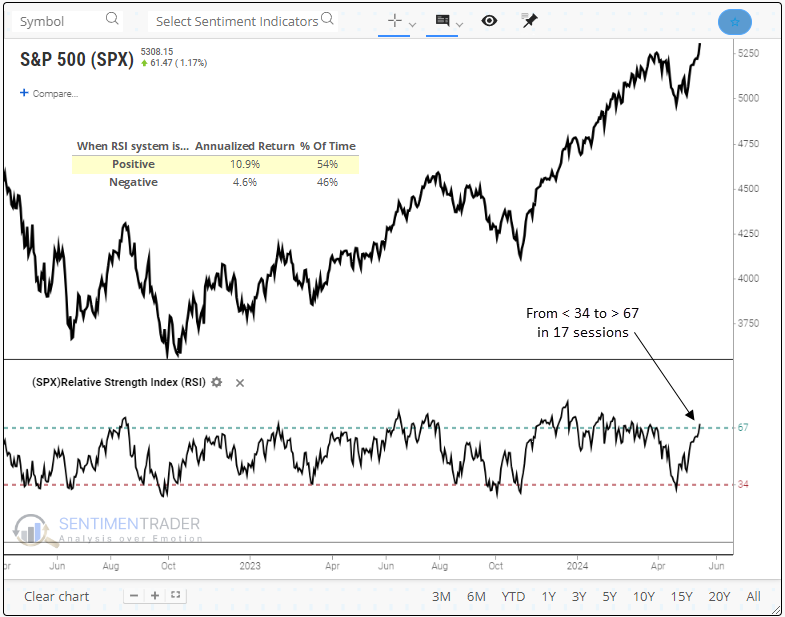

The S&P 500 fell 0.6% since last Thursday after today’s “Nvidia won’t save us!” drop. The Index is up 10.4% year-to-date. According to SentimenTrader, the S&P 500’s Relative Strength Index exceeded 67, triggering a favorable trend profile. Since 1928, there have been 149 instances of a shift from below 34 to above 67. However, this most recent signal occurred in a span of only 17 sessions, a more uncommon event. The previous RSI reversal occurred in November 2023, producing a 12% gain for the S&P 500 over three months.

Click for larger graphic h/t @sentimentrader

Click for larger graphic h/t @sentimentrader

On Tuesday the S&P closed at 5321.41, which was a new all-time high. In the 74 years starting in 1950, there have been 27 years in which a high for the year-to-date was set in May. In those 27 cases, the following June-December performance was 23 up to 4 down, for an average seven-month gain of 7.58%. The 10% moves during the final seven months of those 27 calendar years were 12-0 to the positive side. The fall rally from August 25 to December 8 had 26 wins after a May high versus only one fractional loss. June 21 to July 1 was the weakest period with a 12-14 mark for a modest 0.26% avg loss.

Click for larger graphic h/t @WayneWhaley1136

Click for larger graphic h/t @WayneWhaley1136

The Nasdaq Composite gained a trivial 0.2% and is up 11.5% for the year. It did the same 17-day flip from extreme oversold to extreme overbought:

Click for larger graphic h/t @bespokeinvest

Click for larger graphic h/t @bespokeinvest

The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 3.5%, wiping out last week’s rally. It is flat year-to-date. The small-cap Russell 2000 dropped 2.3% and is just up 1.0% in 2024.

The fractal dimension flipped the downtrend back to a consolidation. I doubt the S&P can drop more than about 100 points from here, so if price isn’t going to consolidate the fractals, we’re in for weeks of churn to get the job done.

The VIX Fear & Greed Index surged over 7% today after hitting its lowest level since November 2019 earlier in the session. That means fear was absent and still is diminished.

Click for larger graphic

Click for larger graphic

Confirmed by the CNN Fear & Greed Index:

Click for larger graphic h/t CNN

Click for larger graphic h/t CNN

The American Association of Individual Investors stock allocation crossed above 68% in March for just the 14th time in the last 20 years. Subsequent three-month and six-month returns have been OK, but one-year returns have been weak.

Click for larger graphic h/t @dailychartbook

Click for larger graphic h/t @dailychartbook

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

TGTX TG Therapeutics – Rapid recovery from overdone pullback

AAPL Apple – AI announcements at June WWDC and September iPhone 16 introduction

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

Goldman Sachs is well above the consensus for 2024-2025 real GDP growth, with no recession in sight. I still think a mild recession is imminent. Danielle DiMartino Booth, a former Fed economist, thinks we’re already in one and the post-election revised data will show it.

Click for larger graphic h/t @WinfieldSmart

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, May 24

Short Interest – After the close

Monday, May 27

Markets closed – Memorial Day

Tuesday, May 28

Stock settlement period changes to one day from three days

RKLB – Rocket Lab – Unspec. – KeyBanc Industrials Conference

EDIT – Editas Medicine – Unspec. – Stifel Genetic Medicines Forum

Wednesday, May 29

QUIK – QuickLogic – 1on1s – Craig-Hallum Institutional Investor Conference

META – Meta Platforms – 1:00pm – Annual meeting

Thursday, May 30

March quarter GDP – 8:30am – Second estimate

PD – PagerDuty – 5:00pm – Earnings conference call

Friday, May 31

Personal Consumption Expenditures Index – 8:30am – The Fed’s favorite measure of inflation

MDNA – Medicenna – 2:40pm – Sachs 10th Annual Oncology Innovation Forum

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Corning (GLW – $36.12) said “We’re seeing encouraging signs of improving market conditions, and we expect that the first quarter will be the low quarter for the year. We continue to execute on our plans to add more than $3 billion in annualized sales within the next three years. Importantly, the required capacity and capabilities to support this growth are in place and already reflected in our financials. As a result, we are poised to deliver powerful incremental profit and cash flow and generate substantial shareholder value.”

CEO Wendell Weeks presented at the JPMorgan Global Technology, Media and Communications Conference (AUDIO HERE and TRANSCRIPT HERE). He said: “We have three core technologies, glass science, ceramic science, and optical physics, along with four proprietary manufacturing and engineering platforms. We’re world leaders in each of these, even in the eyes of our competitors. Today we focus our efforts on five market access platforms. This is what we call our 3-4-5 approach.

“Now, the way this works is that our probability of success increases as we apply more of our world-class capabilities. Our cost of innovation declines as we reapply our talent and we repurpose our existing assets. Perhaps most importantly, by combining the capabilities in our portfolio, we create higher and more sustainable competitive barriers.”

Their Gen 10.5 technology produces glass larger than two king-size beds put together, over 100 square feet, and as thin as a business card, upon which their customers build six 75-inch TVs at a time. Regarding their optical fiber opportunity in AI, he said a 10 kilowatt CPU server rack that’s the front-end of a network today will use 32 fibers that connect to the top of the rack, 16 two-fiber connectors.

In a GPU rack running AI applications, 10 kilowatts will cover two Nvidia H100 servers with eight GPUs per server and an InfiniBand switch with 400G ports that uses 16 fibers. Each of those H100 servers uses 128 fibers, a total of 256 fibers or an 8x increase in the amount of glass per rack.

Corning gets a huge volume increase and because customers have to fit 8x fibers in the same space, the company has developed order-of-magnitude smaller fiber, cables, and connectors that competitors don’t have.

Weeks said Corning has begun to buy back stock this quarter. They expect to generate a significant amount of excess cash in the next three years and accelerate the return of cash to shareholders. They have a 3.0% dividend yield today, so this looks like a perfect stock for the conservative end of your barbell portfolio. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

Gilead Sciences (GILD – $66.17) announced that following their recent acquisition of CymaBay Therapeutics, interim results from the ongoing ASSURE study demonstrated that treatment with seladelpar led to improvements in markers of cholestasis (impaired flow of bile from the liver to the duodenum) and reduced inflammation. Seladelpar reduced pruritus (itch) in people living with primary biliary cholangitis (PBC). There are currently no treatments indicated to treat PBC-related pruritis. Seladelpar has an August 14 PDUFA date.

Gilead will, as usual, dominate the European Association for the Study of the Liver Congress June 5-8 in Milan with 25 presentations. The company said they have a commitment to drive life-changing science in liver disease. GILD is a Long-Term Buy under $80 for a first target of $120.

Palantir (PLTR – $20.72) is the next Nvidia, when people realize their AI software stack is as far ahead of the competition as Nvidia’s hardware is of theirs. As my friend Keith Fitz-Gerald reminded me, Nvidia was under $130 in mid- to late-2022. Today, $1,037.99. PLTR is a Buy under $22 for a $100+ target.

PayPal Holdings (PYPL – $61.58) published their annual report. The new CEO wrote: “I’m pleased with what we’ve been able to accomplish in such a short period of time to reposition PayPal for profitable growth. We’ve put in place a world-class leadership team and organized the business around the customers we serve – consumers, small businesses, and enterprises. We’ve narrowed our focus to the products and services that will have the greatest impact for our customers. And we’ve updated our mission to reflect the evolution of our purpose: revolutionizing commerce globally.

“We’re embracing our roots to reshape commerce for the consumers and merchants around the world who rely on PayPal each day – making it faster and simpler for people to connect with each other and make their money go further. Our entire organization is focused on durable growth priorities that will help solve our customers’ most pressing needs and delight them in new ways. We aim to deliver a best-in-class personalized commerce experience, and drive engagement by creating a richer value proposition that makes PayPal the obvious choice for both consumers and businesses.”

PYPL is a Buy under $68 for a double in three years.

Small Tech

Enovix (ENVX – $9.61) will be at the Smart Manufacturing Summit SMX Automotive on August 28 in Detroit. We could see a joint venture announcement with an EV battery manufacturer this year.

Edge AI is a very interesting application for ENVX batteries. For instance, a drone could benefit from having on-board AI route navigation, making Enovix energy density a huge plus for this particular application. There’s many such instances where moving the energy source closer to the end-device makes sense, especially for mobile deployment of tech. There will be three types of Edge AI apps: (1) phone- and computer-based apps that will execute on the edge; (2) client/server apps that will partially execute on the edge; and, (3), dedicated platforms with AI processors designed to require dramatic energy increases over what is available today.

AI tools executing on smartphones can easily consume 30% to 50% more energy. Enovix is at the center of this emerging demand.

Click for larger graphic

Click for larger graphic

ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

PagerDuty (PD – $19.59) reports March quarter results after the close next Thursday. Analysts expect $111.45 million in revenues with 13¢ earnings per share. June quarter guidance should be for $116.33 million and 15¢.

They announced new capabilities and upgrades for the PagerDuty Operations Cloud focused on advanced AI and automation enhancements to provide more powerful end-to-end incident management capabilities to anticipate, identify and resolve operational issues more quickly than ever. I’m sure we’ll hear more about it next week. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Rocket Lab USA (RKLB – $4.22) CFO Adam Spice presented at the BofA Transportation, Airlines and Industrials Conference (AUDIO HERE).

Electron is a 70′ tall, carbon composite, three-stage rocket capable of putting 660 pounds, roughly refrigerator-size, into low earth orbit. Neutron is a medium-capacity, carbon composite, reusable rocket capable of launching 13 tons into space. That class of rocket currently has only one provider – SpaceX. Other competitors used Russian-built engines that have been sanctioned.

First Neutron launch has been pushed from the end of 2024 to mid-2025 due to delays in developing the propulsion system. The engineers didn’t want to postpone with the new Archimedes engine on the test stand and first fire expected before the end of June, but management wasn’t sure the whole program would be ready by December.

Rockets are hard. Electron has 66,000 parts, all of which have to act perfectly and in unison to have a successful launch. Competitors that made a design or manufacturing process mistake couldn’t recover and ran out of capital. Demand is there – most research firms say tens of thousands of low-earth orbit satellites need to be launched. SpaceX launched 95 or 98 times in 2023 with 80% of those for multiple Starlink satellites. Many other companies and governments plan similar systems – do they really want to depend on SpaceX for launch?

Customers used to have to spend $300 million to $500 million for a low earth orbit launch. SpaceX came in at a $100 million price point, so some customers were willing to take the risk of a new launch provider. Then Rocket Lab played the same game and came in at $10 million, 90% cheaper than SpaceX, to get the first customers. It will be very hard for any new LEO launch providers to get market share. A Neutron launch will cost $50 million to $60 million, half of SpaceX.

Rocket Lab has a $1 billion backlog today, of which Space Systems is $800 million, composed of $150 million for components and $650 million of complete satellites to be launched by them or other companies or governments. The other $200 million is launch backlog.

The Q1 Brycetech Launch Report just came out. SpaceX put 87% of the world’s tonnage in orbit, a new high. The graph uses a magnifying projection to even see the other domestic launch providers. The five Chinese launchers combined lofted 13.6x less than SpaceX. Rocket Lab was ninth. Europe was zero.

Click for larger graphic h/t @FutureJurvetson

RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Velo3D (VLD – $0.18) management says they will be cash flow positive by the end of this year, so they will not need additional outside funds after that. They do need more capital to get through this year. VLD is a Buy up to $1 for my $10 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Biotech MegaShift

Click for larger graphic h/t Janus Henderson Investors

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Akebia Therapeutics (AKBA- $1.09) did a fireside chat at the H.C.Wainwright BioConnect Investor Conference (AUDIO HERE). CEO John Butler said applications for Transitional Drug Add-on Payment Adjustment (TDAPA) approval are next accepted in June. Vafseo (pronounced vaf”-see-o) will get approval in December and launch in January. Their phosphate binder, Auryxia, also will get added to the dialysis bundle in January. Akebia is focused on driving a quick uptake of Vafseo during the two-year TDAPA period. (There’s also an effort to expand TDAPA to three years.)

He said their competitor is not GSK, it is the Erythropoiesis-Stimulating Agents (ESAs) that 90% of the 550,000 US dialysis patient take. Vafseo got a very broad label allowing Akebia to position it as a new oral standard of care for any patient who has been on dialysis for three months. (The company is continuing discussions with the FDA to get rid of the three-month delay, an issue that came up late in the review process.) The only required tests are from a monthly blood draw that dialysis centers already do to monitor hemoglobin levels.

GSK’s Jesduvroq (daprodustat) has a warning label around patients who have a history of hospitalization for heart failure – about 40% of dialysis patients. Vafseo does not have that warning.

This is a $1 billion market even after the prices of ESAs have come down to $2,000 to $3,000 a year per patient. Because of TDAPA, their total market opportunity for 2025-2026 is even larger. They will bring dialysis prices down after that, but will offer volume discounts and continue to produce data supporting a non-dialysis (actually pre-dialysis) label expansion. The FDA wants to talk to them about another trial in non-dialysis.

Home dialysis is 15% to 20% of the market today, growing to 20% to 25%. Doctors have told them that’s low hanging fruit for a Vafseo pill to replace the once or twice a month visit to a dialysis center for an ESA injection.

Another obvious area is patients on the highest dose of ESAs, which are associated with major adverse cardiac events (MACE). Doctors see these patients as the highest safety risk and dialysis centers see them as the highest cost.

Home dialysis plus high dose ESAs are 30% to 40% of the dialysis population, which provides a solid start for the launch. Buy AKBA up to $2 for the vadadustat launches in the EU, UK, and (after TDAPA approval in December) the US.

Primary Risk: Vadadustat doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: TDAPA January

Probable time of next financing: Never

Editas Medicine (EDIT – $5.83) has the US rights to the basic gene therapy patents. It is true that we don’t know if there are any long-term serious adverse effects from gene therapy. Only time can tell us that. But in the near term, many of the patients are miserable or dying and desperate for a cure. Most investors don’t fully comprehend the huge scale and potential of gene editing and how it is going to change our lives. Here’s a great piece about a sickle cell teenage patient and how CRISPR-based CASGEVY changed his life. Editas gets royalties.

EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered; Approved; Owned: Preclinical.

Probable time of next FDA approval: 2025

Probable time of next financing: 2026 or never

Inovio (INO – $10.96) finished the last of their broker grand tour with a fireside chat at the HCWainwright BioConnect Investor Conference (AUDIO HERE and TRANSCRIPT HERE). CEO Jackie Shea did another standard introduction to the company and INO-3107 for recurrent respiratory papillomatosis (RRP), which is patent-protected to the mid-2040s.

She wouldn’t talk about pricing, but the RRP Foundation put out some data a few years ago saying that the average annual cost of surgery is about $72,000 per patient. That doesn’t include the impact on quality of life and all of the other costs associated with treating the disease.

Next up is INO-3112, which is another HPV-related candidate for the treatment of HPV-16 and -18 oropharyngeal squamous cell carcinoma, also known as throat cancer. As I covered last week, they are going to start a Phase 3 trial evaluating -3112 in combination with Loqtorzi, Coherus Biosciences’ PD-1 inhibitor, recently FDA-approved for nasopharyngeal carcinoma.

After that they have INO-4201, an Ebola booster vaccine candidate. They recently had feedback from the FDA giving them a path forward for that drug. And then, INO-5401, partnered with Regeneron, for newly-diagnosed glioblastoma. They have a rich pipeline behind these, which is why Inovio is a likely acquisition candidate for a Gilead, Regeneron, or Pfizer. INO is a Buy under $14 for a very long-term hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: Mid-2025

Probable time of next financing: After FDA approval in 2025

Medicenna (MDNAF – $1.70) will present an update on the MDNA11 ABILITY-1 Trial at the Sachs Oncology Innovation Forum on May 31 on the first day of the American Society of Clinical Oncology (ASCO) annual meeting. They also have a poster presentation on MDNA55 for brain cancer, which they are trying to partner, at ASCO on June 3. Buy MDNAF under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2025

Probable time of next financing: 2025

ScyNexis (SCYX – $2.24) published a new corporate presentation. Aside from saying: “GSK Amended Agreement Including Path Forward for Restart of the MARIO Study” (which requires lifting the clinical hold) there was nothing specific about the new manufacturing partner(s). Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2024

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,332.10) rose but the miners are just starting to participate. More than 40% of gold mining stocks hit a 52-week high last week. This was the first reading over 40% in over a year. The last couple of instances marked the nascent stages of impressive rallies. Over the past 30 years, when gold mining stocks have seen cycles in selling and buying pressure similar to the past few months, they showed gains two to three months later almost every time.

In 2016, gold rose 8.2% and the GDX and GDXJ soared 52% and 64% respectively. So far in 2024 gold is already up 17%, yet the GDX and GDXJ are up just 19% and 22% respectively. Gold stocks began 2024 even cheaper than they began 2016. Relative to their net asset value, gold miners are near the cheapest they’ve been in 40 years.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

I expect miners to catch up in the second half. Gold stalled again this week, interrupting the normal trend down to 30 on the fractal dimension. The odds still favor higher prices.

Miners & Related

Sandstorm Gold (SAND – $5.77) did an interesting interview with Jay Martin:

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $67,344.53) is rebounding from the post-halving selloff. Both bitcoin and ethereum rallied as the House passed the Financial Innovation and Technology for the 21st Century Act (FIT21). This act would make the Commodities Futures Trading Commission (CFTC) the leading regulator of digital assets (instead of the stonewalling SEC) and establish consumer protections. It probably won’t pass in the Senate because Democrats believe it would effectively deregulate most cryptocurrencies by removing them from SEC purview.

But SEC Chairman Gary Gensler seems to be feeling the heat as rumors spread that spot ether ETFs will be approved (see below).

More than 600 money managers have unveiled $3.5 billion in investments in spot bitcoin exchange-traded funds in their quarterly 13F filings with the SEC.

Millennium Management was the largest investor, allocating a whopping $1.9 billion. Their investments include $844.2 million in BlackRock’s iShares Bitcoin Trust (IBIT), $806.7 million in Fidelity’s Wise Origin Bitcoin Fund (FBTC), $202 million in the Grayscale Bitcoin Trust (GBTC), $45.0 million in the ARK 21Shares Bitcoin ETF (ARKB), and $44.7 million in the Bitwise Bitcoin ETF (BITB).

Second was Schonfeld Strategic Advisors, a hedge fund managing $13 billion in assets, with a $248 million investment in IBIT and an additional $231.8 million in Fidelity’s fund. Morgan Stanley, JPMorgan, Wells Fargo, UBS, BNP Paribas, and Royal Bank of Canada also are on the list of investors.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

The iShares Bitcoin Trust (IBIT- $38.27) remains the cheapest and easiest way to buy bitcoin. Last week,The US-listed spot bitcoin (ETFs) had four straight days of inflows, with IBIT receiving $94 million on Thursday alone, signaling a shift in investment sentiment. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $3,785.88) will benefit if the rumor that the SEC is about to approve spot ETH exchange-traded funds is true. At least five of the potential ethereum ETF issuers submitted amended form 19b-4s – Fidelity, VanEck, Invesco/Galaxy, Ark/21Shares, and Franklin. Today, the SEC gave a green light to the NYSE and the Nasdaq to list eight exchange-traded funds that hold ether, but they still have not given approval to money managers that want to issue the new products.

If the SEC does approve ethereum ETFs, it will be one of the biggest regulatory 1800s in recent SEC history and proof that the crypto crowd is a legitimate voting block. All the guidance coming from Gensler was that he was even going to declare ETH a security, which would have made it a complete no-go. I won’t believe it until I see the press release, but if this is approved it’s a very big deal.

Alliance Bernstein, a $725 billion asset manager, said etherium will reach $6,600 after spot Ethereum ETFs approvals. There is a mania in ethereum open interest:

Click for larger graphic h/t @TheMarketEar

Click for larger graphic h/t @TheMarketEar

ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

The Grayscale Ethereum Trust (ETHE- $33.80) will jump if spot ETFs are approved. ETHE is a Buy under net asset value.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $76.86

Oil slipped after crude stocks unexpectedly added 1.83 million barrels this week when a draw of 2.0 million barrels was expected. Gasoline stocks declined sharply. We just printed 9.33 million barrels per day of pre-Memorial Day gasoline demand. March monthly demand will be a five-year high. I still think steady crude draws are the most likely path, and inventory levels remain low. Refining margins are moving higher and global oil inventories are set to drop in the coming weeks.

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

After the Northeast ran out of gasoline following Hurricane Sandy in October 2012, Congress created a one million barrel (42 million gallons) Strategic Gasoline Reserve. The Biden Administration has decided to empty it in advance of the July 4 weekend in an effort to keep gas prices down. It should reduce prices by one to three cents a gallon for a few days. The amount to be released only adds up to about 2.7 hours of total U.S. gasoline consumption.

But as HFI Research said, just as the oil data improves, everyone gets bearish. That’s the nature of the oil market. Demand is up:

Click for larger graphic h/t @HFI_Research

Yet sentiment has tanked:

Click for larger graphic h/t @HFI_Research

Click for larger graphic h/t @HFI_Research

HFI Research wrote: “The funny thing about the oil market is that speculators tend to always swing so wildly from one side to the next that you wonder just what’s going on in their brains. It wasn’t long ago that the conflict between Israel and Iran would send oil prices into the $100s only to not hear a blip about it now when prices are falling. There’s nothing like price-changing sentiment, but I’m here to tell you that the oil data is finally starting to improve just as sentiment bottoms out.”

The July 2026 Crude Oil Futures (CLN26.NYM – $69.14) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $38.44) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $11.95) is a Buy under $11 for a target price of $24 or more.

Primary Risk:Oil prices fall.

EQT (EQT – $39.91) is up because over the past three weeks, US natural gas prices have surged more than 30% to above $2.65 per million British thermal units (mm/BTU), fueled by production declines and increased feedgas demand for liquefied natural gas (LNG) exports.

Last Thursday, Goldman Sachs strategists said the return of gas prices above $2.00/mmBtu aligns with their expectations, as production curtailments “would ultimately lead to lower storage congestion risks for this summer. That said, we see only limited further upside from current levels, with stronger gas prices risking a return of congestion concerns.”

They noted that prices above $2.00/mmBtu reduce gas competitiveness compared to coal, with a $0.50/mmBtu increase potentially cutting gas demand by 1 billion cubic feet per day (Bcf/d). Moreover, higher prices may prompt the restart of previously shut-in wells. EQT, the largest producer in the Appalachia region, indicated it would resume production if prices sustainably exceed $1.50/mmBtu. Appalachia prices have averaged $1.44/mmBtu month-to-date, up 10¢ from last month. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Energy Fuels (UUUU – $6.61) rose after the US government indicated it will ask companies to bid next month on contracts for as much as $3.4 billion of domestically produced nuclear reactor fuel. President Biden signed a ban on imports of enriched uranium from Russia, which provides about 25% of the reactor fuel in the US. The ban takes effect August 11. The signing unlocked $2.7 billion in funding in previous legislation to build out the US uranium fuel industry. UUUU is a buy under $8 for a $30 target.

Primary Risk: Uranium prices fall.

Freeport McMoRan (FCX – $51.20) has run up with the price of copper, but maybe too much or too quickly. I expect copper to hit $7.50 a pound later this year and we may exit FCX then. It has become a crowded trade and you know I don’t like that. I’m staying with it for now because (1) we were early and have a good entry point; and, (2), it really does take a long time to create more supply.

Steno Research says the next few weeks will be absolutely vital in copper as we will see whether China will offload copper stocks to the West as they are currently paid to do. If they DON’T, we can conclude that China is building stocks for strategic purposes.

Click for larger graphic h/t @AndreasSteno

Chinese copper stocks are extremely seasonally elevated:

Click for larger graphic h/t @AndreasSteno

Click for larger graphic h/t @AndreasSteno

China produces twice as many electric vehicles (not just cars, but vehicles, including e-bikes) as gas-powered cars. This makes sense. China is building new sources of electricity, with more nuclear power plants under construction than any other country. And it has ample rare earth metals and battery manufacturing capacity. What it does not have is an overabundance of oil. Going electric makes China more resilient and energy independent.

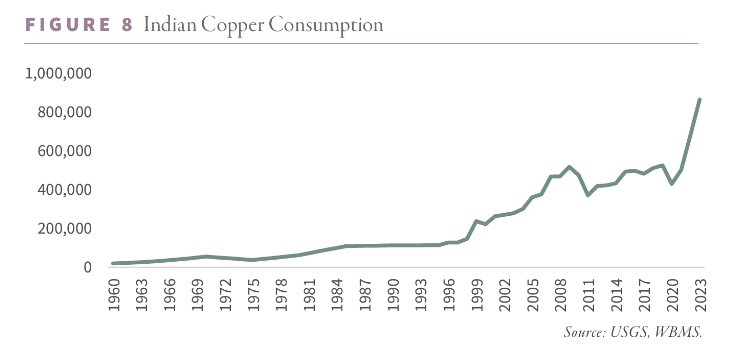

India is another copper story. While China’s economic growth is slowing, India’s is ramping up. Demand for EVs there is surging. The country is building a network of high-speed rail, along with multiple nuclear and solar power plants. The most populated nation in the world will need to expand its energy grid for years to come.

As India becomes a preferred manufacturing center for global companies, it is consuming record amounts of copper.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

Speculators are all-in, which is a negative sign for contrarians. Leveraged funds have built the largest bullish copper position in more than three years: “Long copper” has become a crowded trade, with net speculative long positioning increasing significantly in recent weeks.

Click for larger graphic h/t @WinfieldSmart

Click for larger graphic h/t @WinfieldSmart

Just a few months ago, most analysts didn’t expect a copper deficit until late this decade. But recent mine disruptions and lower production guidance now point to a deficit as soon as this year. Goldman Sachs projects a 5 million ton deficit by 2030.

Increasing supply is not a quick or easy process—it can take decades to bring a new copper mine online. Copper miners like Freeport McMoRan who can ramp up output could be extremely well-positioned.

Investors and large miners are making moves. Activist investor Paul Singer’s investment firm, Elliott Management, has reportedly built a $1 billion stake in miner Anglo American. Anglo has recently received and rejected two buyout offers from behemoth copper miner BHP Group Ltd. (BHP). FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

Other Recommendations

Mongolia Growth Group (MNGGF – $1.18) published their March quarter letter to shareholders. CEO Harris Kupperman said: “Our public securities portfolio produced a $2,335,164 unrealized gain and a $622,011 realized gain. I would like to caution you strongly that returns, as we have recently experienced, are highly unlikely to be repeated in future quarters. At quarter-end, our portfolio was concentrated in investments in oil futures and futures options, energy services companies, uranium equities, and a Florida landowner. Additionally, we own a small position in a cryptocurrency named Monero, which we sold some of during the first quarter of 2024. We view these investments as highly liquid, inflation-protected, alternatives to holding cash, and we intend to liquidate various investments should we find additional businesses to launch or acquire stakes in.

“We believe our shares to be undervalued and during the quarter, MGG repurchased 781,300 shares under its Normal Course Issuer Bid. At quarter end, our share count was 26,094,399, or 27% fewer than during our peak share count in 2016. To date, the company has repurchased a total of 9,438,200 shares.”

MNGGF is a Hold.

Primary Risk: Harris Kupperman makes bad investments.

* * * * *

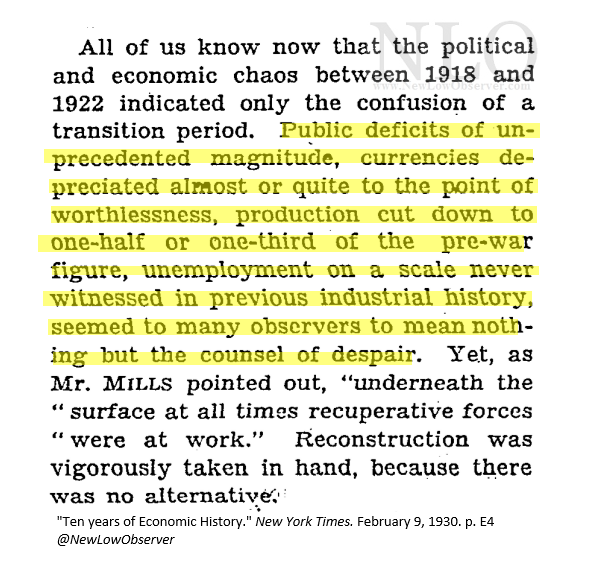

1918-1922: The View After the Spanish Flu Pandemic

Click for larger graphic h/t @NewLowObserver

Click for larger graphic h/t @NewLowObserver

* * * * *

h/t Elon Musk

* * * * *

Your listening to Neil de Grasse Tyson Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 5/23/24. Check out the complete Portfolio page HERE.

Portfolio Protection

June 21 SPY $505 put (SPY240621P00505000 – $1.53)

June 21 SPY $410 put (SPY240621P00410000 – $0.11)

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $186.88) – Buy under $175 for new iPhones

Corning (GLW – $36.12) – Buy under $33, target price $60

Gilead Sciences (GILD – $66.17) – Buy under $80, target price $120

Meta (META – $465.78) – Buy under $345, target price $400

Palantir (PLTR – $20.72) – Buy under $22, target price $100+

PayPal (PYPL – $61.58) – Buy under $68, target price $136

SoftBank (SFTBY – $27.09) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $9.61) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $55.28) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $8.62) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $19.59) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $11.74) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.22) – Buy under $13, target price $30+

Velo3D (VLD – $0.18) – Buy under $1, target price $10

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $3.85) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.09) – Buy under $2, target $20

Aptose Biosciences (APTO – $1.08) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $7.46) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $5.83) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $10.96) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.70) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.24) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $16.98) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($30.33) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $27.44) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $33.62) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $22.38) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $33.86) – Buy under $30, target price $50

Coeur Mining (CDE – $5.37) – Buy under $5, target price $20

First Majestic Mining (AG – $7.04) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.46) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.77) – Buy under $10, target price $25

Sprott Inc. (SII – $45.43) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $67,344.53) – Buy

iShares Bitcoin Trust (IBIT – $38.27) – Buy

Ethereum (ETH-USD – $3,808.45) – Buy

Grayscale Ethereum Trust (ETHE – $33.80) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $69.14) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $38.44) – Buy under $40; $100+ target

Vermilion Energy (VET – $11.95) – Buy under $11; $24 target

EQT (EQT – $39.91) – Buy under $35; $70 first target

Energy Fuels (UUUU – $6.61) – Buy under $8; $30 target

Freeport McMoRan (FCX – $51.20) – Buy under $44; $65 target within two years

Other Recommendations

Acreage Holdings (ACRDF – $0.44) – Buy under $2 for the Canopy Growth merger

Hold

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $149) – Hold for buyout

Mongolia Growth Group (MNGGF – $1.18) – Hold for probable liquidation

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

1

MM – is the MDNAF 5/31 ASCO presentation a possible major stock price move catalyst?

I was wondering the same thing!! MM, also curious of your thoughts on this PR from last week.

ASCO has informed the Company that the previously accepted MDNA11 oral abstract has been withdrawn due to alleged violation of their prior publication policy based solely on their review of the abstract presented at AACR 2024.

Medicenna disagrees with ASCO’s decision as the AACR 2024 abstract was limited to on-going interim results whereas the ASCO 2024 abstract specified data from a completed phase 1 study that were not presented at AACR 2024.

No other matters were raised by ASCO regarding any data included in the submitted abstract, the planned data intended for presentation at ASCO, or any aspect of the clinical trial.

The Company looks forward to sharing the full high-impact data set of our potentially best-in-class IL-2 and emerging results from the ABILITY-1 trial of MDNA11 at a special virtual event to be organized over the next 2 to 4 weeks. Details on the event will follow.

Medicenna Provides Update on its Presentations at the 2024 ASCO Annual Meeting – Medicenna Therapeutics

ASCO hissy fit, but it’s their playground…

Probably not. Wall Street doesn’t care about MDNA55 until the company announces a deal with Big Pharma to fund the Phase 3. The purpose of this presentation is to attract a partner.

“I still expect high-level churning through the election, followed by a sharp move depending on who wins.”

Can you expand on this? Which candidate creates a sharp move up and which candidate creates a sharp move down?

When Trump won in 2016 (giving him a win-loss record thru today in his runs for the presidency of 1-2) markets tanked. That did not happen when Biden was elected.

Were either moves sharp? I can’t recall. Meanwhile, we are at record highs so we all know these knee jerk reactions don’t mean much.

Taking a look on FED St Louis data site I can see the S&P 500 closed at 2111.72 on Tuesday, Nov 1 (election day). It moved down to close at 2085.18 on Friday Nov 4 before starting an uptrend and closing 2016 @ 2,238.83, a 6% increase from election day. I was going to go off my memory and would have been somewhat off. I recall the global markets down heavily when it became apparent Trump would win but then within a day retracing most of the losses.

Tanked?

Election Day Nov 8, 2016 S&P 500 close=2139

Nov 9 2163

Nov 10, 2167

MM–on VLD, you still are silent on the critical cash situation and big dilution coming. Therefore, your buy and target prices cannot be relied on. If orders are delayed beyond their forecasts, the company has a high chance of BK. Another NVTA in that case. The stock may never even reach your buy price of up to $1. Subscribers should base their trading on their own DD if they are qualified, and good amateurs like Brent. We pay you for a thorough financial analysis, so this is your responsibility. We and you watched the 98.2% plunge from your original buy price of $10. You remained a cheerleader all along, and still are, without complete critical financial analysis–income statement, balance sheet and cash flow analysis, debt, etc.

BTW, does the company mean FREE cash flow positive by end of 2024?

Sorry JGMD, mike already got your money ( I assume you went for the lifetime membership like me), don’t expect much.

I did buy VLD at much higher prices because they were a strategic partner with SpaceX. That wasn’t on MM, it was all me.

I fully expect a complete loss now.

I don’t care about subscription costs. They are worth it for a newsletter writer who does careful complete financial analysis in addition to storytelling about company hopes. I estimate that 90+ % of NWI subscribers invested in VLD if they held on as MM advised are sitting on losses 10-500 times the yearly subscription costs. A few like me who averaged down (I’m at 44 cents, have 55-60% losses on paper, still 100X subscription costs). To be fair to MM, he doesn’t make individual investor decisions because he doesn’t offer money management services, but he has steadfastly recommended VLD all the way down from the entry price of $10.

If VLD meets its 2024 revenue forecast and cashflow breakeven, the stock may bottom at 10 cents this year considering the 100+ % of dilution required, then rise out of those ashes to $1 or more a few years from now or sooner upon buyout. I am expecting eventually to at least break even from 44 cents (although having cash tied up while waiting, which could be used for other investments). There is still a reasonable chance of a total loss in BK, mainly if cash breakeven occurs much later than 2024. Even MM projects as late as 2026.

Musk used to be the new kid challenging the space industry behemoths. Now he is the behemoth trying to crush the new kids.

https://www.nytimes.com/2024/05/28/us/politics/elon-musk-space-launch-competition.html?unlocked_article_code=1.vU0.tBNv.yK0qUpWX0hng&smid=url-share

I am planning on writing put options. Does anyone have any experience? Where is a good source to find And follow the best candidates? Or other useful insights?

Try this. NAT will release its quarterly results Wednesday a.m. Traditionally during this oil tanker bull market earnings have been outstanding. If it announces a dividend of 15 cents, shares will rise from current 4.24 to near 4.50. When shares go ex-div, share price generally plummets below $4. When you think shares are near a peak before ex-div, look to sell the $5 or $4.5 put expiring in July or August if the price is right because you can expect NAT to be below $4 a month or so after it goes ex-div.

Thanx

MM, in the previous newsletter you mentioned in one of the comments that the drop in AKBA’s price was due to the launch being delayed until January 2025.(which is true) I follow another trader who recommended AKBA before approval and sold once they released that they were delaying the launch until 2025.(which is what I did as well, thankfully) He mentioned that the price could go down close to $1.00 and wait to re-enter. He also mentioned to wait until the vote below is done to re-enter because the price could go under a $1.00 if passed. How does the dilution below affect your strategy and price targets?

The 2024 Annual Meeting of Stockholders, or the Annual Meeting, of Akebia Therapeutics, Inc., or the Company or Akebia, will be held on Thursday, June 6, 2024, at 10:00 a.m. Eastern Time in a virtual meeting format via live webcast.

Approve an amendment to the Akebia Therapeutics, Inc. 2023 Stock Incentive Plan to increase the number of shares of common stock available for issuance thereunder by 9,800,000 shares.

Thanks for mentioning this critical meeting June 6. Currently there are about 200 million shares outstanding, so this 10 million addition would be 5% dilution, down to a PPS of about $1.00 very soon. (Not as bad as for VLD, probably 100+% dilution for 2024 expenses.). But Auryxia is a money loser and is losing its patent soon. Vafseo sales won’t begin until Jan 2025. What are revenue forecasts for V in 2025? When is AKBA projected to breakeven, thereby avoiding further dilution? I anticipate significant expenses in 2024 in preparation for V launch, as well as high marketing costs after launch, although how much of the marketing costs will be paid by Vfor/Fresenius?

MM, please answer these questions and do a full accounting analysis of AKBA. You already erred in your recent guess of a bottom at $1.60-1.80. Certainly your buy price of $2 is way off track for now. We should have plenty of opportunities to add way below $1.

Good luck with that. I would buy AKBA up to $2. If you think you can get it way below $1, you should wait. I think anyone who waits could completely miss it.

AGAIN and AGAIN you continue to hype long term hopes and ignore short term financial reality. Your reply above is nothing but cheerleading. To have substance to your views, you need to answer hard financial questions which I raised above. Even if you are correct that long term, AKBA is a big winner, your subscribers deserve the opportunity to enter at much lower prices than today. We are being shot by the firing squad of all the NWI small company disasters. Subscriber Michael may be correct that VLD is your next NVTA.

Further, many years ago I bought a small stake in KERX. When it merged into AKBA, my AKBA entry was over $4. It’s a good thing that I didn’t follow you down and down, and waited until about 6 months ago to buy a lot more at $1.15, which brought my average cost down to $1.71. Until Vafseo sales show potential, which won’t be for another full year, we have the opportunity to speculate again by buying way below $1. This bum CEO wants a reverse split and further dilution so he can continue to collect his outlandish salary for destroying shareholder wealth over many years. Another parasite CEO like TN of ARTH. Most subscribers are probably a lot more in the doghouse than I. Please show some fiduciary responsibility, even if we make our own trading decisions. Prove me wrong with data, or at least financial estimates.

It is troubling that the CEO bungled the sales effort for Auryxia. Will he do any better for Vafseo? There are some advantages of V compared to Auryxia. Auryxia is an ordinary iron compound, but V is a real innovation. CEO Butler would have to be mentally incompetent to blow V marketing. But you never know, because his main priority has been to collect an outlandish salary without regard for shareholder interests.

It is also troubling that the comparable drug Daprodustat was turned down for marketing in many countries due to perception of low potential sales. Dapro is almost as good as V. Sales of V could be slower than the hype has suggested. Nearly everyone was predicting $4 for AKBA upon approval, so the plunge to $1.00 today is troubling. I know that the market was troubled by the delay of launch until Jan 2025 due to TDAPA, but if the finances were good before then, the PPS might have stayed at $2-3. The fact that the PPS is dropping like a rock suggests that finances are unstable, and the company can’t afford too many delays. If sales are slow in coming, cashflow breakeven could be far away.

This is why, MM, you must do a serious cashflow analysis. We could be facing much more dilution ahead, with PPS plunging way below $1 or even pennies. A buy price of up to $2 is completely inappropriate at this point. Many of us including myself are devastated at VLD now, and we cannot afford another disaster. AKBA could be next NVTA, ARTH, APTO, etc, etc, etc.

AKBA down 5% so far today, far worse than the general market. MM–can you learn from your mistakes? If you don’t learn, your loss of subscribers will accelerate even more. Very few people are left commenting on this board.

To all,looking at the short interest on EDIT it stands at over 25 precent of the float so investors here beware after the shafting we recieved with nvta the short interest was over 25 percent on that also,have a great safe holiday.

Yes, they are short a company with a market cap under $500 million that will get ~$2 billion in royalties from a single license.

Michael, I just saw your post on the last board about your flight cancellation due to your claim of greedy companies. Bad IT is a worse problem than that. See my reply there.

MM, what is a fair value for QQQ or $SPX? Thanks.

New World Investor for 5.30.24 is posted. Added PLTR to Top 5 Long-Term.