Dear New World Investor:

There is an asymmetric opportunity available – relatively low risk for a relatively large reward. It’s relatively low risk because it’s cheap because Wall Street hates it and it’s a lower-risk legal structure. It’s a relatively large reward because – well – Wall Street is wrong. Here’s why.

Wall Street thinks commercial real estate is falling apart. Recently, investors in the AAA tranche of $308 million of debt backed by 1740 Broadway in midtown Manhattan received only 74% of their money. Creditors in the five lower tranches were totally wiped out. Numerous Wall Street trader/salesmen had to call their clients and say: “Hey, remember that BB+ tranche on 1740 Broadway that I got you when you needed yield? Ummm…you need to reprice it. To zero. Sorry.”

So of course Wall Street hates commercial real estate. The market for office buildings, already on the ropes from higher vacancy rates due to the rise in remote-work policies, has been crushed by high borrowing costs, Roughly $930 billion in commercial real estate loans will come due this year, according to the Mortgage Bankers Association. Commercial mortgages are financed on shorter terms than residential mortgages, often with balloon payments, or large lump sum payments due at maturity.

Many of those loans will have to be refinanced at a substantially higher interest rate than they carry now, yet net rental income can’t cover the interest payments (operating expenses for all types of buildings have gone up dramatically in the last few years, particularly insurance premiums) and the value of the building is less than the debt. The lenders, including many regional banks, are shafted.

Banks are the largest lenders of commercial mortgages and hold about $3 trillion in commercial real estate debt. According to the FDIC, about 98% of banks engage in commercial real estate lending, with those loans making up the largest loan portfolio type for nearly 50% of all banks.

Click for larger graphic h/t St. Louis Fed

Click for larger graphic h/t St. Louis Fed

Banks, investors, and property owners are beginning to accept that many office buildings are worth less than their debt, and that’s leading to a steady drumbeat of distressed sales. Over the last four months, seven office properties were sold at a whopping loss of more than $100 million each, up from just one such sale in the first three months of the year.

Click for larger graphic h/t Moody’s Analytics

Click for larger graphic h/t Moody’s Analytics

With a plethora of vacant office buildings and a shortage of millions of apartments to meet demand, a bipartisan group of Federal lawmakers is trying to make it easier for developers to convert underused properties into housing by giving them a 20% tax credit for qualified property conversion expenditures. New York City developers who set aside 25% of an office conversion’s units for affordable housing can qualify for a 90% tax abatement.

It makes a great photo op for a politician, but the vast majority of Office cannot be economically converted to Multifamily. The sector doesn’t need legislation, it needs to trade for the value of the dirt underneath it. (I may take a look at demolition services firms.)

For office buildings, the day of reckoning is here. But, guess what? Most commercial real estate is not office buildings, yet all commercial real estate stocks have been dragged down by Wall Street’s abandonment of the sector.

Hospitals and assisted living centers are not vacant – far from it, with the aging population. Self-storage centers are full. We have a shortage of multifamily apartment buildings. Target, Walmart, Home Depot, et.al. are not going bankrupt. Many non-office REITs are cheap (market capitalization/funds from operations), down sharply from their highs, and pay a decent growing dividend. I’m not going to veer any further off course from technology in this newsletter, but if you are interested you might take a look at some of the larger REITs like Realty Income (O), Community Healthcare (CHCT), Global Medical (GMRE), Public Storage (PSA), or Extra Storage Space (EXR). Or just buy an exchange-traded fund like the iShares U.S. Real Estate ETF (IYR).

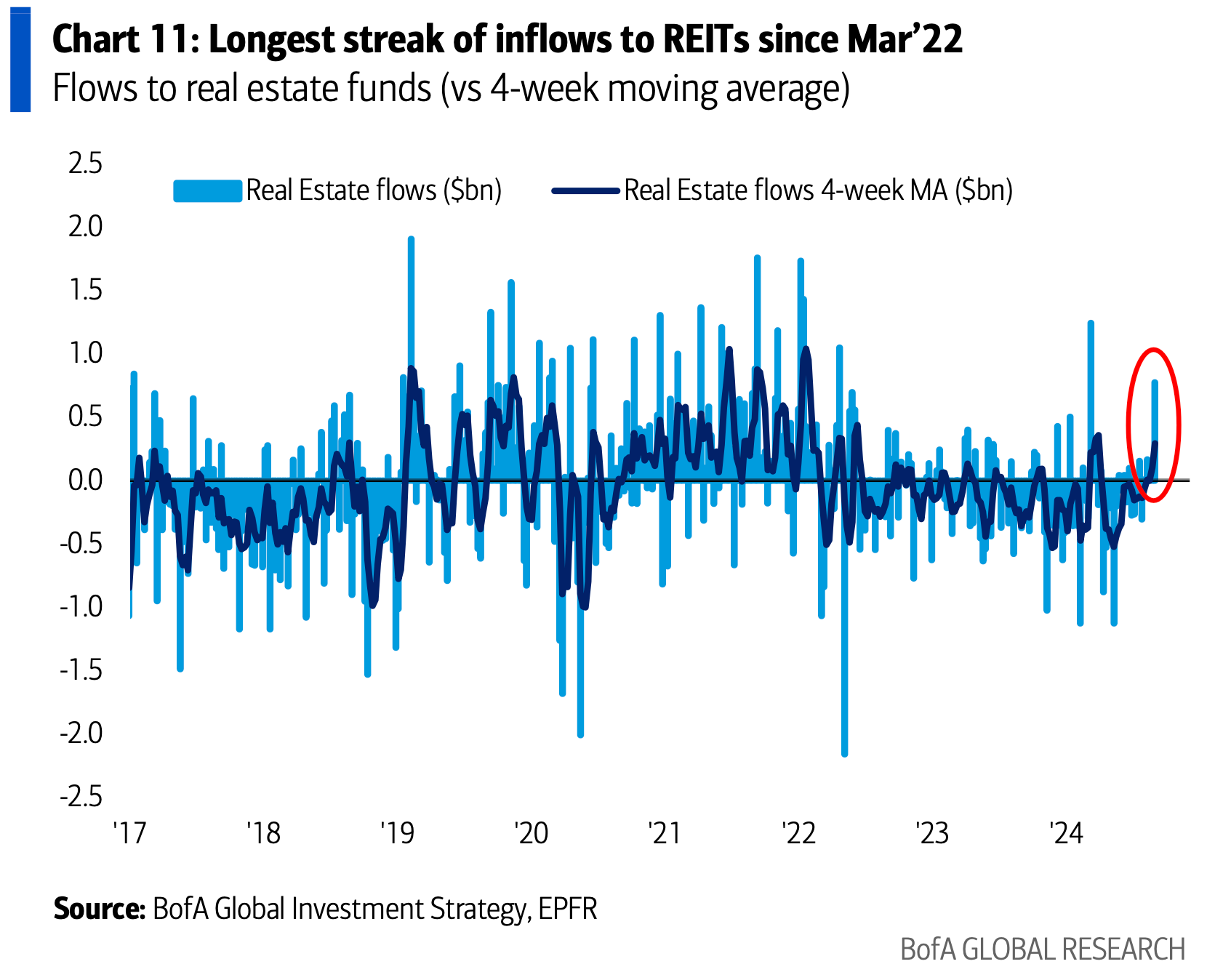

We are not catching a falling knife here. REITs have seen five consecutive weeks of inflows, the longest streak since March 2022, including +$800 million this past week, the most in five months.

Click for larger graphic h/t BofA

Click for larger graphic h/t BofA

In the near term, the REITs probably will move based on the size of the Fed’s September cut. Traders are pricing in a 41% probability of a 50 basis point cut and a a 59% probability of 25 basis points, per the CME FedWatch Tool. I expect just 25bps, so there could be a quick sell-off on September 18 and 19.

Market Outlook

The S&P 500 lost 1.6% since last Thursday, finishing today just under its 50-day moving average at 5506. The Index is up 15.4% year-to-date. The Nasdaq Composite lost 2.2% but is up 14.1% for the year. The SPDR S&P Biotech Exchange-Traded Fund (XBI) fell 2.8%, back to sub-100 territory. It is up 9.9% year-to-date. The small-cap Russell 2000 dropped 3.3% and is up only 5.1% in 2024.

Election year-to-date equity inflows are outpacing four out of the last five election years, but seem likely to flatten or decline from here until the election and then rise.

Click for larger graphic h/t @WallStJesus

The fractal dimension is consolidating fairly quickly, setting us up for the usual December quarter rally.

Top 5

Changes this week: None

Near-Term – chronological order

SCYX – ScyNexis – Data releases and resolution of the manufacturing problem

AAPL Apple – September iPhone 16 introduction

USL United States 12 Month Oil Fund, LP – crude should rise quickly

EQT EQT –natural gas price rebound

CMPS – Compass Pathways – Rebound from negative AdCom review of MDMA and Phase 3 data release in December quarter

FCX Freeport McMoRan – copper shortage

AKBA Akebia Therapeutics – Vafseo TDAPA approval in January

Long-Term – alphabetical order

ABCL AbCelllera – Will become a huge pharma royalty company

EQT EQT – largest US natural gas company

IBIT iShares Bitcoin Trust – Bitcoin is headed for $100,000

META Meta – a (the?) leader in the metaverse

PLTR Palantir – a (the?) leader in AI applications software

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

Economy

The Atlanta Fed’s GDPNow model ticked up to +2.5% last Friday, then back down to 2.1% due to weakness in personal consumption expenditures.

Click for larger graphic

Click for larger graphic

The Job Openings and Labor Turnover Survey (JOLTS) report fell more than expected to 7.67 million jobs open at the end of July, below the 7.91 million at the end of June and the lowest number of job openings since January 2021.

Click for larger graphic h/t Yahoo Finance

Click for larger graphic h/t Yahoo Finance

At the Jackson Hole meeting, Fed Chairman Powell said the cooling in the labor market has been “unmistakable.” Powell added the downside risks to the Fed’s mandate for full employment have risen, and said: “It seems unlikely that the labor market will be a source of elevated inflationary pressures anytime soon. We do not seek or welcome further cooling in labor market conditions.”

Unless tomorrow’s August payrolls report is a barn-burner, the first Fed cut is a done deal. Economists expect the economy added 166,000 jobs in August, up from 116,000 in July, which may be revised in tomorrow’s report. They think the unemployment rate ticked down to 4.2%, the first decrease in the unemployment rate since March.

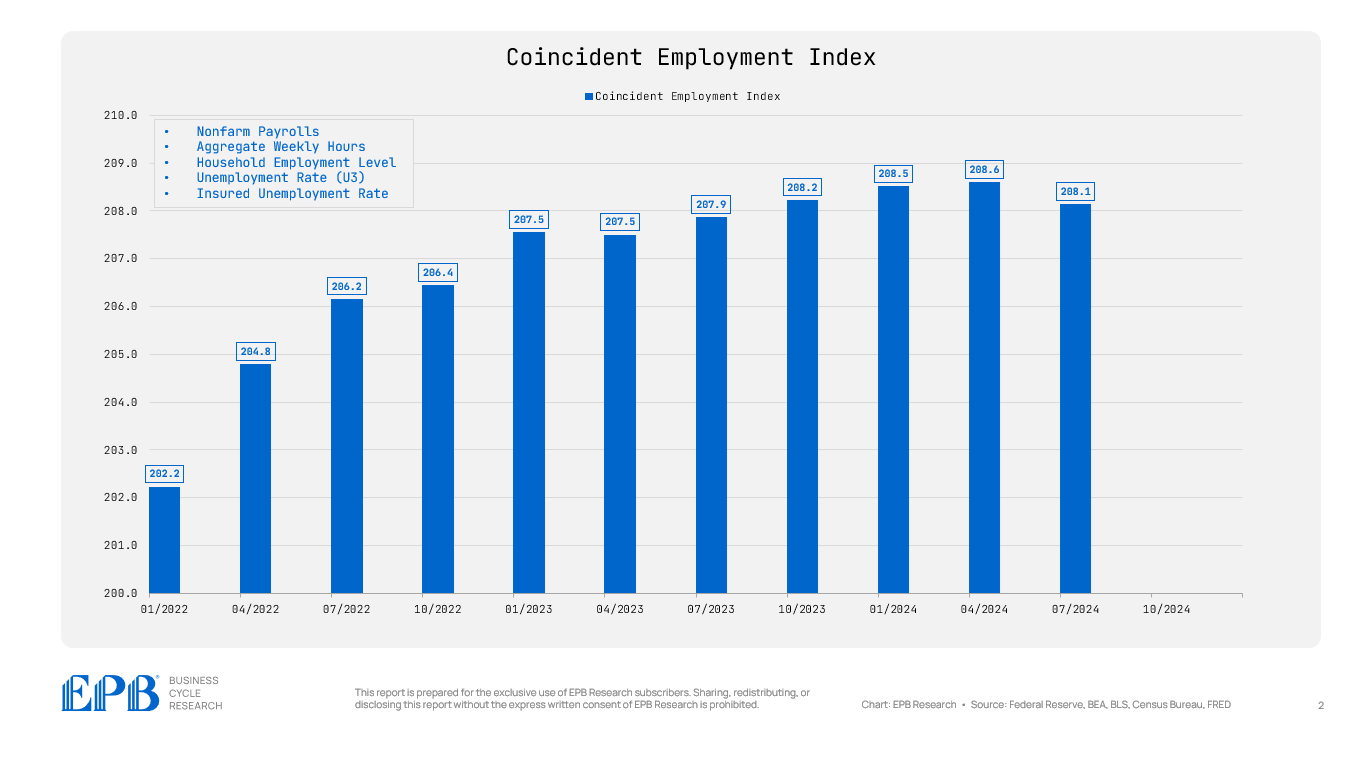

EPB Research created a coincident indicator of the labor market to try to see what is really going on. It includes nonfarm payrolls, aggregate weekly hours, the household employment level, the U3 unemployment rate, and the insured unemployment rate. The chart below shows the quarterly average level of the EPB Coincident Employment Index. The biggest point of note is that the Index has declined so far in the September quarter and now is lower than the average reading in the June and March quarters.

Click for larger graphic h/t @EPBResearch

Click for larger graphic h/t @EPBResearch

Early in 2022, the EPB Coincident Index rose sharply as the labor market was very hot. The rate of increase started to ease throughout 2023, and now is declining. The labor market is weakening and possibly contracting, which has a history of coinciding with economic downturns and interest rate reductions from the Federal Reserve.

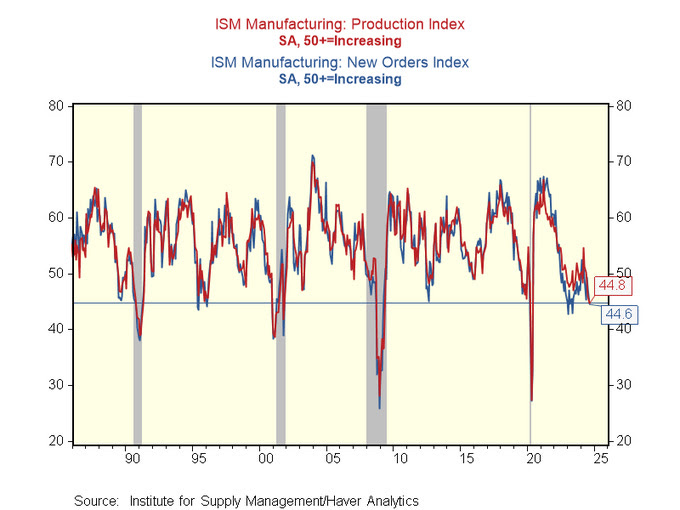

The goods-producing side of the economy is in trouble. The ISM Manufacturing Index came in at 44.8, its lowest level excluding the pandemic since April 2009. New orders declined for the fourth time in the last five months. There is no need to build inventories. Not an encouraging report.

Click for larger graphic h/t @RenMacLLC

Click for larger graphic h/t @RenMacLLC

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, September 6

MDNA- Medicenna – 8:00am – Oral presentation on MDNA209 at the Promise of Interleukin-2 Therapy Conference

August Payrolls – 8:30am – +166,000 expected; July was +116.000

AKBA – Akebia – 9:30am – Wells Fargo Healthcare Conference

Saturday, September 7

MDNA- Medicenna – 3:00am – Oral presentation on MDNA113 at the Promise of Interleukin-2 Therapy Conference

Monday, September 9

PYPL – PayPal – 11:50am – Goldman Sachs Communacopia + Technology Conference

AAPL – Apple – 1:00pm – iPhone 16 introduction

Tuesday, September 10

AG – First Majestic – Through 9/13 – Precious Metals Summit, Beaver Creek, CO

QUIK – QuickLogic – Through 9/13 – H.C. Wainwright Global Investment Conference

GILD – Gilead Sciences – 10.50am – Baird Healthcare Conference

Wednesday, September 11

13 Years Ago Today. Never Forget.

Consumer Price Index – 8:30am

SCYX – ScyNexis – 10:00am – H. C. Wainwright Global Investment Conference

Short Interest – After the close

RKLB – Rocket Lab – 6:45pm – Morgan Stanley Laguna Conference

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $222.38) Sports, the free app for iPhone that gives sports fans access to real-time scores, statistics, live betting odds, and more, introduced updates for NFL and college football games. They include enhancements to play-by-play, offering quick access to scoring drives presented alongside the view of every game play. A new dynamic drive tracker lets fans visualize where the ball is on the field at any time. For college football, fans can now follow the top 25, updated weekly, in addition to any of their favorite teams and conferences. Every game will also feature real-time scores and stats, similar to all other leagues in the app.

After the iPhone 16 introduction next Monday, expect a spate of “too little, too late” notes from Wall Street as they try to shake as many retail holders out of the stock as possible. Guess who will be buying what retail sells? AAPL is a HOLD – I expect to move back to Buy under $175 for new iPhones.

Corning (GLW – $41.37) EVP & CFO Ed Schlesinger presented at the Citi Global TMT Conference (AUDIO HERE and TRANSCRIPT HERE). At the end of 2023 all of their markets were in a cyclical downturn caused by depressed demand at their customers that also caused increased inventories at customers. Corning called the bottom in the March quarter as customers worked through inventories and management is seeing markets recover faster than they expected.

Optical has been especially strong due to AI and they have good visibility there for the next 12 months. Display picked up in the June quarter and that has continued into the September period. Smaller markets are mixed. The heavy-duty diesel market still is depressed but Corning’s emission controls business still is growing. The US requires gas particulate filters on cars starting with the 2027 model year.

Adding $3+ billion of sales in the next three years from ~$13 billion to ~$16 billion a year without adding any costs is their Springboard plan. In June, they went out to five years and an $8 billion opportunity that would take them to ~$21 billion in 2028. So far, they are ahead of plan.

They work hard to be the market leader, the technology leader, and the lowest-cost provider in every market they serve. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2025 .

Gilead Sciences (GILD – $78.77) presented at both the Wells Fargo Healthcare Conference (AUDIO HERE) and the Morgan Stanley Global Healthcare Conference (AUDIO HERE).

Management said they have a new launch in the liver area they dominate that will turn that into a growth business. Seladelpar, acquired when they bought CymaBay, was approved by the FDA on August 14 with a great label. It treats primary biliary cholangitis (PBC), an orphan disease with about 130,000 patients in the US and almost that many in Europe. It’s under-diagnosed and under-treated. Gilead’s sales force already covers the doctors who treat PBC, where there are no other good treatments, and it will drive sales in 2025.

The Lenacapavir trial results in HIV prevention were 100% successful in women in Africa. Their second Phase 3 Lenacapavir trial reads out at the end of 2024 or early 2025 and it looks like a game-changer in both the US and globally. Lenacapavir is an every-six-months injection, which guarantees compliance compared to the oral drugs that people don’t take daily, as they are supposed to. Gilead will hold an HIV Investor Day in the December quarter.

In 2025, the Medicare Part D downward price adjustments will roughly offset the growth in HIV. Product launches, including Seladelpar, will provide growth. I agree with this Seeking Alpha author: Gilead Sciences: Buy This Bargain Before It’s Gone. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $516.86) was named a top Internet pick in initial coverage by Cantor Fitzgerald. Meta was initiated with an Overweight rating and added to Cantor’s Top Pick list as the company has “plenty of levers to capture share gains” as AI deployment can deliver incremental engagement, monetization, and revenue growth over the next two or three years. META is a Hold – I expect to move back to a Buy under $400.

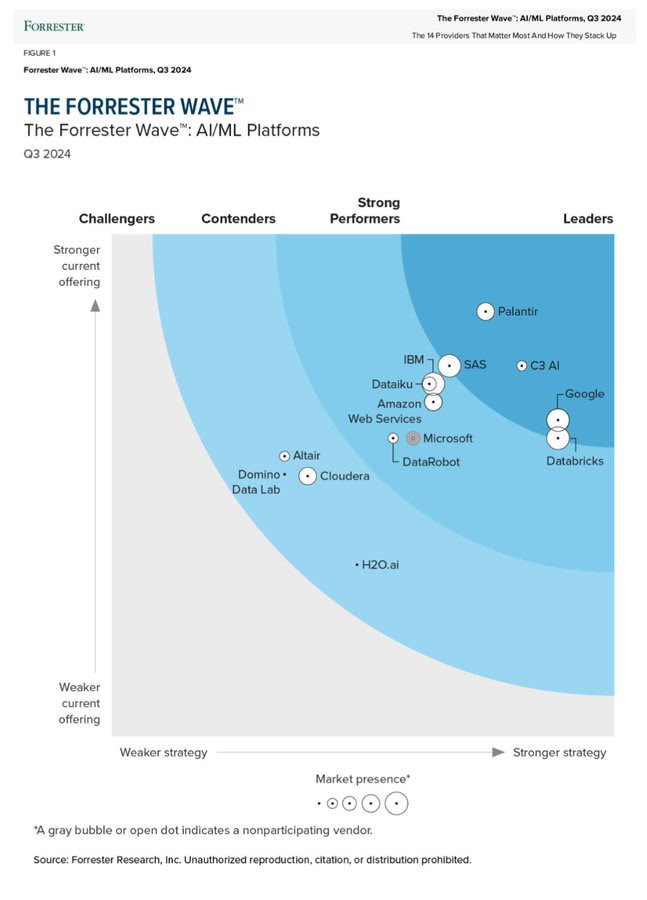

Palantir (PLTR – $30.16) was ranked #1 by Forrester as an AI/ML platform. Forrester said: “Palantir is quietly becoming one of the largest players in this market, seeing a consistent sustained growth rate in the past half-decade by making its platform more accessible to users.”

Click for larger graphic h/t @arnytrezzi

Click for larger graphic h/t @arnytrezzi

Palantir released a new video with Architect Chad Wahlquist explaining how traditional enterprise software created a Tower of Babel that looks poised to tumble, but not Palantir. He said: “If it’s not in production, it’s not adding value.”

PLTR is a Buy under $22 for a $100+ target.

PayPal Holdings (PYPL – $72.03) announced an expansion of its global strategic partnership with Fiserv (FI) to streamline how merchant clients of Fiserv enable PayPal, Venmo, and related services for their customers. Importantly, it provides these businesses with a simple connection point to PayPal’s Fastlane to accelerate guest checkout flows in the US. Adyen last week, Fiserv this week…PYPL is a Buy under $68 for a double in three years.

Small Tech

Enovix (ENVX – $8.15) has completed Site Acceptance Testing for its Fab-2 Agility line in Malaysia and started to produce the first batch of EX-1M samples, which have been sent to customers. The process of obtaining purchase orders has started, and the first order will skyrocket the stock as the shorts cover. Their thesis is that no one will order the battery, and they are unemotional about covering their short if their thesis is wrong.

At-The-Market stock sales in the June quarter gave Enovix a long enough cash runway to execute. ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

PagerDuty (PD – $18.61) reported July second quarter revenue up 7.8% from last year to $115.9 million, just under the $116.48 million consensus estimate. Pro forma earnings of 21¢ per share, their eighth consecutive quarter of pro forma profitability, beat the 17¢ estimate. But on the conference call (AUDIO HERE and SLIDES HERE and TRANSCRIPT HERE), management guided the October quarter to 6% to 8% year-over-year revenue growth to $115.5 million – $117.5 million, below the $120.25 estimate. They guided pro forma earnings to 16¢ to 17¢, also below the 18¢ consensus. That took the stock down 13% in Tuesday’s aftermarket but it recouped all that by today’s close.

For the full fiscal year, they reduced revenue guidance from $471.0 million – $477.0 million to $463.0 million – $467.0 million, a growth rate of 7% – 8% year-over-year, but below the $473.66 million consensus. They raised pro forma earnings guidance from 66¢-71¢ to 67¢-72¢. The Street was at 69¢.

Free and paid customers totaled more than 29,000 as of July 31, representing approximately 12% growth year-over-year. But total paid customers were down slightly to 15,044 compared to 15,146 a year ago. Customers with Annual Recurring Revenue (ARR) over $100,000 grew 6% to 820 compared to 773 a year ago. The number of customers with ARR greater than $500,000 grew over 20%. The crucial Dollar-Based Net Retention rate – how many dollars a customer spends this year compared to last year – was 106% as of July 31, compared to 114% a year ago.

On the call, CEO Jennifer Tejada said: “… these recent global outages and technology disruptions underscore the pivotal role our platform plates. When the world is down, customers rely on PagerDuty to identify issues, orchestrate, and increasingly automate the best possible response to quickly contain and reduce business impact

“The July 19 [CrowdStrike] outage tested our platform on a massive scale. The operations cloud rose to the occasion. We saw an over 1400% increase in incident workflows initiated on that day alone, and we maintained high availability, speed, and fidelity without incurring significant cost surges. Our reliability is a result of our history of investment in innovation, and it’s why companies trust us to deliver operational resilience in their most vulnerable moments.”

I continue to think incident response software will be as important to companies as cybersecurity software. PagerDuty is the market leader.

Click for larger graphic

With a huge market opportunity.

Click for larger graphic

They are almost at their pro forma target operating model. They just need to grow revenues without growing General & Administrative expenses for a bit.

Click for larger graphic

Click for larger graphic

PagerDuty had $33.3 million in free cash flow in the quarter and finished the period with $599.3 million in cash. PD is a Buy up to $30 for a 2- to 5-year hold as their digital operations management Software-As-A-Service gains market share.

Primary Risk: Digital operations management is a competitive area.

Rocket Lab USA (RKLB – $6.08) said its 53rd Electron launch, the second of five dedicated launches for the French company Kinéis, is scheduled to launch during a 14-day window that opens on September 17. This mission will launch just three months after Kinéis’ first launch with Rocket Lab.

Kinéis is backed by private and public investors including the French government’s space agency, CNES (Centre National d’Études Spatiales), and an international space-based solutions provider, CLS (Collecte Localisation Satellites), to improve global Internet of Things (IoT) connectivity. Kinéis’ constellation will connect any object anywhere in the world and guarantee the transmission of targeted and useful data to users, in near-real time, with low energy consumption. Once deployed, these technologies will allow Kinéis to expand across multiple industries and scale from 20,000 devices connected to millions. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

AbCellera Biologics (ABCL- $2.43) presented at the Wells Fargo Healthcare Conference (AUDIO HERE). Management said one evidence that they are the most advanced developer of antibodies is the quality of their partners – Lilly, Regeneron, Novartis, etc. Another is the many scientific presentations and journal articles on difficult-to-develop antibodies. AbCellera has over 100 agreements with downstream royalties. Over 40 of these are in active development with 14 already in the clinic.

They use about $30 million a quarter for operating expenses. Capital spending to build their manufacturing facility has been another $30 billion a quarter, but that ends at the end of this year. AbCelllera has over $700 million in cash plus $200 million in committed Canadian government funding – a cash runway well over three years. The total market cap of the company today is $730 million, so investors are valuing their 100 agreements and two internal drugs entering the clinic in the coming June quarter at minus $170 million. That’s nuts.

They will present again at the Cantor Global Healthcare Conference on September 17. Buy ABCL up to $6 for a long-term hold to $30 or more.

Primary Risk: Partnered and owned drugs fail in the clinic.

Clinical stage of lead product: Partnered: Various Owned: Preclinical

Probable time of next FDA approval: 2027-2028

Probable time of next financing: 2026-2027 or never

Akebia Therapeutics (AKBA- $1.38) presents at the Wells Fargo Healthcare Conference tomorrow and the H. C. Wainwright Global Investment Conference on September 9. Their detailed plan for the TDAPA launch of Vafseo in less than four months is a compelling story and they get better and better at telling it. Buy AKBA up to $2 for the Vafseo launches in the EU, UK, and (after TDAPA approval in December) the US.

Primary Risk: Vafseo doesn’t sell in the US.

Clinical stage of lead product: Approved

Probable time of next approval: TDAPA January

Probable time of next financing: Never

Compass Pathways (CMPS – $6.72) did a fireside chat at the Morgan Stanley Global Healthcare Conference (AUDIO HERE). They expect to be the first company to launch a classic psychedelic as a drug.

Regarding the Lykos MDNA turndown by the FDA, they pointed out that MDNA is a drug that works by having the patient talk, requiring interaction with a therapist to get the benefit. Lykos applied for MDNA-assisted therapy.

COMP360 is an inner-directed experience with little interaction with the person in the room providing psychological support if needed. Compass has carefully trained the Phase 3 trial therapists on how to prepare patients for the experience and what to say afterward.

The company will present at the H. C. Wainwright Global Investment Conference on September 10, and the Cantor Global Healthcare Conference on September 17. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 3

Probable time of first FDA approval: 2026

Probable time of next financing: Late 2025

Editas Medicine (EDIT – $3.49) presented at both the Morgan Stanley Global Healthcare Conference (AUDIO HERE and TRANSCRIPT HERE) and the Wells Fargo Healthcare Conference (AUDIO HERE).

As I expected, management focused on their in-house drugs that few biotech investors care about instead of potential new licenses for their core genetic editing Intellectual Property, which is where the big money will be. Every gene editing approval from the FDA will be followed by a huge licensing deal for Editas, and Wall Street finally will get it. The CFO said they expect licensing fees and low single-digit royalties on the whole industry and that’s why I want you to buy the stock.

They did emphasize their in vivo approach to gene editing to eliminate the costly, time-wasting, and sometimes dangerous need to extract cells, treat them, and reinfuse them. The company will present at the H. C. Wainwright Global Investment Conference on September 10 and the Cantor Global Healthcare Conference on September 17. EDIT is a Buy under $6 for a double in 12 months and a long-term hold to much higher prices.

Primary Risk: Other companies’ gene-sequencing drugs fail in the clinic.

Clinical stage of lead product: Partnered: Approved; Owned: Preclinical.

Probable time of next FDA approval: 2025

Probable time of next financing: 2026 or never

ScyNexis (SCYX – $1.34) presents on September 11 at the H. C. Wainwright Global Investment Conference and this is when they might announce the new manufacturer for ibrexafungerp. Buy SCYX under $2.50 for a first target price of $20 after ibrexafungerp is approved for hospital use and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: 2024

Probable time of next financing: Never

Inflation MegaShift

Gold ($2,545.80) is headed for $2,700 an ounce in 2025 according to Goldman Sachs. They issued a “long gold” recommendation and wrote: “Our preferred near-term long is gold. It remains our preferred hedge against geopolitical and financial risks, with added support from imminent Fed rate cuts and ongoing EM central bank buying.”

BofA analysts estimate gold has now surpassed the euro to become the world’s second-largest reserve asset, behind only the US dollar. Global physically-backed gold exchange-traded-funds have now seen inflows three months in a row as Western investors pile into gold, with North American activity outpacing Europe and Asia in July, according to the latest World Gold Council data. In the near term, though, gold has declined every September since 2017, according to Bloomberg data.

But so far, the fractal dimension shows gold stubbornly staying in an uptrend with plenty of energy left to push higher. $3,000, anybody?

Miners & Related

First Majestic (AG – $4.87) is acquiring Gatos Silver (GATO) for $970 million of stock. After the merger, existing Gatos shareholders will own approximately 38% of First Majestic shares on a fully-diluted basis. Gatos is a silver dominant producer with a 70% interest in the Los Gatos Joint Venture, which owns the producing Cerro Los Gatos (CLG) underground silver mine in Chihuahua, Mexico.

Click for larger graphic

Click for larger graphic

On the conference call (AUDIO HERE and SLIDES HERE), management said the combined company will have annual production of 30 million to 32 million ounces of silver-equivalent, including 15 million to 16 million ounces of silver at all-in sustaining costs of $18 to $20 per silver-equivalent ounce.

Gatos is expected to immediately contribute approximately $70 million of annual free cash flow to the combined company. Cerro Los Gatos adds over 250,000 acres of unencumbered land – no material royalties or streams – with significant exploration potential supported by a large base of mineral reserves. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $0.42) said that the Environmental Evaluation and Socioeconomic Analysis documents for the Grassy Mountain mine will be reviewed at a Project Coordinating Committee meeting on September 12. Following that meeting, final approval is expected at a state Technical Review Team meeting in early October. Approval allows the lead agencies to start writing draft permits, which PZG expect to receive in mid-2025. PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: 2023

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $56,003.99) hasn’t been able to get back over $60,000, although it should be a beneficiary of the Fed’s coming rate cut. We’re back near the July lows and should see new buyers soon.

Click for larger graphic

BTC-USD, ETH-USD, IBIT, and ETHA are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

iShares Bitcoin Trust (IBIT- $31.85) remains the cheapest and easiest way to buy bitcoin. IBIT is a Buy for the 2028, 2032, and 2036 halvings.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil and copper prices slid after Goldman Sachs warned of flagging Chinese commodity demand. They now expect copper prices to average $5.05 a pound in 2025, around one-third lower than their previous forecast of $7.50 a pound. Goldman analysts said Chinese data this summer suggested softening demand for commodities in general, and oil and copper in particular. They ended their longstanding recommendation to buy copper.

I think they threw in the towel at the bottom. UBS just raised Freeport-McMoRan (FCX) from Neutral to Buy with a $55 target price. They said the the medium-term fundamental outlook for copper 1s “compelling” and expect copper to average $4.75/lb in 2025. I expect it to average over $5.00.

Oil – $69.19

The Energy Information Administration reported a whopping 6.9 million barrel crude oil draw last week. Yet oil slipped below $70 as Libya resumed oil production in some southeastern fields as a result of pressure from the Biden Administration. The rumor is that OPEC+ will postpone their scheduled production increase in October.

Click for larger graphic h/t @zerohedge

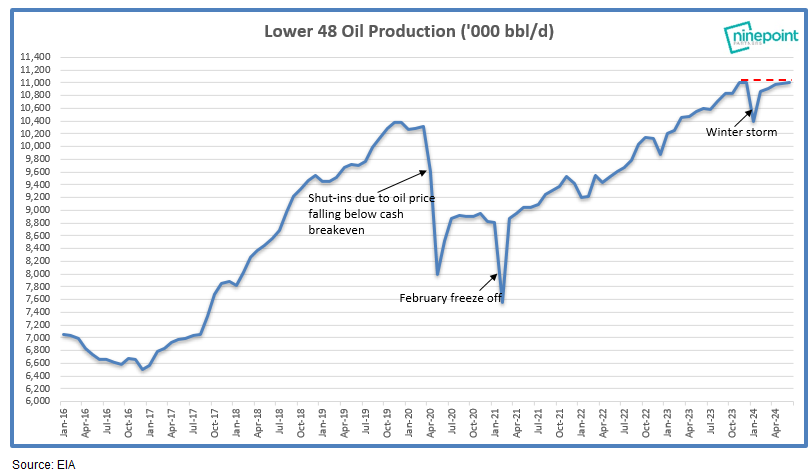

US shale production has been FLAT for the past eight months (!), yet any day oil is down we hear of “record high” and “surging” US production. I don’t get it. The era of US shale hyper growth obviously is over, and OPEC is in the driver’s seat going forward.

Click for larger graphic h/t @ericnuttall

Click for larger graphic h/t @ericnuttall

Also, Phillips 66 CEO Mark Lasher told Bloomberg there will be a refining shortage in 2025 because as much as 700,000 barrels a day of global refining capacity is expected to be taken out of the market. So, let’s recap:

Low OPEC+ crude exports

Global oil inventories low and declining

US oil production stalling

Refining capacity falling

Oil price up…wait… down?

The July 2026 Crude Oil Futures (CLN26.NYM – $65.18) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $35.97) is a Buy under $40 for a $100+ target.

Vermilion Energy (VET – $9.41) is a Buy under $11 for a target price of $24 or more.

Primary Risk: Oil prices fall.

Freeport McMoRan (FCX – $41.40) CEO Kathleen Quirk presented this afternoon at the Jefferies Industrial Conference (AUDIO HERE). She’s been with Freeport for 35 years, the last 20 as CFO, and recently became CEO.

She said their program to recover copper by leaching their miles of waste piles that contain 40 billion pounds of copper has hit the initial 200 million pounds per year target, and they are increasing their goal to 400 million pounds a year and, eventually, to 800 million pounds. They’re using implanted sensors, drones, data analytics, and directional drilling to go after it. The waste piles are like a new mine without the cost of finding it – and there aren’t many new big copper mines, anyway.

They also are targeting reducing US mining expenses because the savings fall right to the bottom line.

The Indonesian smelter is complete and being commissioned now. Freeport built it in return for an extension of their mining rights to at least 2041. In 2025, they will smelter and export 100% refined copper, which relieves them of a payment they have to make to the government on concentrate exports.

They are generating cash flow above their capital spending, so they return 50% of that to shareholders and put 50% on the balance sheet to fund future projects. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

* * * * *

Rev Up Your Engines

* * * * *

Your worried about private equity Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 9/5/24. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Corning (GLW – $41.37) – Buy under $33, target price $60

Gilead Sciences (GILD – $78.77) – Buy under $80, target price $120

Palantir (PLTR – $30.16) – Buy under $22, target price $100+

PayPal (PYPL – $72.03) – Buy under $68, target price $136

SoftBank (SFTBY – $27.54) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $8.15) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $56.99 – Buy under $60; 3- to 5-year hold

Fastly (FSLY – $5.91) – Buy under $14; 3- to 5-year hold to $80+

PagerDuty (PD – $18.61) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $7.31) – Buy under $10, target price $40

Rocket Lab (RKLB – $6.08) – Buy under $13, target price $30+

$20-for-$1 Biotech

AbCellera Biologics (ABCL – $2.43) – Buy under $6, target $30+

Akebia Biotherapeutics (AKBA – $1.38) – Buy under $2, target $20

Compass Pathways (CMPS – $6.72) – Buy under $20, hold a long time for a 10x return

Editas Medicines (EDIT – $3.49) – Buy under $6 for a double in 12 months and a long-term hold to much higher prices

Inovio (INO – $6.50) – Buy under $14, hold a long time

Medicenna (MDNAF – $1.79) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $1.34) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $21.46) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($29.12) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $29.50) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $33.61) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $23.22) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $31.09) – Buy under $30, target price $50

Coeur Mining (CDE – $5.49) – Buy under $5, target price $20

First Majestic Mining (AG – $4.87) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.42) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.53) – Buy under $10, target price $25

Sprott Inc. (SII – $36.56) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $56,003.99) – Buy

iShares Bitcoin Trust (IBIT – $31.85) – Buy

Ethereum (ETH-USD – $2,369.57) – Buy

iShares Ethereum Trust (ETHA- $17.92) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $65.18) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $38.59) – Buy under $40; $100+ target

Vermilion Energy (VET – $9.41) – Buy under $11; $24 target

EQT (EQT – $32.82) – Buy under $35; $70 first target

Energy Fuels (UUUU – $4.37) – Buy under $8; $30 target

Freeport McMoRan (FCX – $41.40) – Buy under $44; $65 target within two years

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Apple Computer (AAPL – $222.38) – Expect to move back to Buy under $175 for new iPhones

Meta (META – $516.86) – Expect to move back to Buy under $400

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2024

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First!

MM–you are way way way off base on SCYX and MDNAF, continuing to be a cheerleader and ignoring details of reality about the crapshoot odds of success for both of these companies. Your price targets are total fantasy with small odds of being proven to be correct. I spent hours today re-reading the clinical studies of both. I doubt you have read these studies, but you just rely on company promotions and biased interpretations of those grim studies.

SCYX–look at the publication pages. April 2023 FURI for serious intra-abdominal candida infections and candidemia (blood-borne candida). Headlines in the article claim 94% complete or partial response in 30 days. This was an open label study of patients getting Brexa who failed common anti-fungal treatments. Mean time to DEATH was 42 days. VERY SAD and unfortunate. Other publications are for urinary infections with candida resistant to other treatments. These patients are not deathly ill. Better results, but no description of long term cures. No wonder the company is doing studies on SCY 247 for serious infections. We all hope that 247 saves many more lives than Brexa, but studies will take many years. Meanwhile, the stock can tread water after a modest bump when they can begin MARIO. We’ll see how much Brexa is prescribed for VVC and serious infections, resulting in milestones/royalties of a speculative amount.

MDNAF–read my posts on the last board. The investigators are diligent, but they think they are God in re-creating superkines that correct the disordered immune system of cancer patients. FAT CHANCE. I have seen this intellectual hubris over my long medical career. The biggest example was the 2002 Women’s Health Initiative study of hormone replacement in menopausal women. Artificial patented drug hormone mimics were used in those studies, which did show that these drug versions of hormones raised cancer and heart attack risks. The headlines were damning to women who abruptly stopped their hormones. But the investigators perpetrated a con job on ignorant doctors who don’t know the chemical differences between drug hormones like medroxyprogesterone and the real thing, progesterone. These have totally different properties. Different structures interact with receptors differently. I could explain this to a 3 year old child who understands that you cannot put a round peg into a square hole. That child is smarter than most doctors and stock promotors who mislead people.

All subscribers should read Yahoo Message Boards and other sites for companies they are interested in. There are many educated people there.

For old timers – these 2 alone with AKBA are our last hope.

TGTX is my main hope. AKBA is speculative by comparison. I like Vafseo as a concept, but who knows how quickly the sales will appear under TDAPA?

John Miller–on TGTX, it deserves a big correction. Refer to the YMB posts of “Very” who discusses Roche’s likely approval of their BTK inhibitor, and the likely approval of Roche’s subQ version of Ocrevus. So Roche can have a nice portfolio of MS options vs the one trick pony of Briumvi for TGTX. I personally think that Briumvi will remain the drug of choice, but superior marketing by Roche can overcome deficiencies of their drugs. Q3 revenue won’t be reported until early Nov, so the stock is vulnerable until then. There is risk of a summer slowdown in revenue growth, so have cash ready. I suggest deploying some MDNAF profits into TGTX, hopefully at much lower prices.

Thanks Doc , I appreciate all your hard work and research on all those companies. Yes , I agree with you that they are oversold and due for a pullback/profit taking. My issue now is I don’t want to trigger another tax event for this year. It’s a situation where I can pay them now or pay them later. I have to ponder that, talk to my CPA and figure out what the best path forward is. I wasn’t planning on selling either of them for at least 3 years and who knows what the capital gains landscape will look like then or where the stock price will be. But, as you stated there is downside risk with that as well. Maybe I can sell 1/3 of my positions and carry the rest forward.

It has to feel good to have capital gains from the picks on this newsletter john,congrats it must feel good that you didn’t invest in stocks like arth.nvta.apto.vld.etc,most coming in with a 100 percent loss,I for one have enough losses to carry over for a lifetime,I feel good for you,I was a faithful believer in MM and his abilities,as for me not much of a fan anymore

Not all my picks are from this newsletter. And like you I also have losers. Not all NWI picks are losers , having said that. Case in point. I put 20k in Apple just before the split. (Ending up with some 300 shares) And sold this year at $299.00. Net profit about $40k. Then another pick from another newsletter blew up way beyond my wildest imagination. So much so I felt I had to sell that triggering another tax event. But , like JGMD said you only get $3000. per year to write off your losses. I absolutely HATE to pay extra taxes. Mainly when I think about all the crap that politicians recklessly spend our tax money on. Mostly , the money I have in TGTX and MDNAF is “house money” . Just got lucky this year. I know what you are saying. Been there, done that.

I know what you are saying about short vs long term capital gains. But when a stock like MDNAF is overbought, it is prudent to take at least some profits. MDNAF has some chance of being a long term winner, but it is gambling, so profits should be taken when you get lucky in the stock casino. Paying short term capital gains is a good problem to have. I have accumulated LOTS of losses mainly from NWI. I take the $3000 deduction every year. My long term blue chip portfolio has done well, but I hold it still. I am almost long term on my TGTX gains, but they will be used to offset the damn NWI losses.

You can do the math yourself. Don’t waste additional money discussing this with your CPA.

First Majestic looks like a persistent failure and the Gatos deal suspiciously engineered to cover strings of disasters. Look at todays slide show: three of six mines in “care and maintenance” mode. Management dialogue was pathetic and referred to the on site mining staff as if they were reporters for the WSJ. This stock has been a dog in a gold bull market…doubt it will turn around as it has been shunted aside by the market and this deal is suspect. Who else bid on it? Gatos was a minor micro cap. FIrst Majestic Track record of exploration and production after huge capex is not pretty.

blob:https://newworldinvestor.com/2ad8f2c0-f646-4587-b829-94a40c01b370

It is tempting to seek leverage to a rising gold price with mining stocks. But mining stocks are very risky businesses, especially juniors. Even majors like Newmont have risks. In the late stages of gold bull markets, gold itself outperforms miners because of high inflation impacting business economics. Even at this point in the relatively early gold bull market I favor gold itself for safety. I did OK with Rick Rule years ago, but have been inactive because of his high commissions. That has been foolish on my part, because he has been in the business for a long time. To be a good stock picker, knowledge and experience is needed.

BREXAFUNGERP FOR HOSPITAL USE?When ? I assume we must wait for SCY-247 for that to happen. Three years ?5 years?NEVER. ? Comon MM TELL US WHAT YOU KNOW TO THE TRUTH. ,!!

Brexa can be used for hospital cases. I don’t know when MARIO (for Brexa) will start, and how long it will take. I hope 247 will be better than Brexa. Is there any pre-clinical data to suggest that?

I believe there is good results as a combination drug. Qualify that by saying that the president Dr David Angula quoted the results at a conference last fall- I haven’t seen these studies to date

MARIO will use Brexa as a step-down from IV echinocandin type drugs. I guess we can say that this is a combination-type treatment. I have a hunch that this combo will be the best use for Brexa. IV drugs are expensive, so an oral drug like Brexa that can reduce the hospital time and maintain IV efficacy will be a great thing. Let’s search Pubmed.org to find info about that. How long will MARIO take? When results are available, that could give life to this languishing stock. If 247 works well, that could be the real payoff we have been waiting for.

zman,

I searched pubmed.org. Type–brexafemme. Ref 18 is recent and pertinent. Click Elsevier Open Access to get the full text free. Here’s an excerpt.

The FDA approved ibrexafungerp, the first new antifungal class in over 20 years, but also rezafungin, an echinocandin with unique pharmacological features and oteseconazole, an azole effective against some resistant isolates, and therefore added three new options in the clinical antifungal armamentarium. Likewise in Europe, ibrexafungerp, foxmanogepix and rezafungin received orphan designation status from the European Medicines Agency. Alongside the new drug olorofim, available as IV and oral formu- lations, amphotericin B formulations offer alternative and prom- ising options for patients with invasive fungal infections resistant or intolerant to existing therapies. All the discussed drugs not only show positive clinical results so far but also give new opportunities in outpatient settings and thus significantly simplify treatment.

My interpretation is that there is lots of competition from new antifungals. There is a new tetrazole called oteseconazole that is 40x more potent than fluconazole. Don’t believe stock promoter hype about Brexa being the ONLY new advancement in 20 years. F’IN BULLCRAP. The bottom line is that SCYX decided that they could only get an advantage with 247. Brexa won’t cut it–too much competition. They couldn’t make a profit on Brexa for VVC, so decided they should get money from GSK to survive for a number of years until they could get 247 approved.

Too much competition is a big reason why biotech investing is a crapshoot. Sell most bios on FDA approval and don’t wait for sales. TGTX is an exception, and I hope AKBA is another.

“Wednesday, September 11

13 Years Ago Today. Never Forget.”

Lose a decade?

“They use about $30 million a quarter for operating expenses. Capital spending to build their manufacturing facility has been another $30 billion a quarter, but that ends at the end of this year.”

$30 billion to build with less than $1 billion cash? “That’s nuts.”

Which company are you referring to?

ABCL, 2nd paragraph

Thanks.

Scotty is the GOAT !!!

Scotty who?

I think the guy in MM’s video, Rev up your engine.

More First Majestic….at the end of the sales pitch yesterday relating to the Gatos acquisition, management cut off any investor or analyst questions. Avoidance of questions is another red flag….I do not trust this management team and see little evidence is expertise in its highly demanding capital intensive mining industry.

Michael – Keevo is offering a beneficiary service for their wallet. I’m thinking of switching from Coinbase since I plan to hold my BC so that my daughter can inherit at a much higher cost basis (mine is $243/coin).

Keevo’s information is very confusing to me. Have you any opinions about it?

thanks so much for the help you give!

All newsletter subscribers – Im polling to ask what stock or asset, either NWI recommended or other, has the best chance for a double by end of yesr? All replies are very much appreciated

I said last month you could double your money in 2 months buying the NAT October 3.50 Call. I bought more this morning at 20 cents. I still expect a double in the next 12 trading days.

Yes I recall Chris but as I replied then I do not play with Calls, and the return – can you give me a quick lessin how and where to buy then sell? Thanks

Elementary knowledge of calls. You buy a call for company XXX. The call is the right to buy XXX before the expiration date. For NAT, the expiration date is a certain time in Oct (I forget which Fri of Oct it is) at a guaranteed price of $3.50. You can look up the current price for that call. Chris paid 20 cents on 9/6. Suppose the price of the stock at expiration is $4.00. The moment before expiration, the call is worth 50 cents, so he makes 30 cents on the 20 cent investment, or 150%. Sounds great, but the negative is that if the stock is still $3.50 on expiration his call is worth 0 and he takes a total loss. If the stock price is $3.70 at expiration, his call is worth 20 cents so he breaks even or losses just the commissions. If the stock rises before expiration, he can sell the call and make money. But this is a short term call, and the time value shrinks rapidly to zero at expiration, so timing is everything whether he will make money or not. Long term calls are known as LEAP’s. The time value of options is always decreasing, but the rate of decline is much smaller if you sell the option long before it expires. Many people consider speculative “cheap” stocks as equivalent to LEAP’s, but the risk is that these stocks take much longer to work out. This is the case with most speculative NWI stocks. The numerous outright near 100% losses are obvious, but even the few successful stocks like TGTX take much longer than most people think to pay off. Things like AKBA are an unknown situation. The potential is great, but nobody knows how long it will take for Vafseo to generate big sales. This is a situation where it would be stupid to buy any call option, but if you wait several years, that’s where the payoff might be.

With that information, you can understand why nobody can rationally give you answers to your questions about which stock is most likely to give you a double in 1-2 years. Don’t even ask those questions–there are no honest answers.

Thanks JGMD for the explanation. Of course I realize theres no guaranteed stock double in 5 months but onviously there are solid opportunities and catalysts that increase the possibility or probability

Also, whats happening on 9/24, 12 trading days from now? I use ETrade, can I buy calls on that platform? Appreciate the guidance

9/25 NAT goes ex-div. Its quarterly dividends have been running about $0.12 per quarter, which is over 13% annual yield if you can buy the stock under $3.60. Even at $4, that’s a 12% yield. Unlikely as it may seem given recent price action, I believe NAT’s share price will rise going into 9/25 as investors pile in to grab that dividend. Come 9/25 the price will likely begin to fall again but with support at 3.50, the decline should be more muted than in the past after ex- date.

A good way to follow tanker rates is fearnpulse.com , Also, NAT announced that they have far fewer tankers than a year ago operating on fixed rate contracts and more in the lucrative spot market.

Anyone looked at NVDY? I first bought around $27 in May and although share price is now $20.88, I have received monthly dividends of $2.56, $2.47, $1.25 and (next Monday) $1.35 for a total of $7.63 in dividends. So I paid about $27 for an asset now valued just under $21, but have received about $7.63 in divvies. so in less than 4 months my $27 is down $6.12 but I’ve collected 7.63 for a net gain of $1.51 or 5.6%. Not an indecent gain for 3.5 months. I’ll continue to hold and to re-evaluate.

Beware of the dividend fallacy. A day after a dividend is “paid”, the stock price is reduced by the value of the dividend. The total value is the stock price plus the dividend, so there is no change in total value. The dividend is not actually paid–it is just an accounting gimmick used to fool investors that they are getting something extra. No, they get nothing extra. Another problem is that dividends are taxed at higher ordinary rates, but long term capital gain tax rates are much lower. Buffett was wise to prefer stocks that have little or no dividends. Of course, if you like the underlying stock as a business, don’t worry about divvies or not.

With all the immigrants eating our pets, what would be a good stock to buy to keep our pets out of harm’s way?

Shorting DJT has been VERY lucrative.

DJT down over 12% today. My asymmetric bet on a Trump victory, NAK, is down 1.4% today. I think it’s time to take profits after last night’s performance. She made him look almost as bad as Biden looked.

I didn’t nail the top of DJT but I’m covering today, It is a worthless company but shorts can get squeezed for no reason.

Pet protection: look at MRU (Mantraps R Us) for kennel countermeasures.

Another that I’ve been considering is Vermin Surprise. The outfit installs dye packets into gerbils and hamsters. A small explosive ignites and coats the unholy (and hungry) non-citizen with bright yellow dye when a fork is stuck into the little critter.

What was the highlight of the debate?

For me it was Trump’s response to Kamala’s statement that world leaders are laughing at Trump.

Trump: “Viktor Orbán said, he said, ‘the most respected, most feared person is Donald Trump. We had no problems when Trump was president.”

The best endorsement he could get is from the biggest fascist in 21st century? Really?

Here’s a balanced view of the debate from one of the few economists who understands free market economics and proper political policy, Mark Skousen. His recent important contribution to economics is the recognition that output is only 30-40% from the consumer, with more from earlier stages of production at raw materials and producer levels. The govt has adopted his Gross Output indicator. GDP is only about the consumer, and is NOT 70% of the economy. MM, take note.

Are you better off than you were four years ago?” — Ronald Reagan, 1980

If you have seen the “Reagan” movie currently in theaters, one of the highlights is his debate with Jimmy Carter when he asked the question, “Are you better off than you were four years ago?”

Most Americans answered “no” and voted Reagan into office. It was a smart decision, as Reaganomics led America into a new era of prosperity and a bull market in stocks and bonds that lasted 40 years.

The same question came up in the beginning of Tuesday night’s presidential debate between Donald Trump and Kamala Harris.

The ABC moderator asked Harris, “How do you respond to the question, ‘Are Americans better off than they were four years ago?’”

When she dodged the question, Trump had the chance to pounce and say, “She didn’t answer the question, and the reason is because everyone knows they are not better off!”

He could have talked about the renewed bout of inflation, the slowing job market, threatened regulations on household appliances and new foreign wars. But he didn’t! Instead, he went on a rant about his own grievances.

Maybe he didn’t want to answer the question because in some ways we ARE better off than four years ago. Remember, in 2020, we were still in the midst of the Covid pandemic, when businesses were shut down, our First Amendment rights to free speech and freedom of assembly and religion were curtailed and we were all forced to wear masks.

I figured Vice President Harris had the advantage at the very beginning when she went over to his side and shook his hand. He wasn’t planning to meet her in the middle. It was a bad omen for Trump. The old angry Trump came out throughout the lengthy debate.Top 20 Living Economist Shares the Largest Position in His Personal IRA

Investing legend Dr. Mark Skousen recently gave a talk to a small group in the heart of Washington, D.C. In it, he revealed the cornerstone of his retirement plan — and the one investment that helped make him a millionaire. Click here to watch Dr. Skousen’s presentation — and learn about “the best way to become a millionaire in America.”Immigration, Protectionism and Other Debate Topics

It wasn’t just Harris dodging the questions; it was Trump, too. When he was asked why he didn’t support the immigration bill in Congress earlier this year, he had a great opportunity to tell the American people why it was a bad bill. For example, it allowed up to 5,000 illegal immigrants per week to still come into the country. That’s 260,000 a year.

Trump constantly exaggerated the facts. Trump’s economy was not the best in the history of the country.

Joe Biden is not the worst president ever.

He will not be able to end the Ukraine and Middle East wars before taking office if he wins.

The nation is not going to “hell,” at least not soon. Inflation is coming down, gas prices are falling, corporate profits are high and a recession has been avoided so far.

If the world was doomed like Trump believes, why would the stock market be at an all-time high?

We do know where Trump stands on economic issues. We don’t know about Kamala Harris. She is a chameleon who has flip-flopped on energy policy, taxes and crime. She says her values have not changed — and that’s the scary part. Her values are socialistic if not Marxist, promising equal outcomes (what she calls “equity”) by taxing the successful and expanding the welfare state.

Trump’s economic policies are pretty good overall — tax cuts and deregulation are good for economic growth — but his doubling down on his protectionist tariffs is a disaster.

Despite Trump’s claim, it will increase prices for many items.

Worse, he’s now threatening to double the tariff on all imports to 20%.

How is that going to “Make America Great Again?” Free trade and globalization are two key factors in a rising standard of living. It will undoubtedly mean Americans will need to change jobs, but it will mean better jobs. Oh, ye of little faith!

And when will our leaders deal with the real problems facing America, such as the growing national debt? Watch it grow: U.S. National Debt Clock : Real Time (usdebtclock.org).This A.I. Spots Trades Like a Spy, See it Live

If you want to trade smarter, not harder, and be prepared for this week’s markets, you won’t want to miss this.

Join us live as we reveal which stocks and commodities might explode in the next few days and how to conquer volatility and avoid losses.

Anticipating market changes is crucial, and nothing is more rewarding to us than helping you steer clear of potential losses.

Secure your spot now!Who Won the Presidential Debate? It Was a Landslide!

Most people think that Harris surprised everyone and beat Trump in Tuesday night’s presidential debate, thanks in part to the bias of the ABC two moderators.

Election betting odds now have Harris winning the White House in November, 52% to 47%. But the betting odds are notoriously volatile.

Whoever wins is going to have a dramatic impact on your pocketbook and your investments. Get ready!

Two Important Investment Conferences After the November Elections

I will be involved in two investment conferences right after the critical November elections:

EconoSummit, Nov. 9-10, Ahern Hotel, Las Vegas: This will be the first investment conference after the all-important Nov. 5 elections. I’ll be speaking on the impact of the elections on your portfolio. Other speakers include political experts John Fund and top economist Sean Flynn, with more to be announced soon. This ticket, valued at $499, is FREE if you sign up for next year’s FreedomFest, set for June (not July!) 11-14, 2025, at the Palm Springs Convention Center in California. To sign up go to http://www.freedomfest.com. After you sign up, you will receive a special code to get a free ticket to EconoSummit. For more information, go to http://www.econosummit.com.

Update on the 50th Anniversary New Orleans Conference

New Orleans 50th Anniversary Investment Conference, Nov. 20-23: I’m excited about New Orleans, host of the grand-daddy of hard-money conferences. It’s after the crucial November elections, so this is a great opportunity to adjust your portfolio. I see that my long-time friend Alex Green, chief investment strategist at the Oxford Club, will be joining me. I’ve been speaking every year at the famous “gold bug” New Orleans conference since 1977, and will give a unique talk, “My Life-Changing Highlights in New Orleans.” Other speakers include James Grant, Gary Alexander, Robert Prechter, Mary Anne and Pamela Aden and Brien Lundin. (See picture above of all the other speakers.) It will be memorable. Sign up now before the early bird discount ends this month! To register, click here.

Good Investing, AEIOU,

Mark Skousen Can Elephants Dance? Big Blue’s TurnaroundBy Mark Skousen

Can Elephants Dance? Big Blue’s TurnaroundBy Mark Skousen

Doti-Spogli Endowed Chair of Free Enterprise, Chapman University

Wikipedia

Newsletter and trading services

Personal website

FreedomFest

Editor, Forecasts & Strategies

“My leadership style is to get people to fear staying in place, to fear not changing.” — Lou Gerstner Jr.

I have a long history with International Business Machines (IBM), known as Big Blue.

Their executives contacted me in the early 1980s after reading my Bantam paperback, “High Finance on a Low Budget.” It offered easy ways to start investing with as little as $100. I did a nationwide tour with the book and sold a quarter of a million copies. (The highlight was appearing on the news show “LA Today” with host Regis Philbin.)

When I arrived at headquarters in Armonk, New York, I was told that IBM was having problems with their employees depending too much on the company’s generous medical, retirement and other benefit programs. They asked me to create a personal finance course to help thousands of IBM employees to save, invest, avoid wasteful spending and unnecessary credit card debt and become more financially independent.

After several months of hard work, my team and I came up with a personal finance course on CD rom. IBM executives were pleased with our training program but insisted that we make it clear in the first slide that IBM has a policy of permanent employment. Once an IBM employee, always an IBM employee.

Years later, I realized that’s what IBM’s problem was. There was little or no incentive to work hard and be creative. Employees were guaranteed lifetime employment, and didn’t need to take risks. They were too dependent on IBM’s generous welfare program.

Despite our efforts, IBM continued to face serious troubles and threatened bankruptcy in the early 1990s.

Their board hired an outsider, Lou Gerstner Jr., as CEO, who immediately downsized the company, laid off thousands of workers and revised its basic business model. He took a lot of risks, but as he said, “Watch the turtle. He only moves forward by sticking his neck out.”

It was only then that IBM returned to its glory years — by incentivizing its employees and appealing to new commercial customers. Gerstner proved that “Elephants Can Dance,” the title of his memoir.

It took a while, but today, a new dynamic Big Blue is making waves, and the stock is now hitting new highs. It is facing stiff competition from Amazon Web Services and Microsoft Azure, but the outlook for IBM as an AI leader is positive. Big Blue is back!About Mark Skousen, Ph.D.:

Mark Skousen is an investment advisor, professional economist, university professor, author of more than 20 books, and founder of the annual FreedomFest conference. For the past 40+ years, Dr. Skousen has been investment director of the award-winning newsletter, Forecasts & Strategies. He also serves as investment director of four trading services: TNT Trader, Five Star Trader, Low Priced-Stock Trader, and Fast Money Alert.About Us:

Mark Skousen is an investment advisor, professional economist, university professor, author of more than 20 books, and founder of the annual FreedomFest conference. For the past 40+ years, Dr. Skousen has been investment director of the award-winning newsletter, Forecasts & Strategies. He also serves as investment director of four trading services: TNT Trader, Five Star Trader, Low Priced-Stock Trader, and Fast Money Alert.About Us:

Eagle Financial Publications is located in Rosslyn, VA. – Blocks from the Capitol. Our products have been helping investors build their wealth for several decades. Whether you’re a long-term investor or short-term trader, you’ll find the right strategy for you, including how to earn more steady income to spend now, preserve and grow your capital to enjoy later, and whatever other investment goals you have.

Visit Our Websites:

To ensure future delivery of Eagle Financial Publications emails please add financial@info2.eaglefinancialpublications.com to your address book or contact list.

Legal Disclaimer: Any and all communications from Eagle Products, LLC. employees should not be considered advice on finances. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed as personalized advice on finances.

Salem Media Group – Eagle Financial Publications | 1735 N Lynn St, Suite 500, Arlington, VA 22209-2016

New World Investor for 9.12.24 is posted. Added UUUU to Long-Term Top Buys.