Dear New World Investor:

September quarter real gross domestic product (GDP) rose at a 2.6% annualized rate, double the Blue Chip consensus for +1.3% and half a percent under the latest Atlanta Fed’s GDPNow model forecast for +3.1%.

Click for larger graphic

Click for larger graphic

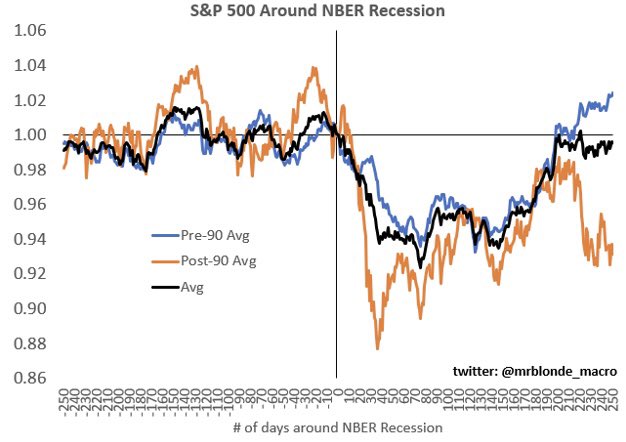

So are we not in a recession? Alas, we are. Although it’s mild so far. Domestic demand was the weakest in two years and residential investment contracted for the sixth straight quarter. Consumer spending, which accounts for more than two-thirds of US economic activity, slowed to a 1.4% rate from the June quarter’s 2.0% pace.

I expect tomorrow’s personal consumption expenditures index and September quarter labor cost numbers to carry more weight with the Fed ahead of their meeting next week. The Fed’s designated leaker of trial balloons, Nick Timiraos of The Wall Street Journal, said the Fed is going to raise the funds rate by another 75 basis points (0.75 percentage points) and then debate the “pace of tightening,” signaling a desire “both to slow down the pace of increases soon and to stop raising rates early next year.” That sounds like a Fed pivot in the offing, presumably because their rearview mirror already sees financial Armageddon signals.

Click for larger graphic

Click for larger graphic

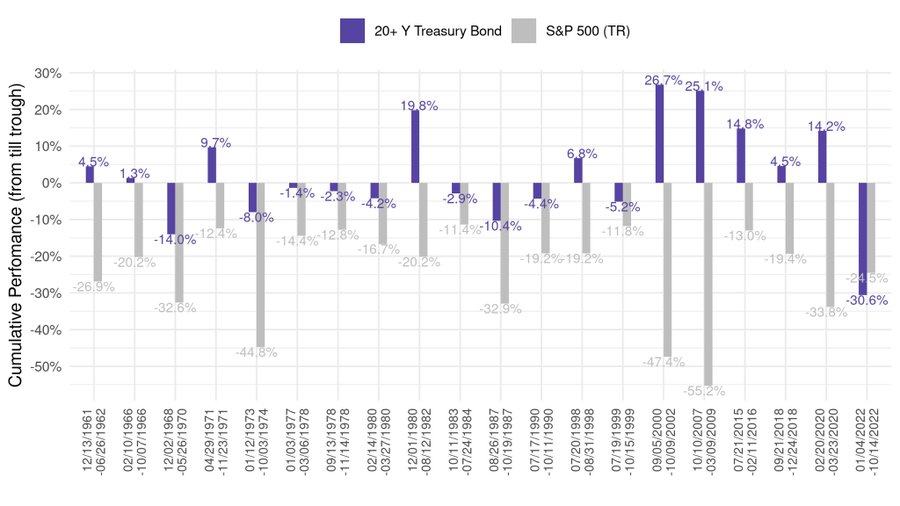

The 10-year US Treasury bond is on pace for its worst year in history with a loss of 19.5%. It’s not stocks that are down over 30% this year, it’s long-duration Treasurys. The 30-year Treasury sold in May 2020 with a 1.25% coupon just traded at 50¢ on the dollar. This is the risk-off asset. Never in history, in an extreme drawdown for stocks, have Treasurys, THE risk-off asset, gone down more than stocks – until now.

Click for larger graphic

Click for larger graphic

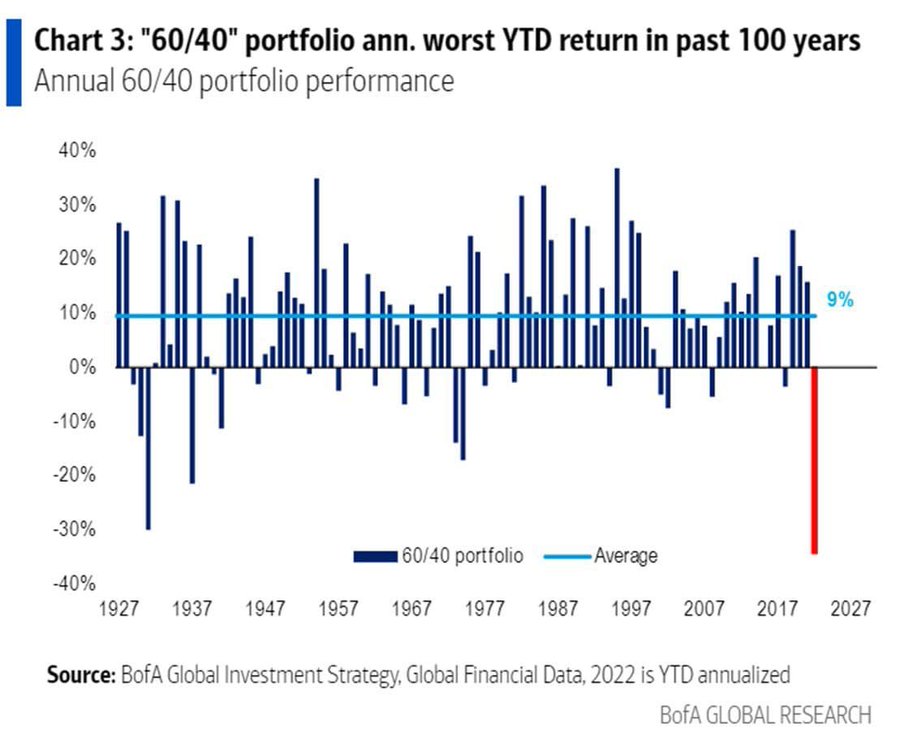

As a result, so much for Target Funds helping investors with their retirement.

Click for larger graphic

Click for larger graphic

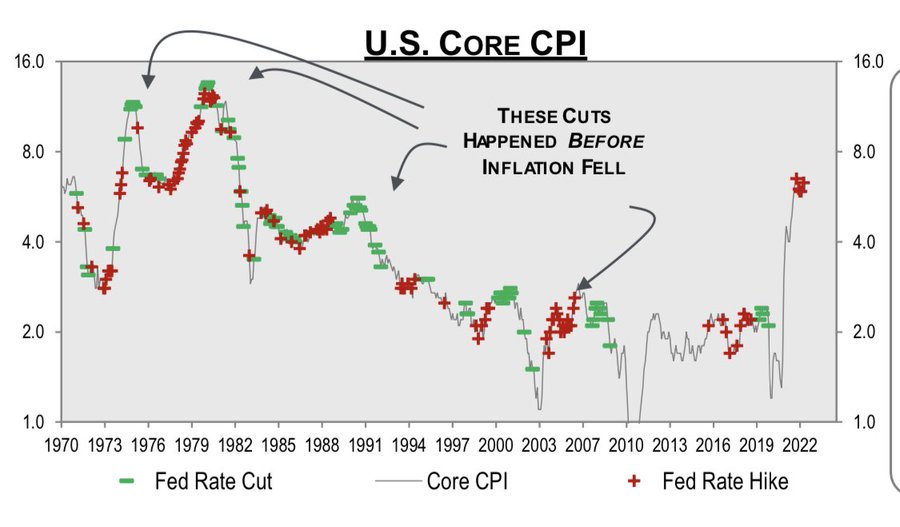

The Fed has always cut before the core consumer price index peaks. Why? Because core inflation is so lagging that something else breaks before it rolls over. Maybe it’s different this time, but that’s their history.

Click for larger graphic

Click for larger graphic

Weaker digital advertising revenues hit Google and Meta this week, dragging down the Nasdaq Composite and the overall market. I know this feels pretty bad, but do you remember the March 2020 lows? It really felt bad then, right as things were very cheap. I think we’re about there again. So far in the September quarter, about 70% of S&P companies have beaten their revenue estimates, which is above both the five- and ten-year averages. As my friend Kieth Fitz-Gerald wrote: “People are pricing the markets like they’re going out of business – that’s almost always a sign of better days ahead. And an opportunity!”

And don’t forget – only eight trading days until the midterm elections drag is over.

Click for larger graphic

Click for larger graphic

The S&P 500 added 3.9% since last Thursday and briefly regained its 50-day moving average. The Index is down 20.1% year-to-date.

Click for larger graphic

Click for larger graphic

The Nasdaq Composite gained only 1.7% due to several tech earnings shortfalls. It is down 31.1% for the year. The small-cap Russell 2000 rose 3.7% and is down 19.6% in 2022.

The fractal dimension is even more consolidated and ready to support a multi-month move in either direction. We’re headed into a period of seasonal strength unless Fed Chairman Grinch steals the Santa Claus rally.

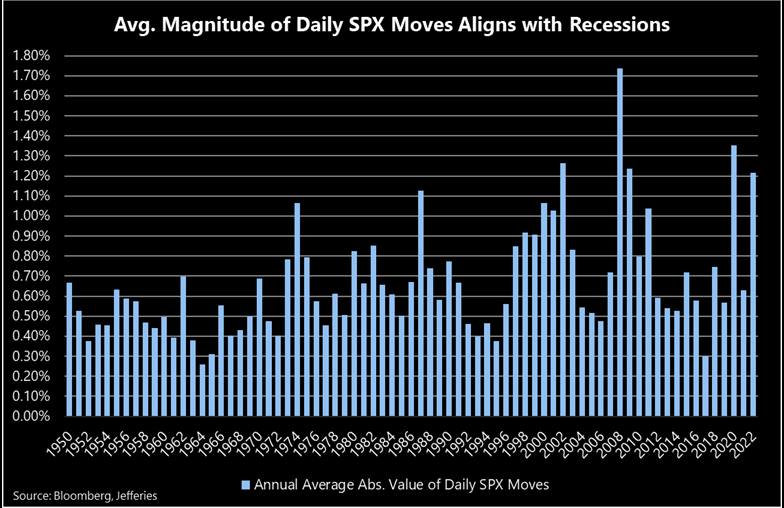

With massive swings the hallmark of 2022, Jefferies took a look this week at how the average absolute magnitude of daily SPX moves this year stacked up versus history. As they show below, the moves are pretty substantial, even when comparing them to the last ~70 years of trading. Since 1950, the average open-close distance of 1.22% observed so far in 2022 is good enough for fourth place. Jefferies highlights that this is likely part of the bottoming process, as other high volatility years tend to see strong performance in the subsequent years… particularly in what would be 2023.

Click for larger graphic

Click for larger graphic

Top 5

Changes this week: Dropped AAPL to make room for TGTX

Near-Term – chronological order

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

INO Inovio – INO-4800 China trial results and VGX-3100 HPV Phase 3 results by yearend

TGTX TG Therapeutics – FDA approval on December 28

META Meta – Bounce from overdone selloff

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

GRPH Graphite Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

VLD Velo3D – Return manufacturing to the US

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, October 28

Personal Consumption Expenditures Index – 8:30am – Expected: +0.5% MoM, +5.2% YoY

Monday, October 31

Happy Halloween!

Tuesday, November 1

APTO – Aptose Biosciences – 5:00pm – Earnings conference call

Wednesday, November 2

Fed meeting – 2:00pm – 75 basis point increase expected

FSLY – Fastly – 4:30pm – Earnings conference call

Thursday, November 3

CMPS – Compass Pathways – 8:00am – Earnings conference call

AKBA – Akebia – 10:00am – American Society of Nephrology Kidney Week poster presentation

AKBA – Akebia – 4:30pm – American Society of Nephrology Kidney Week second poster presentation

Friday, November 4

AG – First Majestic – Through 11/5 – International Precious Metals & Commodities Show

October payrolls – 8:30am – +200K expected; September was +263K

MDNA – Medicenna – 8:30am – Earnings conference call

AGNPF – Algernon Pharmaceuticals – 1:00pm – Business Session Keynote at the Wonderland Psychedelic Conference

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations are typically very low. At the same time, Initial Public Offering valuations had moved very high. We were seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors make 5x to 10x in a reasonable, three- to four-year period if they buy at those valuations. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Algernon Pharmaceuticals (AGNPF – $2.08) entered an unusual investigator-initiated clinical trial agreement with Yale Professor Deepak Cyril D’Souza to investigate multiple intravenous doses of DMT for the treatment of depression. Treating depression is not one of Algernon’s programs right now.

Algernon provides the DMT for the study and will jointly own intellectual property around the clinical use of DMT arising from the study with the option to negotiate licenses to the intellectual property developed jointly or solely by Yale. They will get data from the study that may be relevant to their DMT stroke research program.

Algernon’s strategy seems to be to try much as they can at a very low cost to see if they get lucky. They have patents pending on novel forms of DMT that potentially could be used across a broad range of diseases. I doubt this study will turn into anything useful, but AGNPF is a Hold for the Phase 2b IPF/chronic cough results.

Primary Risk: Ifenprodil fails in clinical trials.

Clinical stage of lead product: Phase 2/3

Probable time of first FDA approval: 2023

Probable time of next financing: 2022

Aptose Biosciences (APTO – $0.47) will report September quarter results next Tuesday. They should lose about 12¢ a share, but the stock will move based on clinical trial progress and any new results. APTO is a Buy under $2.50 for a $30 target in a buyout.

Primary Risk: Either drug fails in clinical trials.

Clinical stage of lead product: Phase 1a

Probable time of first FDA approval: 2025

Probable time of next financing: Mid- to late-2023

Compass Pathways (CMPS – $10.41) will report September quarter results next Thursday. They’ll lose about 65¢ a share. Any news on the impending Phase 3 trial could move the stock. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2024

Probable time of next financing: Mid-2023

Invitae (NVTA – $2.28) partnered with AstraZeneca and the Cholangiocarcinoma Foundation to use Invitae’s natural history data in a retrospective and prospective study of patients diagnosed with cholangiocarcinoma, a rare bile duct cancer. This partnership will enable sharing of high-quality, patient-consented data from the patient community of the Cholangiocarcinoma Foundation, a leading patient advocacy group whose mission is to find a cure and improve the quality of life for those with cholangiocarcinoma. AstraZeneca will do the drug development. Buy NVTA under $10 for a first target of $50 and eventually $100+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

Medicenna (MDNA – $0.71) will report September quarter results next Friday. They should lose about five cents a share. The stock will jump if we get any real news on the effort to find a partner for MDNA55. Buy MDNA under $3 for a first target of $20, then maybe $40.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Entering Phase 3

Probable time of first FDA approval: 2023

Probable time of next financing: March 2024

ScyNexis (SCYX – $2.43) presented excellent cumulative interim outcomes and all-cause mortality data from their Phase 3 trial in hospitalized patients with refractory candidiasis treated with oral ibrexafungerp. Cumulative interim analysis of outcomes by fungal disease type showed 82.3% positive clinical outcomes in patients treated with ibrexafungerp. All-cause mortality analysis showed 94.6% survival 30 days post-therapy in patients with invasive candidiasis or candidemia who were treated with ibrexafungerp. Those are excellent numbers. Buy SCYX under $2 for a first target price of $20 now that Brexafemme is approved and a buyout at $50.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: late-2022

Probable time of next financing: second half of 2023 or newer

Biotech MegaShift

TG Therapeutics (TGTX – $5.31) presented some exploratory analyses from their Phase 3 trials evaluating ublituximab in patients with relapsing forms of multiple sclerosis. Five posters presented at the 2022 European Committee for Treatment and Research in Multiple Sclerosis (ECTRIMS) annual meeting included Disability Changes in the Absence of Relapse and Disease Outcomes With Ublituximab in Treatment-Naive Participants. I expect FDA approval on December 28 and I added TG to the near-term Top Buys. Buy TGTX under $7 for a target price in a buyout of $25 or more after the MS drug is approved.

Primary Risk: FDA turns the MS drug down.

Clinical stage of lead product: Filed for approval.

Probable time of next FDA approval: September 28, 2022

Probable time of next financing: March 2023 quarter

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $144.80) reported September fourth quarter record revenues up 8.1% from last year to $90.15 billion, beating the $88.77 billion estimate. Earnings hit $1.29 per share just above the $1.27 estimate.

Product revenues rose 9.0% to $70.96 billion versus $65.08 billion in last year’s September quarter in spite of foreign exchange headwinds. iPhone revenue hit $42.63 billion, up 9.7% from last year’s $38.87 billion. So much for rumors of soft iPhone sales.

Mac revenue rose 25.4% to $11.51 billion from $9.18. But iPad revenue of $7.17 billion fell 13.1% from $8.25 billion last year. Wearables, homes, and accessories of $9.65 billion were up 9.8% from $8.79 billion. The very important Service revenue, which includes subscriptions to products such as Apple TV+, iCloud storage plans, and Apple Music, hit a record $19.19 billion, up 5.0% from. $18.27 billion in the September 2021 quarter. Earlier this week, the company said it would raise the price of its media service subscriptions from $1 to $3 a month.

On the conference call (AUDIO HERE), management said they generated over $24 billion in operating cash flow and returned over $29 billion to shareholders during the quarter. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Corning (GLW – $32.11) reported September quarter revenues up 2.8% from last year to $3.7 billion with pro forma earnings of 41¢ a share, both in line with consensus estimates. But their Display Technologies (TV) sales declined 22% sequentially and 28% year over year. Volume declined in line with the market while glass price was flat. The lower volume dropped their gross profit margin to 36.1% and their operating margin to 16.9%.

On the conference call (INFOGRAPHIC HERE and TRANSCRIPT HERE), management was cautious on the current quarter and guided for revenues of $3.45 billion to $3.65 billion with 41¢ to 47¢ earrings. The Street was at $3.74 billion and 55¢, so the stock was hit for an 8.2% decline intraday on Tuesday before bouncing back to close down just 2.0%.

Management said the flat year-over-year results were in spite of display panel maker utilization hitting its lowest level since 2008; smartphone, tablet, and notebook retail unit sales declining significantly; and automotive production remaining constrained. They offset those factors with 16% year-over-year growth in Optical Communications and 33% year-over-year growth in Hemlock and Emerging Growth Businesses driven by the solar market.

Corning is a big, diversified business and a technology leader in all its segments. GLW is a Buy under $33 for the 5G cellular buildout, followed by the smartphone upgrade to use 5G services. My target is $60 in 2023 .

Gilead Sciences (GILD – $70.20) reported September quarter revenues down 5.1% from last year but up 14% from the June quarter to $7.04 billion, well above the consensus estimate for $6.13 billion. Sales excluding Veklury (remdesivir) for COVID-19 grew 11% year-over-year to $6.1 billion.

Pro forma earnings of $1.90 clobbered the $1.43 estimate. On the conference call (AUDIO HERE and SLIDES HERE), management said HIV sales grew 7% from last year, oncology grew 79% YoY and 10% sequentially. They increased their 2022 guidance again:

Click for larger graphic

Click for larger graphic

GILD is a Long-Term Buy under $70 for a first target of $100.

Meta Platforms (META – $97.94) reported September quarter revenue down 4.5% year-over-year to $27.71 billion, which beat the consensus estimate for $27.4 billion. But that was the only thing they beat, and the stock crashed 24.6% today.

Earnings per share of $1.64 badly missed the consensus estimate of $1.86. Facebook’s daily active users were 1.98 billion on average, an increase of 3% year-over-year. Monthly active users were 2.96 billion, an increase of 2% year-over-year.

Ad impressions increased by 17% year-over-year but the average price per ad decreased by 18% year-over-year as advertisers adjusted to the lower response rates due to Apple’s privacy updates. On the conference call (SLIDES HERE and TRANSCRIPTS HERE and HERE), they discussed the “problem” (if you are a short-term thinker or an MBA with no operating experience) or “opportunity” (if you are a long-term thinker or Mark Zuckerberg): the expense of becoming a leader in the metaverse. They said: “We expect 2022 total expenses to be in the range of $85-87 billion, updated from our prior outlook of $85-88 billion…We anticipate our full-year 2023 total expenses will be in the range of $96-101 billion.”

They also gave cautious December quarter revenue guidance in a range of $30.0-32.5 billion, below the $32.21 billion consensus. That assumes foreign currency will be an approximately 7% headwind to year-over-year total revenue growth in the fourth quarter, based on current exchange rates.

Look, I get it. Zuckerberg does not come across as a friendly, fun-loving guy. Almost no one has been able to take a company from a dorm room startup to a $100+ billion colossus, and many people are jealous. Reporting expenses up 19% when revenues are down 4% because you see a huge opportunity in the metaverse is going to upset the desk jockeys on Wall Street. Most of them cut estimates, cut target prices, and often downgraded the stock today. The same thing is going to happen to Amazon tomorrow.

But I am with Cestrian Capital Research, which wrote a SeekingAlpha article today: Meta Platforms Is Doomed – Doomed We Tell You! It begins:

“The Market Gods have handed a beating to the Artist Formerly Known As Facebook all year.

* * The stock recently plunged below its COVID crisis level and revisited its 2018 lows.

* * Things might be that bad at Meta Platforms, but they probably aren’t.

* * On sale at 7.5x trailing twelve-month unlevered pretax cash flow, with huge pressure on Zuckerberg to perform, we think the pain trade is up.

* * We rate META at Accumulate and own the stock in staff personal accounts.”

I agree. And guess who benefits the most when the government bans Tik Tok? I’m cutting my buy limit to $150 and keeping the $400 target, but not until 2024. META is a Buy under $150 for a $400 target in 2024.

Other Tech

Fastly (FSLY – $8.50) will report September quarter results next Wednesday. The consensus is looking for $103.46 million in revenues and a loss of 17¢ per share. FSLY is a Buy up to $20 for a 2- to 5-year hold to $80+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,667.40) has been stuck at this level since mid-September as this amazing consolidation continues. There is enough fractal energy to easily reach new all-time highs as we head into the seasonally strong period for precious metals.

Miners & Related

Paramount Gold Nevada (PZG – $0.32) submitted its updated Plan of Operations to the Bureau of Land Management for the Grassy Mountain gold mine. The Plan integrates all the BLM comments related to their previous submission and includes additional supporting documents the BLM requested.

The BLM will take 30 days to review the Plan for completeness, and then file a Notice of Intent in the Federal Register about the upcoming Environmental Impact Statement. The BLM has selected HDR Inc. to complete the EIS in about 12 months. Then the BLM issues a Record of Decision.

Paramount already has the County’s Conditional Use Permit. Once they get BLM approval, they only need the State of Oregon permit to open the mine in 2023. PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: Second half of 2022

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $20,355.57) moved back up over $20,000 after the United Kingdom voted in favor of bitcoin and crypto becoming financial instruments. With investors leery of anything tech-related, anything interest rate-related, and anything that might come under selling pressure due to yearend hedge fund redemptions, a risk-on rally over the next few months should be very strong for bitcoin and ethereum. The true believers have cornered the float while crypto has muddled through multiple large bankruptcies and yet it still won’t drop. That’s a sign of underlying strength.

BofA analysts pointed out that at the start of September, the relationship between bitcoin and gold once again turned positive, and in early October the correlation reached its highest point in a year. That suggests it is being used as a safe-haven asset and a hedge against wider market uncertainty.

Click for larger graphic

Click for larger graphic

BTC-USD, ETH-USD, GBTC and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

The Grayscale Bitcoin Trust (GBTC- $12.15) is selling at a 34.8% discount to net asset value – it’s like buying bitcoin for $13,266 today when it’s selling for $20,355. Not a bad deal.

And Grayscale is suing the SEC for denying conversion of GBTC to a spot bitcoin exchange-traded fund. They are arguing that the agency has illegally applied stricter standards to spot ETFs than to futures ETS — the latter which the agency has approved.

And they’re right. SEC Chairman Gensler is under pressure to hold back the crypto tsunami until the government can roll out its Central Bank Digital Currency that will let them track and control every penny you earn or spend. I expect the SEC to cave and approve the conversion by the end of 2023, which will give you an immediate 53% profit as GBTC goes to net asset value, even if bitcoin goes nowhere. GBTC is a Buy under net asset value.

Primary Risk:Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Ethereum (ETH-USD on Yahoo – $1,519.61) has started to move up now that the network became a proof-of-stake blockchain through The Merge upgrade last month. ETH-USD is a Buy.

Primary Risk: Bitcoin extensions outperform Ethereum.

Grayscale Ethereum Trust (ETHE- $10.46) is selling at a 30.0% discount to net asset value – it’s like buying ethereum for $1,063 today when it’s selling for $1,519. ETHE is a Buy under net asset value.

Primary Risk:Ethereum falls due to over-regulation or is surpassed by another cryptocurrency.

International & Other Recommendations

It is important to hold some non-US assets, especially in China. China’s top leader, Xi Jinping, secured a groundbreaking third leadership term last Sunday and introduced a new Politburo Standing Committee stacked with loyalists. Financial markets were rattled on expectations that Xi’s policy agenda of bolstering national security and the party’s political security would shift the world’s second-largest economy toward a more state-led model that could make maintaining political ties and the party’s ideology a higher priority than achieving economic growth and policy reform. But the Big Dogs can only stay in power if the people are happy, and the people are not happy unless the economy is growing rapidly and they are moving up a class or two.

Xi’s stupid zero-COVID policy, which has resulted in sweeping lockdowns in an effort to contain the virus, will come to an end when cooler heads prioritize economic growth again. Meanwhile, Chinese stocks are dirt cheap with Hong Kong’s Hang Seng Index at a new 13-year low. Here are four easy ways to put some money to work in China:

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $22.78) is a Buy under $38 for a $66 target in 12 to 18 months.

KraneShares Bosera MSCI China A Share Fund (KBA – $27.92) is a Buy under $40 for a three- to five-year hold.

Morgan Stanley China A-Share Closed-End Fund (CAF – $12.54) is a Buy under $18 for a three- to five-year hold.

KraneShares CSI China Internet Exchange-Traded Fund (KWEB – $19.83) is a Buy under $40 for a double over the next three years.

Primary Risk of all four of these: China falls into a recession.

Acreage Holdings (ACRDF – $1.21) got a takeover bid from Canopy Growth. The good news is that our strategy of buying Acreage as a cheap way into Canopy and holding Canopy for an acquisition by Constellation Brands is working.

The bad news is that they sold us down the river on the price. We were supposed to get a minimum of $6.41, but they rewrote the deal to make it 0.45 shares of Canopy for each share of ACRDF. The conference call VIDEO IS HERE.

Yes, it is a 17% premium to where ACRDF was trading and, yes, we still want to hold Canopy for the inevitable Constellation Brands takeover. But it still sucks and I wouldn’t be surprised if they get sued and have to raise the price. The deal won’t close until the second half of 2023. Either way, ACRDF is a buy under $2 for the Canopy Growth merger and beyond.

Primary Risk: Constellation Brands does not acquire Canopy Growth.

Oil – $88.30

Oil hit its highest level in two weeks as the Biden Administration said they intend to repurchase crude oil for the Strategic Petroleum Reserve when prices are at or below about $67-$72 per barrel. Good luck with that, now that OPEC+ is back in control of oil prices.

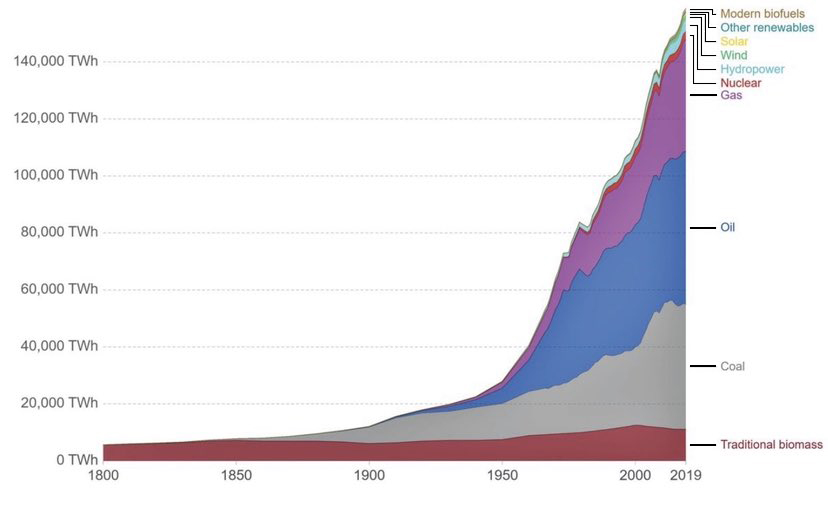

The biggest energy players reporting so far this week, from integrated oil companies to big refiners, have said demand remains healthy despite the economic slowdown. Forecasts have come down – a lot – but oil demand is not contracting. In fact, we’ve never transitioned from any energy source ever. We’ve only consumed more of every energy source.

Click for larger graphic

Click for larger graphic

Got OIL? The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $31.97) is a Buy under $36 for an $80+ target.

* * * * *

Click for larger graphic

Click for larger graphic

* * * * *

Your realizing the CDC has a problem Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Aptose Biosciences (APTO – $0.47) – Buy under $2.50, ultimate target $30

Bellerophon Therapeutics (BLPH – $1.19) – Buy under $5, first target $30, then $100

Compass Pathways (CMPS – $10.41) – Buy under $20, hold a long time for a 10x return

Graphite Bio (GRPH – $3.61) – Buy under $9, hold a long time

Inovio (INO – $2.06) – Buy under $7, hold a long time

Invitae (NVTA – $2.28) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.71) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $2.430) – Buy under $3, target price $20, then $50

Other Biotech

TG Therapeutics (TGTX – $5.31) – Buy under $7, target price $25+

Tech Dominators

Apple Computer (AAPL – $144.80) – Buy under $150 for new iPhones

Corning (GLW – $32.11) – Buy under $33, target price $60

Gilead Sciences (GILD – $70.20) – Buy under $70, target price $100

Meta (META – $97.94) – Buy under $250, target price $400

SoftBank (SFTBY – $20.55) – Buy under $25, target price $50

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $41.12) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $8.50) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $25.22) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $6.53) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.79) – Buy under $13, target price $30+

Velo3D (VLD – $3.74) – Buy under $6, target price $50

Inflation

A Short-Sale or REO House – ($447,000) – Buy while fixed mortgage rates are low

Bag of Junk Silver – ($19.57) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $21.69) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $24.40) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $15.81) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $25.41) – Buy under $30, target price $50

Coeur Mining (CDE – $3.92) – Buy under $5, target price $20

First Majestic Mining (AG – $8.47) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.32) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $5.02) – Buy under $10, target price $25

Sprott Inc. (SII – $34.91) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $20,355.57) – Buy

Grayscale Bitcoin Trust (GBTC – $12.15) – Buy

Ethereum (ETH-USD – $1,513.81) – Buy

Grayscale Ethereum Trust (ETHE – $10.46) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $22.78) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $27.92) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.54) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $19.83) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $1.21) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.26) – Buy under $1.30; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55; $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $31.971) – Buy under $36; $80+ target

Energy Fuels (UUUU – $7.18) – Buy under $8; $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $2.08) – Hold for IPF/chronic cough trial

Akebia Biotherapeutics (AKBA – $0.27) – Hold for FDA meeting

Arch Therapeutics (ARTH – $0.05) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

First.

2nd

tTird. With the longest delay of the ages now at 1:30 AM here in the East. Does this forecast investors waiting for an election or merely free candy nextweek?

The stock market is down (S&P) is down 24 percent,(September) Nasdaq is more. but Joe says (today) the economy is looking good! Go figure. The big “R” word (recession) is slipping under the sheets . Companies are laying off and putting a freeze on hiring. Ad revenue’s are hurting Meta’s numbers. Amazon’s forward guidance is going to be lacking and with the exception of energy companies, earnings aren’t looking good for the rest of the quarter. Putin says he won’t use nuke’s. (which really means he is planning on doing the opposite) . Voting is going to be high on the minds of the public. IMO. Just sayin

Biden is a buffoon, and so is the Nancy and Chuck clown show, November red wave is coming

And this red wave will cure inflation? Not a single candidate has stated HOW they will fix things, they simply point at the dems.

The US is full of simpletons.

Michael, the definition of inflation is too much money chasing too few goods, so the first step the republicans will take is to stop the dem’s massive money flooding spending to reduce the “too much money” side of the equation. The other first step they will take is to return to energy independence which will bring the cost of everything down (gas, heat, goods because most packaging is oil based). Next question?

Sure, sounds easy. What programs are you willing to cut? Will the GOP force big oil to actually produce more oil? Nothing is stopping them.

This inflation hot potato will on the GOP in a few weeks. It will be interesting to see how they can’t/won’t be able to fix it.

what programs? How about starting with not funding 87,000 new IRS field agents.

Drop in the bucket. How about cutting Social Security and Medicare? It’s on the GOP agenda.

Billions is a drop in the bucket? What a typical democratic reckless spending response. Cutting SS and Medicare is more democratic propaganda,

People vote with their pocketbooks. And right now the pocketbook is hurting. Gas is $7.00 a gallon in California, and over$5.00 a gallon in Oregon and Washington. The personal savings rate dipped to 3.1 percent. Meaning consumers are exhausting any discretionary income to keep pace with the rising cost of living . Young people are priced out of buying a house because they don’t have $80,000 for a down payment or $3000. for a monthly payment at 7 percent interest. And the FED is now forced to raise interest rates another 75 basis points next week!! Rents are also crazy expensive along with soaring food costs. Amazon’s numbers are getting bad because consumers can’t buy “stuff” when all their money is going into the gas tank, paying outrageous mortgage or rent payments and putting food on the table.

And how does the GOP fix these global problems? It’s easy to point fingers but we’ll see how they handle things. Seems like their #1 agenda is a revenge impeachment on Biden.

its also an easy out to call it a global problem and so take away any domestic responsibility or solutions – can you stop watching MSNBC for a minute, can you?

I’m not sure how many times I have to say this but I don’t watch cable news. Do you watch Fox? Be honest.

I’ll also say this for the 100th time. Oil is GLOBALLY priced. The US president has NOTHING to do with the price of oil

Jesus.

It’s globally priced based on supply, and by not tapping the huge source domestically we are limiting global supply thus driving the price up, do you really not follow that simple fact, wow!!

You act like an authority on everything yet you don’t understand the basics of supply and pricing, shocking

And you don’t understand the multiple economic benefits of being energy independent and sourcing energy needs from US companies rather than sending trillions to terrorist countries? That’s worthy of a “Cmon man!!”

… when you stop watching Fox. (Actually I also watch CNN, ABC, NBC and occasionally PBS, and read the Washington Post. What’s your crosscheck, OAN?)

Do you get economic and political understanding from just news sources? I believe yes. Reality–news sources are for people who don’t understand basic principles of economics which are timeless. FACT–socialist political economics are inferior to free market economies for nearly everyone except the special interests which are well connected. Study Austrian economics, founded by Ludwig von Mises, or even Milton Friedman.

No , that’s the last thing we want. If Joe gets impeached , we end up with K. Harris (and if she gets the boot the line up behind her gets even less desirable).

. That was Joe’s thinking when he picked her. He wrote the book on “How to stay in office “ Just pick a running mate who is more incompetent than you are.

MM – on SCYX, when is the PDUFA date for ibrexafungerp? You state probable date of next FDA approval is late 2022, and given the excellent interim results, is this a strong buy in anticipation of approval?

PDUFA November 30. I thought the abandonment of Brexafemme could hurt the stock for the rest of the year due to tax loss selling, but it looks like it’s bottomed. Certainly a Buy here.

In an 8/18/22 comment after SCYX released Q2 earnings I said in part:

Based on the very disappointing VVC sales ramp the likelihood of SCYX reaching $400+ million in VVC/rVVC revenues seems extremely unlikely. 2022 revenues will not even hit 2% of that forecast.

Revenues clearly aren’t ramping quickly enough to get them to cash flow positive before additional financing is needed in late 2023/early 2024 as may have been thought earlier.

It’s likely Merck, or its women’s health spinoff Organon, would be much more capable of optimizing the VVC/rVVC market potential. SCYX would benefit by selling off the VVC/rVVC indications & using the money to fund the remaining indications.

I now agree with ROGERinSEATTLE’s comment from last week that the SCYX announcement to out-license Brexafemme puts them in play to be acquired. If companies are evaluating & looking to take over half the business, why not take the whole enchilada. They’re going to get the Brexafemme portion for a screaming deal due to SCYX’s failure in that market & the new data posted today on the fantastic ibrexafungerp numbers make that highly desirable. I think it’s more likely SCYX is bought then they out-license Brexafemme.

Agree mostly, but the problem is that at present, Brexa is a money loser. This may be due to poor marketing by SCYX, but I said long ago that the trials for VVC showed only a modest advantage for Brexa over cheap fluconazole (F). A small % of F failures will do well with Brexa, and no amount of marketing by a Big Pharma will overcome that. So I believe that SCYX buyout won’t happen any time soon. We will need to see excellent large phase 3 trial results for serious hospital infections, where the drug can be priced at a much higher level, and the insurance company will pay. That won’t happen until 2024. The stock is at best a hold.

MM – on ETHE, what is the benefit of the 30% discount to etherium if there is no plan for an etherium ETF like bitcoin?

I’m sure they will convert to an ETF as soon as they can to erase the discount.

MM my understanding is the only petitions out there for conversion to ETFs are for Bitcoin only, not ethereum, can you clarify?

Correct. But once the bitcoin EF is approved, I expect a quick filing and approval for ETHE.

Hi MM,

Thanks for the new RR.

Could you please comment on INO’s press release yesterday and update your opinion and recommendation, particularly concerning the company giving up on INO-4800 and whether that would affect its short term “Top 5” status.

Thanks.

INOVIO Provides Update on COVID-19 Heterologous Booster Vaccine Candidate, INO-4800 (yahoo.com)

INO was one of MM’s biggest mistakes (one of MANY). He correctly pointed out that MRNA had the inside track back in 2020 but stuck to his guns with INO.

MRNA is a terrific buy. Cancer vaccine in the works.

I recommended INO for their DNA medicines. Messenger RNA is an unpredictable technology that’s always had side effects. I doubt an mRNA cancer vaccine can get through regular clinical trials.

Merck disagrees. We’ll see. You’ve been wrong before and so have I.

Hasn’t Messenger RNA had the largest clinical trial ever over the past 2 years? I’m not reading anything about unpredictable technology and side effects appear to be minimal.

Maybe you have alternative data?

INO-4800 is still one of only two vaccines in the WHO Solidarity Trials. I expect it will be the most effective one, but what that will mean for INO’s finances is unclear. The VGX-3100 HPV Phase 3 results are coming by yearend, so INO still is a short-term buy.

Off 98% from the highs. Not sure about this one.

Ok, Thanks.

Will the VGX-3100 HPV Phase 3 results due by yearend really move the stock much given the FDA now wants them to do one or two additional trials given the results weren’t strong enough to support a BLA?

What’s the likelihood of TikTok being banned in the U.S.?

Zero and it’s killing Meta.

Very likely. The new Congress will be for it and Biden has been tougher on China than Trump.

Well, MM, at least someone else thinks so:

https://seekingalpha.com/article/4551043-corning-stock-remains-high-quality-bargain?mailingid=29543143&messageid=2800&serial=29543143.10882&utm_campaign=rta-stock-article&utm_medium=email&utm_source=seeking_alpha&utm_term=29543143.10882

“In determining the pace of future (rate) increases, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.”

Buckle up.

What’s happening with APTO ?? Up 30 percent today?

A very small number of patients among a small number of trial patients, responded to one of their drugs. But read Carol J’s posts on the poor outlook. CEO Rice is like TN, milking the company to pay salaries with VERY little in the way of results, all at a snail’s pace. Ignore MM’s cheerleading for Rice.

The new Radar Report for 11.3.22 is posted.