Dear New World Investor:

Yield curve inversions, where shorter-dated Treasury notes yield more than longer-dated notes or bonds, are both feared and poorly understood by investors. In the past, whenever the yield on the 2-year note has risen above the yield on the 10-year note, there’s been a recession within 12 to 18 months. An inverted yield curve not only predicts but directly contributes to sharp economic slowdowns. As refinancing credit short-term becomes prohibitively expensive while markets already price in poor expectations for long-term growth, the economic engine actually slows down and a vicious circle unfolds.

But the effect on the stock market is not so straightforward. The Fed may cut interest rates as soon as they see a slowdown developing. After the most recent five inversions, stocks fell twice and rose three times.

Click for larger graphic

Click for larger graphic

The Deutsche Bank table below shows the details of every Fed hiking cycle over the last 70 years with the time to a recession, yield curve shape, and inflation at the first hike. Deutsche Bank has ordered this by the length of time from the first hike to a recession, to demonstrate that the quickest recessions following hikes were associated with an inverted curve by the time the Fed stopped hiking.

On average, it takes around three years from the first Fed hike to recession. However, all but one of the recessions in less than 37 months (essentially three years) occurred when the 2s10s curve inverted before the hiking cycle ended. With all the recessions that started later than that, none of them had an inverted curve when the hiking cycle ended.

In fact, hiking cycles that ended with the curve in positive territory saw the next recession hit 53 months on average after the first rate hike, whereas the next recession for hiking cycles that ended with an inverted curve started on average in 23 months, just under two years. All these cycles eventually saw an inverted curve but this happened after the Fed stopped hiking. As a reminder, none of the US recessions in the last 70 years have occurred until the 2s10s has inverted. On average it takes 12-18 months from inversion to recession. Then again, the Fed has never before started a rate hiking cycle when inflation was already 7.9%.

Click for larger graphic

Click for larger graphic

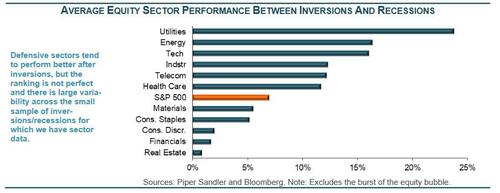

But, as a new Piper Sandler study finds, stocks tend to do quite well in the window between yield-curves inverting and the onset of the actual recessions.

Click for larger graphic

Click for larger graphic

The 2/10-year curves have inverted seven times since 1977. A year later the markets were higher an average of 11.8%, rose six of the seven times, and fell only once, after the February 2000 inversion.

Interestingly, Fed Chairman Powell doesn’t watch inversion in 2s/10s or anything like that. He has said he watches the first 18 months of the curve and does react to that. So far, that’s a non-issue. Powell said: “Frankly, there’s good research by staff in the Federal Reserve system that really says to look at the short – the first 18 months – of the yield curve. That’s really what has 100% of the explanatory power of the yield curve.”

Click for larger graphic

Click for larger graphic

Clearly, the odds of a recession are higher because economic growth from the reopening is slowing just as the Fed is talking about larger interest rate increases. March quarter real GDP growth will be mediocre but positive, so June quarter growth will be important.

Market Outlook

The S&P 500 added only 0.2% since last Thursday and is up 7.2% above where it stood before Russia first moved into Ukraine on February 24 and 357 points since the March 14 low, right before the Fed hiked rates. The Index has exited correction territory and has averaged almost 14% over the year following exiting a correction.

Click for larger graphic

The S&P 500 hasn’t had an up day of less than 1% since February 16. That is nine up days in a row of at least a 1% gain or more. The last two times it did this were June 2009 and April 2020 – not the worst times to be bullish. The Index is still down 4.9% year-to-date.

The Nasdaq Composite also gained only 0.2%, but for the first time since January 3 and 4 there were more new highs than lows on the Naz. That’s only happened three times since November 16. It is down 9.1% for the year. The small-cap Russell 2000 dropped 0.3% and is down 7.8% in 2022.

Ed Yardeni said: “It’s still a bull market, and a new S&P 500 high is likely to come much sooner than we expected…For this year, the downside might have occurred on March 8 around 4200, while the upside might be at 5000. For next year, our range is 5000-6000.”

With a peace deal in sight for the Ukraine war – Ukraine can join the EU but not NATO, won’t develop nuclear weapons or host foreign military bases or troops, and Russia gets Donbas – the stock market can refocus on GDP growth, inflation, and the Fed.

The fractal dimension stalled at a high level of consolidation. The next trend should get underway soon.

Top 5

Changes this week: Dropped near-term on ATRS and (unfortunately) AKBA because they got their FDA decisions

Near-Term – chronological order

OIL iPath Pure Beta Crude Oil Exchange-Traded Note – crude should rise quickly

GBTC Grayscale Bitcoin Trust – Bitcoin is coming out of one of its periodic sharp drops

FB Meta – Bounce from overdone selloff

Long-Term – alphabetical order

ARTH Arch Therapeutics – High-value wound care and hemostat for surgery

CWBR CohBar – mitochondria drugs and life extension

GRPH Graphic Bio – second-generation genetic editing

NVTA Invitae – the winner-take-most of genetic testing

FB Meta – a leader in the metaverse

Virus Update

Worldometers now shows 487,719,794 worldwide confirmed infections, of which 428,908,542 have run their course. Of those, 422,743,848 recovered and 6,164,694 died – a new low case fatality rate of 1.4%.

In the US, there have been 81,742,831 confirmed infections, of which 66,079,833 have run their course. Of those, 65,073,352 recovered and 1,006,481 died, matching last week’s case fatality rate of 1.5%. But the moving average case fatality rate is still over 2.0%.

Click for larger graphic

Click for larger graphic

Daily cases have fallen under 28,000.

Click for larger graphic

Click for larger graphic

Hospitalizations are near the lowest numbers since the pandemic started. My local hospital has stopped updating its COVID-19 page because there are so few admissions.

Click for larger graphic

Click for larger graphic

Daily deaths have fallen under 600.

Click for larger graphic

Click for larger graphic

Pretty much everyone who is going to get vaccinated has done it.

Click for larger graphic

Coming Events

All times below are ET, and most of the presentations and slides are archived on the companies’ websites so you can listen to them.

Friday, April 1

March payrolls – 8:30am – +490,000 expected

Wednesday, April 6

ACRDF – Acreage Holdings – 3:30pm – BTIG Global Cannabis Conference fireside chat

The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks, and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these 12 speculative biotechs might be a good way to start.

The market capitalizations of these recommendations typically are very low. At the same time, Initial Public Offering valuations have moved very high. We are seeing $750 million to $900 million valuations for a good preclinical/Phase 1 IPO, and even $300 million to $500 million for mediocre Phase 1s. I don’t see how investors make 5x to 10x in a reasonable, three- to four-year period. How many biotechs have moved north of $10 billion within 5 years after pricing an IPO in the $700 million to $900 million range? Hardly any. Buying these out of favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a much better strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Antares Pharma (ATRS – $4.10) got FDA approval for Tolando, their oral formulation of testosterone, as I predicted. CEO Bob Apple said: “We have recently expanded our commercial organization to 108 sales representatives and expect to leverage our relationships with urologists and endocrinologists to drive adoption of Tlando. We look forward to launching Tlando commercially, which will provide a complementary treatment option to patients and clinicians, in the second quarter of this year.” ATRS is a Strong Buy up to $5 for a $10 target price based on Xyosted and EpiPen sales, and $50 in three to five years, as they and their partners introduce numerous new products.

Primary Risk: Xyosted prescriptions stop growing or other products don’t sell well.

Clinical stage of lead product: Approved

Probable time of first FDA approval: Approved

Probable time of next financing: Not needed

CohBar (CWBR – $0.31) reported a December quarter GAAP loss of four cents a share, a penny better than Wall Street’s expectations. They are looking for a partner to take CB4211 forward, which I think will be hard to find and not likely to bring in much upfront cash. They will drop their oncology programs to focus on CB5138-3, their idiopathic pulmonary fibrosis (IPF) drug that they expect to get into human trials in the second half of 2023. The delay is caused by a need to develop improved formulations to decrease the risk of local skin reactions in humans, and also increase the drug’s systemic exposure to get better efficacy in IPF patients.

Ken Cundy, the Chief Scientific Officer, resigned effective today. He is replaced by an SVP: Research who was the VP: Biology for CohBar for six years and an acting Chief Medical Officer with a good background in IPF.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management made it clear that CohBar is back to being a preclinical company, which adds a couple of years to the drug approval pathway.

Click for larger graphic

Click for larger graphic

CohBar finished today with a minuscule market capitalization of $27.4 million. They finished the year with $26.2 million in cash, which should carry them into the second half of 2023, and no debt. I still think this is a dramatically different technology that will work, and that they have an amazing patent position. But due to the delays, I’m moving the stock to a Hold until we get closer to human trials of CB5138-3. CWBR is a very long-term Hold.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 1

Probable time of first FDA approval: 2025

Probable time of next financing: March 2022 quarter

Invitae (NVTA – $7.97) pulled together several internal projects to launch Invitae Digital Health, a connected digital health platform providing actionable genomic insights for patients and clinicians. It integrates important health data throughout each patient’s lifetime and is scalable to cover the entire world’s population – which has been Invitae’s goal all along. Patients control their own data.

The company pointed out that there were 19.3 million new cases of cancer worldwide in 2020, 420 million cases of cardiovascular disease, 8 million children born with a serious genetic condition each year worldwide, and 99% of people with genetic variations that can impact drug response. The potential impact of genetics on mainstream healthcare is profound. It’s a winner-take-most market because whoever has the largest database has the broadest, most accurate data. Buy NVTA under $50 for a first target of $100 and eventually $200+ when they become the Amazon of genetic testing.

Primary Risk: A competitor starts taking significant market share.

Clinical stage of lead product: NM

Probable time of first FDA approval: NM

Probable time of next financing: Not needed

ScyNexis (SCYX – $3.91) reported only $597,000 million in revenue for the December quarter versus the consensus expectation for $1.16 million. But here’s the weird thing: the Symphony data had indicated 4,150 prescriptions in the quarter, but the company reported only 3,674. Since the July launch through December 31, Symphony has total prescriptions at 5,239 but the company only reported “more than 4,600.”

In the September quarter, Brexa sales of $516,000 divided by the 1,006 prescriptions gives revenue per prescription of $512 per prescription. But dividing December quarter net sales by the company’s number of prescriptions gives revenue per prescription of just $162.50. I believe the drug lists for $495, but the company records revenue upon the sale of inventory to the wholesaler, minus any discounts from patient assistance programs like their co-pay card. They expect their net selling price to improve in the March quarter over the course of the year.

On the conference call (SLIDES HERE and TRANSCRIPT HERE), management said: “With Brexafemme now approved and the launch for the treatment of VVC, also known as vaginal yeast infections, we plan to expand its labeling by end of this year to prevent recurrent VVC, an indication for which nothing is yet approved. Moreover, we expect to get ibrexafungerp approved for invasive candidiasis in 2024. All these indications when taken together will create a franchise with the potential to generate $700 million to $800 million a year in net sales in the U.S. alone.”

Click for larger graphic

Click for larger graphic

By the end of the year, they had Brexa coverage for more than 81 million commercially insured lives, more than 48% of commercial lives. That is ahead of their goal.

The positive results of the recurrent VVC trial of 300 milligrams of Brexa twice a day for one day a month for six months were statistically significant. The company will submit a supplemental New Drug Application (sNDA) for a label expansion in the June quarter and get approval by yearend. That trial also showed that more than 70% of patients who failed three days of fluconazole therapy – 3x the approved dose – successfully achieved a significant reduction or elimination of signs and symptoms after a one-day course of Brexa.

There are many catalysts for the stock coming:

Click for larger graphic

Click for larger graphic

What is a biotech company worth that already has an FDA-approved drug on the market, based on a novel therapeutic compound, and is in Phase III trials which are likely to end in approval of a therapy for systemic fungal infections—a widespread and burgeoning disease threat? And, in spite of those assets and prospects, the company is valued at less than $115 million—a fraction of what is routinely sunk into the development of drugs with smaller addressable markets, and only speculative prospects for approval? I think it is worth way, way more.

Click for larger graphic

Click for larger graphic

They finished the quarter with $104.5 million in cash and are funded into the June 2023 quarter. Buy SCYX under $24 for a first target price of $54 now that Brexafemme is approved and a buyout at $170.

Primary Risk: Ibrexafungerp fails to sell.

Clinical stage of lead product: Approved

Probable time of next FDA approval: mid-2022

Probable time of next financing: 2023 or never

Biotech MegaShift

Akebia Therapeutics (AKBA- $0.72) did not get the approval for vadadustat for dialysis patients that I predicted, and the stock collapsed. On the conference call (AUDIO HERE), the company essentially said they were blindsided, because the safety data in dialysis patients was clear, presented at medical conferences, and published in the New England Journal of Medicine. It showed no safety difference between the drug and darbepoetin, the comparator.

During the Q&A, the company said the rate of thrombotic events was the same but the FDA looked at the number of events and there were more patients treated with the drug. They will meet with the FDA to discuss this.

Regarding the “risk of drug-induced liver injury,” the FDA looked only at the incidence in vadadustat and ignored the identical incidence in darbepoetin, contrary to their stated policy. This should have been handled through labeling, not a CRL.

The company may appeal the decision. At this point, they don’t know if they’ll do another clinical trial. They will be cutting expenses and focus on growing Auryxia.

The FDA had no questions about the efficacy of vadadustat. I still think the drug eventually will get approval, but I have to move the stock to a Hold until they have the results of the forthcoming FDA meeting. Hold AKBA.

Primary Risk: Vadadustat not approvable without another clinical trial.

Clinical stage of lead product: Complete Response Letter

Probable time of next FDA approval:Unknown

Probable time of next financing: June quarter of 2022

Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $174.61) won the Best Picture Oscar for Coda, becoming the first streaming company to win that award. The stock was up 11 straight sessions through Monday and briefly erased its losses for the year to date. But a rumor citing the ever-reliable “unidentified people” says Apple plans to reduce the output of the new iPhone SEs by about 20% in the June quarter compared with its original plan because of signs that consumer electronics demand is being hurt by the war in Ukraine and rising inflation. The company supposedly told multiple suppliers it was lowering production orders by two million to three million units for the quarter.

I don’t care and you shouldn’t either. These “unidentified people” have identified about eight of the last three Apple production cuts. AAPL is a Hold for new iPhone rollouts and augmented/virtual reality products.

Other Tech

Fastly (FSLY – $17.38) acquired Fanout, a platform that makes it easy to build and scale real-time and streaming application programming interfaces (APIs) at the computing edge, such as live chat support, ecommerce, video streaming, gaming, collaborative editing, and more. FSLY is a Buy up to $45 for a 2- to 5-year hold to $150+ as Compute@Edge drives customer acquisition and revenue growth.

Primary Risk:Content and applications delivery networks are a competitive area.

Probable time of next financing: None needed

QuickLogic (QUIK – $5.50) won a $1.5 million eFPGA contract, bringing the aggregate value of eFPGA contracts in the last three quarters to more than $5 million. The new strategy is working. QUIK is a Buy up to $10 for my $60 target as their sensor hub is widely adopted in smartphones, tablets and wearables.

Primary Risk: New sensor hub competitor emerges.

Probable time of next financing: None needed

Rocket Lab USA (RKLB – $8.05) slid their launch window for BlackSky to tomorrow, which reduces their March quarter revenue guidance from $42 million to $47 million down to $40 million. They’ll recognize the revenue in the June quarter. No big deal. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk:A new competitor emerges.

Probable time of next financing: None needed

Velo3D (VLD – $9.31) announced its Flow 3.0 print preparation software. This new version supports larger models of parts that are able to be manufactured on the Sapphire XC printer, which can produce parts that are up to 400% larger than the original Sapphire printer. Flow 3.0 also supports scheduling additional lasers to maximize the efficiency of the Sapphire XC’s eight 1,000-watt lasers, which increases productivity by up to 5x compared to the Sapphire. VLD is a Buy up to $11 for my $50 target as Velo3D’s high-tolerance metal parts printing business grows.

Primary Risk:A new 3D metal printing competitor emerges.

Probable time of next financing: None needed

Inflation MegaShift

Gold ($1,945.70) could be affected by the Ukraine war. Western sanctions have already frozen roughly $500 billion of bank deposits belonging to Russia’s central bank. Now, the White House has announced that existing sanctions also cover any transaction with the country’s central bank involving gold.

Russia has the world’s fifth-largest gold stockpile. But if it can’t find anyone to trade that gold with, it’s not much use. But I said “if.” There are plenty of countries in the Middle East and Asia that will buy Russia’s gold or use it for trade transactions.

The fractal dimension still has plenty of energy to get to new all-time highs.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy Bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $45,280.45) rallied to a year-to-date high on Monday and is up sharply since the war started.

Click for larger graphic

Click for larger graphic

That’s no surprise because both sides are using it. Last week, the Russian government said it would accept bitcoin in exchange for its oil and gas exports. If the the Russian central bank held on to some of those bitcoins as a new type of reserve asset, could it be the start of a wider move to use bitcoin instead of gold as a store of national wealth?

Bitcoin does have several advantages over gold. Just as you can break up a dollar into 100 cents, you can divide a bitcoin into 100 million satoshis to help with payments. You can’t divide gold as easily. And bitcoin is easier to transport than gold because it’s a purely digital currency. You can send it anywhere in the world in minutes with a phone and an Internet connection.

It’s also decentralized. This makes it hard to stop someone – or some government – from using the network, or letting the White House stop you from using the network. And thanks to some neat cryptography, bitcoin is impossible to counterfeit. So you don’t have to go through an expensive “assay” – or purity verification – as you do with gold when you accept it as payment.

The Ukrainian government has also turned to bitcoin. It has raised more than $54 million through donations in cryptos including bitcoin, ether, and Tether since the Russian invasion began just over a month ago. If you want to donate, government officials in Kyiv posted these crypto wallet addresses to Twitter:

Click for larger graphic

In January, an Arizona state senator introduced legislation to make bitcoin legal tender, allowing Arizonans to settle public debts and pay state taxes with bitcoin. In February, a California state senator introduced a similar bill to allow California to accept crypto payments for state services such as permits and driver’s licenses. Colorado’s governor says his state will accept bitcoin as payment for state taxes and fees by summer.

BTC-USD, ETH-USD, GBTC and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Oil – $103.42

Oil prices fell after President Biden talked about releasing 180 million barrels of oil from the Strategic Petroleum Reserve, which is supposed to be saved for situations where it is desperately needed to keep our industry and military functioning. 180 million barrels – why, that’s a whole two days of global oil demand. That could knock gasoline prices down a nickel a gallon for as long as four days. Big deal.

The weekly API oil and products inventory report showed another big draw, with crude down 3.0 million barrels and gasoline down 1.357 million barrels. So much for demand destruction from high gasoline prices.

All this is just short-term noise against the looming structural deficit. Three to six months from now the world will be materially short of oil, it’s only a question of how much. Biden’s full sanctions impact will begin to bite just as summer gasoline production ramps. OPEC+ just this morning said there’s nothing it can do to stop rising oil prices and is sticking to its 400,000 barrels per month increase in quotas – which they can’t hit anyway.

Beyond 2022, Russia’s oil industry has been isolated from most of the global capital market and lost access to many of the key sources of oilfield expertise, from former joint ventures (Shell, Exxon, BP) to the withdrawal of major oilfield services companies. Russia probably can’t prevent a collapse in crude production, let alone grow it anytime soon. And the world needs more black gold every year. Got OIL?

The July 2026 Crude Oil Futures (CLN26.NYM – $53.16) are a Buy under $55 for a $200+ target.

The iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $32.24) is a Buy under $24 for an $80+ target.

Energy Fuels (UUUU – $9.15) will benefit as the price of uranium rises. It looks like the Sprott Physical Uranium Trust (SPUT) is hoovering up so much U3O8 that we soon may run out of physical.

Click for larger graphic or https://www.sprott.com/investment-strategies/physical-commodity-funds/uranium/#uranium-held

Click for larger graphic or https://www.sprott.com/investment-strategies/physical-commodity-funds/uranium/#uranium-held

Got rare earth elements? Got uranium? UUUU is a buy under $11 for a $30 target.

Primary Risk: Uranium prices fall.

* * * * *

Scientists build circuit that generates clean, limitless power from graphene

A team of University of Arkansas physicists has successfully developed a circuit capable of capturing graphene’s thermal motion and converting it into an electrical current.

“An energy-harvesting circuit based on graphene could be incorporated into a chip to provide clean, limitless, low-voltage power for small devices or sensors,” said Paul Thibado, professor of physics and lead researcher in the discovery.

* * * * *

How to quickly end the war in Ukraine with $10 laser pointers

* * * * *

Your worried about food shortages in the US and a global famine Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

$20-for-$1

Antares Pharma (ATRS – $4.10) – Buy under $5, first target $10, then $50

Aptose Biosciences (APTO – $1.36) – Buy under $4, ultimate target $45

Arch Therapeutics (ARTH – $0.10) – Buy under $0.70, first target $2, then $7

Bellerophon Therapeutics (BLPH – $2.36) – Buy under $11, first target $30, then $300

Compass Pathways (CMPS – $12.89) – Buy under $36, hold a long time for a 10x return

Graphite Bio (GRPH – $5.10) – Buy under $26, hold a long time

Inovio (INO – $3.59) – Buy under $21, hold a long time

Invitae (NVTA – $7.97) – Buy under $50, first target $100, then $200+

Medicenna (MDNA – $1.28) – Buy under $4, first target $40, then maybe $80

ScyNexis (SCYX – $3.91) – Buy under $24, target price $54, then $170

Other Biotech

TG Therapeutics (TGTX – $9.51) – Buy under $40, target price $80+

Tech Dominators

Corning (GLW – $36.91) – Buy under $33, target price $60

Meta (FB – $222.36) – Buy under $320, target price $400

Gilead Sciences (GILD – $59.45) – Buy under $105, target price $130

SoftBank (SFTBY – $22.31) – Buy under $30, target price $60

Other Tech

First Trust NASDAQ Cybersecurity ETF (CIBR – $53.11) – Buy under $32; 3- to 5-year hold

Fastly (FSLY – $17.38) – Buy under $45; 2- to 5-year hold to $150+

PagerDuty (PD – $34.19) – Buy under $40; 2- to 5-year hold

QuickLogic (QUIK – $5.50) – Buy under $10, target price $60

Liberty Media Acquisition Corporation (LMACA – $9.91) – Buy under $10.50, target price $20 to $30

Rocket Lab (RKLB – $8.05) – Buy under $13, target price $30+

Velo3D (VLD – $9.31) – Buy under $11, target price $50

Inflation

A Short-Sale or REO House – Buy while fixed mortgage rates are low

Bag of Junk Silver – $25.18 – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $33.01) – Buy under $25, target price $50

ALPS Sprott Junior Gold Miners ETF (SGDJ – $43.44) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $19.38) – Buy under $15, target price $30

Global X Silver Miners ETF (SIL – $36.37) – Buy under $30, target price $50

Coeur Mining (CDE – $4.45) – Buy under $10, target price $20

First Majestic Mining (AG – $13.16) – Buy under $15, next target price $23

Paramount Gold Nevada (PZG – $0.65) – Buy under $5, first target price $10

Sandstorm Gold (SAND – $8.08) – Buy under $10, target price $25

Sprott Inc. (SII – $50.24) – Buy under $30, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $45,280.45) – Buy

Grayscale Bitcoin Trust (GBTC – $30.55) – Buy

Ethereum (ETH-USD – $3,239.83) – Buy

Grayscale Ethereum Trust (ETHE – $26.95) – Buy

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $32.78) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $36.64) – Buy under $34 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $16.35) – Buy under $24 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $28.50) – Buy under $50 for a double over the next three years

Acreage Holdings (ACRDF – $1.38) – Buy under $4.49 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.49) – Buy under $1.25; long-term hold

Energy

Crude Oil Futures – July 2026 (CLN26.NYM – $53.16) – Buy under $55, $200+ target

iPath Pure Beta Crude Oil Exchange-Traded Note (OIL – $32.34) – Buy under $24, $80+ target

Energy Fuels (UUUU – $9.15) – Buy under $11, $30 target

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Algernon Pharmaceuticals (AGNPF – $4.60) – Hold for CEO comment

CohBar (CWBR – $0.31) – Hold for human trials of CB5138-3

Akebia Biotherapeutics (AKBA – $0.72) – Hold for FDA meeting

Apple Computer (AAPL – $174.61) – Hold for 5G iPhones

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2022

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

Outstanding Radar Report Michael Murphy. Glad you found some great opportunities in this Radar Report. GLTA Love the $10 end the war lasers,

2 Where is everyone?

We are all here.

TIME: “Here’s What You Can Do to Help People in Ukraine Right Now”

https://time.com/6151353/how-to-help-ukraine-people/

TIME/NextAdvisor: “How to Donate Crypto to Ukraine, and Ensure Your Coins Are Going to the Right Places”

Same BTC/ETH addresses as listed by Murphy with more explanation, and other NGO organizations for donations:

https://time.com/nextadvisor/investing/cryptocurrency/donate-crypto-to-ukraine/

Yes, great RR, MM. I agree with your assessment that food is going to get very expensive and in short supply. Fertilizer is being caught in a demand /supply squeeze because Ukraine and Russia usually are big exporters of it. The cost is usually about 30 percent of the cost of food. But with this crazy situation with Ukraine it is estimated to go to 50 percent or more of the cost. And the planting season is just around the corner. When that message gets out to the public people are going to do the same thing with food that they did with toilet paper during Covid. If people think food is expensive now. Wait until that wrinkle kicks in. As for oil being released from the government oil tank ; just look at what happened the last time we did it!! The only difference is we will make a bigger profit from the sale because the price of oil per barrel when we stored it was considerably less than what is sells for now. And the government will have to pay $120?? a barrel to replace it. Then what happens IF we have a real emergency and we need it for military action sometime in the next 6 months or more?? Just IMO

Boston, MA — Johnson & Johnson offers $1 Billion for miraculous bleeding agent AC5 from Arch Therapeutics (ARTH). Arch CEO Terry Norchi responds, “We are considering the offer and other possibilities and will respond in the best interest of our shareholders.”

https://corporatefinanceinstitute.com/resources/excel/study/insert-todays-date-in-excel/

https://news.yahoo.com/daily-calendar-april-1-2-070705558.html?fr=yhssrp_catchall

You had me there for 2.34 seconds. Still, one can hope.

You had me for a moment until I saw Norchi saying “in the best interest of our shareholders”…

Too true.

MM–On AKBA, you are ignoring the data about the difference in baseline CV characteristics in the dialysis trial, which I mentioned several times and the company had no answer for. In data analysis, assume that the FDA is smart and picked up on this just as I did. Has appealing FDA decisions been successful by any company? The only saving grace for investors is whether Otsuka buys out AKBA at $2-3. When do you think that will occur?

SCYX–whatever methodology is used for numbers of scripts, they are trendless because MD’s aren’t impressed. MD’s are free to use Brexa for recurrent VVC now, so approval for this later 2022 will be a nonevent. Dr. Michael Burry has likely exited as a shareholder. The important trials for serious hospital infections are far into the future, so the stock will continue to fall due to lousy financial losses.

CWBR–looming NWI bankruptcy on top of the existing near-100% plunge. Big pharma is a total failure on NASH. But look near you in Colorado at Quicksilver Scientific. Their 3 month detox protocol for eliminating toxins via liver drainage has improved markers of liver function, reduced the ultrasound presence of liver swelling, eliminated gallstones in 25% of people, and reduced the size of gallstones in 75%. This protocol costs a few hundred bucks. Big pharma pales in comparison, with their failures and even if someday some drug makes it, it will be many times the price of natural treatments such as offered by Quicksilver.

ARTH–actually the next bankruptcy, despite Chris’ April Fools post.

TGTX–possibly the only bright spot, but you never know.

I really appreciate your counterpoint to Micheal Murphy’s points. Will have a look at Quicksilver Scientific. Would love your thoughts on NervGen (NGENF) which is my biggest investment. Also, you might want to have a look at ACHV which will soon announce P3 results in its smoking cessation drug.

You probably have local doctor friends in your work. Mention Quicksilver to them, and they could open up a professional account for their own practices and get big savings and buy for you. Some important products need to be shipped with ice packs and refrigerated on delivery, so your local contacts are valuable. These products are liposomal glutathione, Pure PC, NAD Gold or Platinum and a few others.

Consumers can buy directly and get some information, but the nitty gritty science is only available to professionals with accounts. Unfortunately many great Quicksilver videos on YouTube have been deleted due to censorship of nutritional info that goes against agendas of you know who.

Bought more SCYX

Please answer my question about Otsuka buying AKBA.

They might want to buy, but AKBA won’t want to sell at least until after the FDA meeting.

Thanks. The FDA said the only path to approval will be a new clinical trial, which would be large and out of the question for AKBA. If you are correct that the FDA bungled the data analysis, has there ever been a case where the FDA admitted they were wrong and they later approved? When would the FDA meeting occur?

MM: do I understand correctly that SCYX market cap of $115 mil is just about equal to the $105 mil cash on hand?? Why is this company so undervalued? What am I missing?

They’re burning through about $ 75M-100M per year, so that cash won’t last. They need fund operations with product sales rather than raised capital.

Read my post just above. Doctors aren’t impressed with expensive Brexa because it is only slightly more effective than cheap fluconazole. Script growth has been questionable. Dr. Michael Burry, a former investor posted a few weeks ago that scripts would have to grow significantly before the company breaks even in 2024. They will drain the cash fast, go through dilutive capital raises, the usual crap.

MM do you have any counter to the negative SCYX comments below? I see you bought more but it’s not one of your top 5 so what say you?

Fluconazole completely fails many women who can be cured by Brexa because it is fungicidal. The company has a series of positive news events coming this year – the first patient in the IV trial enrolled this quarter, the FURI and CARES interim analysis this quarter, the recurrent VVC filing at the end of this quarter, and FDA approval for recurrent VVC at the end of the year. It’s true that doctors can use Brexa off-label for recurrent VVC now, but payers won’t pay for it (different dosage). As I said in the Radar, the IV Phase 3 trials are likely to end in approval of a therapy for systemic fungal infections — a widespread and burgeoning disease threat that hospitals need a new drug for.

Your first sentence is wildly exaggerated. Fluconazole in my experience helps most women. I don’t see women banging down the doors with distress from refractory VVC as though it was a covid pandemic. Brexa has marginally better efficacy, but the trials showed that it too is no great panacea, with still lots of failures. The hype is the new chemical entity, which has not translated into much better efficacy.

As for the payors not paying for use for recurrent VVC until the rVVC trial shows favorable results, that is a major common problem with market acceptance of any drug for different uses. The FDA process of approving drugs only for narrowly defined specific conditions is unnecessarily prolonged due to accompanying narrow mindedness. I just learned about an excellent topical drug for pain, Pennsaid. I have recommended good topical OTC drugs like Salonpas and diclofenac. Pennsaid is better because of its added ingredient, DMSO which improves penetration of similar NSAIDS such as in Salonpas and diclofenac. But Pennsaid is only covered by insurance for knee pain. Come on, it would be effective for pain elsewhere, but that company would have to do individual trials for pain in the shoulder, then hip, then feet, etc. This is a big reason why drugs are expensive and not available in a timely manner. A corollary is that investing in biotechs treating non-life threatening conditions is a poor investment strategy. Similar analysis for ARTH’s AC5, a great product for an important problem, but no big pharma is interested because wounds don’t make headlines.

When SCYX gets approval for life threatening conditions like invasive candidiasis or aspergillosis in late 2024, their drug will make good money and get covered by insurance. Then the stock will rise, but in the meanwhile, look for a steady decline to $1-2, or bankruptcy if no partner saves the day.

Several months ago when SCYX was $6, I said it would plunge to $4-5. Now we are in the high 3’s, on its way to an avalanche of disillusionment to below 2.

ARTH – should be interesting to see how much revenue they will report for the quarter that just ended.

MM and Board any suggestions for agriculture stocks etf’s we all know the shortage is coming. ((-:

MM–how about fertilizer companies? Fertilizer has risen through the roof, but it may be only a short-medium term play.

The VanEck Agribusiness ETF (MOO) is well-known, but the portfolio (CLCK HERE) doesn’t thrill me. I’ve worked on AppHarvest (APPH) but I’m not covinced they can get their production costs down.

ARTH — new video (nice job) courtesy of Electric Phred on SA article:

I had missed this new website on AC5: https://ac5aws.com/

If you missed the new website as an interested shareholder, almost 100% of the doctors who would use AC5 are unaware. So this week ARTH is having merely a poster presentation describing a measly 2 new cases. Posters are usually in the hallway on the way to the bathroom. This should be a major presentation at this SAWC meeting, but ARTH doesn’t have the money to pay for promotion to get big meeting time, since it has been squandered on high salaries for passive, do-nothing management. Two cases do not constitute good marketing.

At comedy clubs, the no-name newcomer gets good attention prior to the main attraction of the big name guy. ARTH will just be whizzed by as prospective doctors rush to go take a whizz.

Nothing they tried seemed to work – They could find someone to stand there who had used the product to success – instead of just a poster – lord knows they have never had success on any other way.

Right–good common sense. But then that person would be accused of being a shill for the company. There is no trust or confidence in good people these days. Everything has to be documented, but we all know that these toilet paper documents are trash and are ignored anyway. Journal articles are loaded with hidden politics–data is suppressed and manipulated to serve certain agendas. Academics scoff at testimonials, but I scoff at the corrupt agenda-ridden academics who are dishonest themselves. I trust a few testimonials from my patients who I know are telling me the truth from their answers to my specific questions, much more than academic studies of 1000’s of patients where there is no way to know the real data. Double blind placebo controlled studies, the so-called science, are nullified by liars who write the articles.

MM, are you averaging down on SCYX ? Why wouldn’t NVTA be a better use of capital now?

I have a bigger position in NVTA than SCYX. I do think it has more upside in the long run.

More good, bad and the ugly on the oil

Sector. Several major oil companies have joined McDonalds and others in pulling out of Russia. Exxon, BP, Shell, Schlumberger LTD, Halburton Co. and Baker Huges Co have all pulled up stakes and left Russia. Leaving behind years if not decades of work and investments in the billions of $$$$$. Not only do we NOT have any new wells being drilled in the US, now the wells we HAD operational in Russia, are going to be taken over by Putin for his war machine!! Which means the oil companies that have survived the carnage of the global warming parade will be minting money as this crisis plays out. IMO

The major oil companies you mentioned survived the carnage, but if they relinquish their Russian oil assets, they will take the losses and NOT mint money from that, although they will mint money in other countries with the high price of oil. Meanwhile Russia can mint money from selling the high priced oil to their Commie comrades in China, etc. The SWIFT dollar sanctions won’t work, since Russia will demand payment in rubles. Putin has lots of gold, so he could care less and charge on.

MM, I see that MDNA hit another 52 week low of $1.13 today with unusually high volume. Are you expecting anything significant from their presentations at the American Association for Cancer Research (AACR) Annual Meeting this weekend?

Medicenna Announces Upcoming Poster Presentations at the AACR Annual Meeting

TORONTO and HOUSTON, March 09, 2022 (GLOBE NEWSWIRE) — Medicenna Therapeutics Corp. (“Medicenna” or “the Company”) (NASDAQ: MDNA TSX: MDNA), a clinical stage immuno-oncology company, today announced the publication of two abstracts that have been accepted for electronic poster presentations at the American Association for Cancer Research (AACR) Annual Meeting, which is taking place both virtually and in-person at the Ernest N. Morial Convention Center in New Orleans, Louisiana from April 8-13, 2022.

The full texts of the published abstracts can be found on the AACR Annual Meeting website. Details on the corresponding electronic posters, which will be available to registered attendees starting at 1:00 pm ET on April 8, 2022 and on Medicenna’s website following the meeting, are shown below:

Poster Title: An ‘Anti-PD1-IL2 Beta-Only Super-Agonist’ Displays Potent Anti-Tumor Efficacy

Session Category: Immunology

Session Title: Preclinical Immunotherapy

Location: On-line only

Abstract Number: 5532

This poster will describe preclinical studies evaluating a therapeutic candidate derived from Medicenna’s BiSKITs™ program (Bifunctional SuperKineImmunoTherapies). The evaluated bifunctional Superkine is designed to activate anti-cancer immune cells while limiting their exhaustion, and is composed of an anti-PD-1 antibody linked to an IL-2 Superkine exhibiting enhanced affinity for IL-2 receptor beta, and no binding to IL-2 receptor alpha.

Poster Title: Characterization of a Long-Acting IL-13 Super-Antagonist Engineered to Target Tumor Associated Macrophages and Myeloid Cells

Session Category: Immunology

Session Title: Preclinical Immunotherapy

Location: On-line only

Abstract Number: 5542

This poster will describe preclinical studies evaluating a long-acting IL-4/IL-13 super-antagonist that targets the IL-13 receptor alpha-1 component of type II IL-4 receptor expressed on tumor associated macrophages and myeloid derived suppressor cells. Inhibition of this receptor with the super-antagonist is intended to prevent tumor growth by promoting a pro-inflammatory tumor microenvironment.

MM Are you going to put a near term on RKLB due to their first time attempt at mid air capture of rocket? Or will it make a difference?

The new Radar Report for 4.7.22 is posted.