Dear New World Investor:

The Fed paused (good news for stocks) at their 22-year high for the Fed funds rate, but made it clear my “Higher for Longer” scenario is their current policy (bad news for stocks). Twelve memberssaid they expect one more hike this year while seven are ready to pause for good. The median participant projects two rate cuts in 2024. They expected four cuts at the last meeting. They now forecast the Consumer Price Index rising 2.6% in 2024.

Chairman Powell said real interest rates are “meaningfully positive” and need to stay that way “for some time” because economic activity has been stronger than they all expected. It appears that the

recession scenario is no longer on the table.

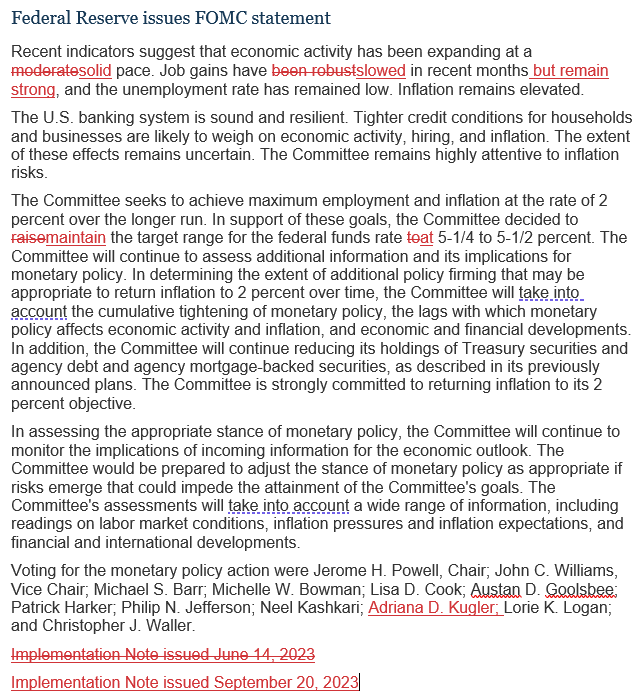

The actual statement showed only a few changes (in red) from the last meeting:

Click for larger graphic

Click for larger graphic

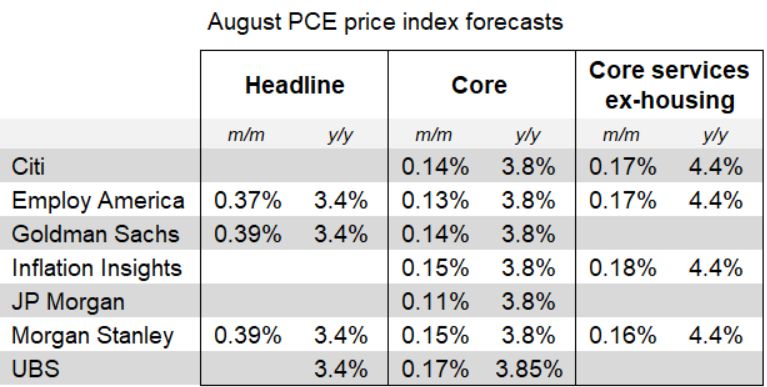

The markets now have a 50% probability of another rate hike by December – in other words, flip a coin. The Fed’s median core Personal Consumption Expenditures (PCE) inflation rate projection for the December quarter ticked down to 3.7% from 3.9%. We get the August number a week from tomorrow. Based on the August Consumer Price Index (CPI) and Producer Price Index (PPI), forecasters expect the core PCE index rose 0.14% in August, the smallest rise in 13 months. This would lower the 12-month rate to 3.8% (the lowest since June 2021) and the three-month annualized rate to 2.3% (the lowest since December 2020).

The core PCE rate is expected to show half of the month-to-month increase that the core CPI did for August because several areas of strength in the August CPI were not quite so strong in the Aug PPI components that feed into the PCE calculations.

Click for larger graphic h/t @NickTimiraos

Click for larger graphic h/t @NickTimiraos

The problem with this whole process has been that the Fed tried to address an atypical economic cycle with their typical measures, using theory that last (and only) worked in the 1970s. This creates problems where the Fed employs over-restrictive monetary policy in order to “fight” a problem that was here two or three years ago, but has not been here for quite a while. If they used accurate shelter cost data, we’d already be under 2% inflation. A natural result of all this is unnecessary economic damage that only reveals itself after a long lag time. The longer the lag, the larger the damage.

I think Chairman Powell knows this and that is why he is proceeding cautiously towards the 2% goal. In this environment – a slowing economy, a mild or no recession, and interest rates higher for longer – the winners are companies that can grow rapidly (tech, biotech) and producers of commodities in short supply (oil, copper, uranium).

Market Outlook

The S&P 500 lost 3.9% since last Thursday as investors decided “higher for longer” was worse than “pause with strong economy.” On Monday, for the first time since 2018, it booked its 100th straight session without a drop of at least 1.5%. But over the last 20 years, the market has typically seen its September peak on or around the 11th trading day of the month, which was last Monday. The average decline from mid-September through the end of the month has been about 2% – no big deal. The Index is up 21.4% year-to-date.

The Nasdaq Composite lost 5.0% and is up 26.3% for the year. The small-cap Russell 2000 dropped 4.5% and now is up only 1.3% in 2023.

The fractal dimension can consolidate by fluctuating around a magnet level over a period of weeks or via a sharp drop over a period of days. This week’s sharp drop jumped the fractals to fully consolidated. There is enough energy to power the next uptrend – we just watch and wait to see what the spark is.

Top 5

Changes this week: None

Near-Term – chronological order

TGTX TG Therapeutics – Rapid recovery from overdone pullback

EQT EQT –natural gas price rebound

USL United States 12 Month Oil Fund, LP – crude should rise quickly

FCX Freeport McMoRan – copper shortage this fall

SFTBY SoftBank – for ARM IPO valuation

AKBA Akebia – Vadadustat NDA filing 2023; approval 2024

VLD Velo3D – Rapid revenue growth; low market cap

Long-Term – alphabetical order

EQT EQT – largest US natural gas company

GBTC Grayscale Bitcoin Trust – Bitcoin is headed for $100,000

NVTA Invitae – the winner-take-most of genetic testing

META Meta – a (the?) leader in the metaverse

RKLB Rocket Lab – #2 to SpaceX in space

SCYX ScyNexis –First new antifungal in 20 years

VLD Velo3D – Return manufacturing to the US

Economy

The Atlanta Fed’s GDPNow model forecast for September quarter real GDP growth has dipped a bit to +4.9%. That’s still well above the Blue Chip consensus and the Fed.

Click for larger graphic

Click for larger graphic

Coming Events

All times below are ET, and most presentations and slides are archived on the companies’ websites so you can listen to them.

Saturday, September 23

Fall Equinox – 2:50am

Tuesday, September 26

Short Interest – After the close

Wednesday, September 27

META – Meta Platforms – Through 9/28 – Meta Connect Conference

ACRDF – Acreage Holdings – Through 9/28 – Benzinga Cannabis Capital Conference

APTO – Aptose Therapeutics – 9:10am – Cantor Global Healthcare Conference fireside chat

CMPS – Compass Pathways – 9:45am – Cantor Global Healthcare Conference

Thursday, September 28

June quarter GDP – 8:30am – Third estimate

MDNA – Medicenna – 10:00am – Annual meeting

SCYX – ScyNexis – 1:50pm – Cantor Global Healthcare Conference

Friday, September 29

Personal Consumption Expenditures Index – 8:30am

Big Tech: The Biotech & Digital Dominators MegaShift

There are at least four ways to make money in the stocks of these large, growing, dominant companies. You can:

* * Buy a stock and hold it

* * Buy a stock and write a call option against it

* * With a Level IV options account, write an out-of-the-money put option

* * With a Level IV options account, write an out-of-the-money put option and use part of the premium to buy an out-of-the-money call option

Apple (AAPL – $173.93) shipped iOS17 today, as well as watchOS10 and iPadOS17. Apple puts new features in each iOS release, and eventually – usually after about five years – older iPhones can’t be upgraded to the latest operating system. If the new features are security upgrades, financial institutions will require the feature to access an online account and – voilà! – you’ll need to buy a newer phone to access your accounts. Pretty clever. AAPL is a Buy under $150 for new iPhone rollouts and augmented/virtual reality products.

Gilead Sciences (GILD – $75.27) reported positive results of a Phase 2 trial of Yescarta in patients with relapsed/refractory large B-cell lymphoma after one prior line of therapy who were deemed ineligible for high-dose chemotherapy and autologous stem cell transplantation. The full findings from the study were published in Nature Medicine. The trial met its primary endpoint, with a complete metabolic response of 71% versus 12% expected with standard of care, based on historical controls.

Separately, and as expected, the Committee for Medicinal Products for Human Use of the European Medicines Agency granted a positive opinion for the use of Veklury (remdesivir) to treat people with COVID-19 with mild to severe hepatic impairment. If adopted by the European Commission, Veklury will become the first and only authorized antiviral COVID-19 treatment that can be used across all stages of liver disease.

Europe has the highest burden of liver disease in the world and people with liver disease represent a population that is highly vulnerable to COVID-19 and are at increased risk of morbidity and mortality. GILD is a Long-Term Buy under $80 for a first target of $120.

Meta Platforms (META – $295.73) launched WhatsApp Channels to over 150 countries to create a private way to receive updates that matter to someone. Meta is building the most private broadcast service available. Who you choose to follow is not visible to other followers and Meta protects the personal information of both administrators and followers.

They also introduced creating multiple personal profiles to organize your experience on Facebook – think one profile for the foodie scene you love and another one to keep up with your friends and family. Each profile will have a unique Feed with relevant content and you can easily switch in between profiles without having to log in again.

They are expanding Meta Verified to businesses on Instagram, Facebook and WhatsApp. A Meta Verified business subscription will include business authentication with a verified badge, impersonation protection, access to account support, and features to help a business stand out. META is a Buy under $150 for a $400 target in 2024.

SoftBank (SFTBY – $20.77) said the underwriters exercised their full “green shoe” option for seven million shares of ARM, so SoftBank will get $5.123 billion in new cash to make investments and buy back stock. ARM will be added to the Nasdaq 100 shortly.

What’s next for a SoftBank investment IPO? Could be Bytedance (the owner of TikTok), Flipkart (Indian e-commerce giant), Kavak (Mexican used-car platform), or PayPay (Japan’s largest mobile payments service). Lots of potential gains waiting for Masa and us. SFTBY is a Buy under $25 for a first target of $50 in the next two years.

Small Tech

Enovix (ENVX – $12.31) is acquiring Routejade, a privately-held Korean battery manufacturer, for 6.2 million shares of ENVX common stock and $16.5 million in cash. Enovix gets vertical integration of electrode coating and battery pack manufacturing while adding an established lithium-ion battery business with factories in Korea, along with complementary products, customers, and suppliers. The deal will close in the December quarter and be immediately accretive.

Click for larger graphic

Click for larger graphic

Routejade already was qualified as a supplier of coated rolls of electrodes for Enovix batteries with capacity to support the Fab2 scale-up that begins in 2024. By bringing coating capability in-house, Enovix gets significant cost savings while speeding up battery development cycles as modern materials are quickly incorporated to improve energy density. Securing the coating supply chain is also intended to ensure the quality of incoming battery materials, which can positively impact manufacturing yield and throughput.

Routejade brings over 20 years of experience as a manufacturer and supplier of lithium-ion batteries, targeting end markets such as wearables, hearables, medical, industrial, and the South Korean military. Their patented encapsulation technology allows for circular and asymmetric battery form factors, complementing the ability of Enovix to support multiple customer requirements.

Click for larger graphic

Click for larger graphic

On the conference call (SLIDES HERE) and

the CEO said: “This is a compelling acquisition with a strong ROI profile for Enovix given the obvious financial benefits of vertically integrating coating while providing our R&D team quicker access to new materials to enhance our product roadmap and benefit customers. My vision is for Enovix to grow our battery performance metrics at a significantly faster rate than the industry by harnessing the materials agnostic nature of our architecture and this transaction accelerates our ability to execute that plan.

“We are also making tremendous strides in manufacturing with yield gains in Fremont, which positions our Gen2 equipment for a strong start in 2024. We have been very impressed with Routejade’s coating know-how and believe it will only improve our ability to deliver competitive yields while producing batteries in high volume at an attractive cost structure.”

ENVX is a Buy up to $20 for a 4-year hold to $100+ as their BrakeFlow lithium-ion battery takes market share.

Primary Risk: A new competitor invents a better battery.

Rocket Lab USA (RKLB – $4.48) had their first launch failure ever as Stage 2 of the Capella Space launch blew up. They’ve postponed the next mission, scheduled before the end of September, until they can identify and fix the problem. That means a slight revenue shortfall is coming, so the stock dropped.

This is a temporary setback in a massive long-term story. Buy the dip. RKLB is a Buy up to $13 for my $30+ target as low earth orbit satellites and space exploration grow.

Primary Risk: A new competitor emerges.

Biotech MegaShift: The $20-For-$1 Stocks

Say you put $2,000 into a stock that goes from 50¢ a share to $10. The $2,000 turns into $40,000. Then you put the $40,000 into another stock that goes from 50¢ to $10. That turns the $40,000 into $800,000. You did it with two stocks and never risked going negative more than $2,000. (Not that you won’t be mad at me if the first one works and then the second one doesn’t, taking your $40,000 to Money Heaven.)

If you can afford it – and it would not be too big a position in your portfolio – putting $2,000 into each of these speculative biotechs might be a good way to start. Buying these out-of-favor, fallen, or forgotten companies that can get important products through the FDA at very low market capitalizations seems like a good strategy to me.

Risks

Development-stage biotechs are subject to investor sentiment swings from wildly optimistic to excessively pessimistic – mostly the latter recently. After the Primary Risk for each company, I’ve added the clinical stage of their lead product, the probable time of their first FDA approval, and the probable time of their next financing.

As always, you need to think about an appropriate position size. You could buy a full position upfront and then just hold on, or buy some upfront and leave room to add more on the inevitable financings, transient clinical trial setbacks, and the like.

Compass Pathways (CMPS – $7.96) CEO and CMO did a fireside chat at the TD Cowen Novel Mechanisms in Neuropsychiatry Summit (ZOOM HERE). It was a thorough review of where they are with the FDA and their clinical trials. CMPS is a Buy under $20 for a very long-term hold to a 10x.

Primary Risk: Their drugs fail in the clinic.

Clinical stage of lead product: Phase 2

Probable time of first FDA approval: 2025

Probable time of next financing: Late 2025

Inflation MegaShift

Gold ($1,940.20) dropped $26.90 today, its biggest one-day drop since August 1, as the Fed said “Higher for Longer.” The $1,950 tractor beam continues to rule. Long oscillations around a particular price create very consolidated markets. The fractal dimension hit full consolidation at the end of today, so like the S&P 500 we are locked, loaded, and ready for action (sorry, I’ve been watching the superb Band of Brothers on Netflix).

Miners & Related

Coeur Mining (CDE – $2.12) produced the first silver and gold ounces from the Rochester Mine expansion project in Nevada. Following a ramp-up period that will last into early 2024, Rochester is expected to drive a step-change in their overall production levels, cost profile, and cash flow.

Today they published slides from a Rochester Site Tour (SLIDES HERE).

Click for larger graphic

Click for larger graphic

Click for larger graphic

Click for larger graphic

CDE is a Buy under $5 for a $20 target as gold goes higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

First Majestic (AG – $5.14) launched First Mint, LLC, a 100%-owned and operated minting facility. First Mint will expand First Majestic’s existing bullion sales by vertically integrating the production of investment-grade fine silver bullion and allow First Majestic to sell a substantially greater portion of its silver production directly to its shareholders and bullion customers. AG is a Buy under $11 for a $23 next target price as production increases and the price of silver rises.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Paramount Gold Nevada (PZG – $0.29) completed an S-K 1300 Technical Report Summary for its 100% owned Sleeper Gold & Silver Project in Nevada. Total gold resource ounces increased nearly 30%. Measured and Indicated gold resource ounces increased to 1.9 million ounces or 60% of total resource from nil. The Measured and Indicated silver resource hit 21 million ounces. An additional 1.2 million ounces of gold and 9.5 million ounces of silver are in the inferred category.

Click for larger graphic

PZG is a Buy under $1 for a $10 target as gold moves higher.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Probable time of next financing: 2023

Sandstorm Gold (SAND – $4.97) did an interview with Crux Investor focusing on their projected 30%+ production growth with debt reduction.

SAND is a Buy under $10 for a $25 target.

Primary Risk: Prices of precious metals fall due to US dollar strength.

Cryptocurrencies

Cryptocurrencies are a diversifying asset that offer a unique opportunity to make (or lose!) a lot of money quickly. You can easily buy bitcoin and other cryptocurrencies at Coinbase, Block, or Robinhood.

Bitcoin (BTC-USD on Yahoo – $26,573.87) held up well in light of the Fed’s “Higher for Longer.” That’s partly due to BlackRock, the asset management colossus, proposing to launch a bitcoin exchange-traded fund. This move has attracted significant attention due to BlackRock’s strong marketing and distribution capabilities, which are expected to draw a new wave of investors to bitcoin.

Click for larger graphic

Click for larger graphic

If bitcoin remains above $26,000 in 12 days time then it will snap a six-year “Red September” streak. BTC-USD, ETH-USD, GBTC, and ETHE are Strong Buys.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Grayscale Bitcoin Trust (GBTC- $19.00) has reached nearly $14 billion in assets since it was introduced about two years ago. Grayscale won their lawsuit against the SEC on August 29. The SEC has 45 days to appeal, so by October 13 we could have a decision to allow spot exchange-traded funds. GBTC is a Buy under net asset value.

Primary Risk: Bitcoin falls due to over-regulation or is surpassed by another cryptocurrency.

Commodities

Oil – $89.55

Oil is clinging to the $90 area. I think the next major move is up to $100 as does Goldman Sachs, which recently wrote: “We have nudged up our 12-month ahead Brent forecast from $93/bbl to $100/bbl as we now expect modestly sharper inventory draws. The key reason is that significantly lower OPEC supply and higher demand more than offset significantly higher US supply.”

As for that “significantly higher US supply,” this week the US Energy Information Administration (EIA) said in its monthly drilling productivity report that US oil output from top shale-producing regions is on track to fall for a third month in a row in October to the lowest level since May 2023. The estimated decline of about 40,000 barrels per day would be the biggest monthly drop since December 2022. I’m not sure what Goldman is looking at. The US drilling rig count still is down about 122, or 16%, below this time last year, according to Baker Hughes.

The US had reached an all time high level of importing oil from Russia just prior to Russia’s invasion of Ukraine.

Click for larger graphic

Click for larger graphic

The July 2026 Crude Oil Futures (CLN26.NYM – $71.42) are a Buy under $70 for a $200+ target. Only buy futures for all cash; do not use margin.

The United States 12 Month Oil Fund, LP (USL – $40.32) is a Buy under $40 for a $100+ target.

EQT (EQT – $38.74) signed another tolling agreement for liquefaction services from Commonwealth LNG’s facility in Cameron, Louisiana, to produce one million tons per annum of LNG for 15 years. Commonwealth anticipates a final investment decision on the project in the first quarter of 2024, with first cargo deliveries expected in 2027.

EQT’s tolling capacity gives them the flexibility to sell gas directly to end users globally and they currently are pursuing long-term purchase agreements with prospective international buyers. EQT is a buy under $35 for a first target of $70 and a long-term hold for much higher prices.

Primary Risk:Natural gas prices fall.

Freeport McMoRan (FCX – $37.23) announced a 15¢ per share dividend, which included a 7.5¢ base dividend and a 7.5¢ variable dividend. I expect the variable dividend to increase rapidly over the next few years as the copper shortage hits. FCX is a buy under $44 for a $65 target within two years.

Primary Risk: Copper prices fall.

International & Other Recommendations

It is important to hold some non-US assets, especially in China. Contrary to the popular press, China is not melting down.

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $28.87) is a Buy under $38 for a $66 target in 12 to 18 months.

KraneShares Bosera MSCI China A Share Fund (KBA – $22.36) is a Buy under $40 for a three- to five-year hold.

Morgan Stanley China A-Share Closed-End Fund (CAF – $12.39) is a Buy under $18 for a three- to five-year hold.

KraneShares CSI China Internet Exchange-Traded Fund (KWEB – $26.53) is a Buy under $40 for a double over the next three years.

Primary Risk of all four of these: China falls into a recession.

Acreage Holdings (ACRDF – $0.36) will benefit from the move to reclassify marijuana as a lower-risk substance, boosting expectations of legalization at the federal level. The Subversive Cannabis exchange-traded fund’s portfolio manager said: “We do not believe a Congress this politically divided will meaningfully act on cannabis at the federal level. However, we do believe a regulatory move to a Schedule III status meaningfully changes the trajectory for this business in the United States without Congressional action.”

ACRDF is a buy under $2 for a hold for the Canopy Growth merger and beyond.

Primary Risk: Canopy Growth does not acquire the company.

Mongolia Growth Group (MNGGF – $1.05) said they have bought back 242,600 shares under their repurchase authorization for 1.9 million shares. MNGGF is a buy under $1.30 for a long-term hold.

Primary Risk: Harris Kupperman makes bad investments.

* * * * *

RIP Gary Wright

* * * * *

Your worried that A War in Mexico Would Mean War in America

Editor,

![]()

Michael Murphy CFA

Founding Editor

New World Investor

All Recommendations

Priced 9/21/23. Check out the complete Portfolio page HERE.

Buys

These are the stocks everyone needs to own because transformative events are happening over the next year or two, and I expect to hold them long-term.

Tech Dominators

Apple Computer (AAPL – $173.93) – Buy under $150 for new iPhones

Corning (GLW – $31.18) – Buy under $33, target price $60

Gilead Sciences (GILD – $75.27) – Buy under $80, target price $120

Meta (META – $295.73) – Buy under $250, target price $400

SoftBank (SFTBY – $20.77) – Buy under $25, target price $50

Small Tech

Enovix (ENVX – $12.31) – Buy under $20; 4-year hold to $100+

First Trust NASDAQ Cybersecurity ETF (CIBR – $45.25) – Buy under $40; 3- to 5-year hold

Fastly (FSLY – $18.19) – Buy under $20; 2- to 5-year hold to $80+

PagerDuty (PD – $22.54) – Buy under $30; 2- to 5-year hold

QuickLogic (QUIK – $8.51) – Buy under $10, target price $40

Rocket Lab (RKLB – $4.48) – Buy under $13, target price $30+

Velo3D (VLD – $1.45) – Buy under $6, target price $50

$20-for-$1

Akebia Biotherapeutics (AKBA – $1.16) – Buy under $2, target $20

Aptose Biosciences (APTO – $3.11) – Buy under $10, ultimate target $300

Compass Pathways (CMPS – $7.96) – Buy under $20, hold a long time for a 10x return

Inovio (INO – $0.39) – Buy under $7, hold a long time

Invitae (NVTA – $0.70) – Buy under $10, first target $50, then $100+

Medicenna (MDNA – $0.30) – Buy under $3, first target $20, then maybe $40

ScyNexis (SCYX – $3.40) – Buy under $3, target price $20, then $50

TG Therapeutics (TGTX – $9.25) – Buy under $12 for buyout at $30+

Inflation

A Short-Sale or REO House – ($415,400) – Hold

Bag of Junk Silver – ($23.67) – hold through silver bull market

Sprott Gold Miners ETF (SGDM – $24.49) – Buy under $28, target price $50

Sprott Junior Gold Miners ETF (SGDJ – $27.28) – Buy under $39, target price $100

Sprott Physical Gold and Silver Trust (CEF – $18.02) – Buy under $18, target price $30

Global X Silver Miners ETF (SIL – $25.11) – Buy under $30, target price $50

Coeur Mining (CDE – $2.12) – Buy under $5, target price $20

First Majestic Mining (AG – $5.14) – Buy under $11, next target price $23

Paramount Gold Nevada (PZG – $0.29) – Buy under $1, first target price $10

Sandstorm Gold (SAND – $4.97) – Buy under $10, target price $25

Sprott Inc. (SII – $32.06) – Buy under $40, target price $70

Cryptocurrencies

Bitcoin (BTC-USD – $26,573.87) – Buy

Grayscale Bitcoin Trust (GBTC – $19.00) – Buy

Ethereum (ETH-USD – $1,586.64) – Buy

Grayscale Ethereum Trust (ETHE – $10.90) – Buy

Commodities

Crude Oil Futures – July 2026 (CLN26.NYM – $71.42) – Buy under $70; $200+ target

United States 12 Month Oil Fund, LP (USL – $40.32) – Buy under $40; $100+ target

EQT (EQT – $38.74) – Buy under $35; $70 first target

Energy Fuels (UUUU – $7.89) – Buy under $8; $30 target

Freeport McMoRan (FCX – $37.23) – Buy under $44; $65 target within two years

International & Other Recommendations

EMQQ Emerging Markets Internet & Ecommerce ETF (EMQQ – $28.87) – Buy under $38 for a $66 target in 12 to 18 months

KraneShares Bosera MSCI China A Share Fund (KBA – $22.36) – Buy under $40 for a three- to five-year hold

Morgan Stanley China A-Shares Fund (CAF – $12.39) – Buy under $18 for a three- to five-year hold

KraneShares CSI China Internet ETF (KWEB – $26.53) – Buy under $40 for a double over the next three years

Acreage Holdings (ACRDF – $0.36) – Buy under $2 for the Canopy Growth merger

Mongolia Growth Group (MNGGF – $1.05) – Buy under $1.30; long-term hold

Holds

These are holds but not sells – yet. They could get moved back to one of the buy categories if their prices drop or outlook improves, or they could become sell recommendations in the future.

Arch Therapeutics (ARTH – $1.75) – Hold for buyout

Publisher: GwynRose LLC, 5348 Vegas Drive, Suite 868, Las Vegas, NV 89108

New World Investor does not act as a personal investment adviser or advocate the purchase or sale of any security or investment for any specific individual. The recommendations and analysis presented to members are for the exclusive use of members. Members should be aware that investment markets have inherent risks and there can be no guarantee of future profits. Likewise, past performance does not assure future results. Recommendations are subject to change at any time. Nothing in this presentation should be considered personalized investment advice. No communication to you by Michael Murphy or any of our employees or contractors should be deemed as personalized investment advice.

Copyright ©GwynRoseLLC 2023

New World Investor Mastermind Group

1. Post unto others as you would have them post unto you.

2. Keep it clean, like a 1950s family television show. Your alter ego can run free on Twitter.

3. NO PERSONAL ATTACKS! If you don’t like the stock, don’t trash the person. Everyone is responsible for their own due diligence and investments.

4. Don’t post here about politics or religion – you aren’t going to change anyone’s mind. Again, NO PERSONAL ATTACKS!

5. The investment implications of something going on in politics or religion is OK.

6. Of course, there’s never a reason to slur someone based on race, religion, gender, sexual orientation, or country of national origin.

7. Please, no snark!

Print This Post

Print This Post

are we having fun yet ?

I’d rather be having fun than a funeral….

Speaking of which, I just bought a cemetery plot!! Before inflation pushes the price up for a final place to rest. Not to mention the number of people getting older and closer to their expiration date pushing up demand and decreasing availability.

Jesus said ” I go to prepare a place for you that where I am there you may be also.” Plan ahead, get ready.

I have never seen a U Haul following a hearse

Is NVTA going to go out of business ?

MM What do you think of NVDA at these prices?

I have a buy on it in Boomberg.

Nope

I agree Don. Just like the expression, you only live once, you only die once. How do you want that to go? Be proactive and take some off the heat off of your heirs at a very emotional time in their life.

Like the old gentleman said “Being of sound mind I spent it all”

Mm,did you see the notice of non-compliance minimum share price that nvta recieved today at 4.15,really feel that we all deserve you chimming in on this,and not avoiding it,that’s the least you can do.

We all have to assume that nvta will do a reverse split to get the share price obove a dollar,they will probably push share price down to 50 cents company could do a 10 for 1 taking it back up to the 5 dollar range,we’re screwed

They’ll probably reverse split in six months. We’ll vote against it and maybe defeat it, as we did with AKBA.

NVTA has been the biggest loss for me in 50 years of investing, both in dollars and %. We never see fundamental research from MM, only generalities wishing for seismic shifts. Shame on me.

Ditto

NVTA is not in compliance.

Invitae has notified the NYSE that it intends to bring the company into compliance with the listing standards within the required cure period.

Would this be considered a standard reply or does it portend good growth in revenue in Q3? What say you Michael.

NVTA probably means a REVERSE SPLIT unfortunately. How many of those have occurred in the NWI portfolio over the years? Must be a record.

Standard reply. They have at least six months to produce results/persuade institutions to get the stock back over $1.

NVTA–on the surface for the layman, “Amazon of genetic testing” sounds like a megashift. I warned repeatedly as a practicing MD that genetic testing is only an infinitesimal part of clinical practice. It is clinically relevant in only a few situations where it improves prognosis. Profitable companies serving niche patients like oncology charge big bucks for chemotherapies, etc. NVTA charges too little to be profitable for the few patients it could benefit. MM listens to financial and company promotors, not to people with actual experience.

Thank you JGMD for the good observation re nvta

In reply to your request for better doctors–In brief, there are no good medica institutions/clinics. For narrow specialized patch up care, there are plenty of MD’s doing procedures who get good results. But for profound insights on chronic care and solving multidimensional problems, forget it. That’s because institutions follow politically correct medical dogma. But the best docs are independent thinkers. They don’t accept medical insurance because insurance only pays according to politically correct standards established by puppets of Big Pharma, etc. There are pioneering labs such as Genova Diagnostics, Great Plains Lab (now Mosaic), Doctors Data, Cyrex Labs. They teach fundamental clinically relevant biochemistry which has long been forgotten by almost all practicing docs. Big Pharma companies have patents for drugs which are basically bastardized versions of real, natural products. They are preying on the ignorance of MD’s who have forgotten their basic chemistry. I could show a nursery school kid how you can’t fit a square peg into a round hole, and they would appreciate how an altered structure of a drug has different properties from the natural, original structure. The nursery kid is smarter than most docs in that respect.

You can search these labs for docs in your area or call them. In my state of NY, corrupt politics bars these labs from accepting any specimens from NY patients or docs. A NY patient cannot get these tests done even if he is willing to pay out of pocket and not use their insurance. This is an egregious example of anti-medical freedom. In their regulatory efforts to “protect” patients from “quacks,” the real ignorance of these medical authoritarians with their anointed political powers allow the sabotage of the health of people who want to go outside the “system.”

Some innovative docs I have met are Jonathan Wright in Seattle, Datis Kharrazian in Calif, Aristo Vojdani (PhD) an innovative immunologist who runs Cyrex. I regular read and watch youtube videos of Peter Osborne, a GP in Texas. Osborne has little of the credentials and published peer reviewed journal articles required to join the elite academic clubs, but I consider him one of the top experts in gluten and its wide-ranging effects on numerous autoimmune and other multi system diseases. Prestigious specialists in rheumatology, endocrinology, GI, cardiology, neurology are quite ignorant of what Osborne teaches to docs and his patients. The medical specialists merely prescribe drugs, but Osborne talks about proper diets and supplements. His patients have been failures at the hands of the academic specialists, but pay big money and get well from his care.

David Minkoff in Clearwater, Fla is a brilliant holistic MD who has used IV ozone therapy to reverse Parkinson’s disease. Big shot neurologists never reverse neuro diseases like Parkinson’s, Alzheimers dementia, but people like Minkoff do much better. Patients come from all over the US to stay for a few months near his office for intensive treatments and real work. David Perlmutter in Fla is a holistic neurologist who is worth following. Dale Bredesen wrote an important book, THE END OF ALZHEIMERS. Everyone knows someone with dementia, and we all eventually develop it. Bredesen has been rebuffed by academia in his efforts to get funding for his research on multimodality options. Note how there is plenty of funding for drugs that target amyloid, but academia never admits that their theories are wrong–drugs based on these theories have all failed.

I buy SOTA supplements from companies like Quicksilver Scientific, Designs for Health, Pure Encapsulations, Orthomolecular Products. They have webinars for docs, but consumers can buy retail from them, and get names of docs in their area.

SCYX? Buy on the barfing?

Yes. Manufacturing problems are the easiest to fix (and avoid – SCYX should qualify a second source & GSK probably will handle it).

SCYX

Here’s the reason for selloff:

US MARKETS

SCYX

-43.43%

Scynexis to recall GSK-partnered antifungal from marketSeptember 25, 2023 — 08:55 am EDT

Written by Manas Mishra for Reuters ->

Adds background on drug throughout

?itok=VUsgUp6K

?itok=VUsgUp6K

Sept 25 (Reuters) – Drugmaker Scynexis SCYX.O said on Monday it would voluntarily recall its antifungal drug Brexafemme from the market and put a temporary hold on studies of the therapy due to the potential risk of cross contamination with another compound.

The company said it became aware that substances used to make beta-lactam, which can cause allergic reactions in some people, are manufactured using equipment common to the manufacturing process for Brexafemme.

British drugmaker GSK GSK.L has licensed the yeast infection pill from Scynexis.

Scynexis said the recall was cautionary and that it had not received any report of any adverse events due to possible beta-lactam cross contamination.

Up to 75% of women have at least one episode of vulvovaginal candidiasis, commonly known as a vaginal yeast infection, in their lifetimes, according to the U.S. Centers for Disease Control and Prevention.

(Reporting by Manas Mishra in Bengaluru; Editing by Krishna Chandra Eluri)

((Manas.Mishra@thomsonreuters.com; http://www.twitter.com/Manaswrites15;))

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

TagsUS MARKETS

Reuters

Reuters, the news and media division of Thomson Reuters, is the world’s largest international multimedia news provider reaching more than one billion people every day. Reuters provides trusted business, financial, national, and international news to professionals via Thomson Reuters desktops, the world’s media organizations, and directly to consumers at Reuters.com and via Reuters TV.

More articles by this source ->

Possibly a buying opportunity. Hopefully, MM will weigh in after assessing the situation

Thank you

“… with a down down, very very, very down down.” -42.5%

He will weigh in Thursday night. He rarely comments on news, sadly

Hi

So flippant. INO, NVTA, VLD .. incredible losses. Give it up.

Cross contamination is a common problem, especially with food. Nuts and grains which are wheat-free may be processed on equipment that handles wheat. There is a warning label about this, but people continue to buy and eat these only theoretically contaminated foods. All the Brexa manufacturer needs to do is use a dedicated manufacturer separate from the manufacturer of beta-lactam.

GSK could still be engaging in a coverup. Possible, but doubtful. Just because there have been no REPORTS of adverse reactions, doesn’t mean they don’t exist, unreported. But then, how does anyone know whether any adverse reaction would be from the materials in the drug tablet, or the actual drug itself? Just use a separate manufacturer. I doubt there is any actual beta-lactam in Brexa. Penicillin and its analogs have beta lactam as part of the molecule. These analog antibiotics have beta-lactamase incorporated, an enzyme to degrade the beta lactam.

My instinct is that this may be a buying opportunity for SCYX. The new separate manufacturer will have to be vetted by the authorities, but this is not the kiss of death for Brexa.

Dedicated manufacturing should be very easy to fix. I do think this is a buying opportunity. There may be more to the story yet. I hope MM can investigate fully before I pull the trigger. It appears the selling was a bit overdone early on and some of the risk remains, The momentum players have exited and the price has settled into a range.

Pull the trigger

You first my man. Why do you continue to lead your subscribers to slaughter?

Realistically, how long would it take SCYX/GSK to fix the manufacturing problem? How long would it take to get Brexa back on the market? Until then, the trials for serious infections like C auris can’t be done without product. Right now, SCYX is a homeless guy in the gutter, prison, etc.

I think so too. Bought some more today @$2.00 and change.

Possibly a good move. However, I bought VLD at $1.54 when MM thought it was a gift about a month ago. TGTX plunged from 20 to 11 quickly on lower sales, but it continues to plunge to below 9 yesterday. I am learning not to pull the trigger too fast, and be more patient until the dust settles.

I have Covid. No Radar Report this week.

Drugs for covid have questionable value re: risks and benefits. The best safe approach is with Quicksilver Scientific products. They are in Colorado near you. Maybe your wife can drive there or they can ship overnight. You can buy direct as a consumer, or get your doctor to order and save you lots of money. Get liposomal glutathione, spray 5 pumps in your mouth 6x/day away from meals and liquids. Let it absorb completely thru your tongue and cheeks. Do the same with liposomal vitamin C 1000 mg (1 teaspoon) 6x/day. Quicksilver’s liposomal technology is much better than the many other liposomal delivery products on the market. Quicksilver’s liposomes are much smaller and have superior bioavailability. Their liposomal products are almost as good as intravenous delivery. Retail you’ll spend $300 for 3-4 bottles of each, which will last about 2 weeks. Add zinc (any source) 50 mg 1x/day.

Less potent than lipo glutathione/Vit C but reasonable for people with less money is NAC (N acetyl cysteine) 600 mg 4x/day with Ester C (better absorption of vitamin C than ordinary C) 1000 mg tablets 4x/day concurrently. NAC builds glutathione, the active agent.

Vitamin D3 5000 IU is a must, permanently. Adjust your dose to get blood levels of D 25 hydroxy to 50-80, which brings a much lower chance of significant covid morbidity. Covid death rates are much higher if the blood level is below 20 and there are associated medical problems like vascular disease. Vit K2 in the form of MK7 180 mcg/day from Orthomolecular Products is important to avoid arterial calcification from Vit D3. Next best is Super K, 1 cap/day from Life Extension.

Get fresh air and do a little walking as tolerated to reduce the chance of blood clots which occur in covid illness.

Best wishes.

Out of curiosity, and obviously you don’t have to answer. Were you vaxxed?

No. Many vaxed people get COVID anyway.

Absolutely correct. Looks like you are recovering–I hope ultimately completely.

Every stock picker with a newsletter to sell is pushing AI as the next Nirvana, I wonder what Michael/other New World members think is the best way to follow AI development and how to reap the accompanying rewards.

PLTR and TSLA. But this is a horrible time of year to invest. Perhaps scaling in SLOWLY. I think we are in for a bad Sept/Oct.

bot some tsla today

“Every stock picker with a newsletter to sell is pushing AI as the next Nirvana”

Nirvidia?

https://www.youtube.com/watch?v=hTWKbfoikeg

Great song, video, great band Nirvana

I like that…. funny…

nvidia seems to have bottomed

It’s gone from 142 to 424 YTD. Slow your roll.

Any chance that this new hire will prevent a reverse split?

September 25, 2023 – 4:30 pmSAN FRANCISCO, Sept. 25, 2023 — Invitae (NYSE: NVTA), a leading medical genetics company, today announced the appointment of finance veteran Ana Schrank as the Company’s chief financial officer (CFO), effective October 2. Robert Dickey, who has been the Company’s interim CFO since August 2023, will transition to a consulting role for the Company and will work closely with Ms. Schrank and the leadership team to ensure a smooth transition.

we have to assume doyle at this price no,unless wall street really feels she can do the job,time will tell if the shares rise because of her credentials heres hoping,have a nice day

Adding to RIVN here. Amazon will be buying 100k e-vans over the next couple years so we have a nice base. A brand new Rivian Amazon van pulled up to my house a couple of days ago. I spoke with the driver and he loves the van .. in fact the drivers fight over who gets to use it for the day 🙂

SCYX: someone doesn’t think it’s worth waiting:

https://seekingalpha.com/article/4637522-scynexis-from-fungal-to-bungle-the-brexafemme-recall-slippery-slope-downgrade?mailingid=32842447&messageid=2800&serial=32842447.206&utm_campaign=rta-stock-article&utm_medium=email&utm_source=seeking_alpha&utm_term=32842447.206

VLD – Today’s price drop due to yesterday’s announcement that VLD’s CFO has resigned to pursue other opportunities.

https://ir.velo3d.com/news-events/press-releases/detail/124/velo3d-announces-cfo-transition

There’s not much for a CFO to do if orders are nil. Except figure out how to get money at the expense of shareholders. Some MM gift! NOT.

I wish I bought some at the low of $1.11. It’s now back to $1.62.

Hoping for a speedy Covid recovery for Murphy, I’d like to present an investment idea that Murphy mentioned back on December 17, 2020, but he realized the price was too high at the time. The company is NernGen Pharma (NGENF). In 2020, the company had only been public for a year, but the drug they licensed had already been shown to have unprecedented effects in various species in models of various human diseases, including Spinal Cord Injury, stroke and MS. Back then, the company had not even begun Phase 1 development. Thanks to a clinical hold after Phase 1 began, development of the drug was delayed for a couple of years. However, the FDA has authorized NervGen to proceed with a Phase 2 for their drug, NVG-291, in patients with chronic and sub-acute Spinal Cord Injury and screening for patients began this month. On Monday, September 25, they announced that the first of 20 patients in their chronic SCI trial had received his/her first daily dose of NVG-291 or a placebo. Daily dosing in the form of a subcutaneous injection will continue for 12 weeks while the patient also undergoes physical, elctrophysiological and radiological examinations. Half of the 20 patients will receive a placebo and half will get NVG-291. Measurements will continue for an additional 4 weeks after 12 weeks of drug therapy because in animal models, improvements in mobility and dexterity have been shown to continue even weeks after cessation of the drug. There will also be a second cohort of 20 sub-acute SCI patients (10 to 49 days post-injury).

The chronic cohort is expected to read out in mid-2024. As these are patients who have plateaued in improvement, any improvement will be game-changing. Indeed, the University of Akron just received a 3/4 million dollar grant from the Dept. of Defense for a study in SCI of NVG-291 combined with stem cell therapy.

I have long maintained that this could legitimately be a 100-bagger. If that seems excessive, Rich Macary, an early investor in Sarepta (which has a mkt cap of $11B) recently said NervGen has the potential to be worth 10 or 15 times Sarepta’s valuation. Current market cap is $114M. Macary says it could be 1000 times higher. An expert in MS, Hannah Zhang, said that she had never seen any drug have results as good as NVG-291 in a feline model of MS. A little research will show video results of rats with SCI after treatment with NVG-291 vs placebo. And there are more recent results of rats in a stroke model showing better improvement after NVG-291 therapy vs. placebo several days post-stroke.

MM used to write about his $1 to $20 stocks and how if you got two of these you could turn $2,000 into $64,000. By Macary’s math NGENF could turn $2,000 into $2,000,000 to $3,000,000.

Thank you for your analysis, Do they have any potential news on the horizon?

Their sale of product for the $750,000 study at University of Akron may be PR’d if the company deems it a material development. Even better would be positive results from the combo of NVG-291 with stem cells. The PR that the first patient had been dosed didn’t do much, so I don’t expect that a PR that the chronic SCI cohort is fully enrolled to do much either, but that will give investors a countdown knowing that the trial in chronic SCI will be complete in 16 weeks. After that, they’ll have to analyze data before releasing results, which they plan to do in mid-2014. But if the patient who started receiving daily injections about a week ago (or any of the other 19 people in the study) starts seeing dramatic gains in the coming days/weeks/months, I can easily imagine his or her friends/family spreading the word and the news being picked up by local news media and going viral. That would cause a healthy pop, and send the shares into double digits, imho.

I hate the rigidity of trial protocols. Suppose there are no statistically significant benefits after 16 weeks. But benefits may be seen in 6-12 montha or longer. Nobody knows or can predict when for humans. The stock will plunge to pennies if no benefits after 16 weeks because the company will be out of money. Another company may pick up the rights for pennies, do a better long term trial, and those shareholders will get rich. In the real world outside of rigid trials, good docs don’t give up, and support the patient while waiting for responses.

Quick question, does Bio Pub still recommend CAPR?

They have not dropped coverage, if that’s what you are asking. They don’t recommend anything, but they do cover companies they consider to have merit and which could go up a good bit in value. I don’t own CAPR.

Thank you.

NGENF is a speculation on how well do humans match rats or other animals in clinical trials. Metabolism in rats is faster than in humans, so doses/kilogram weight of rats is higher than for humans. Let’s assume that the investigators figured out the dose for humans that corresponds to the dose that worked for the rats. But they don’t yet know how long it will take for the patients to respond compared to the rats. It seems to me that the trial design for the patients is just guesswork. Will 12 + 4 weeks be enough time to measure benefits? The trials could show no difference between patients getting NVG-291 after 16 weeks, but begin to show exciting differences if the study went on for 6-12 months. The stock could plunge to pennies if 16 weeks failed. They won’t be able to do capital raises at pennies for a lengthier trial which could well succeed.

“The stock could plunge to pennies if 16 weeks failed.” True. But if it works? I think every $1 you put in now will be over $10 in less than a year and over $100 a few years later (of course, Macary says over $1000, but that’s when fully mature. To me, it’s worthy of a few of my investment dollars. As was Soleno (SLNO) which I bought as a trade in May after it was discussed at BioPub. That turned out VERY well.

Acurx Pharmaceuticals Announces Successful Completion and Early Discontinuation of the Ibezapolstat Phase 2b Trial for Treatment of C. difficile Infection Download as PDF October 02, 2023

STATEN ISLAND, N.Y., Oct. 2, 2023 /PRNewswire/ — Acurx Pharmaceuticals, Inc. (NASDAQ: ACXP) (“Acurx” or the “Company”), a clinical stage biopharmaceutical company developing a new class of antibiotics for difficult-to-treat bacterial infections, announced today that the Company has discontinued the Phase 2b clinical trial of its lead antibiotic candidate, ibezapolstat, for the treatment of patients with Clostridioides difficile infection (CDI) due to success. The Company made this decision in consultation with its medical and scientific advisors and statisticians based on observed aggregate blinded data and other factors, including the cost to maintain clinical trial sites and slow enrollment due to COVID-19. The Company has determined that the trial performed as anticipated for both treatments, ibezapolstat and the control antibiotic vancomycin (a standard of care to treat patients with CDI), with high rates of clinical cure observed across the trial without any emerging safety concerns.

Accordingly, the Independent Data Monitoring Committee will not be required to perform an interim analysis of this Phase 2b trial data as originally planned and the Company has discontinued the trial. Acurx will analyze the data and report topline efficacy results promptly. The Company anticipates that this decision will allow the Company to advance this first-in-class, FDA QIDP/Fast Track-designated antibiotic product candidate to Phase 3 clinical trials more expeditiously.

Robert J. DeLuccia, Executive Chairman of Acurx, stated: “Considering the totality and weight of evidence of our preclinical, Phase 1 and Phase 2a clinical results and now with the observed aggregate blinded data, we determined it was in the best interests of the Company and its shareholders to discontinue the Phase 2b clinical trial early and prepare for Phase 3 clinical trials. Mr. DeLuccia stated further, “We look forward to compiling, analyzing the data and reporting topline results for the study’s primary clinical endpoint and safety aspects as soon as possible”. He further stated: “We thank the clinical trial investigators and patients across the country who participated in this study allowing advancement of this promising new antibiotic into late-stage clinical trials for this serious and life-threating infection which is classified by FDA and CDC as an urgent priority for which new classes of antibiotics are needed.”

David P. Luci, the Company’s President and Chief Executive Officer, stated: “We also look forward to reporting the full ibezapolstat data which will include the most extensive data for any antibiotic on sustained clinical cure to date in patients with CDI, as well as a comparison of the effect on the microbiome between oral ibezapolstat and oral vancomycin. We believe that, if approved by FDA for marketing, these attributes will support the use of ibezapolstat for front-line treatment of CDI.”

About the Ibezapolstat Phase 2 Clinical Trial

The completed multicenter, open-label single-arm segment (Phase 2a) study was followed by a double-blind, randomized, active-controlled, non-inferiority, segment (Phase 2b) at 28 US clinical trial sites which together comprise the Phase 2 clinical trial (see https://clinicaltrials.gov/ct2/show/NCT04247542). This Phase 2 clinical trial was designed to evaluate the clinical efficacy of ibezapolstat in the treatment of CDI including pharmacokinetics and microbiome changes from baseline and continue to test for anti-recurrence microbiome properties seen in the Phase 2a trial, including the treatment-related changes in alpha diversity and bacterial abundance and effects on bile acid metabolism.

The completed Phase 2a segment of this trial was an open label cohort of up to 20 subjects from study centers in the United States. In this cohort, 10 patients with diarrhea caused by C. difficile were treated with ibezapolstat 450 mg orally, twice daily for 10 days. All patients were followed for recurrence for 28± 2 days. Per protocol, after 10 patients of the projected 20 Phase 2a patients completed treatment (100% cured infection at End of Treatment), the Trial Oversight Committee assessed the safety and tolerability and made its recommendation regarding early termination of the Phase 2a study and advancement to the Ph2b segment. In the now discontinued Phase 2b trial segment, 32 patients with CDI were enrolled and randomized in a 1:1 ratio to either ibezapolstat 450 mg every 12 hours or vancomycin 125 mg orally every 6 hours, in each case, for 10 days and followed for 28 ± 2 days following the end of treatment for recurrence of CDI. The two treatments were identical in appearance, dosing times, and number of capsules administered to maintain the blind. This Phase 2 clinical trial will also evaluate pharmacokinetics (PK) and microbiome changes and test for anti-recurrence microbiome properties, including the change from baseline in alpha diversity and bacterial abundance, especially overgrowth of healthy gut microbiota Actinobacteria and Firmicute phylum species during and after therapy. In the event non-inferiority of ibezapolstat to vancomycin is demonstrated, further analysis will be conducted to test for superiority.

Medically and scientifically, this is great news. Financially, lousy. The stock has declined for the past few months, waiting for another 5 patients to be enrolled in 2b. They only got 1, for a total of 32 patients. Without a partner to fund phase 3, we won’t live long enough to see the required number for phase 3. It has also been disturbing to see low trading volumes, which indicates lack of interest. On the other hand, this company will survive and hopefully prosper if a big partner steps up. Today’s AM plunge in the stock price on very high volume seems to agree with my analysis. At around $1.00, it is a reasonable speculation only.

I get the feeling ibezapolstat again had a 100% rapid cure and the vancomycin arm had 2, 3 or 4 subjects without a permanent cure (and of course, wrecked gut biomes). I bought more this a.m.

Crazy price action on this. Pre-market high was $2.44 and Afterhours low was $1.25!!

Totally agree that ibexa is superior to Vanco, to be confirmed by a PR soon. My main worries are lack of interest with very low trading volumes (except for today) and enrollment growing at a snail’s pace. Phase 2a was terminated because of obvious good results. P2b was the same situation. because enrollment was slow for both P2a and 2b. It will take forever for P3. This is the major problem for the stock. Why the lack of interest, unless the predator who makes Vanco is scheming to pick up ibexa in a bankruptcy fire sale? This situation killed off Algernon, which had promising repurposed products and decent trial results.

ACXP has about a year’s worth of cash. Ibezapolstat will be sold or partnered before then. The last raise they did came with warrants. The buyer has been shorting the stock while hanging on to the warrants for the pay day, as the buyer has done with other companies.

Assume the PR on the detailed results of P2b occurs in 1-2 months. The next milestone will be partnership to do P3. A successful P3 (highly likely) will generate a much higher sale price than after the PR on P2b. If the partner funds the P3, how long would P3 take? Possibly a year or less, before the cash runs out, if the partner gets fast P3 enrollment. But if no partner, no P3 within our lifetime, so the company goes BK unless they accept a low b/o price of $5 or so.

NVTA

FDA Approves Invitae’s DNA Test To Assess Predisposition For Certain CancersLot’s of premarket activity.

Not sure this is such a big deal

Anybody add to this assessment

Hopefully it’s a enough to pump it over the dollar mark it needs to avoid a reverse split

It is no big deal. The real utility of genetic tests is for patients with established cancers. My friend and patient with stage 4 lung cancer lived for 7 years after diagnosis. He was lucky to have the EGFR mutation which enabled targeted drugs which had few side effects and gave him a high quality of life for 6 years before the cancer mutated and these drugs were no longer effective. The typical patient with most other genetic profiles that are not responsive to targeted drugs does very poorly.

NVTA UP 37% ???

ENVX. Another one bites the dust. Id be a wealthy man if I shorted all of MM’s picks.

Yep.

I can only blame myself for buying into these names, especially as I lost almost all my money in KERX

Your not alone Robert alot of us are feeling your pain,maybe m.m. shorts everything he recommends to this newsletter

Scyx, envx, ino, blph, apto, kerx, and on and on.

Totally agreed ,after holding so many of these especially for me nvta going from 38.00 to .60 cents in two years I’m sick every day now knowing I can pick that good ,like you said shame on me,keeping my money in my pocket,have a nice day

Subscriber Chris is an excellent stock picker and analyst, but even his top picks of ACXP and NGENF have high risks of bust, but maybe reasonable chances of boom to make up for the risks. This is just the nature of early stage speculative biotechs.

Did pick up a few shares of acxp,tx for the tip

of course not

MM, Glad to see you up and about,I hope your feeling better and everyone wishes you a speedy recovery.

I bought some TGTX and some ENVX today

I hope Gary Wright made it to the Light. I hope to see you there Gary. “If we walk in the light as He is in the light, we have fellowship with one another, and the blood of Jesus, His son purifies us from all sin ”

1 John1:7

The new Radar Report for 10.5.23 is posted. It’s good to be back!